Sample Category Title

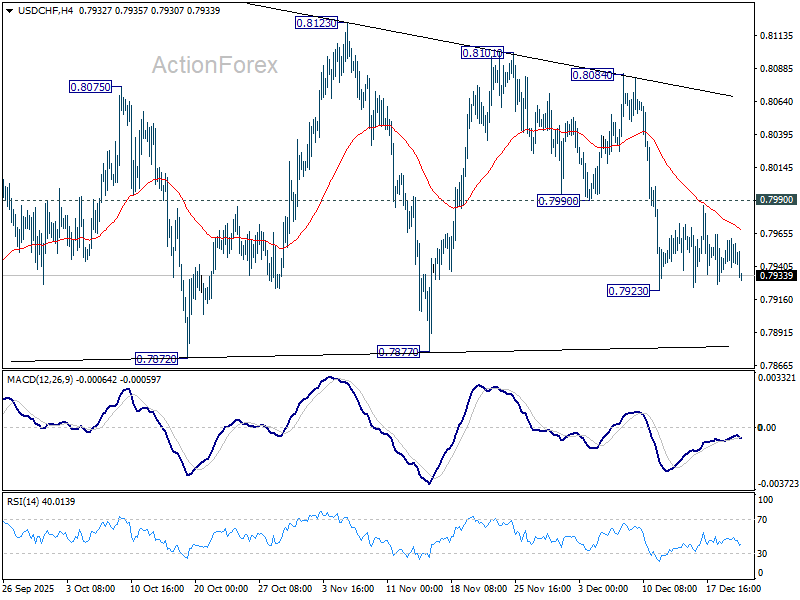

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7945; (P) 0.7953; (R1) 0.7968; More….

Intraday bias in USD/CHF stays neutral as sideway trading continues above 0.7923 temporary low. Outlook is unchanged that corrective pattern from 0.7828 could extend further. On the downside, below 0.7923 will target 0.7877 support. On the upside, though, break of 0.7990 support turned resistance will bring stronger rebound towards 0.8084.

