Sample Category Title

Markets Stabilize as Oil Falls Below $100, Yen Rallies in Crosses on Intervention Threats

Market sentiment showed tentative signs of stabilization today as Brent crude slipped back below the psychological $100 per barrel level. The modest pullback in energy prices helped European equities recover from earlier losses while U.S. futures also moved back into positive territory.

However, the shift appears to reflect stabilization rather than a genuine improvement in risk appetite. The underlying geopolitical backdrop remains tense, with no clear end in sight for the Iran war, leaving markets reluctant to fully embrace risk.

Comments from U.S. President Donald Trump reinforced that uncertainty. In a social media post, Trump said the US has “unparalleled firepower, unlimited ammunition, and plenty of time.” Rather than calming markets, the message was interpreted by some investors as a signal that the conflict could drag on for an extended period.

Against this uncertain backdrop, Yen has emerged as the strongest performer in currency markets today. Yet the rally is being driven by a complex set of forces rather than a straightforward safe-haven move. One key factor supporting the yen is rising intervention risk as USD/JPY approaches the psychologically important 160 level, widely seen by markets as a potential line in the sand for Japanese authorities.

Japan’s Finance Minister Satsuki Katayama said today that the government is in “closer contact with U.S. authorities,” while also highlighting the impact of rising crude oil prices on household finances. Such language is typically interpreted as Tokyo seeking tacit approval from Washington for currency intervention.

At the same time, speculation is growing that the Bank of Japan could accelerate its policy normalization path. According to a Reuters report citing sources familiar with the central bank’s thinking, the inflationary impact of Middle East supply shocks may increase the likelihood of another rate hike as soon as April.

Despite Yen’s strength, Dollar is also attracting strong demand. Risk aversion tied to the ongoing Middle East conflict is supporting safe-haven flows into U.S. assets, while fading expectations for Fed rate cuts are further underpinning the greenback.

These opposing forces have effectively trapped USD/JPY in a narrow range. Intervention fears prevent the pair from moving significantly higher, while Dollar strength keeps it from falling decisively. As a result, traders are expressing Yen demand through cross instead. The market is actively selling currencies such as Euro and Pound against Yen, creating a steep decline in Yen crosses even while USD/JPY remains largely unchanged.

Sterling is particularly under pressure following disappointing UK economic data released earlier today. January GDP showed no growth on the month, missing expectations for a 0.2% expansion and reinforcing concerns that the UK economy entered 2026 with limited momentum. For the BoE, with oil prices elevated due to the Iran conflict, the risk of a stagflation scenario—sluggish growth combined with rising energy-driven inflation—has become a central concern for policymakers.

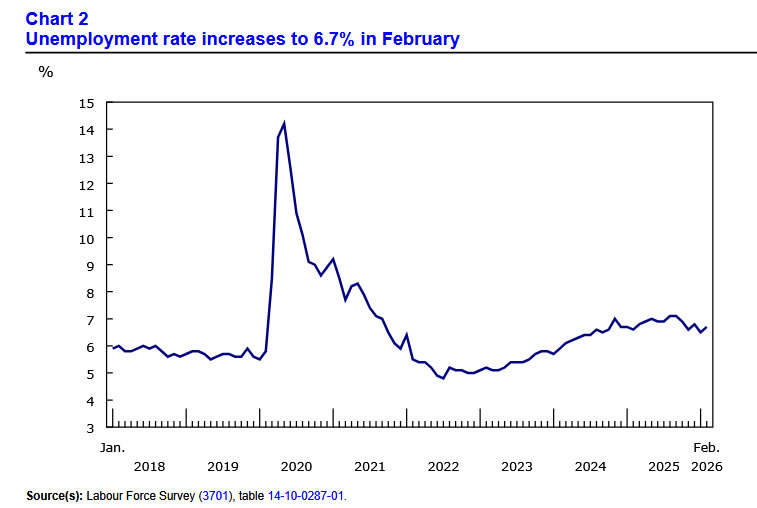

Loonie is also underperforming after a sharply weaker labor market report. Employment plunged by -83.9k in February, far worse than expectations for a modest increase, while the unemployment rate rose to 6.7%. The sudden deterioration in employment conditions raises questions about the underlying strength of the Canadian economy. The BoC is widely expected to remain on hold next week, but today’s data increases the risk that policymakers may eventually need to consider additional support if labor market weakness persists.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.20%. CAC is up 0.02%. UK 10-year yield is up 0.003 at 4.716. Germany 10-year yield is down -0.010 at 2.951. Earlier in Asia, Nikkei fell -1.16%. Hong Kong HSI fell -0.98%. China Shanghai SSE fell -0.82%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield rose 0.057 to 2.245.

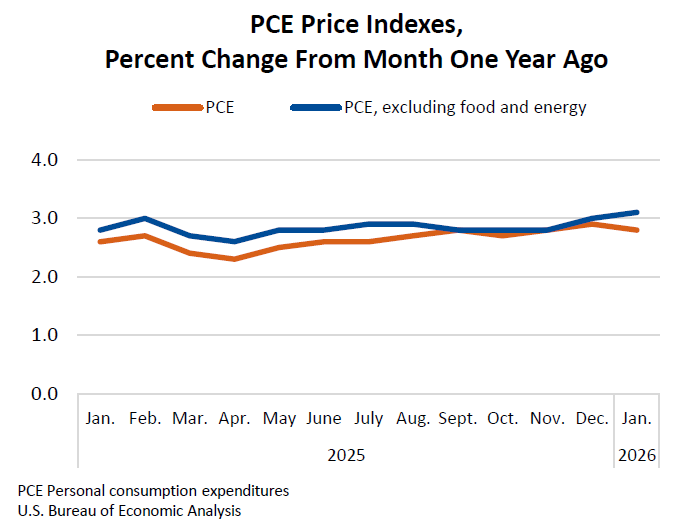

US core PCE rises 0.4% mom in January as consumer spending stays strong

US inflation data for January presented a mixed picture, with price pressures remaining firm even as the headline annual pace eased slightly. The headline PCE price index rose 0.3%om, while the core measure—which excludes food and energy—increased by 0.4% min. Both readings matched market expectations and indicate that underlying inflation remains somewhat sticky.

On an annual basis, headline PCE inflation slowed modestly from 2.9% to 2.8%, coming in slightly below forecasts. However, core inflation edged higher from 3.0% to 3.1% year-on-year, highlighting persistent price pressures in the broader economy and reinforcing the view that the disinflation process remains uneven.

Consumer demand remained resilient during the month. Personal spending increased by USD 81.1B, or 0.4% mom, exceeding expectations of 0.3% mom. Meanwhile, personal income rose by USD 113.8B, also translating into a 0.4% monthly gain but falling slightly short of 0.5% mom forecasts.

