Sample Category Title

Nikkei 225: Bulls Showing Signs of Resilience

- Japanese stock market has continued to outperform against the rest of the world.

- Positive earnings momentum from Japanese corporations is providing support.

- BoJ Governor Ueda has sounded optimistic about the current upward inflationary trend in Japan.

The Japanese stock market has continued to show resilience despite the current heightened risk of global stagflation and rising geopolitical tensions. The benchmark Nikkei 225 and MSCI Japan have recorded a month-to-date return of +1.30% and +0.95% for May respectively at this time of the writing outperformed the US S&P 500 (-0.75%), MSCI Asia Ex Japan (+0.57%), MSCI Emerging Markets (+0.72%) and STOXX Europe 600 (+0.06%).

Strategic and tactical reasons that explained the potential outperformance of the Japanese stock market against the rest of the world have been highlighted in our previous article.

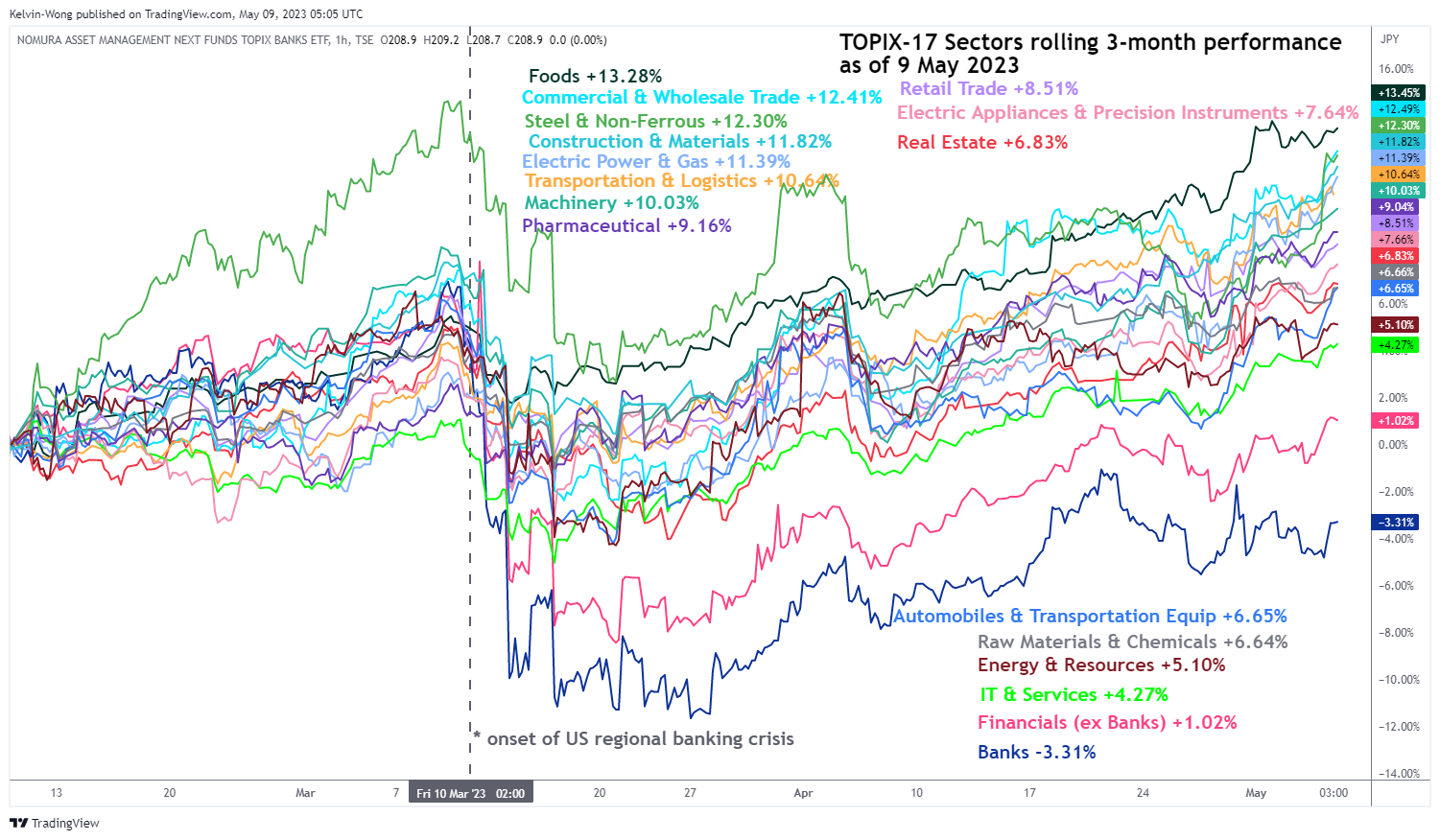

Earnings momentum is supporting several TOPIX-17 Sectors

In today’s Asian session, the Nikkei 255 has added a further intraday rally of +1.00% on the backdrop of upbeat and better-than-expected corporate earnings of steelmakers and shipping companies which has reinforced the 3-month rolling outperformance of the TOPIX Steel & Non-Ferrous Sector (+12.30%) and Transportations & Logistic Sector (+10.64%) that enable these sectors to rank 3rd and 6th positions among the 17 TOPIX sectors.