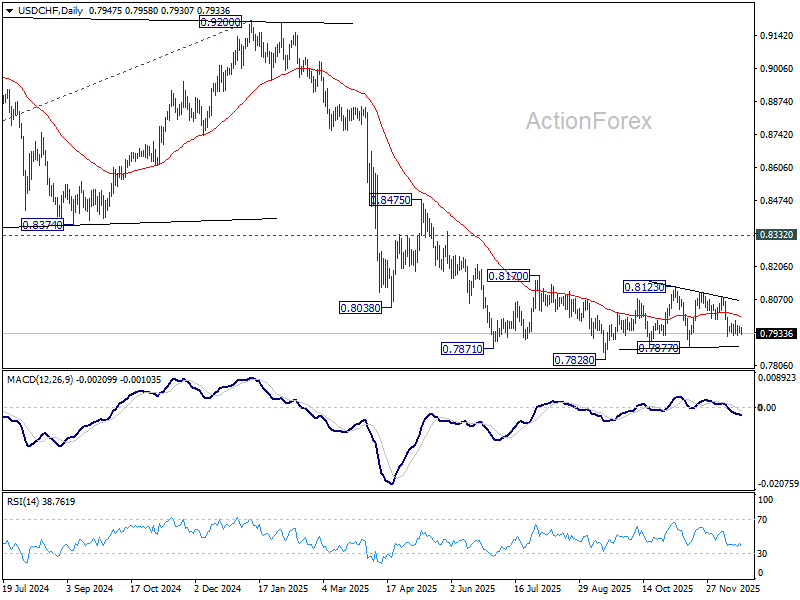

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

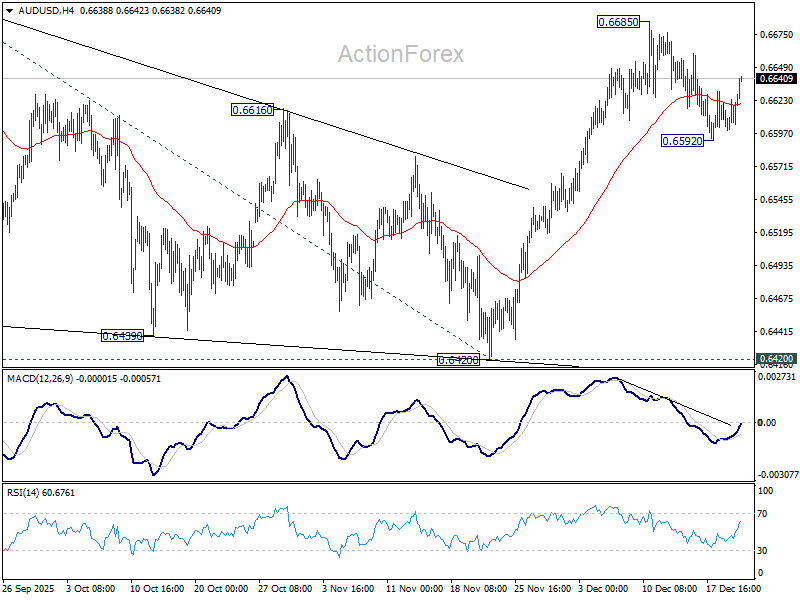

AUD/USD Daily Report

Daily Pivots: (S1) 0.6599; (P) 0.6612; (R1) 0.6624; More...

Intraday bias in AUD/USD stays neutral and more consolidations could be seen below 0.6685. But further rally is still in favor for now. On the upside, decisive break of 0.6706 will resume the whole rise from 0.5913 and target 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. However, sustained break of 55 D EMA (now at 0.6566) will extend the corrective pattern from 0.6706 with another falling leg back to 0.6420 support.

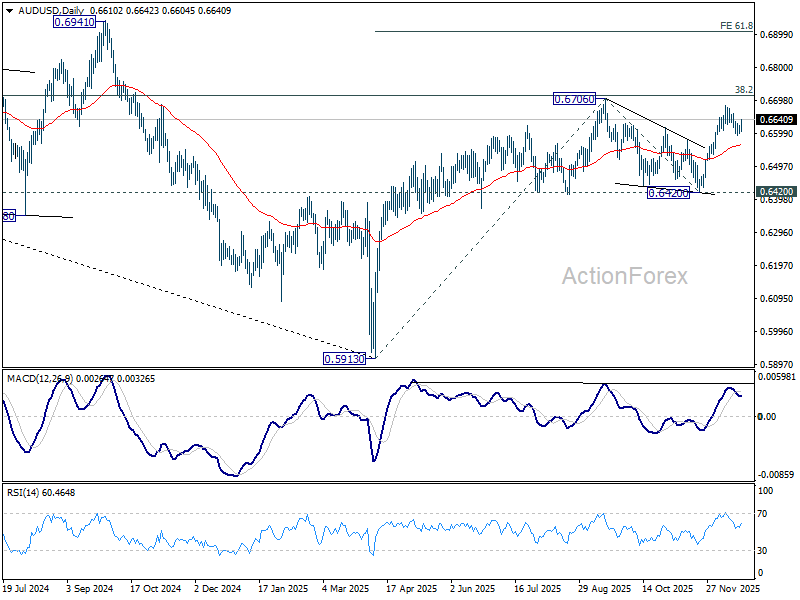

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 0.8006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

