Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.81; (P) 159.12; (R1) 159.67; More...

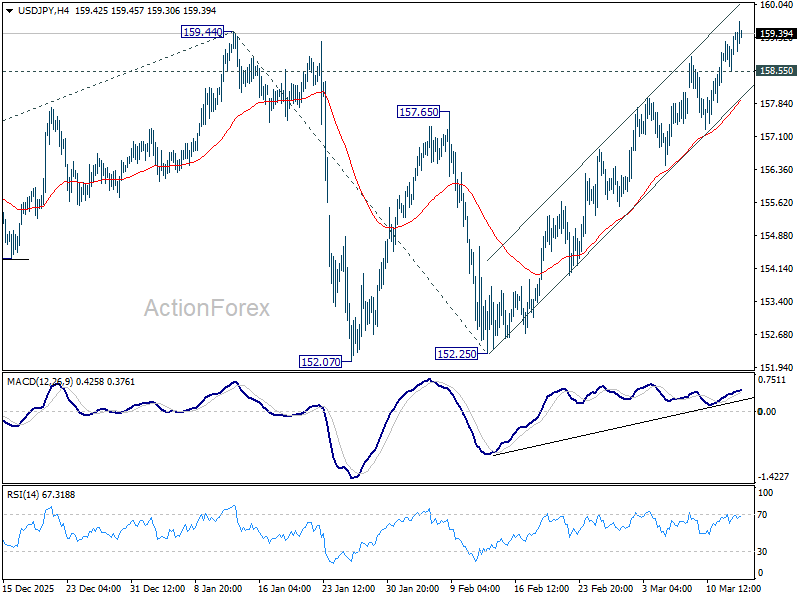

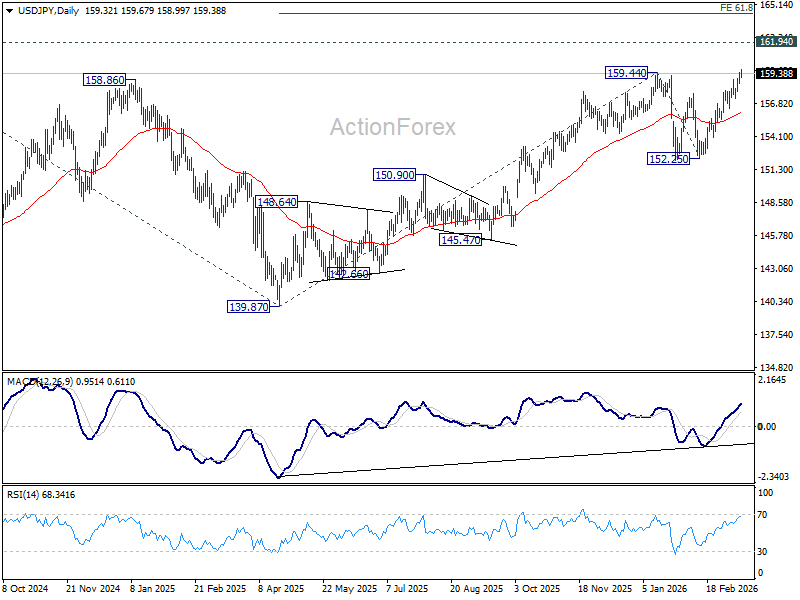

USD/JPY's break of 159.44 resistance suggests that whole rally from 139.87 is resuming. Intraday bias stays on the upside for retesting 161.94 high. Firm break there will confirm larger up trend resumption. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. On the downside, below 158.55 minor support will turn intraday bias neutral first.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

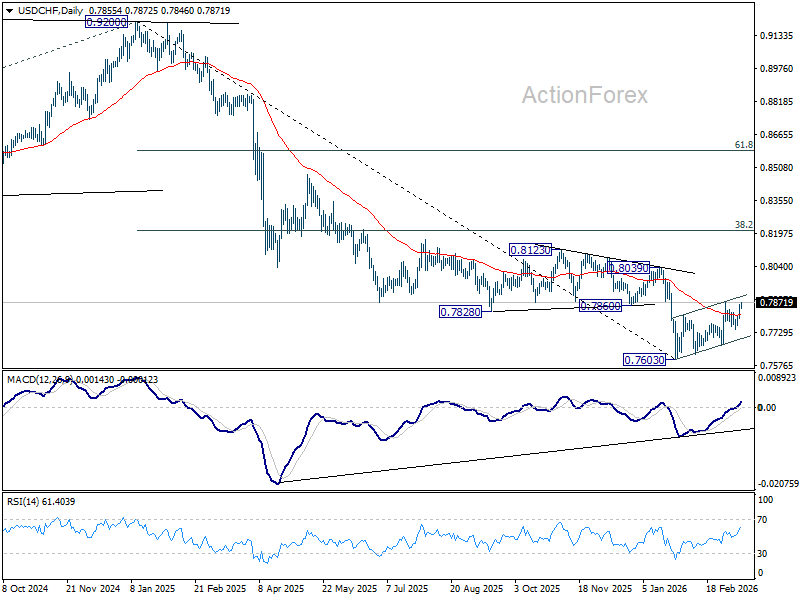

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7815; (P) 0.7840; (R1) 0.7886; More….

