Sample Category Title

FOMC to Remain Constrained by Inflation in 2026

The growth outlook is sanguine, but for inflation risks are clear.

The US economy continued to perform strongly through the turn of the year despite acute uncertainty. According to the latest Atlanta Fed GDPnow nowcast, not even the longest Federal Government shutdown on record was enough to slow GDP growth to trend, let alone below it. In 2026, growth is likely to normalise towards trend after five years of outperformance, but the prospect of a sustained period of disappointing momentum currently seems remote. Despite the Administration’s preference for lower rates, there is little cause for the FOMC to continue cut materially from here.

Now available to January, nonfarm payrolls growth looks to be forming a base, having edged backwards during the six months to October but averaging monthly gains of 73k since. The unemployment rate has also oscillated between 4.2% to 4.4% since February 2025 – evidence of stabilisation not an upward trend.

Other labour market indicators also point to a fully employed labour force and balance between new entrants and job listings. Most notably, the Employment Cost Index and hourly earnings from the establishment survey both continue to point to robust nominal income gains, and the ISM employment indexes have recently bounced back from depressed levels.

US household wealth is meanwhile at record highs and continuing to grow thanks to broad-based gains across equities and real estate, albeit with the latter tracking a modest pace. Established households are benefiting from comparatively low debt levels and the historically low interest rates locked in following the pandemic. Marginal borrowers are also beginning to see adjustable rates edge lower – a 5-year fixed rate which then converts to a variable rate versus the traditional standard 30-year fixed rate.

Household cash flows and wealth therefore stand ready to offer robust support to renovation activity, new home purchases and discretionary consumption from 2026. Sentiment is the risk, however, with households still acutely aware of the cost to real incomes brought by sustained elevated inflation.

On that front, the latest readings are a concern, with the University of Michigan measure of sentiment 13% below its 5-year average and 32% below its full history average as at February. That is in large part due to backward-looking perceptions of household finances, despite the aforementioned nominal gains.

While there is less hard evidence, many businesses are arguably similarly placed to households, benefiting from robust conditions but concerned over what tomorrow may bring. For companies, the risk is two-sided, being exposed to supply constraints related to tariffs and reduced labour supply on the one and with consumers’ financial anxiety limiting their ability to reprice on the other. We therefore expect to see firms invest for efficiency and productivity through 2026 but, in aggregate, to eschew expanding capacity – the hyperscalers being an obvious exception.

This backdrop highlights a concern of ours not only for 2026 but also 2027 and into the medium term. Put simply: if consumption remains above trend, the labour market fully employed and businesses (in aggregate) capacity-constrained, it will be extremely difficult for the FOMC to bring inflation sustainably back to their 2.0%yr target from circa 2.5%yr pace in January. Indeed, given the persistent weakness seen in business investment since the GFC, an acceleration in inflation pressures remains a distinct possibility – annual core services inflation was 2.9%yr in January, and close to 5.0% on an annualised basis.

In light of the above, we have pushed out the last cut forecast for the FOMC this cycle from March to June 2026. We also must make clear that we have low conviction in this call, believing the economy is more likely to outperform than disappoint on activity and / or prices, in which case the FOMC would be justified to remain on hold for the foreseeable future.

We recognise this view deviates considerably from market pricing, which currently has two cuts by year-end and a high chance of another by June 2027, much of this reflecting expectations of a shift in approach once Kevin Warsh takes over from Jerome Powell as FOMC Chair in May. But, for the data to warrant such a course by the FOMC, we would need to see a material deterioration in the labour market, or the rapid abating of inflation pressures and associated risks. These outcomes are possible but, at present, seem unlikely.

This analysis first appeared in Westpac Economics’ February Market Outlook which also includes our latest forecasts for Australia, the global economy and financial markets.

Dollar Set to Test Multi-Decade Levels

Key themes for the US dollar and global FX markets.

The US dollar initially rallied from 97.9 in late-December to 99.4 mid-January. However, it then lost its way, falling back to a near 4-year low of 96.2, now 97.0. At the current level, the US dollar is around 15% below its mid-2022 peak and circa 1.5% under its 10-year average. Our baseline expectation is that the dollar will settle between its current level and the 20-year average over the coming 12-18 months, but risks are arguably skewed to the downside.

It is not as though we have a pessimistic view on the US economy, however. Indeed, quite the opposite. As detailed on page 16 of the February Market Outlook (linked below), our baseline expectation for 2026 is another year of above-trend growth, led by the consumer and tech infrastructure investment. Underlying this expectation is the view that the labour market will remain fully employed and wage growth ahead of inflation.

Along with the lagged effect of tariffs and evidence of capacity constraints across a number of key sectors such as housing, transport, energy and health, there is therefore good reason to believe that inflation will remain above the FOMC’s 2.0%yr target and risks skewed to the upside. The above views on growth and inflation are why we hold the expectation of one more cut from the FOMC loosely against market pricing for at least two cuts this year.

Why then do we expect the US dollar to fall further and risks to remain skewed to the downside? It is because of the opportunities elsewhere.

Regarding financial opportunities, the strong run for US equities limits the chance of further outperformance, the global dominance of US technology firms notwithstanding. Also, unlike the years immediately following the pandemic, the narratives around both Europe and Asia’s economies are increasingly focused on growth and economic development rather than trade risks, and investors have been taking note of these themes.

As important as the trends themselves are their likely persistence, with economic growth in Europe and Asia to continue receiving support over the coming decade and potentially beyond. This is a striking contrast to the US’ current situation where the upcycle in infrastructure spending is likely at or very near its peak, and the dividend from it likely to come in the form of distributed efficiency wins across the economy and for profits, more so than an outright surge in production and national income.

