Sample Category Title

Iran War Fuels King Dollar Comeback as Oil Shock Ripples Through Markets

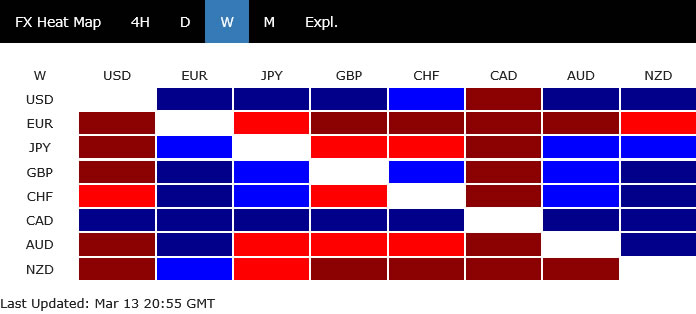

“King Dollar” returned with a vengeance last week as global markets were jolted by a volatile mix of geopolitical escalation and a dramatic repricing of U.S. monetary policy expectations. The greenback surged broadly, pushing Dollar Index back above the psychological 100 level. The question now is how long Dollar can keep the “throne”. To answer that, we need to examine the macro forces driving markets and how they could evolve in the coming weeks.

The ultimate driver remains the Iran war. Since the February 28 escalation between the U.S./Israel and Iran, the conflict has entered what analysts describe as a phase of “horizontal escalation,” widening its geographic and economic reach. Reports indicate that the Strait of Hormuz—responsible for roughly a quarter of global seaborne oil shipments in 2025—has effectively been closed to major tanker traffic. Recent U.S. strikes targeting Iranian installations on Kharg Island have further raised fears that part of Iran’s export capacity could be permanently removed from global supply.

The energy shock triggered violent reactions in oil markets, with WTI crude spiking toward $120 before stabilizing slightly below $100 by the end of the week. The International Energy Agency attempted to ease the situation by announcing a record 400 million barrel emergency release, the largest in its 52-year history. Yet traders remain skeptical. The release represents only about 20 days of disrupted supply if Hormuz remains blocked, meaning a sizeable “war premium” is still embedded in crude prices.

The consequences have quickly spread across global markets. Inflation fears have triggered a sharp hawkish shift in central bank expectations. In particular, markets are increasingly abandoning forecasts for Fed rate cuts in 2026. U.S. Treasury yields surged toward the critical 4.3% zone, equities sold off sharply with DOW threatening 45,000 psychological level, and Dollar Index pushed above 100 for the first time in months. If the Iran war drags on—as Iranian strategists increasingly signal through their “endurance” doctrine—elevated oil prices, rising yields, and fragile risk sentiment could allow the Dollar to keep its "throne" for longer than many expected.

Why the War May Drag On

One reason markets remain reluctant to unwind the recent risk-off move is the growing belief that the Iran conflict would not end quickly. Analysts note that the war has already moved beyond a conventional exchange of airstrikes and into a broader regional confrontation involving shipping lanes, energy infrastructure, and proxy forces. Even after heavy U.S. and Israeli strikes, Iran has continued missile and drone attacks across the region while disrupting traffic through the Strait of Hormuz.

Meanwhile, neither Washington nor Tehran appears willing to compromise. U.S. officials insist the campaign will continue until strategic objectives are achieved, while Iran’s leadership has signaled a willingness to prolong the confrontation and impose economic pressure through energy disruption

More importantly, reopening the Strait is not simply a political decision but a complex military and logistical challenge. Naval mines, tanker attacks, and insurance withdrawals have effectively halted commercial traffic, and experts warn that securing the waterway could take weeks even in the absence of active fighting.

Most analysts are now pricing in a conflict duration of three weeks to two months. However, the "horizontal" nature of the attacks means that even if the main bombing stops, the guerrilla-style disruption of oil and shipping could haunt markets for the rest of 2026.

Dollar Index Breaks Above 100, Eyes 101.13 as Trend Reversal Builds

Dollar Index extended its rebound from the 95.55 low last week and pushed above the key 100.39 structural resistance, marking an important technical development. Equally notable was the close above the 55 W EMA (now at 99.62), which reinforces the view that medium-term momentum has turned bullish after the prolonged decline through much of 2025.

The immediate focus now turns to 100% retracement of 110.17 (2025 high) to 95.55 at 101.13. Decisive break above this level would confirm that the medium-term bottom at 95.55 is likely already in place. Such a move would open the door for a strong rally recovery toward 61.8% retracement at 104.58, particularly if the current macro backdrop of elevated oil prices, rising yields, and persistent geopolitical tensions continues to support Dollar demand.

On the downside, rejection by 101.13 followed by a break of 98.49 support would suggest that the current rebound has run its course. In that case, the move from 95.55 could be interpreted as merely a corrective bounce within the broader bearish structure that dominated 2025.

From a longer-term perspective, a sustained move above 101.13 would also carry important implications for the Dollar’s structural outlook. Such a breakout would likely push Dollar Index through the 55 M EMA (now at 102.31).

That would strengthening the case that the entire down trend from 114.77 (2022 high) to 95.55 trough was a completed three-wave correction, after hitting the long-term rising channel floor that has been in place since 2010. If that scenario unfolds, it could signal that the broader uptrend originating from the 70.69 low in 2008 is probably resuming.

DOW Correction Targets 45,000 as Risk-Off Pressure Builds

DOW’s decline from the 50,512.79 medium term accelerated last week, reflecting the sharp shift in global market sentiment triggered by rising oil prices and the hawkish repricing of interest rate expectations. The index finished the week on a weak note, signaling that sellers remain in control for the time being.

Technically, the correction still has room to run as long as 48,220.54 resistance caps any near-term rebounds. The next major downside objective is the 38.2% retracement of 36,611.78 to 50,512.79 at 45,202.60.

Even if the index briefly slips below 45,202.60, strong support could emerge near 45,000 psychological threshold. This region aligns closely with the former 2024 peak at 45,071.29 and could attract bargain hunting that stabilizes the correction.

Nevertheless, decisive breakdown below 45,000 would mark a significant shift in the technical outlook. Such a move would imply that the entire advance from the 36,611.78 base (2025 low) is reversing and could expose DOW to deeper fall toward 61.8% retracement at 41,921.97. A decline of that magnitude would likely amplify risk-off flows and further support Dollar.

10-Year Yield Eyes 4.311 Break as Inflation Fears Intensify

US 10-year Treasury yield extended its rebound from 3.956 last week and accelerated sharply higher to close at 4.285. The move reflects a dramatic repricing of inflation and monetary policy expectations as markets digest the energy shock triggered by the Iran war and the growing likelihood that the Fed at current restrictive level for longer.

