Sample Category Title

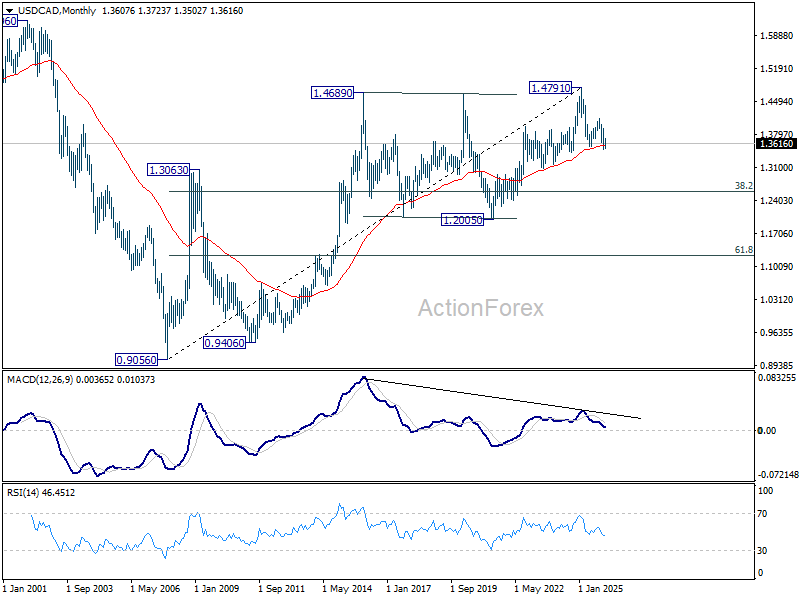

USD/CAD Weekly Outlook

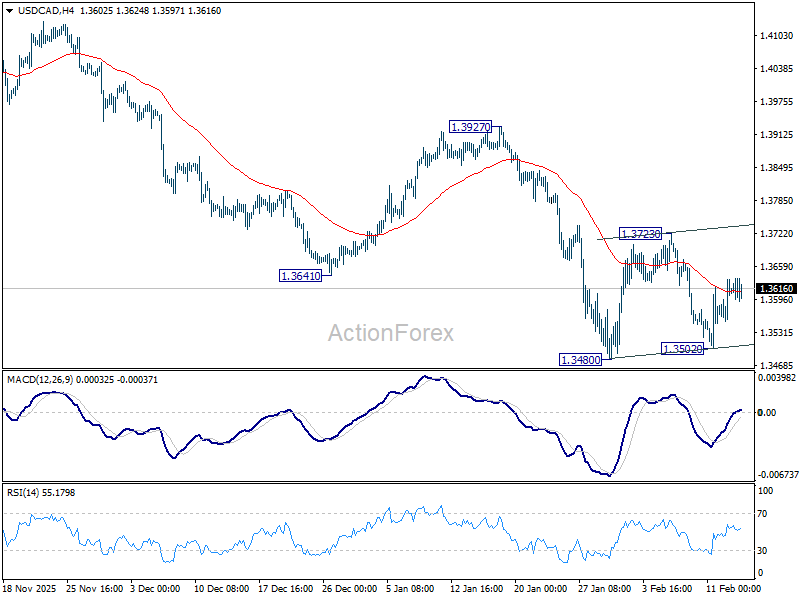

USD/CAD extended the consolidation pattern from 1.3480 last week. Initial bias stays neutral this week first. While stronger rebound cannot be ruled out, upside should be limited by 55 D EMA (now at 1.3752) to complete the pattern. On the downside, firm break of 1.3480 will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

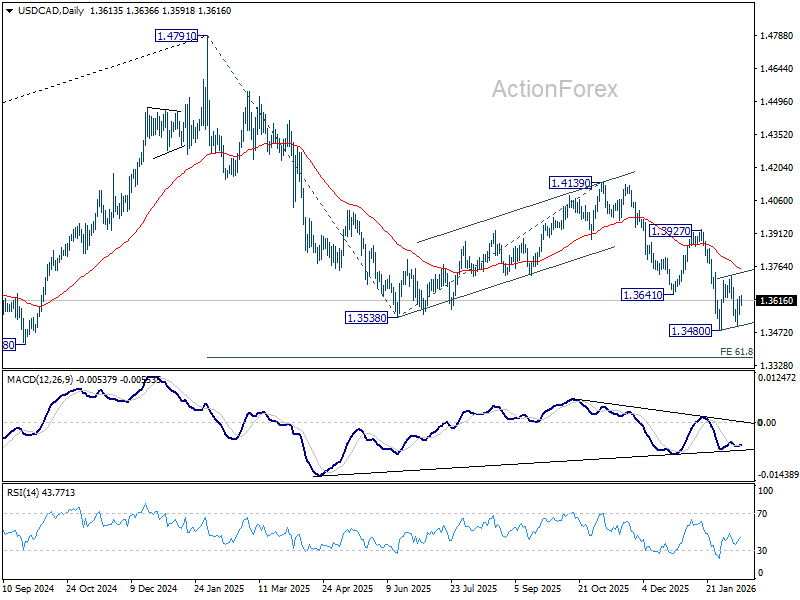

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

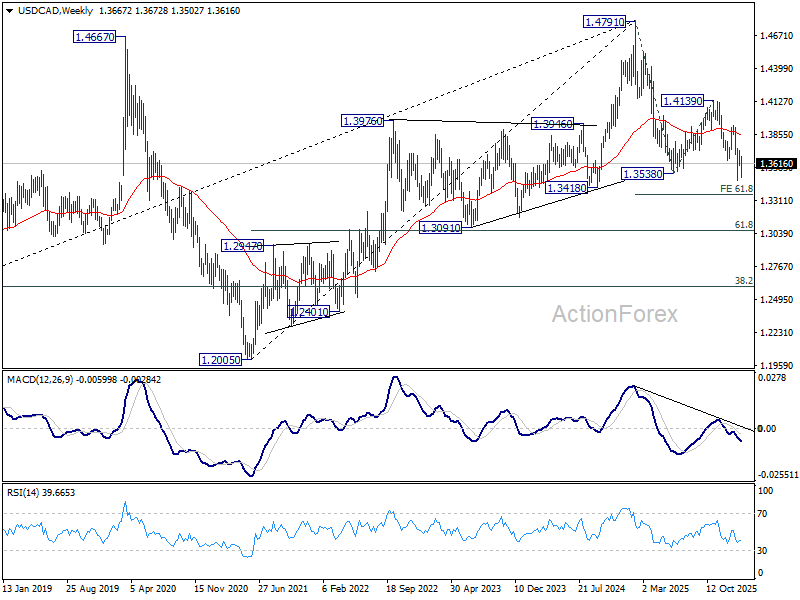

In the long term picture, rising 55 M EMA (now at 1.3569) remains intact. Thus, up trend from 0.9056 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

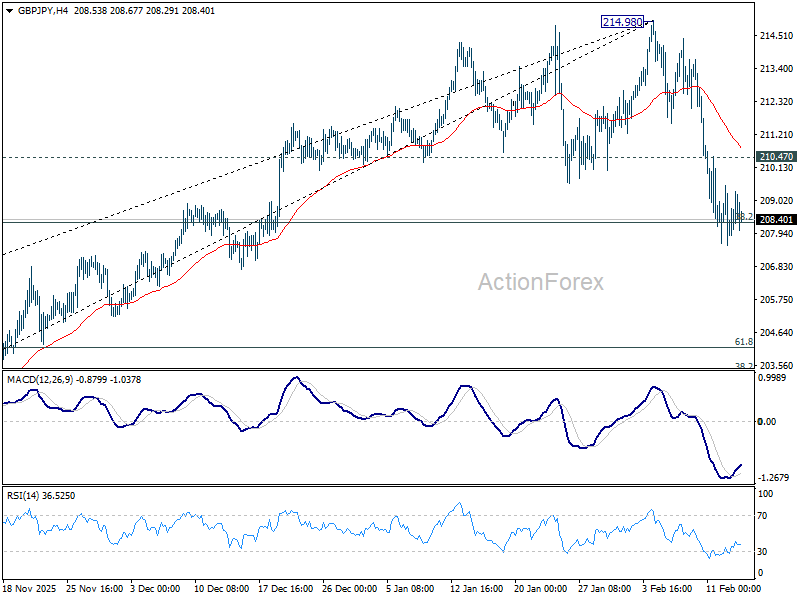

GBP/JPY Weekly Outlook

GBP/JPY's fell sharply last week but the decline halted after hitting 38.2% retracement of 197.47 to 214.98 at 208.29. Initial bias is neutral this week first. On the downside, sustained break of 208.29 will suggest that larger scale correction is already underway and target 203.27 fibonacci level. Nevertheless, strong rebound from current level, followed by break of 210.47 minor resistance will retain near term bullishness, and bring retest of 214.83/98 resistance zone.

In the bigger picture, considering the break of 55 D EMA (now at 209.96), a medium term top could be formed at 214.98. Deeper correction would be seen, but downside should be contained by 38.2% retracement of 184.35 to 214.98 at 203.27. On the upside, break of 214.98 will resume larger up trend from from 123.94 (2020 low), and target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90.

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 184.02) holds.

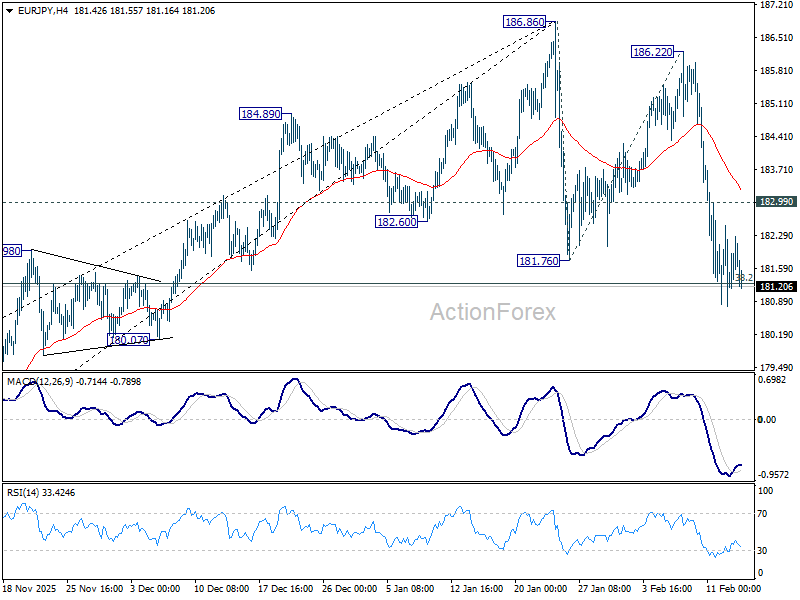

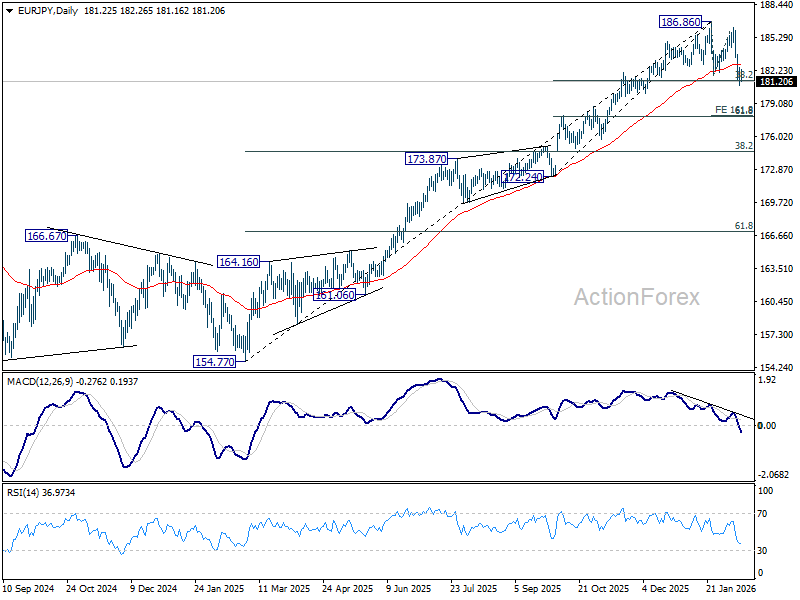

EUR/JPY Weekly Outlook

EUR/JPY fell sharply last week but the declined stalled after hitting 38.2% retracement of 172.24 to 186.86 at 181.27. Initial bias is neutral this week first. On the downside, sustained break of 181.27 will argue that fall from 186.86 is correcting whole up trend from 154.77. Next near term target will be 161.8% projection of 186.86 to 181.76 from 186.22 at 177.96. Nevertheless, strong rebound from current level, followed by break of 182.99 minor resistance will retain near term bullishness, and bring retest of 186.86 high first.