Fig 1: TOPIX-17 Sectors 3-month rolling performances as of 9 May 2023 (Source: TradingView, click to enlarge chart)

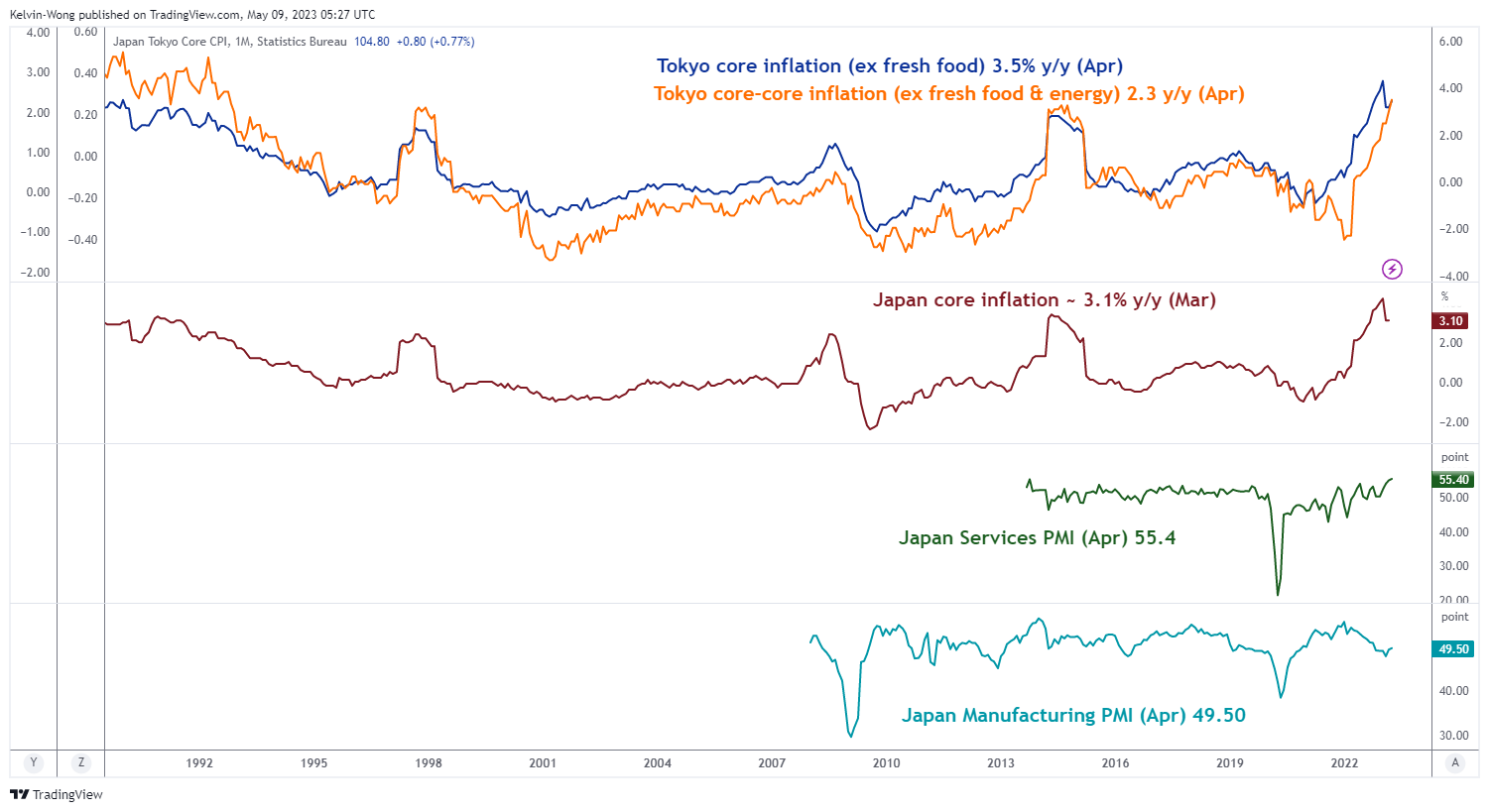

Also, the finalized April reading of the Jibun Bank Japan Services PMI has been revised up to a record high of 55.4 from its preliminary print of 55.0; it also marked the 8th consecutive month of expansion in the services sector with new orders growing the most in over 15 years amid greater spending on travel, leisure, and tourism. These latest data observations suggest that Japan’s domestic internal economic growth is showing potential signs of sustainable recovery.

Expansion in Japan’s Services PMI is moving in tandem with inflation

Fig 2: Japan inflation, manufacturing & services PMIs as of Mar & Apr 2023 (Source: TradingView, click to enlarge chart)

Also, the rise in the services sectors’ activities has coincided closely with the leading Tokyo inflationary data (core & core-core) that has continued to grow and surpassed the Bank of Japan (BoJ)’s 2% inflation target for the 11th consecutive month. Thus, the urgency of the BoJ to normalize its current ultra-easy monetary policy stance has quickened its “pressure” which in turn may lead to further anticipation of Japanese corporate investors’ overseas capital flow back to the domestic Japanese financial markets in the search for better yields on a hedged currency basis.

BoJ’s Ueda sounded “optimistic” about the current trend of Japan’s inflation

BoJ Governor Ueda made an upbeat parliamentary speech on the prospects of Japan’s inflation situation earlier today.

He has mentioned that Japan’s economic growth has picked up and inflationary expectations remain at high levels, seeing some positive signs of an inflation trend that implied the current pace of inflationary growth is sustainable.

Added that BoJ will end its 10-year Japanese Government Bond (JGB) yield curve control programme and start to shrink its balance once the 2% inflation target has been met in a sustainable and stable manner.