Canada jobs plunge -83.9k in February as unemployment rate climbs to 6.7%

Canada’s labor market suffered a sharp setback in February, with employment plunging by -83.9k, far worse than expectations for a modest gain of around 10k. The decline marks a significant deterioration in labor conditions.

The drop in employment was broad-based across sectors. Services-producing industries shed around -56k jobs, while goods-producing sectors lost roughly -28k positions. The deterioration pushed the unemployment rate higher to 6.7% from 6.5%, while the participation rate edged down slightly to 64.9%.

Despite the sharp decline in employment, wage growth accelerated noticeably. Average hourly wages rose 3.9% yoy in February, up from 3.3% in January.

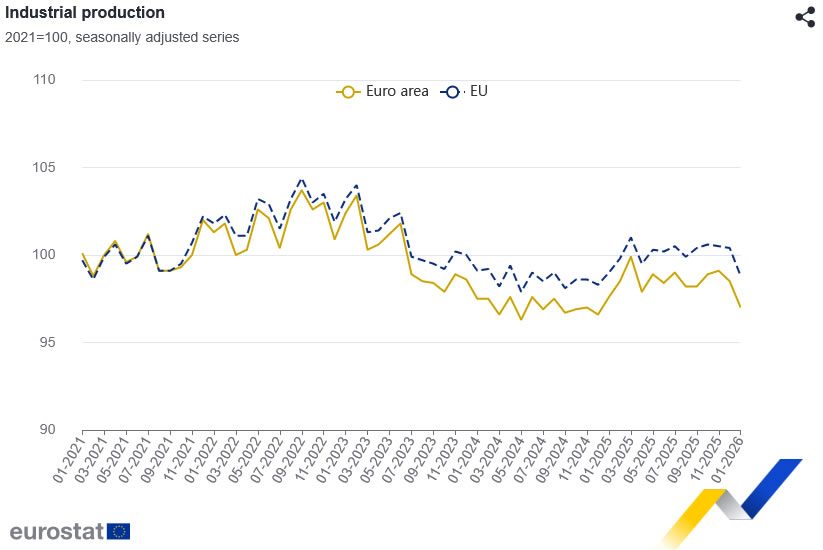

Eurozone industrial production drops -1.5% mom as manufacturing weakness deepens

Eurozone industrial production fell sharply in January, highlighting renewed weakness in the region’s manufacturing sector. Output declined by -1.5% month-on-month, well below expectations for a 0.7% increase, suggesting that industrial momentum at the start of 2026 was significantly weaker than anticipated.

The decline was broad-based across most categories. Production of intermediate goods dropped by -1.9%, while capital goods output fell by -2.3%. Durable consumer goods production also declined by -1.9%, and non-durable consumer goods saw the steepest fall with a -6.0% drop. Energy output was the only bright spot, rising by 4.7% during the month and partially cushioning the overall decline.

Across the broader European Union, industrial production fell by -1.6% month-on-month. Ireland recorded the largest contraction with a -9.8% drop, followed by Luxembourg (-4.3%) and Sweden (-4.1%). In contrast, a few smaller economies posted gains, with Portugal leading the increases at +4.2%, followed by Latvia (+3.3%) and Lithuania (+2.7%).

UK GDP flat in January as services stall, production contracts

UK economic growth stalled at the start of the year, with GDP showing no expansion in January, falling short of expectations for a modest 0.2% mom rise. Sector data showed a mixed picture beneath the headline reading. Services output, which accounts for the largest share of the UK economy, was flat during the month. Production declined slightly by -0.1%

Construction posted 0.2% mom growth, but the sector remains under sustained pressure following a prolonged period of contraction driven by high borrowing costs and subdued investment.

Looking at the broader trend, the UK economy still managed a modest expansion of 0.2% in the three months to January, an improvement from the 0.1% growth recorded in the three months to December. Services output rose by 0.2% over the period, while production delivered stronger growth of 1.3%. However, construction was a significant drag, contracting by -2.0% over the same period.

New Zealand BNZ manufacturing holds firm at 55 in February

New Zealand’s manufacturing sector continued to expand in February, with BusinessNZ Performance of Manufacturing Index edging slightly lower from 55.1 to 55.0. While the headline reading dipped marginally, the index remains comfortably above the 50 breakeven level, signaling ongoing growth in the sector.

Underlying components showed mixed but generally positive trends. Production rose modestly from 56.5 to 56.7, while new orders strengthened from 56.6 to 57.6, indicating improving demand conditions. Employment, on the other hand, fell notably from 52.6 to 50.4.

Survey responses pointed to improving business sentiment, with the share of positive comments rising to 55.5% in February from 47.7% in January. Manufacturers reported stronger orders, enquiries, and sales, helped by firmer export demand and improving conditions across certain sectors.

BNZ Senior Economist Doug Steel noted that while geopolitical tensions in the Middle East are dominating market attention, February’s PMI reading provides a solid starting point for the manufacturing sector heading into an uncertain global environment.

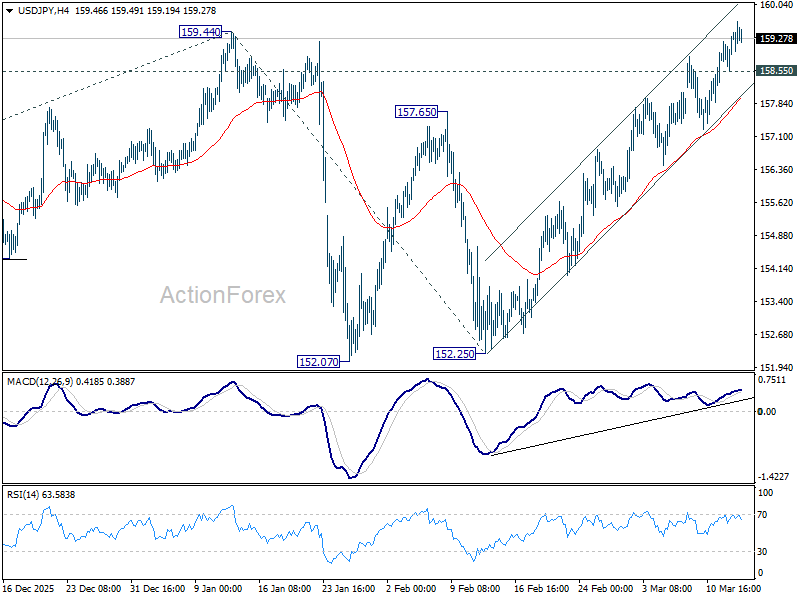

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.81; (P) 159.12; (R1) 159.67; More...

Intraday bias in USD/JPY remains on the upside at this point. rise from 139.87 is resuming and should target a retest on 161.94 high. Firm break there will confirm larger up trend resumption. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. On the downside, below 158.55 minor support will turn intraday bias neutral first.

