Sample Category Title

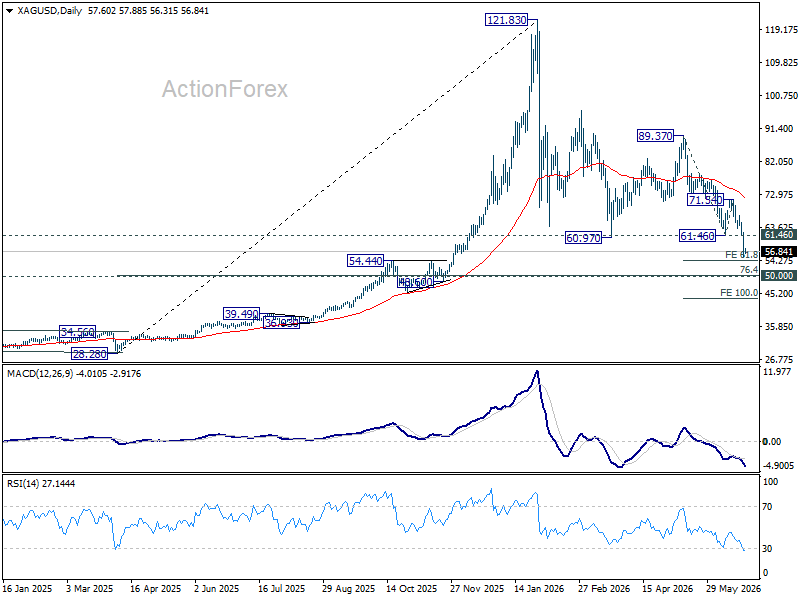

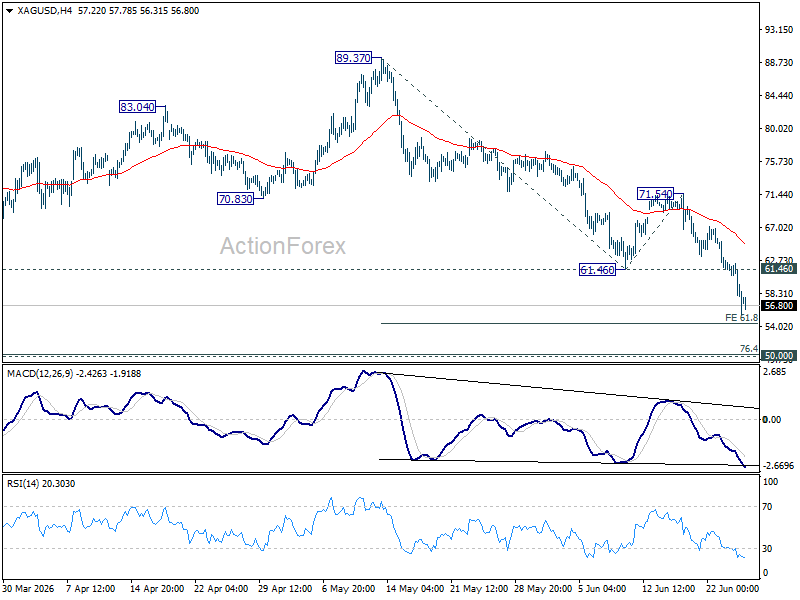

Silver Breaks Below $60, Can $50 Hold?

The battle in Silver has entered a far more important stage. Breaking below $60 is psychologically significant, but the market's attention is already shifting to another level roughly ten dollars lower. Around $50 sits one of the strongest combinations of technical and fundamental support on Silver's chart. Whether that area survives the current wave of selling is now the center of focus.

The immediate culprit is the Dollar. As markets become increasingly convinced that the Federal Reserve is returning to tightening, capital has continued flowing into the Greenback at the expense of precious metals. The debate has evolved rapidly over the past week. Deutsche Bank now expects two Fed rate hikes this year, in September and December. BofA has gone even further, forecasting hikes in September, October and December, making it the most hawkish major Wall Street house. Even though both banks expect the Fed to pause throughout 2027, the prospect of several more hikes this year has been enough to send Dollar sharply higher and precious metals sharply lower.

The Case for $50 Holding

For Silver, attention is rapidly shifting from the break below $60 to whether the much more important $50 area can withstand the current selling pressure. From a technical angle, there is a compelling argument that it should. The region lies within the fourth-wave consolidation (48.60 to 54.44) of the five-wave advance from the 2025 low at 28.28 to the record high at 121.83. It also coincides closely with the 76.4% retracement of that rally at 50.35, creating an important cluster of long-term support.

Fundamentally, Silver also enjoys an advantage that Gold does not. While both metals are suffering from higher real yields and a stronger Dollar, Silver remains a critical industrial commodity. The market is expected to record a sixth consecutive annual structural supply deficit, while demand from AI data-center construction, electric vehicles and renewable energy projects continues to provide longer-term support. Those structural drivers suggest buyers could emerge around the $50 area even if prices briefly trade below that level.

The Risks to the $50 Floor

However, downside risks remain significant. Gold has already broken below the key $4,000 psychological threshold for the first time since late last year, and further weakness there would likely drag the entire precious metals complex lower. In addition, a sharper-than-expected slowdown in global growth caused by tighter Fed policy could erode Silver's industrial demand premium. In a hard-landing scenario, Silver could behave more like base metals such as copper and zinc than a traditional precious metal.

Technically, next near term target for Silver is 61.8% projection of 89.37 to 61.46 from 71.54 at 54.29. Selling pressure may begin to moderate below that level as bargain hunters return, potentially establishing a medium-term trading range between 50 support and the former support at 61.46, now resistance.

But if downside momentum accelerates through 54.29 and ultimately breaks the 50 support cluster decisively, the 100% projection at $43.63 would come firmly into view, signaling that the longer-term correction has entered a much deeper phase.

BoJ’s Tamura Lays Out Tightening Roadmap to 2%

Bank of Japan board member Naoki Tamura laid out his clearest roadmap yet for further policy normalization on Thursday, saying the central bank's baseline should be to raise interest rates by 25 basis points every few months until the policy rate reaches around 2%, which he views as a neutral level. Tamura said, "what I envisage as a baseline path is raising the policy interest rate by 0.25 percentage points at intervals of a few months toward the neutral interest rate level of 2 percent," highlighting the BoJ's increasingly hawkish stance following last week's rate hike to 1.0%.

Tamura argued that inflation risks have become more pronounced, with underlying inflation already reaching the Bank's 2% target and inflation expectations continuing to rise. He noted that companies are passing on higher import costs "more quickly, significantly and broadly" than after Russia's invasion of Ukraine in 2022, reflecting a structural shift in corporate pricing behavior. While the conflict in the Middle East has contributed to higher energy costs, he stressed that upside inflation risks warrant attention regardless of how the geopolitical situation evolves.

Tamura also left the door open to a faster pace of tightening if inflation pressures prove more persistent. "If the chance of upside price risks materializing heightens, it's necessary to accelerate the pace of rate hikes without hesitation by increasing the frequency or size of rate hikes," he said. Although Tamura is widely regarded as one of the BoJ's most hawkish policymakers, his remarks reinforce the message from last week's policy meeting and Wednesday's Summary of Opinions that the debate within the Board has shifted firmly toward how quickly, rather than whether, rates should continue moving higher.