In the bigger picture, considering bearish divergence condition in D MACD and break of 55 D EMA (now at 182.67), a medium term top could be formed at 186.86 already. Deeper correction would be seen but downside should be contained by 38.2% retracement of 154.77 to 186.86 at 174.60 to bring rebound. Meanwhile, firm break of 186.86 will resume larger up trend to 78.6% projection of 124.37 to 175.41 from 154.77 at 194.88 next.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

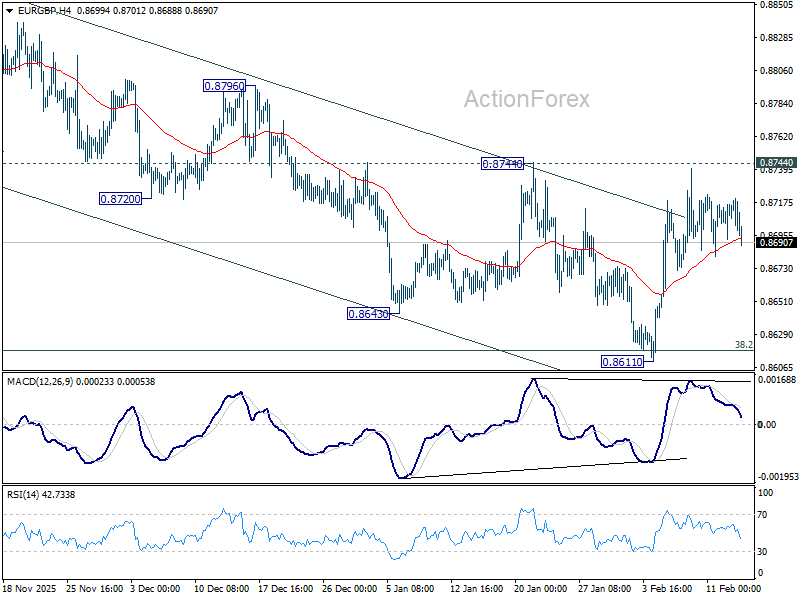

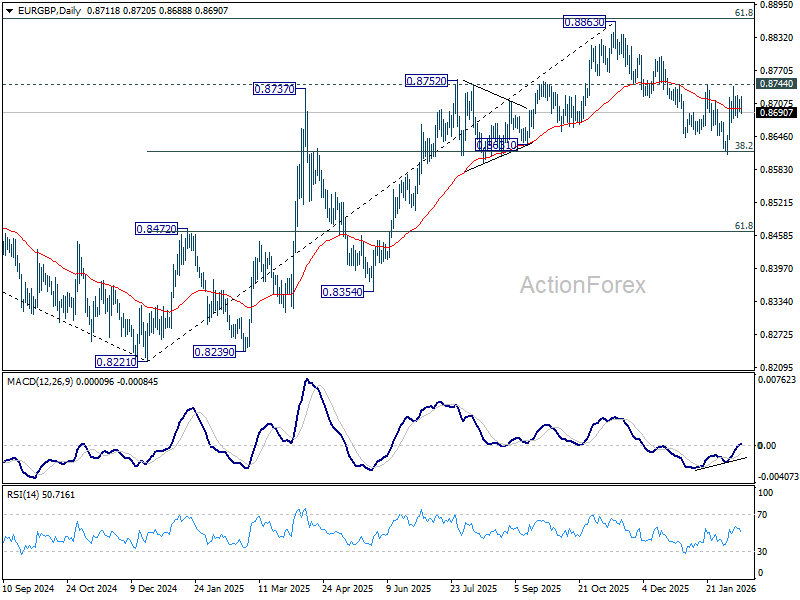

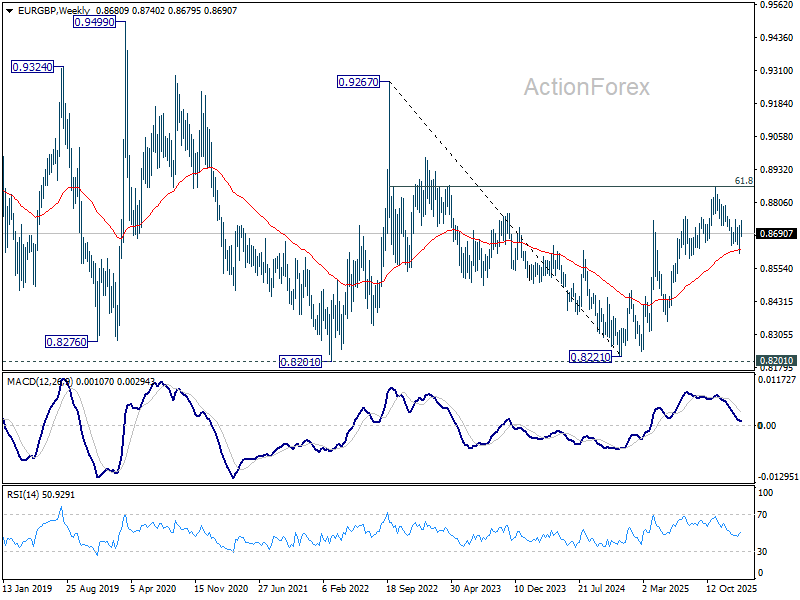

EUR/GBP Weekly Outlook

EUR/GBP edged higher last week but failed to break through 0.8744 resistance. Initial bias remains neutral this week first. Firm break of 0.8744 will indicate that fall from 0.8863 has completed as a correction. Further rally should then be seen back to retest 0.8863 high. On the downside, sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8629) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