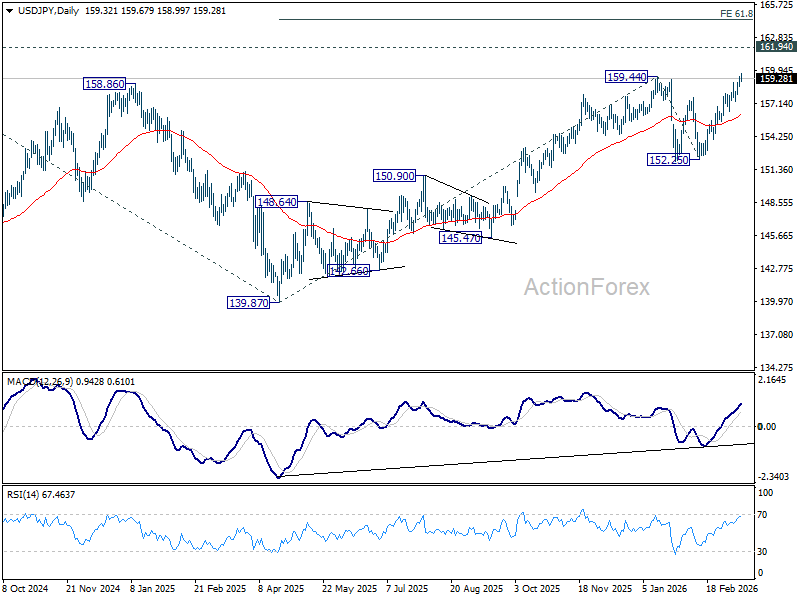

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

US core PCE rises 0.4% mom in January as consumer spending stays strong

US inflation data for January presented a mixed picture, with price pressures remaining firm even as the headline annual pace eased slightly. The headline PCE price index rose 0.3%om, while the core measure—which excludes food and energy—increased by 0.4% min. Both readings matched market expectations and indicate that underlying inflation remains somewhat sticky.

On an annual basis, headline PCE inflation slowed modestly from 2.9% to 2.8%, coming in slightly below forecasts. However, core inflation edged higher from 3.0% to 3.1% year-on-year, highlighting persistent price pressures in the broader economy and reinforcing the view that the disinflation process remains uneven.

Consumer demand remained resilient during the month. Personal spending increased by USD 81.1B, or 0.4% mom, exceeding expectations of 0.3% mom. Meanwhile, personal income rose by USD 113.8B, also translating into a 0.4% monthly gain but falling slightly short of 0.5% mom forecasts.

Canada jobs plunge -83.9k in February as unemployment rate climbs to 6.7%

Canada’s labor market suffered a sharp setback in February, with employment plunging by -83.9k, far worse than expectations for a modest gain of around 10k. The decline marks a significant deterioration in labor conditions.

The drop in employment was broad-based across sectors. Services-producing industries shed around -56k jobs, while goods-producing sectors lost roughly -28k positions. The deterioration pushed the unemployment rate higher to 6.7% from 6.5%, while the participation rate edged down slightly to 64.9%.

Despite the sharp decline in employment, wage growth accelerated noticeably. Average hourly wages rose 3.9% yoy in February, up from 3.3% in January.

US Dollar Index (DXY) Rises Above the 100 Level

Today the US Dollar Index (DXY) climbed above the psychological 100 mark for the first time in 2026, supported by a tense fundamental backdrop, with the military conflict in the Middle East acting as the main driver.

- → Financial market participants are selling riskier assets (such as equities and emerging market currencies) and reallocating funds into the US dollar, which is traditionally viewed as a safe haven during periods of war.

- → Iran’s statements about potentially closing the Strait of Hormuz, along with strikes on fuel infrastructure, are driving oil prices higher and increasing global inflation risks.

- → The strength of the US economy is also supporting the dollar. Yesterday’s labour market data showed no increase in unemployment.

Technical Analysis of the DXY Chart

On the morning of 9 March, while analysing the US Dollar Index (DXY) chart, we:

- → updated the ascending channel (marked in blue), within which the index had set its yearly high at that time;

- → suggested that DXY price movements might begin to stabilise.

Between 9 and 12 March, the DXY chart showed a pullback followed by a renewed upward move, which remained within the range defined by last week’s levels:

- → support at 98.60;

- → resistance at 99.68.

However, the developments mentioned above allowed bulls to regain momentum and extend the rally within the blue channel. In other words, if the earlier fluctuations between these levels reflected a balance between supply and demand, then today, 13 March, buyers appear to be taking the initiative, showing a willingness to pay more for the US dollar.

At present, the market looks overbought, as:

- → the RSI indicator has moved above the 70 level;

- → the price is trading above the upper boundary of the channel that had contained it since late January.

In the short term, a modest pullback cannot be ruled out, although it is unlikely to significantly alter the current market picture.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