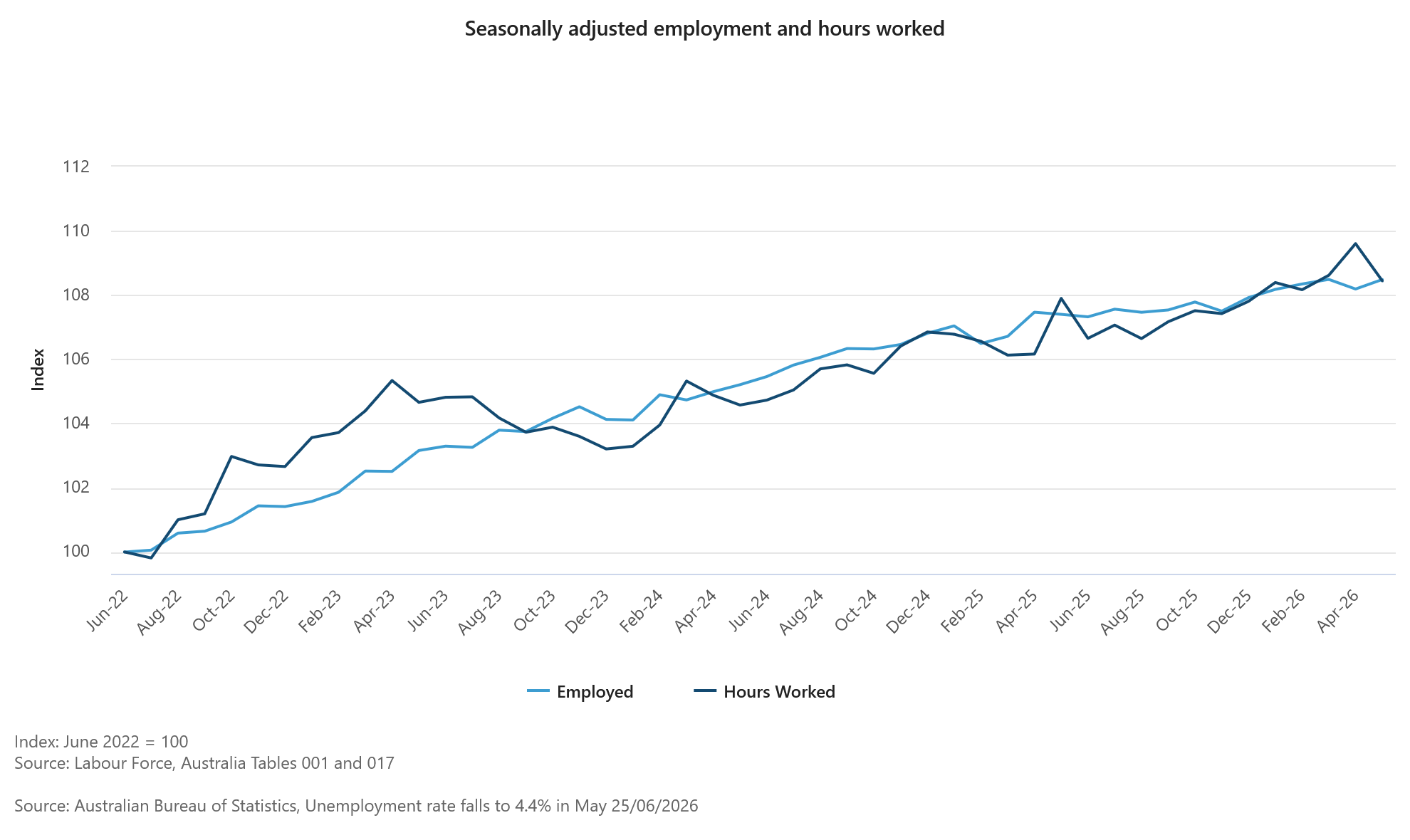

Australia Employment Beats Forecasts, But April Revision Tempers Strength

Australia's labor market rebounded in May, with employment rising by 40.3k, above expectations of a 30.5k increase, while the unemployment rate edged down from 4.5% to 4.4% as expected. The participation rate also ticked higher from 66.6% to 66.7%, pointing to resilience in labor supply. However, the headline gain was partly offset by a sharp downward revision to April's figures, with the previously reported -18.6k decline revised to a much steeper -40.7k contraction.

The composition of employment growth was also mixed. Full-time employment increased by just 5k, while part-time positions accounted for the bulk of the recovery with a 35k gain. Meanwhile, monthly hours worked fell -1.1% mom after rising 0.9% mom in April, suggesting overall labor demand was softer than the headline employment figures alone might indicate.

ABS head of labor statistics Sean Crick said the rebound reflected an easing in the backlog of unemployed people waiting to start new jobs. "Over the past few months, we have recorded higher proportions of unemployed people waiting to start jobs who then remained unemployed in the following month," he said. "The backlog of people waiting to start a job has eased in May, contributing to the 40,000 rise in employment and 18,000 fall in unemployed persons."

Crick also noted that April's unusually strong hours worked reflected fewer people taking Easter leave, with May's decline bringing hours worked "back in line with employment growth since the end of the pandemic in June 2022."

Overall, the report suggests the labor market remains relatively resilient, but softer hours worked and the large revision to April may temper expectations of a significantly stronger labor market.

Data Summary Table

| Indicator | April | May | Expectation |

|---|---|---|---|

| Employment Change | -40.7k (revised from -18.6k) |

+40.3k | +30.5k |

| Unemployment Rate | 4.5% | 4.4% | 4.4% |

| Participation Rate | 66.6% | 66.7% | |

| Monthly Hours Worked | +0.9% m/m | -1.1% m/m |

Employment Breakdown

| Category | May Outcome |

|---|---|

| Total Employment | +40.3k |

| Full-time Jobs | +5.0k |

| Part-time Jobs | +35.0k |

| Unemployed Persons | -18.0k |

| Participation Rate | Increased to 66.7% |

Back to the Future: RBNZ to Scale Back OCR Hikes as Energy Price Worries Recede

- Recent developments mean that the RBNZ's outlook for the OCR has likely moved back towards that forecast in the February MPS.

- We are similarly updating our forecasts to reflect the unexpectedly quick resolution of the Iran conflict and associated significant decline in the price of oil and refined fuels prices and related commodities.

- We now see headline inflation peaking at 4.0% in the June quarter this year and ending 2026 at 3.5% - possibly lower if the most recent fall in oil prices is sustained.

- We have marked up our 2026 GDP growth forecast to 2.0% from 1.5% previously, although this remains lower than our pre-war forecast.

- We affirm our view that the OCR will be held at 2.25% at the upcoming 8 July meeting. Indeed, we expect this decision to be far less contentious than in May, and don't rule out that this decision is made by consensus and so without a vote.

- We also affirm our view that the RBNZ will begin to tighten at the September MPS. However, beyond September, we now expect just one further tightening this year - rather than two - which will probably occur at the December MPS meeting.

- Relative to pre-conflict forecasts made by both Westpac and the RBNZ, this implies one extra OCR increase in 2026. This is justified by the more elevated path for inflation relative to that expected in early 2026.

- We have reduced the forecast peak in the OCR to 4% and thus retain the same pattern of OCR changes through 2027. A lower peak OCR is consistent with the smaller and shorter duration oil related supply shock now assumed.

- There are two-sided risks around this profile that depend on how quickly the economy recovers through the second half of 2026 and the pace at which underlying inflation pressures recede.

- Downside risks persist for the New Zealand dollar as interest rate differentials are likely to weigh on the exchange rate given much higher US and Australian policy rates. We will review our FX forecasts next month in the July Market Outlook produced jointly with our Australian colleagues.

A Revised Economic Outlook Is Warranted

A great deal has changed since early May when we last reviewed our forecasts for the global and domestic economies - more than the market appears to have appreciated considering the continued pricing of a RBNZ rate hike at next month's policy review. The key issue has been the unexpectedly quick progress on reducing Persian Gulf tensions and the potential for a faster return of shipping flows in the Strait of Hormuz, with resultant improvements in trade flows of oil, petrochemical products and natural gas, as well as a range of other key products (such as fertiliser).

While it is premature to conclude that tensions in the region will be durably settled, there are sufficient signs that diplomatic efforts are well underway such that a decent period of ceasefire and more normal shipping flows is in prospect. Hence, it's appropriate to incorporate this new information into our New Zealand macroeconomic view.

