Sample Category Title

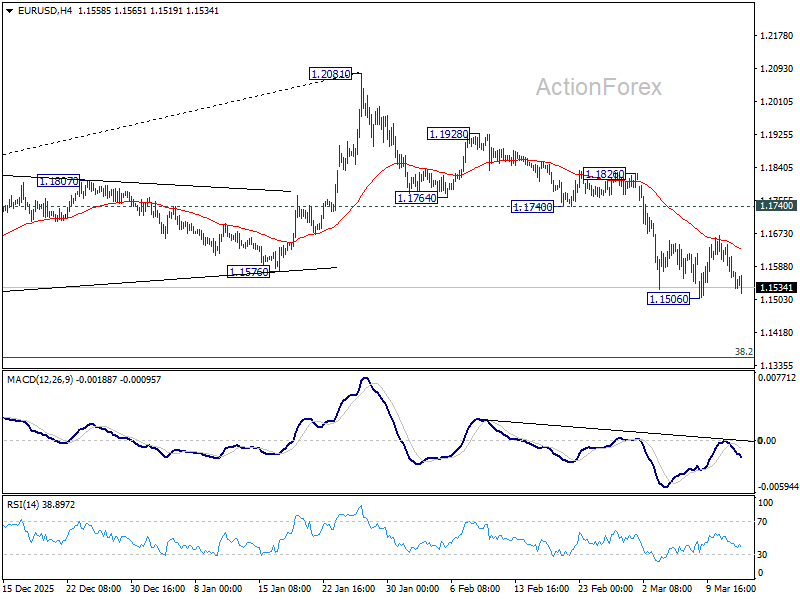

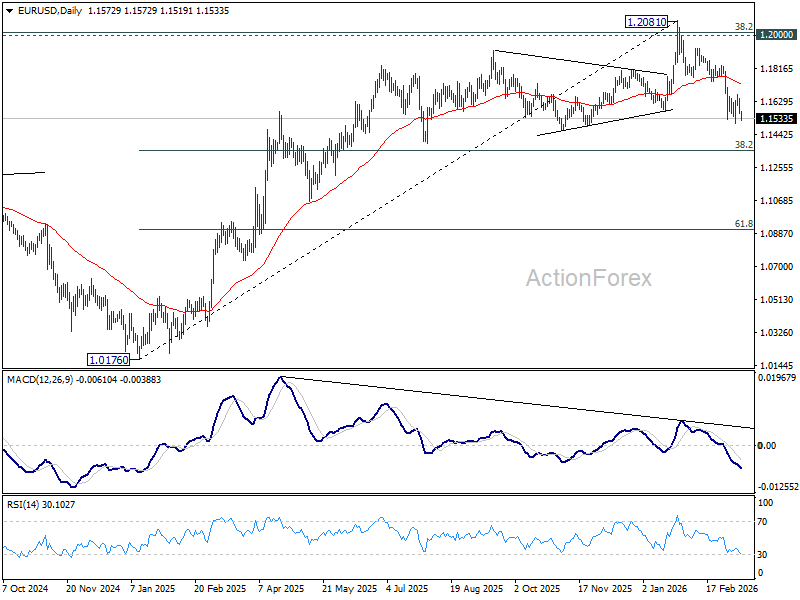

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1590; (P) 1.1628; (R1) 1.1650; More….

Intraday bias in EUR/USD stays neutral for the moment. On the downside, firm break of 1.1506 will resume the fall from 1.2081 and target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Overall, near term outlook will stay cautiously bearish as long as 1.1740 support turned resistance holds.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