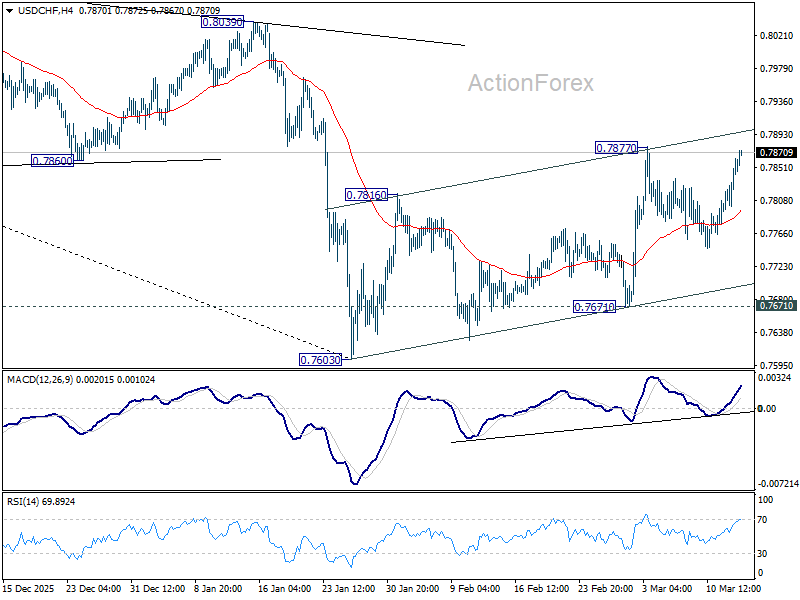

Intraday bias in USD/CHF remains neutral at this point. On the upside, break of 0.7877 will resume the whole rise from 0.7603. Further rally should then be seen to 0.8039 resistance next. On the downside, break of 0.7671 support will revive near term bearishness and bring retest of 0.7603 low.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, break of 0.7603 will resume the down trend to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

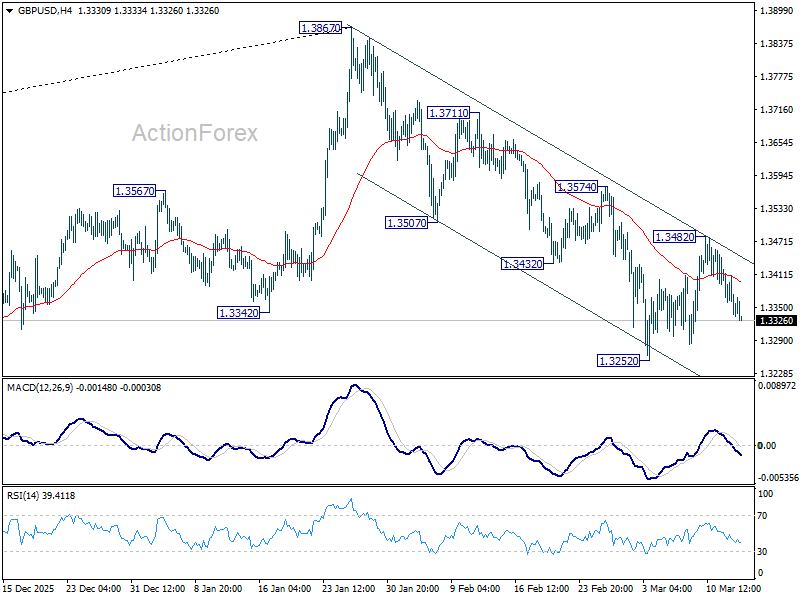

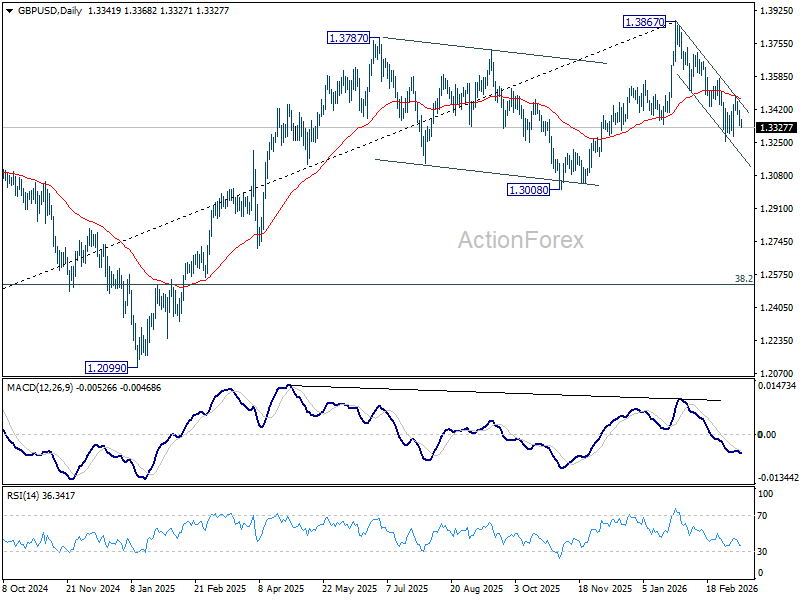

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3392; (P) 1.3438; (R1) 1.3463; More...

GBP/USD is still bounded in range of 1.3252/3482 and intraday bias remains neutral. Further decline is expected with 1.3574 resistance intact. On the downside, below 1.3252 will extend the decline from 1.3867 to 1.3008 structural support. Decisive break there will carry larger bearish implications.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least corrective the whole rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

