Sample Category Title

Fed’s Goolsbee discusses May FOMC Prospects, robust job market, and lingering inflation concerns

Chicago Fed President Austan Goolsbee discussed the upcoming May FOMC meeting, the strength of the job market, and persistent inflation in an interview. Goolsbee cautioned against reading too much into his stance on interest rates, stating, "We still got a couple of weeks before the actual meeting, so if anybody imputed some specific basis points of what I was for, that'd be inaccurate."

Goolsbee acknowledged the strong job market as the most robust part of the economy, with "unprecedented numbers," while noting that inflation remains a concern. He said, "Inflation — there's been some improvement, but in a way that's the worst part of the economy," adding that it has been "more persistent than we wanted."

As for the potential impact of the recent failure of two US banks on the economy, Goolsbee said it is essential to monitor the extent of the slowdown. He explained, "How much squeezing is going to be coming from the bank side I think is going to matter for whether this economy is going to slow down." Goolsbee emphasized that the intensity of the anticipated growth slowdown in the second half of the year would depend significantly on the financial sector.

ECB Schnabel emphasizes data-driven approach amid banking sector disturbances

European Central Bank (ECB) Executive Board member Isabel Schnabel emphasized the importance of a data-driven approach to policy decisions in light of recent disturbances in the banking sector. She stated yesterday, "I can't tell you what we'll decide at the next meeting, and especially at the following meetings," adding that the situation has become "even more complex."

Schnabel noted the significance of monitoring the potential impact of banking sector uncertainty on lending, saying, "It's even more important that we look at all the data we'll get. It's important whether the uncertainty in the banking sector will have an additional impact on lending."

When discussing the ECB's future plans for its balance sheet, Schnabel admitted that the endpoint remains uncertain and is currently under discussion. She emphasized the need to manage the balance sheet in a way that markets can digest during these turbulent times and expressed satisfaction with the current approach, stating, "So far, it's worked extraordinarily well."