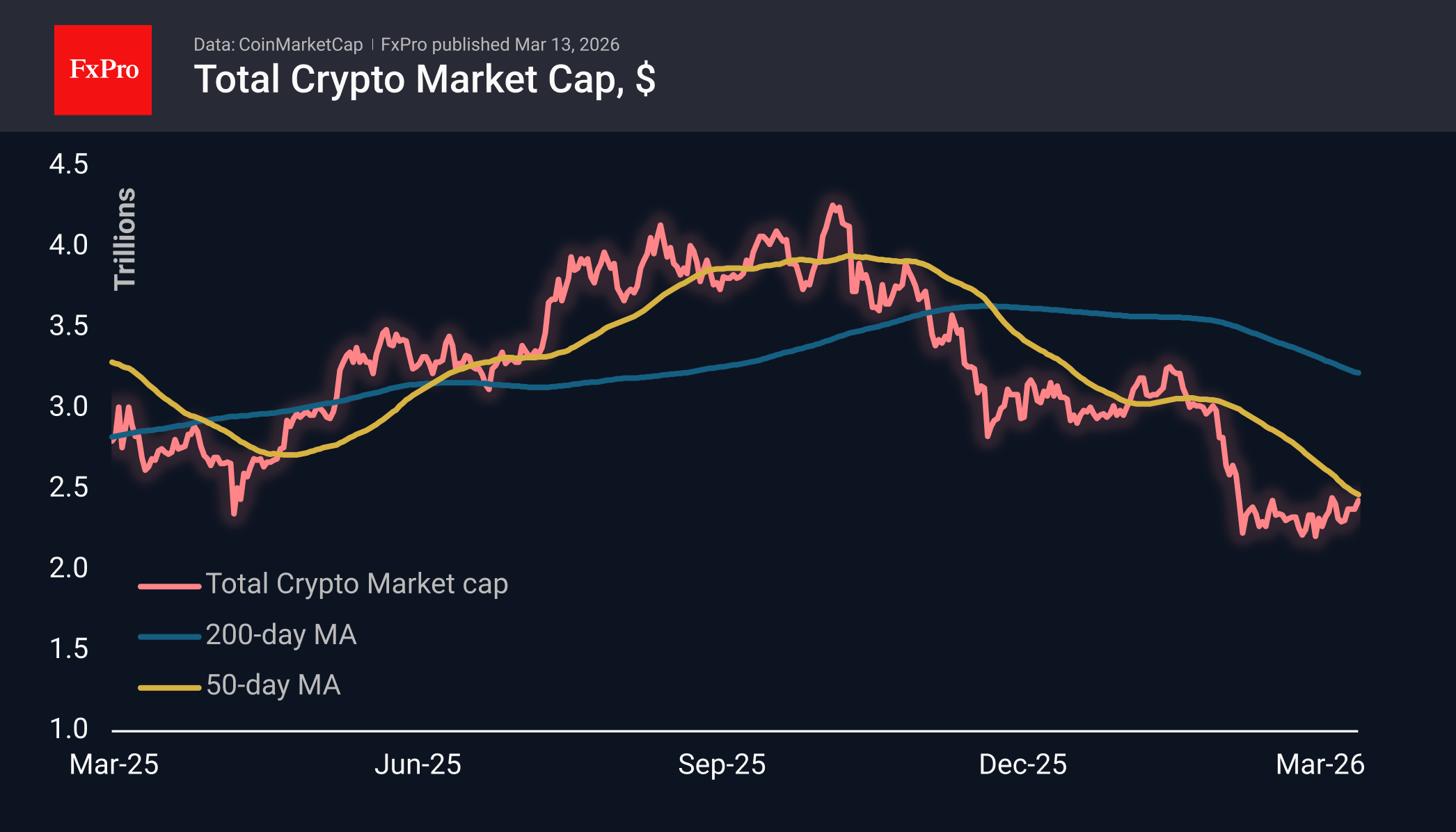

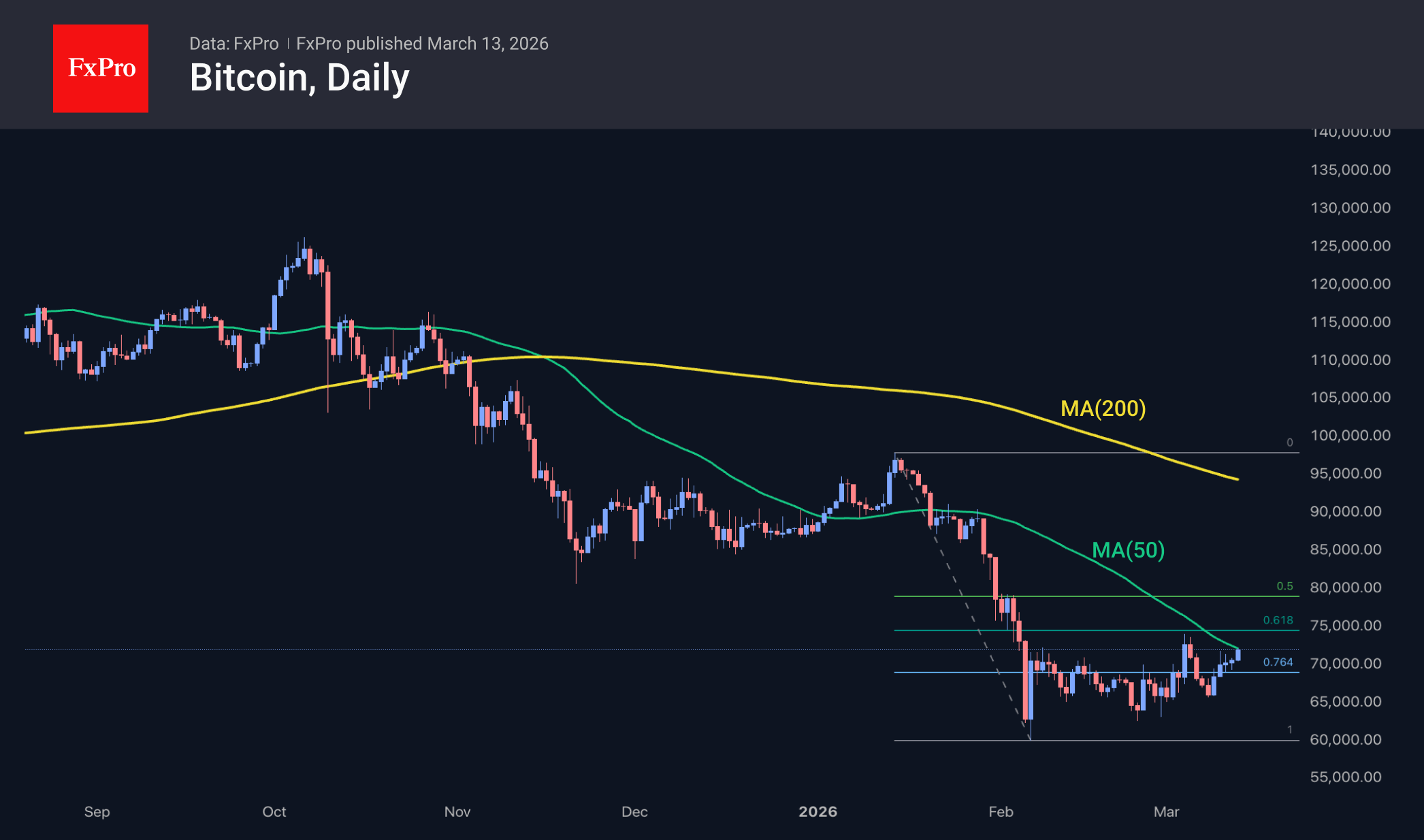

Bitcoin, Facing Headwinds, May Not Have Enough Strength

Market Overview

The crypto market cap has risen 2% over the past 24 hours, to $2.43T, close to the upper limit of last month’s range and slightly below last week’s mid-range. We continue to note the positive momentum in cryptocurrencies, in contrast to the pressure on the Nasdaq 100 and gold prices. However, we believe this divergence is short-term and will only continue until traditional markets begin to collapse. At the same time, the markets are now testing key technical support levels, forcing cryptocurrency traders to stay on guard.

Bitcoin has exceeded $71.5K, approaching its 50-day moving average. External factors are acting as a headwind, including rising oil and dollar prices, as well as the Nasdaq100 and S&P 500 indices falling to their 200-day lows. We doubt Bitcoin will have the strength to withstand the wind for long, and internal resistance may soon become a significant obstacle to growth.

News Background

Galaxy Digital CEO Mike Novogratz expects Bitcoin to trade between $60K and $80K this year. According to him, in recent weeks, it is not large hedge funds that have played a key role in the crypto market, but private investors, who are driving the main demand for the first cryptocurrency.

Options market participants are betting that Bitcoin will rise to $80K by the beginning of summer. According to Derive estimates, the probability of BTC rising above $80K by the end of June is 35%. However, there are also large bearish bets in the market.

Bloomberg Intelligence senior strategist Mike McGlone is confident that the bearish trend for Bitcoin is not over and again expects the price to fall to $10K, recommending using local rebounds to lock in profits.