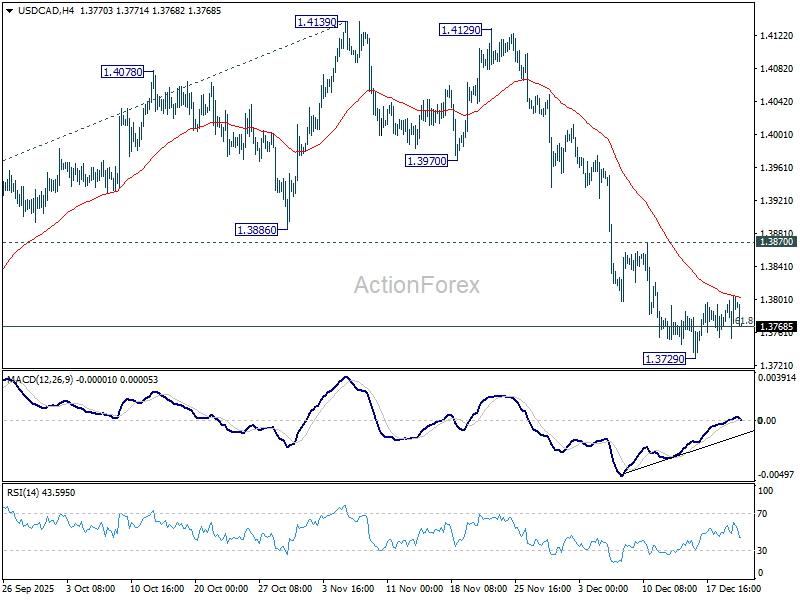

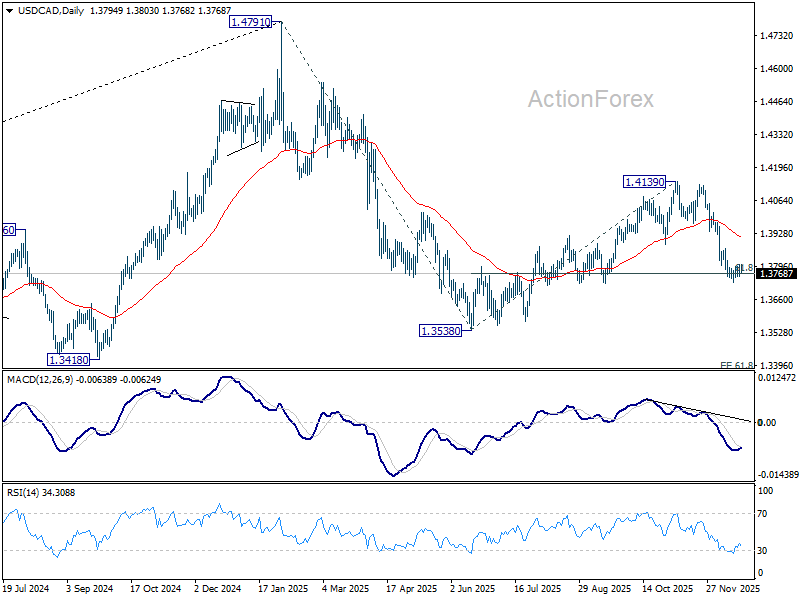

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3769; (P) 1.3788; (R1) 1.3820; More...

Intraday bias in USD/CAD remains neutral for consolidations, but further fall is expected with 1.3870 resistance intact. On the downside, sustained trading below 61.8% retracement of 1.3538 to 1.4139 at 1.3768 will argue that whole decline form 1.4791 might be ready to resume, and bring retest of 1.3538 low next. However, break of 1.3870 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