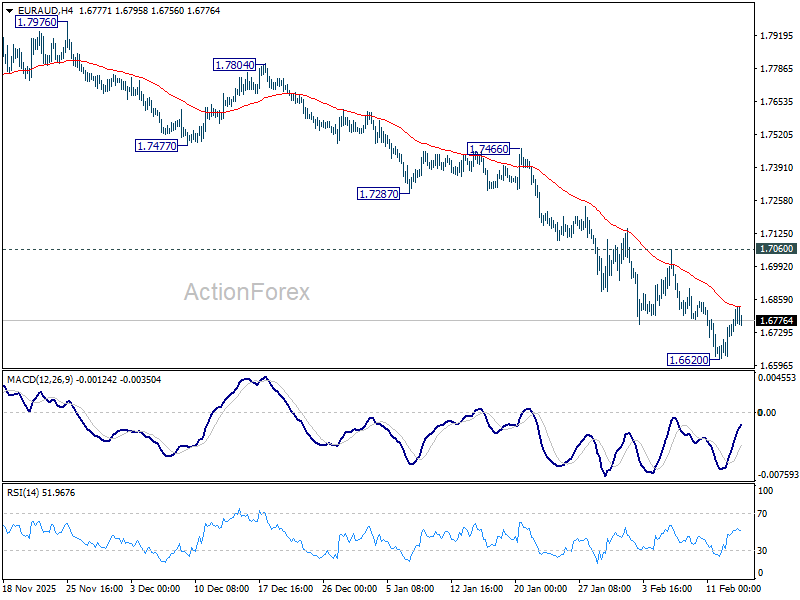

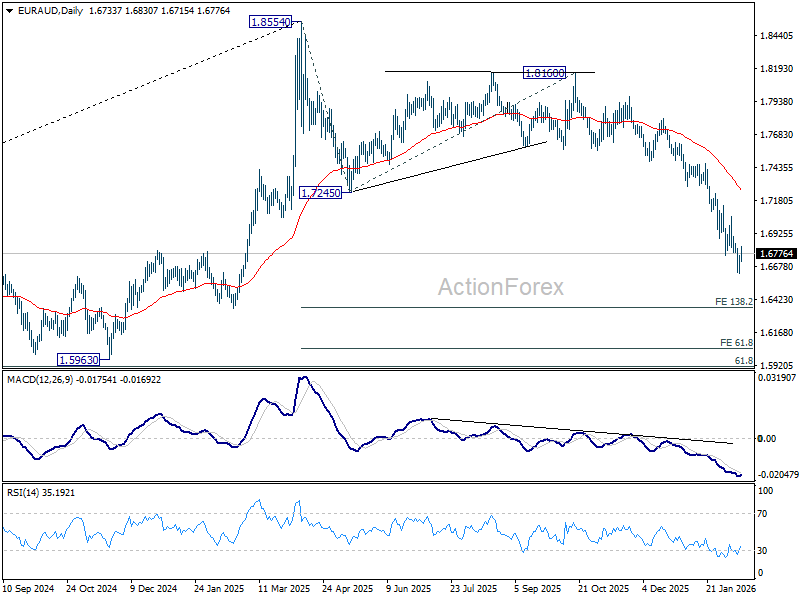

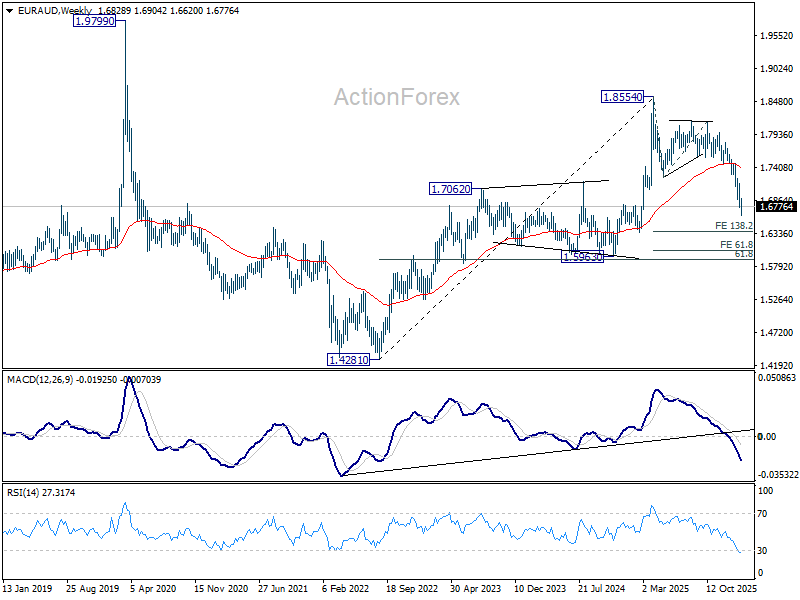

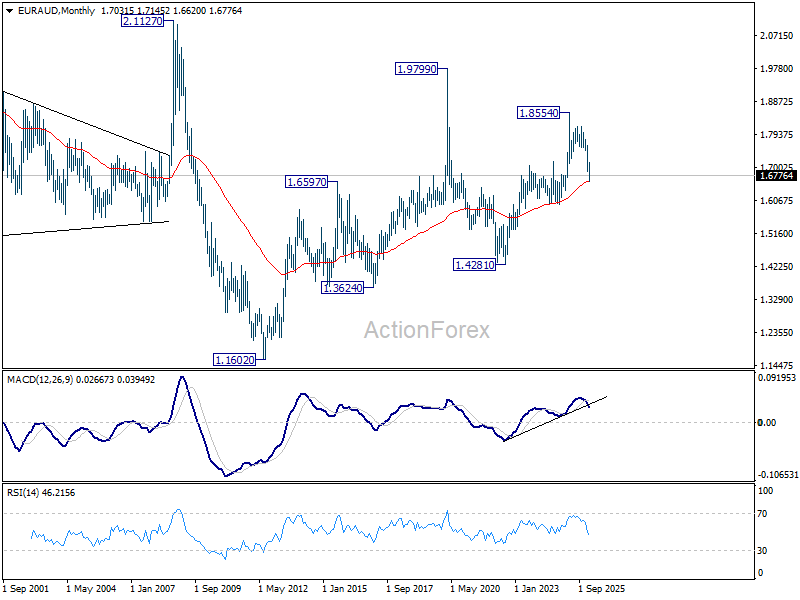

EUR/AUD Weekly Outlook

EUR/AUD's decline resumed last week and hit 1.6620, but recovered since then. Initial bias remains neutral this week for consolidations. Outlook will stay bearish as long as 1.7060 resistance holds. Break of 1.6620 will resume larger down trend from 1.8554 to 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 next. However, firm break of 1.7060 will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Current development argue that it has already completed at 1.8554. Sustained trading below 55 M EMA (now at 1.6603) will confirm this bearish case, and pave the way back towards 1.4281.

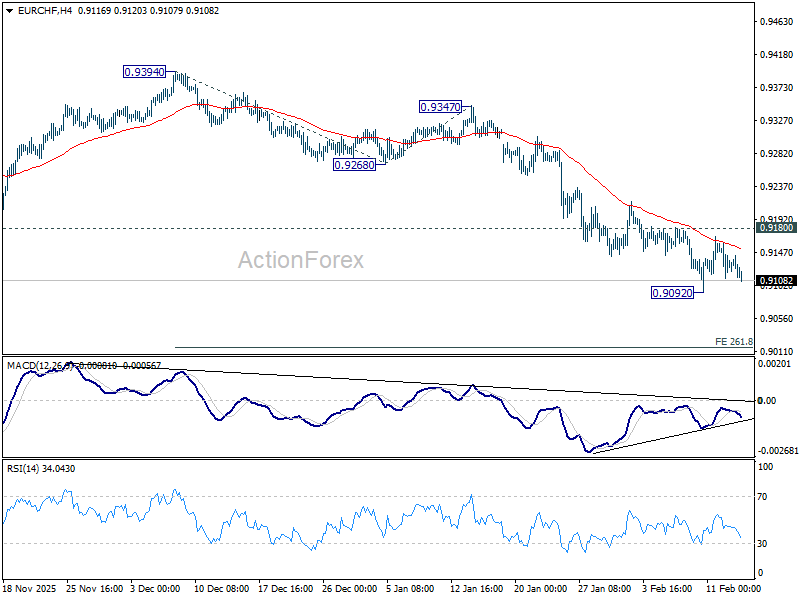

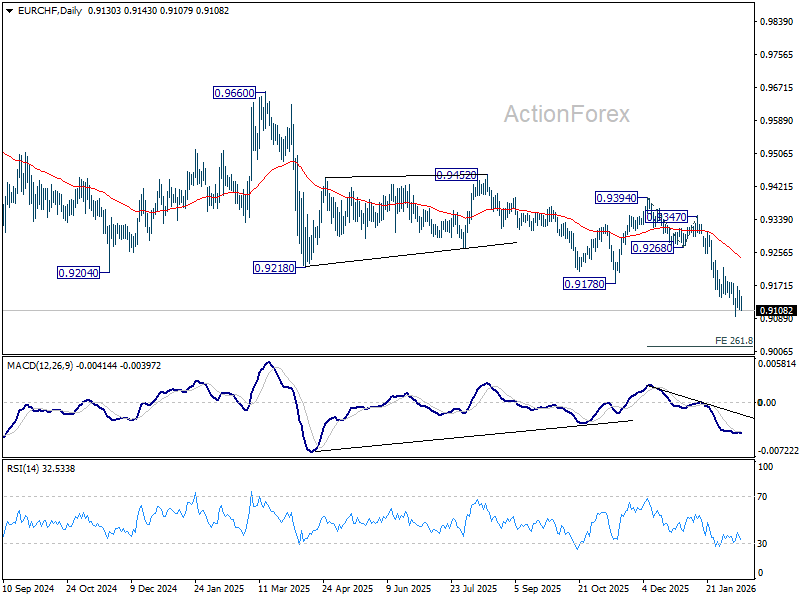

EUR/CHF Weekly Outlook

EUR/CHF's down trend resumed last week and dived to 0.9092, but recovered from there. Initial bias stays neutral this week first, and more sideway trading could be seen. Outlook will remain bearish as long as 0.9180 resistance holds. Firm break of 0.9092 will target 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. However, considering bullish convergence condition in 4H MACD, firm break of 0.9180 will indicate short term bottoming, and bring stronger rebound towards 55 D EMA (now at 0.9241).

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9333) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

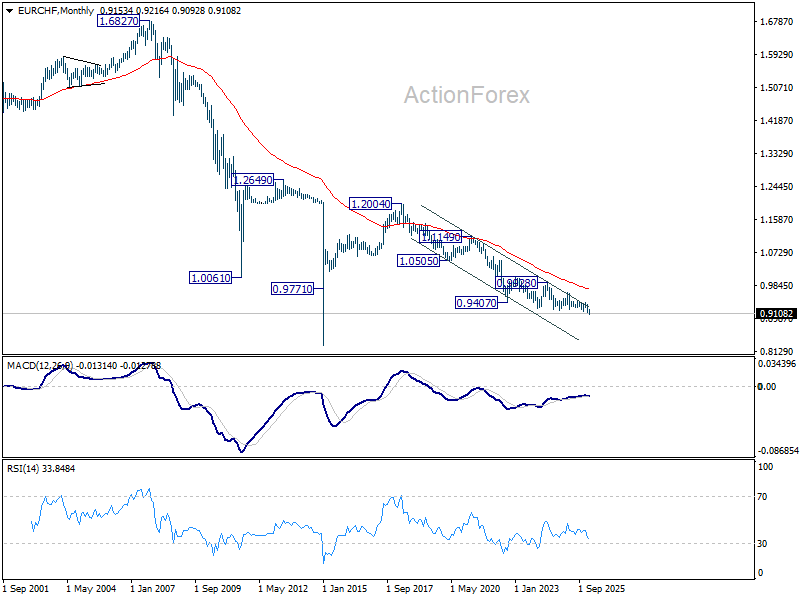

In the long term picture, EUR/CHF is also holding well inside long term falling trend channel. Down trend from 1.2004 (2018 high) is still in progress. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9739) holds.

Supreme Court Tariff Decision and Key Tests Ahead – Markets Weekly Outlook

- Discover our Weekly Market Outlook, exploring themes and events that forged financial flows throughout the week.

- After a volatile stretch, traders buckle for a heavy-slate of US data.

- Get ready for next week's action by exploring upcoming events across global Markets.

Week in review – Volatile swings and deleveraging continue

Markets are subject to particular waves of volatility in the past weeks, as years of upward trajectories and the recent acceleration are now questioning extreme valuations.

The culprit? Artificial Intelligence.

What had been a boon for Stocks is now coming back to bite the investor where it hurts, with investors realising that AI won't just be an upside-only catalyst.

Productivity gains by AI are now turning into fears of destruction for many firms, industries, and their components – Look at Tech and Softwares, straight-up bleeding since October.

The Tech Sector is bleeding. 3-month Performance – Courtesy of Finviz

High investments and Capital Expenditures that were seen as only positive are now being targeted by profit-takers and short-sellers, as investors question how long it will take to materialize into profits.

This comes amid times when OpenAI, the founder of ChatGPT, is under heavy scrutiny for its fast-paced cash burning, and it gets even more damaging when OpenAI is pretty much the firm that started this entire AI trend to begin with.

In other words, AI won't just allow Markets to shoot higher eternally.

Some firms and industries will face pain ahead as the global economy prepares for an existential restructuring.

If and when large numbers of firms see their activities stolen by revolutionary technology, it could not only lead to massive layoffs and reduced consumption but also trigger cascades of entire industries unable to function correctly, resulting in lower profits and, in turn, an inability to repay their heavy debt levels.

This could quickly turn into a global liquidity and credit crisis – but for now, it's mostly fear: fear of creative destruction, which is for now still lifting global earnings to all-time highs.

To put things into perspective, the Dow Jones still reached a 50,000 all-time high just last week, and Nasdaq is still well below 10% to its record, so for now, it's only a turn in narrative – With Stock Indexes maintaining a broadly rangebound picture, it's essential to take a step back and not get too afraid too fast.

Dow Jones (CFD) Daily Chart – February 13, 2026 – Source: TradingView

Markets are all about risk, so too little risk could prevent seizing good opportunities.

And in any case, volatility is great, not for investors, but for traders who will enjoy more movement.

The narrative could also change quite suddenly, particularly after today's soft CPI print (2.4% vs 2.5% expected), which could finally wake the soft-landing hypothesis, especially with Non-Farm Payrolls beating expectations on Wednesday.

A harsh reality is settling in, and traders will have to keep that in mind when trading: in the times to come, price action will dominate the narratives, so always look at the bigger picture (and check higher-timeframe charts) to stay ahead of what's to come.