Considering recent developments by each bilateral exchange rate within the DXY group, euro and sterling have clearly been the big winners. Since mid-January, EUR/USD has risen from USD1.16 to USD1.19, which is materially above the average of the past decade, USD1.12. Sterling has followed suit, GBP/USD rising from USD1.30 in November (also its decade average) to USD1.36 today.

The Canadian dollar’s recent gain has been more modest, USD/CAD only falling from CAD1.39 in mid-January to CAD1.36, above the decade average of CAD1.33 (i.e. the Canadian dollar is still below its 10-year average versus the US dollar). Meanwhile, Japan’s yen has been little changed on net since mid-December, albeit with considerable volatility day-to-day amid a myriad of political and geopolitical developments.

Ahead, amongst the DXY pairs, relative changes are likely to follow a similar pattern, with euro and sterling most likely to show strength – we believe to respective peaks of USD1.22 and USD1.41 by mid-2027. The Canadian dollar is also expected to rally materially, but likely not until late-2027 and 2028 once growth has strengthened and trade uncertainties have been put to rest. At June 2027, we expect USD/CAD to only be marginally lower at CAD1.34. But by June 2028, we forecast USD/CAD to have fallen to CAD1.30. For each currency, there is clear upside against the US dollar, but likely only if downside US economic and / or policy risks assert.

A similar logic can be laid out for the yen. Prime Minister Sanae Takaichi and the LDP’s historic win in February’s lower house election will provide considerable scope for fiscal policy to aid growth and confidence amongst businesses and consumers – the latter group particularly if the suspension of the consumer tax on food goes ahead. Still, the stance of monetary policy is unlikely to change materially in the near term, and so yield support for the yen should hold at current levels, not increase. Yen appreciation is therefore only seen gaining momentum as growth sustains and persistent inflation gives the Bank of Japan cause to act. Global investment flows are also important for the yen’s outlook. We continue to look for USD/JPY to slowly track down to JPY145 at end-2026, then JPY139 come mid-2028, still well above 2019’s JPY109 level.

While not a constituent of the DXY index, China’s renminbi is evidence of participants growing belief in Asia. From a peak of CNY7.35 last April, USD/CNY has declined to CNY6.90 at present, a 6% appreciation for the renminbi. Ahead, we expect a similar sized appreciation against the US dollar, albeit spread across the next 18 months to CNY6.35 at mid-2028. If China’s Central Government can reset the domestic economy decisively, then additional strength could be seen over a short period. The investment China has undertaken across Asia and its underlying development prospects are likely to see gains in the renminbi spread to other regional currencies over time.

This analysis first appeared in Westpac Economics’ February Market Outlook which also includes our latest forecasts for Australia and the global economy.

Eco Data 2/16/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Jan | 50.9 | 51.5 | 51.7 | |

| 23:50 | JPY | GDP Q/Q Q4 P | 0.10% | 0.40% | -0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | 3.40% | 3.20% | 3.40% | |

| 04:30 | JPY | Industrial Production M/M Dec F | -0.10% | -0.10% | -0.10% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | -1.40% | -1.50% | 0.70% | |

| 13:15 | CAD | Housing Starts Y/Y Jan | 238K | 265K | 282K | 281K |

| 13:30 | CAD | Manufacturing Sales M/M Dec | 0.60% | 0.50% | -1.20% | -1.30% |

| 21:30 | NZD |

| Business NZ PSI Jan | |

| Actual | 50.9 |

| Consensus | |

| Previous | 51.5 |

| Revised | 51.7 |

| 23:50 | JPY |

| GDP Q/Q Q4 P | |

| Actual | 0.10% |

| Consensus | 0.40% |

| Previous | -0.60% |

| 23:50 | JPY |

| GDP Deflator Y/Y Q4 P | |

| Actual | 3.40% |

| Consensus | 3.20% |

| Previous | 3.40% |

| 04:30 | JPY |

| Industrial Production M/M Dec F | |

| Actual | -0.10% |

| Consensus | -0.10% |

| Previous | -0.10% |

| 10:00 | EUR |

| Eurozone Industrial Production M/M Dec | |

| Actual | -1.40% |

| Consensus | -1.50% |

| Previous | 0.70% |

| 13:15 | CAD |

| Housing Starts Y/Y Jan | |

| Actual | 238K |

| Consensus | 265K |

| Previous | 282K |

| Revised | 281K |

| 13:30 | CAD |

| Manufacturing Sales M/M Dec | |

| Actual | 0.60% |

| Consensus | 0.50% |

| Previous | -1.20% |

| Revised | -1.30% |

The Under-Appreciated Effects of FX Appreciation

The USD sell-off has caused the AUD to appreciate beyond what the recent shift in the rates outlook would imply.

- Geopolitics and AI-generated investor nervousness have contributed to a growing pivot out of the USD since the beginning of the year, if not out of US-domiciled assets necessarily. The result has been compressed credit spreads elsewhere and vibrant activity in non-US credit markets, including Australia.

- The USD has therefore depreciated noticeably in recent weeks but remains overvalued on standard metrics, though less so than a year ago. The AUD has appreciated even more, with a bit more than half the shift in the TWI since the beginning of 2025 being an arithmetic consequence of the USD move. The rest is attributable to other factors, including but not limited to the shift in the rates outlook over the past couple of months.

- Normally, the AUD moves in ways that offset other shocks rather than being a shock in its own right. However, the nature of the USD sell-off and shifts in hedging suggest that the appreciation could dampen imported inflation by more than is implied by rate moves alone.

If the procession of geopolitical events in the year’s opening weeks wasn’t enough, global markets have been buffeted by a growing pivot out of USD-denominated assets. Some of that pivot has involved investors retaining exposure to the underlying US assets but hedging the exchange rate exposure, while in other cases, portfolios are being reallocated outright.