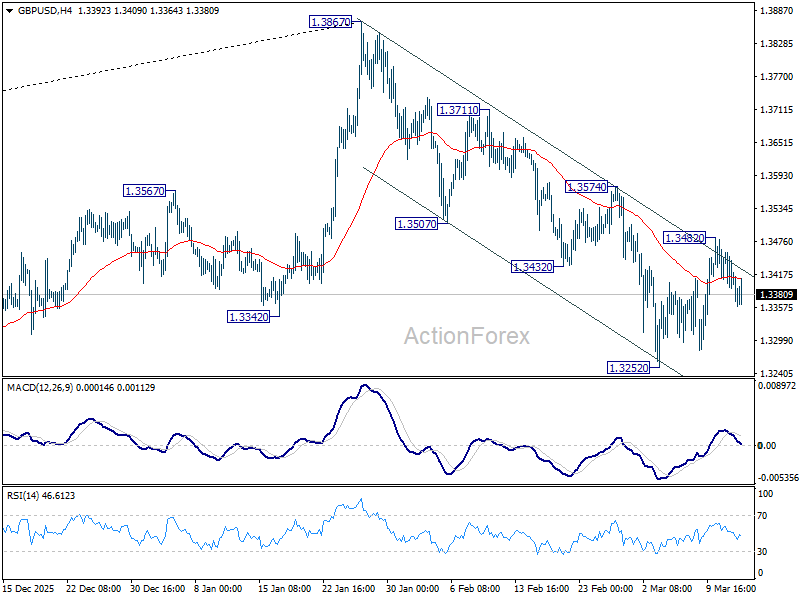

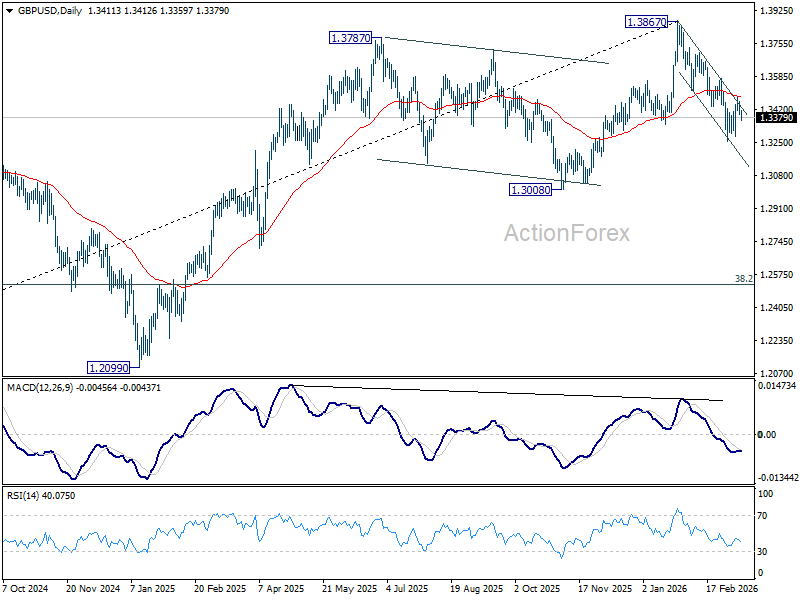

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3392; (P) 1.3438; (R1) 1.3463; More...

Intraday bias in GBP/USD remains neutral at this point. Further decline is expected with 1.3574 resistance intact. On the downside, below 1.3252 will extend the decline from 1.3867 to 1.3008 structural support. Decisive break there will carry larger bearish implications.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least corrective the whole rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

