Sample Category Title

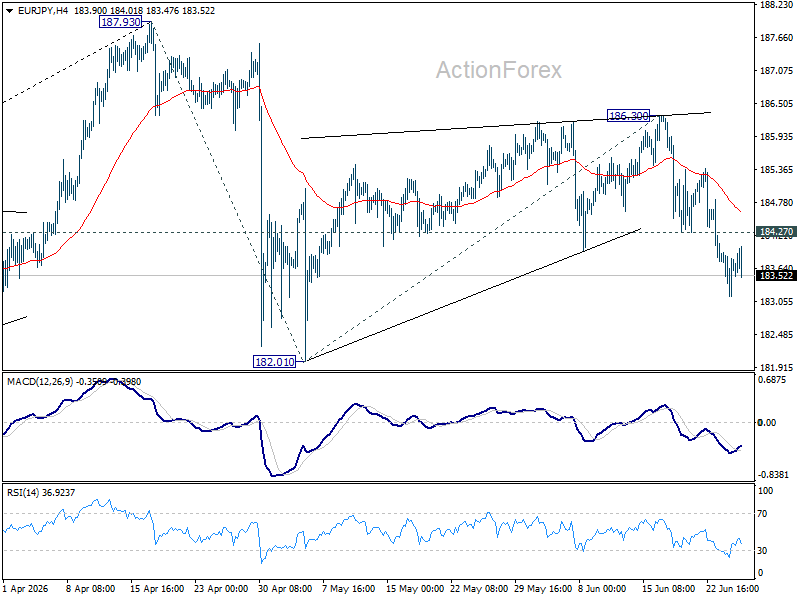

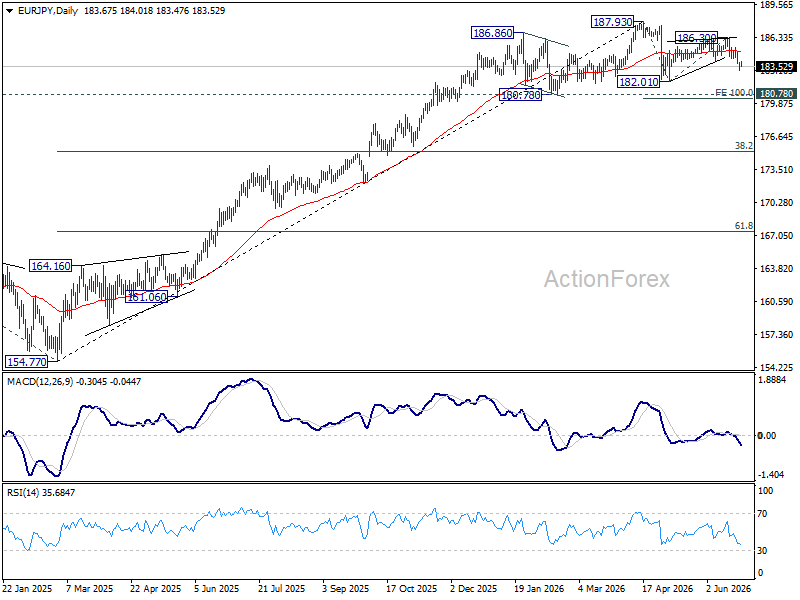

EUR/JPY Daily Outlook

Intraday bias in EUR/JPY remains on the downside fro retesting 182.01. Firm break there will resume the fall from 187.93 and target 100% projection of 187.93 to 182.01 from 186.30 at 180.38. On the upside, above 184.27 minor resistance will turn intraday bias neutral first.

In the bigger picture, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 179.41) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

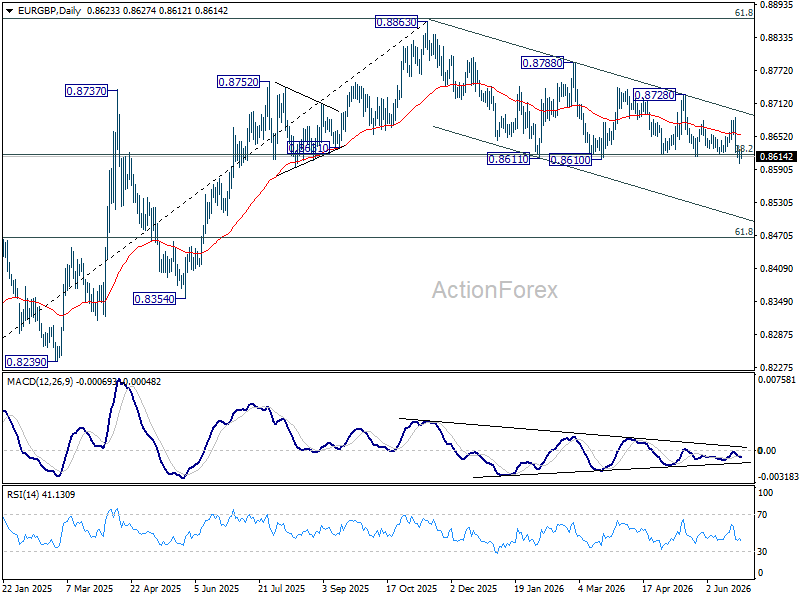

EUR/GBP Daily Outlook

Immediate focus remains on 0.8610/8 key support zone. Decisive break there will will revive the case of bearish trend reversal, and target 0.8466 fibonacci level. Nevertheless, firm break of break of 0.8686 resistance will bring further rally back to 0.8728 resistance.

In the bigger picture, focus is staying on 38.2% retracement of 0.8221 to 0.8863 at 0.8618. Strong rebound from there will retain medium term bullishness. Rise from 0.8221 should resume through 0.8863 at a later stage. Nevertheless, sustained break of 0.8618 will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least.

