Sample Category Title

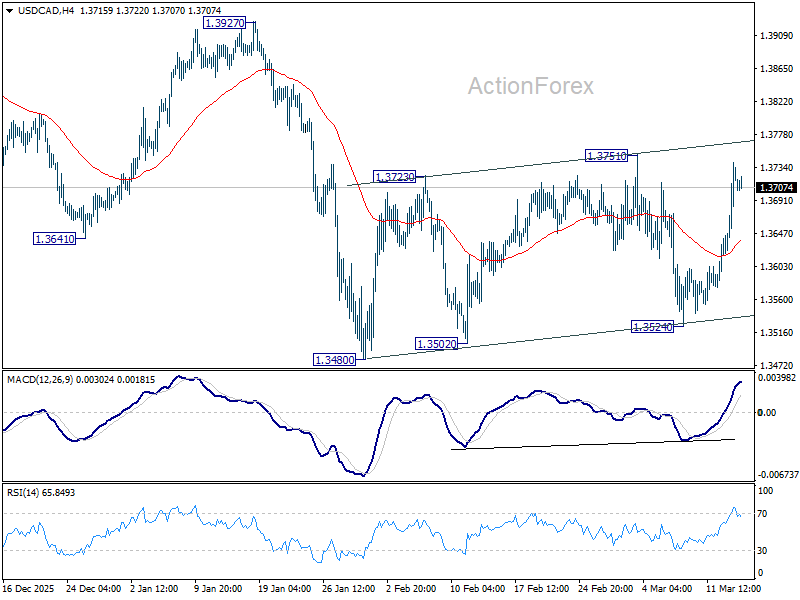

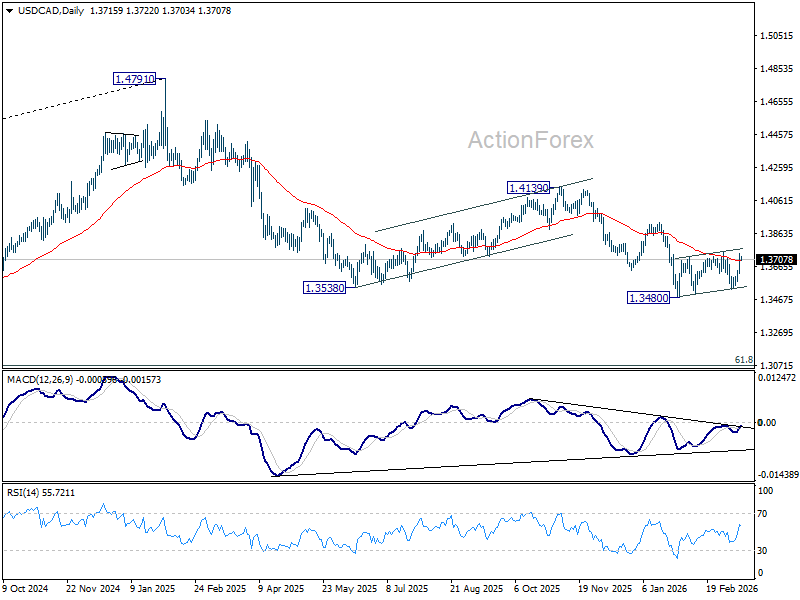

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3656; (P) 1.3699; (R1) 1.3778; More...

Intraday bias in USD/CAD stays neutral first with focus on 1.3751 resistance. Firm break there will suggest that stronger rebound is underway, and target 1.3927 resistance first. Meanwhile, break of 1.3524 support will bring resumption of whole down trend from 1.4791.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