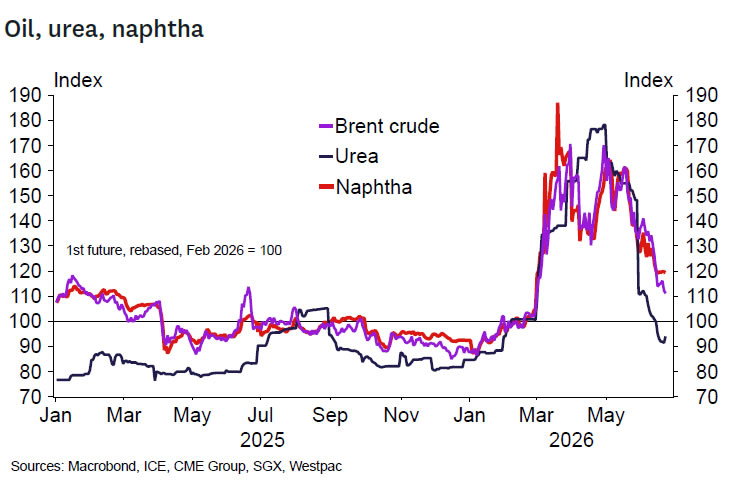

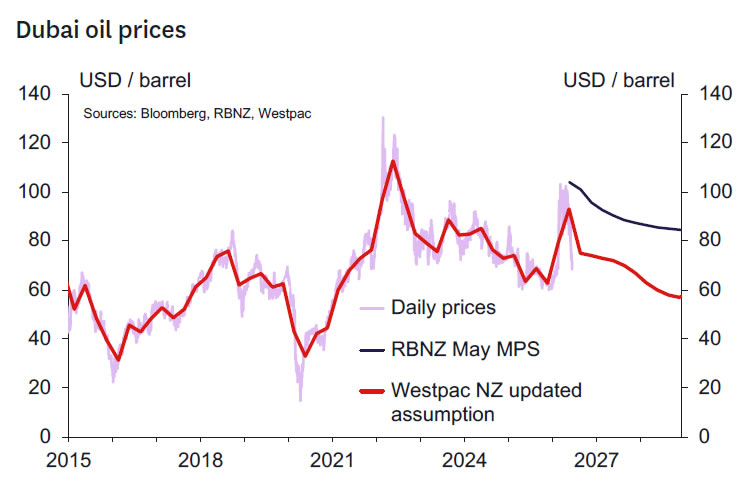

The key updates to our assumptions relate to the assumed level and future path for oil and refined fuels prices. These have converged much more rapidly than expected to levels we previously didn't expect to see until mid-2027. Brent crude oil is currently trading around US $73/bbl, close to the levels we saw prior to the war. We expect that prices will ease further over 2027 to $69/bbl. Refined fuels prices have been easing more gradually, but have still fallen substantially from a peak of US $195 bbl in March to US $110 bbl at the time of writing (vs around US $92/bbl prior to the war). Refined fuel prices are expected to continue easing back over the coming months, falling to US $102 bbl by the end of this year and US $90 bbl by the end of 2027.

Importantly, oil prices are now much lower than the RBNZ assumed in the May forecasts.

We have also accounted for recent economic data on GDP, selected price indices, and other higher frequency data on output when reviewing our economic view. We have not reviewed our global economic forecasts, or the exchange rate forecasts (aside from updating the starting point for the exchange rate) as these will next be reviewed, in conjunction with our Australian colleagues when we prepare our July Market Outlook publication forecasts.

We also have not included the implications of the new fiscal position revealed in Budget 26. Having said that we think the implications are likely modest and will be fully incorporated into our forecasts when we prepare our next Economic Overview in late August.

GDP Growth - Recovery to Resume Sooner

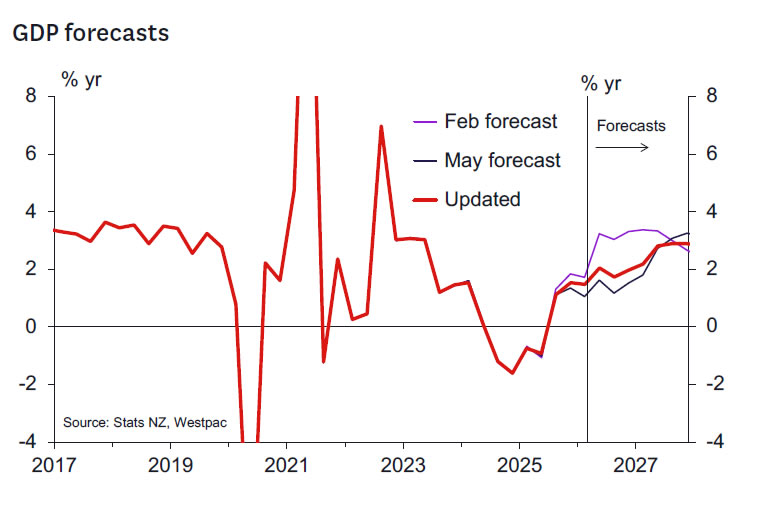

We have upgraded our GDP forecasts for both the June quarter - the peak of the oil shock impact - and over the second half of this year. Much of this reflects a bringing-forward of the timing of the economy's recovery as the oil shock fades, so we now expect a slightly slower rate of growth through 2027. GDP growth for 2026 is now forecast to be 2% and 2.9% in 2027.

A review of the most recent data suggests that the economy held its ground through the peak of the oil price shock in April and May, faring a bit better than we had assumed in our last forecast update. We now expect GDP to fall by just 0.1% for the June quarter, from our previous forecast of -0.3%.

We should note that both forecasts include an allowance for the seasonal distortions that remain an issue in the GDP data. Our new forecast implies an underlying growth pace of around +0.2%, with seasonal factors knocking 0.3% off the reported result.

With oil prices receding faster than we'd assumed, the economy is set to resume its pre-conflict recovery path sooner as well. We expect quarterly growth to pick up to 0.6% and 0.7% in the September and December quarters, from 0.4% and 0.6% previously. Altogether that would see the economy grow by 2.0% over the course of this year, compared to our previous forecast of 1.5%. That's still some way below the 3.3% growth that we were expecting this year prior to the Iran conflict, which will still prove to be a significant setback to the momentum that was otherwise building in the economy.

Labour Market - Hiring to Resume

With a stronger GDP outlook for this year, we now expect a lower peak and a quicker turnaround in the unemployment rate over the next year. We still expect some softness in the jobs market in the near term - the uncertainty generated by the Iran conflict has likely led some businesses to hold off on hiring decisions. The high-frequency jobs data so far suggests that we're on track for flat rather than falling employment over the June quarter. But that won't be enough to absorb the growth in the working-age population, so we expect to see the unemployment rate tick up again to 5.4% after having eased to 5.3% in the March quarter.

Beyond that though, we see less risk of a further rise in unemployment over the coming quarters. Our forecast now peaks at 5.4% through the middle part of this year, easing to 5.3% by year-end and 4.9% by the end of 2027 (the latter forecast is unchanged).

Housing - Still Moving Sideways

We have revised up modestly our forecasts for house price growth in 2026. Recent house price data confirms a flat profile for house prices in recent months and a similarly flat path for the days to sell a property. Looking forward, we anticipate a mildly more positive tone to return to the market as consumer and business sentiment improves with falling energy prices. Previously we had thought we might see a relatively weak outcome for September quarter house prices, but now it seems more like a flat outcome is closer to the mark. Weaker expectations for RBNZ OCR hikes have translated through to lower mortgage rates in recent weeks which should also assist sentiment.

We now expect very modest house price growth of 0.6% in 2026 (previously we expected a modest 1% fall). We still expect prices to rise by 2% over 2027. We continue to expect house prices in the regions to outperform those in the major North Island urban centres as it will take some time for the services sector to pick up and the labour market to strengthen to the point where we see a decent fall in the unemployment rate (now forecast to begin late in 2026 and picking up pace through 2027).