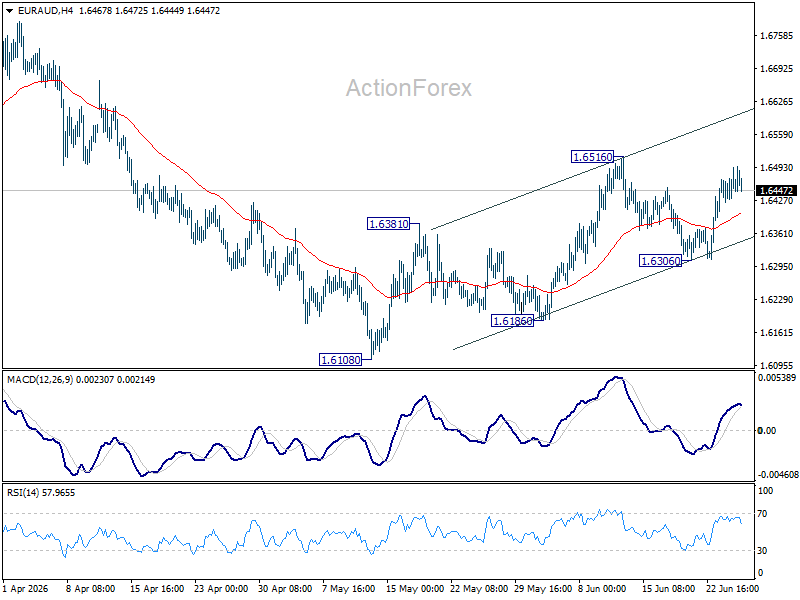

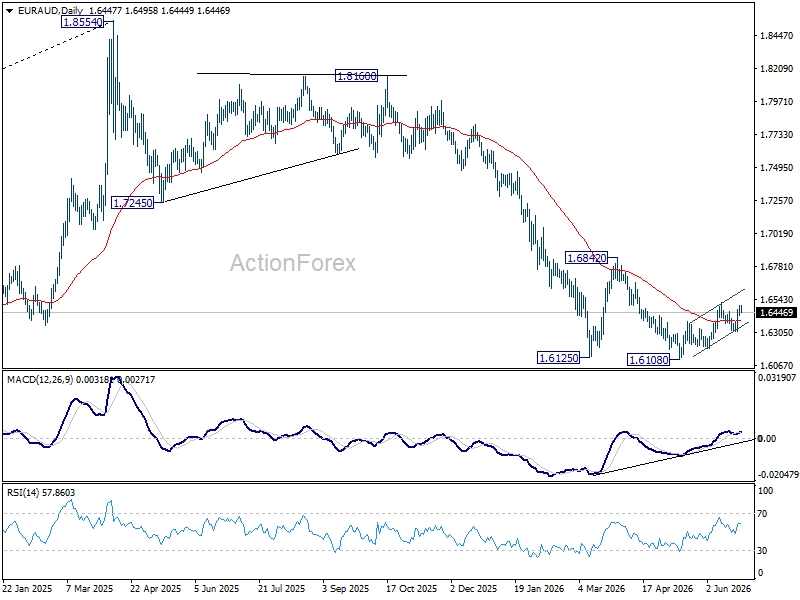

EUR/AUD Daily Outlook

Intraday bias in EUR/AUD remains mildly on the upside for 1.6516 resistance. Firm break there will resume the rebound form 1.6108 towards 1.6842 resistance. For now, risk will stay mildly on the upside as long as 1.6306 support holds, in case of retreat.

In the bigger picture, outlook will stay bearish as long as 1.6842 resistance holds. Fall from 1.8554 (2025 high) is expected to continue to 61.8% retracement of 1.4281 to 1.8554 at 1.5913. Decisive break there will pave the way back to 1.4281 (2022 low). However, firm break of 1.6842 should confirm medium term bottoming, and bring stronger rally.