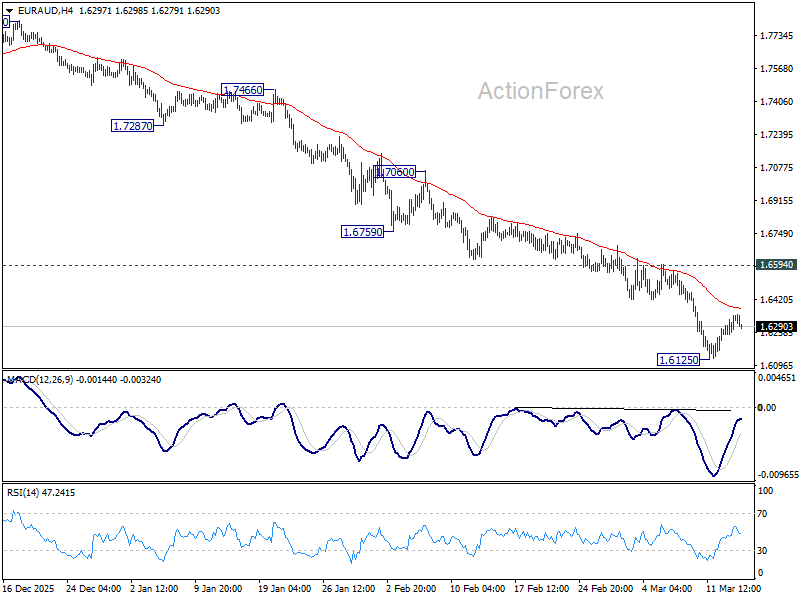

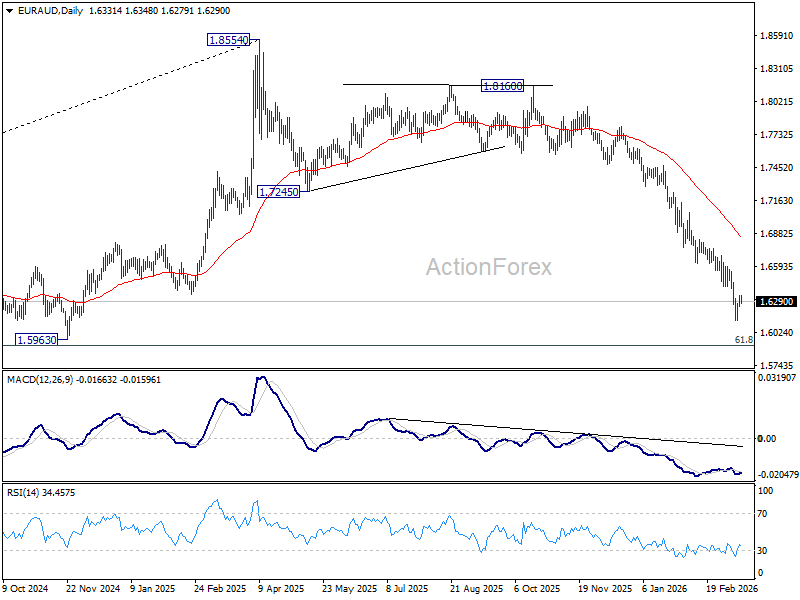

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6284; (P) 1.6321; (R1) 1.6393; More...

Intraday bias in EUR/AUD remains neutral and more consolidations would be seen above 1.6125 first. Outlook will remain bearish as long as 1.6594 resistance holds. Firm break of 1.6125 will resume the fall from 1.8554 to 1.5913 fibonacci level next. Nevertheless, break of 1.6594 will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7238) holds, even in case of strong rebound.

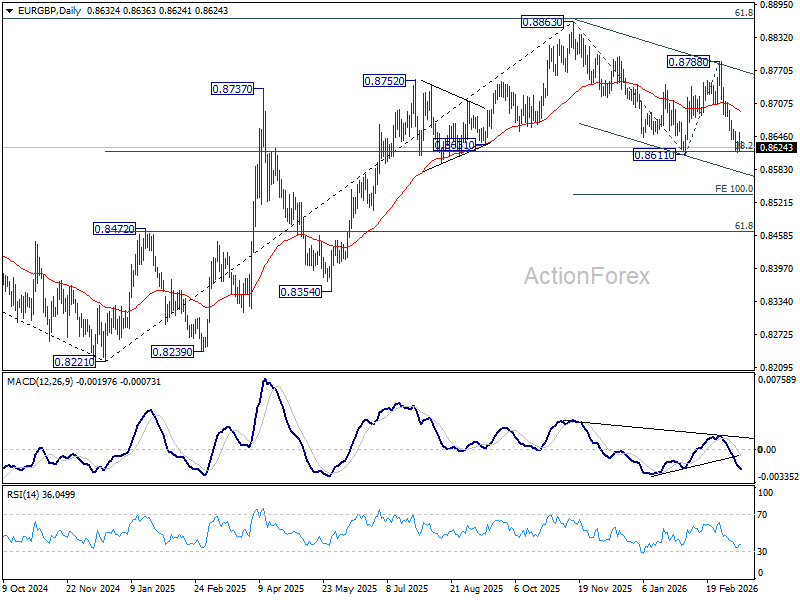

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8619; (P) 0.8638; (R1) 0.8656; More…

Intraday bias in EUR/GBP stays neutral and more consolidations could be seen above 0.8615 first. Further decline is expected as long as 55 D EMA (now at 0.8691) holds. Firm break of 0.8611 will resume the whole fall from 0.8863 to 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

