Sample Category Title

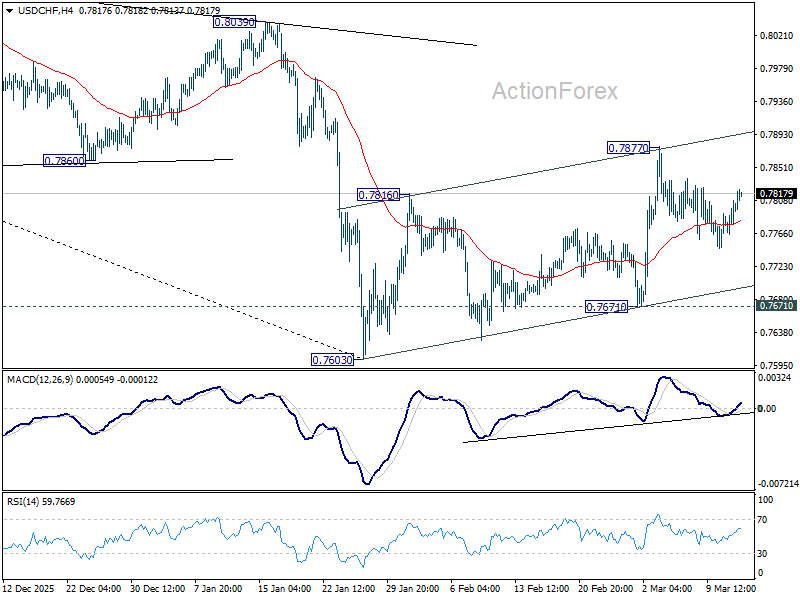

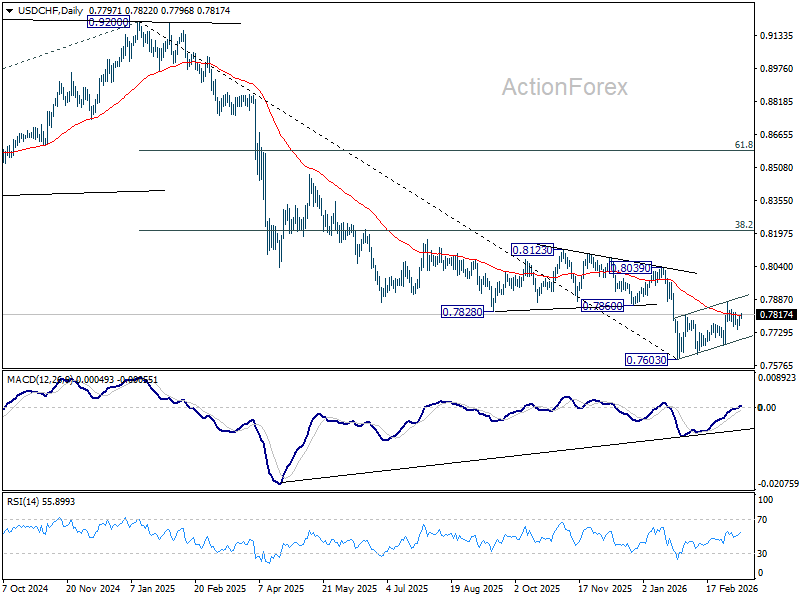

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7775; (P) 0.7792; (R1) 0.7820; More….

Range trading continues in USD/CHF and intraday bias remains neutral. On the downside, break of 0.7671 support will revive near term bearishness and bring retest of 0.7603 low. Decisive break there will resume larger down trend. On the upside, though, break of 0.7877 will bring stronger rally to 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, break of 0.7603 will resume the down trend to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

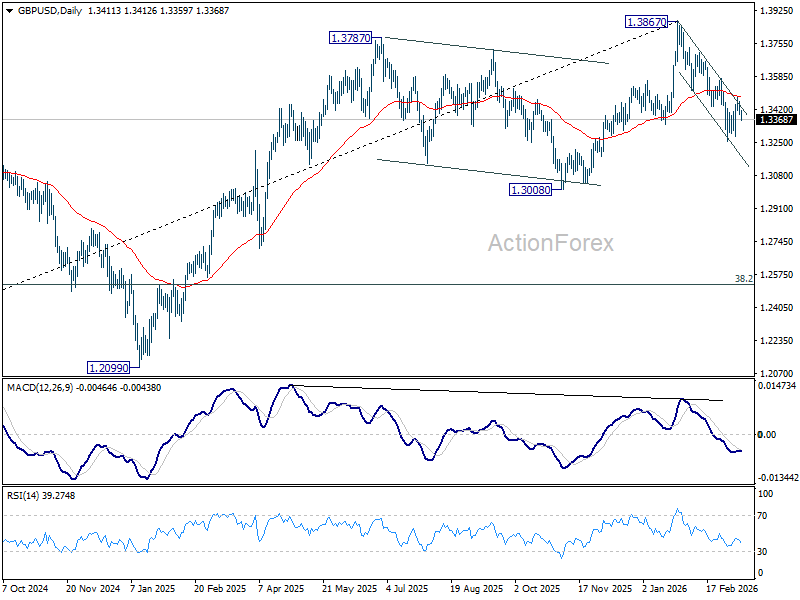

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3392; (P) 1.3438; (R1) 1.3463; More...