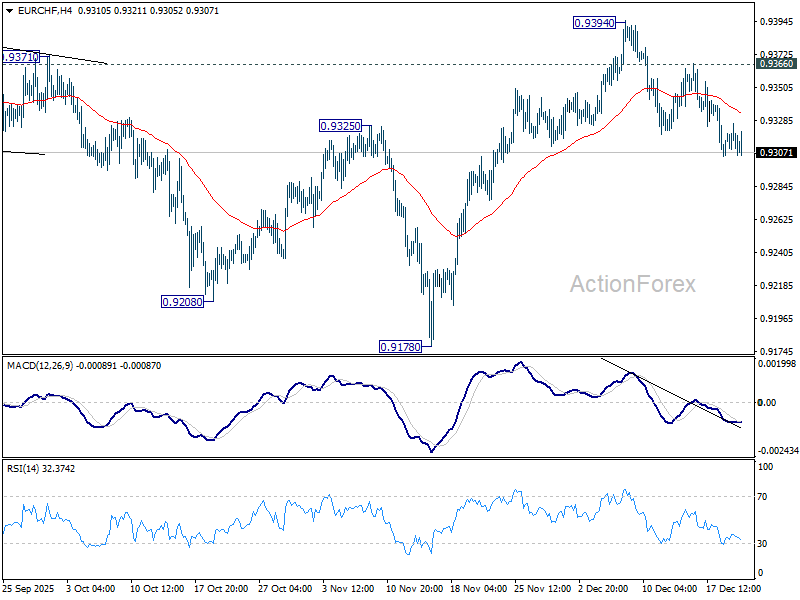

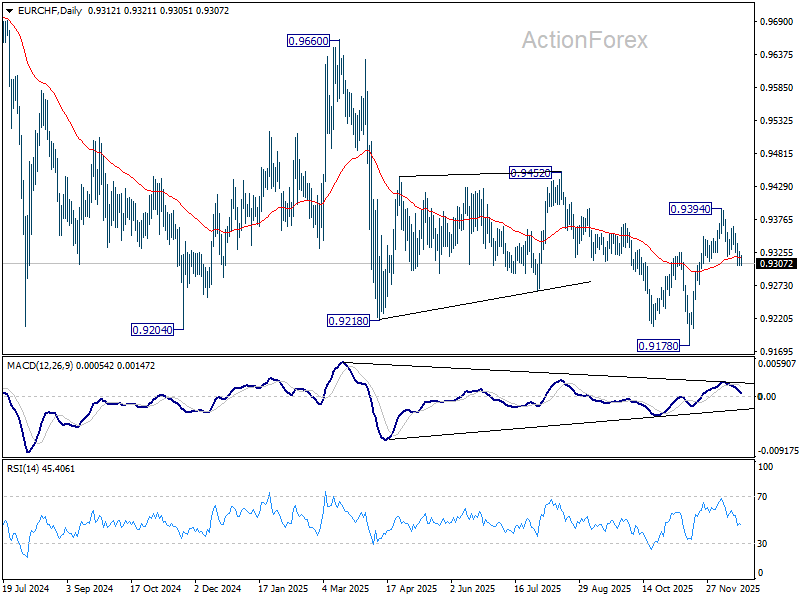

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9308; (P) 0.9318; (R1) 0.9326; More....

Intraday bias in EUR/CHF remains mildly on the downside for the moment. Sustained trading below 55 D EMA (now at 0.9317) will argue that rebound from 0.9178 has already completed. Deeper fall should then be seen back to retest this low. On the upside, however, break of 0.9366 resistance will resume the rebound through 0.9394 to 0.9452 structural resistance.

In the bigger picture, EUR/CHF has breached long term falling channel resistance as the rebound from 0.9278 extends. Considering bullish convergence condition in W MACD, sustained trading above 55 W EMA (now at 0.9369) will indicate medium term bottoming at 0.9178, and suggests that it's already in larger scale rebound. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9928 resistance next. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9178 at a later stage.