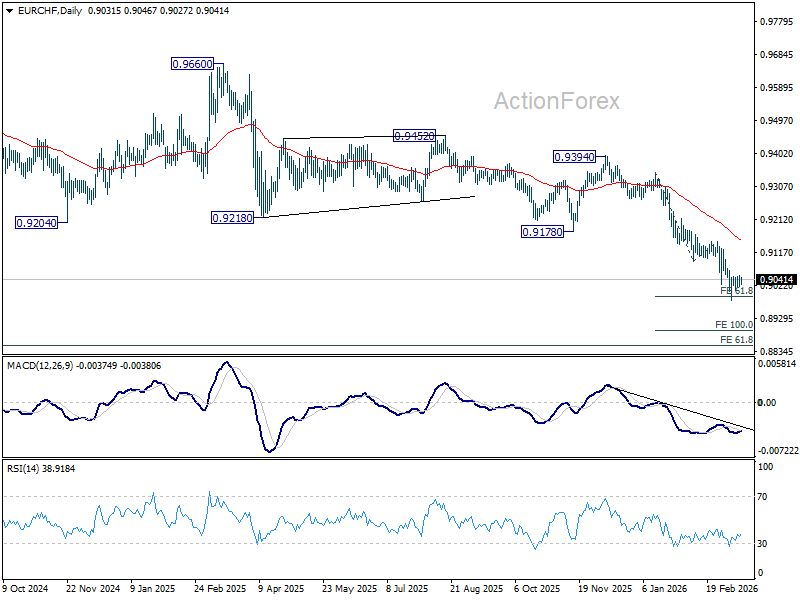

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9018; (P) 0.9038; (R1) 0.9054; More....

EUR/CHF is still extending the consolidation pattern from 0.8979 and intraday bias stays neutral. Risk will stay on the downside as long as 0.9092 support turned resistance holds. On the downside, firm break of 0.8979 will resume larger down trend to 100% projection of 0.9347 to 0.9092 from 0.9149 at 0.8894.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

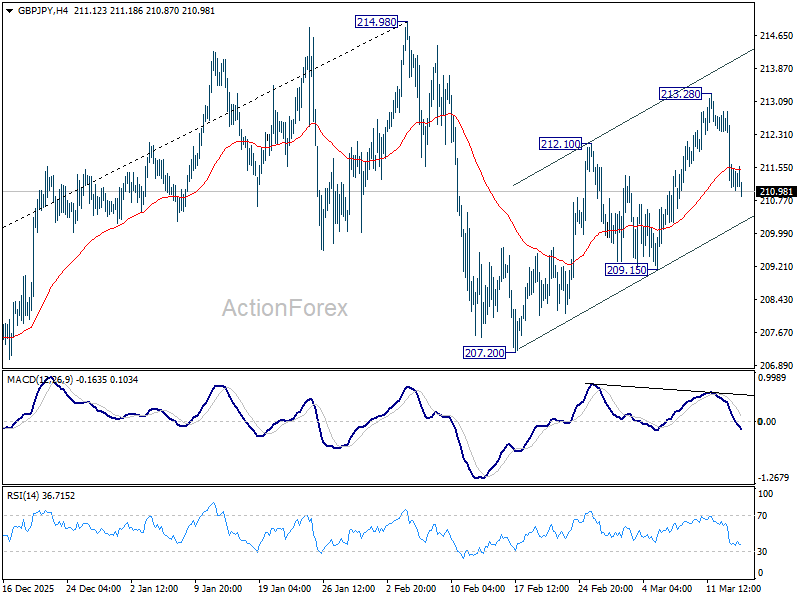

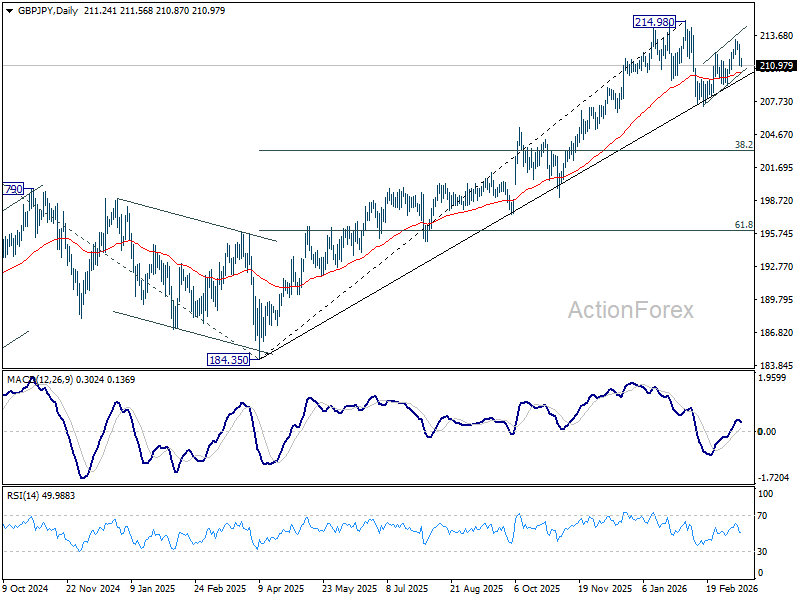

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.28; (P) 212.75; (R1) 213.09; More...

Intraday bias in GBP/JPY remains mildly on the downside at this point. Rebound from 207.20 should have completed with three waves up to 213.28. Deeper fall would be seen to 209.15 support first. Firm break there will solidify this case and target 207.20 next. On the upside, however, above 213.28 will target a retest on 214.98 high instead.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.08) holds, even in case of another deep pullback.

What Will Central Banks Say?