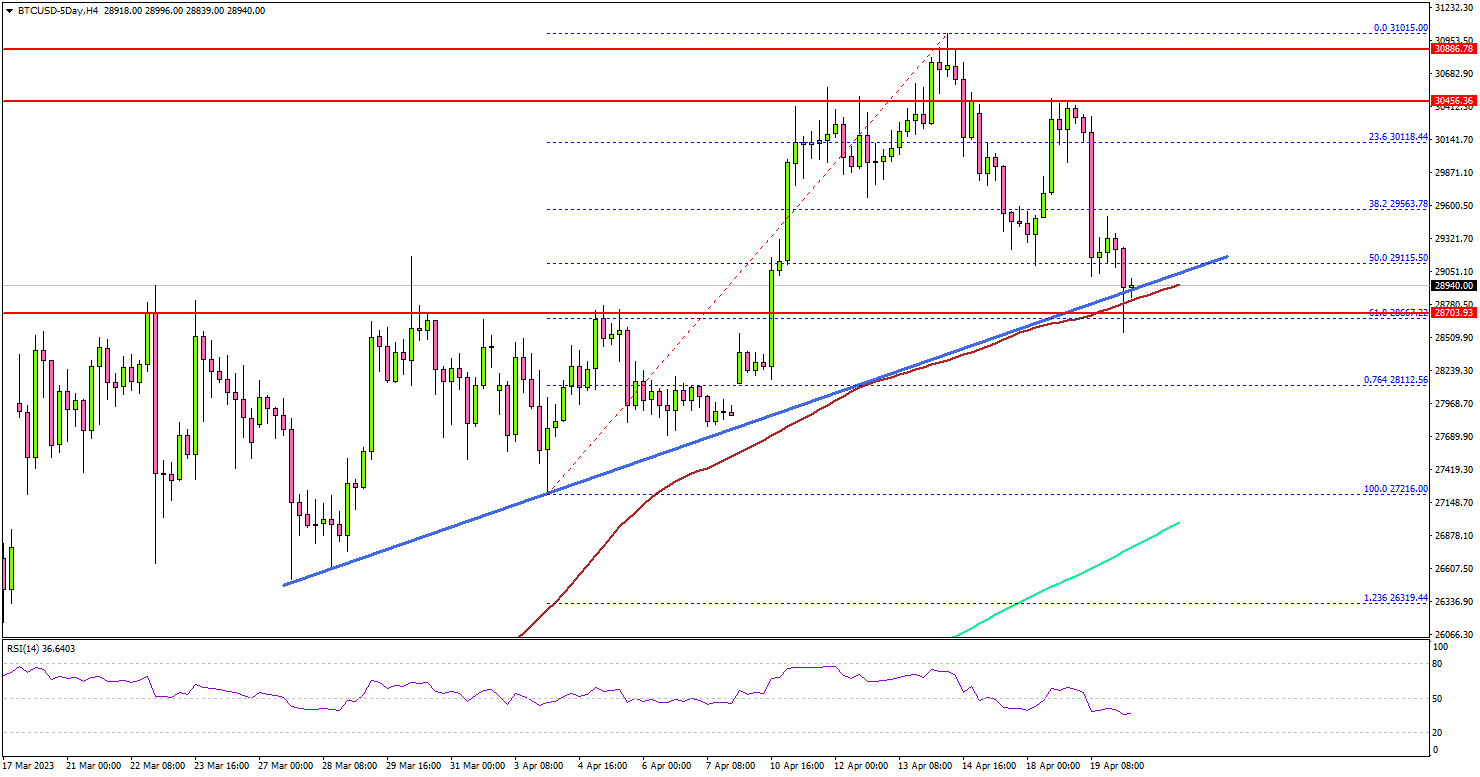

Bitcoin Price Dips But Key Uptrend Support Intact

Key Highlights

- Bitcoin price started a downside correction below $30,000.

- BTC is still above a key bullish trend line with support at $28,900 on the 4-hour chart.

- EUR/USD could attempt a fresh increase above 1.1000.

- The US Initial Jobless Claims could rise from 239K to 240K.

Bitcoin Price Technical Analysis

Bitcoin price struggled to clear the $31,000 resistance zone. BTC/USD started a downside correction below the $30,500 and $30,200 support levels.

Looking at the 4-hour chart, the price gained pace after it broke the $30,000 pivot level. It dipped below the 50% Fib retracement level of the upward move from the $27,216 swing low to the $31,015 high.

The price is now near a key bullish trend line with support at $28,900 on the 4-hour chart. The main support sits near the $28,800 level and the 100 simple moving average (red, 4 hours).

The 61.8% Fib retracement level of the upward move from the $27,216 swing low to the $31,015 high is also near $28,680. If there is a downside break and a close below $28,680, bitcoin might start another decline in the coming days toward the 200 simple moving average (green, 4 hours).

On the upside, the price is facing resistance near the $30,000 level. The first major resistance is near the $30,450 level (a multi-touch zone).

A successful close above the $30,450 level might spark another bullish wave. In the stated case, the price may perhaps rise toward the $31,220 level.

Any more gains could set the pace for a larger increase to $32,000.

Economic Releases

- US Initial Jobless Claims - Forecast 240K, versus 239K previous.

- US Existing Home Sales for March 2023 (MoM) - Forecast +1.5%, versus +14.5% previous.

First Impressions: NZ Consumers Price Index

Consumer prices rose 1.2% in the March quarter and are up 6.7% over the past year. The March result was below our forecast, and much lower than the RBNZ's expectation.

Consumers Price Index, March quarter 2023

Quarterly change: +1.2% (prev: +1.4%)

- Westpac: +1.5%, RBNZ (February MPS): +1.8%

- Median market f/c: +1.5%, range +1.3% to +1.8%

Annual change: +6.7% (prev: +7.2%)

- Westpac: +6.9%, RBNZ: +7.3%, Market f/c: +6.9%

Key points

New Zealand consumer prices rose 1.2% in the March quarter, with prices up 6.7% over the past 12 months.

Today's result was lower than market expectations, and well below the RBNZ's forecast for a 1.8% rise.

Annual inflation remains painfully high. However, inflation looks like it has now peaked.

Core inflation, while still high, is not pushing higher.

Today's result supports our forecast for just one more OCR hike from the RBNZ in May.