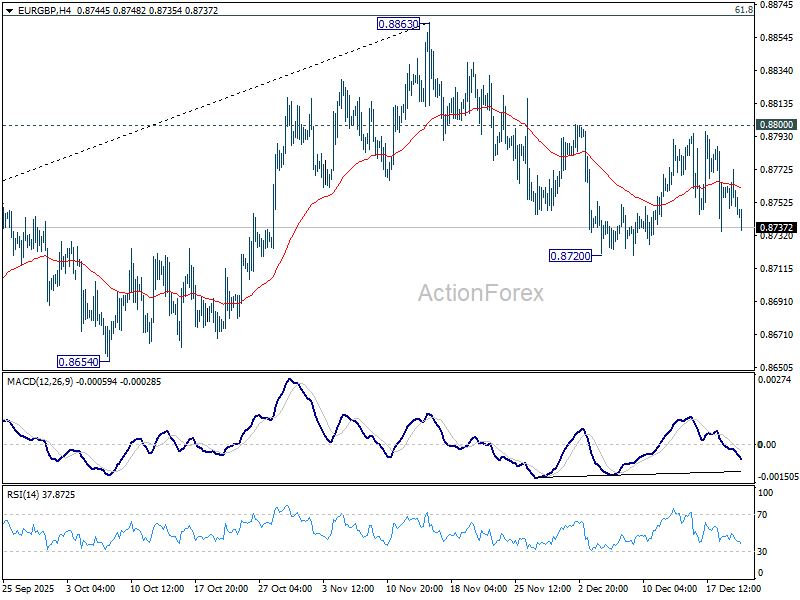

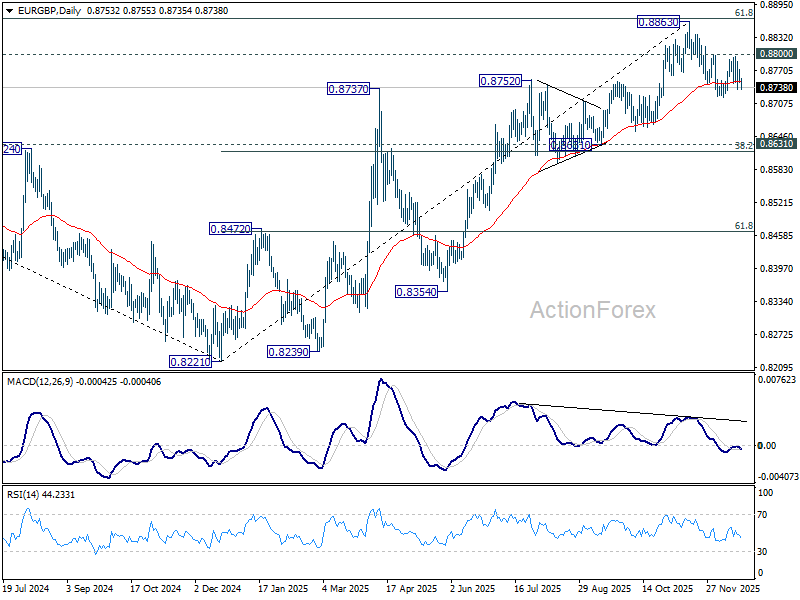

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8744; (P) 0.8759; (R1) 0.8768; More…

Intraday bias in EUR/GBP stay neutral and further decline is mildly in favor with 0.8800 resistance intact. On the downside, break of 0.8720 will bring deeper fall to 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, on the upside, break of 0.8800 will argue that the fall has completed as a correction, and turn bias back to the upside for retesting 0.8863.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8610) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

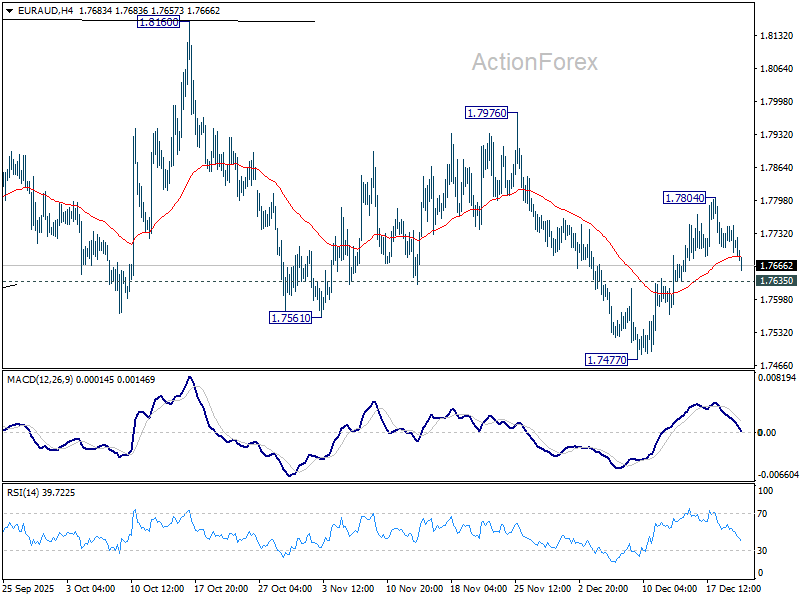

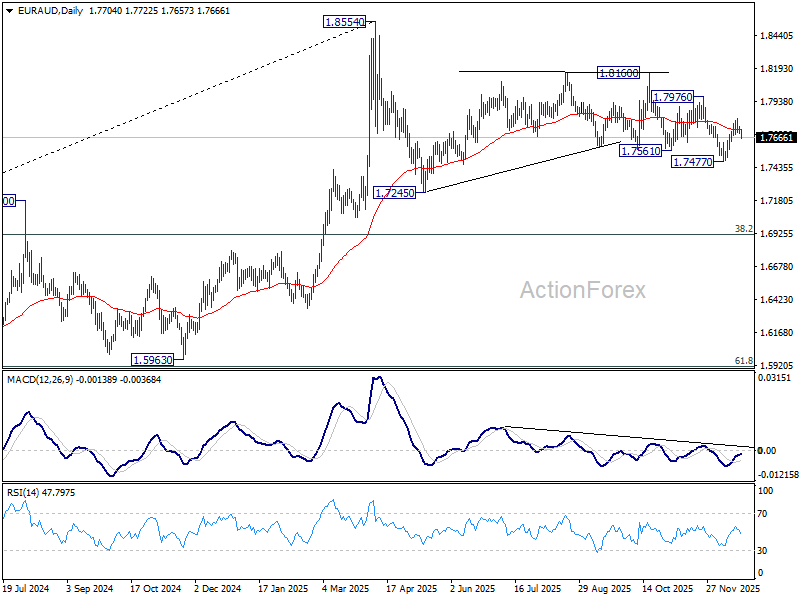

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7690; (P) 1.7719; (R1) 1.7743; More...