However, Ueda highlighted several uncertainties in growth such as whether the recent surge in wage growth can be sustained and spread to smaller and medium-sized corporations.

Overall, BoJ Ueda’s latest speech which came on the latest backdrop of positive macro data and earnings releases for Japanese corporates seems to be skewed toward an increase in optimism that Japan may soon emerge from its decade-plus long deflationary spiral and increase the prospects of bringing forward the normalization of BoJ’s current ultra-easy monetary policy.

Hence, it may create a positive feedback loop back into the Japanese stock market at least in the short to medium term. Next up, we will have the earnings results from the two heavyweights; Toyota Motor Corp on Wednesday and SoftBank Corp on Thursday to provide further clues on whether Japan’s current positive earnings momentum can be maintained.

Japan 225 Technical Analysis – Short-term uptrend intact

Fig 3: Japan 225 trend as of 9 May 2023 (Source: TradingView, click to enlarge chart)

The Japan 225 Index (a proxy for the Nikkei 225 futures) has staged the expected bullish breakout from its major “Symmetrical Triangle” range resistance in place since 14 September 2021 as highlighted in our previous article.

Interestingly, the price actions of the Index have managed to retest the former “Symmetrical Triangle” range resistance now turns pull-back support at 28,480 on 3 May 2023 and staged a rebound thereafter.

Current price actions have evolved into a short-term ascending channel in place since its 15 March 2023 low of 26,380. In addition, the 4-hour RSI oscillator has continued to exhibit upside momentum and has not yet reached a prior extreme overbought level of 81.55%.

The next resistance to watch in the short-term will be at 29,700/29.970 (the upper boundary of the short-term ascending channel, swing high areas of 4 Nov/16 Nov 2021 & a cluster of Fibonacci extension levels)

However, a break below the 28,480 key short-term pivotal support may jeopardize the bullish tone to expose the next support coming in at 28,065 which also confluences closely with the upward-sloping 50-day moving average.

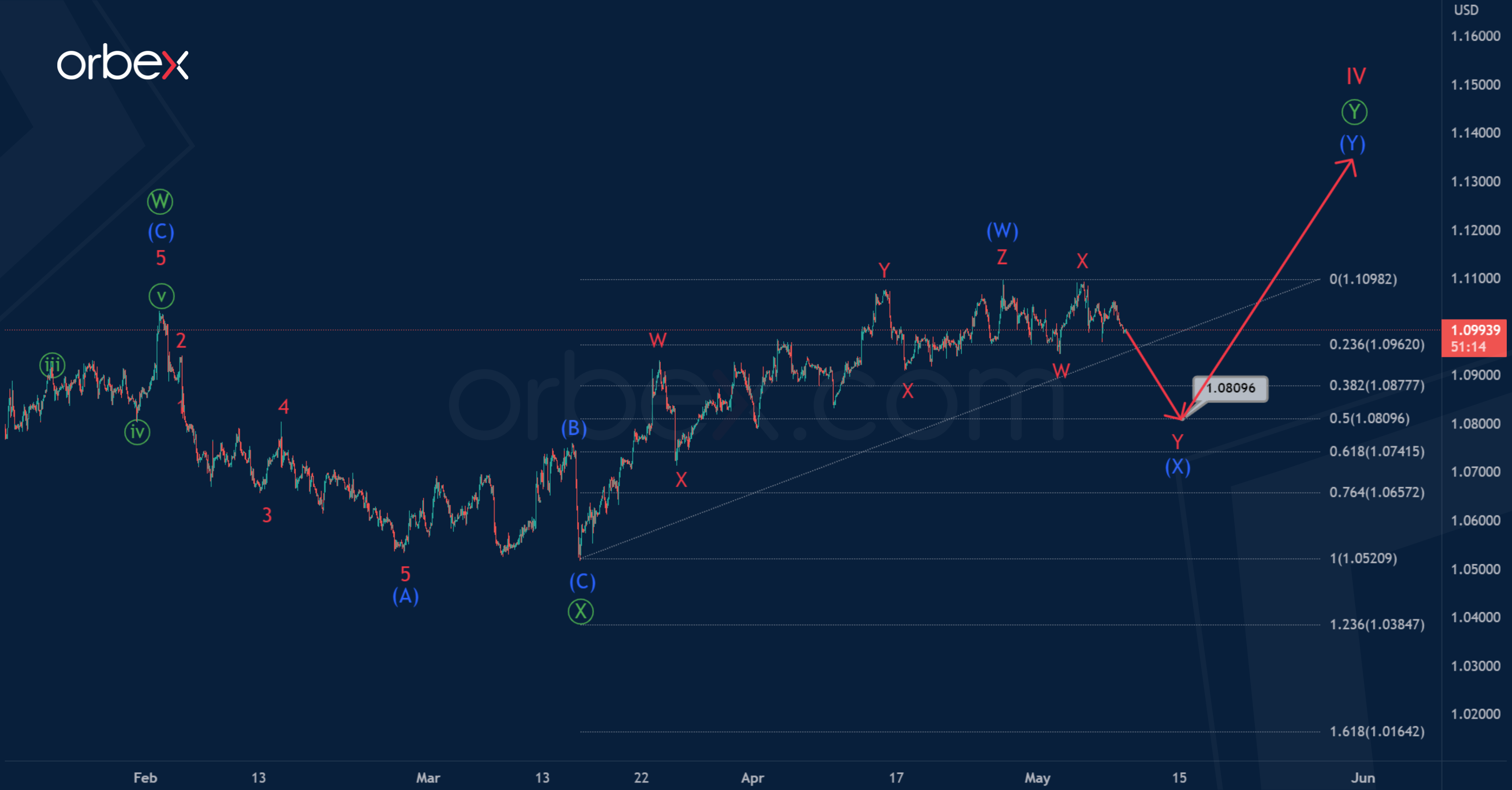

EUR/USD: A Completed Skewed Triangle Gives a Signal of Further Growth

For the EURUSD pair, in the long term, we can observe the formation of a correction wave IV inside a large impulse. Cycle correction IV, most likely, takes the form of a primary double zigzag.