The week started on a now-usual pattern, with oil prices pushing higher at the open and retracing part of their gains as investors digested the latest news from the Middle East. The major developments include the bombing of the major Iranian export hub late Friday, Iran’s announcement that the Strait of Hormuz could be used by countries that are not the US, Israel and their allies – though it remains unclear how “allies” would be defined and enforced – and the announcement from the IEA that oil reserves (you know - the 400 million barrels they’re ready to release from strategic reserves) could be made available immediately in Asia, which is the region most dependent on oil passing through this very Strait of Hormuz.

Overall, the bombing of Kharg Island – and the continued attacks between the parties – suggests the conflict is not close to an end.

Still, there is some relief in Asia this morning on news that two tankers carrying liquefied petroleum gas to India were able to sail through the strait. The US has asked countries around the world to send ships to the region to help keep shipping routes open. The response, however, has been mixed – it is indeed a very politically and geopolitically sensitive call to make.

US crude kicked off the week with a spike above $100 per barrel and is now consolidating near $98.50, while Brent started just below the $100 mark and is now trading slightly above it. Dubai crude is diverging, with the barrel trading above $123.

The relief that oil could continue flowing toward Asia pushed several regional indices higher: the Nikkei is up nearly 1% at the time of writing, the Korean Kospi is rebounding more than 1%, while China’s CSI 300 dipped at the open but managed to retrace early losses on data showing better-than-expected investment, production and retail sales figures, although the uptick in the unemployment rate raised concerns.

Now that we’re speaking of data, Friday’s US figures came with surprises – and not necessarily good ones. US GDP was revised further down to 0.7% for Q4, from 1.4% printed a month earlier and well below the 4.4% recorded in Q3. Sales grew just 0.4%, while price pressures increased to 3.8%. More recent data showed that the core PCE index – the Federal Reserve’s (Fed) preferred gauge of inflation – ticked higher to 3.1% in January from 3.0% the month before. The uptick was broadly expected and priced in, yet confirmation that price pressures were already rising before the Middle East conflict pushed energy prices higher did little to reassure Fed doves.

The Fed will meet this week and will most probably leave rates unchanged. Pressure from the White House is unlikely to change that – especially after the reason Jerome Powell was attacked by the White House was judged to be “thin and unsubstantiated”. So no rate cuts this week in the US – and possibly none this year. If the war continues and keeps energy prices elevated, rate cuts will remain unlikely.

The US 2-year yield is now at its highest level since last August, while the US dollar index spiked to the highest levels since November. The greenback is softer in Asia this morning – which is also supporting regional equities – but the conflict is far from over, and the US dollar’s appreciation could continue in the coming weeks, alongside rising global energy prices and fading expectations of Fed easing.

The Fed is not the only central bank delivering a decision this week. The calendar is packed with major policy meetings: the European Central Bank (ECB), the Bank of England (BoE), the Swiss National Bank (SNB), the Bank of Japan (BoJ), the Reserve Bank of Australia (RBA) and the People’s Bank of China (PBoC) will all announce their latest policy decisions, and their task is not an easy one.

All of them will be torn between the upcoming spike in inflation due to rising oil and gas prices and the threat of slowing economies and rising unemployment.

The ECB, for example, was expected to stay put on rates just two weeks ago, but markets are now wondering whether the bank may need to tighten further to avoid “making the same mistake” as during the energy crisis triggered by the invasion of Ukraine.

The BoE, meanwhile, had been expected to cut rates on confidence that inflation was heading toward the 2% target and that easing could support the economy. And the British economy clearly needs help: recent data showed that the UK economy didn’t grow at all in January. Unfortunately, the UK may not get that help just yet – the BoE will first have to deal with the renewed inflationary pressures before supporting growth.

The SNB is expected to keep rates unchanged; the strong franc could help counter the impact of rising oil prices on inflation and allow the SNB to stay on hold for a while. For the BoJ, rising energy prices and the notable depreciation of the yen will likely keep the bank on a path toward further normalization. The RBA, on the other hand, is expected to announce a 25bp hike on Tuesday to address inflation risks.

Overall, if we summarize in one sentence: central banks around the world are likely to deliver hawkish signals, and that could weigh on sentiment this week if Middle East tensions do not de-escalate.

Happily, for those who are craving for other things to talk about, the NVIDIA GTC taking place between today and Thursday could shift the spotlight back to AI, as Nvidia and Jensen Huang are expected to unveil the latest chip roadmap—announcements that often ripple through the broader tech sector and move semiconductor stocks. Let’s see if they can find space in the war-crowded headlines.

Central Banks Face the Heat from the Energy Shock

In focus today

Today, focus continues to be on tensions in the Middle East and its impact on energy markets. Trump stated on Friday that the US will be hitting Iran "very hard over the next week", which likely will continue to disrupt already volatile energy markets.

Norway will release its February trade balance. The data will largely be driven by energy exports, although the recent surges in oil prices will not be reflected in the numbers.