No change in GBP/USD's outlook as range trading continues. Intraday bias stays neutral, and further decline is expected with 1.3574 resistance intact. On the downside, below 1.3252 will extend the decline from 1.3867 to 1.3008 structural support. Decisive break there will carry larger bearish implications.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least corrective the whole rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

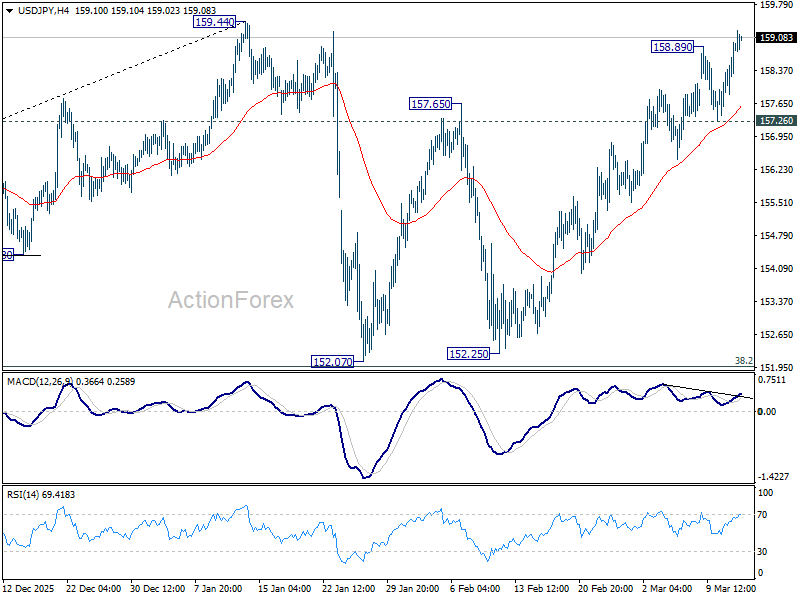

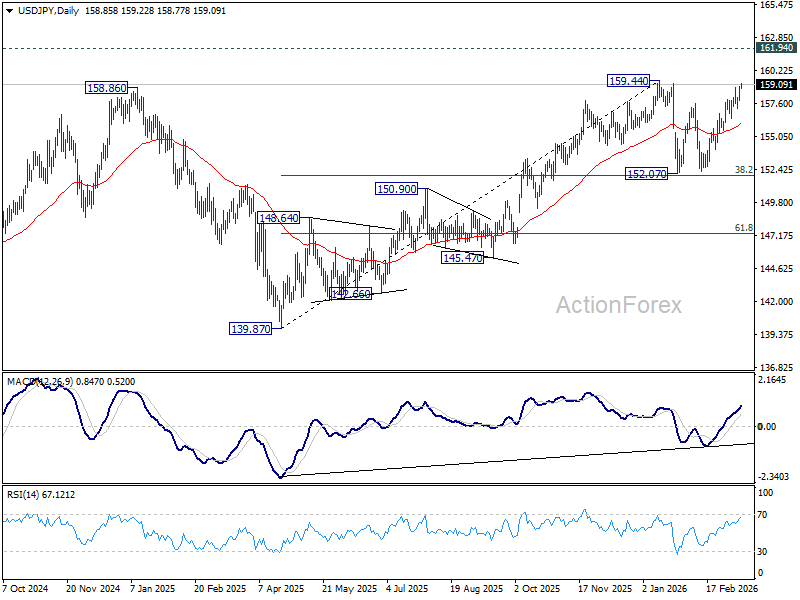

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.23; (P) 158.60; (R1) 159.34; More...

USD/JPY's rise from 152.07 resumed by breaking through 158.89. Intraday bias is back on the upside for 159.44 resistance first. Firm break there will target 161.94 high next. On the downside, below 157.26 support will turn intraday bias neutral again. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