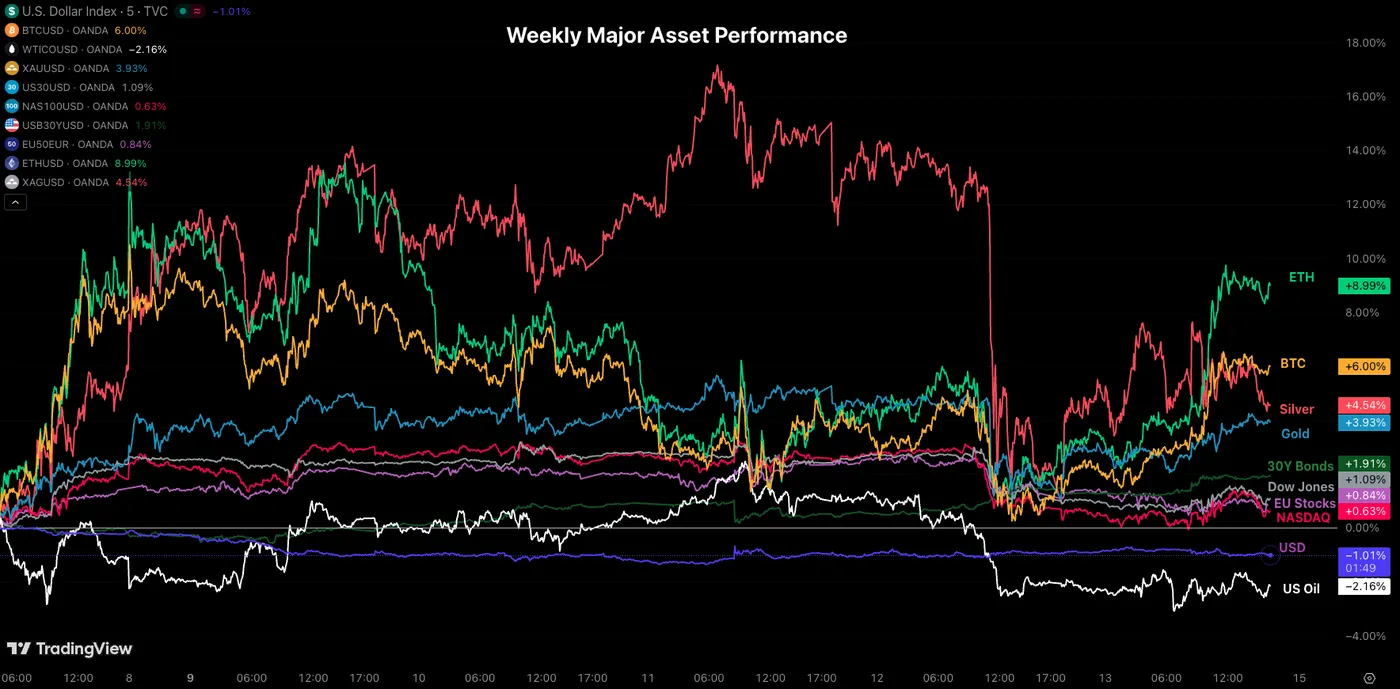

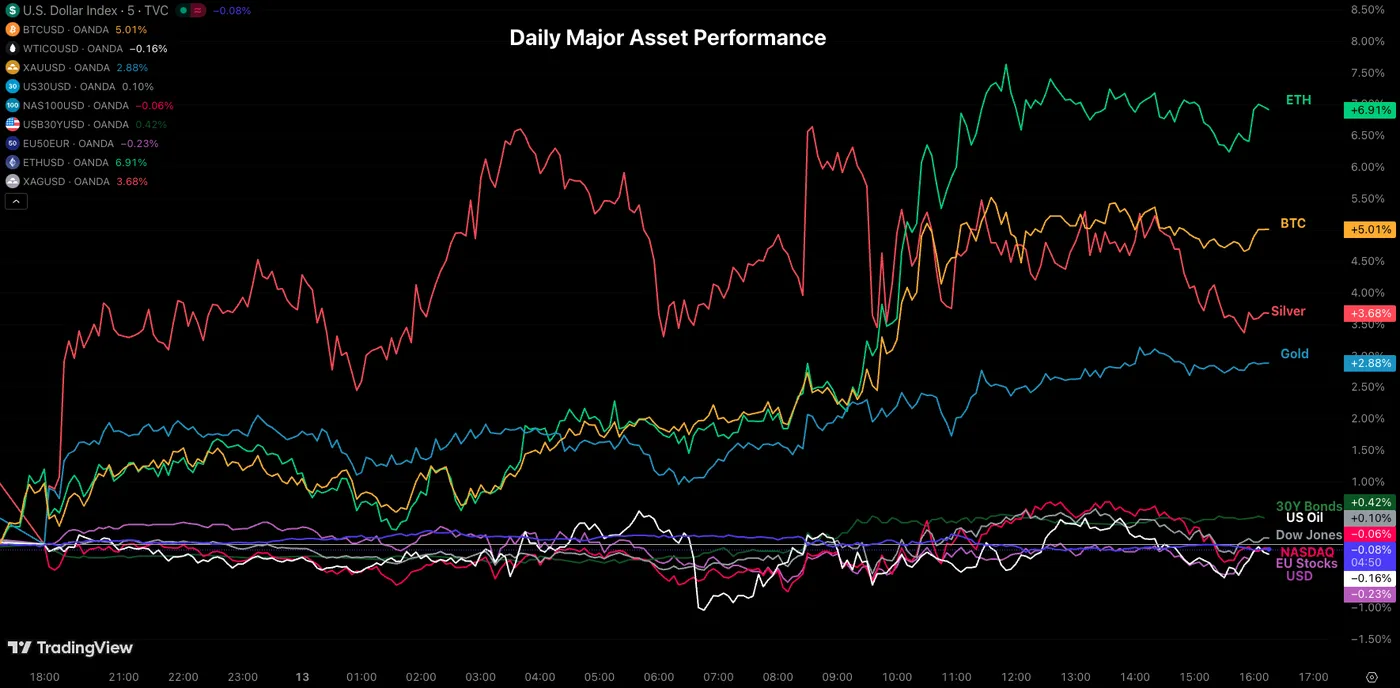

Weekly Performance across Asset Classes

Weekly Asset Performance – February 13, 2026 – Source: TradingView

Most of the assets which got beaten down last Friday attempted a rebound in this week's action.

The best examples of this are of course Cryptocurrencies and Metals, which suffered heavily last week and are up between 3% to 8% on the week.

What also really shifted is the sudden interest in US Treasuries, which could launch a wave of repositioning.

Bonds had widely been left out of the everything rally in the past three years, bullied by risk-assets and elevated inflation, so keep a close eye to see if this changes.

The Week Ahead – Global Macro is back

Asia Pacific Markets – RBNZ Rate Decision and Australian Employment

Traders are getting ready for quite a heavy week for APAC trading.

Sunday will commence with the Japanese GDP for Q4 where traders will now spot whether the effect of Takaichi's appointment turned into a positive for the Land of the Rising Sun.

Looking at how the JPY bounced last week, expect large reactions.

Monday will present the RBA Minutes, pretty important for FX traders particularly considering that the Australian Central Bank is the only one back to hiking.

The Aussie will also see an important test on Wednesday with its employment figures, essential to track whether last hike was just a one off or the beginning of a new cycle.

Tuesday however brings the most important test for APAC traders, with the RBNZ Rate decision. It will be the first press conference for Anna Breman, the new RBNZ Governor.

She will also appear on Thursday so make sure to listen to how she communicates for further clues.

A reminder that Antipodean currencies (AUD and NZD) have rallied quite severely since the beginning of 2026. They will both face a huge test next week.

Europe and UK Markets – Major data for Great Britain

Despite some key releases for the Eurozone and Germany (Surveys and German CPI on Tuesday, key speeches and PPI on Friday), participants will keep focus on UK data.

Similar to the US last week, they will face a confluence of high-tier releases.

Starting Tuesday, Markets await their Employment data, followed by UK inflation data (CPI, PPI and Retail Price Index) before concluding the week with Retail Sales on Friday.

The release are all during the overnight session in North America (2:00 A.M. ET), so make sure to keep your risk in check.

And of course Euro traders will have to stay aware for Lagarde's speech on Sunday (early) morning.

North American Markets – US Core PCE, Supreme Court Decision on Tariffs and Canadian CPI

North American traders will also have some work to do next week.

Not mentioning the few speeches (keep an eye on Bowman Monday), the week really starts on Tuesday with Canadian CPI.

Swap traders are aware that any beat there could significantly add pricing for hikes in Canada for the year to come, particularly after this week's BoC Minutes where it was noted that the current 2.25% rate is on the "Stimulative side".

Turning back to the US, FOMC Minutes will be presented on Wednesday, and while they are not expected to be a Market mover, they could provide interesting views on Inflation, particularly considering how this week's CPI release changed the narrative.

In any case, traders will have to await for Friday before seeing the release of Major data, with a streak of US releases.

The weekly closing session will commence with Core PCE (where Markets await to see if there is any real improvement in the Fed's favorite inflation tracker).

Promptly after, US Services and Manufacturing PMIs will be on deck.

It has been announced just this morning that the Supreme Court will give the decision regarding Trump's tariffs next Friday. This will be a major market mover.

Even after the latest ease in narrative, keep a close eye on geopolitical developments, particularly those involving the US-Iran talks, as they are likely to continue influencing Commodity and broader Markets.

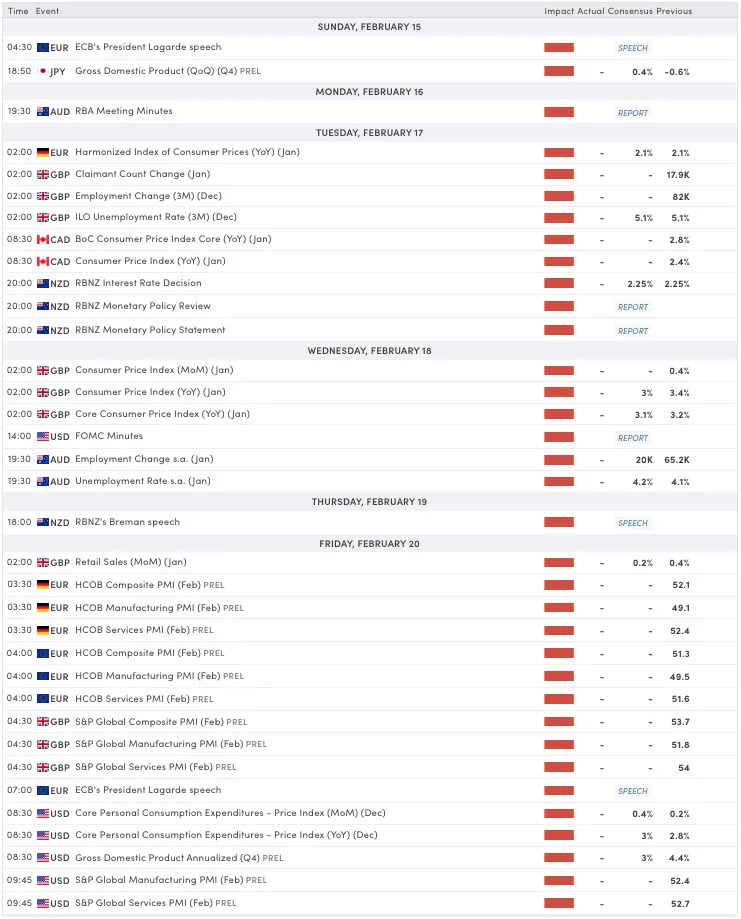

Next Week's High Tier Economic Events

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Friday 13 Market Wrap

Cross-Asset Daily Performance, February 13, 2026 – Source: TradingView

Today's session brought quite a shift in the Market, with today's inflation report allowing for struggling Stocks, Cryptos and Metals to rebound.