The actionary leg and the bearish corrective intervening wave are completed. The final actionary wave may be under development.

Like the previous primary waves, can take the form of an intermediate zigzag (A)-(B)- (C). The first impulse (A) and correction (B) in the form of a skewed triangle are fully completed. In the near future, we expect growth in the potential impulse (C) to 1.135. At that level, this impulse will be equal to wave (A).

An alternative scenario suggests that the primary wave is not a simple zigzag, but a double one. It is marked with sub-waves (W)-(X)-(Y).

The intermediate wave (W) looks like a completed triple zigzag. Currently, an intermediate wave (X) may be in the process of construction, which may take the form of a minor double zigzag W-X-Y.

In the near future, the price may go down to 1.080. At that level, wave (X) will be at 50% along the Fibonacci lines of wave (W).

USD Recoups Some Losses

USD/CHF tries to hold its ground

The US dollar steadies as traders await US inflation data in April. Latest rebounds have so far met stiff selling pressure with new swing lows encouraging the bears to add onto their short positions. 0.8990 is a fresh supply zone where offers have kept the greenback in check. A bullish close would break the downward momentum and help the pair start to build a base near its 28-month lows. 0.8820 is the immediate support and its breach would force bargain hunters out and send the price to January 2021’s low of 0.8760.

EUR/GBP drifts lower

The pound rallies ahead of an expected Bank of England rate increase. A drop below April’s low of 0.8730 has put the bulls on the defensive after a previous bounce off 0.8760 failed to contain the sell-off. More profit-taking by the buy side could weaken demand in the medium-term and make the pair vulnerable to a bearish reversal. 0.8690 is the next level to see if any meaningful buying interest would emerge again. On the upside, 0.8760 has turned into a resistance and only a close above 0.8800 would improve sentiment.

DAX 40 tests resistance

The Dax 40 takes a breather after lacklustre German industrial production. A pop above 15860 then the recent peak of 15960 has put the index back on track after it found solid support over the 30-day SMA (15680). This confirms that the market mood remains optimistic and the consolidation was merely an opportunity for the bulls to stake in with 15860 becoming a fresh support. The psychological level of 16000 would be a formality before the price retests the all-time high of 16300 from January 2022.

Market Mood Mixed Ahead of US CPI

Asian markets were a mixed bag on Tuesday as caution kicked in ahead of tomorrow’s key US inflation report, although Chinese shares rose after export data beat market expectations. European futures are pointing to a positive open despite the mixed sentiment, with UK financial markets reopening after a public holiday. In the currency arena, the dollar has entered standby mode ahead of talks between US President Joe Biden and congressional leaders on the debt-ceiling issue. The yen is dominating the G10 space this morning after the new BoJ Governor Ueda mentioned that the central bank could drop its yield curve control policy if inflation reaches its 2% goal. Looking at commodities, gold is limping higher but clearly struggling to nurse the deep wounds inflicted by last Friday’s strong NFP report.

US CPI report in focus

After last Friday’s hot jobs report that saw the US economy create 253,000 jobs in April, much attention will be directed towards the pending inflation data for fresh clues on the Fed’s policy path.

It is worth keeping in mind that even though the Fed signaled a pause in further rate increases, it also left the door open to further tightening if incoming data warrants. Traders are currently pricing in a 49% probability of a 25-basis point cut at the September Fed meeting, according to Fed funds futures. CPI year-on-year is expected to rise 5.0% which would be the slowest pace in almost 2 years while core CPI is forecast to cool to 5.5% from the 5.6% in the prior month.

Looking at the technical picture, the Dollar Index (DXY) remains trapped within a range on the daily charts. Resistance can be found around 102.30 while support is at 101.00. A breakout could be on the horizon with the help of a potent catalyst. If prices slip below 101.00, the next level of interest can be found at 100.80. A rebound from 101.00 may trigger a move up towards 102.30.

Currency spotlight – GBP/USD

Could GBPUSD be gearing up for further upside after jumping to a fresh 2023 high on Monday? Well, it looks like bulls are taking a breather ahead of the US CPI data on Wednesday and BoE decision on Thursday. Markets widely expect the BoE to hike interest rates by 25 basis points with much focus on the minutes, quarterly Monetary Policy Report (MPR), and Governor Bailey’s press conference. Looking at the technical picture, GBPUSD could rally to fresh 2023 highs if BoE hawks dominate the scene with key levels of interest found at 1.2730 and 1.2870 where the 200- week SMA resides.

Commodity Spotlight – Gold

Gold drifted higher on Tuesday as investors braced for the US inflation report mid-week. After being whacked by last Friday’s solid US jobs report which raised the odds of the Fed keeping rates higher for longer, the precious metal could sink further if US inflation remains sticky. Such a development may drag gold back below the $2015 level with bears eyeing the psychological $2000. Alternatively, signs of cooling inflation could inject gold bulls with renewed confidence, propelling prices back toward $2045 and 2023 high at $2063.