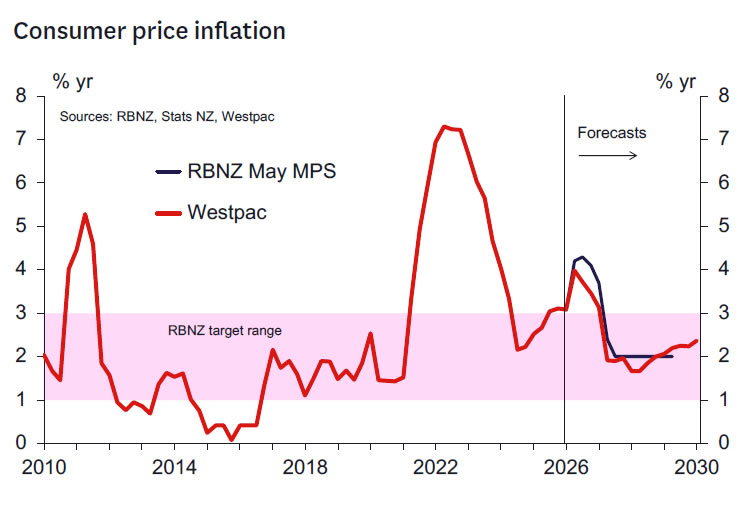

Inflation - Lower Peak, Quicker Reduction

In response to the faster than expected fall in oil prices, we have pulled down our inflation forecasts. We now expect that annual inflation will peak at 4.0% in the June quarter (down from the peak of 4.5% we assumed in our May forecasts), slowing to 3.5% in the December quarter - possibly lower if oil prices remain as low as they are today. That would be well below the 4.1% rate the RBNZ assumed for year-end inflation in its recent May MPS projections.

The earlier than expected fall in global oil prices has already flowed through to lower prices at the pump for New Zealand consumers. The average price of 91 unleaded around the country has fallen to $3.02/ltr (down nearly $0.50/ltr from its peak in May), while diesel has fallen to $2.56 (down more than $1/ltr). Further price falls are likely given current spot energy prices. Those lower oil prices have directly shaved about 0.5ppts off our year-end inflation forecasts.

We have also dialled back assumed second round inflation effects reflecting the smaller and shorter duration cost shock. That's taken about 0.2ppts off our inflation forecasts. We retain around 50% of the second-round effects included in previous CPI forecasts as although oil prices have fallen substantially, they are still well above the levels we saw prior to the conflict. We will review these estimates as we receive more definitive CPI data in coming quarters.

More generally, we think that subdued demand has constrained how far many businesses have been able to raise their prices despite increases in operating costs.

Looking to 2027, inflation is expected to drop back as the impact of the oil price shock dissipates. Indeed, given base effects associated with this year's oil shock, headline inflation will briefly dip below 2% in 2027, before rising as the economy recovers.

Smoothing through the volatility associated with fuel prices, core inflation has lingered at firm levels over the past few years despite the softness in economic activity. The average of the RBNZ's suite of core inflation measures sat at 2.3% in the March quarter. Inflation excluding food and fuel prices, is currently around 3% and it is expected to linger close to the top of the RBNZ target band for the remainder of this year, before easing over 2027.

Monetary Policy - Less Urgency Required

Our forecasts imply the RBNZ's outlook for the OCR will likely move back towards the economic outlook envisioned back at the February MPS (when the Bank expected at most one 25bp hike this year). This would imply much less urgency to raise the OCR compared to the view in the May MPS (which had assumed two to three 25bps hikes this year).

The key question is: just how far will the RBNZ have moved? We think it reasonable that the RBNZ will likely have taken at least one 25bp hike out of its internal projections and will likely now be projecting one to two 25bp OCR hikes this year. Hence, we don't think the RBNZ will have reverted all the way back to its pre-Iran war views - in part because the inflation outlook remains significantly elevated for a while yet relative to what the RBNZ expected back in February. But nevertheless, the significant shift in circumstances since May should imply a significant shift in the forward stance.

So, what does this imply for the upcoming 8 July meeting? We think that the sharp fall in energy prices and the resulting improvement in the inflation outlook will have undermined the case for pre-emptive action. The hawks on the MPC may well still see a strong case for OCR increases this year but will likely be significantly comforted by the big change in the immediate inflation outlook as it must imply lower risks of persistently high inflation. At the least, the argument for moving earlier will look a lot weaker than back in May when those views were ultimately outweighed by the dovish camp. There's a significant chance that the hawkish bloc opts for no change in the OCR in July while remaining open for OCR hikes later in 2026.

The more dovish MPC members that wanted to see more evidence of enduring second-round inflation impacts in May will likely have hardened their views. Indeed, with the key June CPI, labour market and QSBO reports all due between the RBNZ's July and September meetings, together with the next round of inflation expectations surveys, there seems little to be lost in waiting to see what these key reports reveal (and to see whether the current US-Iran negotiations progress to a durable final deal). We don't think we have learned much about the extent of second-round inflation impacts since May aside from the fact that the short-term inflation outlook now looks far less threatening than then. And of course, there is more tangible evidence the economy stalled in the June quarter (the RBNZ's June quarter Nowcast indicates flat Q2 growth). Looking ahead, as discussed previously, there are likely good reasons to expect a stronger H2 2026 growth performance than felt back in May, but this is likely to still need to be confirmed by data and still likely to be far weaker than hoped for in early 2026 when even then just one OCR hike for 2026 was said to be on the cards. We don't think that any of the doves are likely to want to shift camp to the hawk's side in the July meeting.

A key argument market participants seem to rely on is the sense that the RBNZ may have almost promised a July hike back in May. We don't think this is accurate as the MPC will always fiercely note that any forward guidance on the OCR will be data dependent. We understand that mathematically, the RBNZ May forecast for an average OCR for the September 2026 quarter at 2.51% seems consistent with a July hike. But this will not have been a non-data dependent promise. In most cases, the RBNZ's short term OCR forecasts provide broad guidance on the likely direction of the OCR rather than a definitive forecast and have historically proven to be a poor guide to the next policy decision. More importantly, the Governor's words when describing the outlook are likely to be more prescient. The Governor noted that an increase in the OCR seemed likely "in coming meetings" - this is not a promise of an OCR increase in July. This is rather an expression of the intention to lift the OCR later in the year - and even that intention will (and should!) be data dependent.

Therefore, we affirm our view that the RBNZ will hold the OCR at 2.25% at the 8 July meeting. In fact, we expect this to be far less contentious than the May decision, and do not rule out the possibility that this decision is reached by consensus and so without a vote.

Looking beyond July, it remains reasonable to expect the RBNZ to tentatively begin lifting the OCR at the September MPS meeting and move again once more towards neutral settings before the end of the year - most probably at the December MPS meeting. But even these forecasts are not a slam dunk and have two-sided risks. Should the June quarter CPI provide benign in terms of core inflation measures then the RBNZ could leave the OCR unchanged until December. If the CPI runs hot, then we could still see the three 25bp rate hikes that we forecast before today.

Our central view implies one fewer hike this year than we had forecast most recently but one more than we had forecast prior to the conflict. This is justified by the more elevated path for inflation relative to that expected in early 2026. We have retained the same OCR changes that we had previously forecast to occur in 2027 and so the OCR is now forecast to peak 25bps lower at 4.0%. A lower peak OCR is consistent with the smaller and shorter duration oil-related supply shock now assumed. Our view on the neutral OCR remains at 3.75%.

In this update we have made no change to our FX forecasts. Downside risks persist for the New Zealand dollar as interest rate differentials are likely to weigh on the exchange rate given much higher US and Australian policy rates. We will review our FX forecasts next month in the July Market Outlook produced jointly with our Australian colleagues.