In Canada, February inflation data is released this afternoon, ahead of this week's monetary policy meeting, with headline inflation expected at 1.9% y/y (Jan: 2.3%). That would place inflation right around the Bank of Canada's 2% target, marking a 6-month low if realized.

Also in the afternoon, US industrial production data will be released for February.

Overnight, Australia kicks off a busy week of monetary policy meetings. The Reserve bank of Australia is expected to hike the interest rate by 25bp to 4.10% from 3.85%, which would mark the second consecutive hike in a row. Markets have priced in an 80% probability for the hike.

For the rest of the week, we have interest rate decisions by Canada and the Fed on Wednesday followed up with decisions from Japan, Sweden, Switzerland, England, and the ECB on Thursday.

Economic and market news

What happened overnight

China released the monthly batch of data today covering both January and February (the two months released together due to Chinese New Year). The data were overall a bit better than expected with retail sales for the two months rising 2.8% y/y (cons: 2.5%, prev.: 0.9%). Housing data were also moderately positive as home prices declined less than in previous months. New home prices declined 0.43% m/m in February vs 0.54% m/m in January, the smallest decline since April last year. This is the most positive part of the report as a stabilisation in the housing market is key for lifting consumption as well. Industrial production for January and February increased 6.3% y/y (cons: 5.3%, prev.: 5.2%). As usual China comes stronger out of the gates in a new year, which may ease some growth concerns. However, we have tended to see growth decline again later in the year. Overall, the data is still in line with our scenario of continued muddling through and in line with the government's growth target of 4½-5%.

In geopolitics and Nato, Trump warned Nato late on Sunday, stating it faces a "very bad" outlook if US allies in Europe fail to assist in opening the Strait of Hormuz. He emphasised that European nations, which rely heavily on Gulf oil, have a responsibility to ensure the security of the crucial waterway.

What happened over the weekend

The US-Israeli conflict with Iran has now entered its third week with tensions continuing. On Saturday, US forces struck Kharg Island, which handles ~90% of Iran's oil exports, destroying key military infrastructure. President Trump warned that Iran's energy infrastructure on the island could also be targeted if Tehran continues to interfere with shipping in the Strait of Hormuz, a move that would likely intensify the conflict and tighten global oil supplies further. The potential for a ceasefire, however, remains slim as positions appear to have hardened as the conflict has dragged on. Gulf states are reportedly pushing both sides to return to negotiations, but so far without success. While some Iranian political figures (most recently FM Araghchi) have signalled openness to talks, the ultimate decisions rest with the supreme leadership and the IRGC, so these signals should be treated cautiously. The new supreme leader was wounded earlier last week according to US secretary of war Pete Hegseth, but his current condition remains unclear.

The oil price is on the rise again. It opened close to USD107/bbl after another weekend of escalation in the war in Iran. The oil market is likely concerned about the US attacks on Kharg Island and Iran's attacks on Fujairah in the United Arab Emirates - both important key points for the oil market. If oil installations are hit, it risks affecting oil supplies from the region, keeping prices high even after a reopening of the Strait of Hormuz.

In the US, the Fed's preferred measure of inflation, the PCE, landed at 0.4% m/m for January (cons: 0.4%) and was close to expectations in both headline and core terms. However, Q4 GDP was revised quite notably lower to 0.7% q/q AR from the already below-expectations flash print of 1.4%. The revision comes particularly from weaker services consumption, and slightly weaker investments into structures and software intangibles. Contribution from net exports was also revised from mildly positive to negative, as the trade deficit re-widened towards the end of last year.

The University of Michigan's consumer sentiment preliminary March survey showed that the 1-year inflation outlook was 3.4%, unchanged from the final February reading. This is the first consumer inflation expectation measure partially overlapping with the Iran war period. However, the survey period included only the first week of the war, and US gasoline prices had not yet picked up.

The delayed U.S. JOLTs report for January revealed 6.946m job openings, surpassing expectations of 6.700m (Dec: 6.55m). The solid labour market performance provides the Fed with room to monitor developments in the ongoing Iran conflict without immediate pressure to adjust policy rates.

Trade delegations from US and China met for a new round of trade talks yesterday with talks continuing today, preparing for some kind of deal at the Xi-Trump summit in Beijing at the end of this month. With the US focused on the ongoing conflict with Iran, Trump suggested on Sunday he might delay this month's Beijing summit if China does not help unblock the Strait of Hormuz, leaving little prospect for a breakthrough.

In Norway the Technical Calculation Committee revised its price forecast for 2026 to 3.2% (prev: 3.0%), an important assumption ahead of this year's central wage negotiations (starting 23 March) as it could affect nominal wage claims. In Norges Bank's latest expectation survey, labour unions on average expected real wage growth at 1.2% in 2026. If so, nominal wage growth will end at 4.4%.