Markets Keep Close Eye at Meeting of Biden with Congressional Leaders on Debt Ceiling

Markets

US yields yesterday rebounded further from the key support levels (10-y 3.25%/3.30% area, 2-y 3.60/3.65% area) that were at risk after the Fed hinted at a pause in its hiking cycle last week. However, last week’s payrolls at least suggested that the feared-for collapse in demand apparently isn’t around the corner yet while wage growth remains higher than what is consistent with an easy return to the 2% target. Yesterday, the Senior Loan Officer Opinion survey and the Fed financial stability report as expected showed a tightening of lending standards and a decreasing demand for loans, a move that already started before the SVB crisis. In its financial Stability report, the Fed also concluded that bank’s anticipation on slower growth and lower credit quality, amongst others, might reduce the availability of credit. At the same time, the Fed assessed bank funding and liquidity are relatively stable. Commercial real estate remains an area of concern. Looking at the market reaction, both reports apparently didn’t bring additional negative news. US yields closed near the intraday peak levels, adding between 8.7 bps (2-y) and 6.9 bps (30-y). Bunds outperformed Treasuries with German yields rising between 5.1 bps (2-y) and 2.6 bps (30-y). The fall-out from the interest rate repositioning on other markets was modest. US equities closed little changed. The dollar gained modestly (DXY close 101.38; EUR/USD 1.0004). However, the technical picture hasn’t changed, with the US currency still unable to really move away from recent lows. Even with UK markets closed sterling outperformed. EUR/GBP tested the 0.8721/0.8691 support area (close 0.872). However, we don’t draw any in depth conclusion before Thursday’s BoE policy decision, including a new economic assessment/monetary policy report.

Asian equities are trading mixed this morning with Japan outperforming. US yields decline 1-2 bps. The dollar gains marginally. There are again few data in Europe or the US. US NFIB small business sentiment is an interesting pointer on activity, but no market mover. Several ECB (Rehn, Lane, Vasle, Vujcic, Schnabel) and Fed (Jefferson, Williams) members are scheduled to speak. Markets will also keep a close eye at a meeting of US president Biden with Congressional leaders on debt ceiling. At least for now, there are no clear signs of a break-through. Later this evening the US Treasury will sell $40 bln of 3-y notes. After yesterday’s rebound in yields, we expect markets to take a wait-and-see approach ahead of tomorrow’s US CPI data. Lingering uncertainty on the US banking sector and on the debt ceiling will probably prevent any sustained comeback of the dollar. UK BRC retail sales this morning were reported at 5.2% Y/Y (from 4.9). Sterling maintains its recent gains (EUR/GBP 0.8715 area).

News Headlines

Chinese export growth decelerated in April, slowing down from 14.8% to 8.5% y/y in USD terms. While that’s slightly better than the 8% expected, favourable base effects play a role as well with Shanghai and other parts of the country under lockdown in the same period last year. Exports are expected to ease further as the effects of aggressive monetary policy tightening on global demand kick in. Vehicles printed by far the biggest surge (+195.7%), followed by ships & boats (+79.2%) and packages & containers (+36.8%). Imports slumped 7.9% in April, well surpassing a -0.2% estimate. The decline was broad-based across categories. While there’s some effect of sharply lower energy prices on import prices (thus lowering the import value), it still adds concerns to China’s post-lockdown demand recovery. China’s yuan trades a tad weaker this morning. USD/CNY rises toward 6.92.

The Polish zloty’s closing level yesterday was the strongest since the Russian invasion. At EUR/PLN 4.56, the currency pair does hit quite strong support which in case of a break paves the way for a return to the 2022 lows at around 4.50. Sentiment regarding the Polish currency improved materially in recent weeks after having lagged peers for much of 2023. The country’s external balance has been improving sharply lately, inflation in April finally started to ease and Poland’s ruling party last week introduced legislation in a bid to unlock a stalemate at the country’s Constitutional Tribunal. The latter, on President Duda’s request, is reviewing a proposed judiciary overhaul needed to access EU pandemic funds even though it has already been approved by parliament back in February. The stronger zloty is likely to be welcomed by the National Bank of Poland as it helps the fight against inflation. The central bank kicks off its two-day meeting today.