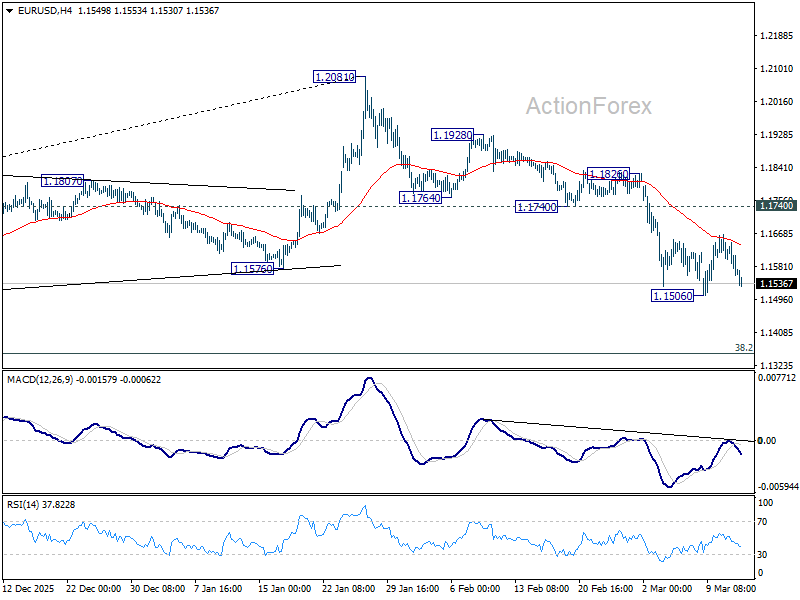

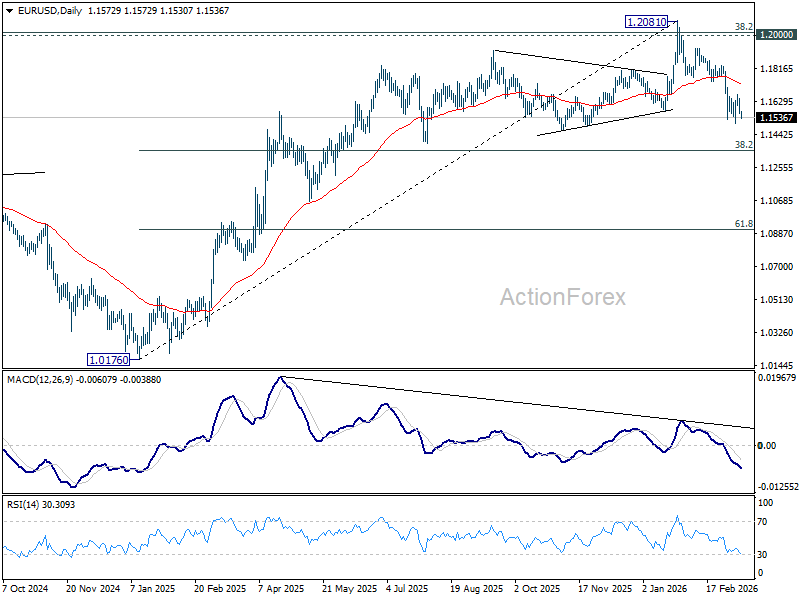

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1590; (P) 1.1628; (R1) 1.1650; More….

Intraday bias in EUR/USD remains neutral first, but focus is back on 1.1506 temporary low with today's decline. Firm break there will resume the fall from 1.2081 and target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Overall, near term outlook will stay cautiously bearish as long as 1.1740 support turned resistance holds.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

Dollar Gains as Iran War Escalates and Brent Oil Reclaims 100

Dollar advanced broadly today as risk aversion swept through global markets. Asian equities declined while investors moved back toward safe-haven assets amid growing doubts about the narrative that the Iran war is nearing an end. Instead, markets are back pricing the possibility of prolonged energy scarcity and fragmentation in global trade.

The shift in sentiment followed fresh evidence that the conflict in the Middle East remains far from resolved. On the one hand, speaking at a rally in Kentucky, US President Donald Trump declared that the US had effectively won the war against Iran. Yet within hours, Iranian explosive boats attacked two oil tankers near Iraq’s Basra terminal, setting both vessels on fire and forcing Iraq to halt operations at its export facilities.

These events reinforced fears that critical energy infrastructure across the Gulf remains highly vulnerable. With the Strait of Hormuz effectively disrupted, traders increasingly view the region’s oil flows as exposed to further attacks.

Markets also reassessed the significance of the International Energy Agency’s emergency intervention. On Wednesday, the IEA authorized a historic release of 400 million barrels from strategic reserves in an attempt to stabilize the energy market following the supply shock.

Rather than reassuring investors, the sheer scale of the release has been interpreted as a warning signal. At more than twice the size of the 2022 Ukraine-related release, the move suggests authorities are preparing for a prolonged disruption to global oil supply.

Even so, the numbers highlight the limits of the intervention. With around 20 million barrels per day typically flowing through the Strait of Hormuz, the emergency reserves would replace only a small fraction of the potential supply loss. Brent crude quickly rebounded above 101 per barrel after an initial dip, reflecting the market’s skepticism.

Adding to market anxiety are renewed tariff threats from Washington. The US Trade Representative has launched Section 301 investigations into sixteen major trading partners, including China, Mexico, India and the European Union. Because Section 301 was the legal mechanism used during the first Trump administration’s trade war, investors see the move as laying the groundwork for a more durable tariff regime.

For the day so far, Loonie leads gains, followed by Dollar and Yen. Risk-sensitive currencies are under pressure, with Aussie the weakest performer of the session ahead of Sterling and Euro.

Looking at the week as a whole, however, Aussie remains the strongest currency thanks to growing expectations of back-to-back RBA rate hikes. Dollar ranks second, followed by Kiwi. Yen remains the weakest performer overall, with Swiss Franc and Euro also lagging, while Loonie and Sterling sit near the middle of the global currency performance table.

In Asia, at the time of writing, Nikkei is down -1.52%. Hong Kong HSI is down -1.19%. China Shanghai SSE is down -0.56%. Singapore Strait Times is down -0.55%. Japan 10-year JGB yield is up 0.018 at 2.184. Overnight, DOW fell -0.61%. S&P 500 fell -0.08%. NASDAQ rose 0.08%. 10-year yield rose 0.072 to 4.208.

AUD/JPY rally accelerates, GBP/AUD falls as RBA turns more activist on inflation

Aussie's broad-based strength continues today as markets further strengthened expectations that the RBA will deliver two consecutive rate hikes in the coming months. Investors are increasingly convinced that the RBA will raise the cash rate at the March 17 meeting and follow up with another increase in May, lifting the policy rate from the current 3.85% to 4.35%.

What has significantly reinforced the narrative this week is the alignment among Australia’s major banks. Commonwealth Bank and ANZ have now joined NAB and Westpac in forecasting back-to-back hikes. With all four major institutions now projecting the same policy path, the market has quickly embraced the view that the RBA is preparing to act more decisively against inflation risks.