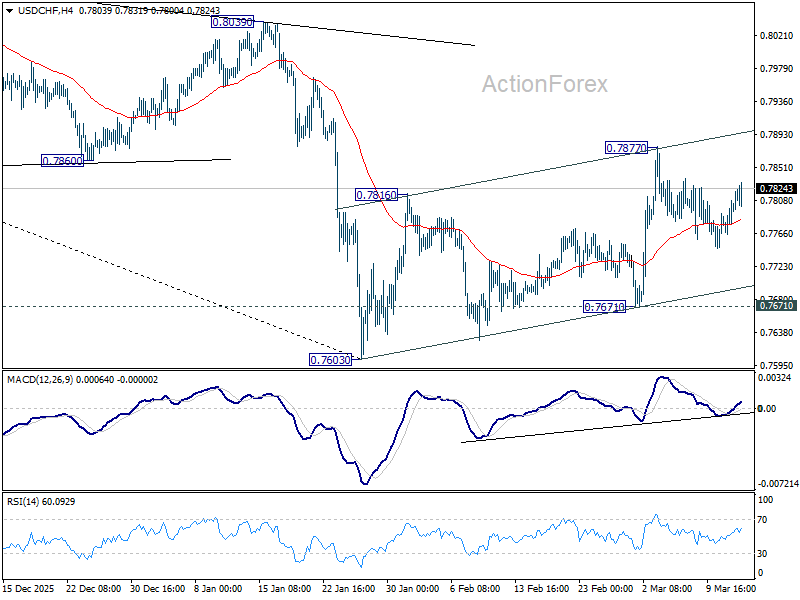

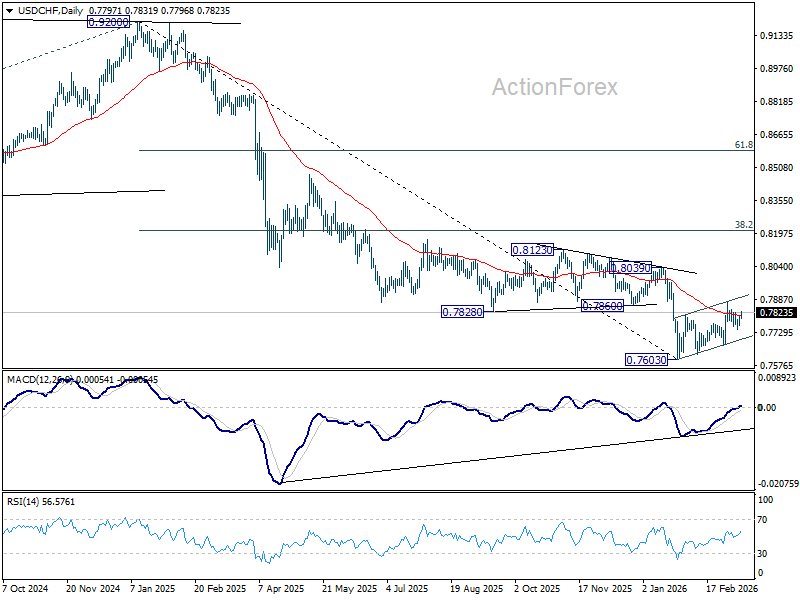

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7775; (P) 0.7792; (R1) 0.7820; More….

Intraday bias in USD/CHF stays neutral for the moment. On the downside, break of 0.7671 support will revive near term bearishness and bring retest of 0.7603 low. Decisive break there will resume larger down trend. On the upside, though, break of 0.7877 will bring stronger rally to 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, break of 0.7603 will resume the down trend to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

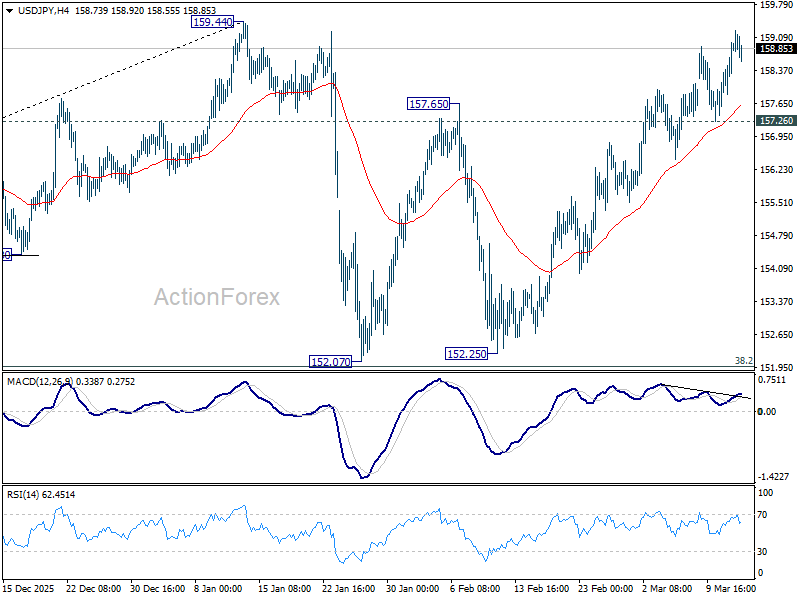

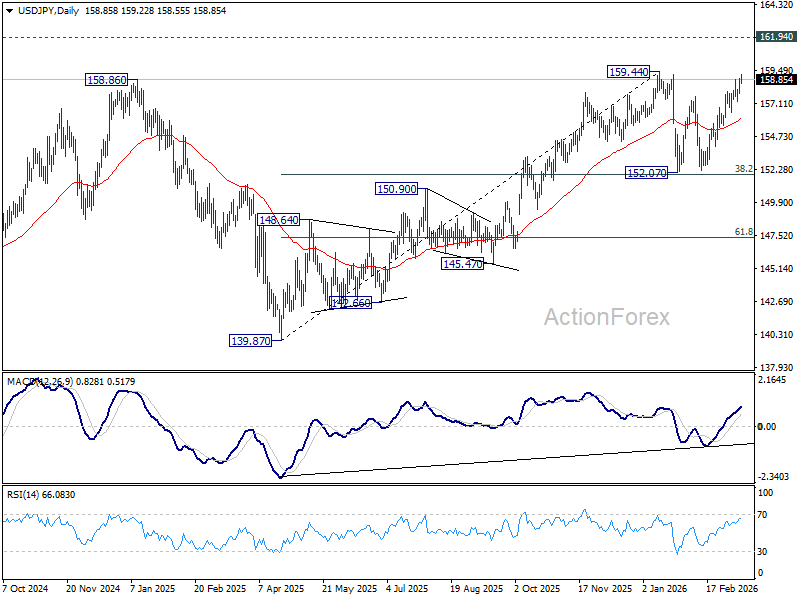

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.23; (P) 158.60; (R1) 159.34; More...