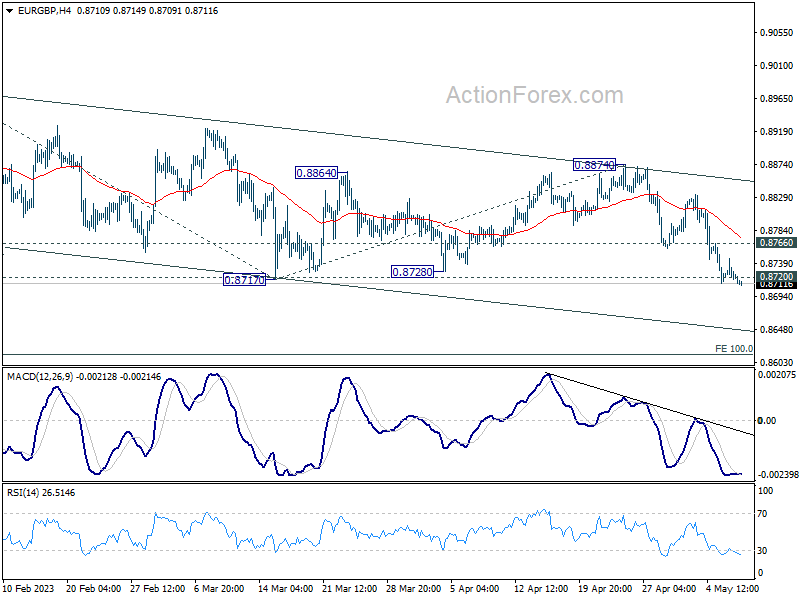

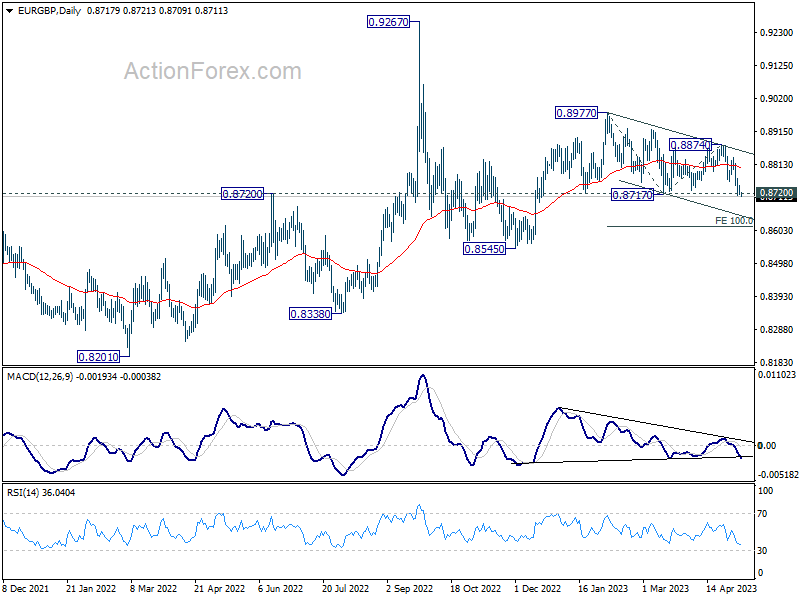

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8711; (P) 0.8728; (R1) 0.8738; More...

Intraday bias in EUR/GBP on the downside at this point. Firm break of 0.8717 will confirm resumption of whole choppy decline from 0.8911. Deeper fall would be seen to 100% projection of 0.8977 to 0.8717 from 0.8874 at 0.8614. On the upside, above 0.8766 minor resistance will turn intraday bias neutral first.

In the bigger picture, outlook remains rather mixed for now, except that price actions from 0.9267 (2022 high) are part of the long term range pattern from 0.9499 (2020 high). With 0.8720 support intact, rise from 0.8545 is in favor to continue through 0.8977. However, firm break of 0.8720 will argue that such rebound has completed, and open up deeper fall through this support level.

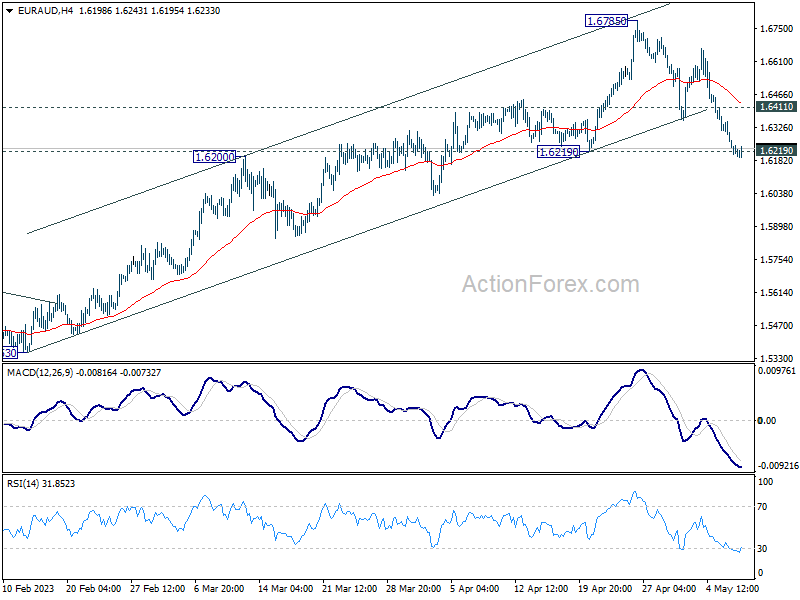

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6176; (P) 1.6264; (R1) 1.6316; More...

Immediate focus is now on 1.6219 support in EUR/AUD. Considering bearish divergence condition in D MACD, decisive break of 1.6219 will argue that it's already in correction to whole up trend from 1.4281. Deeper decline would then be seen towards 1.5254/5976 support zone instead. Meanwhile, rebound from current level, followed by 1.6411 minor resistance will retain near term bullishness, and turn bias back to the upside for retesting 1.6785 resistance instead.