Details

The March quarter saw large price swings in some specific areas:

- Food prices rose by 3.7% over the March quarter and are up a massive 11% over the past year. In part, that strength was due to disruptions stemming from January's storms and Cyclone Gabrielle, which resulted in significant damage to some crops. There have also been large increases in the prices of items like groceries (including eggs).

- March quarter inflation was also boosted by the annual increase in the tobacco excise tax, with cigarettes and tobacco prices up 7.6%.

- Providing some offset to those increases has been the fall in petrol prices, with prices at the pump dropping by around 2.6% in recent months.

But while there were some large swings in some specific prices, the big takeout for the BNZ was core inflation. The various measure of core inflation (which smooth through the quarter-to-quarter swings in prices and track the underlying trend in inflation) remain high at around 6%. Crucially, however, they are not continuing to push higher.

This is an important development for the RBNZ. Interest rates have been on the rise for over 18 months. Although price pressures still remain very strong, we're now seeing signs that the rise in prices is starting to lose some steam.

Digging under the surface, the March quarter saw softness in the prices of a range of imported durable items like furnishings. That's consistent with anecdotes from retailers of softening demand.

Looking across the broad product groups, domestic (or non-tradable) prices were up 1.7% in the March quarter and have risen by 6.8% over the past year. That's still very strong, but lower than the RBNZ had expected.

Prices for imported goods (sometimes referred to as tradables) rose by 0.7% over the past three months and are up 6.4% over the past year. That's a big step down from the rates we saw earlier in the year.

What does today's result mean for the RBNZ?

We're forecasting another 25bp increase in the Official Cash Rate at the RBNZ's May policy meeting. Inflation is still running red-hot and it remains well outside the central bank's target range.

However, it's looking increasingly likely that May will be the last rate hike in the current cycle. Inflation has fallen well short of the RBNZ's forecasts for a second quarter, and there are signs that underlying inflation pressures have peaked and may be starting to ease. Those developments come on top of softening demand in sectors such as construction. Together these are important indications that the policy tightening over the past 18 months is at last having the intended dampening effect.

More details to follow in our Bulletin later today.

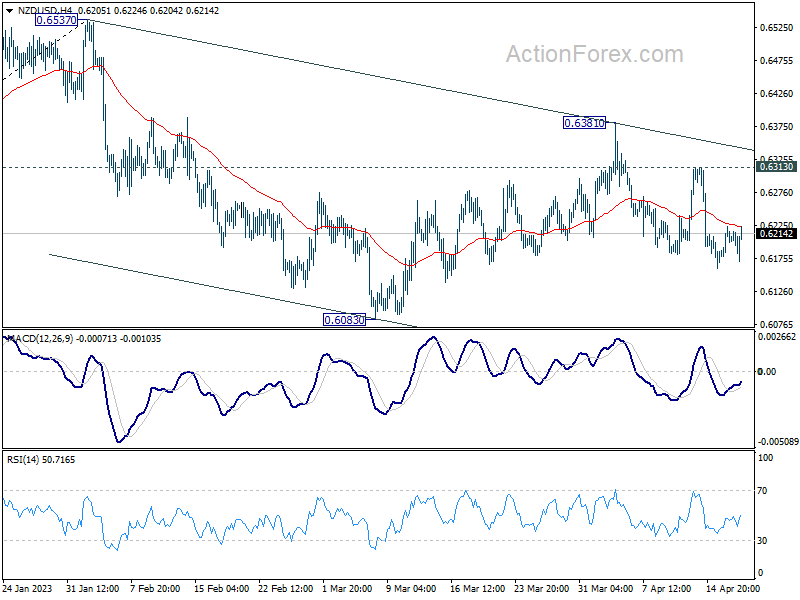

New Zealand Q1 CPI in Focus, NZD/USD in decline with weak momentum

Attention will turn to New Zealand's Q1 in the upcoming session. Consensus expectations suggest that CPI will slow from Q4's 7.2% yoy, with the majority of forecasts range from 6.9% to 7.1% yoy. Realizing such figures would present a downside surprise for RBNZ, which had projected a Q1 inflation rate of 7.3% yoy. With further slowing expected in subsequent quarters, the case for the RBNZ to pause at a terminate rate of 5.50% rate after another 25bps hike in May would strengthen if inflation indeed begins to cool.