Stocks are however closing unchanged despite the very positive CPI report – This could be a rough sign for bulls.

The best outperformers there are of course Ethereum and Bitcoin which are both coming from very far after last week's tumble.

With FX remaining fairly muted, the US Dollar will be key to watch next week as traders await a repricing of FOMC cuts in 2026.

If it doesn't reach new lows next week, this sends a sign of relative strength for the Greenback, particularly with the upcoming Decision on Tariffs.

Safe Trades and enjoy your weekend!

The Weekly Bottom Line: Markets Blink, Jobs Hold Firm

Canadian Highlights

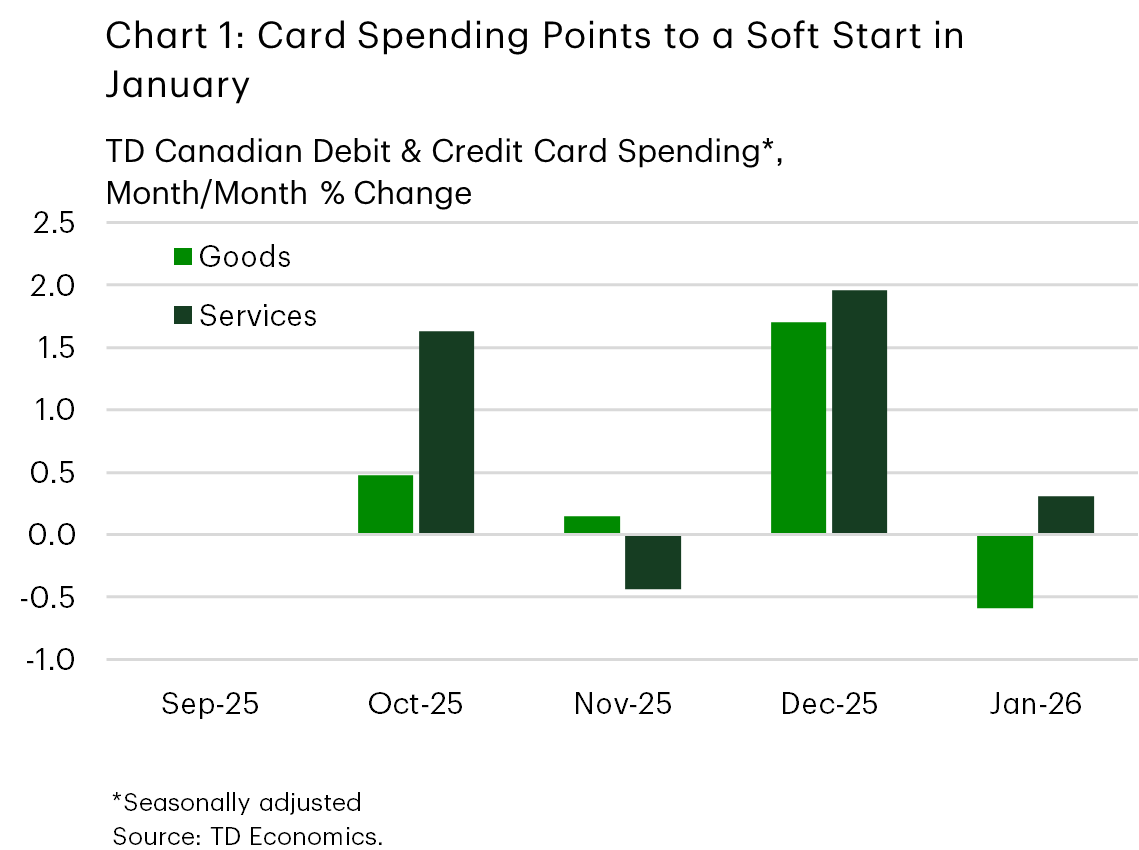

- The economic calendar was bare this week, but internal card spending data offered a glimpse into consumers early in 2026, suggesting a soft start to January.

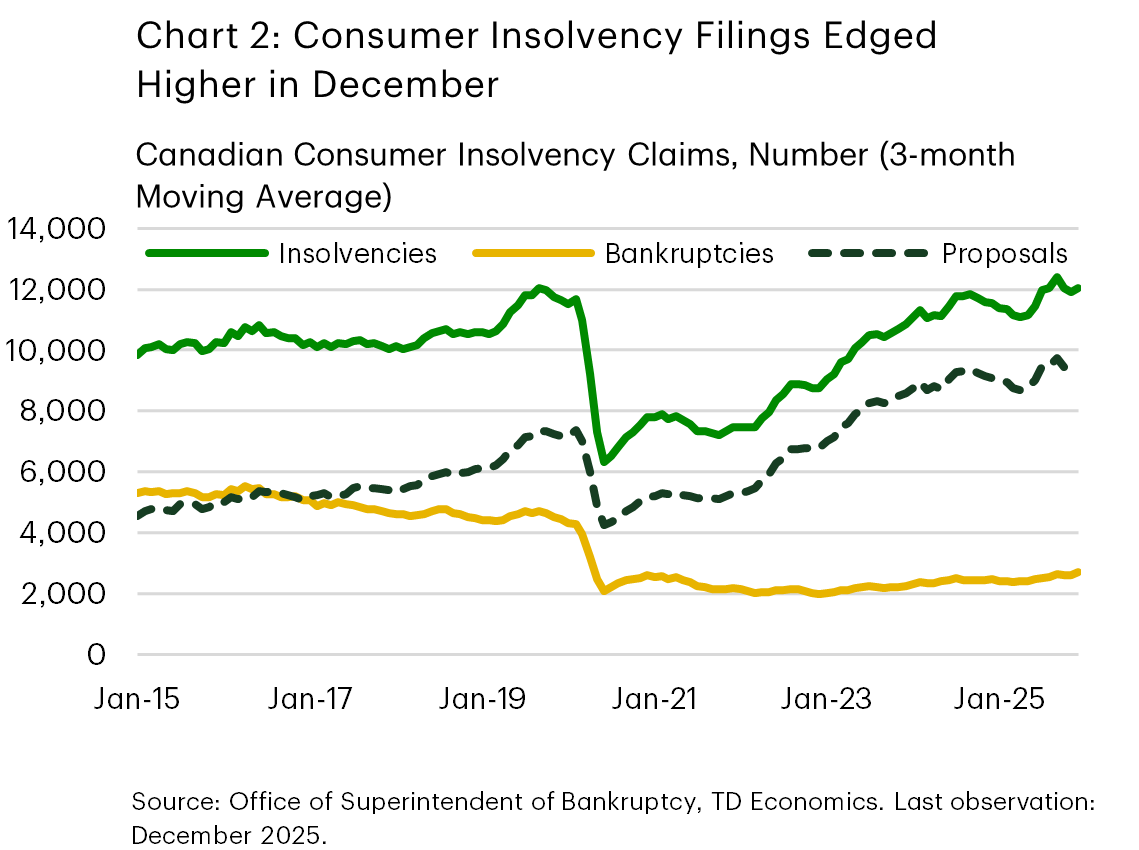

- December insolvency data showed that the three-month moving average trend in consumer filings started to rise again – worth watching, but not yet alarming.

- The next week promises to be far more eventful with a slew of data releases. With risks to inflation looking balanced ahead of January’s CPI update next week, we think the Bank of Canada has enough reason to stay on hold when it meets in March.

U.S. Highlights

- Financial markets sold off this week as developments in AI and tech raised doubts about future earnings.

- January’s employment report delivered a clear upside surprise, easing concerns that the labor market was rolling over after last year’s slowdown.

- In other important data releases, there were softer signals from consumer spending and housing. Inflation had a softer-than-expected headline number, but some cautionary signs of inflation pressures in the core.

Canada – A Week to Reflect

The shooting in Tumbler Ridge overshadowed all else this week, as Canadians mourned the victims of this tragedy. As a result, the Prime Minister postponed his planned defence-industrial strategy announcements, and with no economic data on the calendar, the week was somberly quiet.

Markets, though, kept moving. Canadian equities fluctuated over the week but are set to finish with more than 1% gain. The bond markets followed suit, with the 10-year Government of Canada yield falling roughly 15 basis points to 3.25% (yields move inversely to prices).

With the data calendar bare, it’s a good moment to step back and frame the bigger picture. We expect Canada’s economy to remain lukewarm in 2026, with a bit more heat by year-end. Our forecast sees the economy ending next year about 1.4% larger than in 2025, although with the coming CUSMA review likely to be bumpy, the risks to growth are tilted to the downside.

Business investment remains subdued amid lingering trade uncertainty and slower population growth is capping employment gains. But there are also reasons for optimism. Government spending is poised to provide support toward the end of 2026, and household spending remains one of the more stable pillars of the economy. TD card spending data point to a relatively solid December, with gains concentrated in services – particularly recreation and travel (Chart 1). Travel stayed strong in January too, as Canadians fled the winter storms for warmer destinations. Card spending on goods was firm in December, but softened in January, likely reflecting weather-related disruptions and reduced willingness to venture out. This sits somewhat at odds with the December retail sales flash estimate, which signaled a contraction. But auto sales, which were soft according to industry data, are included in retail sales and likely explain the gap. We also see a pullback in holiday-related categories such as clothing and electronics after strong December gains.

Above-trend growth in personal income and solid wealth gains helped support this spending. Still, not everyone is on solid ground. December insolvency data consumer filings rose 16% month-on-month. On a three-month moving average, filings rose 1.6%, reversing declines in the prior two months (Chart 2). The increase was driven by consumer proposals, though bankruptcies edged higher as well. While this bears watching, the trend is not yet alarming. Population-adjusted insolvency rates remain below pre-pandemic levels. Notably, bankruptcies are still historically low, with most of the rise coming from proposals – a mechanism that allows households to retain assets, maintain structured repayment plans, and face a comparatively milder hit to credit ratings.

Despite being short, next week promises to be far more eventful, with releases on inflation, merchandise trade, housing starts, home sales, and retail trade. Inflation bears close watching ahead of the Bank of Canada’s rate decision on March 18th. With inflation risks roughly balanced ahead of next week’s CPI, the central bank is right to share the Valentine’s Day spirit: committed but not quite ready to make a big move.