This ‘de-dollarisation’ pivot has in part been driven by the various geopolitical events of recent weeks, many of which are seen as US-negative and USD-negative, but there is more to it than that. Compounding the nervousness has been ongoing uncertainty about the implications of the AI technology and investment boom. The major players’ investment plans are of such enormous scale that digesting the resulting issuance will inevitably affect the market more broadly. This is especially so when we are already seeing cases where investment with an economic life of less than a decade is being funded by a 100-year bond issue.

Another element of this nervousness has been seen in negative equity market reactions to recent releases of new AI products that are seen as potentially disrupting incumbent industries. We remain of the view that these new technologies will not destroy jobs and industries in the way some fear. After all, the intellectual property of a software firm is less that they have people who know how to code, and more that they have people who know what makes a good payroll system, or drawing software, or whatever it may be. That design knowledge is harder to ‘vibe’ than the code. But for now, the rate of change is so rapid that the first reaction will be fear, until the broader implications can be worked through.

An intense appetite to invest in credit products means that neither the shift out of USD or the boom in AI investment funding has materially shifted fixed-interest pricing in the large US and other major markets. For example, 10-year government bond yields are little changed over the past couple of months. Rather, we see the impact in compressed credit spreads, and in smaller debt markets such as Australia’s, where issuance volumes have expanded to take advantage of strong investor demand. New participants have entered both sides of the Australian credit market and activity broadly has been vibrant.

The pivot out of USD assets has materially contributed to a sell-off of the USD in recent weeks. Over the past month, DXY is down around 2%, and it touched even lower levels in late January. Despite this, standard metrics still show the USD as moderately overvalued, with the real effective exchange rate around 12% above its long-run average. This overvaluation was even more pronounced at the beginning of 2025 and has progressively unwound in fits and starts.

Meanwhile, because the Chinese currency is closely managed to maintain its USD exchange rate, it has moved relatively little in trade-weighted terms. But because inflation has been much lower there than in the US and many other major industrialised economies, its real effective exchange rate is around 15% below its peak in early 2022. The resulting increased competitiveness is one reason why China has been able to meet its growth targets by increasing exports.

Domestically, the main result of these developments is that the AUD has appreciated noticeably. In trade-weighted terms, it is up 5% since the beginning of the year and 10% since the start of 2025. These are large shifts that cannot be entirely attributed to the higher rates outlook in Australia recently.

To be fair, the rates environment has contributed: yields on Australian 10-year sovereign bonds are now around 65bp above their US equivalents, despite the Australian sovereign being more highly rated, after being closer to flat in the middle of last year. This has made Australian assets particularly attractive to global investors, within the broader pivot away from USD-denominated assets. But if shifts in domestic rates alone had been the driver, cross-rates against other currencies would have risen by more than they have done; in particular, AUD/EUR would not be below where it was at the beginning of 2025.

At least some of the AUD’s appreciation instead stems from other factors, including higher prices for some key commodities and the previously mentioned sell-off in the USD. Many of the entities increasing their hedging or reallocating new flows are Australian superannuation funds, so the impact on the AUD/USD exchange rate can be expected to be pronounced.

The AUD/USD bilateral rate is up nearly 15% since the beginning of last year, versus 10% on the TWI. The USD and CNY together have a roughly 40% weight in the trade-weighted index, and slightly less than that in the RBA’s import-weighted index. A crude way of thinking about this is that the USD bilateral move, and accompanying CNY move, accounts for 6ppt of the 10ppt move in TWI since the beginning of 2025. Since the AUD/USD rate would have moved anyway with the higher Australian rates outlook, not all of this relates to the USD sell-off. Again, though, movements against other major currencies imply that most of it was USD-driven.

Another way of thinking about the appreciation is through the lens of the real effective AUD exchange rate (using the IMF monthly real effective exchange rate data supplemented with nominal TWI movements, given the RBA’s quarterly index only goes to the December quarter). The 5½% lift in this measure in February to date compared with December is considerably larger than the impact of the roughly 100bp shift in the interest rate path implied by the RBA’s own models.

If the AUD remains at this level or appreciates further, some downward pressure on inflation in imported items can be expected over the next year or two. While estimates are necessarily imprecise, there are good reasons to think that size of the effect will not be fully captured in the impulse response from interest rate shock to inflation in a whole-economy model. Our assessment is that – partly for timing reasons – the RBA might not have fully incorporated this possibility into its February forecasts or assessment of risks.

In this week’s Market Outlook publication, we highlighted several reasons to expect that the current elevated inflation rate will unwind over time. Some of them, like the conclusion of public infrastructure projects and their impetus to demand, are purely domestic developments. The exchange rate appreciation, on the other hand, depends a lot on how attractive US markets remain to global investors or whether the sell-off continues.

This is quite a different dynamic to how policymakers usually think about the exchange rate. Normally, the AUD is seen as a shock absorber, the depreciation that cushions the effect of a global downturn, or the appreciation that absorbs and widely distributes the benefits of a commodity boom. Policymakers in Australia remember the difficulties their NZ and Canadian counterparts got into back in the 1990s by treating the exchange rate as an independent factor in a Monetary Conditions Index. It is therefore understandable that they might downplay a move that happened at the same time as the rates outlook moved a lot.

This time round, though, it will pay to keep a weather eye on the implications of global asset reallocation and Australian hedging patterns for AUD, and what this might do to the cost base for imported goods.