Intraday bias in USD/JPY remains on the upside as rise from 152.07 is still in progress. Firm break of 159.44 will target 161.94 high next. On the downside, below 157.26 support will turn intraday bias neutral again. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

DOW, Yields and $100 Oil Form Critical Risk Triangle for Markets

Global markets have entered a fragile calmness as investors await the next major catalyst. With only second-tier data scheduled and Fed officials in their pre-meeting blackout period, the usual policy signals that guide markets are temporarily absent. Barring any dramatic geopolitical development, this vacuum has shifted the spotlight entirely onto technical levels.

The first critical area to watch lies in the U.S. equity market. While the broader indexes have shown some resilience, the weakness in U.S. futures suggests a cautious hand-off to the regular trading session. The key to watch is this week's low of 46,615.52 in DOW. While a breach of this level seems unlikely within the next few hours, a move in that direction would signal that the “buy the dip” sentiment is fading. Such a development could quickly shift market psychology toward defensive positioning, especially given the heightened geopolitical risks surrounding the Iran war.

Meanwhile, the bond market is delivering its own warning signal through the sharp rise in Treasury yields. 10-year yield surged above 4.2% handle yesterday, highlighting persistent concerns that the energy shock caused by the conflict could reignite inflation pressures. Remaining above 4.2% suggests that markets are beginning to price in a scenario where inflation proves more persistent than expected. In that case, the Fed may be forced to turn to a more hawkish stance despite broader concerns about global growth.

If yields extend toward the 4.3% level, it would reinforce the view that investors expect the Fed to signal stronger inflation vigilance at next week’s meeting. The market would effectively be preparing for a shift away from the earlier narrative of steady policy easing in 2026.

Oil markets are the third and most volatile piece of the current puzzle. Brent crude’s return to the 100 level represents a major psychological barrier for traders and a critical threshold for global inflation expectations. What makes the move particularly striking is that it comes despite the IEA’s unprecedented 400-million-barrel reserve release. Rather than suppressing prices, the intervention has highlighted the scale of the supply disruption currently facing global energy markets.

These three forces—equities, bond yields and oil prices—are now closely interconnected. A sustained break above $100 in oil would likely push Treasury yields higher as inflation expectations rise, which in turn could place additional pressure on equity markets.

In the currency market, Aussie remains the strongest currency for the week so far as markets continue to price in aggressive RBA tightening. Dollar follows, while Kiwi ranks third. Swiss Franc sits at the bottom of the table, followed by Euro and Yen, with Sterling and the Canadian Dollar trading closer to the middle of the performance spectrum.

In Europe, at the time of writing, FTSE is down -0.40%. DAX is down -0.35%. CAC is down -0.55%. UK 10-year yield is up 0.067 at 4.691. Germany 10-year yield is up 0.009 at 2.949. Earlier in Asia, Nikkei fell -1.04%. Hong Kong HSI fell -0.70%. China Shanghai SSE fell -0.10%. Singapore Strait Times fell -0.17%. Japan 10-year JGB yield rose 0.022 to 2.188.