A key driver behind this shift is the belief that the RBA is becoming increasingly "activist" in defending inflation expectations. Westpac Chief Economist Luci Ellis, a former senior RBA official, noted that policymakers may now respond more aggressively to the headline inflation shock caused by rising oil prices. Acting pre-emptively could help prevent the energy-driven spike from becoming embedded in longer-term inflation expectations.

The urgency is understandable given Australia’s recent inflation data. Core inflation jumped to 3.4% in January, already well above the RBA’s 2–3% target range. With global energy prices surging following the Iran war, policymakers appear increasingly concerned that the inflation outlook could deteriorate further if action is delayed.

Despite the growing hawkish expectations, markets still broadly believe the tightening cycle will peak at around 4.35%. This level is widely viewed as sufficiently restrictive to contain inflation pressures while avoiding a sharp economic downturn. However, the more important question may be how long rates remain elevated. Many analysts now believe policy could stay at that level well into the second half of 2027.

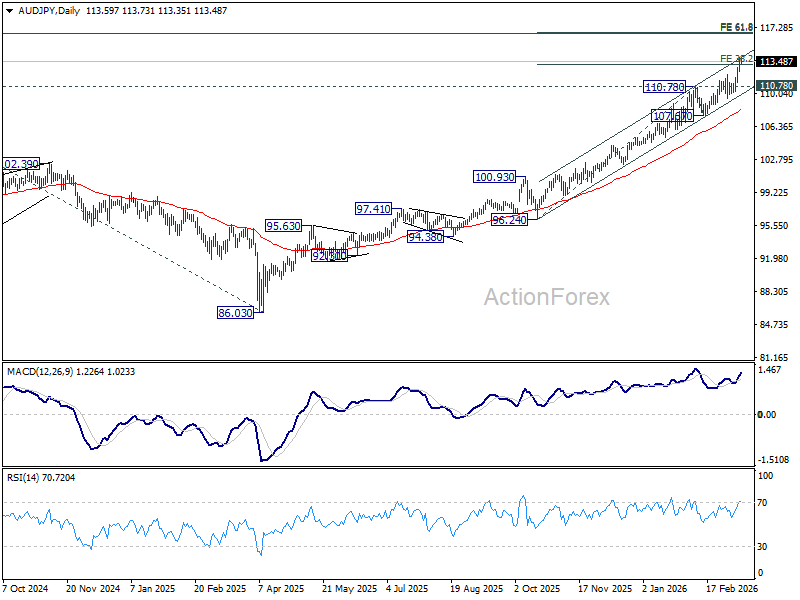

Technically, AUD/JPY has been one of the clearest beneficiaries of this shift in expectations. The cross surged above 38.2% projection of 96.24 to 110.78 from 107.67 at 113.22 this week. While the cross is now testing the ceiling of its rising channel and could see short-term consolidation, the broader outlook remains bullish as long as the former resistance at 110.78 holds as support. The next upside target for AUD/JPY is 61.8% projection at 116.20.

Meanwhile, GBP/AUD has continued its decline and has already reached 200% projection of 2.0848 to 1.9984 from 2.0472 at 1.8744. While the cross may attempt a temporary rebound from the falling channel floor, the broader outlook remains bearish. As long as resistance at 1.9114 caps any recovery, the downtrend is likely to continue toward 261.8% projection at 1.8210.

EU warns 100+ Brent could push inflation above 3%, cut growth by 0.4%

European policymakers are deeply concerned that the Iran war could deliver a fresh stagflation shock to the region’s economy. In a private briefing to EU finance ministers earlier this week, Economy Commissioner Valdis Dombrovskis reportedly warned that the conflict’s impact on energy markets could push inflation higher while simultaneously weighing on growth.

According to officials cited by Bloomberg, sustained Brent crude prices around $100 per barrel could lift EU inflation above 3% in 2026. That would mark a significant setback, reversing the disinflation progress achieved in 2025 as inflation gradually moved to the ECB’s 2% target.

The growth outlook could deteriorate at the same time. The European Commission estimates that economic expansion could be reduced by about 0.4 percentage points this year. With the bloc’s baseline forecast previously standing at just 1.4%, such a hit would meaningfully weaken Europe’s already fragile recovery.

Natural gas prices represent another key risk. Dombrovskis warned that gas could climb to around €75 per megawatt-hour by year-end. Such a move would likely feed directly into broader price pressures and could add another full percentage point to core inflation across the Eurozone economy.

Despite these warnings, the outlook still depends heavily on how long the conflict lasts. Dombrovskis emphasized that if the war is contained within a few weeks, inflation pressures could ease and growth forecasts might stabilize. But if the conflict drags on and Gulf energy infrastructure continues to face attacks, the EU may have to confront what he has already described publicly as a “stagflationary shock.”

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1590; (P) 1.1628; (R1) 1.1650; More….

Intraday bias in EUR/USD remains neutral first, but focus is back on 1.1506 temporary low with today's decline. Firm break there will resume the fall from 1.2081 and target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. Overall, near term outlook will stay cautiously bearish as long as 1.1740 support turned resistance holds.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

Bitcoin’s (BTC/USD) Price Outlook: Why Bitcoin’s Recovery Still Lacks the Ingredients for a Decisive Bullish Turn

- Bitcoin is in a "transition phase," consolidating below $70,000 after retreating from $71,000, however the recovery lacks the "ingredients of a decisive bullish turn".