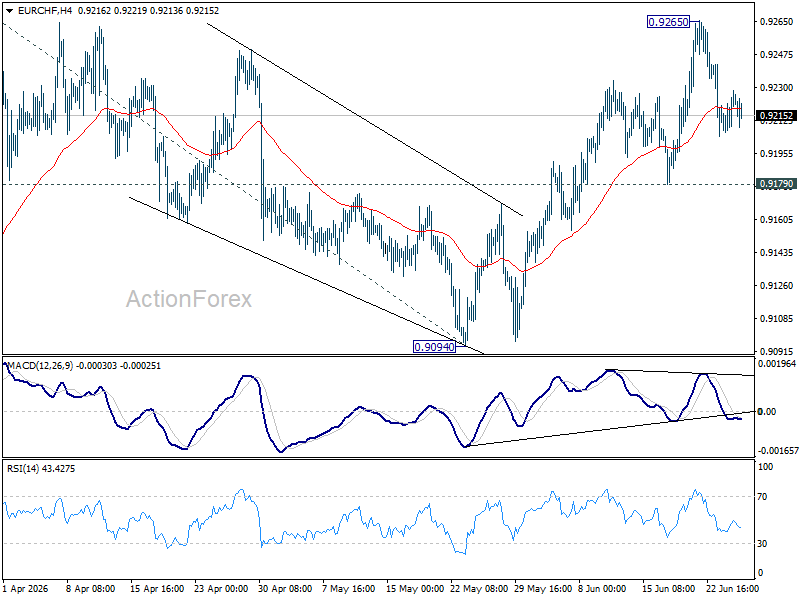

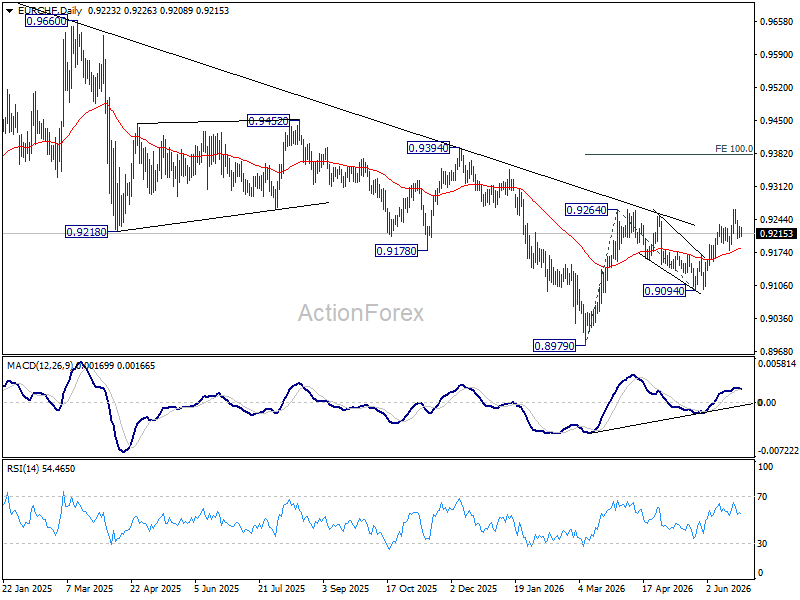

EUR/CHF Daily Outlook

EUR/CHF is staying in consolidations and intraday bias remains neutral. As long as 0.9179 support holds further rally is expected. On the upside, decisive break of 0.9264 resistance will resume the rally from 0.8979 to 100% projection of 0.8979 to 0.9264 from 0.9094 at 0.9379. However, firm break of 0.9179 will turn bias back to the downside for 0.9094 support instead.

In the bigger picture, the break of medium term falling trend line resistance indicate that 0.8979 is already on medium term bottom. Considering bullish convergence condition in W MACD, rise from there should at least be reversing the fall from 0.9928, with prospect of developing into a medium term up trend. Firm break of 0.9394 resistance will add more credence to this case. For now rise will remain on the upside as long as 0.9094 support holds, in case of retreat.

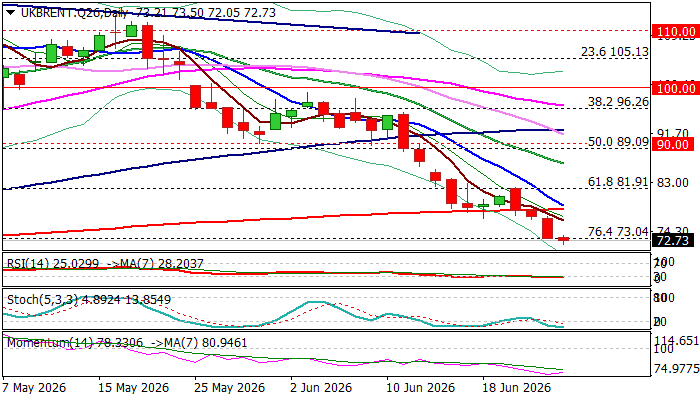

Brent Oil Falls to Pre-War Levels as Supply Normalization Provides Relief

Brent oil price hit pre-war levels (last traded on February 27) in early Thursday’s trading, as re-opening of Hormuz strait (20 million barrels passed through only yesterday) provides strong relief and continues to deflate oil prices.

Analysts estimate that situation is going to completely normalize in next couple of weeks, with increased production from Iran (after the US temporarily lifted sanctions) to boost oil supply, mainly to China, the world’s biggest oil importer and the biggest buyer of Iranian oil.

Fresh acceleration lower that extends into fourth straight day, cracked target at $73.04 (Fibo 76.4% of $58.70/$119.47 rally) and eyes next significant support at $70 (psychological), though oversold conditions on daily chart suggest that traders may opt for a partial profit taking.

Daily studies remain in full bearish configuration (strong negative momentum / multiple MA bear-crosses, with converging 10/200DMAs about to form death cross) maintaining downside pressure.

Violation of $70 to expose targets at $69.15 and $66.80 in extension, with upticks to face strong resistance at $78.16 (200DMA) which should cap and guard upper breakpoint at $81.91 (recent tops / broken Fibo 61.8%).