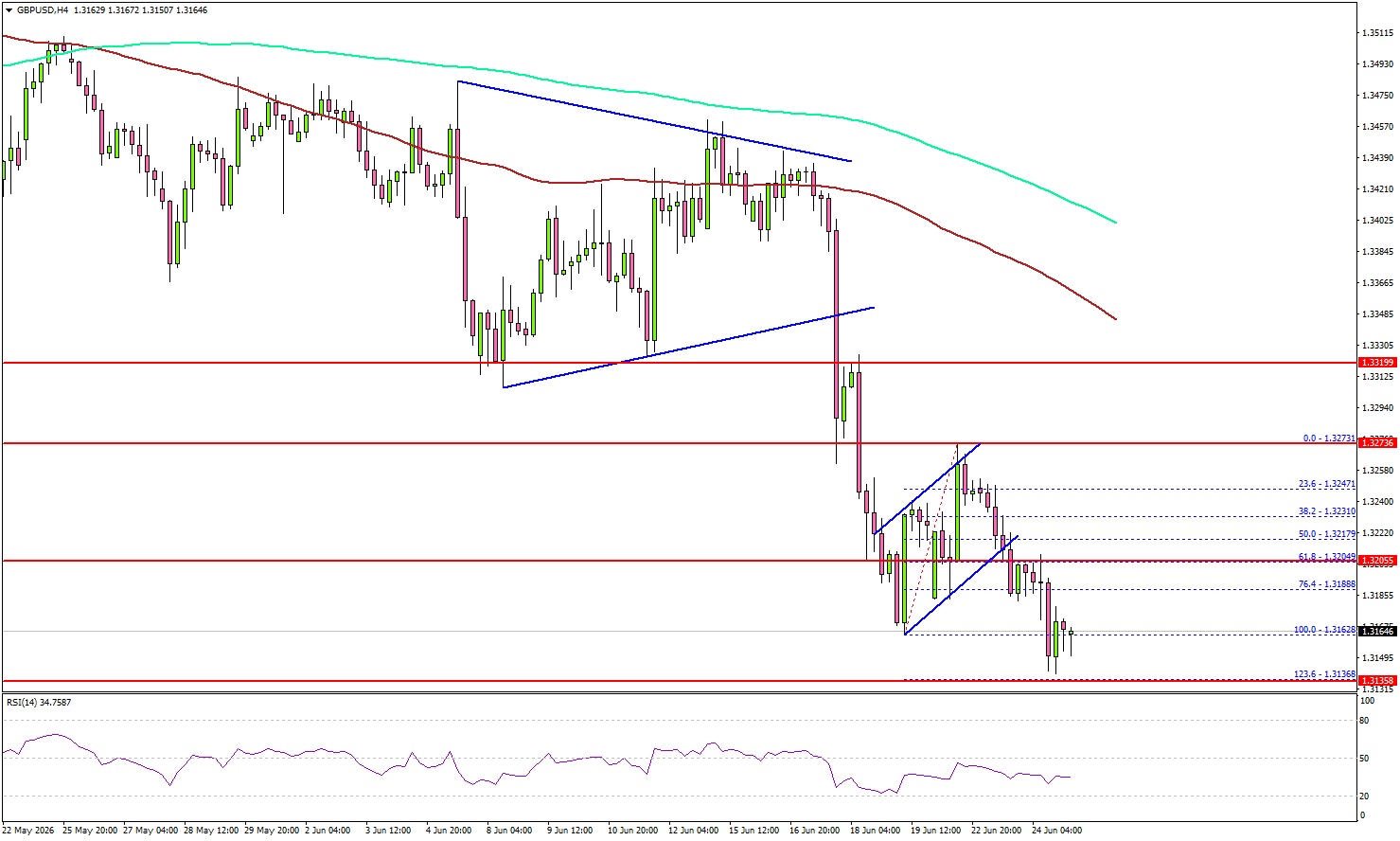

GBP/USD Back on the Defensive as US GDP Looms Large

Key Highlights

- GBP/USD extended losses and traded below 1.3200.

- The bears might remain active near 1.3200 and 1.3250 on the 4-hour chart.

- Gold prices declined sharply to a new multi-week low below $4,000.

- The US GDP could grow by 1.6% in Q1 2026.

GBP/USD Technical Analysis

The British Pound faced rejection near 1.3275 against the US Dollar. GBP/USD reacted to the downside and traded below 1.3200.

Looking at the 4-hour chart, the pair settled below 1.3200, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The bears even pushed the pair to a new multi-week low below 1.3150.

The greenback seems to be gaining strength ahead of the US GDP data. If the bears remain in action, the pair could dip further below 1.3120.

The first major support could be near 1.3050. The main support might be 1.3000. A downside break and close below 1.3000 might spark bearish moves. In the mentioned case, the bears could aim for a test of 1.2880.

If there is a recovery wave, GBP/USD could face resistance at 1.3200. The next major resistance might be 1.3250. A close above 1.3250 could open the doors for a larger increase. In the stated case, the bulls could aim for a move to 1.3350.

Looking at Gold, the bears remained in action, pushed the price below $4,000, and might continue to pressure the market in the near term.

Upcoming Key Economic Events:

- US Gross Domestic Product for Q1 2026 – Forecast 1.6% versus previous 1.6%.

- US Personal Income for May 2026 (MoM) - Forecast +0.4%, versus 0% previous.

- US Initial Jobless Claims - Forecast 225K, versus 226K previous.

- US Durable Goods Orders for May 2026 – Forecast -4.3% versus +8.0% previous.