The immediate focus now turns to 4.311, a key structural resistance level. Decisive break above there would suggest that the converging triangle pattern that began from the 4.809 (2025 high) has already completed with five waves down to 3.956. Such a breakout would signal that yields are entering a fresh medium-term rally phase.

If confirmed, the next upside target would lie at 4.629 resistance, with the possibility of a further move back toward the 4.809 peak should inflation expectations continue to rise. A sustained yield rally of that magnitude would likely intensify pressure on equity markets while providing a powerful tailwind for Dollar.

On the other hand, rejection at 4.311 followed by a break below 4.104 support would suggest that the current move higher is merely another leg within the broader consolidation pattern. In that case, Treasury yields could remain trapped within a range as markets wait for clearer signals on inflation and central bank policy.

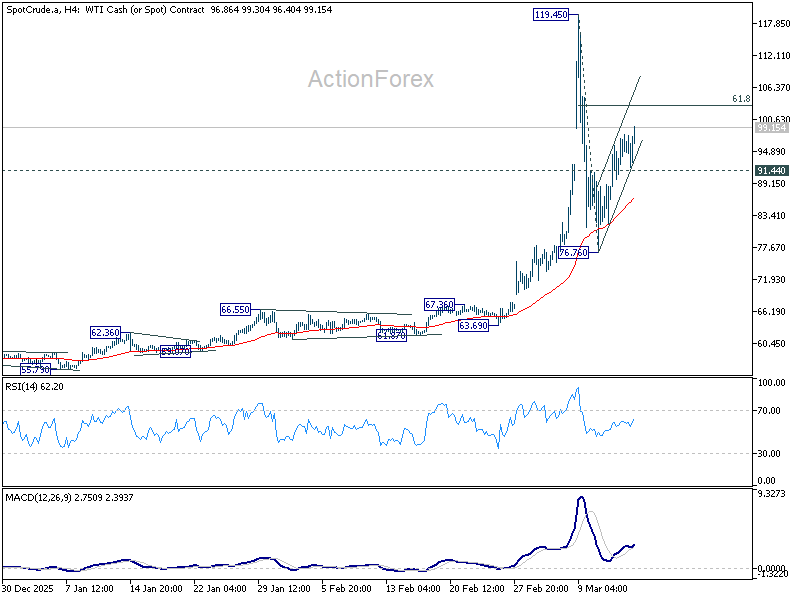

WTI Rebound Should Slow Above 103

WTI crude is now in a consolidation phase following last week’s extreme volatility. Technically, the rebound from 76.76 is seen as the second leg of the corrective pattern from 119.45. As long as the 91.44 support level holds, the near-term bias remains tilted to the upside, with the next key objective located at 61.8% retracement of 119.45 to 76.76 at 103.14.

Upward momentum should begin to fade once prices breaks above 103.14 that region. WTI should form a near-term top below 119.45 and reverse from there to extend the corrective pattern.

That said, any decisive acceleration above 103.14 would be a warning signal that the consolidation has ended. Such a breakout could trigger a renewed rally through 119.45 peak, especially if supply disruptions in the Middle East persist.

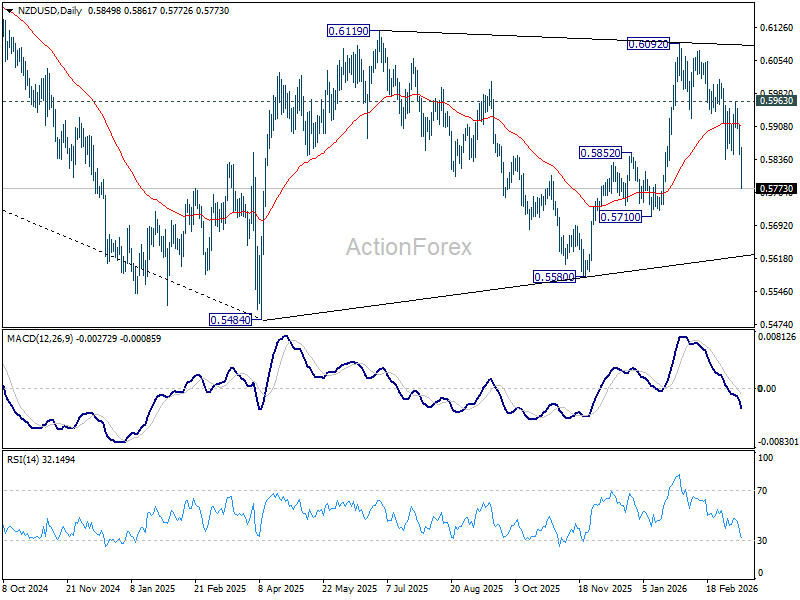

NZD Slides as RBNZ Outlook Diverges From Global Hawkish Shift

New Zealand Dollar was the worst performer for the week, with NZD/USD being the top mover, down -2.12%. That reflects the widening policy divergence between RBNZ and other major economies where markets are increasingly pricing in renewed tightening.

While investors are now betting on rate hikes from central banks such as the RBA and potentially others, expectations for the RBNZ remain far more cautious. Policymakers face a difficult dilemma: raising rates to combat oil-driven inflation risks pushing an already fragile economy into a deeper recession.

Additionally, the RBNZ continues to emphasize the presence of significant spare capacity in the economy, which policymakers believe will limit the risk of second-round inflation effects. As a result, the most hawkish outcome markets currently expect from the central bank is simply maintaining current policy settings throughout the year.

Technically, NZD/USD's accelerated decline and break of 0.5852 support turned resistance suggest that rebound from 0.5580 has completed.

Risk will stay on the downside as long as 0.5963 resistance holds. Further break of 0.5710 support will argue that whole consolidation pattern from 0.5484 (2025 low) has completed with three waves to 0.6092. That should bring deeper fall through 0.5580 support to retest 0.5484.

In the long term picture, current development suggests that NZD/USD was rejected by the falling 55 EMA (now at 0.6117) again. Firm break of 0.5484/67 support zone will resume whole down trend from 0.8835 (2014 high). Next medium term target will be 0.4890 (2009 low).