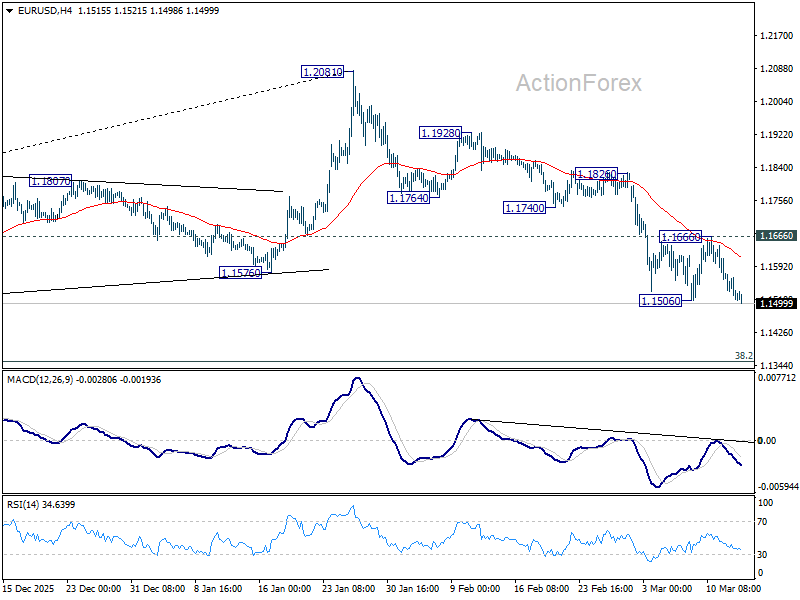

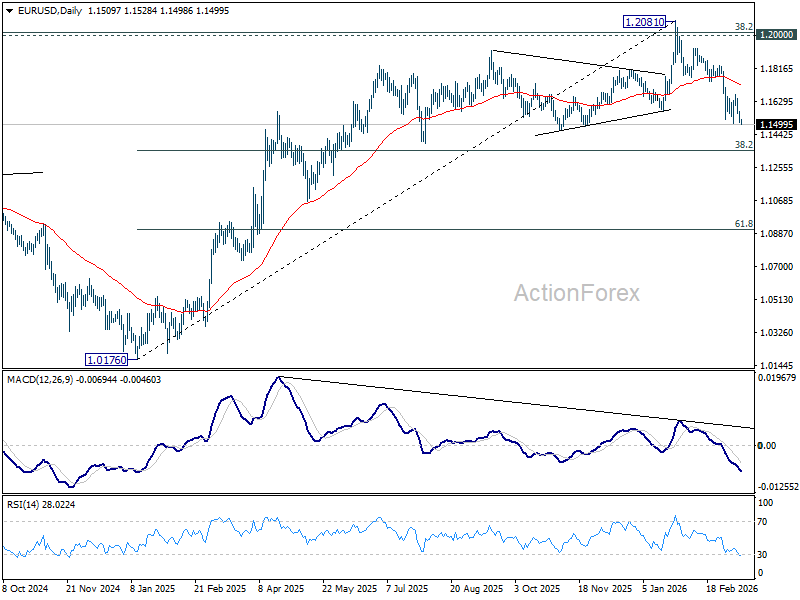

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1533; (R1) 1.1556; More….

EUR/USD's fall from 1.2081 resumed by breaking 1.1506 temporary low and intraday bias is back on the downside. Deeper decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Overall, near term outlook will stay cautiously bearish as long as 1.1666 resistance holds, in case of another recovery.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

Dollar Jumps as Risk-Off Returns on New Iran Leader’s Hormuz Threat

Global markets remain firmly locked in risk-off mode as investors grapple with a renewed escalation in the Iran conflict and the growing risk of prolonged disruptions to global energy supply. Asian equity markets traded broadly lower today, following a weak lead from Wall Street where DOW dragged major U.S. indexes down overnight. The deteriorating sentiment has triggered a renewed flight to safety in currency markets. Dollar is strengthening broadly, pushing to fresh highs against both Euro and Yen amid rising geopolitical uncertainty and inflation risks.

The latest catalyst came from Iran’s newly installed supreme leader, Mojtaba Khamenei, who issued his first major statement since succeeding his father. In a televised message, Khamenei declared that the Strait of Hormuz should remain closed and warned that Iran would continue attacks on Persian Gulf neighbors.

Such rhetoric has reinforced fears that the conflict could persist for longer than previously expected. The Strait of Hormuz remains one of the world’s most critical energy chokepoints, handling roughly a fifth of global oil shipments, and any prolonged disruption would have significant implications for global supply.

Oil markets have responded accordingly. Brent crude remains firmly above $100 per barrel mark. Although prices briefly eased toward $100 after the US issued a second waiver allowing certain Russian oil cargoes to move forward, the broader war premium remains deeply embedded in energy markets.

Meanwhile, inflation concerns are now feeding directly into interest rate expectations. Markets are rapidly scaling back bets that the Fed will be able to resume its easing cycle this year. The probability of a 25-basis-point rate cut in June has fallen sharply to around 20%, compared with roughly 50% just one month ago. More strikingly, the probability of even a single rate cut by the end of the year has slipped to around 55%. This suggests investors are increasingly uncertain whether the Fed will have sufficient room to ease policy at all in 2026 if energy prices remain elevated.

Against this backdrop, a trio of key market indicators should be closely monitored: DOW, U.S. 10-year Treasury yield, and oil prices. Together, these assets form a critical barometer of how markets are pricing the inflation shock triggered by the war.

- For equities, the immediate focus is on DOW’s weekly low of 46,615.52. A decisive break below this level would signal that sellers have regained control, opening the door for a deeper correction toward 45,000 psychological mark.

- Meanwhile, the bond market is also flashing warning signs. The 10-year Treasury yield has extended its climb and is now approaching the 4.3% level. A sustained move above that threshold would indicate that markets are increasingly worried that the energy shock could reignite persistent inflation pressures.

- Ultimately, both equities and bond yields remain heavily dependent on oil prices. Should WTI decisively break above the $100 level, it would likely reinforce inflation fears, push yields higher, and intensify the broader risk-off dynamic currently sweeping global markets.

In the currency markets, Aussie remains the strongest performer for the week so fa. However, the currency is beginning to show signs of vulnerability as risk aversion intensifies. The Dollar now sits firmly in second place and could soon take the lead if the defensive mood deepens further.

In Asia, at the time of writing, Nikkei is down -1.14%. Hong Kong HSI is down -0.46%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.06%. Japan 10-year JGB yield is up 0.051 at 2.240. Overnight, DOW fell -1.56%. S&P 500 fell -1.52%. NASDAQ fell -1.78%. 10-year yield rose 0.065 to 4.273.

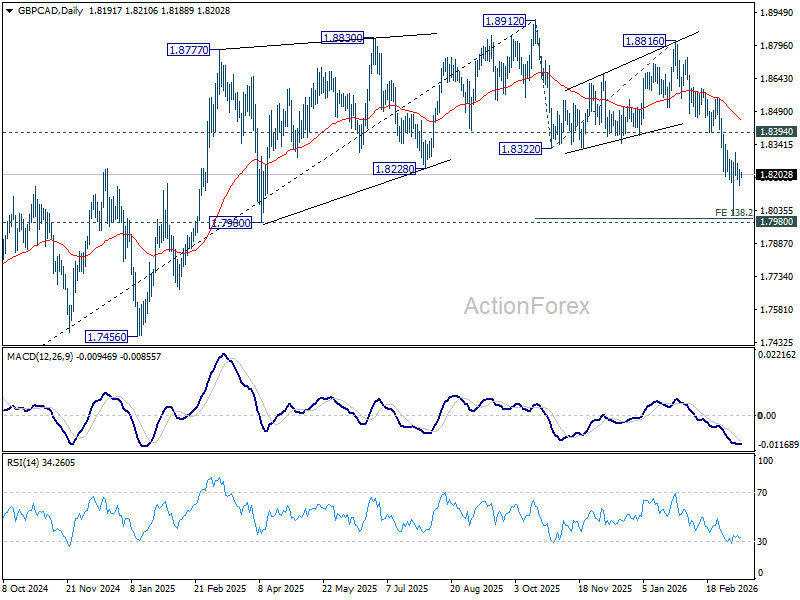

GBP/CAD eyes major break below 1.80 ahead of UK GDP and Canada jobs

GBP/CAD is entering a decisive moment as markets prepare for two key economic releases today: UK January GDP and Canada’s February employment report. The data arrives just days before the BoC’s policy decision on March 18 and the BoC’s meeting on March 19, making the numbers particularly influential for near-term policy expectations.