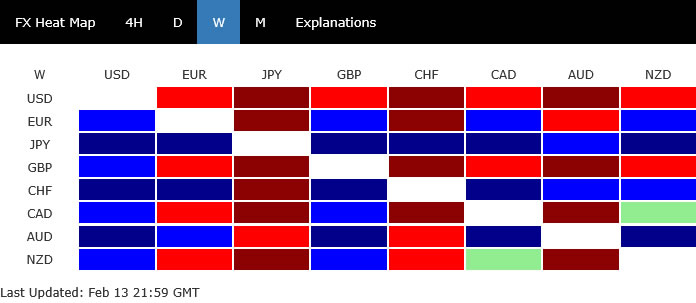

Dollar Drift With Yield Shock, Yen Breaks Tradition

There was no single, dominant theme in currency markets last week. Instead, price action reflected a mix of cross-asset divergences. Dollar ended as the worst performer, despite the fact that Fed expectations barely shifted following high-profile releases of non-farm payrolls and CPI. Meanwhile, US Equities experienced volatility, particularly around renewed AI disruption fears, yet there was no decisive breakout in either direction.

The most consequential development was the sharp dive in US yields. The 10-year yield’s slide appeared disproportionate to changes in Fed pricing, hinting that capital flows and positioning dynamics may be playing a larger role than policy expectations. That yield compression likely weighed on the Dollar, even though the selloff has been restrained rather than disorderly. Dollar Index was under pressure but has not yet entered an accelerated downtrend.

In contrast, Yen emerged as the standout performer. Notably, its rally occurred alongside continued strength in Japanese equities, breaking from the traditional inverse correlation between the currency and risk sentiment. Yet momentum in Yen has already begun to stall near key resistance levels. Also the durability of its decoupling from risk appetite is uncertain.

Elsewhere, Sterling ranked as the second weakest currency, pressured by renewed political instability within the Labour government and soft GDP data. Swiss Franc, by contrast, was the second strongest, reinforcing the impression of underlying caution even if global equities did not fully reflect risk aversion.

Aussie also posted solid gains, supported by hawkish RBA commentary that kept the door open for further tightening. However, momentum there is fading as broader risk appetite softens. Euro, Loonie and Kiwi drifted in the middle, lacking clear directional conviction — like passersby in a market still searching for its next unifying theme.

Data Fails to Inspire; NASDAQ's Rejection Raises Caution

US equities experienced elevated volatility last week but ultimately failed to establish a decisive direction. Stronger-than-expected non-farm payrolls and a slightly softer CPI print provided headline movement, yet neither report altered the broader narrative in a meaningful way.

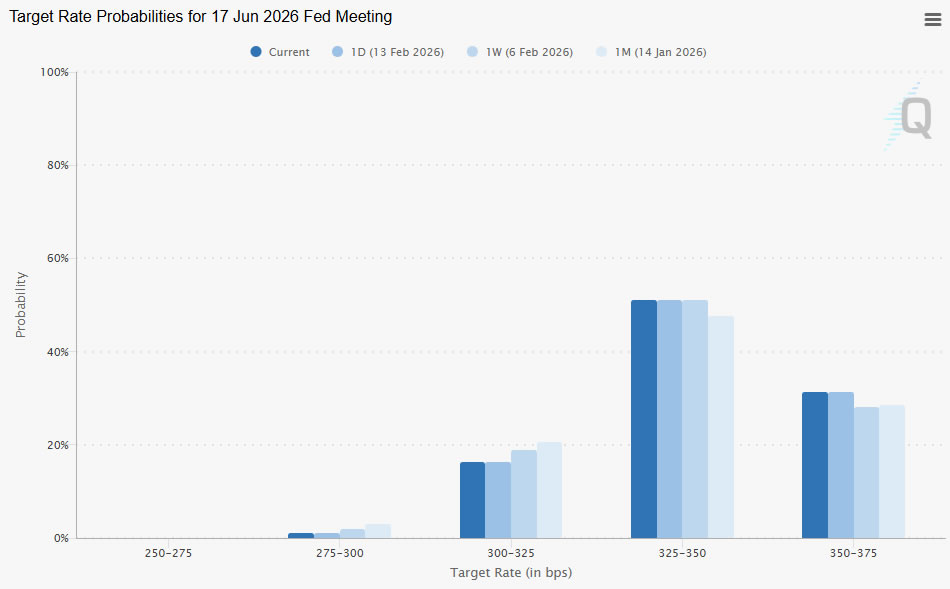

Markets quickly recognized that the data did little to shift Federal Reserve expectations. Pricing for a March hold moved from around 80% to roughly 90%. June cut odds dipped marginally from 72% to 69%. Those are incremental adjustments rather than regime changes.

With policy expectations stable, investor focus drifted back toward structural concerns — particularly renewed fears around AI-driven disruption. Technology and software shares remained sensitive, though selling pressure has so far lacked the intensity of a full risk-off unwind.

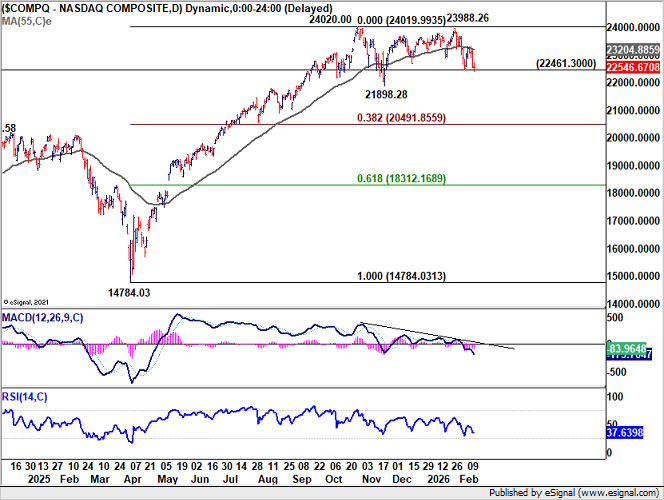

Importantly, the broader indexes are still holding within familiar ranges. The S&P 500 and NASDAQ remain contained inside consolidation structures, while DOW even managed to print a fresh record before paring gains.