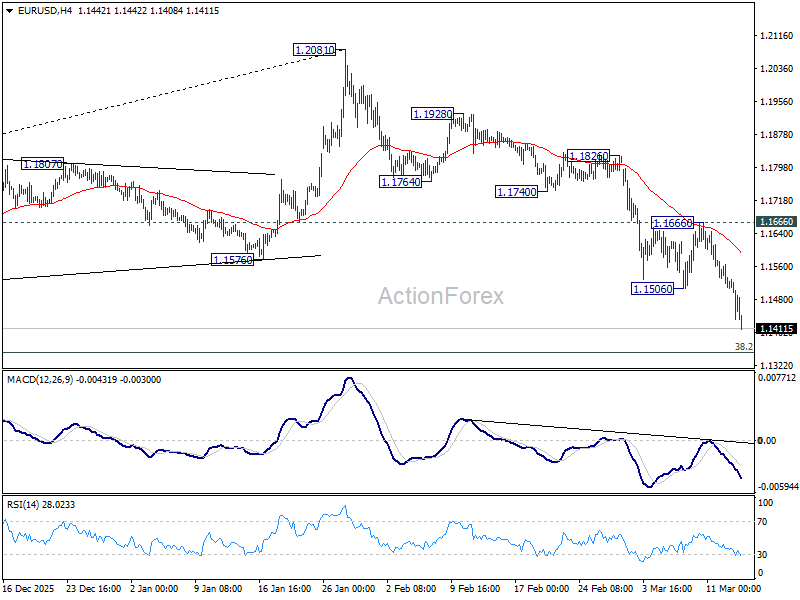

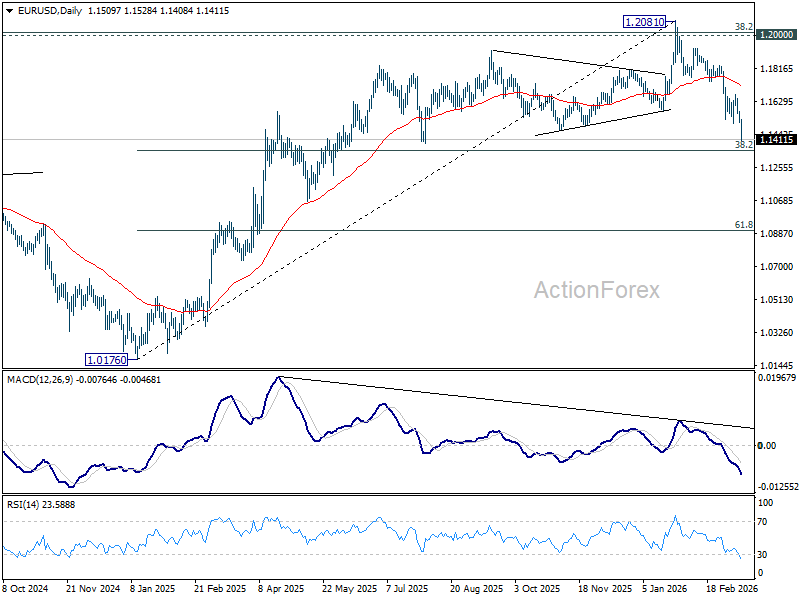

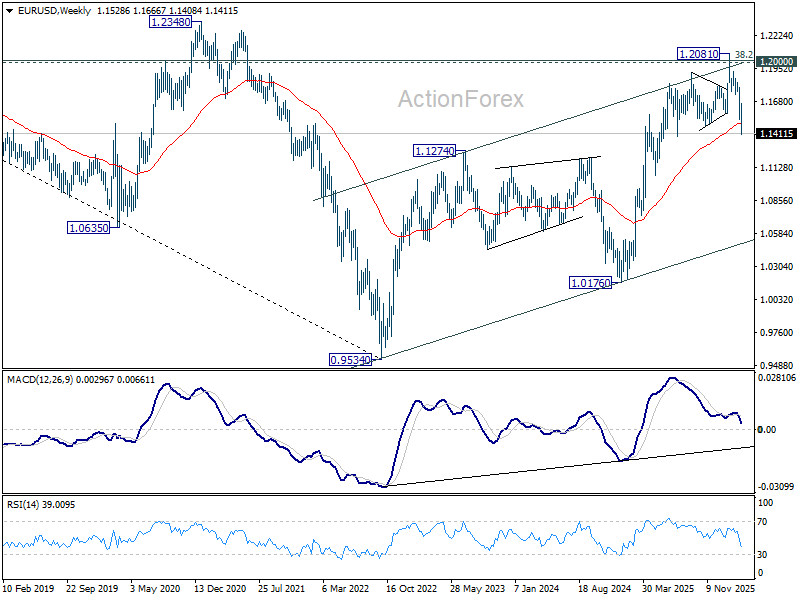

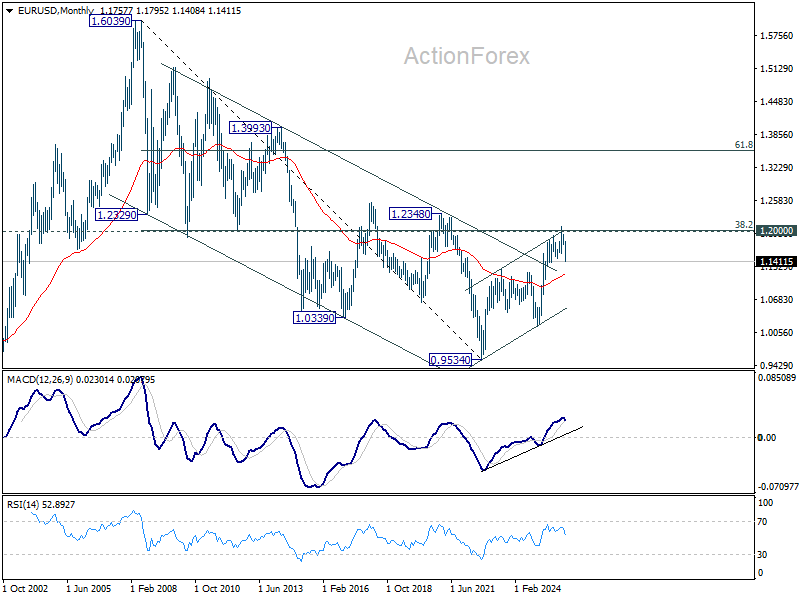

EUR/USD Weekly Outlook

EUR/USD's fall from 1.2081 resumed by breaking through 1.1506 last week. Initial bias stays on the downside this week for 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Firm break there will target 61.8% projection at 1.0904 next. Overall, near term outlook will stay cautiously bearish as long as 1.1666 resistance holds, in case of another recovery.

In the bigger picture, the break of 55 W EMA (now at 1.1495) confirms rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. In either case, deeper fall is now expected to long term channel support (now at 1.0528. Risk will stay on the downside as long as 1.2081 holds, in case of recovery.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

EUR/USD Weekly Outlook

EUR/USD's fall from 1.2081 resumed by breaking through 1.1506 last week. Initial bias stays on the downside this week for 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Firm break there will target 61.8% projection at 1.0904 next. Overall, near term outlook will stay cautiously bearish as long as 1.1666 resistance holds, in case of another recovery.