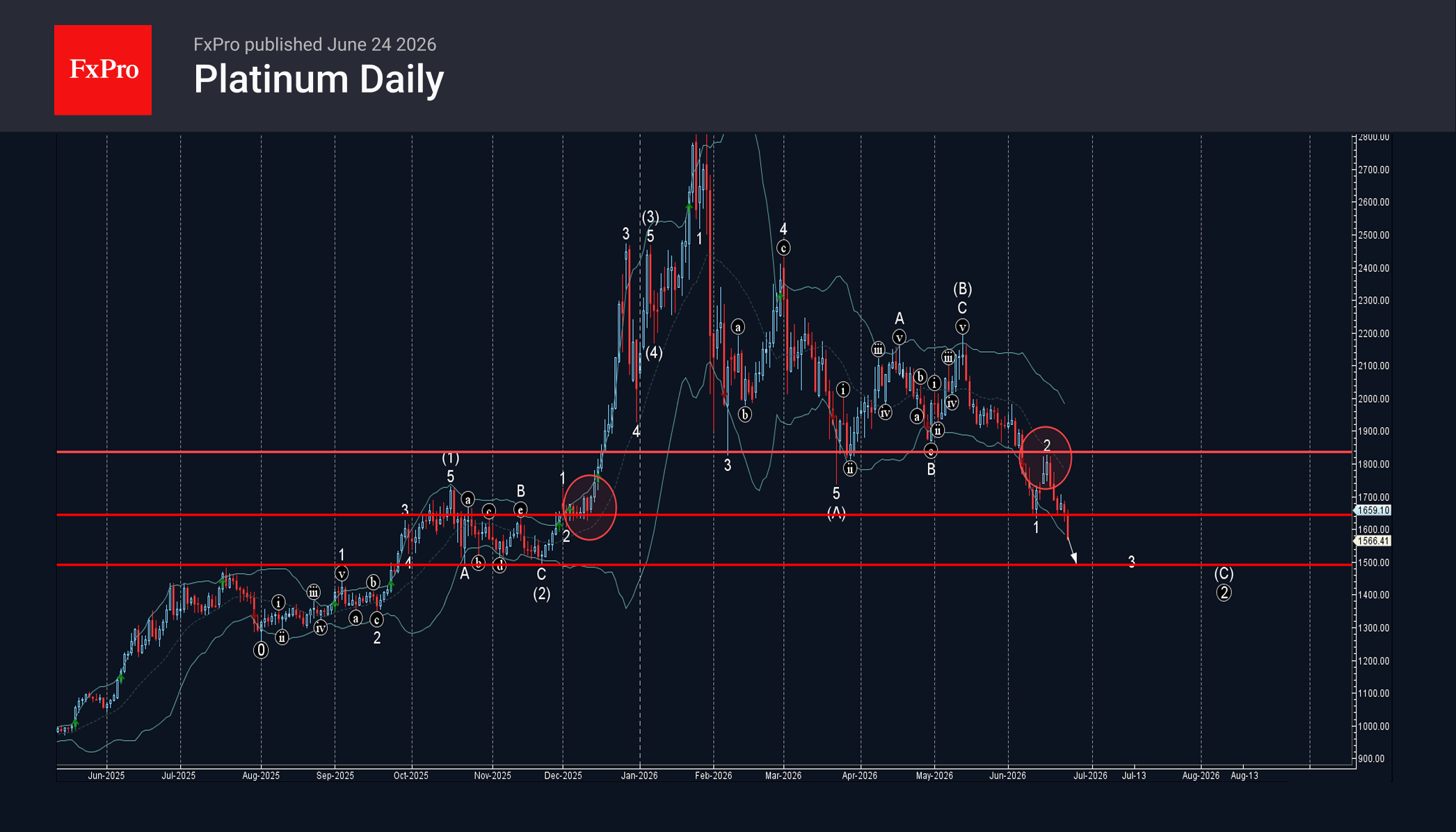

Platinum Wave Analysis

Platinum: ⬇️ Sell

– Platinum broke support level 1645.00

– Likely to fall to support level 1500.00

Platinum under the bearish pressure after the earlier breakout of the support level 1645.00, which has been reversing the price from December.

The breakout of the support level 1645.00 continues the active minor impulse wave 3 of the higher impulse wave (C) from May.

Given the strong daily downtrend, Platinum can be expected to fall to the next major support level 1500.00 (target for the completion of wave 3), which has been revering the price from October.

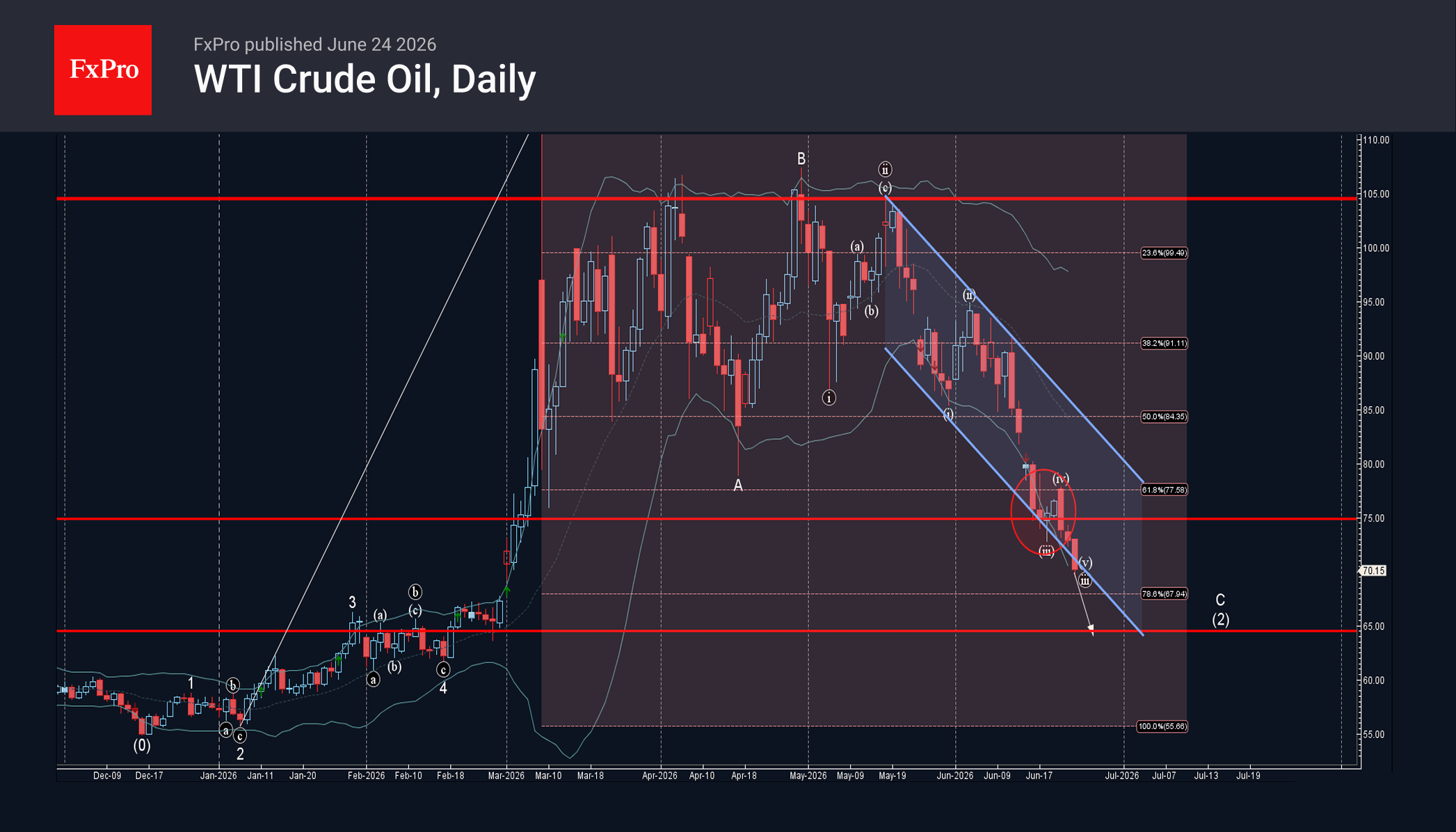

WTI Crude Oil Wave Analysis

WTI Crude Oil: ⬇️ Sell

– WTI Crude Oil broke support level 75.00

– Likely to fall to support level 65.00

WTI Crude Oil recently broke the support zone between the support level 75.00, support trendline of the daily down channel from May and the 61.8% Fibonacci correction of the upward impulse from January.

The breakup of this support zone accelerated the active impulse wave C of the intermediate ABC correction (2) from March.

WTI Crude Oil can be expected to fall further to the next support level 65.00 (target for the completion of the active impulse wave C).

Eco Data 6/25/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Employment Change May | 40.3K | 30.5K | -18.6K | -40.7K |

| 01:30 | AUD | Unemployment Rate May | 4.40% | 4.40% | 4.50% | |

| 06:00 | EUR | Germany GfK Consumer Confidence Jul | -29.2 | -28 | -29.8 | -29.7 |

| 12:30 | USD | Initial Jobless Claims (Jun 19) | 215K | 225K | 226K | 227K |

| 12:30 | USD | Personal Income M/M May | 0.70% | 0.40% | 0.00% | |

| 12:30 | USD | Personal Spending May | 0.70% | 0.60% | 0.50% | 0.40% |

| 12:30 | USD | PCE Price Index M/M May | 0.40% | 0.50% | 0.40% | |

| 12:30 | USD | PCE Price Index Y/Y May | 4.10% | 4.10% | 3.80% | |

| 12:30 | USD | Core PCE Price Index M/M May | 0.30% | 0.30% | 0.20% | |

| 12:30 | USD | Core PCE Price Index Y/Y May | 3.40% | 3.40% | 3.30% | |

| 12:30 | USD | Durable Goods Orders May | -4.50% | -4.70% | 8.00% | 8.50% |

| 12:30 | USD | Durable Goods Orders ex Transport May | 1.30% | 0.50% | 1.10% | 1.40% |