In the bigger picture, the solid break of 1.6434 resistance argues that whole down trend from 1.9799 (2020 high) has completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

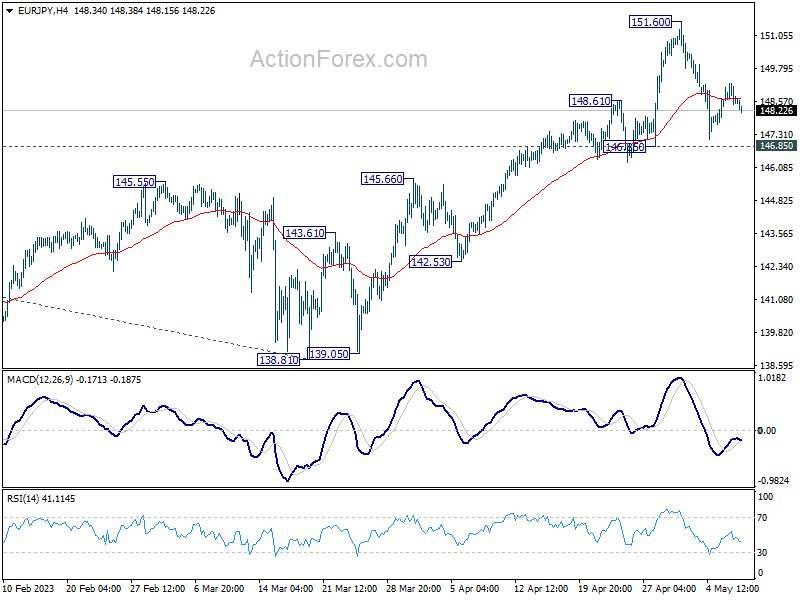

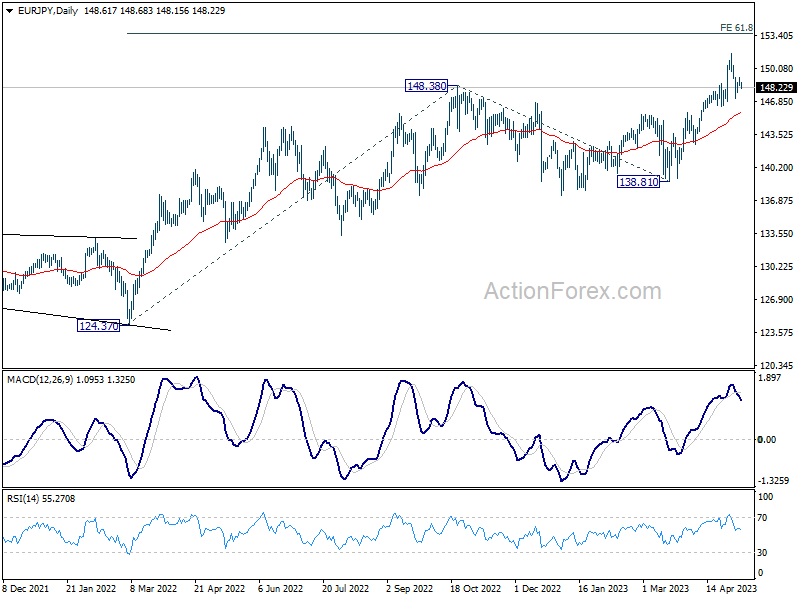

EUR/JPY Daily Outlook

Daily Pivots: (S1) 148.34; (P) 148.81; (R1) 149.15; More....

Range trading continues in EUR/JPY and intraday bias remains neutral. Also, further rise is still expected with 146.85 support intact. On the upside, break of 151.60 will resume larger up trend to 153.64 projection level. Nevertheless, firm break of 146.85 will confirm short term topping and turn bias to the downside for deeper pull back.

In the bigger picture, current development indicates that rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 138.81 support holds, even in case of deep pull back.