Additionally, these events are unfolding against an unusually volatile global backdrop. The Iran war continues to drag on while oil prices have surged back toward the $100 level, as traders increasingly price the risk of prolonged supply disruptions. For central banks, this environment complicates the policy outlook by raising inflation risks even as growth remains fragile.

For the BoE, market expectations have already shifted dramatically over the past two weeks. Investors previously anticipated a 25bps rate cut from the current 3.75% policy rate. However, the energy shock and renewed inflation fears have pushed consensus toward a hold at next week’s meeting.

That shift places even greater emphasis on today’s UK GDP report. Expectations are already modest, with forecasts centered around a monthly gain of roughly 0.1% to 0.2%. A result in line with those estimates would likely provide relief for BoE policymakers by confirming that the economy is at least maintaining modest growth.

Such an outcome would allow the BoE to keep policy steady while waiting to see how the oil shock affects inflation dynamics. In that scenario, the central bank could delay easing until later in the year once the immediate energy volatility subsides.

However, a negative GDP print would represent a far more troubling outcome. Contraction even before the recent oil surge would strengthen the argument that the UK economy is drifting toward stagflation—an environment where growth weakens while inflation rises due to external energy shocks.

In such a situation, the BoE could find itself effectively paralyzed. Cutting rates to support growth would risk pushing Sterling lower, which would further raise the cost of energy imports and intensify inflation pressures.

On the other hand, the BoC faces a different but equally complex challenge. Markets widely expect the BoC to remain on hold at 2.25% for an extended period, but the oil shock adds a unique twist for Canada as a major energy exporter.

Higher oil prices tend to support Canada’s national income and strengthen the currency, even though they can simultaneously hurt household purchasing power through higher fuel costs. This dual effect makes interpreting economic data particularly important for policymakers.

Expectations for today’s employment report point to job gains of roughly 10,000 to 15,000, with the unemployment rate edging up from 6.5% to 6.6%. Stronger-than-expected employment would reinforce the case for the BoC to maintain its pause while allowing the oil-driven boost to support the economy.

Conversely, a sharp deterioration—particularly if unemployment climbs toward 6.7% or even 6.8%—could force policymakers to reconsider whether an additional “insurance” rate cut might be necessary to support the labor market.

In terms of immediate market reaction, the more volatile and relatively unpredictable Canadian employment report is likely to be the main volatile driver for GBP/CAD. Additionally, the directional bias leans slightly toward further downside in GBP/CAD. If Canadian data holds up, Loonie is well positioned to ride the wave of high oil prices.

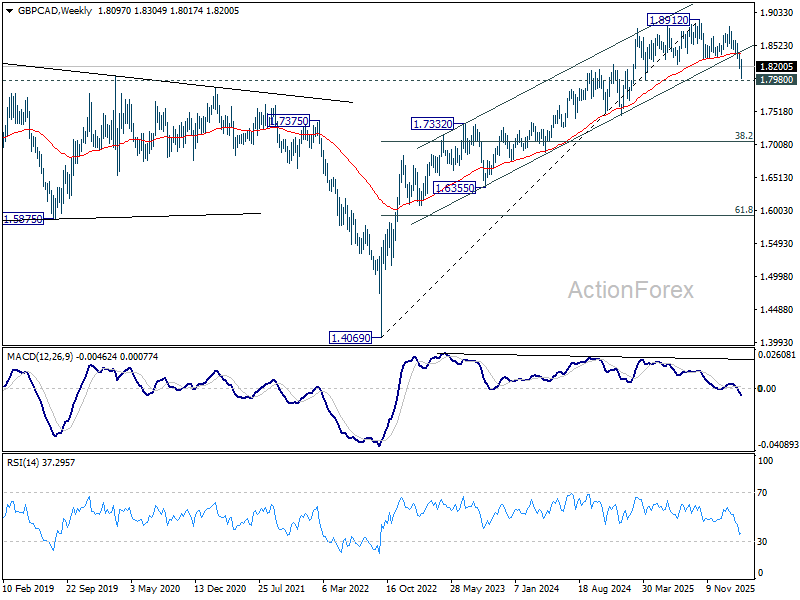

Technically, GBP/CAD is approaching a critical inflection point. The pair is now testing the major psychological and structural support zone around 1.80, near the 1.7980 level 1.382% projection of 1.8912 to 1.8322 from 1.8816 at 1.8001.

The importance of this level is amplified by broader technical signals. GBP/CAD has already broken below its 55 W EMA and the lower boundary of a multi-year rising channel, while bearish divergence has appeared on the weekly MACD indicator.

A decisive break below 1.80 would suggest that the decline from 1.8912 is evolving into a deeper correction of the entire uptrend from 1.4069 (2022 low). Such a move would open the door to a slide toward 38.2% retracement of 1.4069 to 1.8912 at 1.7062 in the medium term.

However, if the pair manages to hold above the 1.80 region and stage a strong rebound, the current move could instead be interpreted as a near term sideway consolidation within the broader uptrend that has defined GBP/CAD since 2022.