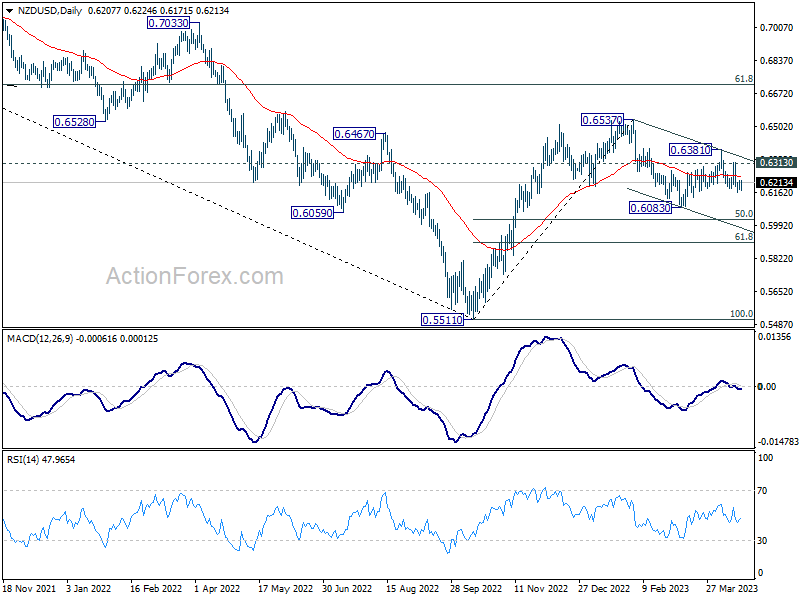

From a technical perspective, NZD/USD's decline from its February high of 0.6537 is viewed as a correction to the uptrend originating from the 2022 low of 0.5511. The corrective structure of the bounce from 0.6083 to 0.6381 suggests the decline isn't over yet. As long as the 0.6313 resistance holds, a deeper fall remains favored.

However, it's worth noting that downside momentum has been relatively weak thus far. Consequently, even if the rate dips below 0.6083, strong support could emerge around 50% retracement of 0.5511 to 0.6537 at 0.6024, potentially completing the correction and forming a base.

New Zealand Dollar Eyes Fourth-Quarter Inflation

- New Zealand’s inflation estimate for Q1 stands at 7.1%

- Fed’s Bostic expects one more rate hike

- NZD/USD showing limited movement

New Zealand inflation expected to remain above 7%

New Zealand releases inflation for the first quarter later today. It has been a light data week so far in both New Zealand and the US, which explains why NZD/USD is almost unchanged this week. That could change in a hurry following the inflation report, which should be treated as a market-mover.

Inflation has barely budged over the past few months, despite relentless interest rate hikes from the central bank. CPI came in at 7.2% y/y in both the third and fourth quarters of 2022 and is projected to inch lower to 7.1% in Q1. Reserve Bank of New Zealand Governor Orr can’t be blamed for not being aggressive against inflation, as he has raised rates to 5.25% in the current rate-hike cycle, the highest level amongst the major central banks.

The RBNZ shocked the markets earlier this month when it delivered a 50-basis point hike, as the markets had expected a modest 25-bp move, given a lackluster New Zealand economy. The oversize rate hike isn’t expected to have much impact on the upcoming inflation release. Economists will explain that it takes time for the rate hikes to percolate through the economy, but that is cold comfort for households who are struggling with rising mortgage payments but not seeing any improvement in red-hot inflation. The fight to contain inflation has been slow to show results and RBNZ policy makers will be hoping for a lower reading than the 7.1% consensus estimate.

In the US, the Fed is widely expected to raise rates next month, with an 84% probability according to the CME Group. On Tuesday, Fed member Bostic said that he expects one more rate hike in May and then a hold policy all the way into 2024. The markets are more dovish and anticipate rate cuts before the end of this year due to the economy continuing to weaken as the rate hikes make themselves felt and dampen economic activity.