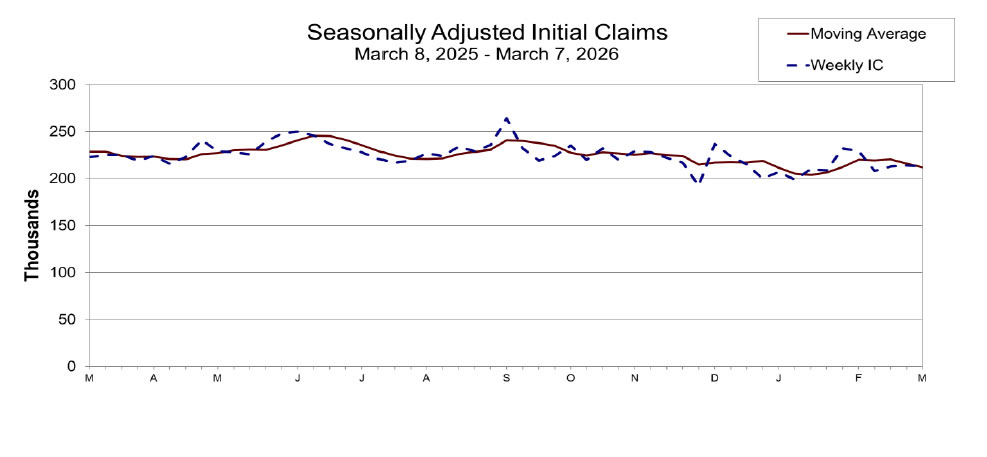

US initial jobless claims fall to 213k, vs exp 215k

US initial jobless claims fell -1k to 213k in the week ending March 7, below expectation of 215k. Four-week moving average of initial claims fell -4k to 212k.

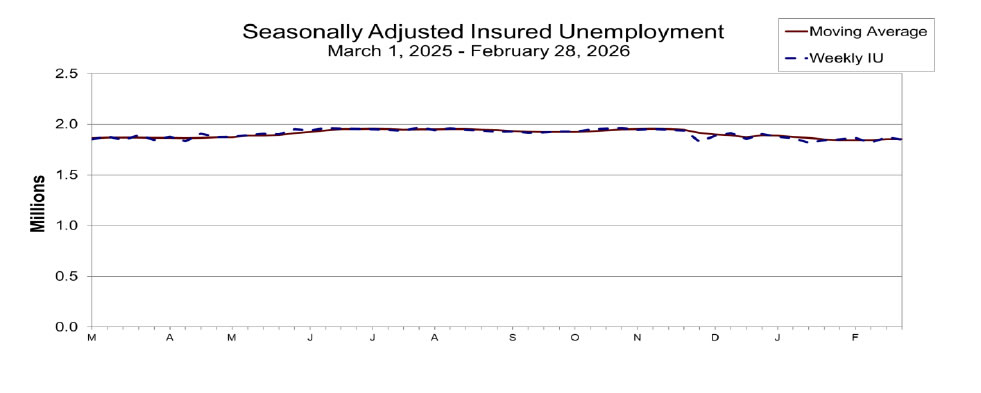

Continuing claims fell -21k to 1,850k in the week ending February 28. Four-week moving average of continuing claims fell -500 to 1,852k.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.23; (P) 158.60; (R1) 159.34; More...

Intraday bias in USD/JPY remains on the upside as rise from 152.07 is still in progress. Firm break of 159.44 will target 161.94 high next. On the downside, below 157.26 support will turn intraday bias neutral again. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

US initial jobless claims fall to 213k, vs exp 215k

US initial jobless claims fell -1k to 213k in the week ending March 7, below expectation of 215k. Four-week moving average of initial claims fell -4k to 212k.

Continuing claims fell -21k to 1,850k in the week ending February 28. Four-week moving average of continuing claims fell -500 to 1,852k.

Chart Alert: WTI Crude Oil Resumes Uptrend Above $88.00 Despite Historical IEA Stockpile Release

Key takeaways

- Extreme oil volatility amid geopolitical risks: West Texas Intermediate crude oil has swung violently during the ongoing US–Iran war 2026, rallying to a 4-year high of $119.54, plunging to $76.83, and then rebounding as fears of disruption around the Strait of Hormuz intensified.

- IEA stockpile release fails to cap prices: Despite the International Energy Agency announcing a record 400-million-barrel emergency reserve release by G-7 nations, oil prices surged again as Iran escalated retaliatory attacks on Gulf oil infrastructure and threatened tanker traffic.

- Technical trend remains bullish above key support: WTI has held its ascending trendline support with $88.36 as the key short-term level; holding above it keeps the bullish uptrend intact toward $102.25 and $116–$119, while a break lower could trigger a deeper pullback toward $81–$76.

Oil prices have swung sharply in both directions since the start of the week, reacting to rapidly shifting geopolitical developments surrounding the US–Iran war 2026, which has now entered its 13th day. Heightened uncertainty over potential supply disruptions in the Strait of Hormuz, a critical global energy chokepoint, has kept energy markets highly volatile.