In the UK, January GDP growth was below expectations and stalled at 0.0% m/m (cons: 0.2% m/m, Dec: 0.1% m/m). While services growth was flat at 0.0% m/m (Dec: 0.2%), production declined 0.1% m/m (Dec: -0.9%). On a year-on-year basis, GDP expanded by 0.8% y/y, slightly higher than December figures of 0.7% y/y.

In Sweden, unemployment came in as expected at 8.4% after the big drop to 8.0% in January according to the Labour Force Survey. The increase in the unemployment rate was due to higher activity rate. Employment increased by 0.3% m/m, better than expected and encouraging given the weaker January GDP.

In China, credit and money data for February was released stronger than expected with Aggregate Financing YTD at CNY 9600bn (cons: 9245bn). M1 growth was up 5.9% y/y (prev: 4.9%), while M2 growth was flat at 9.0% y/y. It points to a moderate rebound after credit growth has been slowing during 2025.

Equities: Global equities traded on a weak footing towards the back end of the week. While the oil price surge on Monday took all the headlines, the theme towards the end of the week was more concerning of 'stagflationary'ish' dynamics. The sell-off has now resulted in a general decline across equity sectors, with only the energy sector posting positive return since the Iran war started. On Friday the S&P500 was -0.6%, Nasdaq -0.9%, Russell2000 -0.4% and Stoxx600 -0.5%. US futures are up this morning by about 0.4%, while Asian indices are somewhat down.

FI and FX: The war in the Middle East continues to impact markets, with rising yields and heightened inflation expectations. This week is packed with central bank meetings, (in order: the RBA, BoC, FOMC, BoJ, Riksbank, SNB, BoE and ECB), where markets will focus on how the central banks assess the impact of higher oil prices. In general, we expect a "wait and see" mode while signalling readiness to address inflation risks. Oil prices opened at close to USD107/bbl after another weekend of escalation in the war in Iran. The oil market is likely concerned about the US attacks on Kharg Island and Iran's attacks on Fujairah in Iran - both key points for the oil market. Energy supply uncertainty could well prolong even further, and as long as it lasts, we see risks skewed towards EUR/USD declining even lower.

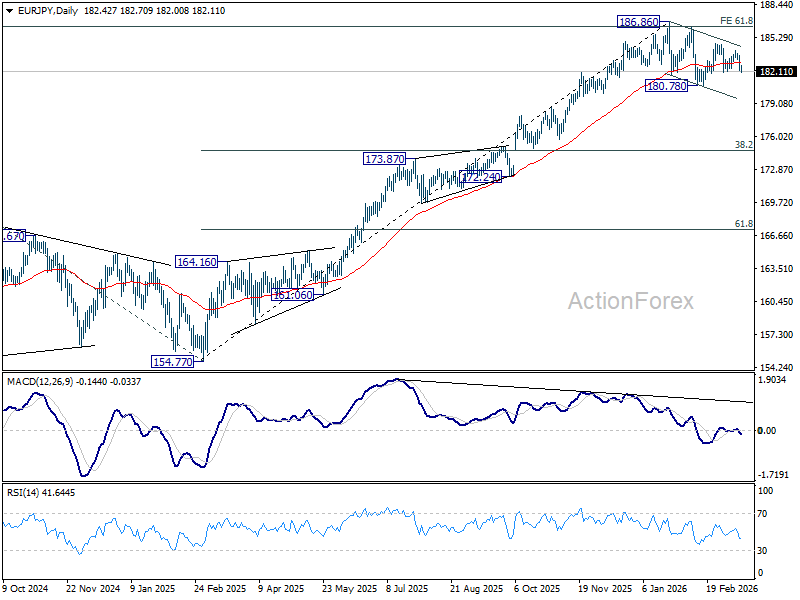

EUR/JPY Daily Outlook

Daily Pivots: (S1) 181.85; (P) 182.75; (R1) 183.26; More...

Immediate focus is now on 182.00 support in EUR/JPY with today's decline. Firm break there will resume the fall from 184.75 to retest 180.78 low. Decisive break there will indicate that fall from 186.86 is already correcting whole up rise from 154.77, and solidify the near term bearish outlook. On the upside, above 184.75 will resume the rebound from 180.78 to retest 186.86 high.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.29) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

Markets Cautious as Hormuz Escort Plan Runs Into Resistance

Markets stayed cautious today as hopes for a multinational naval coalition to escort tankers through the Strait of Hormuz ran into early resistance from key governments. While the proposal briefly raised expectations that the disruption to Middle East energy flows might be contained, several countries have so far stopped short of committing naval assets, leaving traders waiting for clearer signals before taking large positions.

Oil prices remain elevated as a result. With the lack of progress on securing shipping routes, energy markets continue to price in the risk that crude flows through the Strait could face sustained disruption. At the same time, prices have not exploded higher because investors still believe some form of protection for tanker traffic could eventually emerge.