Blockchain developer activity has declined by 75% over the year due to the outflow of specialists to the artificial intelligence industry, according to Artemis. The number of active developers has fallen by 56% to approximately 4,600 people.

Eurozone industrial production drops -1.5% mom as manufacturing weakness deepens

Eurozone industrial production fell sharply in January, highlighting renewed weakness in the region’s manufacturing sector. Output declined by -1.5% month-on-month, well below expectations for a 0.7% increase, suggesting that industrial momentum at the start of 2026 was significantly weaker than anticipated.

The decline was broad-based across most categories. Production of intermediate goods dropped by -1.9%, while capital goods output fell by -2.3%. Durable consumer goods production also declined by -1.9%, and non-durable consumer goods saw the steepest fall with a -6.0% drop. Energy output was the only bright spot, rising by 4.7% during the month and partially cushioning the overall decline.

Across the broader European Union, industrial production fell by -1.6% month-on-month. Ireland recorded the largest contraction with a -9.8% drop, followed by Luxembourg (-4.3%) and Sweden (-4.1%). In contrast, a few smaller economies posted gains, with Portugal leading the increases at +4.2%, followed by Latvia (+3.3%) and Lithuania (+2.7%).

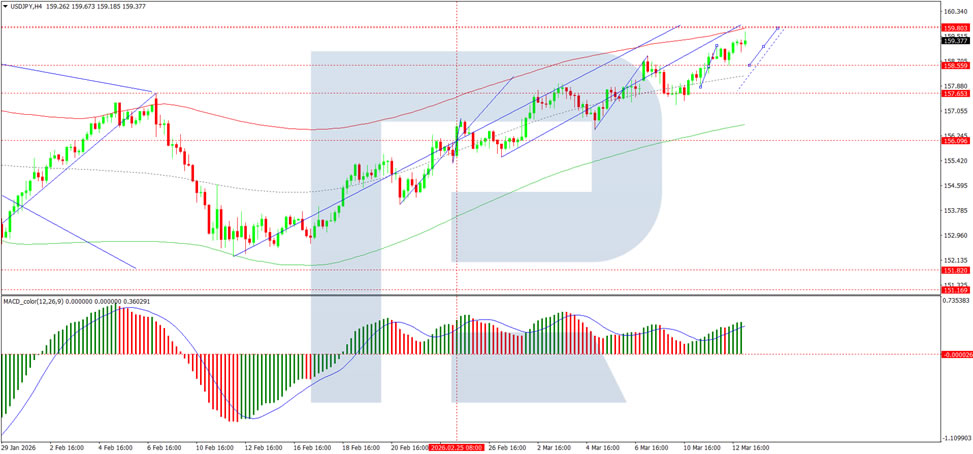

USD/JPY at Highest Since July 2024: Market Awaits BoJ Intervention

USD/JPY rose to 159.29 on Friday, marking one of the weakest levels for the Japanese yen since July 2024. The yen's decline is heightening market concerns about possible intervention by authorities in the foreign exchange market.

Bank of Japan Governor Kazuo Ueda warned that a weak yen could exacerbate imported inflation amid rising oil prices. According to him, this may accelerate the BoJ's transition towards normalising monetary policy.

Ueda also noted that exchange rate fluctuations are now having a more pronounced impact on inflation than in the past, increasing their significance for policy decisions.

Oil prices surged following a pledge by Iran's new Supreme Leader, Mojtaba Khamenei, to maintain the effective closure of the Strait of Hormuz. Tehran is intensifying attacks on oil and transport infrastructure across the region.

There is no sign of de-escalation in the Middle East conflict. Tough rhetoric from both Tehran and Washington indicates that the confrontation involving Iran remains far from resolution as it enters its second week.

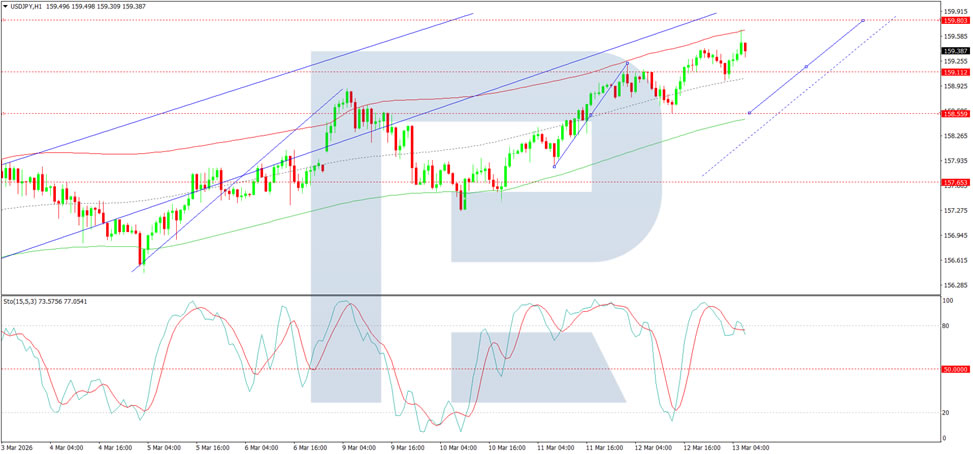

Technical Analysis

On the H4 USD/JPY chart, the market is forming a consolidation range around 159.12, currently extending to 159.60. A decline to test 159.20 from above is expected today, followed by a possible growth wave towards 159.88.

Technically, this scenario is confirmed by the MACD indicator, whose signal line is high above zero and pointing firmly upwards.

On the H1 chart, USD/JPY is forming a growth wave targeting 159.88, with a possible extension to 160.00. Thereafter, a downward correction is likely towards at least 158.55.

Technically, this scenario is supported by the Stochastic oscillator, whose signal line is above 80 and continuing to trend upwards.

Conclusion

USD/JPY has surged to multi-month highs amid a weakening yen, driven by rising oil prices and evolving expectations for BoJ policy. Governor Ueda's remarks suggest that currency weakness may accelerate the Bank's policy normalisation, though speculation over intervention continues to grow. With geopolitical tensions in the Middle East showing no signs of easing, and technical indicators pointing to further near-term upside, the pair appears poised to test the psychologically significant 160.00 level. However, verbal warnings from Japanese officials could amplify volatility.