NZD/USD Technical

- NZD/USD is testing support at 0.6213. Below, there is support at 0.6127

- 0.6289 and 0.6368 are the next resistance lines

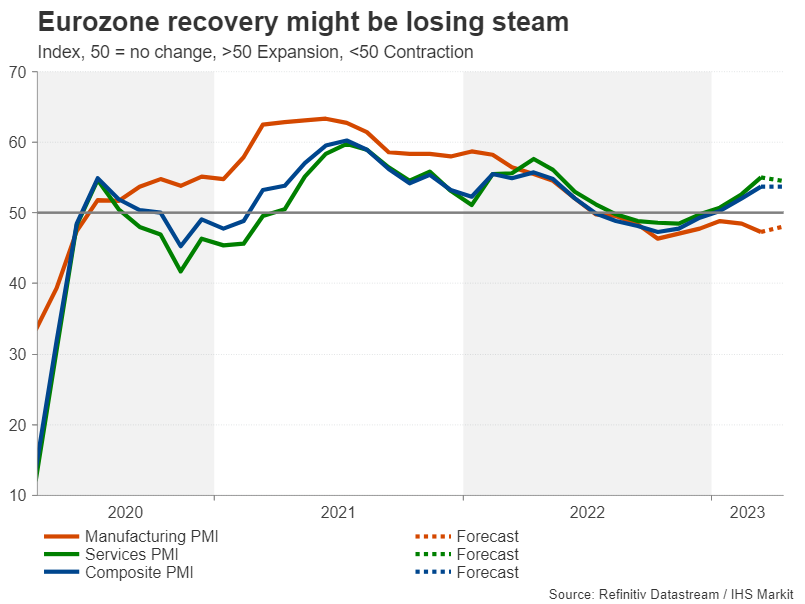

Eurozone PMIs Eyed as ECB Ponders Size of Next Rate Hike

Having defied recession predictions, the Eurozone economy will attract some headlines on Friday when the latest flash PMI readings are due (08:00 GMT). Growth in the euro area has been slowly gaining momentum since late 2022 when the impact of the energy crisis started to dissipate. But there are some doubts as to how strongly the economy can bounce back when interest rates continue to go up. With the European Central Bank’s next policy decision approaching, how important will the data be, and can it help the euro make a convincing break above $1.10?

Relief as Europe avoids a recession

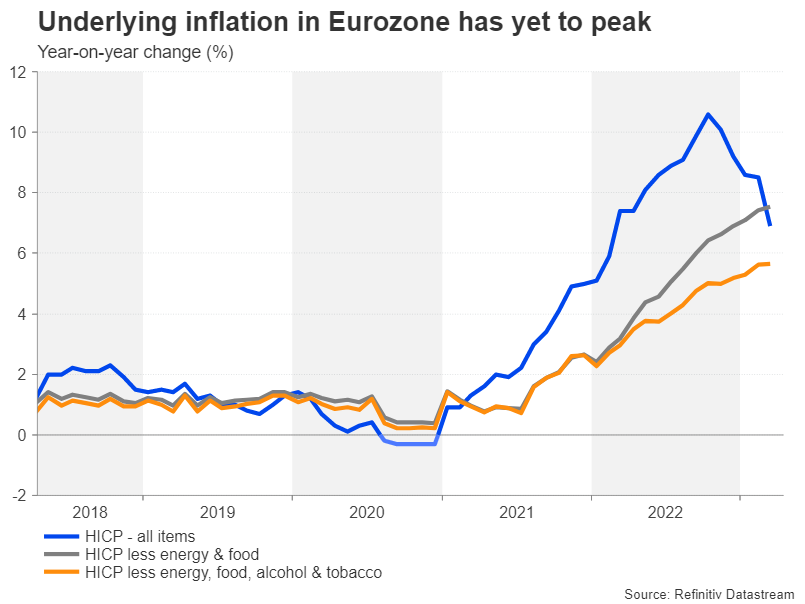

Summer is just around the corner and it’s looking like European economies managed to exit the winter season with only a few minor bruises. Yes, energy bills remain too high for most households and businesses and higher prices in general have been a heavy burden, hampering growth. But inflation in the euro area is on its way down and a recession isn’t on the near-term horizon.