That balance between risk and hope has produced a relatively calm tone across broader markets. Currency trading has been subdued, with most major pairs holding within Friday’s ranges. Investors appear reluctant to commit ahead of both geopolitical developments and a packed week of central bank meetings.

The proposed escort mission first gained traction after US President Donald Trump publicly urged several nations to contribute naval forces to protect commercial shipping. Countries mentioned included Japan, South Korea, Britain, France and China. The idea was that a coordinated patrol effort could shift the situation from fears of a complete supply cutoff toward a scenario of “managed disruption.”

However, the diplomatic response has been cautious at best. Australia directly rejected participation, with Transport Minister Catherine King stating that Canberra would not be sending a naval vessel and that the country had not been asked to contribute in that capacity.

European responses have been similarly restrained. British Prime Minister Keir Starmer has adopted a “wait and see” approach while coordinating discussions with Canadian Prime Minister Mark Carney, and Germany’s foreign minister Johann Wadephul openly expressed skepticism about the proposal, saying Berlin does not intend to become an active participant in the conflict.

France has taken a more conditional stance, noting that it has previously examined the possibility of an international mission to escort vessels through the strait but stressing that such an operation would only be considered when circumstances permit and once the intensity of fighting subsides.

In Asia, Japanese Prime Minister Sanae Takaichi also indicated that Tokyo has made no decision on dispatching escort vessels. She told the Upper House that Japan is still studying what actions might be possible within the country’s legal framework and what could be done independently.

Equity markets in the region showed mixed reactions. Hong Kong’s Hang Seng Index managed to edge higher, supported by stronger-than-expected Chinese economic data showing improved industrial production, retail sales and investment. Still, gains remained limited amid continued uncertainty about the global outlook.

China’s property sector remains the elephant in the room. The ongoing real estate slump continues to weigh on investor confidence, and the country also faces a unique vulnerability to any Hormuz disruption as roughly half of its seaborne crude imports originate from the region. Even if Chinese vessels receive assurances of safe passage, higher global shipping costs could still squeeze manufacturing margins.

In currency markets, the Japanese Yen strengthened slightly following renewed intervention warnings from Tokyo. Finance Minister Satsuki Katayama told Parliament the government is maintaining “maximum vigilance” and stands ready to take “decisive steps” against excessive volatility. The 160 level in USD/JPY is now seen by some as the "red line" that could trigger official action.

Elsewhere, currencies remain largely range-bound as traders look ahead to one of the busiest weeks of monetary policy decisions this year. Meetings from the RBA, BoC, Fed, BoJ, BoE, SNB and ECB are scheduled, keeping investors cautious as they wait for both geopolitical and policy clarity.

In Asia, Nikkei fell -0.09%. Hong Kong HSI is up 1.44%. China Shanghai SSE is down -0.37%. Singapore Strait Times is up 0.26%. Japan 10-year JGB yield rose 0.029 to 2.274.

Gold breaks 5,000 as “Safe Haven Paradox” returns, 4,815 now key

Gold came under pressure earlier in the day, slipping below the 5,000 psychological level in what could be described as a “safe haven paradox,” where Dollar strength is overpowering traditional war-driven demand for bullion. Technically, the break of key support suggests downside risk toward 4,815.

China industrial production, retail sales, investment beat expectations in Jan–Feb

China’s economic activity showed a stronger-than-expected start to 2026, with industrial production, retail sales and fixed-asset investment all beating forecasts. However, the property sector remains a key drag on the broader recovery.

New Zealand BNZ services falls back Into contraction, weak demand hits

New Zealand’s services sector slipped back into contraction in February, with the BusinessNZ Performance of Services Index dropping to 48.0. Weak demand, high living costs and elevated interest rates continue to weigh on activity.

Seven central banks, one energy shock: Critical monetary policy week

The coming week marks one of the most consequential policy periods of 2026, with seven major central banks—including the Fed, RBA, BoJ, BoE and ECB—meeting within days of each other. The decisions come as surging oil prices from Middle East tensions reshape the global inflation outlook, forcing markets to reassess expectations for rate cuts and the broader direction of monetary policy.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 181.85; (P) 182.75; (R1) 183.26; More...

Immediate focus is now on 182.00 support in EUR/JPY with today's decline. Firm break there will resume the fall from 184.75 to retest 180.78 low. Decisive break there will indicate that fall from 186.86 is already correcting whole up rise from 154.77, and solidify the near term bearish outlook. On the upside, above 184.75 will resume the rebound from 180.78 to retest 186.86 high.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.29) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