- Despite accelerating institutional inflows into US Spot Bitcoin ETFs, the average ETF holder is currently "underwater" (negative MVRV ratio), interpreted as "capitulation-like conditions" for recent institutional entrants.

- On-chain network activity shows large-scale capital moving, but engagement metrics for the broader retail network, such as active addresses and transaction fees, remain quiet.

For a sustained bullish expansion, Bitcoin must decisively reclaim the primary overhead resistance at the True Market Mean ($79000)

Bitcoin (BTC) is exhibiting a classic transition phase as it navigates between macroeconomic pressure and resilient technical demand. After a brief surge toward the $71,000 mark, the premier cryptocurrency has retreated to consolidate just below the psychologically significant $70,000 level.

Source: TradingView

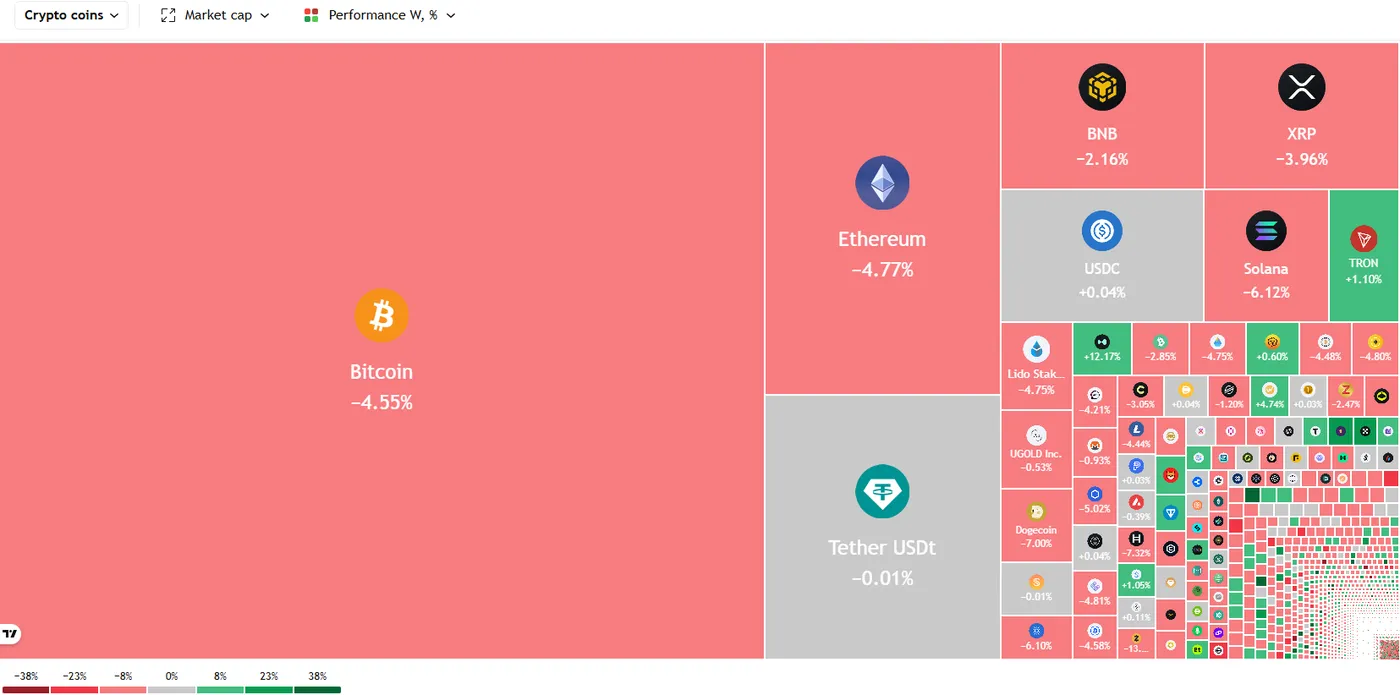

Bitcoin is down around 4.58% this week with red being the dominant color on the crypto heatmap. It shouldn't be a surprise as the general market feeling is still one of unease as haven demand remains strong. The US dollar has benefitted from this which adds further headwinds for Bitcoins recovery.

What does the on-chain data tell us?

According to on-chain data an analysis from Glassnode, Bitcoins price remains bounded between two critical valuation anchors: the Realized Price (~$54.9k), which acts as a long-term support floor, and the True Market Mean (~$79k), which currently serves as the primary overhead resistance.

While the market has managed to break back above the psychologically significant $70,000 barrier, Glassnode warns that the recovery lacks the "ingredients of a decisive bullish turn." Instead, the environment is defined by improving internals at the margins, while broader conviction and capital flows remain soft.

This is reflected by the swift drop after Bitcoin reclaimed the $70000 handle.

Spot demand and ETF dynamics

One of the most constructive signals is the activity within the US Spot Bitcoin ETF complex. Net inflows have accelerated, rising from $776 million to $934 million weekly, alongside a significant jump in trading volume. However, this institutional demand carries a nuanced signal.

The ETF MVRV ratio recently dropped into negative territory, meaning the average ETF holder is currently "underwater" on their position. Glassnode interprets this as "capitulation-like conditions" for recent institutional entrants, suggesting that while they are continuing to buy, they are doing so under considerable price stress.