In the bigger picture, the break of 55 W EMA (now at 1.1495) confirms rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. In either case, deeper fall is now expected to long term channel support (now at 1.0528. Risk will stay on the downside as long as 1.2081 holds, in case of recovery.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

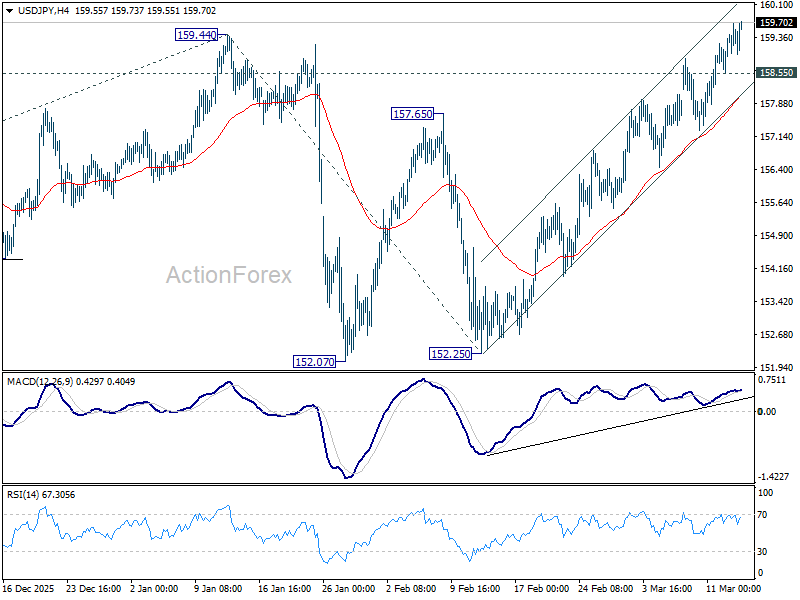

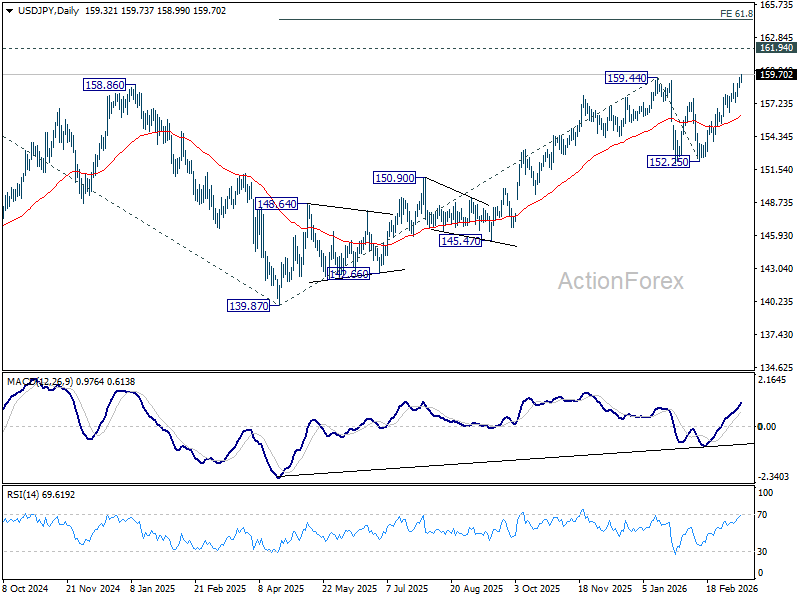

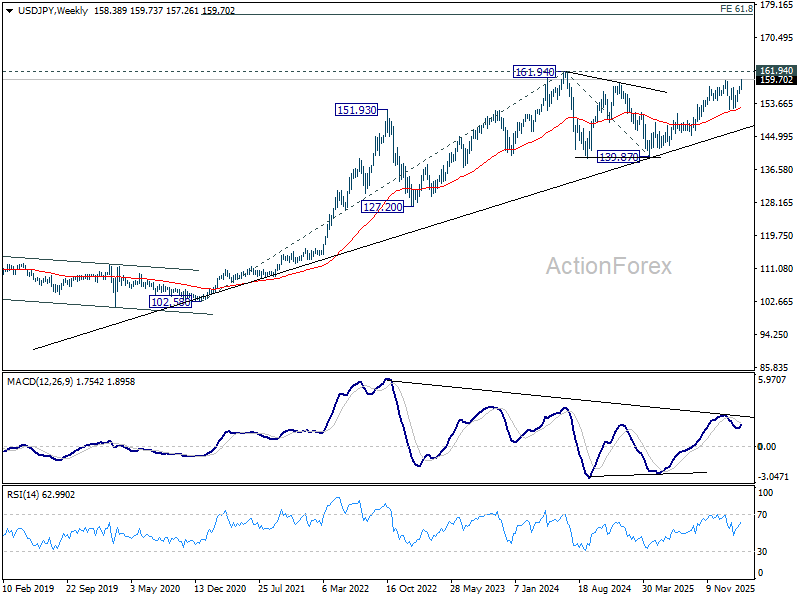

USD/JPY Weekly Outlook

USD/JPY's up trend from 139.87 resumed by breaking through 159.44 last week. Initial bias remains on the upside this week for retesting 161.94 high first. Firm break there will confirm larger up trend resumption and target 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. On the downside, below 158.55 minor support will turn intraday bias neutral first.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

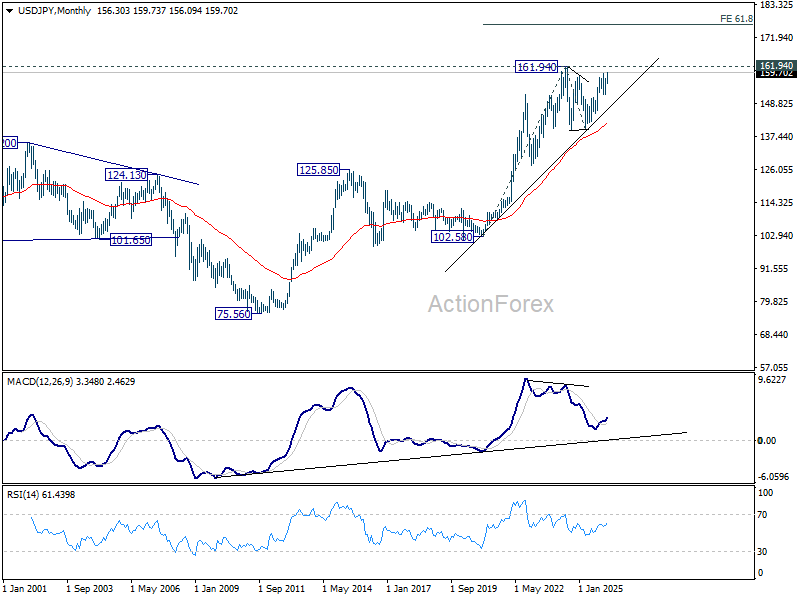

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resume. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