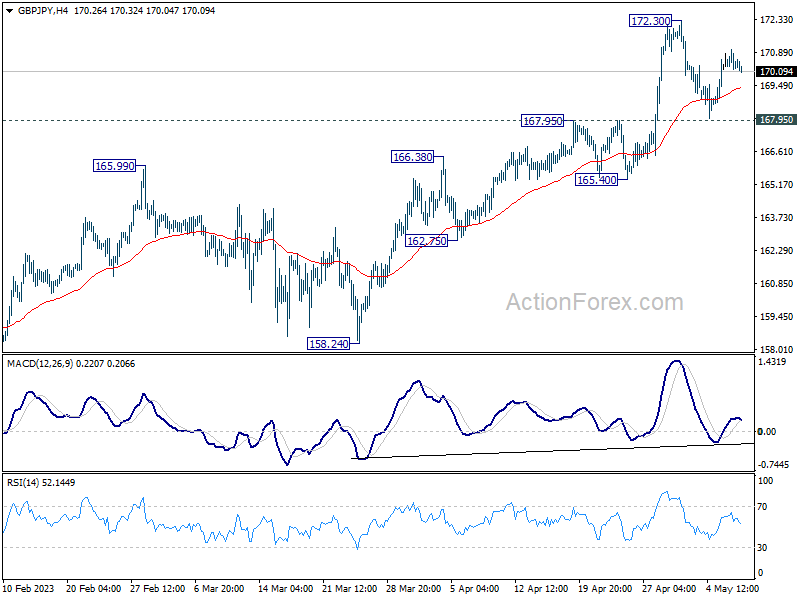

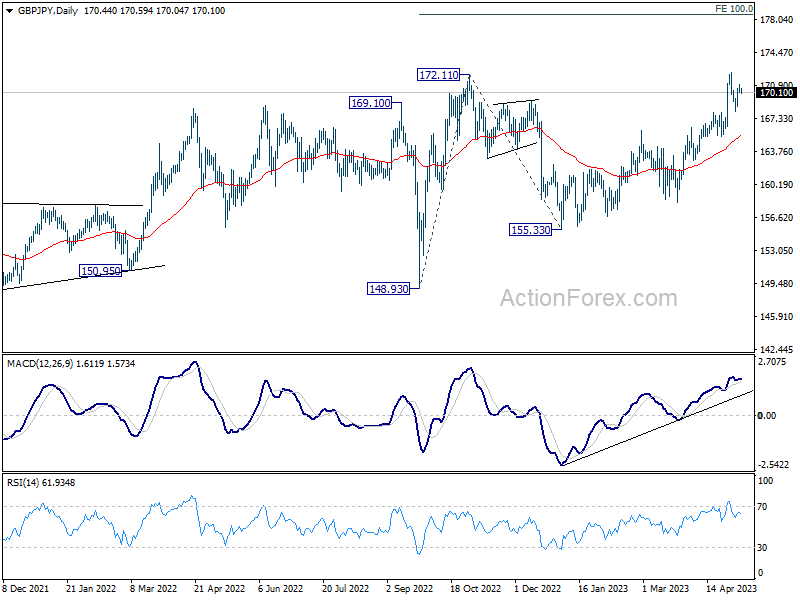

GBP/JPY Daily Outlook

Daily Pivots: (S1) 170.11; (P) 170.59; (R1) 171.00; More...

GBP/JPY is staying in consolidation below 172.30 and intraday bias remains neutral. Further rally is in favor with 167.95 resistance turned support intact. On the upside, break of 172.30 will resume larger up trend to 100% projection of 148.93 to 172.11 from 155.33 at 178.51. Nevertheless, firm break of 167.95 should confirm short term topping, and turn bias back to the downside for deeper pull back to 165.40 support instead.

In the bigger picture, based on current momentum, up trend from 123.94 (2020 low) is likely ready to resume. Next target is 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. This will now remain the favored case as long as 165.40 support holds, in case of retreat.

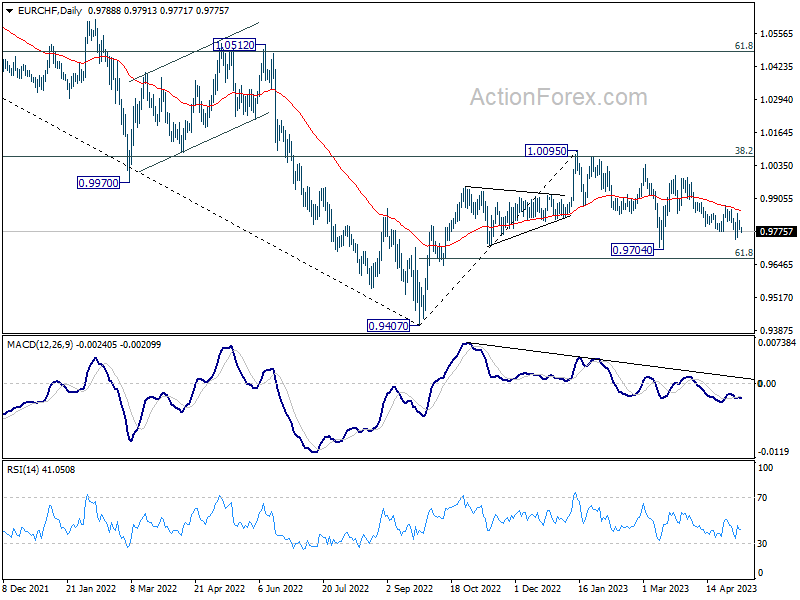

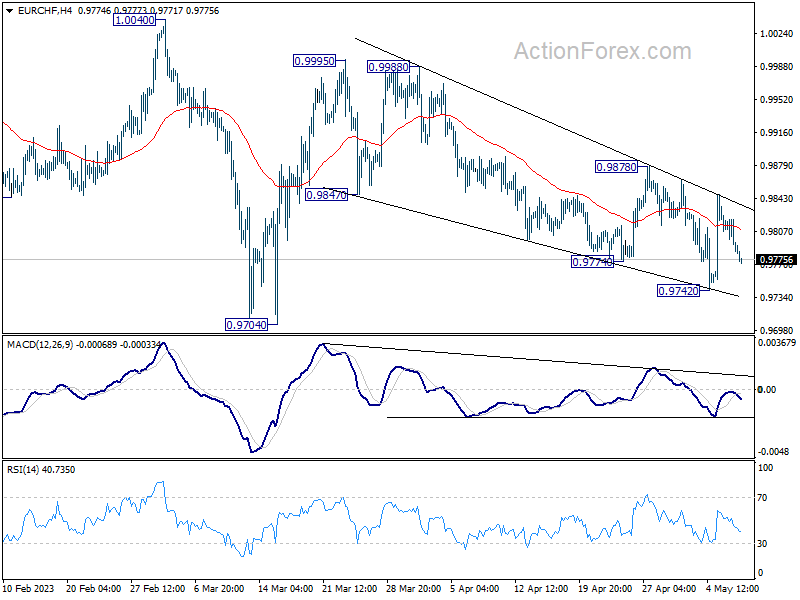

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9775; (P) 0.9799; (R1) 0.9811; More...

Intraday bias in EUR/CHF stays neutral with range trading continuing. Outlook is unchanged that fall from 0.9995 is a correction to rise from 0.9704 only. Break of 0.9878 resistance will indicate that such correction has completed and target 0.9995. Firm break there should confirm that larger corrective decline from 1.0095 has completed at 0.9704 too.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9971) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).