On Monday, 9 March 2026, the West Texas (WTI) crude oil rallied hard by 30% at the Asian open to hit a 4-year high of $119.54/barrel before it tumbled by 35% to print an intraday low of $76.83 on Tuesday, 10 March 2026’s US session; due to US President Trump’s remarks that touted the “end of the US-Iran war is soon” and the expected historical amount of coordinated release of stockpile of oil reserves among G-7 nations of more than 183 million barrels released in 2022 after Russia invaded Ukraine.

On Wednesday, 11 March 2026, the International Energy Agency (IEA) made the official announcement to release 400 million barrels from emergency oil reserves of G-7 nations, its largest ever release, with 172 million barrels coming from the US.

Iran’s retaliatory attacks on Gulf states’ oil assets overshadowed the IEA’s historical stockpile release

However, WTI crude oil surged by 13% despite news of a historic stockpile release by the International Energy Agency, reaching an intraday high of $96 during the Asian session on 12 March 2026 at the time of writing.

Iran has continued to intensify its retaliatory attacks on the oil assets of other Gulf countries, on top of the “indirect closure” of the Strait of Hormuz, where Iran has threatened to destroy any “unfriendly” oil tankers passing through the strait.

Let's now focus on the potential short-term trajectory (1 to 3 days) of WTI crude oil from a technical analysis perspective.

WTI Crude Oil – Held at ascending trendline support from 26 February 2026

Fig. 1: West Texas Oil CFD minor trend as of 12 Mar 2026 (Source: TradingView)

The recent declines seen in the West Texas Oil CFD (a proxy of the WTI crude oil futures) on Tuesday, 10 March, and Wednesday, 11 March have managed to stall at a minor ascending trendline support in place since the 26 February 2026 low of $63.68 that kickstarted the most recent bullish impulsive up move sequence of 87% to print the current 4-year high of $119.54.

Watch the $88.36 key short-term pivotal support to maintain the current minor bullish up leg in the West Texas Oil CFD for the next intermediate resistance to come in at $102.25, and a clearance above it may see a retest on $116.56/119.54 next in the first step.

However, a break with an hourly close below $88.36 negates the bullish tone to expose the next intermediate supports at $81.85 and $77.26/76.83. A break below $76.83 increases the odds of a further minor corrective decline to mean-revert towards $69.80 and $63.68 (also the 20-day and 50-day moving averages).

Key elements to support the bullish bias on WTI crude oil

- The recent declines seen in the West Texas Oil CFD (a proxy of the WTI crude oil futures) on Tuesday, 10 March, and Wednesday, 11 March have managed to stall at a minor ascending trendline support in place since the 26 February 2026 low of $63.68 that kickstarted the most recent bullish impulsive up move sequence of 87% to print the current 4-year high of $119.54.

- The hourly RSI momentum indicator has formed a prior bullish divergence condition at its oversold region on Tuesday, 10 March 2026.

USD/JPY Approaches Key Resistance Level

The USD/JPY chart shows a bullish trend at the start of March, influenced by the escalation of military activity in the Middle East.

On one hand, the US dollar is strengthening due to increased demand for safe-haven assets. On the other, the Japanese economy is under pressure because of its heavy reliance on oil imports from the Middle East.

These factors have pushed the pair above 159.20 JPY per USD this week, surpassing the January high (point A). The 2026 peak lies nearby; however, technical analysis suggests that bullish momentum may be fading.

In our note of 26 February, we:

- → updated the wide ascending channel along with the intermediate growth trajectory (shown in purple);

- → highlighted signs of seller activity near 156.600.

As indicated by the arrow on the USD/JPY chart, after a small pullback to the lower purple line, buyers resumed their efforts, with the 156.600 level now acting as support.

Currently, we can observe that:

- → the RSI indicator is forming a bearish divergence;

- → it is becoming increasingly difficult for the price to reach the upper boundary of the purple channel;

- → the brief breach of point A resembles a bearish Liquidity Grab.

Additional bearish factors include:

- → the line dividing the upper half of the long-term channel into two parts;

- → proximity to the psychological 160 JPY per USD level.

It is worth recalling that in 2024, 1 USD briefly exceeded 160 JPY, but this level did not hold, as the Bank of Japan intervened. This context adds significance to the upcoming BOJ announcements, scheduled for next Thursday. Ahead of this event, USD/JPY may consolidate around current levels.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Moderately Lower as Market Pressures Intensify

Gold prices fell below 5,150 USD per ounce on Thursday, marking a second consecutive session of decline. Pressure on the market has intensified amid a sharp rise in oil prices, which heightens inflation risks and reduces the likelihood of imminent interest rate cuts by central banks.