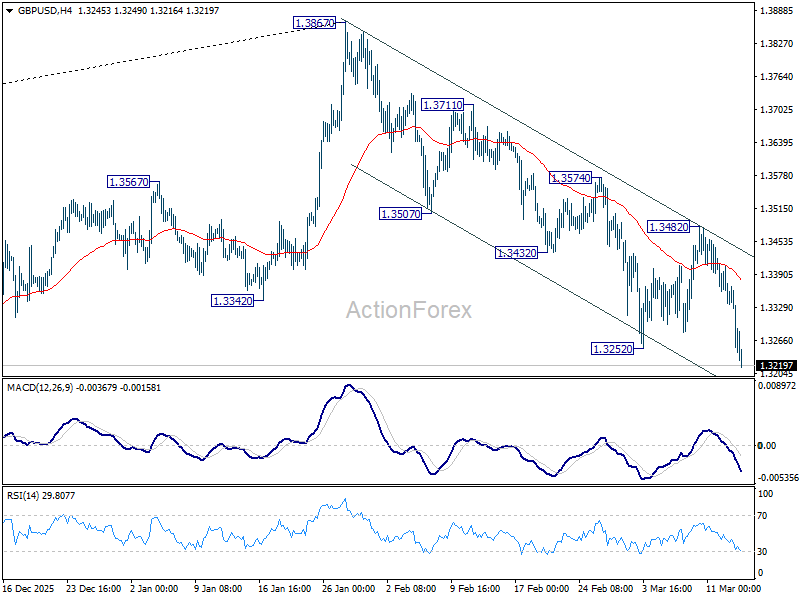

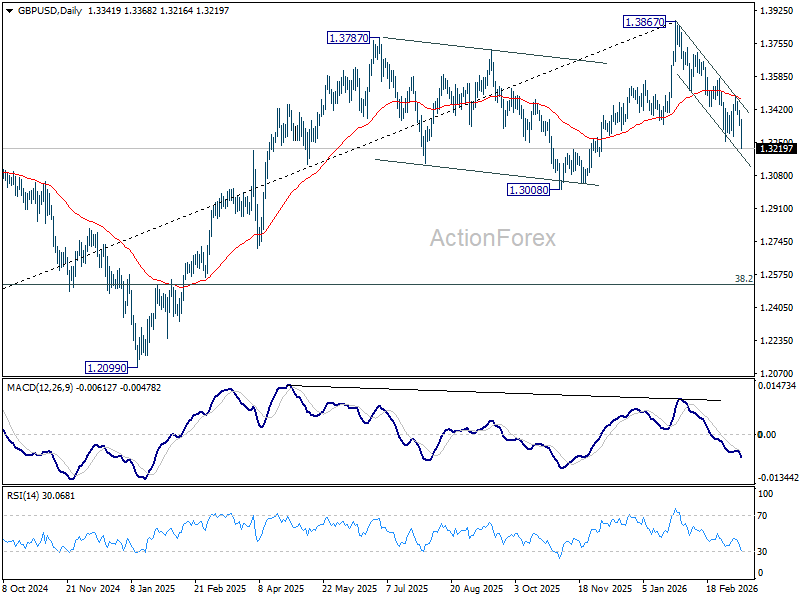

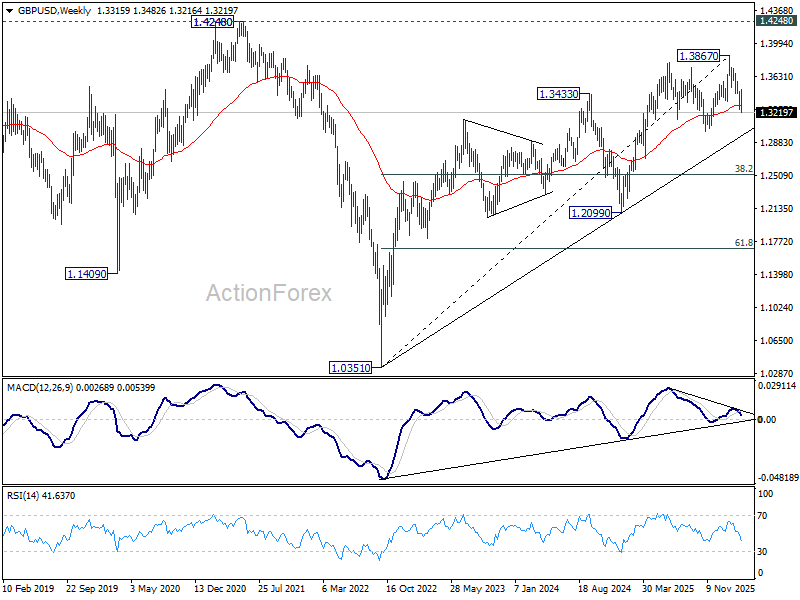

GBP/USD Weekly Outlook

After initial rebound, GBP/USD's fall from 1.3867 resumed by breaking through 1.3252. Initial bias remains on the downside this week for 1.3008 structural support. Firm break there will carry larger bearish implication and target 1.2524 fibonacci level. For now, risk will stay on the downside as long as 1.3482 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