U.S. – Markets Blink, Jobs Hold Firm

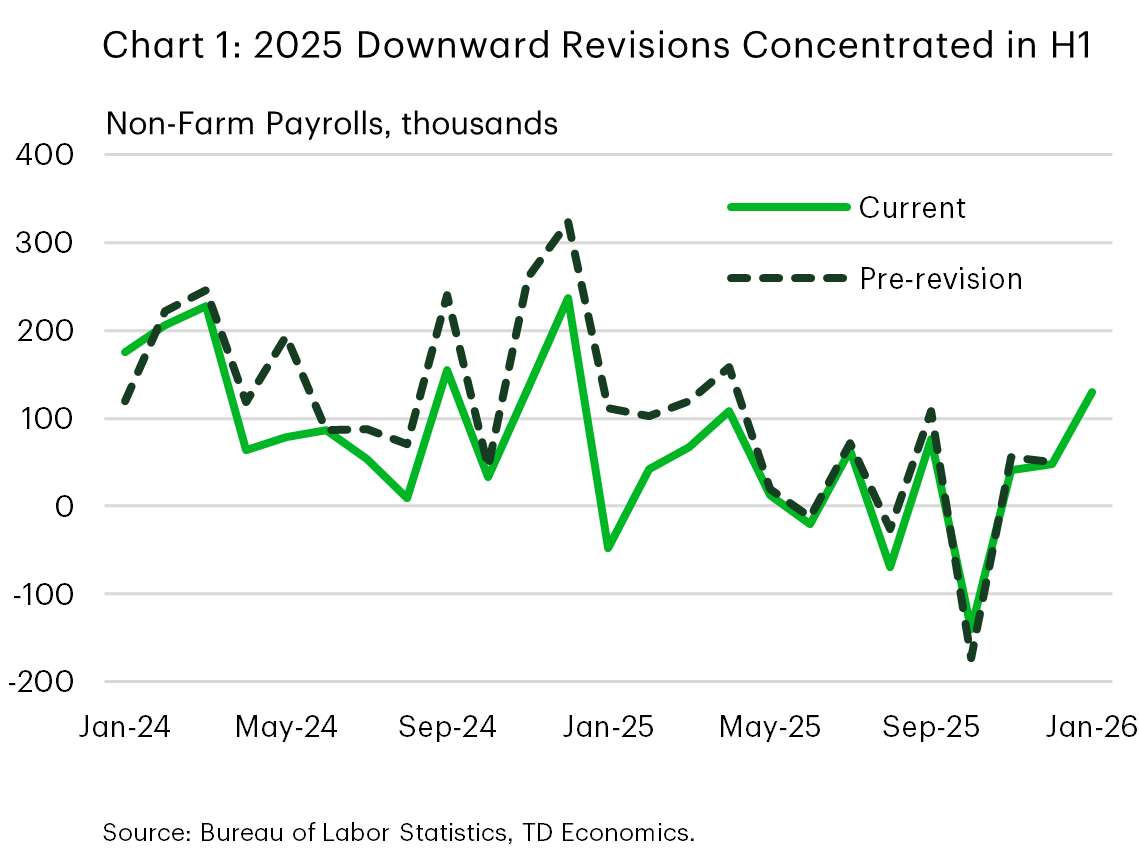

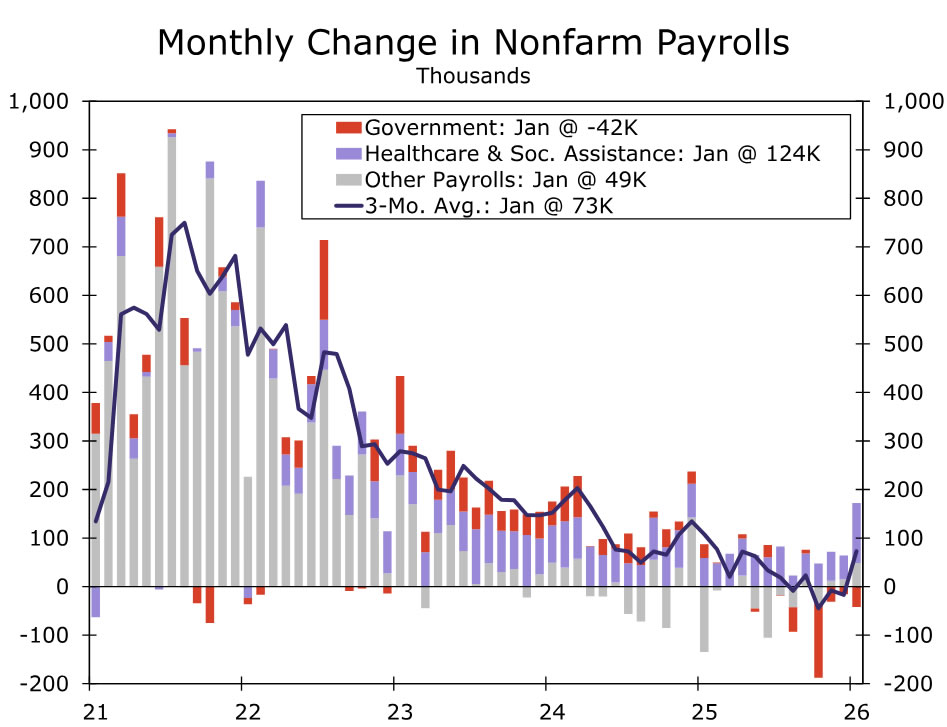

Financial markets endured a rough patch this week, with a broad sell off across equities reflecting anxiety about the threat AI could pose to earnings and employment, the path of interest rates, and the durability of the ongoing expansion. That market reaction stood in contrast to the message from the January employment report. Payrolls growth came in well ahead of expectations, accompanied by a further dip in the unemployment rate. While revisions did reveal that job growth over much of 2025 was weaker than previously thought, the January rebound suggests that labor demand remains intact (Chart 1).

The rest of the data flow painted a more mixed picture of the economy. Headline CPI inflation came in softer than expected this morning, but core CPI picked up the most since August. Services inflation heated up while core goods inflation (excluding used vehicles) rose at its fastest monthly pace in nearly a year. The inflation report comes at a pivotal moment, as reports that the Trump administration may scale back its steel and aluminum tariffs suggest the administration is conscious of inflation risks.

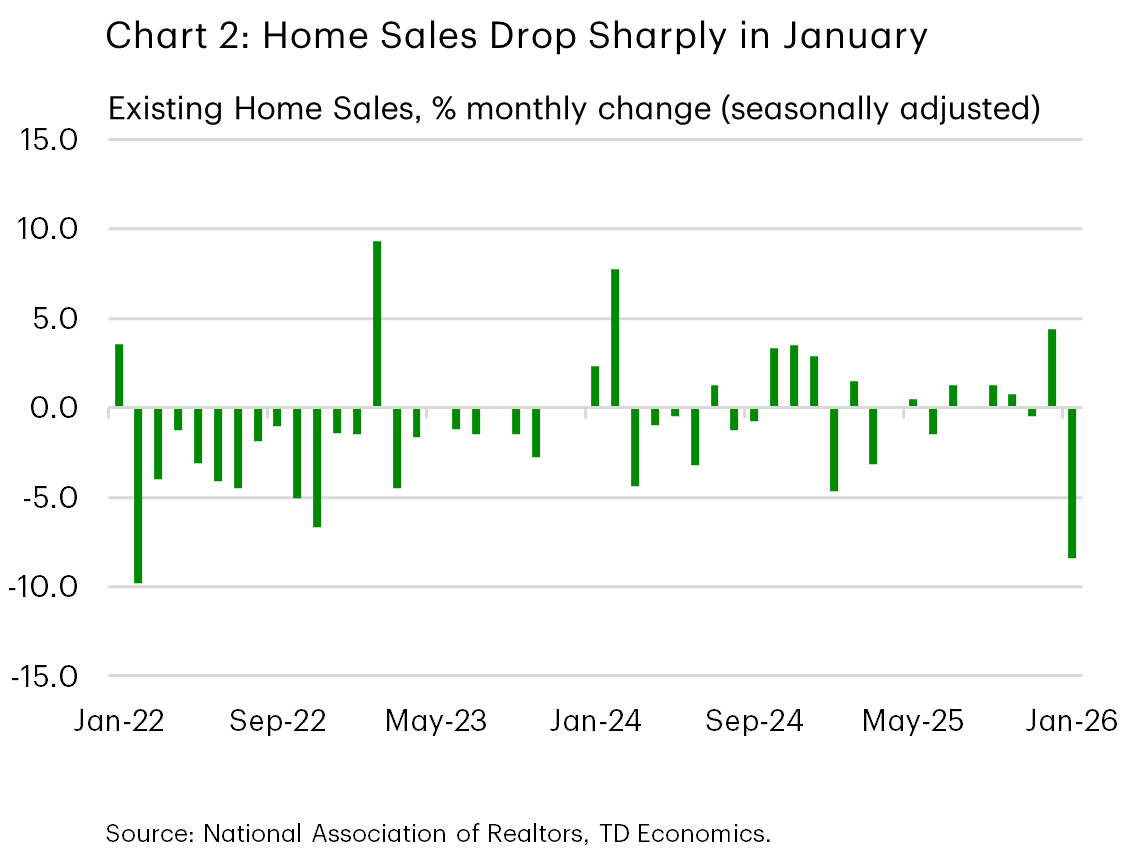

Retail sales ended 2025 on a soft note. December sales were flat after a solid November, and downward revisions tempered the momentum implied by earlier releases. Housing data were also notably weak. Existing home sales posted their largest monthly decline in nearly four years in January, reflecting a combination of affordability constraints and bad weather (Chart 2).

Markets, meanwhile, struggled to reconcile the week’s macro data with a less accommodating policy backdrop. The equity sell off reflected concerns about growth-sensitive sectors and fear that advancements in AI may dislodge large incumbents across a wide swath of the economy, and a reassessment of the path for interest rates following a string of Fed communications. Market pricing for the Federal Reserve to reduce rates in its June meeting have fallen from 60% to around 50% over the course of this week. Speeches this week from Federal Reserve officials revealed a balance of opinion. More hawkish voices stressed that inflation remains above target and warned against premature easing, while others acknowledged that, even with a strong jobs report, there is still an argument for rate cuts later this year if disinflation continues. On balance, we read the prevailing sentiment from Fed officials as one of patience rather than urgency, but still hold on to our call for a rate cut in June. This morning’s softer CPI release may help move the Fed’s perceived balance of risks slightly towards easing, particularly if the disinflationary pressure were to persist over the coming months.

Looking ahead, our eyes will be on next week’s release of the FOMC meeting minutes, which should provide additional insight into how policymakers have been weighing inflation risks against signs of labor market stabilization. And next Friday’s PCE inflation and consumer spending data will be helpful in assessing the durability of consumer spending and the extent of momentum in recent inflation data.