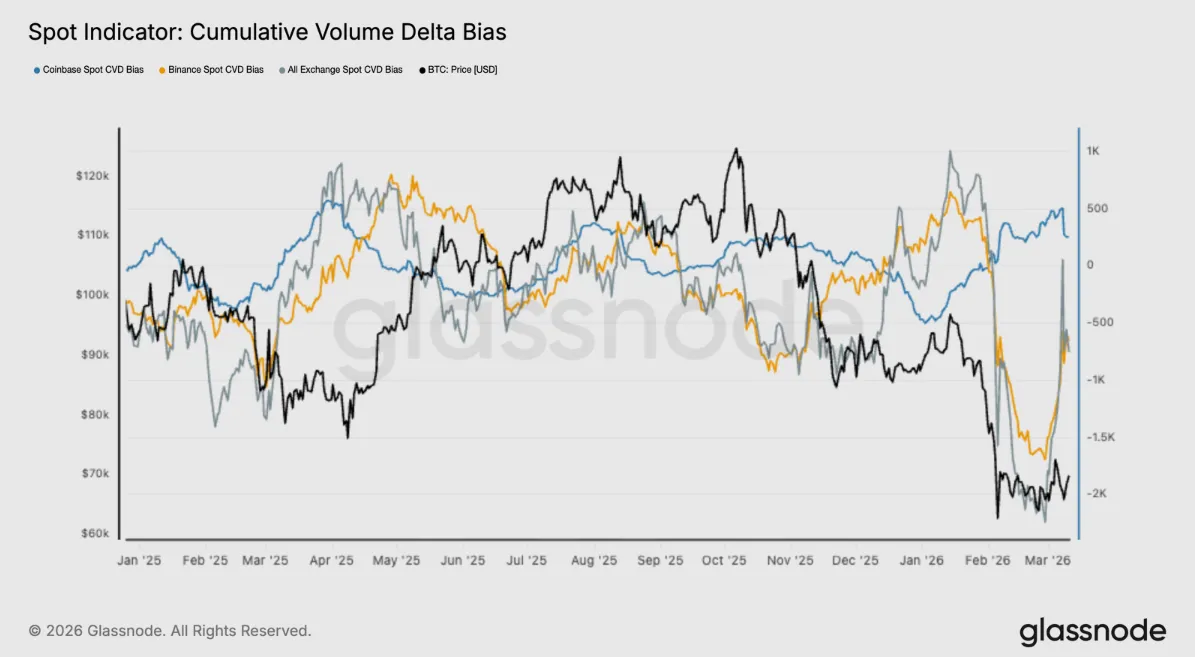

In the broader spot market, demand is showing early signs of recovery, but it remains structurally weak. The Cumulative Volume Delta (CVD), a measure of net buying vs. selling pressure, showed a rebound as buyers began to absorb sell-side liquidity.

Despite this, the lack of aggressive "follow-through" indicates that many participants are still waiting for clearer directional cues before committing significant capital.

Source: Glassnode

On-chain activity

On-chain network activity presents a mixed picture. While transfer volume saw a healthy 23.7% increase, other engagement metrics like active addresses and transaction fees have slipped. This divergence suggests that while large-scale capital is moving (likely institutional or whale-tier transfers), the broader retail network remains quiet and disinterested.

Derivatives: hedging vs. speculation

The derivatives market reflects the general uncertainty of the spot market. Options traders have become notably less defensive; the volatility spread has narrowed, and the 25-delta skew has declined. This indicates that the "panic hedging" seen in previous weeks is fading, and traders are beginning to price in a more balanced near-term outlook.

In the futures market, Open Interest has climbed, signaling a modest rebuild of leverage. However, the funding rates have turned sharply negative, falling below the statistical low band. This suggests a surge in demand for short exposure, highlighting that leveraged traders are far from reaching a bullish consensus.

Technical Outlook: The path ahead

Despite the retreat below $70,000, the technical outlook remains cautiously optimistic rather than bearish.

Long-term holders (whales) and institutional players appear to be "buying the dip."

The formation of an accumulation cluster near the range midpoint is a positive sign, but its intensity is currently lower than the levels that preceded previous major bull runs, per Glassnode data.

If Bitcoin can reclaim and hold the $72000 level, it would likely trigger a wave of FOMO (fear of missing out). However such a move may prove temporary as the one we just had.

For a sustained bullish expansion to occur, Bitcoin needs to decisively reclaim the True Market Mean ($79000) and see a return of "hot capital", speculative interest that has been notably absent.

Until then, the market remains on "unsteady ground," showing the potential to bounce but lacking the aggregate demand required to break out of its defensive structure.

Bitcoin (BTC/USD) Four-Hour Chart, March 11, 2026

Source: TradingView.com (click to enlarge)

GBP/USD Presses Key Barrier, Breakout Momentum Building?

Key Highlights

- GBP/USD started a recovery wave above 1.3380.

- A major bearish trend line is forming with resistance at 1.3450 on the 4-hour chart.

- Crude oil prices saw heavy swing moves above the $80.00 pivot level.

- EUR/USD is slowly moving lower from the 1.1665 resistance.