However, the ECB is not done raising rates and growth has been quite sluggish in the last three quarters, so a brighter outlook is far from certain. The most pressing issue for policymakers is the stickiness in core inflation (excluding food, energy, alcohol & tobacco prices), which currently stands at 5.7%.

But more rate hikes to come

Given all the hawkish soundbites coming from the Governing Council, it’s clear that the ECB won’t be satisfied until underlying price indicators have made more progress in edging closer to the 2% target. At the moment, the Eurozone’s two core inflation measures have yet to show a definite sign of having peaked, despite the significant drop in headline CPI in recent months.

What this means is that a 50-basis-point rate hike is essentially at play at the May 4 policy meeting. It wasn’t so long ago in the aftermath of the banking turmoil that investors had priced out the likelihood of large rate increases. But recent remarks from policymakers suggest that the option is firmly on the table in May and Friday’s data may help sway some minds.

Risk of growth stagnating again

After an impressive rebound, the services sector might have lost some steam in April as analysts expect the services PMI to edge lower slightly from 55.0 to 54.5. Any figure above 50 indicates expansion and that hasn’t been the case for the manufacturing sector. Weak domestic and overseas demand have been a drag on business orders, but the manufacturing PMI is forecast to improve somewhat to 48.0 in April from 47.3 previously. This modest uptick is expected to keep the composite PMI unchanged at 53.7.

There are other data coming up ahead of the May decision that will be important, particularly the flash CPI numbers on May 2. But the PMI surveys will nevertheless offer a crucial insight on how well optimism is holding up, as well as the direction the various components such as input prices and employment are headed in.