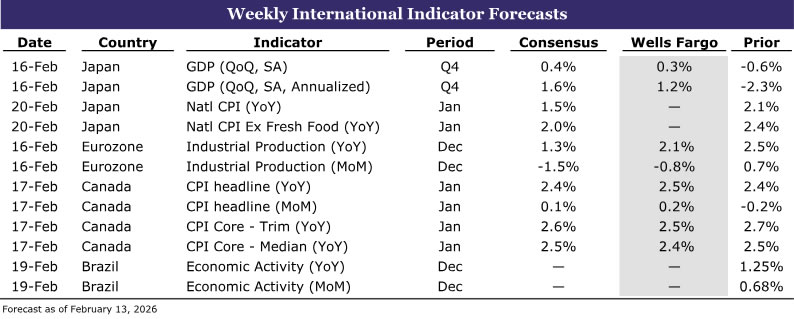

International Week Ahead: Growth Rebound to Keep BoJ Hikes in Play

Summary

International Week Ahead

- Japan Q4 GDP: Growth Rebound to Keep BoJ Hikes in Play • (02/16)

- Canada January CPI: Noisy Headline and Cooling Core to Give BoC Breathing Room • (02/17)

- Brazil December Activity: Year-end Momentum to Influence Early ’26 BCB Policy • (02/19)

- Banxico February Meeting Minutes: Cryptic Communications, but Perhaps Minutes Clear the Smoke? • (02/19)

G10

Japan Q4 GDP • Monday

Growth Rebound to Keep BoJ Hikes in Play

While both we and consensus expect a rebound in Q4-2025 following the quarter-over-quarter annualized 2.3% contraction in Q3, we forecast a milder recovery of 1.2% versus 1.6% for consensus. The contraction in Q3 was driven largely by weaker net exports after shipments were pulled forward into Q2 ahead of anticipated U.S. tariffs. With tariffs lowered in July 2025, the drag from net exports should ease and turn supportive, while January trade data points to continued strength in global semiconductor demand, underpinning exports. Domestically, business sentiment has improved, as shown in the Bank of Japan's (BoJ) Q4 Tankan survey, which should translate into firmer business investment. Additionally, the front-loading of construction and residential investment ahead of new environmental regulations introduced in Q2 should also have faded, supporting a broader improvement in investment. Taken together, stronger exports and higher investment should be sufficient to drive a rebound in Q4 growth. A return to growth would keep BoJ rate hikes in play, though the broader policy backdrop warrants caution. The Takaichi administration’s recent landslide victory has revived concerns around expansionary fiscal policy, contributing to upward pressure on yields and pushing 10-year JGBs to historical highs. However, if new debt issuance is avoided, as the administration has indicated, the policy rate may not need to rise as much as markets currently expect. The BoJ is likely to proceed cautiously as it assesses fiscal developments and waits for clearer evidence of wage-price firming, particularly with inflation expected to cool further in data to be released next week due to government energy subsidies and stabilizing food prices. We maintain our base case for a 25 bps rate hike by Q3-2026, bringing the policy rate to 1.00%.

Canada January CPI • Tuesday

Noisy Headline and Cooling Core to Give BoC Breathing Room

We expect headline inflation to rise in Canada to 2.5% in January from 2.4% in the previous month as base effects peak. Base effects reflect the lowering of prices between December 2024 and February 2025 because of the temporary GST/HST holiday. Elsewhere, measures of underlying inflation such as the trimmed and weighted median inflation are likely to decline to 2.5% year-over-year and 2.4%, respectively, from 2.7% and 2.5% in December. The temporary rise in year-over-year headline inflation is likely to keep the market and consensus baseline view for an on hold Bank of Canada (BoC) intact near-term. We believe these base effects are worth about 0.6-0.8 percentage points and imply a substantial stepdown in inflation as early as the February report. It’s notable that underlying inflation as suggested by the 3m average of trimmed and weighted median inflation are running at 1.45% and 1.85% respectively vs. 6m averages around 2%. We believe headline inflation is likely to step down to below 2% as soon the February report (1.8% per our nowcast). As such, the macro narrative is likely to shift from the noise of elevated headline inflation to cooling underlying core inflation. This, combined with sub-trend growth, economic slack and downside risks to growth from continued trade uncertainty with the US, we see greater room for the BoC to cut rates than hike. Current policy rate at 2.25% is within the range of neutral rate estimates (2.25-3.25) for an economy that is likely undergoing a structural transition with more to come as USMCA negotiations continue. On the flip side, a faster rollout of fiscal stimulus is likely to contain downside risks and reduce the need for deeper rate cuts.

EMs

Brazil December Activity • Thursday

Year-end Momentum to Influence Early ’26 BCB Policy

The December activity index is likely to show Brazil’s economy lost steam at the end of last year. Uber-restrictive monetary policy settings and limited fiscal stimulus as well as pre-holiday spending rolling off should push the activity index lower relative to the prior month. We will be attentive to the activity index as data will fill in the rest of the economic story for Q4 as well as how Brazil’s economy performed for all of 2025. But more importantly, the December activity index will act as the last major gauge of activity that Brazilian Central Bank (BCB) policymakers will be able to assess before meeting in March. Inflation takes precedence for the BCB, but policymakers have committed to cutting interest rates at the March Copom with the only outstanding question being how aggressive policymakers want to lower the Selic Rate. December activity could play a more influential role this time around as recent commentary from BCB policymakers leave the door open to move gradually with a 25 bps cut or remove monetary policy restriction quicker by starting with a 50 bps rate reduction. For us, we believe policymakers will opt for caution and deliver a 25 bps cut, but we could be swayed toward a 50 bps cut come March if activity is especially weak. Right now, markets lean only slightly toward the BCB lowering the Selic Rate by 50 bps, so the activity index could reinforce calls for a larger move or dial back near-term easing expectations. We hold a less dovish view on BCB monetary policy for all of 2026, which also means a more rapid pace of easing to start the year would also force us to recalibrate our YE-26 Selic Rate forecast.

Banxico February Meeting Minutes • Thursday

Cryptic Communications, but Perhaps Minutes Clear the Smoke?

Central bank meeting minutes rarely offer a ton of new insight into future interest rate decisions. Minutes are backward-looking and do not reveal which policymaker said what, a dynamic which is especially true for Banxico. As such, we do not expect anything groundbreaking to come out of February Banxico minutes, but the official statement as well as post-meeting communications are sending mixed messages and creating more smoke than clearing the fog. Maybe Banxico minutes next week will offer clarity? Again, skeptical, especially after policymakers left rates on hold earlier this month, told markets keeping rates unchanged may prove to be a “pause” in the easing cycle, all while revising their inflation forecasts sharply higher. Adding a bit more confusion to the mix are Banxico Deputy Jonathan Heath’s recent comments to a local bank. Heath appeared to shred Banxico’s inflation forecasts as unrealistic (again) this time going so far as to say “almost nobody believes that not only are we not going to meet the goal for Q2-2027, but not even in the next four, five or ten years.” He did, however, mention that if inflation evolves in line with Banxico’s inflation target, which has again been revised higher, a majority of members could opt to vote for a rate reduction at the next meeting in March. At least based on how Banxico framed its latest official statement, that appears to be the message it is sending to markets, according to Heath. If policymakers are willing to accept higher inflation, why not just cut in January? Why “pause.” Why bury any kind of guidance in a podcast? Confused? Us too. Markets seem to be pricing more Banxico easing after Heath’s comments, which we believe is a mistake. Banxico may wind up cutting in March, but for now, we are sticking with our view that Banxico will hold rates steady at its next meeting and keep rates on hold for all of 2026. Minutes may offer some insight, but either way, we expect Banxico to communicate again with markets ahead of the March meeting.

Weekly Economic & Financial Commentary: Strong Payrolls Dampen Hopes for Near-Term Rate Cuts

Summary

U.S. Week in Review:

- Stronger labor market data and cooler inflation reduce the odds of near-term Fed easing. Job growth surprised to the upside (+130K), unemployment fell (4.3%) and recent hiring looks more stable than in outright deterioration—strengthening the Fed's case to stay on hold. At the same time, CPI cooled more than expected with the annual rate on core inflation touching its lowest in nearly five years (2.5%), reinforcing the disinflation trend and keeping the door open to cuts later in the year. The latest data suggest a March rate cut looks increasingly unlikely, but the prospects for additional rate cuts remains alive for later in the year.

U.S. Week Ahead:

- December Trade Balance (Thursday)

- December Personal Income & Spending (Friday)

- Q4 GDP (Friday)

U.S. Week in Review

Strong Payrolls Dampen Hopes for Near-Term Rate Cuts

The upshot of a mini-government shutdown last week was the somewhat unusual alignment of indicators that brought fresh data on both jobs and inflation inside a span of 48 hours. This pivotal double header showed improvement on both of the Fed's mandates. The job market improved, even if hiring remains quite concentrated in the healthcare and social services sector, and inflation cooled more than expected. Hawks on the FOMC can now point to a labor market that is regaining its footing, but doves can cite the improvement in bringing inflation closer to target as a rationale for adjusting rates down another notch closer to neutral.

For months now, we've been saying that the window for additional Fed cuts is closing. Taken together, this week's data has likely pushed the next rate cut out until June, with the prospects for any further rate cuts in this cycle remaining dependent on how the data evolve over the next few months. If the breadth of robust hiring extended beyond just a few sectors, we'd say the window for additional cuts is closed. For now though, the tepid pace of hiring ex-healthcare does not warrant such conviction.

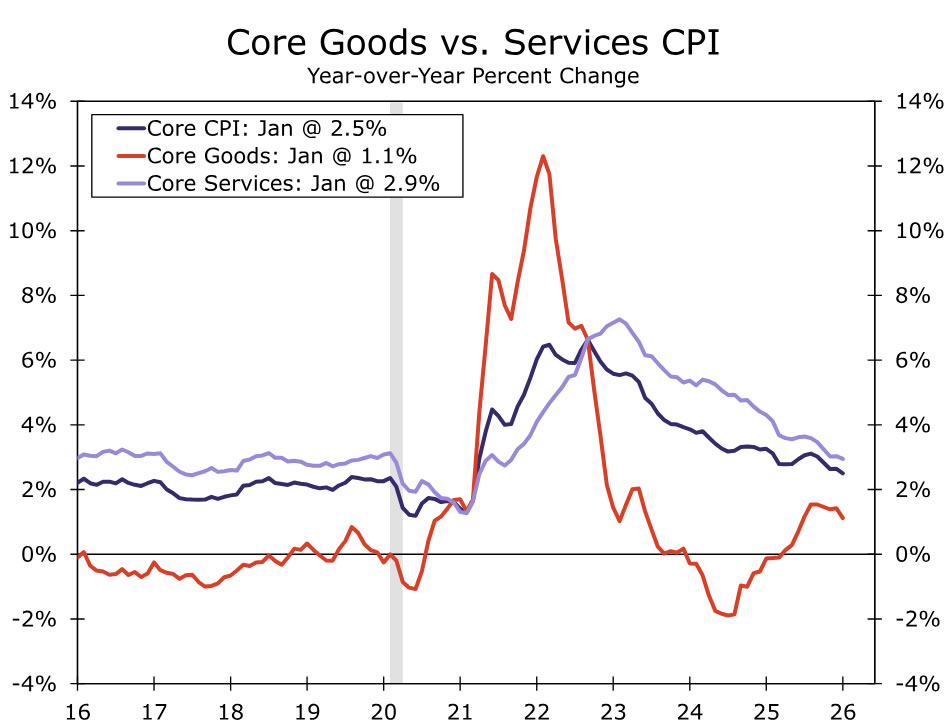

January payrolls handily exceeded modest expectations with a +130K gain in net hiring. This lifted the three‑month average to 73K (chart) and pushed the unemployment rate back down to 4.3%—where it was in August 2025 before the FOMC cut rates at its three subsequent meetings. While revisions were deeply negative, they were largely anticipated and did little to change the forward signal: job growth appears to be stabilizing rather than rolling over. Inflation data were more constructive. Headline and core CPI both cooled in January, and core inflation is now running at its lowest annual level since early 2021 (chart). While core PCE inflation is likely to come in stronger for January (~0.37% m/m) due to different weightings, source data and seasonal adjustment factors, the disinflation narrative remains intact. That said, the combination of firm labor data and still-above-target inflation makes a March rate cut look highly unlikely, even as it preserves optionality for cuts later in 2026.