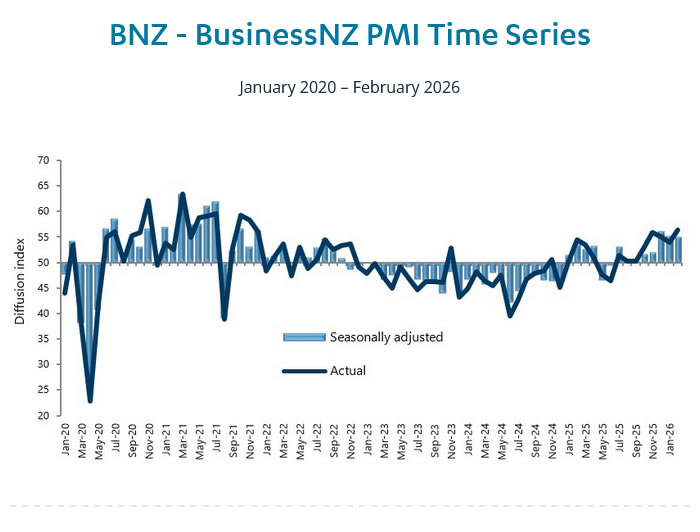

New Zealand BNZ manufacturing holds firm at 55 in February

New Zealand’s manufacturing sector continued to expand in February, with BusinessNZ Performance of Manufacturing Index edging slightly lower from 55.1 to 55.0. While the headline reading dipped marginally, the index remains comfortably above the 50 breakeven level, signaling ongoing growth in the sector.

Underlying components showed mixed but generally positive trends. Production rose modestly from 56.5 to 56.7, while new orders strengthened from 56.6 to 57.6, indicating improving demand conditions. Employment, on the other hand, fell notably from 52.6 to 50.4.

Survey responses pointed to improving business sentiment, with the share of positive comments rising to 55.5% in February from 47.7% in January. Manufacturers reported stronger orders, enquiries, and sales, helped by firmer export demand and improving conditions across certain sectors.

BNZ Senior Economist Doug Steel noted that while geopolitical tensions in the Middle East are dominating market attention, February’s PMI reading provides a solid starting point for the manufacturing sector heading into an uncertain global environment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1533; (R1) 1.1556; More….

EUR/USD's fall from 1.2081 resumed by breaking 1.1506 temporary low and intraday bias is back on the downside. Deeper decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Overall, near term outlook will stay cautiously bearish as long as 1.1666 resistance holds, in case of another recovery.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

FOMC Preview: Powell’s Job Not Getting Any Easier

Stagflation risks have risen since the FOMC last met in January. Higher inflation and a weaker labor market is the FOMC's worst nightmare as it puts the dual mandate in tension. How will Chair Powell and company balance these risks?

We expect the FOMC to hold rates steady and maintain maximum flexibility. It goes without saying the conflict in Iran has a highly uncertain outlook, with oil prices gyrating wildly in response to the uncertainty. Looking past the geopolitical whirlwind, key data from the monthly jobs report whipsawed over the inter-meeting period, with strong job gains and lower unemployment in January offset by a train wreck of a February jobs report. On net, labor market conditions appear little changed: lukewarm and still muddling along.

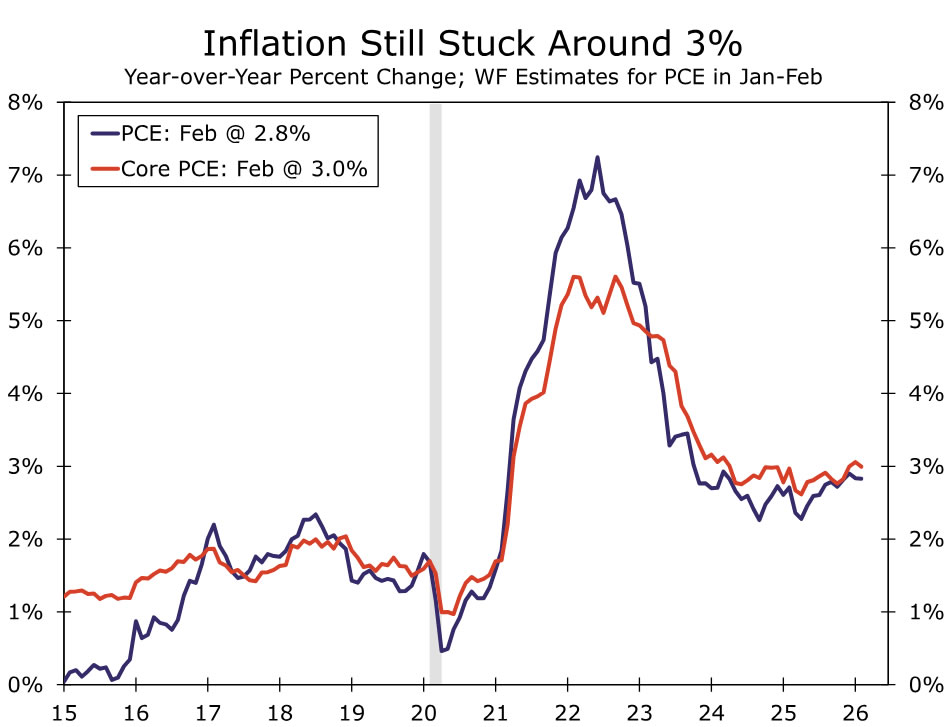

There has been no further progress toward 2% inflation over the inter-meeting period. Recent data point to PCE inflation remaining stuck right around 3% (chart). The energy shock will strengthen headline inflation and have a small pass-through to core but also crimp economic growth.

Fed speak has been mixed. Governors Miran and Waller are likely unconvinced that the labor market is stabilizing and probably want to "look through" the supply-side oil shock—a view for which we have plenty of sympathy. But, with inflation entering its sixth year and counting above 2%, there are signs some of the Committee's hawks are digging in amid yet another inflationary shock.

The post-meeting statement probably won't change dramatically. We expect it to highlight additional uncertainty in the outlook due to the Iran conflict. We also would not be surprised if the language around "some signs of stabilization" in unemployment is tweaked to be a bit more pessimistic.