GBP/USD Technical Analysis

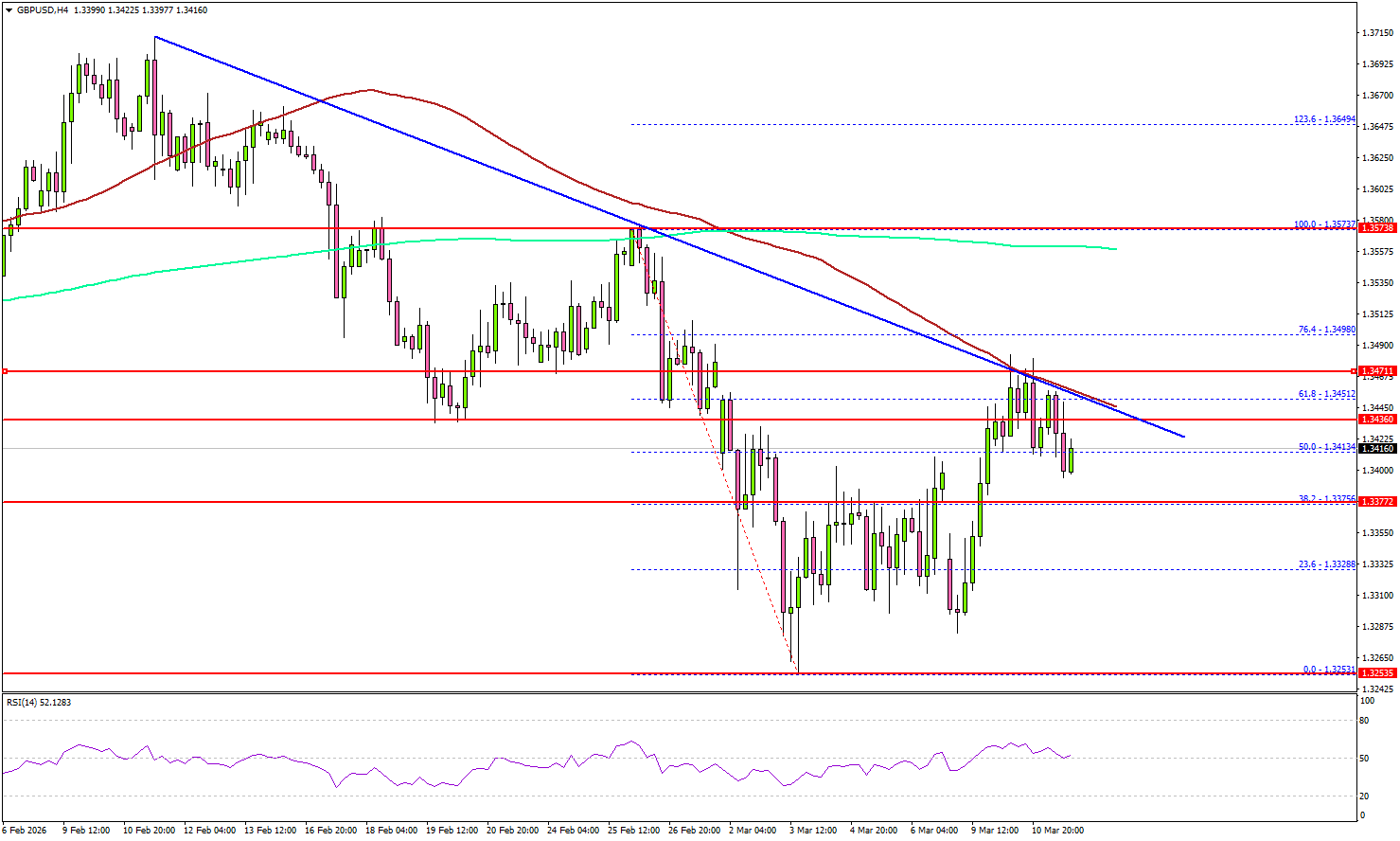

The British Pound recovered some losses and climbed above 1.3350 against the US Dollar. GBP/USD even cleared 1.3400 before the bears appeared.

Looking at the 4-hour chart, the pair faced a strong resistance near the 100 simple moving average (red, 4-hour) and it stayed well below the 200 simple moving average (green, 4-hour). There is also a major bearish trend line forming with resistance at 1.3450.

On the upside, the pair is now facing sellers near 1.3450. The first major resistance sits at 1.3470. A close above 1.3470 could open the doors for more gains. In the stated case, the bulls could aim for a move to 1.3520. Any more gains might open the doors for a test of 1.3550 and the 200 simple moving average (green, 4-hour).

If there is no break above the trend line, the pair might start a fresh decline. Immediate support is seen near 1.3375. The first major area for the bulls might be near the 1.3330 zone.

A downside break below 1.3330 could send the pair toward 1.3280. The main support sits at 1.3250, below which the pair might gain bearish momentum. In the stated case, it could even revisit 1.3120 in the coming days.

Looking at EUR/USD, the pair started a fresh decline from 1.1665, and there are chances of more losses in the near term.

Upcoming Key Economic Events:

- US Initial Jobless Claims - Forecast 215K, versus 213K previous.

- US Monthly Budget Statement (Feb).

AUD/JPY rally accelerates, GBP/AUD falls as RBA turns more activist on inflation

Aussie's broad-based strength continues today as markets further strengthened expectations that the RBA will deliver two consecutive rate hikes in the coming months. Investors are increasingly convinced that the RBA will raise the cash rate at the March 17 meeting and follow up with another increase in May, lifting the policy rate from the current 3.85% to 4.35%.

What has significantly reinforced the narrative this week is the alignment among Australia’s major banks. Commonwealth Bank and ANZ have now joined NAB and Westpac in forecasting back-to-back hikes. With all four major institutions now projecting the same policy path, the market has quickly embraced the view that the RBA is preparing to act more decisively against inflation risks.