Res: 74.46; 75.76; 77.03; 78.16

Sup: 72.05; 70.43; 70.00; 69.15

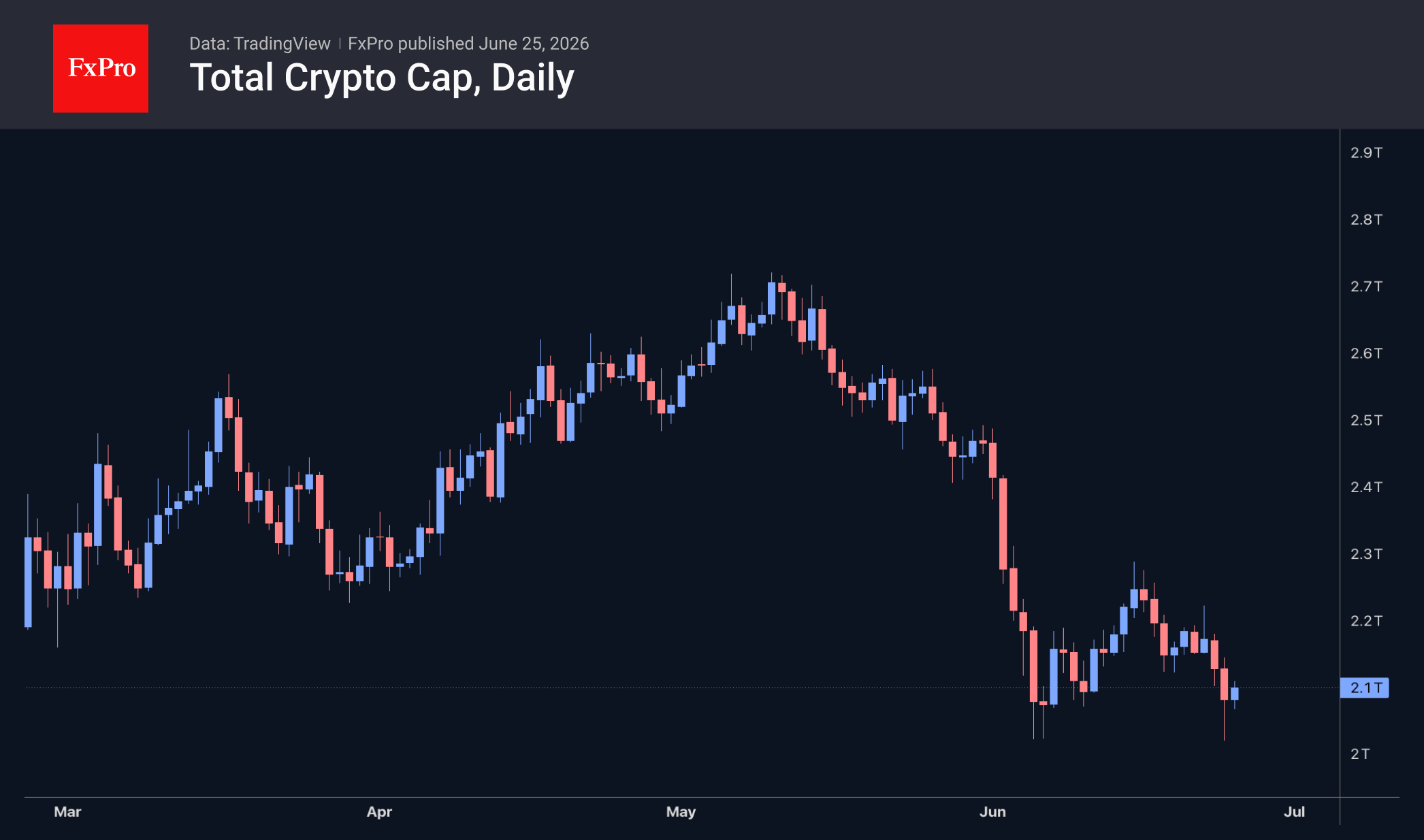

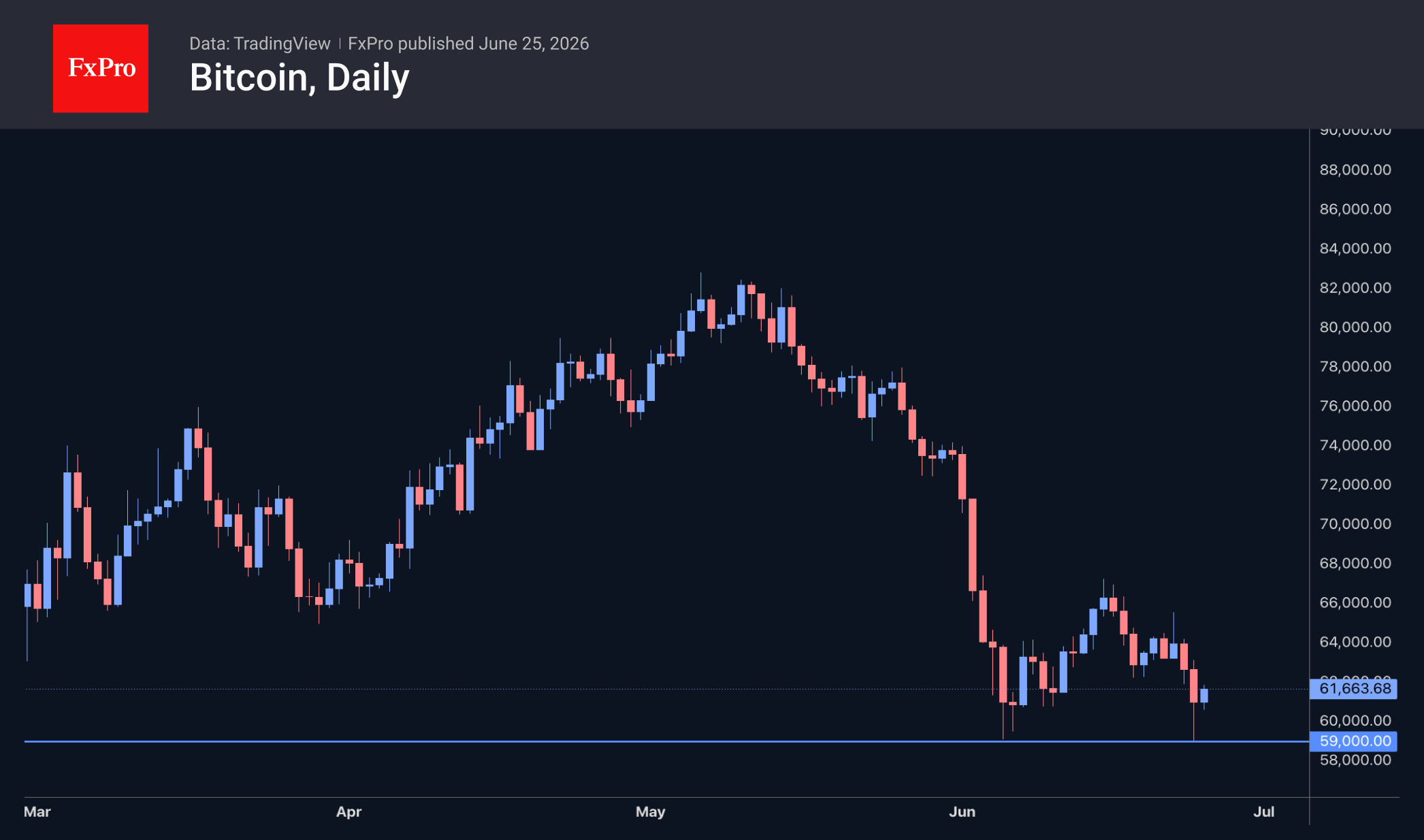

Bitcoin Has Formed a Double Bottom at $59K

Market Overview

The crypto market has fallen 1.4% over the past 24 hours, retreating to $2.12T as it continues its gradual return to the lows seen at the start of June. Notably, this time, cryptocurrencies were in no hurry to rebound alongside the stock market, preferring to wait for a more confident recovery to take shape. Over the past 24 hours, the top gainers were Aave (+14.2%), Internet Computer (+3.6%) and Gram (formerly Toncoin, +2.9%). The biggest declines were SushiSwap (-7.7%), Theta Network (-7.5%) and IOTA (-5.7%).

Bitcoin re-tested its early-June lows, touching $59K at the low point of Wednesday’s sell-off. This was followed by a decisive rebound, fuelling the bulls’ hopes of a double bottom forming. Should the rebound continue, the nearest upside potential is $67K, mirroring the movement seen in the first half of the month. For now, however, we are sticking to the ‘boring scenario’ described earlier, involving several weeks of consolidation near the 200-week moving average. This is trending higher and currently sits near $62.2K, with a likelihood of reaching $68K by October.

News Background

Strategy’s (STRC) preference shares have traded below their $100 par value for almost a month. Since the start of 2026, Strategy’s US-dollar cash reserves have fallen by 38 per cent. Over the same period, annual dividend liabilities have risen almost fourfold to $1.2 billion. Any attempt to quickly replenish the reserves by selling BTC would ‘destroy’ the company’s shareholder value.

Activity on the Bitcoin network has reached its highest level in the past two years, according to Glassnode. The rise in transaction volume is atypical for bear market phases and was triggered by the Runes protocol, which allows fungible tokens to be issued and transferred directly on the BTC network.

Bitcoin can be a useful way to diversify an investment portfolio when its share of total assets does not exceed 1–2 per cent, according to BlackRock. The investment firm advises investors to approach this asset with caution.

The Ethereum Foundation (EF) has announced a major reorganisation, unveiled an updated governance structure, and moved into cost-cutting mode, reducing its budget by 40 per cent. A former EF coordinator recently stated that around $30 million per year is required to support the network’s core infrastructure.

MoneyGram, one of the largest money transfer operators, has become a validator on the Solana network. Joining the Solana ecosystem will enable MoneyGram to expand its range of financial services using blockchain technology.