Oil has rallied for a second straight day. The market remains concerned about the prospect of a protracted conflict involving Iran, with these worries outweighing the effect of a coordinated release of strategic oil reserves by major economies.

Despite the International Energy Agency's decision to execute the largest release in history—400 million barrels—investors considered the move insufficient to stabilise the market.

A strengthening US dollar and rising Treasury yields have added further pressure on gold. Increased inflation expectations have diminished the probability of Federal Reserve easing, with the market now pricing in only one rate cut before year-end.

Data released yesterday showed that core inflation in the United States remains moderate at the start of the year. Meanwhile, the European Union has warned that inflation in the region could exceed 3% in 2026.

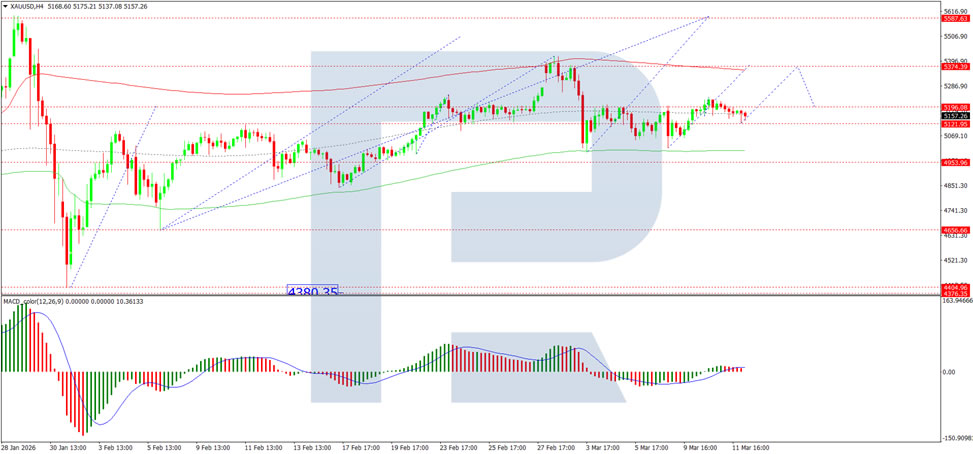

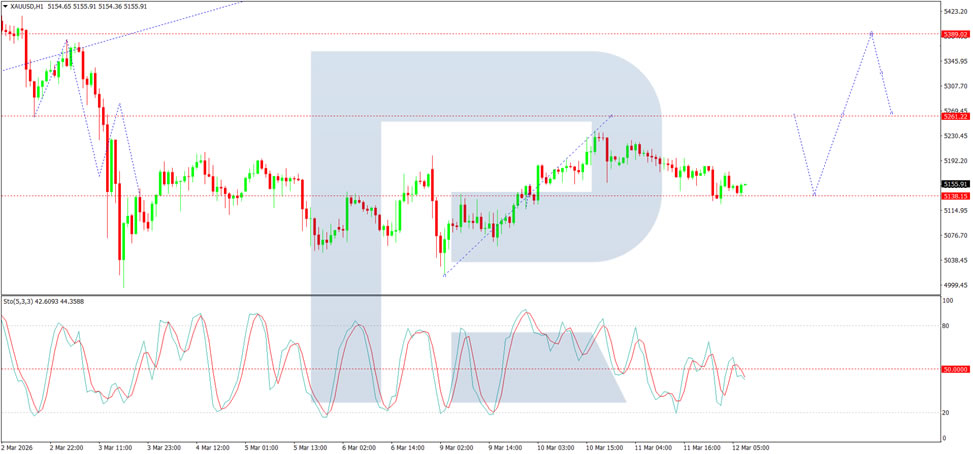

Technical Analysis

On the H4 XAU/USD chart, the market is forming a consolidation range around the 5,196 USD level. A downside breakout would open potential for a continuation of the correction towards 4,953 USD. Conversely, an upside breakout would suggest the development of a growth wave towards the 5,390 USD level. The MACD indicator confirms the current momentum, with its signal line above zero and pointing upwards.

On the H1 chart, the market broke above the 5,135 USD level and completed a growth wave to 5,233 USD, before retracing to 5,140 USD. Looking ahead, the likelihood of a new growth wave developing towards the 5,262 USD level will be considered. The Stochastic oscillator supports this scenario, with its signal line remaining above the 50 level and retaining upside potential towards level 80.