Technically, however, risk is tilting to the downside for NASDAQ. The index was rejected at its 55 D EMA (now at 23,204), a development that often signals near-term vulnerability. NASDAQ should have already entered the third leg of the corrective pattern from 24,020.00 high. Deeper decline toward 21,898 support, and possibly below, is likely in the near term.

But for now, it's seen as in correction to the up trend from 147,84.03 only, not a larger scale one. Hence, downside should be contained by 38.2% retracement of 14,784.03 to 24,020.00 at 20,491.85 to bring rebound.

10-Year Yield Collapse, Dollar Index Softens

If there was one development that truly defined the week, it was the sharp decline in US Treasury yields. 10-year yield plunged to close near 4.056, a dramatic reversal from its January high at 4.311.

At first glance, some attributed the fall to expectations of faster Fed easing. However, interest rate pricing tells a different story. March remains firmly priced as a hold, while June cut probabilities have only shifted marginally. The yield move appears disproportionate to changes in Fed expectations.

A more plausible explanation lies in shifting asset allocation. With precious metals suffering steep declines in late January — Gold dropping more than 20% and Silver nearly 50% at one point — capital may have rotated back into Treasuries. Bitcoin’s sharp drawdown reinforces the broader de-risking narrative.

Safe-haven demand for US government bonds appears to have quietly re-emerged. The nomination of Kevin Warsh as the next Fed Chair may also have restored some institutional confidence in policy continuity, reducing fears of structural instability.

Technically, the break below 4.108 support in 10-year yield confirmed that the rebound from 3.947 was merely corrective, and topped at 4.311. The move decisively shifted near-term risk back to the downside. As long as 55 D EMA (now at 4.173) caps upside attempts, the path of least resistance remains lower. The next obvious target is a retest of 3.947.

For now, sustained break below 3.947 is not the base case. But if equity markets deepen their correction, that level could give way, potentially resuming the broader downtrend visible on the weekly chart. Indeed, rejection by 55 W EMA (now at 4.207) carries medium term bearish implications.

Meanwhile, Dollar Index's dip last week suggests that recovery from 95.55 has failed 55 D EMA (now at 98.04) on first attempt. There is prospect of a strong rebound in Dollar Index if stock market correction intensify. But upside should be capped below 100.39 resistance.

Medium term outlook remains bearish for now. Firm break of 95.55 will resume the down trend from 110.17 (2025 high) to 61.8% projection of 110.17 to 96.37 from 100.39 at 91.86.

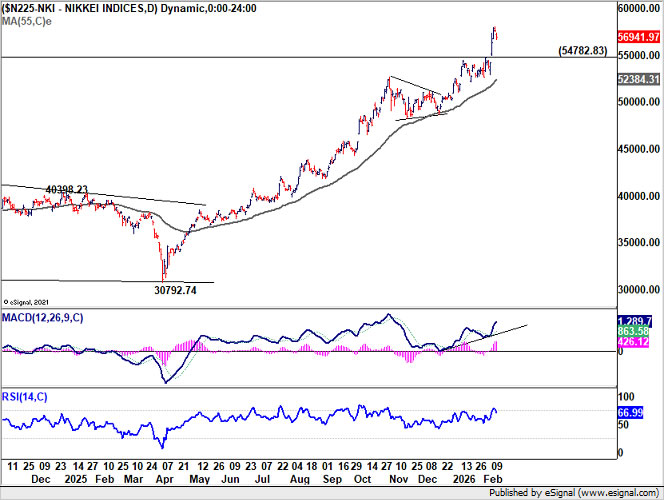

Japan Breaks the Mold as Yen Decouples From Equities

Japan delivered the clearest directional story of the week. Nikkei surged to fresh record highs while Yen rallied alongside equities — a rare decoupling from its traditional inverse correlation with risk assets.

The catalyst was political. Prime Minister Sanae Takaichi’s landslide snap election victory provided markets with clarity and a strong mandate. Investors interpreted the LDP supermajority as enabling more coherent fiscal execution without heavy concessions to coalition partners. Equity markets embraced the prospect of targeted stimulus, tax adjustments and structural reform. The rally was not merely momentum-driven; it was narrative-driven. Political certainty replaced fragmentation.

What made the move more unusual was Yen’s strength. Historically, a surging Nikkei tends to coincide with Yen weakness. This time, however, currency markets priced in a different dynamic. Markets appear to believe that a stronger mandate could lead to more disciplined fiscal management rather than unchecked stimulus. That interpretation has lent support to Yen, at least temporarily.

Still, Yen momentum began to stall toward the end of the week as the rally ran into key resistance levels, suggesting election optimism may now be largely priced in. The relations between Yen and stocks could revert back to normal ahead.

Technically, Nikkei is approaching a critical long-term Fibonacci resistance at 161.8% projection of 25,661.89 to 42,426.77 from 30,792.74 at 57,918.32. Overbought conditions raise the risk of consolidation.

A break below 54,782 would signal that Nikkei has entered a corrective phase with risk of deeper pullback. Such a move could revive Yen strength and push USD/JPY through 150 toward 145.

Conversely, decisive clearance above 57,918 would open the door to 60,000 and potentially 200% projection near 64,322.50. That scenario would likely reintroduce downward pressure on Yen. Sustained Nikkei strength could push the USD/JPY back toward 160.

As for Yen's next move, CHF/JPY is worth some monitoring. Both are safe have currencies and thus the cross is a good candidate to indicate the underlying direction of Yen.

Risk of a deep medium term correction in CHF/JPY is building even though confirmation is still needed. Bearish divergence condition in D MACD suggests that momentum has been persistently diminishing since last June. Also, it's medium term target of 161.8% projection of 173.06 to 186.02 from 183.95 at 204.92 was nearly met.