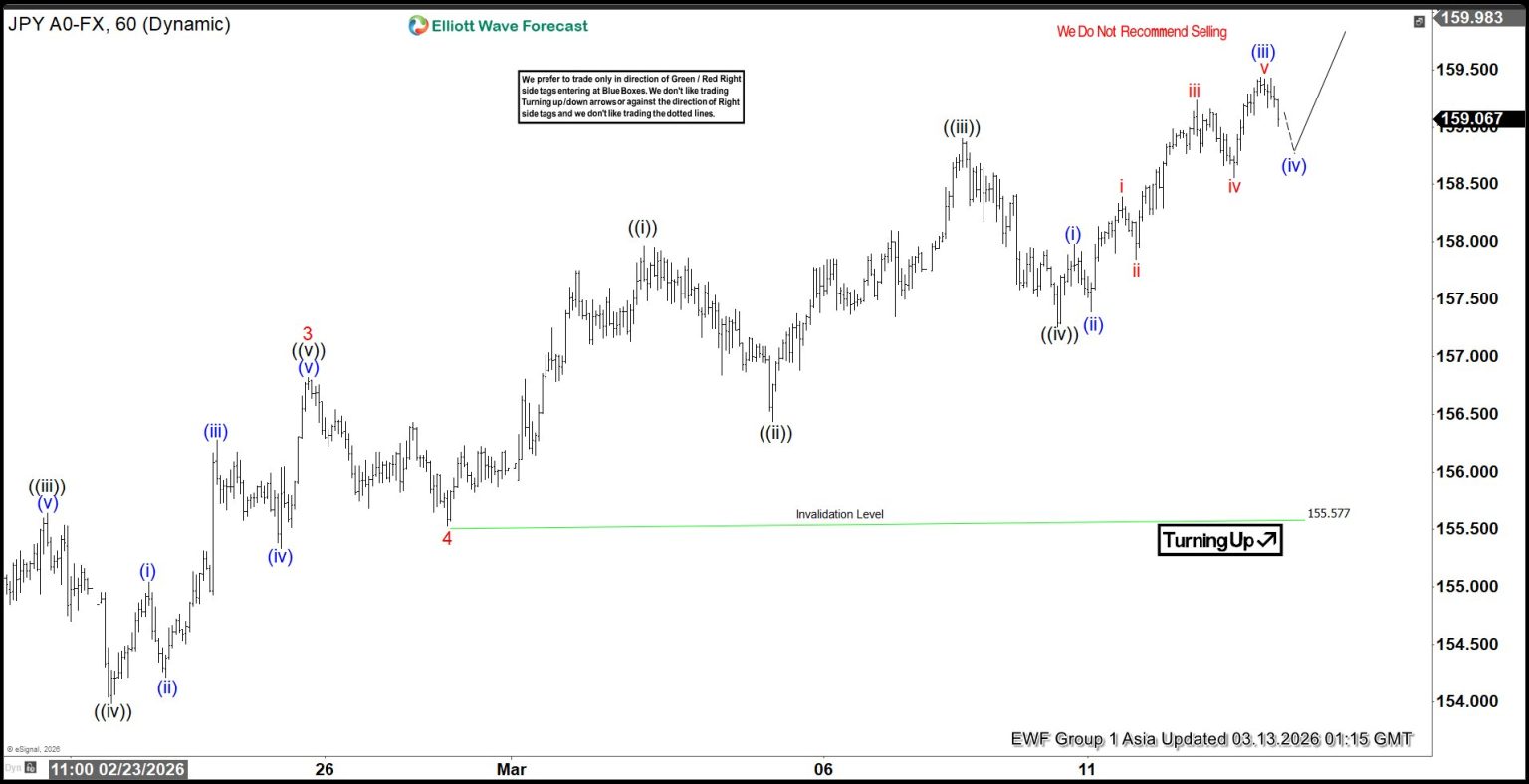

USDJPY Impulsive Advance: Elliott Wave Signals More Upside

The short-term Elliott Wave outlook for USDJPY indicates that the cycle from the January 28, 2026 low remains in progress, unfolding as an impulsive structure. From that low, wave (1) concluded at 157.72, followed by a corrective pullback in wave (2), which ended at 152.25. The market then advanced into wave (3), developing as an impulse of lesser degree. Within this sequence, wave 3 of (3) terminated at 156.82, as reflected in the one-hour chart. Subsequently, wave 4 of (3) completed at 155.57, setting the stage for the current advance in wave 5.

From the wave 4 low, wave ((i)) finished at 157.97, while the corrective wave ((ii)) ended at 156.44. The rally then resumed, with wave ((iii)) reaching 158.90 before another modest pullback in wave ((iv)) concluded at 157.26. The structure now points toward the completion of wave ((v)), which should finalize the broader wave 5 of (3) sequence. This progression highlights the sustained impulsive character of the rally, with each corrective phase finding support before resuming higher.

Near term, as long as the pivot at 155.57 remains intact, dips are expected to hold in either three or seven swings. This technical condition favors continued upside extension, reinforcing the view that the impulsive rally is not yet complete. Traders should monitor short-term corrections carefully, as they are likely to provide opportunities for participation in the ongoing bullish cycle. The overall structure suggests that USDJPY retains upward momentum, with the Elliott Wave framework offering a clear roadmap for the next stages of development.

USDJPY 60-Minute Elliott Wave Chart

USDJPY Elliott Wave Video:

https://www.youtube.com/watch?v=uadiJpnYZ5Q

Chart Alert: Dow Jones (DJIA) on the Brink of Major Bearish Breakdown Below 200-Day Moving Average at 46,330

Key takeaways

- Dow’s performance reversal amid geopolitical shock: The Dow Jones Industrial Average shifted from one of the best-performing US indices earlier in 2026 to one of the worst since the start of the US–Iran war 2026, falling 4.7% between 27 Feb and 12 Mar as global risk sentiment deteriorated.

- Financial sector exposure weighing on the index: Heavy weighting in financial stocks, particularly Goldman Sachs, has amplified downside pressure as rising oil prices increase stagflation risks and reduce expectations of interest rate cuts by the Federal Reserve.

- Yield curve dynamics signalling downside risk: A bear flattening of the US Treasury yield curve (10Y–2Y), driven by faster increases in short-term yields, is tightening financial conditions. Technically, the Dow is near key support at 46,330 (200-day moving average), where a breakdown could trigger deeper losses.

The Dow Jones Industrial Average (DJIA) has undergone a remarkable change of fortune since our last report published on 13 February 2026, “Chart alert: Dow Jones (DJIA) potential recovery at 20-day MA support, bulls need to break above 49,940”.