Conclusion

Gold faces mounting headwinds as surging oil prices, driven by geopolitical tensions in the Middle East, reinforce inflation concerns and push central bank rate cut expectations further out. The dollar's strength and rising yields compound the pressure on the non-yielding asset. While technical indicators suggest potential for a short-term bounce, the broader outlook remains cautious as markets digest the implications of sustained energy price inflation and its impact on monetary policy trajectories.

We Believe ECB Will Hike at Next Week’s Meeting or in April

Markets

We believe that the ECB will hike its policy rate at next week’s meeting or in April. In absence of any surprise cease-fire this weekend, the central bank be presented with a $100/b oil price and a tough dilemma when it gathers next Thursday. Even yesterday’s announcement by the International Energy Agency that members will release a record 400mn barrels of oil from their emergency stocks provided no relief. Iran keeps attacking the few vessels trying to pass through the blocked Straight of Hormuz with the US unable/unwilling to provide military escort. In the meantime, overall production grinds to a halt while Oman also evacuated a key oil port following attacks. Recall that also LNG production remains halted at QatarEnergy (force majeure since March 6). On top, it will take time to restore both confidence and supply chains once the conflict does come to an end. Having touted that policy is in a good place with room to address symmetric risks around the outlook, it might already be time for the ECB to put the money where the mouth is. Technical assumptions for the December 2025 Eurosystem staff macroeconomic projections counted on an average Brent crude price of $62.5/b this year and next to help stabilize inflation near the 2% target over the complete policy horizon. The cut-off date for new projections was just before the start of the conflict in the Middle-East with the ECB planning scenario analysis to help explain its potential reaction function. We believe the ECB to be more trigger-happy because it learnt the hard way four years ago that supply-related energy/inflation shocks are able to ignite second-round effects. They lure this time around as well through for example food prices (fertilizer supply disrupted) and inflation expectations (already sticky above ECB’s inflation target) and by far exceed downside economic risks. ECB president Lagarde in her most recent testimony before European parliament flagged the gap between perceived and actual inflation and why it complicated the ECB’s task to anchor inflation expectations. And while headline inflation may be significantly lower than compared with the start of Russia’s full-scale inflation in Ukraine, core inflation levels are at pretty similar levels. Going into the blackout period ahead of Thursday’s meeting, ECB President Lagarde said they should be vigilant to developing inflation risks. That wording contrasts sharply with the “transitory” narrative which dominated in the spring of 2022. This set-up suggests that the central bank won’t wait until July to address the energy price shock (timeline of 2022 with more or less similar starting dates to conflicts). Failure to respond risks pushing the long end of the curve up as well through rising inflation risk premia and complicates the process of getting any inflationary risks/expectations back under control. The break-down of the German 10-yr yield already shows inflation expectations being responsible for the latest increase in nominal yields. They rose to 2.3%, the highest level since 2023 and ending a period of two years of near stability around the ECB’s 2% inflation target. The persistent bear flattening of EMU yield curves is testament to the market shift towards embracing a different ECB reaction function. While a March rate hike is currently a wildcard (6%), odds for April action are becoming significant (25%).

News & Views

US Trade Representative Greer yesterday announced the first series of new trade investigations that ultimately may end up in new import tariffs. The eventual goal is to by and large replicate the levies introduced under the International Emergency Economic Powers Act that were struck down by the Supreme Court last month. The probes are initiated under Section 301 of the Trade Act which allows the US to impose tariffs in response to other nation’s trade measures that are considered discriminatory. The USTR’s case rests on allegations of production overcapacity in many sectors including aluminum, automobiles, electronics, paper, plastics, machineries and chemicals. Some of the biggest economies that are subject to the investigation are China, the EU, Mexico, India, Japan, South Korea and Taiwan, along with Switzerland, Norway and other ASEAN countries (Cambodia, Singapore, Malaysia …). The Trump administration is expected to announce today separate probes that could lead a ban on imports if found to be made with forced labour. Greer seeks to conclude findings before the 10% Section 122 levies, introduced after the Supreme Court decision, fade out by end-July.

Australian consumer inflation expectations in March hit the highest level since July 2023. The 5.2% is another acceleration from February’s 5% and compares with 3.6% one year ago. The release comes just days before the central bank (RBA) meeting next Tuesday and gives a slight boost to the market implied probability of a rate hike (73%). Chances jumped sharply yesterday after RBA Deputy Governor Hauser issued a stark warning yesterday that they won’t made the same mistake of having inflation at a way too high level following the energy price surge in 2022. Governor Bullock just last week called the March meeting a live one, citing the inflationary risks.