The FxPro Analyst Team

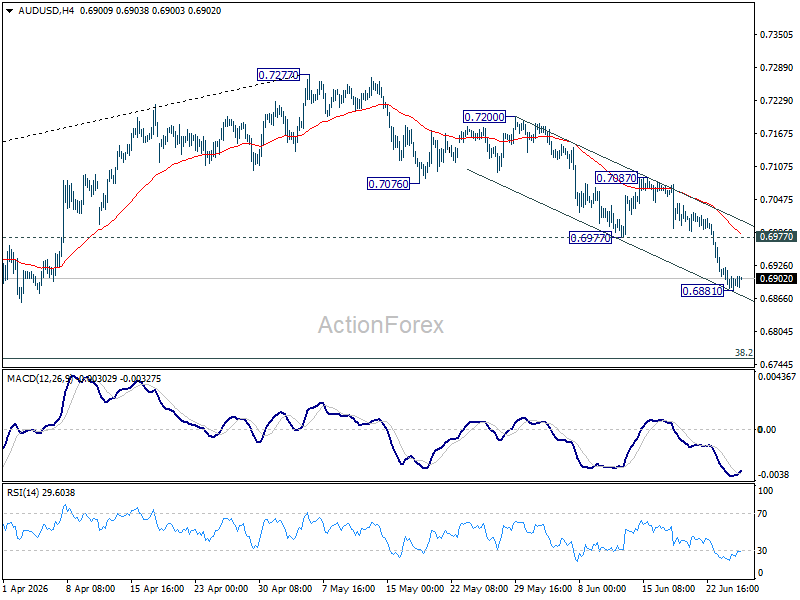

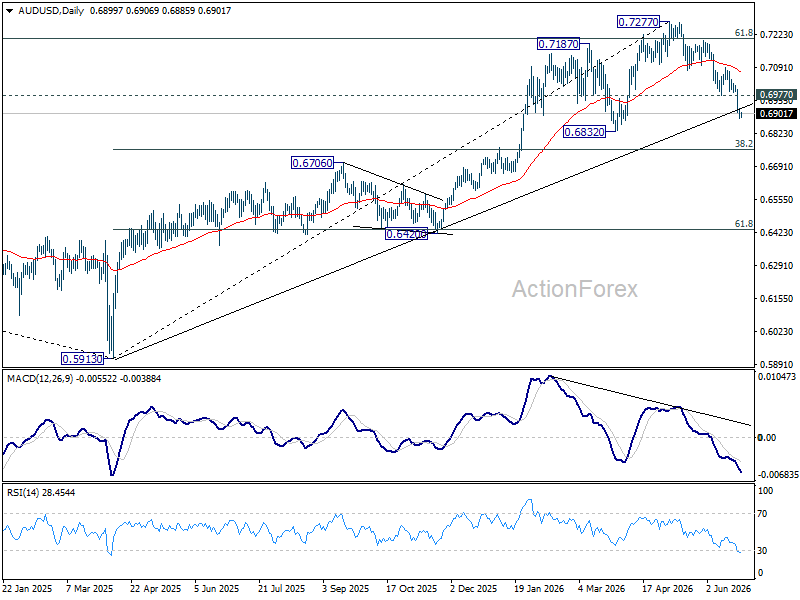

AUD/USD Stabilizes as Inflation, Jobs and Spending Keep August RBA Hike Alive

Australia's latest economic data were supposed to answer one question: has April's oil shock weakened the economy enough to keep the Reserve Bank of Australia comfortably on hold?

Instead, they delivered a more complicated answer.

AUD/USD has begun to stabilize after a sharp selloff this week, reflecting a data flow that was mixed at first glance but surprisingly consistent underneath. Headline inflation eased, yet core inflation accelerated. Employment rebounded, even if the quality of hiring softened. Most importantly, household spending bounced back strongly, suggesting consumers have largely absorbed the hit from higher energy prices.

Inflation remains the biggest challenge for policymakers. Annual CPI slowed to 4.0% from 4.2%, helped by lower fuel prices. But that is unlikely to provide much comfort to the RBA. Its preferred trimmed mean inflation measure accelerated to 3.6%, while services inflation picked up to 3.7%, showing that domestic price pressures remain stubborn despite improving energy costs. In other words, imported inflation may be easing, but home-grown inflation is proving harder to tame.

The labor market offered a similarly balanced picture. Employment rose by a stronger-than-expected 40.3k and unemployment edged down to 4.4%, but April's job losses were revised substantially deeper. Full-time employment increased by only 5k, with most hiring concentrated in part-time work, while hours worked declined -1.1% over the month. The report does not point to an overheating jobs market, but neither does it suggest labor conditions are deteriorating rapidly.

Perhaps the most significant report received the least attention. Household spending rebounded 1.3% mom in May after April's -1.7% mom decline, with all nine spending categories recording gains. That broad-based recovery indicates domestic demand has regained much of the ground lost during the oil-price shock, raising the possibility that stronger consumption could keep underlying inflation elevated over coming months.

The combined message from this week's releases is that the RBA's job has become more difficult rather than easier. A softer headline inflation reading alone might have strengthened the case for staying on hold. But resilient demand, sticky core inflation and a labor market that continues to hold together mean another rate hike in August remains very much in play, though not confirmed

Technically, AUD/USD may have established a temporary low at 0.6881, allowing for a period of consolidation. However, any recovery is likely to remain capped below 0.6977, now acting as resistance. The broader decline from 0.7277 is still viewed as a correction of the rally from the 2025 low at 0.5913, with scope for a deeper fall toward the 38.2% retracement at 0.6756 before a more sustainable bottom is formed.

Schnabel: ECB Will Need More Rate Hikes Despite Middle East Ceasefire

European Central Bank Executive Board member Isabel Schnabel reinforced the ECB's hawkish stance on Thursday, arguing that the recent ceasefire in the Middle East does not diminish the need for further policy tightening. "The ceasefire is no reason for monetary policymakers to let their guard down," she said in an Interview with Die Zeit, warning that while oil prices have retreated from their recent peaks, medium-term energy prices remain elevated and uncertainty is still high. Schnabel also defended the ECB's June rate hike, saying the decision "was appropriate in all the scenarios we considered, including a milder scenario in which oil prices normalise rapidly."

Looking ahead, Schnabel made clear that additional tightening remains her baseline expectation. "From today's perspective, we will need to raise interest rates further in order to bring inflation back to our two percent target over the medium term," she said. At the same time, she emphasized that policymakers are not following a predetermined path, adding that "the extent and timing of further measures will depend on how the conflict, the economy and inflation evolve." Her remarks are consistent with market expectations that the ECB will proceed cautiously while retaining a tightening bias.

Schnabel argued that the central bank's priority is preventing higher energy prices from feeding into broader inflation through wages and corporate pricing. "It was necessary to prevent elevated medium-term energy prices from causing second-round effects and even higher inflation," she said, warning that policymakers "can't let it get to a point where prices and wages enter into a mutually reinforcing spiral." While acknowledging that higher borrowing costs will weigh on growth, Schnabel maintained that interest rates are "not yet restrictive," reinforcing the message that the ECB believes further policy normalization will still be needed even if geopolitical tensions continue to ease.

Bitcoin: Corrective Channel Broken as Traders Turn More Active

Bitcoin has come under the influence of several factors simultaneously. The wave of selling at the beginning of June was linked to Strategy's first disclosed Bitcoin sale in several years, a prolonged series of outflows from spot ETFs, and a large transfer of funds from a Mt. Gox wallet to a new address. The run of outflows from US spot Bitcoin ETFs became one of the longest and largest since these products were launched in January 2024.

Bloomberg Intelligence analyst James Seyffart noted that around $9 billion has exited Bitcoin ETFs since their peak, although most long-term fund investors have chosen to maintain their positions.

Technical picture

On the H4 chart of BTC/USD, an ascending corrective channel formed after an impulsive decline towards the $59,000 area. Price subsequently advanced to the upper boundary of the channel at $67,250, but failed to hold those levels. The channel was then broken to the downside, with quotations moving towards a test of the lower boundary of the current profile at $60,800.