A key driver behind this shift is the belief that the RBA is becoming increasingly "activist" in defending inflation expectations. Westpac Chief Economist Luci Ellis, a former senior RBA official, noted that policymakers may now respond more aggressively to the headline inflation shock caused by rising oil prices. Acting pre-emptively could help prevent the energy-driven spike from becoming embedded in longer-term inflation expectations.

The urgency is understandable given Australia’s recent inflation data. Core inflation jumped to 3.4% in January, already well above the RBA’s 2–3% target range. With global energy prices surging following the Iran war, policymakers appear increasingly concerned that the inflation outlook could deteriorate further if action is delayed.

Despite the growing hawkish expectations, markets still broadly believe the tightening cycle will peak at around 4.35%. This level is widely viewed as sufficiently restrictive to contain inflation pressures while avoiding a sharp economic downturn. However, the more important question may be how long rates remain elevated. Many analysts now believe policy could stay at that level well into the second half of 2027.

Technically, AUD/JPY has been one of the clearest beneficiaries of this shift in expectations. The cross surged above 38.2% projection of 96.24 to 110.78 from 107.67 at 113.22 this week. While the cross is now testing the ceiling of its rising channel and could see short-term consolidation, the broader outlook remains bullish as long as the former resistance at 110.78 holds as support. The next upside target for AUD/JPY is 61.8% projection at 116.20.

Meanwhile, GBP/AUD has continued its decline and has already reached 200% projection of 2.0848 to 1.9984 from 2.0472 at 1.8744. While the cross may attempt a temporary rebound from the falling channel floor, the broader outlook remains bearish. As long as resistance at 1.9114 caps any recovery, the downtrend is likely to continue toward 261.8% projection at 1.8210.

EU warns 100+ Brent could push inflation above 3%, cut growth by 0.4%

European policymakers are deeply concerned that the Iran war could deliver a fresh stagflation shock to the region’s economy. In a private briefing to EU finance ministers earlier this week, Economy Commissioner Valdis Dombrovskis reportedly warned that the conflict’s impact on energy markets could push inflation higher while simultaneously weighing on growth.

According to officials cited by Bloomberg, sustained Brent crude prices around $100 per barrel could lift EU inflation above 3% in 2026. That would mark a significant setback, reversing the disinflation progress achieved in 2025 as inflation gradually moved to the ECB’s 2% target.

The growth outlook could deteriorate at the same time. The European Commission estimates that economic expansion could be reduced by about 0.4 percentage points this year. With the bloc’s baseline forecast previously standing at just 1.4%, such a hit would meaningfully weaken Europe’s already fragile recovery.

Natural gas prices represent another key risk. Dombrovskis warned that gas could climb to around €75 per megawatt-hour by year-end. Such a move would likely feed directly into broader price pressures and could add another full percentage point to core inflation across the Eurozone economy.

Despite these warnings, the outlook still depends heavily on how long the conflict lasts. Dombrovskis emphasized that if the war is contained within a few weeks, inflation pressures could ease and growth forecasts might stabilize. But if the conflict drags on and Gulf energy infrastructure continues to face attacks, the EU may have to confront what he has already described publicly as a “stagflationary shock.”

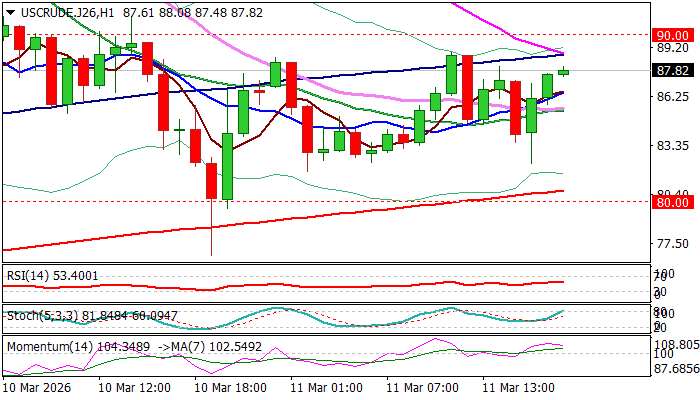

WTI Oil – Near-Term Price Action Holds in Extended Sideways Mode, Awaiting Fresh Signals

WTI oil remains in a sideways mode and ranging between $80 and $90 for the second consecutive day, suggesting that the price action has temporarily stabilized after surge to near $120 per barrel on opening on Monday and subsequent drop of about $40 during Mon/Tue trading.

The latest comments from President Trump about the end of the war in the Middle East and about partial lifting of sanctions on sales of Russian oil, provided relief, with decision of International Energy Agency to release record 400 million barrels from strategic reserves in response to crisis, further cooling the situation and stabilizing the price for now.

On the other hand, fears that global economies could start feeling a full impact of the war through significant supply shortages, as Iran warned the world to be prepared for disastrous scenario of oil price running to $200 per barrel, produce an opposite effect that could inflate the price quickly in scenario of prolonged and escalating war (the US said on Monday that the war may extend towards September).

Long-legged Doji candle on Tuesday and today’s action being in similar shape, signal indecision, with significant barriers at $89.00 and $90, break of which to generate initial reversal signal and open way for stronger recovery.

Conversely, $82.00 (range base) offers solid support, followed by $80, loss of which would further weaken near-term structure.

Res: 89.00; 90.00; 91.41; 92.50

Sup: 81.80; 80.00; 78.40; 76.80