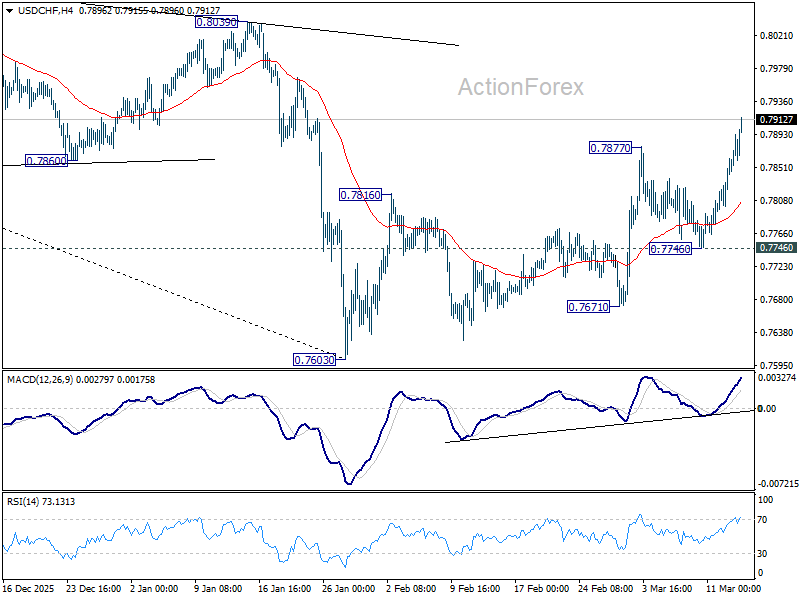

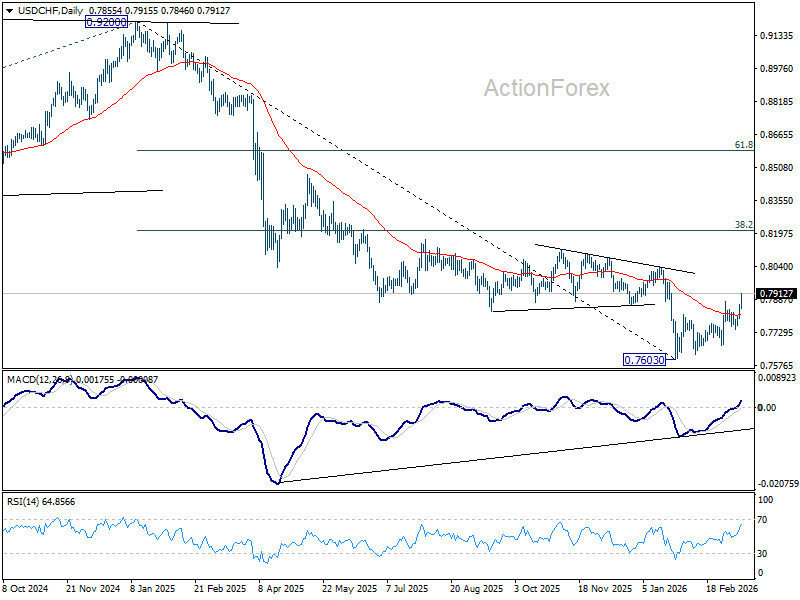

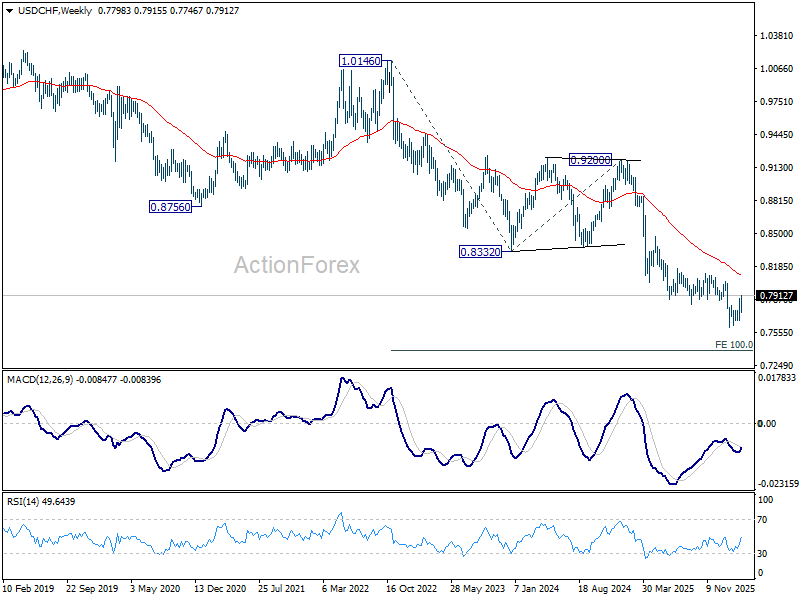

USD/CHF Weekly Outlook

USD/CHF's rally from 0.7603 extended higher last week. The strong break of 55 D EMA (now at 0.7817) suggests that it's already corrective whole down trend from 0.9200. Initial bias is on the upside this week for 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, risk will stay on the upside as long as 0.7746 support holds, in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8100) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

AUD/USD Weekly Report

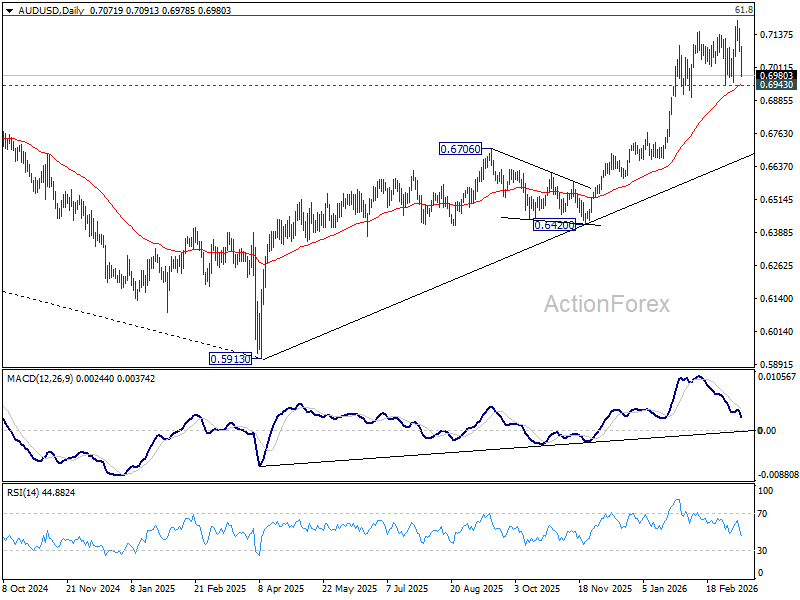

AUD/USD edged higher to 0.7187 last week but fell sharply from there. Nonetheless, downside is contained above 0.6943 support so far. Initial bias remains neutral this week first, and further rally is in favor at a later stage. However, firm break of 0.6943 will confirm initial rejection by 0.7206 fibonacci level, and turn bias back to the downside for deeper pullback.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above.