The Point of Control (POC) is concentrated in the $62,700–$62,800 area and could attract market attention if price rebounds from the lower boundary.

The upper boundary of the profile is located near $64,180 and could act as resistance if the POC zone is breached. The RSI + MAs indicator stands at 34, 37 and 42 respectively. The oscillator remains below the neutral zone but has recovered from oversold territory, while the moving averages remain bearish and continue to point lower.

At the same time, vertical volume surged sharply during the decline on 24 June, which may have been interpreted by market participants as a sign that the local downtrend was nearing completion.

Summary

The unusually high volume recorded on 24 June, combined with the current RSI position, does not provide strong confirmation that the latest local impulse will continue, although the moving averages remain pointed lower for now.

Further price action may be influenced by upcoming US inflation data, as well as flows into Bitcoin ETFs, which experienced record outflows during June.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service (additional fees may apply). Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US Dollar Strengthens Amid Equity Market Weakness and Hawkish Fed Rhetoric

The US dollar continues to hold firm near multi-year highs as sentiment across equity markets deteriorates and investors increasingly expect the Federal Reserve to maintain a restrictive monetary policy stance for longer. The US economy remains resilient, while inflation risks continue to run elevated, prompting market participants to reassess the timing of potential interest rate cuts. Against this backdrop, demand for the dollar is being supported both by attractive US asset yields and its status as a safe-haven currency.

An additional source of support for the greenback has come from the decline in stock markets, which has increased investor caution and encouraged capital flows into the dollar. Despite some easing in geopolitical tensions surrounding Iran and a correction in oil prices, expectations of a more hawkish Fed remain the key market driver. Interest-rate futures continue to reflect a high probability that restrictive policy will remain in place for an extended period, supporting the dollar against most major currencies.

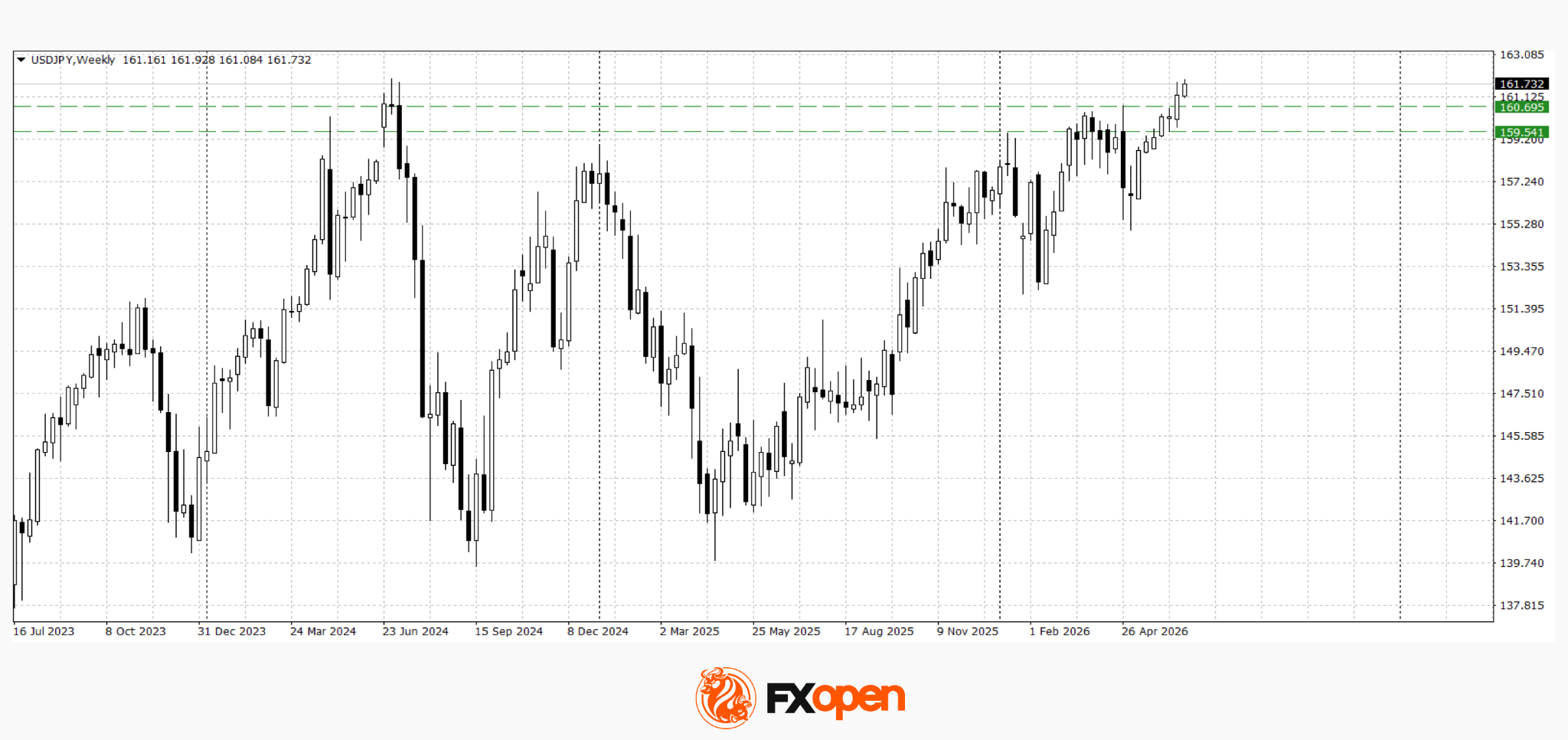

USD/JPY

USD/JPY continues to advance and is trading close to multi-year highs near 162.00. Pressure on the yen persists due to the wide interest-rate differential between the United States and Japan, as well as market doubts about the willingness of Japanese authorities to carry out further currency interventions. Technical analysis suggests the pair could extend its advance towards the psychological 163.00–164.00 area.