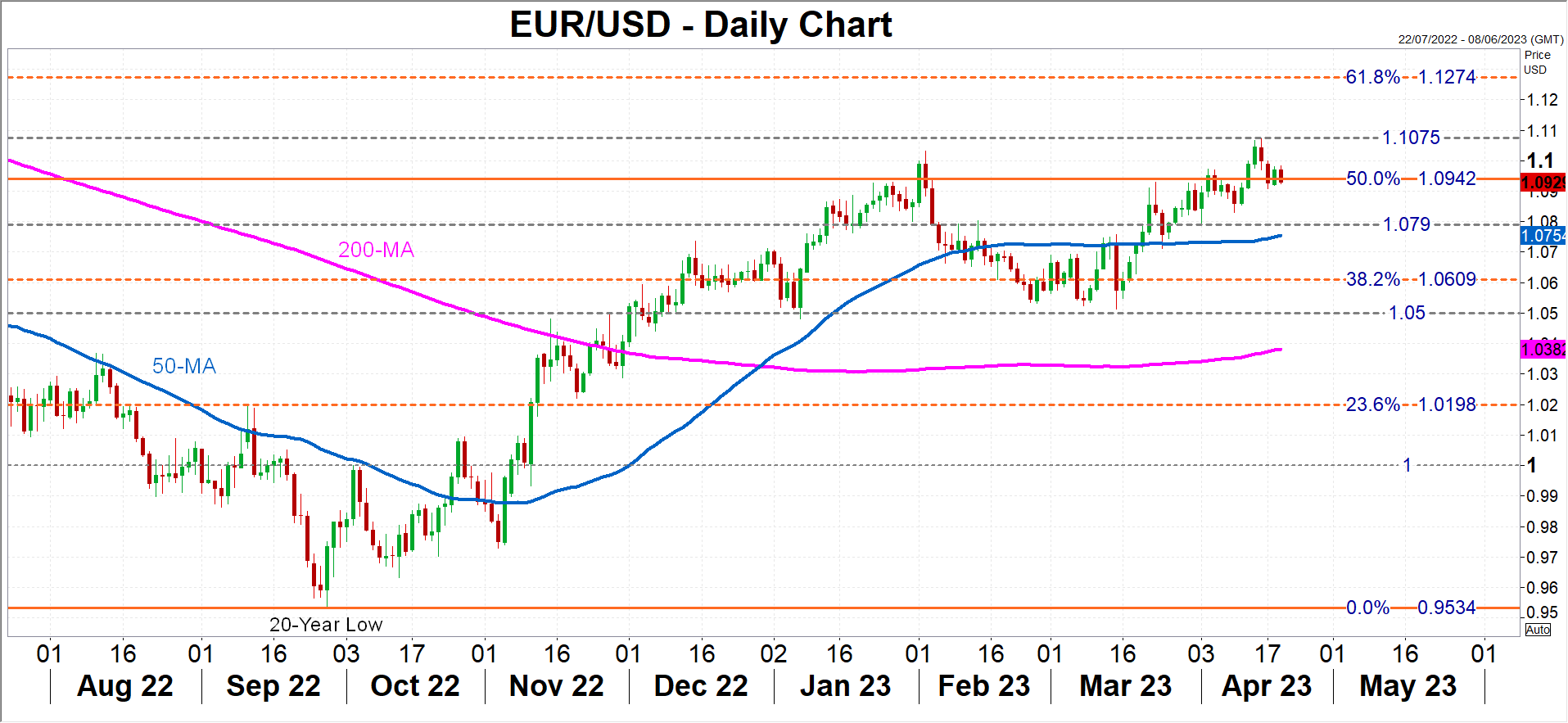

Euro outlook positive amid hawkish ECB, soft dollar

Stronger-than-expected PMI figures could push up bets for a 50-bps hike at the next meeting, which at the moment is only about 35% priced in, setting the stage for another leg up for the euro. The single currency suffered a mild pullback after hitting a wall at $1.1075. Hawkish expectations could enable a break above this key resistance, bringing the 61.8% Fibonacci retracement level of the 2021-2022 downtrend at $1.1274 into view.

However, any disappointment in the PMI indicators may facilitate a deeper downside correction, forcing the 50% Fibonacci to give way. Immediate support is likely to form in the $1.0750-$1.0790 region, comprising the 50-day moving average and a recent congestion point, after which, the $1.05 level would come into focus.

Yet, traders should be wary about anticipating an even sharper slide, as in the bigger picture, the US dollar’s heydays seem to be over. Yield spreads between US and European government bonds have been steadily narrowing over the past few months amid the growing expectation that the Fed will pause its tightening cycle before the ECB does. Unless that view starts to alter, the euro’s downside will be limited.

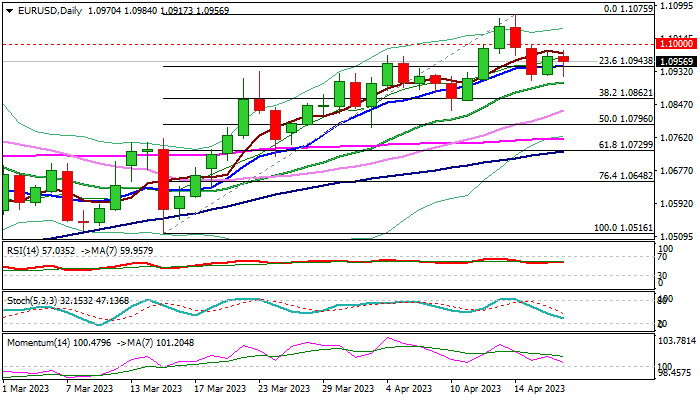

EUR/USD: Euro Looks for Fresh Direction Signals

The Euro remains constructive and returns above 10DMA (1.0947) in early US session, but continues to move within 1.1000/1.0910 congestion, which extends into third straight day.

Eurozone March inflation report showed persistently high underlying inflation which adds to expectations of more than one ECB rate hike in coming months and offers support to the single currency.

Renewed risk appetite started to fade and weigh on recovery attempts, along with weakening positive momentum on daily chart, although overall bullish structure is expected to remain intact while the price stays above 20DMA (1.0902), but sustained break above psychological 1.10 barrier needed to shift focus to the upside.

Caution on break of 20DMA, with stronger bearish signal expected on break below pivotal Fibo support at 1.0862 (38.2% of 1.0516/1.1075).

Res: 1.1000; 1.1041; 1.1075; 1.1100.

Sup: 1.0902; 1.0862; 1.0831; 1.0796.