| 12:30 | USD | GDP Annualized Q1 F | 2.10% | 1.60% | 1.60% | |

| 12:30 | USD | GDP Price Index Q1 F | 3.60% | 3.50% | 3.50% | |

| 14:30 | USD | Natural Gas Storage (Jun 19) | 76B | 67B | 73B |

| 01:30 | AUD |

| Employment Change May | |

| Actual | 40.3K |

| Consensus | 30.5K |

| Previous | -18.6K |

| Revised | -40.7K |

| 01:30 | AUD |

| Unemployment Rate May | |

| Actual | 4.40% |

| Consensus | 4.40% |

| Previous | 4.50% |

| 06:00 | EUR |

| Germany GfK Consumer Confidence Jul | |

| Actual | -29.2 |

| Consensus | -28 |

| Previous | -29.8 |

| Revised | -29.7 |

| 12:30 | USD |

| Initial Jobless Claims (Jun 19) | |

| Actual | 215K |

| Consensus | 225K |

| Previous | 226K |

| Revised | 227K |

| 12:30 | USD |

| Personal Income M/M May | |

| Actual | 0.70% |

| Consensus | 0.40% |

| Previous | 0.00% |

| 12:30 | USD |

| Personal Spending May | |

| Actual | 0.70% |

| Consensus | 0.60% |

| Previous | 0.50% |

| Revised | 0.40% |

| 12:30 | USD |

| PCE Price Index M/M May | |

| Actual | 0.40% |

| Consensus | 0.50% |

| Previous | 0.40% |

| 12:30 | USD |

| PCE Price Index Y/Y May | |

| Actual | 4.10% |

| Consensus | 4.10% |

| Previous | 3.80% |

| 12:30 | USD |

| Core PCE Price Index M/M May | |

| Actual | 0.30% |

| Consensus | 0.30% |

| Previous | 0.20% |

| 12:30 | USD |

| Core PCE Price Index Y/Y May | |

| Actual | 3.40% |

| Consensus | 3.40% |

| Previous | 3.30% |

| 12:30 | USD |

| Durable Goods Orders May | |

| Actual | -4.50% |

| Consensus | -4.70% |

| Previous | 8.00% |

| Revised | 8.50% |

| 12:30 | USD |

| Durable Goods Orders ex Transport May | |

| Actual | 1.30% |

| Consensus | 0.50% |

| Previous | 1.10% |

| Revised | 1.40% |

| 12:30 | USD |

| GDP Annualized Q1 F | |

| Actual | 2.10% |

| Consensus | 1.60% |

| Previous | 1.60% |

| 12:30 | USD |

| GDP Price Index Q1 F | |

| Actual | 3.60% |

| Consensus | 3.50% |

| Previous | 3.50% |

| 14:30 | USD |

| Natural Gas Storage (Jun 19) | |

| Actual | 76B |

| Consensus | 67B |

| Previous | 73B |

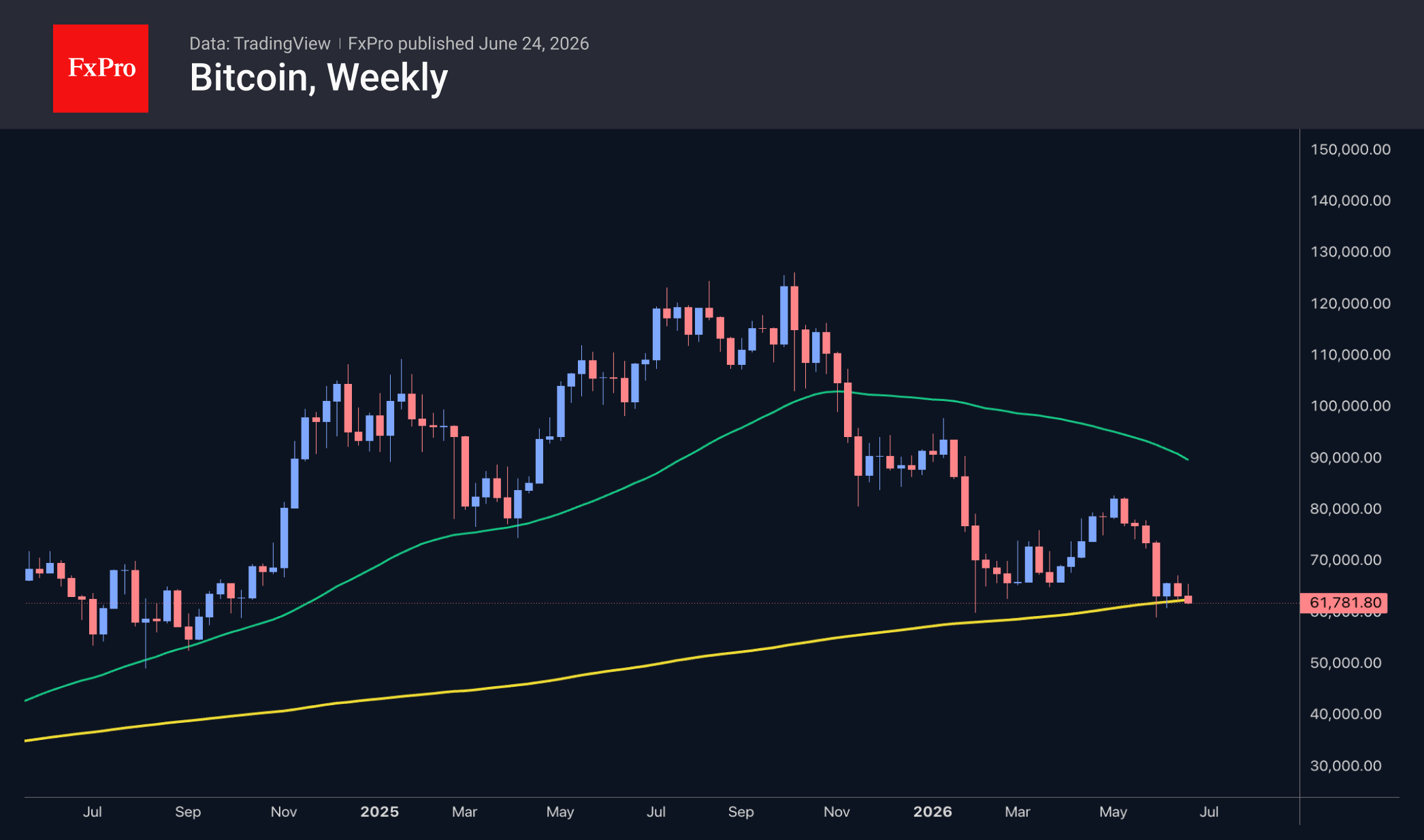

Bitcoin at the 200-Week Ma Hints at a Long Winter

Market Overview

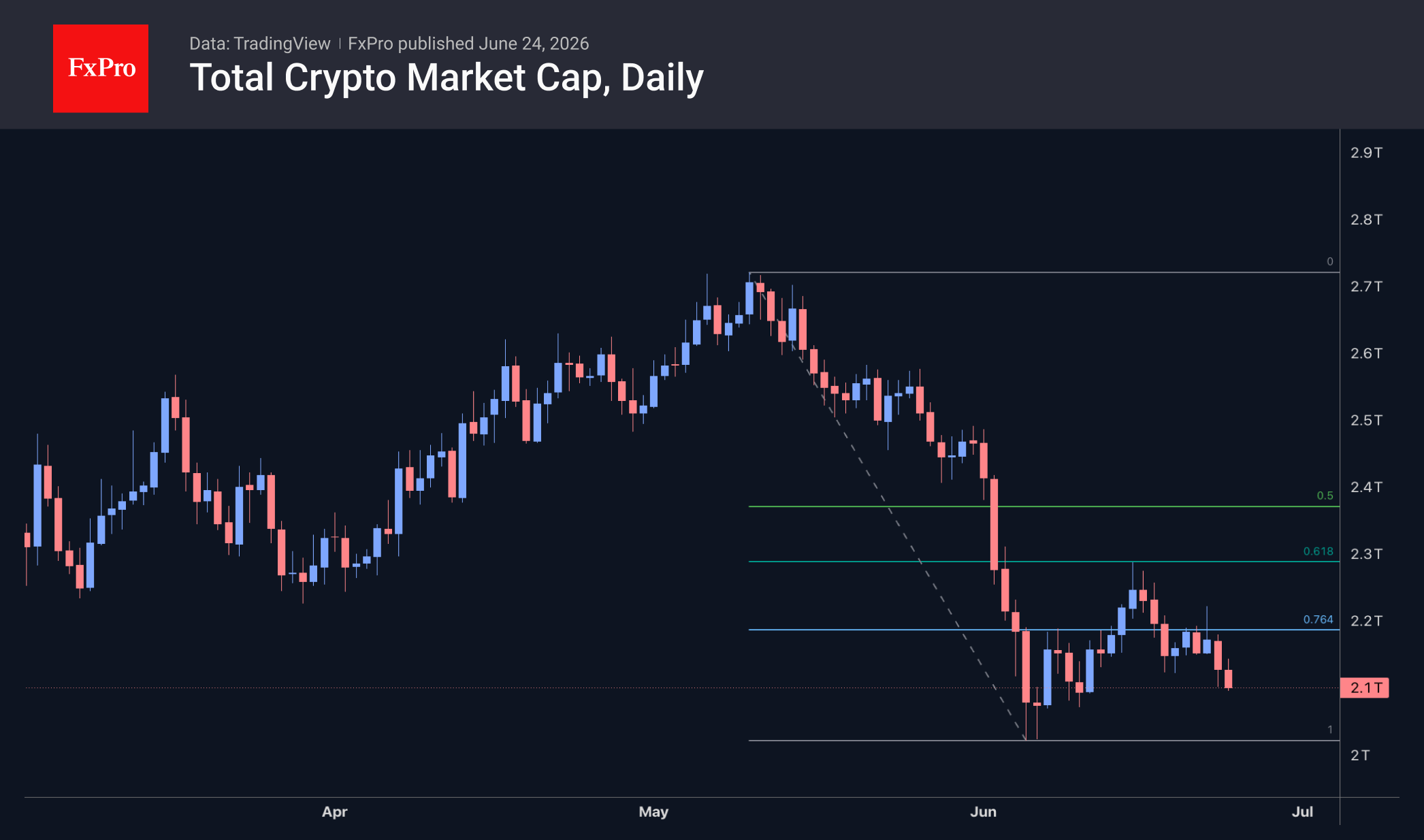

The crypto market capitalisation has stabilised at a low of $2.14T, having lost its recovery momentum in the second half of June after touching the 61.8% line. Consequently, there is a risk of a bearish expansion pattern forming, with the potential for a decline to a market capitalisation of $1.6T, a quarter below the current level. A break below the early-June lows would confirm this scenario, although increased buyer activity is evident near current levels. In any case, the stock market and the US dollar remain the key drivers, while cryptocurrencies are reacting to changes in the fundamental backdrop.

Bitcoin is trading below $63K, once again hovering near its seven-day lows. At these levels, the leading cryptocurrency remains close to its 200-week moving average. A dip towards this line in 2022 marked the start of nearly six quarters of poor performance, with prices hovering near this curve; in 2018, such a period lasted six months, and in 2015, nine. In other words, history suggests we should brace for a crypto winter rather than a rapid rebound.

News Background

Strategy purchased an additional 520 BTC last week for $34.9 million. The company now holds 847,363 BTC, acquired for $64.1 billion at an average price of $75.7K per Bitcoin.

Investment firm Strive acquired 759 Bitcoins last week for $50 million at an average price of $65.9K per coin. The total Bitcoin on Strive’s balance sheet now stands at 19,864 BTC. Since January, the company has increased its holdings by approximately 3,700 BTC.

BitMine has increased its Ethereum reserves to 5.67 million ETH, having purchased an additional 52,203 ETH over the past week. BitMine’s reserves now account for 4.7% of the total Ethereum supply.

BitMine Chairman Tom Lee remains optimistic about ETH despite incurring multi-billion-dollar losses on his positions. In his view, the crypto market is currently in the early stages of a ‘crypto spring’.

Mexican billionaire Ricardo Salinas Pliego has compared investing in Bitcoin to investing in property. He urged investors not to fixate on short-term price fluctuations but to view BTC as a means of preserving wealth for many decades.

The FxPro Analyst Team

Sunset Market Commentary

Markets