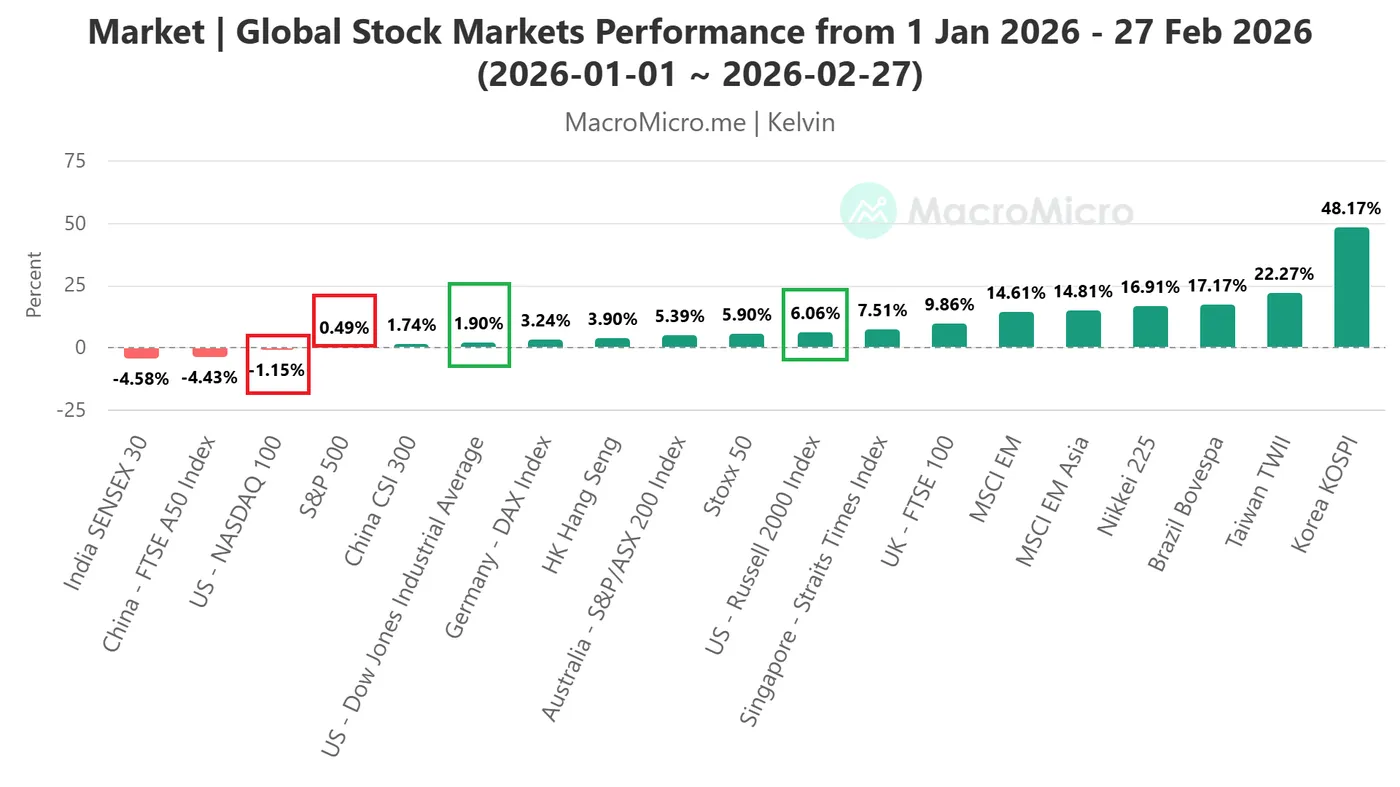

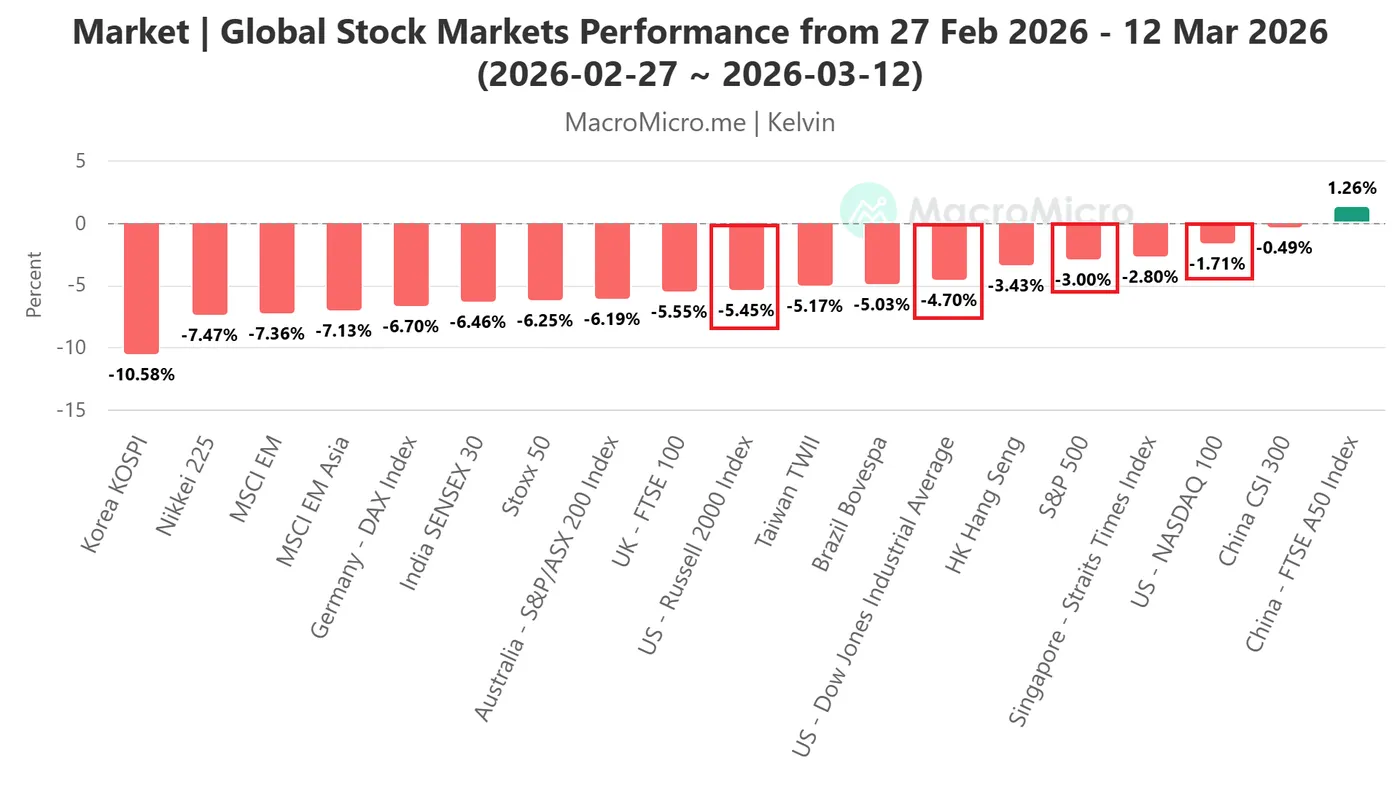

Dow Jones (DJIA) from outperformer to underperformer

Fig. 1: DJIA & major global stock indices performances from 1 Jan 2026 to 27 Feb 2026 (Source: MacroMicro)

Fig. 2: DJIA & major global stock indices performances from 27 Feb 2026 to 12 Mar 2026 (Source: MacroMicro)

Before the ongoing US-Iran war (entering its 14th day) that started on Saturday, 28 February 2026, the DJIA was the second-best US stock index (+1.9%), trailed behind the small-cap Russell 2000 (+6.1%), which came in top and outperformed the tech-heavy S&P 500 (+0.5%) and the Nasdaq 100 (-1.2%) from 1 January 2026 to 27 February 2026.