Sunset Market Commentary

Markets

The reaction to strong data UK labour data yesterday was mainly confined to underperformance of UK gilts and an unconvincing attempt of sterling to profit from a rising interest rate support. With few other data or eco news in the US and Europe, the impact of higher than expected UK price data this time also left its traces outside the UK. The monthly dynamics of headline inflation hardly slowed (0.8% M/M from 1.1%) keeping the Y/Y measure north of 10% (10.1% from 10.4% vs 9.8% expected). The rise was still broad-based with subcategories food, alcohol & tobacco, clothing & footwear, household goods, recreation and restaurants & hotels all showing a monthly rise of 1.0%+. Core inflation was unchanged at 6.2%. So, the cycle peak reached in autumn last year (6.5%) still isn’t that far behind. In the March policy statement, the BoE made further tightening conditional on evidence of more persistent inflationary pressures, ‘including the tightness of labour market conditions and behaviour of wage growth and services inflation’. After yesterday’s and today’s data, this condition is (more than) fulfilled. A May 11 rate hike is now fully discounted an markets see the BoE peak cycle policy rate close to 5.0% in September. UK government bond yields add between 10 bps (2-y) and 7.0bps (30-y) (was more intraday). Sterling strengthened below EUR/GBP 0.88 after the release, but again still struggles to hold on to these gains (currently near 0.8805). The UK data also provided a reality check for global (interest rate) markets. US yields add between 4.5 bps (2-y) and 2 bps (30-y), with key resistance at 4.26% (2y) and 3.64% now under test intraday. German yields in a similar move are rising between 5.4 bps (2-y) and 1.6 bps (30-y). The prospect a further/long-lasting tightening also dampened stock market sentiment, but for now losses remain contained (Euro Stoxx 50 -0.2%). Higher core yields and a hesitant risk sentiment slightly favour the dollar. DXY trades near 101.90 from 101.70 this morning. EUR/USD slipped from the 1.0970/80 area this morning to current currently trade near 1.095. Even gains in USD/JPY (134.4) stay modest. Among the smaller currencies, underperformance of the Canadian dollar (USD/CAD 1.343) and the Norwegian krone (EUR/NOK 11.55) is catching the eye as oil dropped from near $85 p/b to the low $83 area.

In central Europe, the forint at some point ceded about 2.0%. Vice governor Virag of the Hungarian central bank (MNB) overnight in an interview signaled that recent improvement in sentiment opened the way to start policy normalization. The multi-step move might already include a reduction in the top of the rate corridor (currently 25%) next week. A reduction in the key 18% deposit rate can be put on the agenda of subsequent policy meeting. Inflation in Hungary still printed at 25.2% Y/Y in March but Vice governor Virag indicated this was expected and still expects a sharp disinflation later this year. At EUR/HUF 376 the forint currently recouped part of the early losses.

News & Views

Swiss National Bank governing board member Maechler commented on the central bank’s latest inflation forecasts (March 23). “We use the conditional inflation forecast as an important communication tool. Even with our last 50 bps rate hike, we only get down to exactly 2% by the end of the forecasting horizon (2025)”. It signals that another rate increase at the June 22 policy meeting will be needed to bring inflation fully under control. SNB chair Jordan last Friday also suggested that more tightening is possible. SNB vice-chair Schlegel is scheduled to speak after European close tonight. The Swiss franc doesn’t move today with EUR/CHF trading around 0.9830. The SNB warned in March that it is actively preventing the currency from becoming too weak as it interferes with actions taken via policy rates to achieve a tighter monetary framework and curb inflation.

Bloomberg cites sources close to the Bank of Japan in an article suggesting that the first meeting under new governor Ueda won’t bring any changes (to yield curve control) so soon after the banking crisis overseas which clouded the economic outlook. There’s a preference to keep current yield caps in place to support the economy while buying some more time on how inflation’s behaving. BoJ governor Ueda in an earlier appearance before parliament also hinted to a preference to stick with current monetary policy settings for the time being. JPY was losing ground against the dollar, touching the psychologic 135 barrier. The move didn’t persist with the greenback coming under pressure as the US trading session got started.