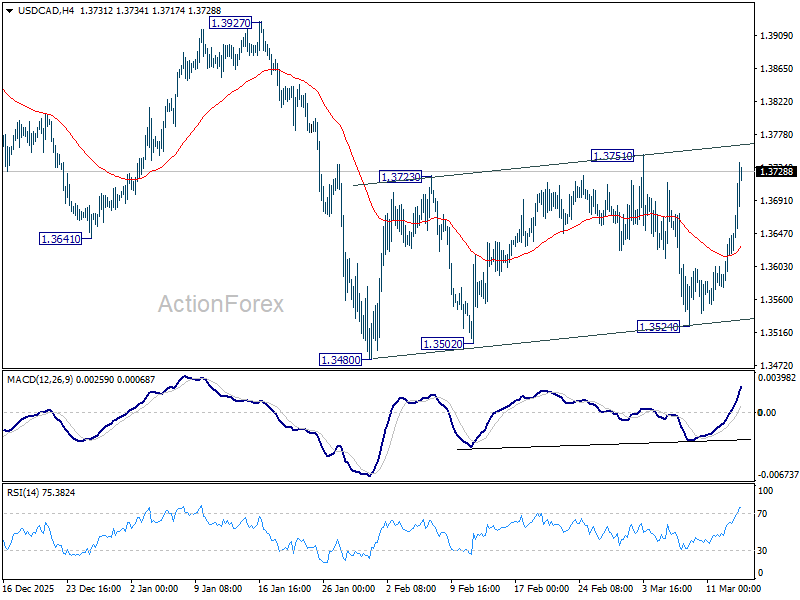

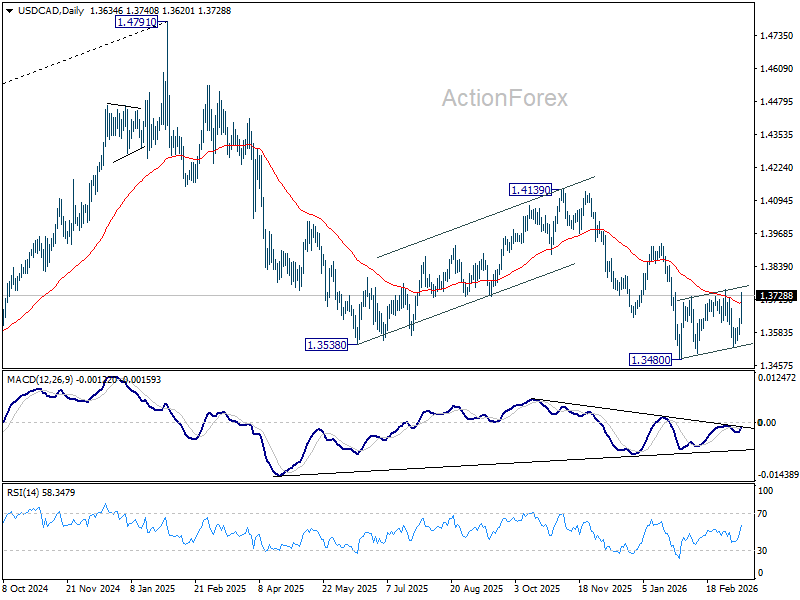

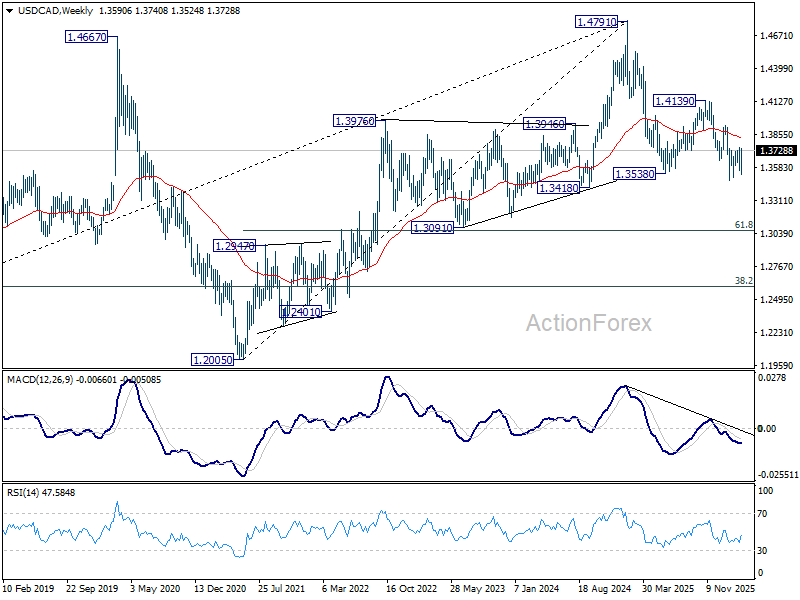

USD/CAD Weekly Outlook

USD/CAD staged a strong rebound after initial dip to 1.3524 last week. But upside is still capped below 1.3751 resistance. Initial bias remains neutral this week first. On the upside, firm break of 1.3751 will suggest that stronger rebound is underway, and target 1.3927 resistance first. Meanwhile, break of 1.3524 support will bring resumption of whole down trend from 1.4791.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

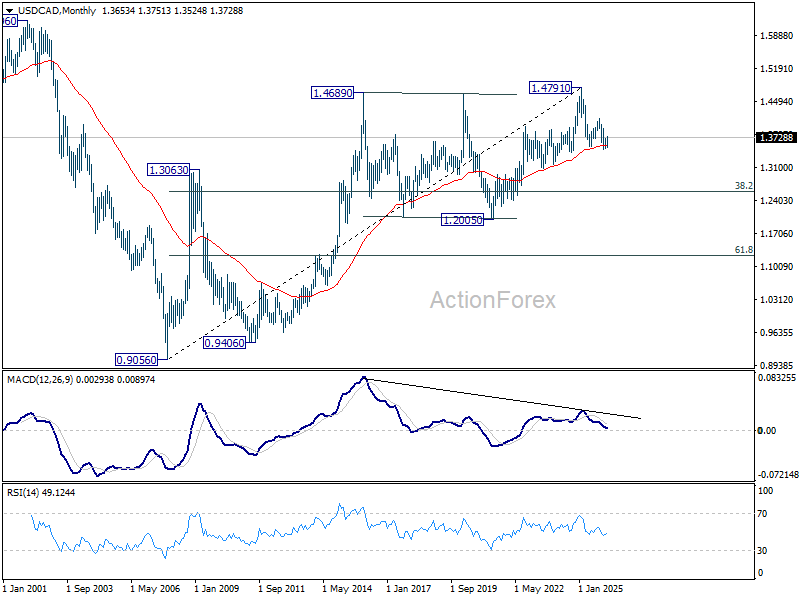

In the long term picture, rising 55 M EMA (now at 1.3569) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