In a significant reversal, the DJIA is now the second-worst-performing US stock index (-4.7%), and the Russell 2000 is the worst (-5.5%), versus the S&P 500 (-3%), and the Nasdaq 100 (-1.7%) from 27 February 2026 to 12 March 2026 (see Fig. 1 & Fig. 2).

Why did the DJIA fare the worst in the current period?

Banking/financial stocks are the main trigger for such underperformance in the DJIA.

The Financials sector is the top sector in the DJIA with a weightage of around 27%, and Goldman Sachs is the top price-weighted component stock in the DJIA with a weight of 10.4% as of Thursday, 12 March 2026.

The recent swift jump in oil prices due to global oil supply disruption arising from the US-Iran war has increased the risk of a stagflation environment, in turn, reducing the odds of interest rate cuts by the US Federal Reserve in 2026.

Bear flattening in the US Treasury yield curve can trigger further downside in DJIA

Fig. 3: DJIA & US Treasury yield curve (10-YR minus 2-YR) major trends as of 13 Mar 2026 (Source: TradingView)

The US Treasury market has adjusted to rising stagflation risks and expectations of a less dovish Federal Reserve. Since 27 February 2026, the 2-year US Treasury yield has climbed by 37 basis points (bps), outpacing the 32 bps increase in the longer-term 10-year yield.

As a result, the US Treasury yield curve (10-year minus 2-year) has undergone a bear flattening, where short-term interest rates rise faster than long-term yields. Such a shift typically signals tighter financial conditions, which can weigh on economic growth and pressure bank profitability (see Fig. 3).

Let's examine the short-term trajectory of the US Wall Street 30 CFD index and its supporting elements.

Dow Jones (DJIA) – Oscillating within a steeper bearish trend, at risk of breaking below 46,330

Fig. 4: US Wall Street 30 CFD index minor trend as of 13 Mar 2026 (Source: TradingView)

Watch the 47,460 key short-term pivotal resistance on the US Wall Street 30 CFD index (a proxy of the Dow Jones Industrial Average futures), a break below the 46,330 key long-term support (also close to the 200-day moving average) damages the major uptrend phase of the DJIA in place since the October 2022 low (see Fig. 4).

Further potential weakness to expose the next intermediate supports at 45,780 and 45,485 in the first step.

On the other hand, a clearance and an hourly close above 47,460 negates the bearish tone for a squeeze up to retest the next intermediate resistance at 48,119 (also the pull-back of the former medium-term ascending channel support from 23 May 2025 low).

Key elements to support the bearish bias on Dow Jones (DJIA)

- The price actions of the US Wall Street 30 CFD index have started to evolve within a steeper minor descending channel in place since the 26 February 2026 minor swing high of 49.837.

- The hourly MACD trend indicator has just flashed out a bearish crossover condition below its centreline, which supports the ongoing downtrend phase of the US Wall Street 30 CFD index.

Dollar Grows Stronger Everyday

Markets

Core bonds continue to feel the heat as the Brent crude price cruises above the $100/b mark. Again despite all efforts to lower them. The latest initiative came from the US Treasury which said that it would allow countries to buy Russian oil stranded at sea. As long as the US and Iran continue trading jabs with the latter blocking the supply chain, oil prices won’t retreat. US President Trump this morning warned that the US has plenty of time in the war against Iran and added “watch what happens to these deranged scumbags today”. The German yield curve continued bear flattening with yields rising by up to 4 bps at the front end of the curve. The German 10-yr yield (+2.5 bps) closed at the second highest level (2.96%) since 2011 and is ready for a take at key 3% resistance. In the UK, bear flattening turned into a slight bear steepening as rising inflation expectations start impacting the long end of the curve in absence of monetary responses. UK yields rose by 8.8 bps (2-yr) to 9.6 bps (30-yr). For the first time, US Treasuries also faced significant selling pressure at the front end of the curve as US money markets start pricing out rate cut bets this year. The US yield curve bear flattened with yields rising by 0.3 bps (30-yr) to 9 bps (2-yr). From a technical point of view, the 2-yr yield broke the 3.6% resistance barrier which capped rangebound trading between September of last year now. That also coincided with a longer term downward trend line and the 200d moving average in a technically significant move. On FX markets, the dollar grows stronger everyday. The trade-weighted greenback moved beyond the YtD high at 99.70 and is has its sights at the November top at 100.40. EUR/USD loses the 1.15 barrier this morning with the August low at 1.1392 being the next target. A weaker euro is further complicating matters for the ECB and (upward) inflation risks when it meets next week. USD/JPY is back at January levels (just below 160) which prompted rate checks by the NY Fed and talk of potential coordinated interventions. This morning, the verbal treat only comes from the Japanese corner. Risk sentiment suffers from the lasting conflict with key European indices yesterday losing 0.5% to 1% and losses in the US exceeding 1.5%. We expect these underlying market dynamic – high oil prices, rising interest rates, stronger dollar, weaker equities – to remain in place going into a very uncertain weekend. Today’s eco calendar contains (outdated) January PCE deflators in which goods inflation is the one the watch. The University of Michigan’s March consumer survey could be the more important one from a market point of view. Interviews are conducted through the Monday before the release implying that inflation expectations will be impacted by the (start of) the conflict in the Middle-East and could further dent bond sentiment. US durable goods orders (January) and JOLTS job openings (January) are also in today’s data mix but will play second fiddle.

News & Views

Rating agency S&P warned that a sustained rise in energy prices could result in a lower Hungarian credit rating. With Hungary holding BBB- with a negative outlook (confirmed in October), such a downgrade would mean the country loses its investment grade status. S&P’s head analyst for the EMEA region said that if gas prices would develop similarly to 2022, Hungary’s current account could deteriorate significantly, inflation would rise and the forint could dramatically depreciate, pressuring “their fiscal indicators and their rating”. S&P said that the risk of a downgrade is compounded by pre-election fiscal stimulus measures which - unlike those in 2022 - are expected to have a longer-lasting fiscal impact. Hungary’s budget deficit at the end of February reached HUF2.1tn, which was already 40% of the full year target of 5%. The next S&P rating review is on May 29.

Fed vice-chair for supervision Michelle Bowman announced yesterday that US banks will get relaxed capital proposals from regulators in the coming week. While adopting the final package of Basel III rules would result in a small increase in capital requirement, Bowman said that the other proposed changes to surcharge for global systemically important banks would more than offset that. “These changes to the capital framework eliminate overlapping requirements, right-size calibrations to match actual risk and comprehensively address longstanding gaps in our prudential framework,” Bowman explained. The reform package is designed to encourage bank lending and to reverse the trend of mortgage activity increasingly being done by non-banks.