At the same time, a spike in volatility and a sharp pullback towards 160.00–161.00 cannot be ruled out, as the pair is already trading within a zone of long-term resistance on higher timeframes.

Key events for USD/JPY:

- Today at 15:30 (GMT+3): US Core Personal Consumption Expenditures (PCE) Price Index;

- Today at 15:30 (GMT+3): US GDP data;

- Today at 15:30 (GMT+3): Continuing Jobless Claims in the United States.

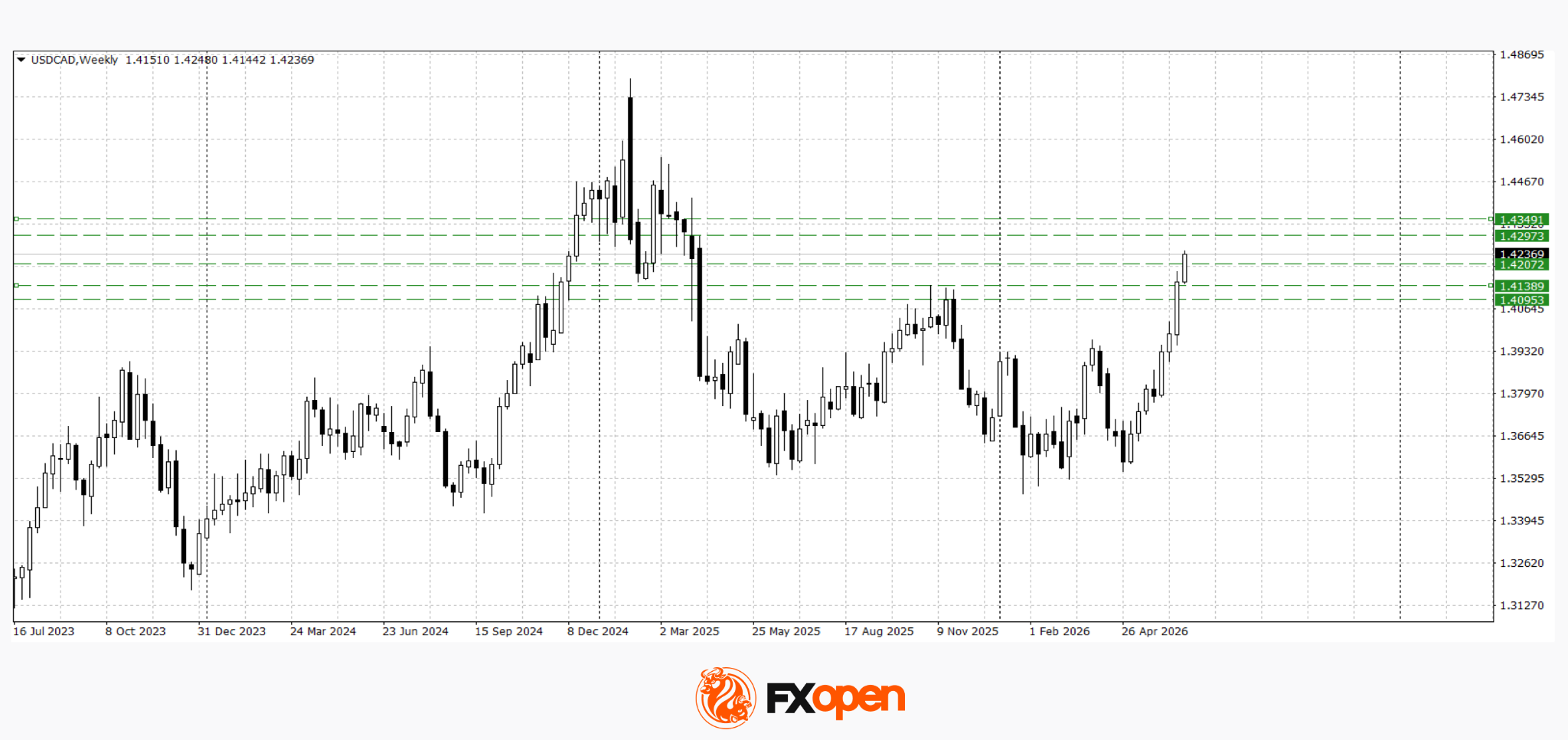

USD/CAD

USD/CAD also remains in an uptrend and is approaching long-term resistance levels in the 1.4300–1.4350 area. The pair is being supported by US dollar strength and the relative weakness of the Canadian dollar amid lower oil prices and expectations of further divergence between Bank of Canada and Federal Reserve policy.

A sustained move above 1.4300 could open the way for further gains towards 1.4350. However, a rejection from these levels and the formation of bearish reversal patterns could trigger a corrective decline towards the 1.4140–1.4200 region.

Key events for USD/CAD:

- Today at 15:30 (GMT+3): Average Weekly Earnings in Canada;

- Today at 15:45 (GMT+3): speech by Federal Open Market Committee (FOMC) member Michelle Bowman;

- Today at 17:00 (GMT+3): Atlanta Fed GDPNow estimate.

The US dollar remains the primary beneficiary of the current market environment. Equity market weakness, expectations of a prolonged period of restrictive Fed policy and the relative weakness of competing currencies continue to support the greenback.

At the same time, both USD/JPY and USD/CAD are approaching significant long-term resistance levels. As a result, further price action is likely to depend on whether upcoming macroeconomic data can confirm the resilience of the US economy and whether the Federal Reserve maintains its hawkish tone in forthcoming commentary.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.