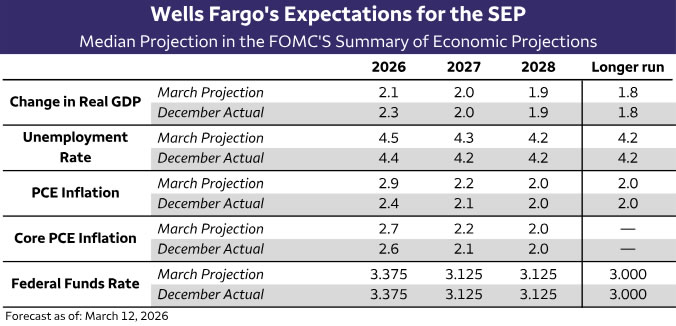

The SEP will shift in a stagflationary direction: We expect the FOMC's inflation projections to be revised up, in part due to higher energy prices and in part due to recent strength in some core PCE components. The slightly stickier picture of inflation is likely to carry through to 2027 and keep the anticipated return to 2.0% two years away. GDP projections for 2026 are likely to be lower but still consistent with above-trend growth. Median estimates for the unemployment rate are likely to edge up as the low hire/low fire environment drags on. Our point estimates for the March SEP can be found in the table on the next page.

"First, do no harm" keeps median dots unchanged. It would take two dots moving down to drop the 2026 median from 3.375% to 3.125% and three moving higher to shift the median projection up to 3.625%. With estimates for inflation drifting up but growth projections shifting down, we think the net impact will be no change to the median dots. From a balance of risks standpoint, our hearts lie with a downside surprise in the dots. Yet our heads think it will be very difficult for the dots to surprise in the dovish direction as inflation worries escalate, even if it is a supply shock that monetary policy is poorly equipped to solve. Our own forecast remains for two 25 bps rate cuts in June and September.

We expect the Fed to slow reserve management purchases to a $20-$25 billion/month pace. This would be a slowdown from the current $40 b/mo pace and has been well-telegraphed by Fed officials. The downshift is in response to funding markets returning to a more stable equilibrium (chart). Since the Fed has been buying exclusively Treasury bills, this should not have a material impact on longer-term interest rates.

Energy Prices & Economic Growth: The Difference Between Now and Then

Between our FAQ with the team and our note on what it would take to have a serious conversation about recession, we have tossed a lot at you over the last week related to the conflict with Iran. Let us provide just a bit more context around some of the numbers we’ve been talking about.

The reality is the U.S. economy is less sensitive to higher energy prices than it once was. In the note we penned on recession risks we referenced our model simulations that suggest a sustained 50% rise in oil prices would reduce the average annual growth rate of real personal consumption expenditures (PCE) by around one percentage point. But consider this. We estimate that same 50% sustained rise in prices would have had about twice the effect back in the 1980s, lopping off around two percentage points off PCE growth. In other words, back then, talk of recession would already be gathering steam, all else equal.

The country was highly energy-sensitive then, heavily reliant on imported oil and far more exposed to sudden increases in energy costs. Higher prices translated quickly into weaker real income growth, reduced consumption and slower top-line economic activity.