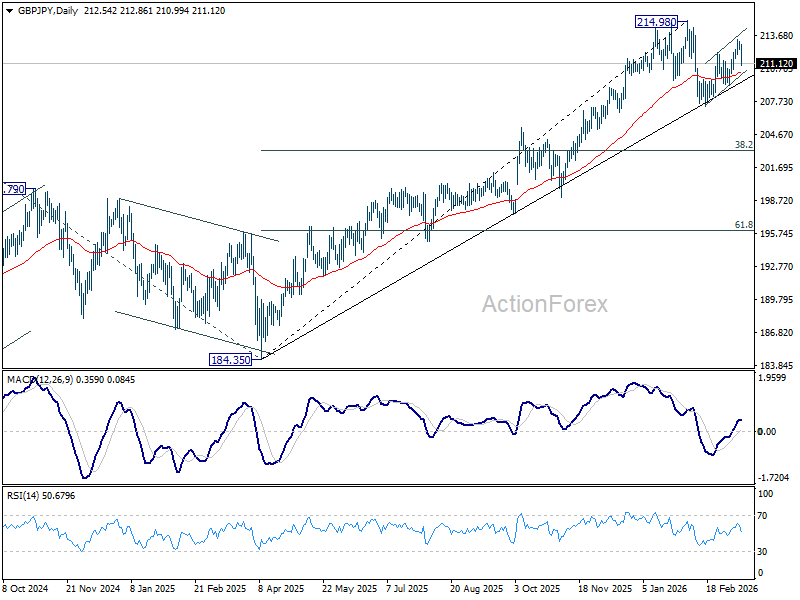

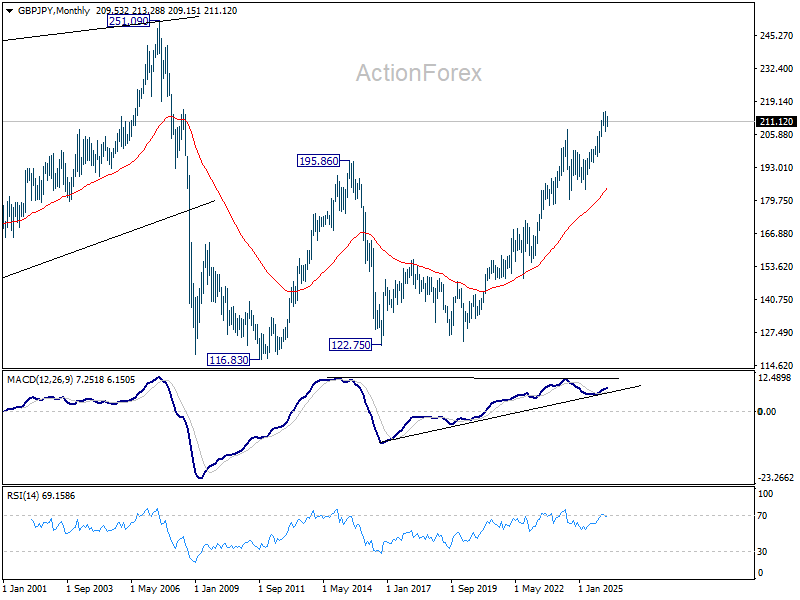

GBP/JPY Weekly Outlook

GBP/JPY rose further to 213.28 last week. But subsequent selloff from there argue that the rebound fro 207.20 has completed as a three-wave corrective move. Initial bias is mildly on the downside this week for 209.15. Firm break there will solidify this case and target 207.20 next. On the upside, however, above 213.28 will target a retest on 214.98 high instead.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 202.80) holds, even in case of another deep pullback.

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 184.02) holds.

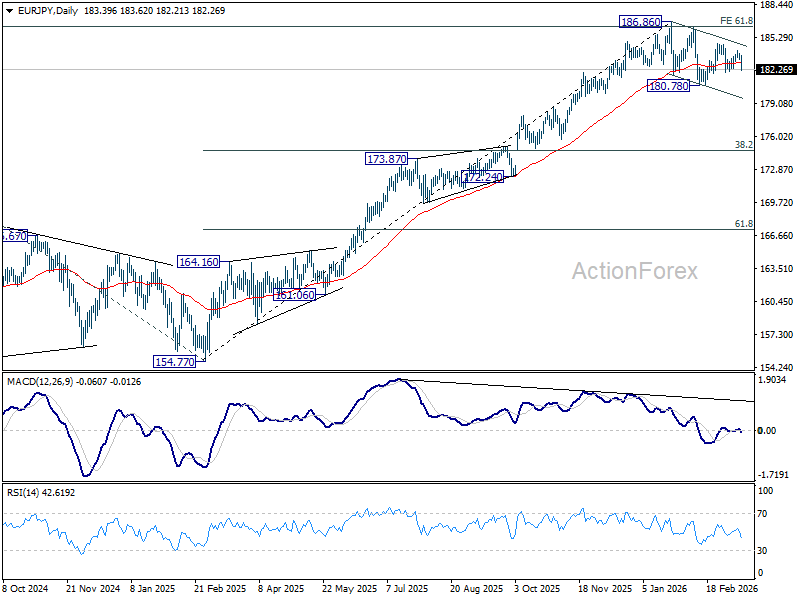

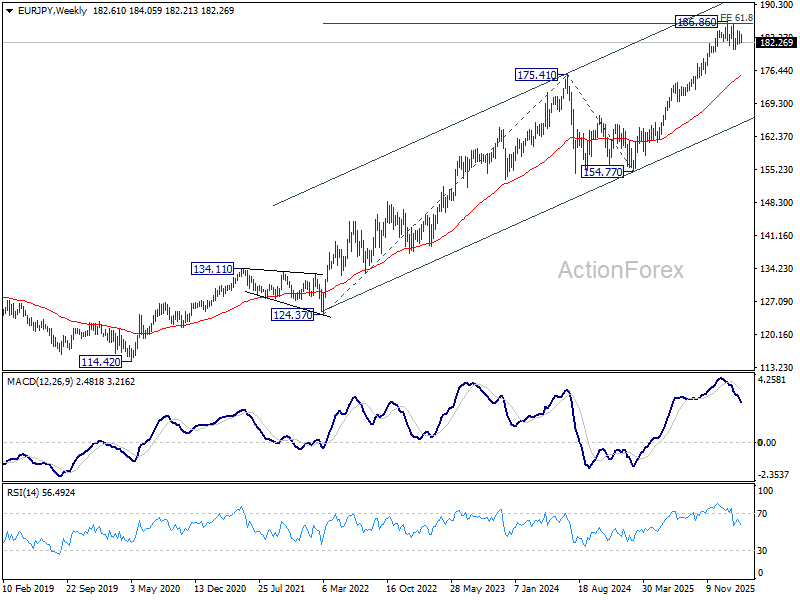

EUR/JPY Weekly Outlook

Range trading continued in EUR/JPY last week and overall outlook is unchanged. Initial bias remains neutral this week first. On the downside, below 182.00 will target 180.78. Firm break there will indicate that fall from 186.86 is already correcting whole up rise from 154.77. On the upside, above 184.75 will resume the rebound from 180.78 to retest 186.86 high.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 174.73) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

EUR/GBP Weekly Outlook

EUR/GBP accelerated lower to 0.8615 last week but recovered just ahead of 0.8611 support. Initial bias is turned neutral this week for some consolidations first. Further decline is expected as long as 55 D EMA (now at 0.8694) holds. Firm break of 0.8611 will resume the whole fall from 0.8863 to 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.