Sustained break of 55 D EMA (now at 197.53) will indicate that a medium term top should be formed at 203.64 already. CHF/JPY should then correct the whole five-wave up trend from 165.83 (2025 low), and target 38.2% retracement of 165.83 to 203.64 at 189.19.

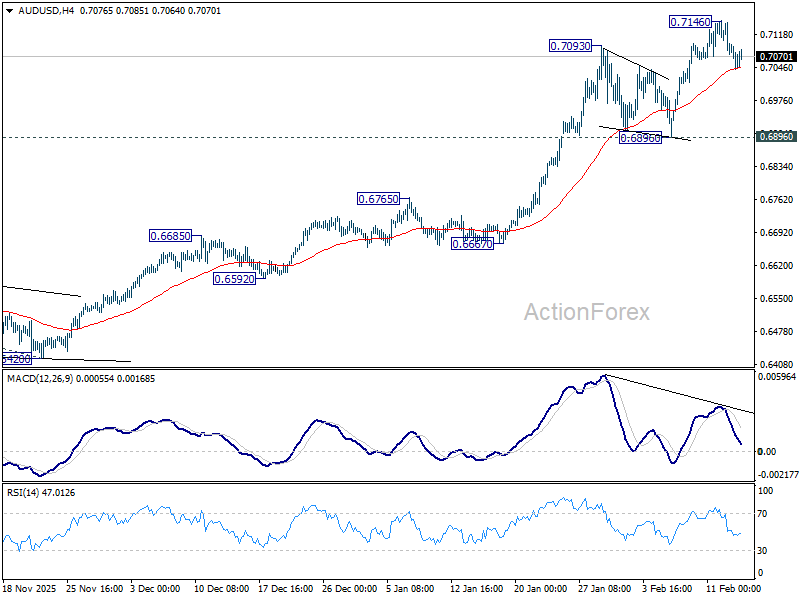

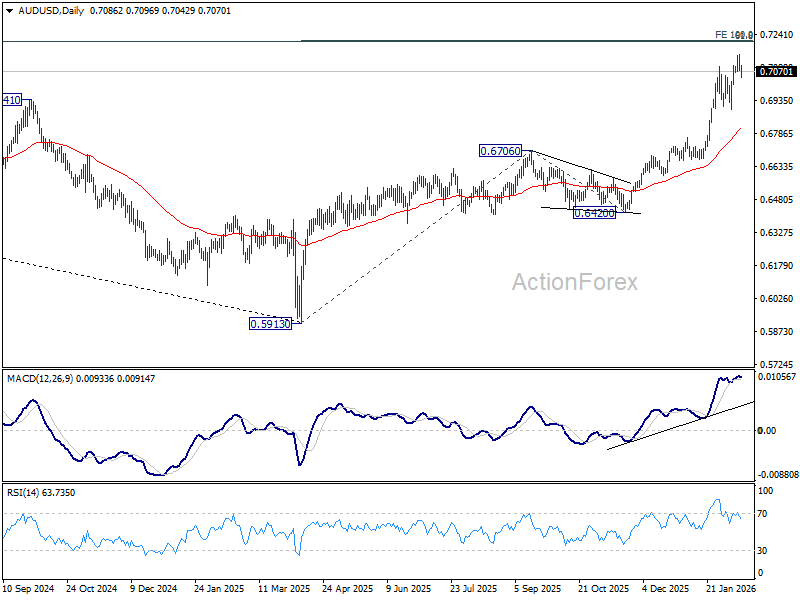

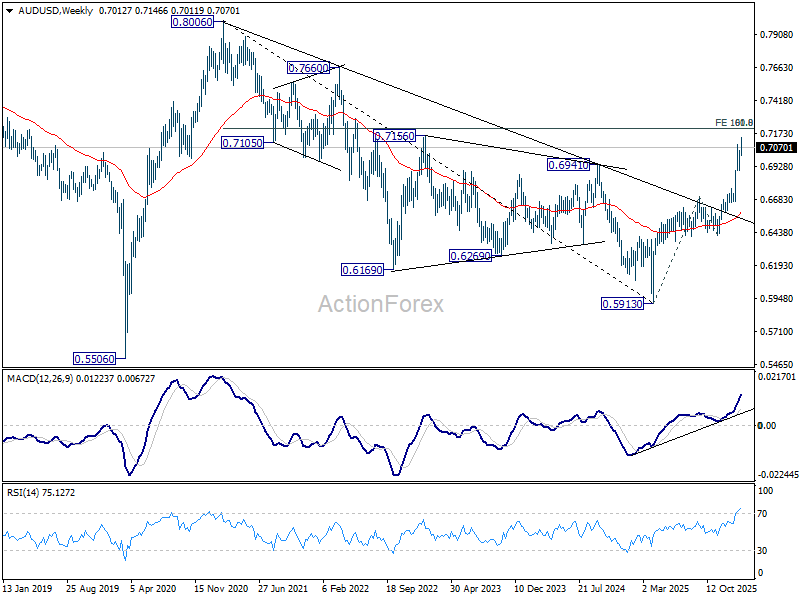

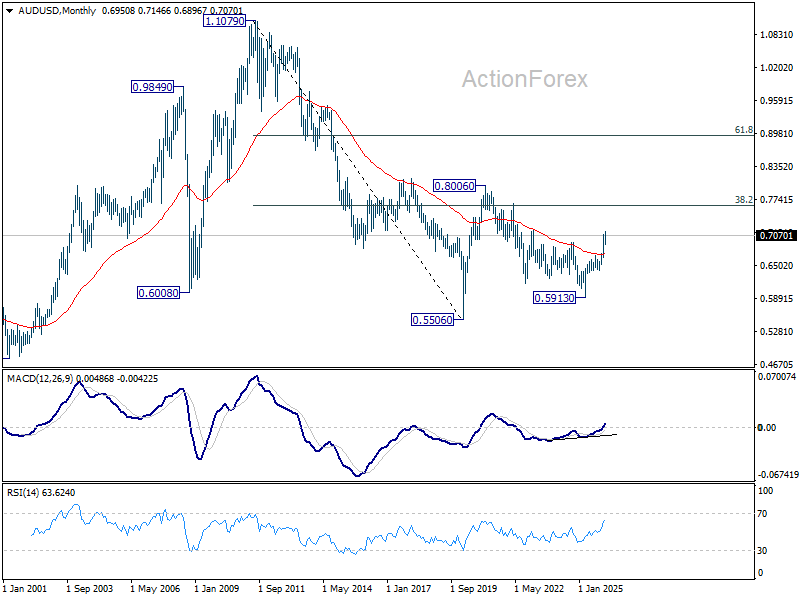

AUD/USD Weekly Report

AUD/USD edged higher to 0.7146 last week, but subsequent retreat indicates short term topping, on bearish divergence condition in 4H MACD. Initial bias remains neutral this week for consolidations, and deeper retreat might be seen. But downside should be contained above 0.6896 support to bring another rally. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above.