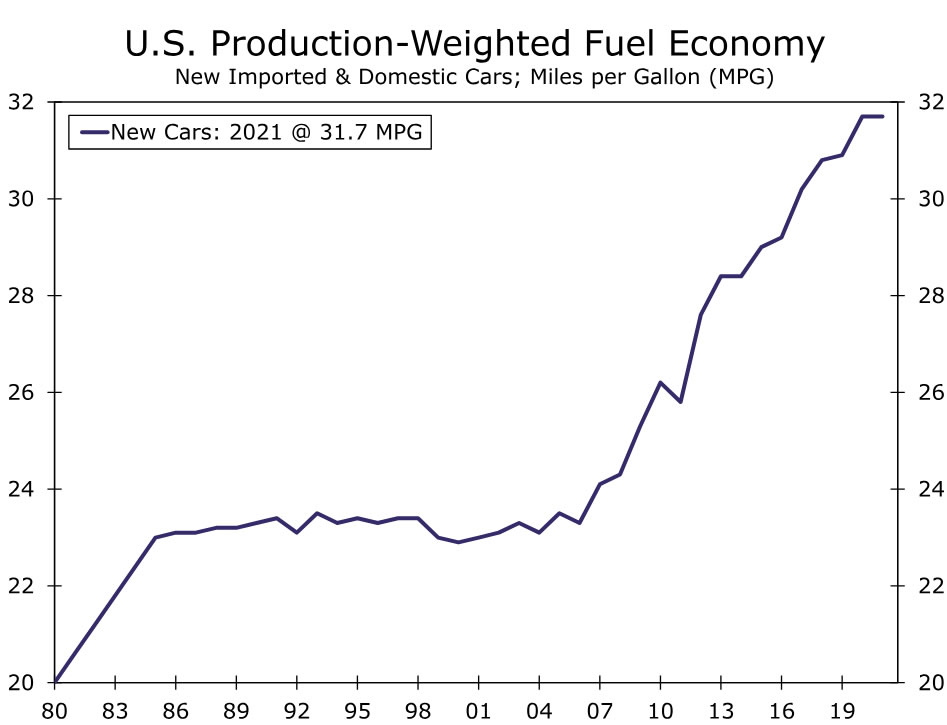

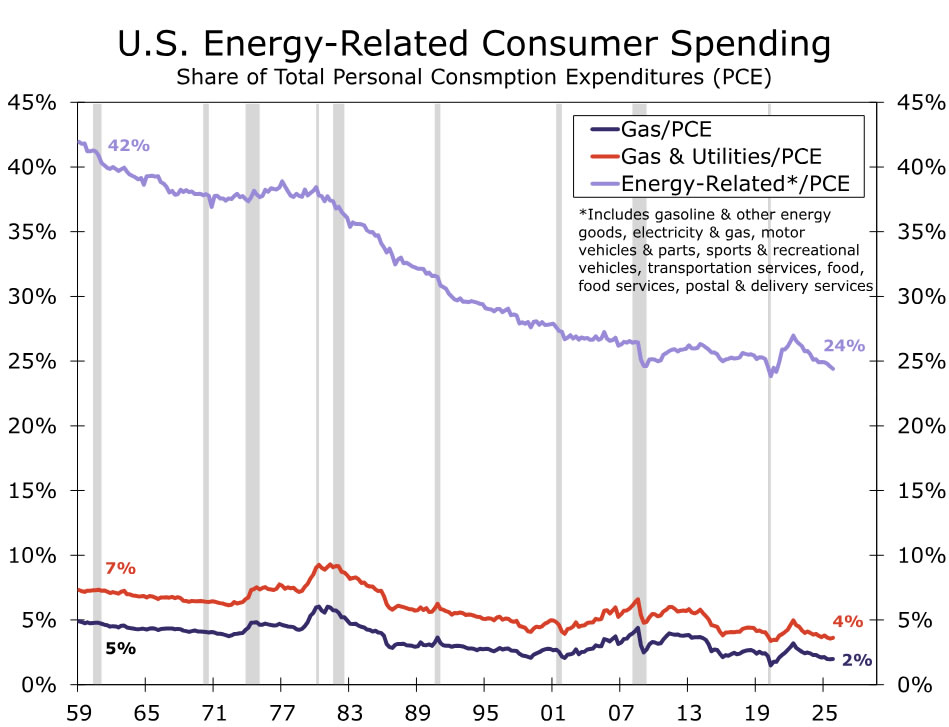

Things are different today. For starters, we are far more energy efficient. Back in the 1980s new cars averaged about 20mpg compared to today’s 32mpg (Figure 1). Second, Households are earning more too; gasoline and even broader energy-related purchases make up a smaller share of household spending today then they once did (Figure 2). And third, the U.S. also produces more domestically meaning it is less reliant on foreign supply (Figure 3).

The bottom line is that improvements in energy efficiency, a smaller energy footprint (relative to output) and the broader U.S. transition from being a net energy importer to a net energy exporter have together reduced the direct drag on growth and particularly consumption from oil and gas price shocks.

That does not mean higher prices today are painless. Energy demand remains relatively inelastic in the short run, and lower-income households remain disproportionately exposed. We've marked down our real PCE growth forecast as a result of the recent move higher in prices.

It seems prudent to again state the obvious here that this still remains an incredibly fluid situation, but at the aggregate level, the effect of higher energy prices is more likely to show up as slower consumption growth, rather than the abrupt retrenchment that characterized past oil shocks. But let’s see where this goes.

GBP/CAD eyes major break below 1.80 ahead of UK GDP and Canada jobs

GBP/CAD is entering a decisive moment as markets prepare for two key economic releases today: UK January GDP and Canada’s February employment report. The data arrives just days before the BoC’s policy decision on March 18 and the BoC’s meeting on March 19, making the numbers particularly influential for near-term policy expectations.

Additionally, these events are unfolding against an unusually volatile global backdrop. The Iran war continues to drag on while oil prices have surged back toward the $100 level, as traders increasingly price the risk of prolonged supply disruptions. For central banks, this environment complicates the policy outlook by raising inflation risks even as growth remains fragile.

For the BoE, market expectations have already shifted dramatically over the past two weeks. Investors previously anticipated a 25bps rate cut from the current 3.75% policy rate. However, the energy shock and renewed inflation fears have pushed consensus toward a hold at next week’s meeting.

That shift places even greater emphasis on today’s UK GDP report. Expectations are already modest, with forecasts centered around a monthly gain of roughly 0.1% to 0.2%. A result in line with those estimates would likely provide relief for BoE policymakers by confirming that the economy is at least maintaining modest growth.

Such an outcome would allow the BoE to keep policy steady while waiting to see how the oil shock affects inflation dynamics. In that scenario, the central bank could delay easing until later in the year once the immediate energy volatility subsides.

However, a negative GDP print would represent a far more troubling outcome. Contraction even before the recent oil surge would strengthen the argument that the UK economy is drifting toward stagflation—an environment where growth weakens while inflation rises due to external energy shocks.

In such a situation, the BoE could find itself effectively paralyzed. Cutting rates to support growth would risk pushing Sterling lower, which would further raise the cost of energy imports and intensify inflation pressures.

On the other hand, the BoC faces a different but equally complex challenge. Markets widely expect the BoC to remain on hold at 2.25% for an extended period, but the oil shock adds a unique twist for Canada as a major energy exporter.

Higher oil prices tend to support Canada’s national income and strengthen the currency, even though they can simultaneously hurt household purchasing power through higher fuel costs. This dual effect makes interpreting economic data particularly important for policymakers.

Expectations for today’s employment report point to job gains of roughly 10,000 to 15,000, with the unemployment rate edging up from 6.5% to 6.6%. Stronger-than-expected employment would reinforce the case for the BoC to maintain its pause while allowing the oil-driven boost to support the economy.

Conversely, a sharp deterioration—particularly if unemployment climbs toward 6.7% or even 6.8%—could force policymakers to reconsider whether an additional “insurance” rate cut might be necessary to support the labor market.

In terms of immediate market reaction, the more volatile and relatively unpredictable Canadian employment report is likely to be the main volatile driver for GBP/CAD. Additionally, the directional bias leans slightly toward further downside in GBP/CAD. If Canadian data holds up, Loonie is well positioned to ride the wave of high oil prices.

Technically, GBP/CAD is approaching a critical inflection point. The pair is now testing the major psychological and structural support zone around 1.80, near the 1.7980 level 1.382% projection of 1.8912 to 1.8322 from 1.8816 at 1.8001.

The importance of this level is amplified by broader technical signals. GBP/CAD has already broken below its 55 W EMA and the lower boundary of a multi-year rising channel, while bearish divergence has appeared on the weekly MACD indicator.

A decisive break below 1.80 would suggest that the decline from 1.8912 is evolving into a deeper correction of the entire uptrend from 1.4069 (2022 low). Such a move would open the door to a slide toward 38.2% retracement of 1.4069 to 1.8912 at 1.7062 in the medium term.

However, if the pair manages to hold above the 1.80 region and stage a strong rebound, the current move could instead be interpreted as a near term sideway consolidation within the broader uptrend that has defined GBP/CAD since 2022.