Brent oil slid to a new post-war low today. One barrel currently sells for $74.65, the first sub $75 print since the Middle East conflict erupted end-February. This compares to a $120 peak end-April and the $60-$70 range prior to the war. Prices have dropped dramatically in anticipation of flows restoring rapidly through the Strait of Hormuz. Official tankers vessel crossings have indeed picked up in recent days, following the interim peace deal between the US and Iran, but remain well below the levels seen before (15 vs roughly 60 on average). The US and Iran meanwhile are working their way towards a permanent deal (that amongst others deals with the nuclear issue). Negotiations are likely to be time-consuming and prone to setbacks but markets are willing to look through. Core bonds extended gains after the oil break lower with US Treasuries outperforming German bunds. US rates drop 3.2 to 6.2 bps in a flattening move. We note that for the 10-yr yield the inflation expectations component recently (June 22) turned below the real yield. Such a cross-over is rare (happened only a handful of times the last 15 years+) and gained further traction since the Fed policy meeting of last week. Warsh's pledge to deliver on price stability has compressed inflation expectations further. Real yields meanwhile have also climbed higher in what can be seen as a vote of confidence in the US economy. European (swap) yields drop 3.1-4.1 bps in similar flattening fashion. The 10-yr tenor is trading at the lowest level since mid-March. The US dollar confirms yesterday's technical push higher against the euro with EUR/USD sliding towards 1.133. This 13-month low offers negligible support (38.2% retracement on the 2025-2026 EUR/USD rally) before the 1.12 area and more important 1.11 zone pops up. DXY soars to 101.77 with targets from a technical point of view seen at 102.86 & 104.59. USD/JPY grinds higher, testing the patience of Japanese officials. Finance minister Katayama yesterday said he and his US counterpart Bessent agreed on taking "bold" steps if needed. Stock markets trade with caution. The EuroStoxx50 sheds 0.4% towards first support at 6200. Wall Street opens little changed. The Nasdaq rises 0.2% after yesterday's 2.5% beating. After-market results from chipmaker Micron will help shape sentiment tomorrow.

News & Views

The Czech composite economic sentiment indicator rose 1.6 pts in June as both of its components improved. Business confidence improved only slightly (+0.8 pts to 99.8). The gain in consumer confidence was more outspoken (+3.1 pts to 106.5), coming after two monthly declines. The share of consumers expecting a deterioration in the overall economic situation in the country decreased. More households expect an improvement in their financial situation. Concerns about rising prices & higher in unemployment stayed unchanged. Regarding business sentiment, confidence increased in industry, but decreased slightly in trade and in selected services and significantly in construction. Better confidence in June comes as the Czech National Bank (CNB) last week raised its policy rate by 25 bps to 3.75%. CNB assessed that especially core inflation remained too elevated on a range of domestic factors including accelerating credit growth, public expenditure, a tight labour market and rapidly rising wages and household spending. At 4.12% the Czech 2-y swap rate currently trades 3 bps higher compared to after the CNB decision. The krone is losing ground to EUR/CZK 24.24, partially driven by a stronger dollar.

The Swedish Riksbank today published the Minutes from its June 16 policy meeting when it kept the policy rate at 1.75%. The post-meeting statement indicated an increased probability of a hike later this year due to upside inflation risks for the supply shock of the war in the Middle East. The Minutes today showed divergence between the MPC members on the degree of the upside inflation risks. In its assessment on the upward risks to inflation, governor Thedéen in particular addressed the importance of the koruna exchange rate as a factor which in an unfavourable scenario could strengthen the inflationary impulse. Last year's strength of the koruna had continued to the Swedish context of low underlying inflation. However, the Swedish currency in the previous months declined from a cycle best near EUR/SEK 10.50 end January to currently trade near EUR/SEK 11.09. If this trend continues, the currency could gain weight as a factor in the Riksbank decision making process. For now governor Thedéen concludes that the Riksbank decision means that they are shifting the earlier course in a slightly tighter direction, but that the rudder angle remains small as it can increase or decrease depending on the risks.