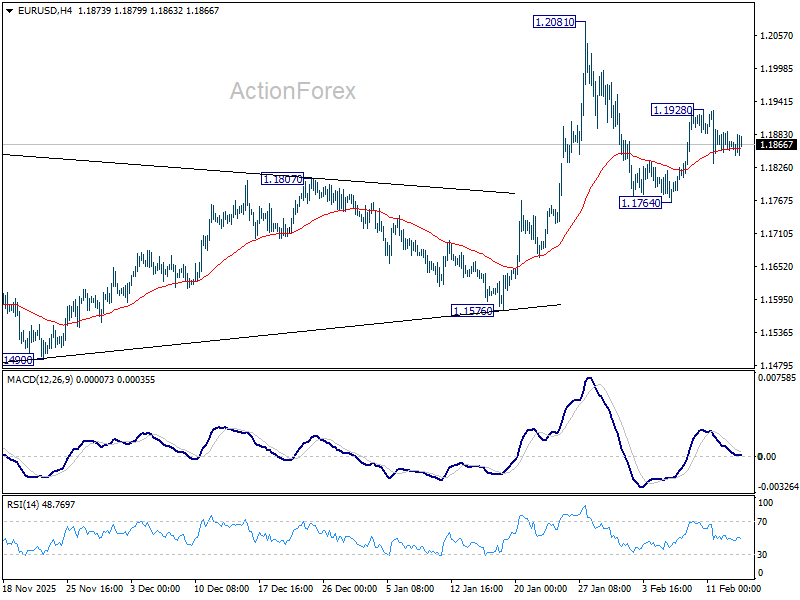

EUR/USD Weekly Outlook

EUR/USD's rebound stalled after hitting 1.1928 last week and retreated. Initial bias stays neutral this week first. On the upside, above 1.1928 will target a retest on 1.2081 high. Decisive break there and sustained trading above 1.2 psychological level will carry larger bullish implications. On the downside, however, sustained trading below 55 D EMA (now at 1.1756) will raise the chance of reversal on rejection by 1.2, and target 1.1576 support for confirmation.

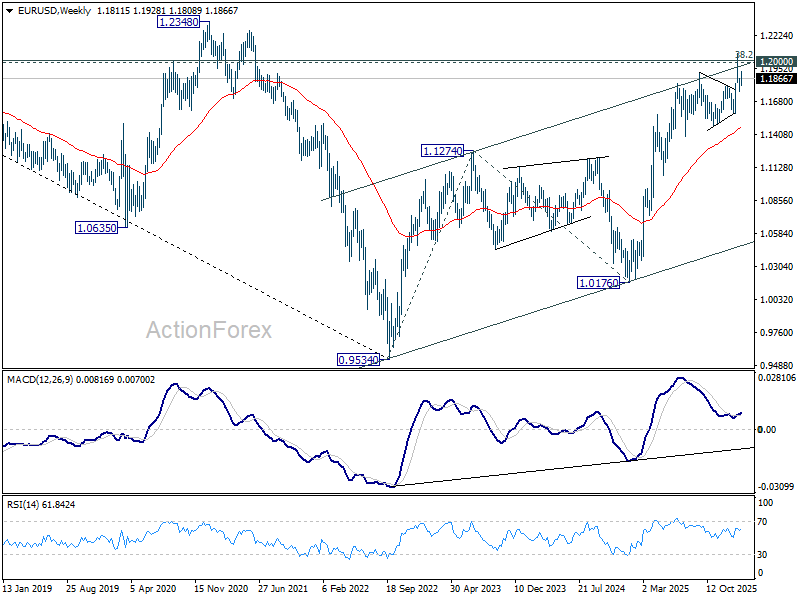

In the bigger picture, as long as 55 W EMA (now at 1.1471) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