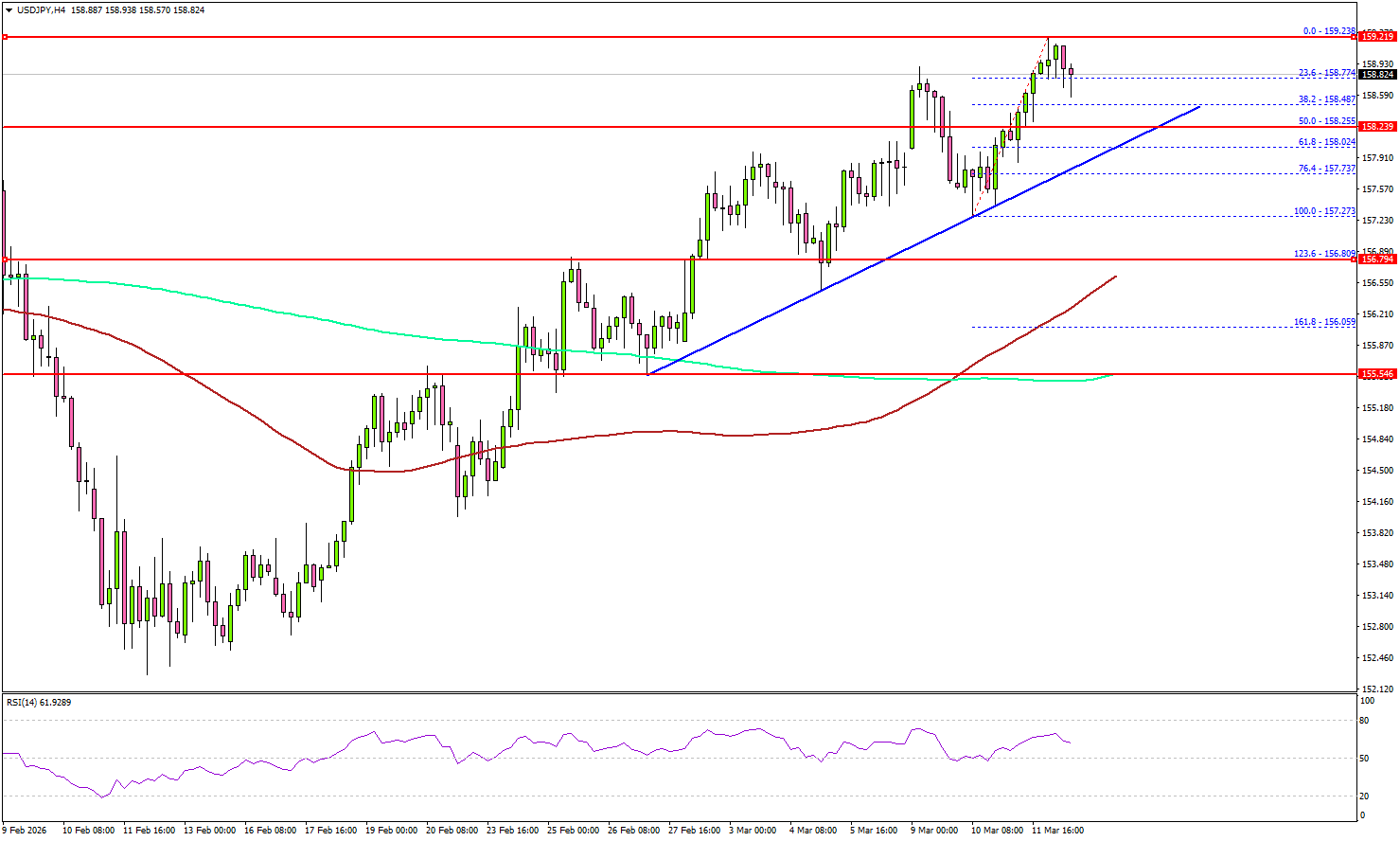

USD/JPY Strength Persists — Is Another Rally Leg Coming?

Key Highlights

- USD/JPY remained in a bullish zone and climbed above 158.00.

- A key bullish trend line is forming with support at 158.20 on the 4-hour chart.

- Bitcoin could form a base for a move above $72,000 and $72,500.

- Crude oil prices are again showing signs of strength for a move to $105.

USD/JPY Technical Analysis

The US Dollar remained supported at 156.50 against the Japanese Yen. USD/JPY started a fresh increase above 157.20 and 158.00.

Looking at the 4-hour chart, the pair settled well above 158.00, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). There is also a key bullish trend line forming with support at 158.20.

On the upside, the pair is now facing sellers near 159.20. The first major resistance sits at 159.50. A close above 159.50 could open the doors for gains above 160.00. In the stated case, the bulls could aim for a move to 162.00. Any more gain might open the doors for a test of 165.00.

If there is no upside continuation, the pair might start a downside correction. Immediate support is seen near 158.25, the 50% Fib retracement level of the upward move from the 157.27 swing low to the 159.23 high, and the trend line.

A close below the trend line support might send USD/JPY to 157.25. The main support sits at 156.80 and the 100 simple moving average (red, 4-hour), below which the pair might gain bearish momentum. In the stated case, it could even revisit 155.00 in the coming days.

Looking at Crude oil, the bulls seem to be active above $85.00, and they could soon aim for a fresh wave above $100 and $105.

Upcoming Key Economic Events:

- US Durable Goods Orders for Jan 2026 – Forecast +1.2% versus -1.4% previous.

- US Personal Income for Jan 2026 (MoM) - Forecast +0.5%, versus +0.3% previous.

- Michigan Consumer Sentiment Index for March 2026 (Prelim) – Forecast 55.0, versus 56.6 previous.

New Zealand BNZ manufacturing holds firm at 55 in February

New Zealand’s manufacturing sector continued to expand in February, with BusinessNZ Performance of Manufacturing Index edging slightly lower from 55.1 to 55.0. While the headline reading dipped marginally, the index remains comfortably above the 50 breakeven level, signaling ongoing growth in the sector.

Underlying components showed mixed but generally positive trends. Production rose modestly from 56.5 to 56.7, while new orders strengthened from 56.6 to 57.6, indicating improving demand conditions. Employment, on the other hand, fell notably from 52.6 to 50.4.

Survey responses pointed to improving business sentiment, with the share of positive comments rising to 55.5% in February from 47.7% in January. Manufacturers reported stronger orders, enquiries, and sales, helped by firmer export demand and improving conditions across certain sectors.

BNZ Senior Economist Doug Steel noted that while geopolitical tensions in the Middle East are dominating market attention, February’s PMI reading provides a solid starting point for the manufacturing sector heading into an uncertain global environment.