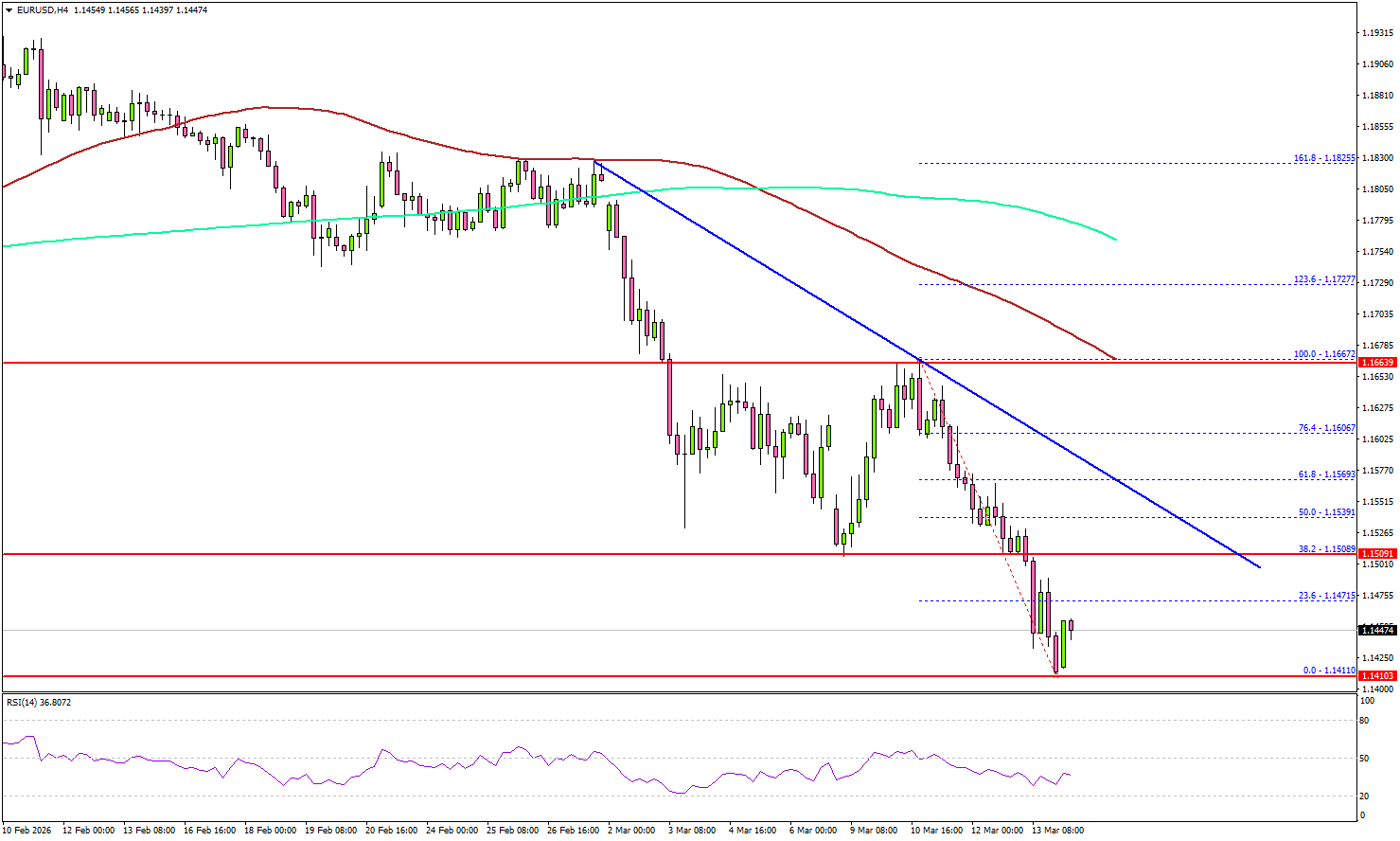

EUR/USD Extends Decline — Bears Target Fresh Lows

Key Highlights

- EUR/USD extended losses and traded below 1.1480.

- A key bearish trend line is forming with resistance at 1.1550 on the 4-hour chart.

- GBP/USD also declined further and traded below 1.3320.

- Crude oil prices could continue to rise and might test $112.

EUR/USD Technical Analysis

The Euro failed to stay above 1.1550 against the US Dollar. EUR/USD declined further and traded below 1.1500 to enter a bearish zone.

Looking at the 4-hour chart, the pair settled well below 1.1500, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). There is also a key bearish trend line forming with resistance at 1.1550.

The pair traded as low as 1.1411 and is currently consolidating losses. On the upside, the pair is now facing sellers near 1.1470. The first major resistance sits at 1.1500. A close above 1.1500 could open the doors for gains above 1.1520.

In the stated case, the bulls could aim for a move to 1.1550 and the trend line. Any more gain might open the doors for a test of 1.1660 and the 100 simple moving average (red, 4-hour).

If there is no recovery wave, the pair might start a fresh decline. Immediate support is seen near 1.1420. The first key support sits at 1.1400. A close below 1.1400 might call for heavy losses. In the stated case, it could even revisit 1.1320 in the coming days.

Looking at Crude oil, the bulls seem to be active above $95.00, and they could soon aim for a fresh wave above $105 and $112.

Upcoming Key Economic Events:

- US Industrial Production for Feb 2026 (MoM) – Forecast 0.2%, versus 0.7% previous.