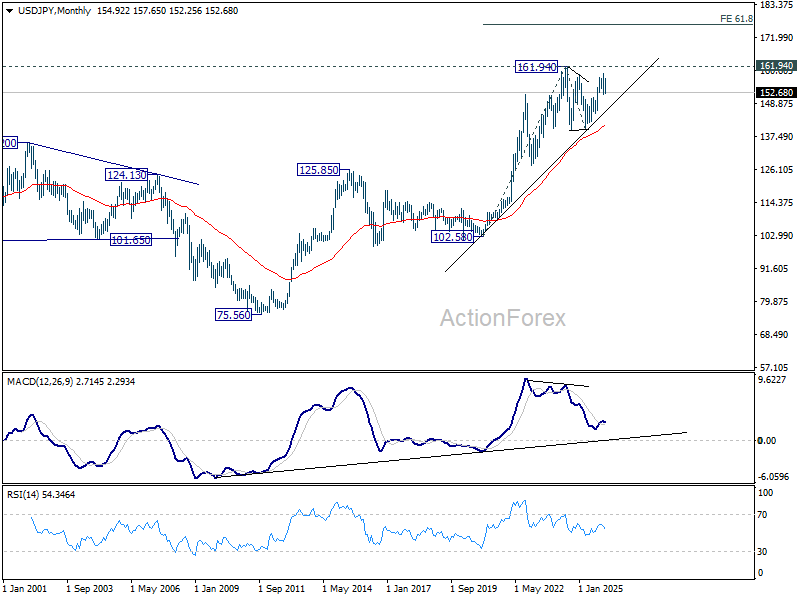

USD/JPY Weekly Outlook

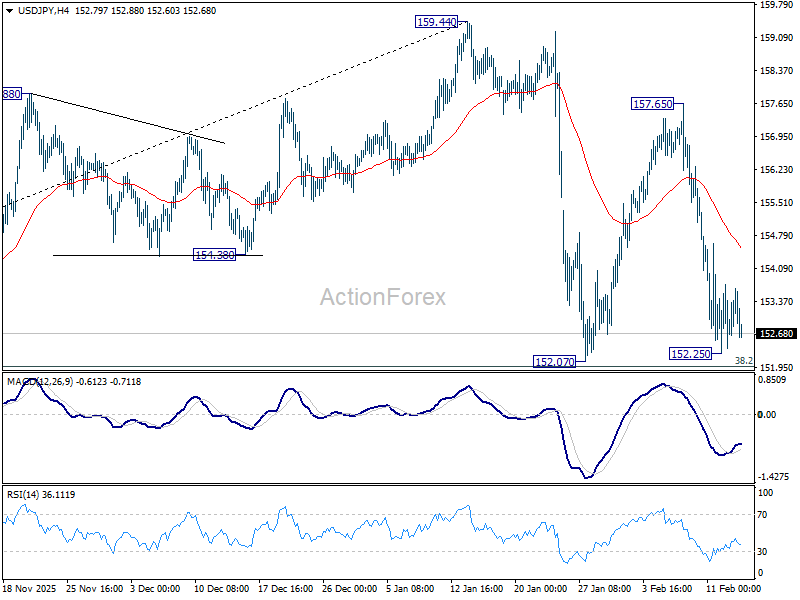

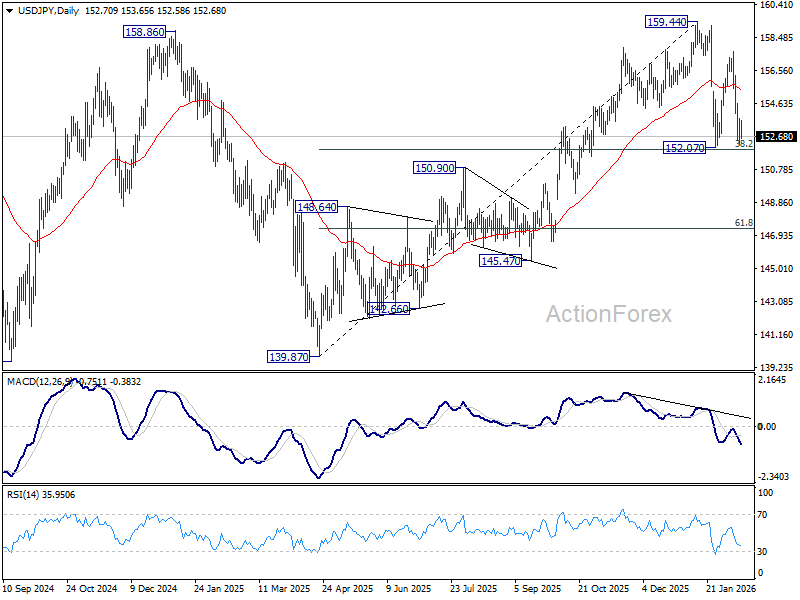

USD/JPY fell sharply last week but the decline lost momentum ahead of 152.07 support. Intial bias stays neutral this week first. With 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a consolidations pattern only. On the upside, sustained break of 55 4H EMA (now at 154.51) will bring stronger rebound towards 157.65. However, decisive break of 151.96 will argue that it's reversing the rise from 139.87 already. In this case, deeper fall should then be seen to 61.8% retracement at 147.34, and possibly below.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.71) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resumption. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

GBP/USD Weekly Outlook

GBP/USD stayed in range above 1.3507 last week and outlook is unchanged. Initial bias stays neutral this week first. On the upside, firm break of 1.3732 will suggest that pullback from 1.3867 has completed as a correction at 1.3507. Retest of 1.3867 should be seen first. Firm break there will resume larger up trend towards 1.4284 key resistance. On the downside, however, sustained trading below 55 D EMA (now at 1.3509) will raise the chance of larger scale correction, and target 1.3342 support for confirmation.

In the bigger picture, rise from 1.0351 (2022 low) still in progress and should target 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.3051 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

USD/CHF Weekly Outlook

USD/CHF stayed in consolidations from 0.7603 last week. Initial bias stays neutral this week first. Stronger rebound cannot be ruled out but upside should be limited by 55 D EMA (now at 0.7861) to complete the pattern. On the downside, break of 0.7603 will resume larger down trend, and target 0.7382 projection level next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

AUD/USD Weekly Report

AUD/USD edged higher to 0.7146 last week, but subsequent retreat indicates short term topping, on bearish divergence condition in 4H MACD. Initial bias remains neutral this week for consolidations, and deeper retreat might be seen. But downside should be contained above 0.6896 support to bring another rally. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above.