The Employment Situation report may hoard the limelight especially with a big upside surprise, but other measures of the jobs market have not been quite so rosy. Wage pressures continue to fade. The Employment Cost Index undershot expectations in the fourth quarter, with compensation growth slowing to a 3.4% year-over-year rate—the weakest pace since 2021. Cooling wages and benefits (outside of healthcare) alongside solid productivity gains ease concerns about a labor-cost-driven inflation resurgence. But it's these signs of a gradually moderating labor backdrop that keeps downside growth risks on the Fed’s radar. The latest consumer data point to some weakness with retail sales stalling in December. But, aggregate holiday spending rose 3.6% in November and December compared to a year-earlier, broadly in line with our earlier expectations. The year-end weakness appears narrow and goods-led rather than a broad retrenchment, leaving the outlook for consumer demand largely intact heading into 2026.

U.S. Week Ahead

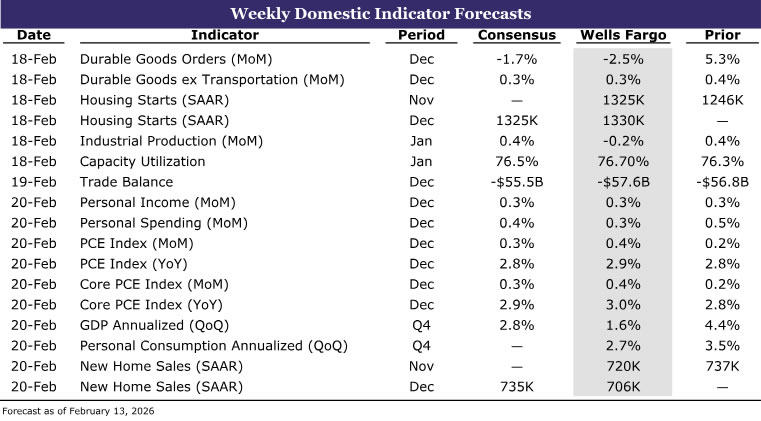

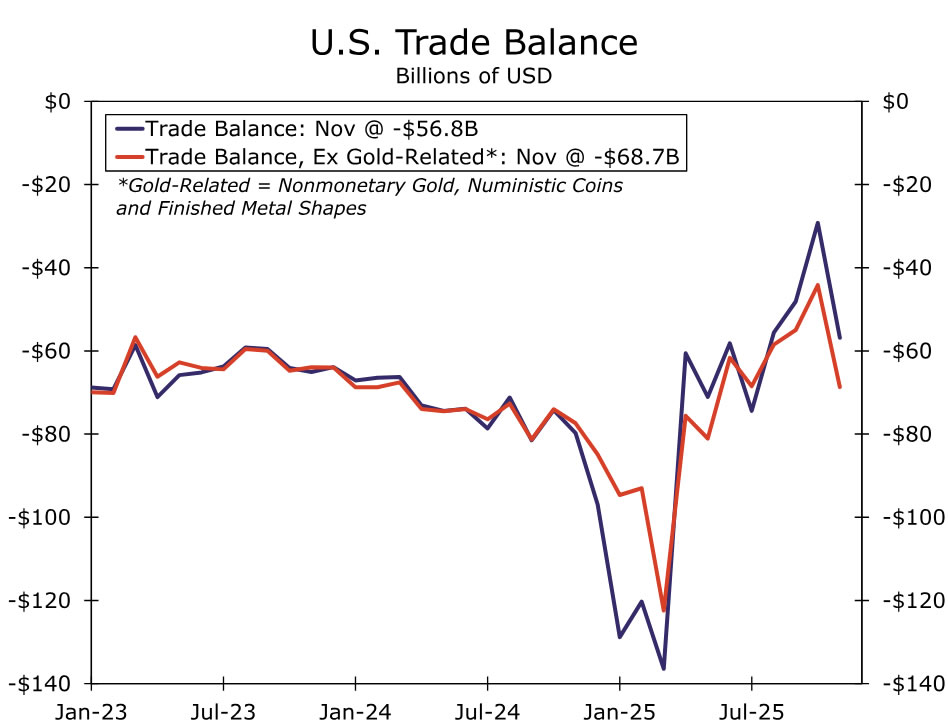

U.S. Trade Balance • Thursday

Recent trade data have been noisy, but the signal remains intact. After narrowing sharply in October, the trade deficit widened again in November, driven largely by volatility in a handful of categories—most notably gold, pharmaceuticals, and high‑tech imports. These swings reflect category‑specific distortions, not a broad deterioration in trade fundamentals. Stripping out gold and high‑tech effects, underlying import demand was soft in 2025, weighed down by tariff uncertainty and slower capital spending outside the technology sector.

Looking ahead, we expect the trade deficit to widen further to -$57.6 billion in December, as these specific factors continue to influence the year‑end data. However, the outlook for early 2026 is more constructive. Firm consumer demand, a recovery in more traditional areas of capital spending, and inventory normalization—absent evidence of a structural shift toward onshoring—should support a rebound in import growth as we move into the new year.

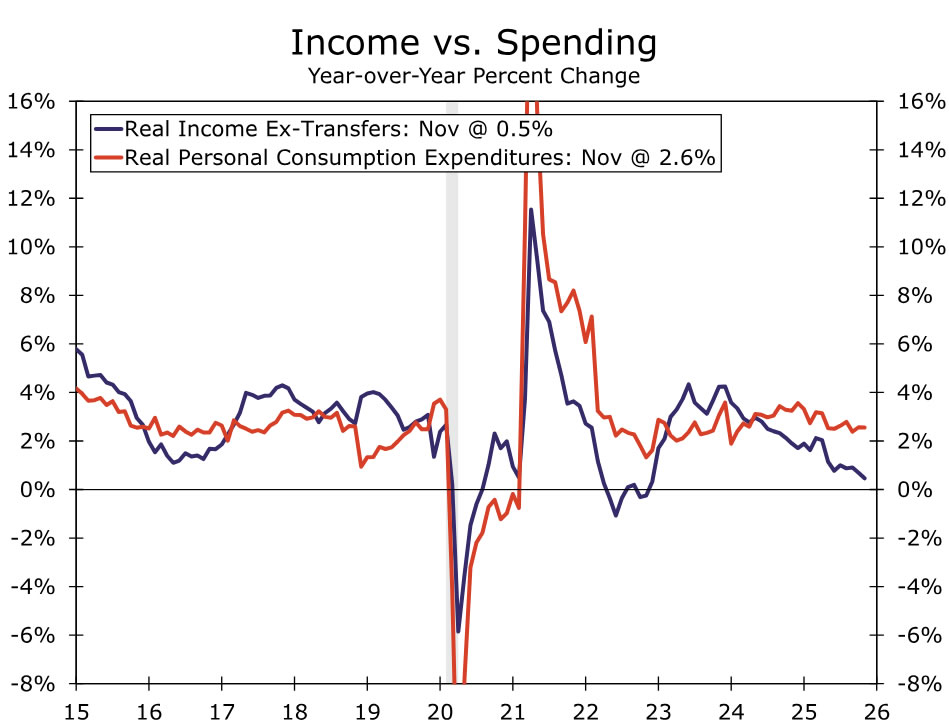

Personal Income & Spending • Friday

U.S. consumers remain on solid footing heading into 2026. Household spending continues to run at a healthy pace, and we look for nominal personal spending to rise 0.3% in December, leaving real spending roughly flat. While December retail sales were softer than expected and should weigh modestly on year‑end spending, the weakness appears driven by timing and pull‑forward effects rather than a deterioration in underlying demand. As a result, the softer retail print does not meaningfully change our constructive view of the consumer entering the new year.

Income growth remains the key watch point. Soft income gains have required households to lower saving rates, and we expect personal income to rise only 0.3% in December. Even so, the near‑term outlook for consumption remains supportive. Tax relief, easing inflation, and steadier job growth should help offset income headwinds and keep real consumer spending growing at a moderate pace through 2026.

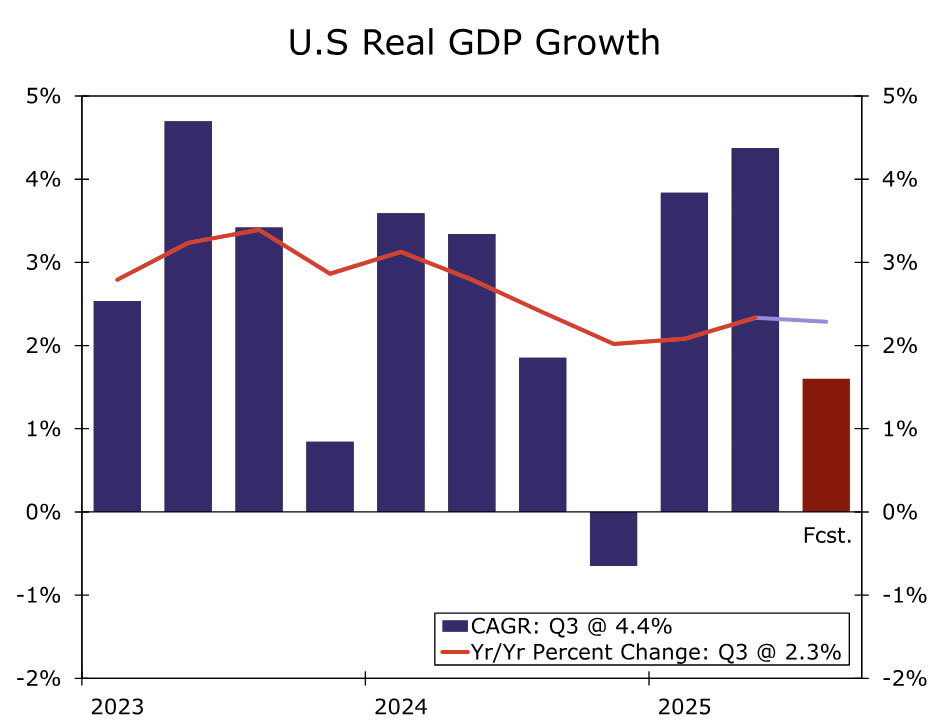

Q4 GDP • Friday

U.S. growth likely slowed at year‑end, but underlying fundamentals remain solid. We estimate real GDP grew at a 1.6% annualized pace in Q4, with most of the weakness attributable to the extended government shutdown from early October through mid‑November, which likely shaved roughly 1.2 percentage points from headline growth.

Stripping out shutdown effects, activity held up well. We expect real PCE to grow at a 2.7% annualized rate, while business investment likely posted a modest gain led by high‑tech equipment and intellectual property. Net exports and inventories remain the key sources of volatility. Beyond tariff uncertainty, a surge in investment‑related gold flows continues to cloud the signal from monthly trade data, while inventories remain inherently difficult to forecast given limited real‑time information. Through this noise, the economy appears to have ended 2025 in a healthy position, growing at a 2.2% average pace over the year.