Intraday bias in EUR/AUD remains neutral for the moment. Fall from 1.8160 could have completed at 1.7477. On the upside, above 1.7804 will solidify this case and target 1.7976 resistance next. However, break of 1.7635 minor support will bring retest of 1.7477 low instead. Overall, corrective pattern from 1.8554 could extend further.

In the bigger picture, as long as 55 W EMA (now at 1.7468) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

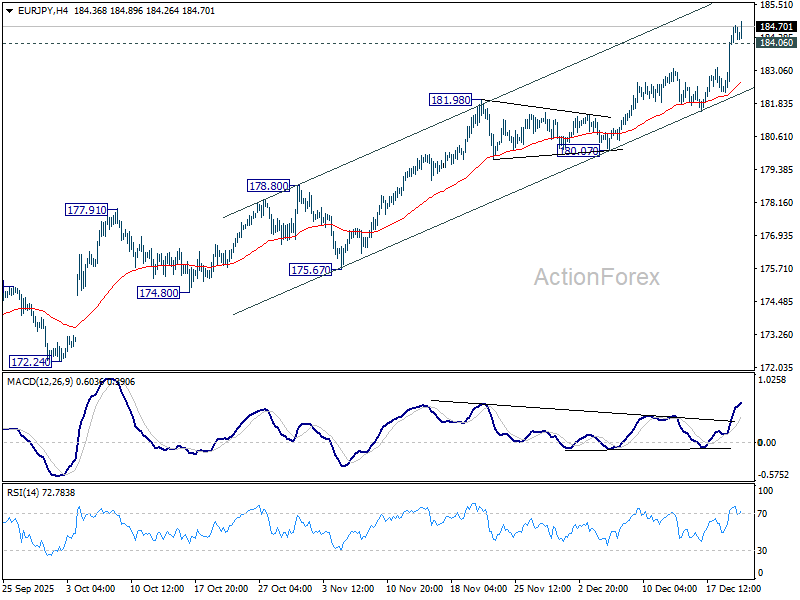

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.01; (P) 183.88; (R1) 185.56; More...

EUR/JPY's rally is in progress and intraday bias stays on the upside for 186.31 long term projection level next. On the downside, below 184.06 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 181.98 resistance turned support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 170.83) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 100% projection at 205.81 next.

EUR/USD: ECB Policy Stance Fails to Surprise Markets

At its meeting on 18 December, the European Central Bank (ECB) left all key interest rates unchanged, maintaining the deposit facility rate at 2.0%. The decision was widely anticipated, offering no fresh catalyst for meaningful euro movement. While headline inflation for the eurozone remained close to target at 2.15% in November, the ECB's updated projections saw a slight upward revision for the coming years, primarily driven by persistent price growth in the services sector.

Concurrently, the ECB improved its GDP growth forecast for 2025–2027. However, with the decision fully priced in, it provided neither additional support nor pressure to the single currency.

The primary driver for EUR/USD now stems from US monetary policy. The recent Federal Reserve rate cut from 4.00% to 3.75% has narrowed the yield differential between the dollar and the euro. This reduces the dollar's interest rate advantage and makes euro-denominated assets relatively more attractive, providing a moderate tailwind for the euro.

Looking ahead, medium-term dynamics will hinge on relative expectations for central bank policy. Should markets continue to price in a more aggressive easing cycle from the Fed compared to the ECB, the euro is likely to find further support. Conversely, any signs that the ECB is preparing to proactively ease policy in response to eurozone economic weakness would limit the euro's upside potential.

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, the pair is consolidating near the breakdown level of the previous growth channel's lower boundary. We anticipate a downside breakout from this range and a resumption of the third decline wave, with an initial target at 1.1650.

The MACD indicator technically confirms this bearish outlook. Its signal line is below zero and pointing decisively downward, reflecting sustained bearish momentum and potential for further downside.

H1 Chart:

On the H1 chart, the market completed another decline wave to 1.1702, followed by a correction to 1.1737. A new downward impulse towards 1.1650 is currently forming. A sustained break below this level would signal the potential for an extended third wave, targeting the 1.1645 area as a local objective.

This scenario is supported by the Stochastic oscillator, with its signal line below the 50 level and trending firmly downwards.

Conclusion

The euro's trajectory remains more sensitive to shifting US policy expectations than to the ECB's predictable stance. While the narrowed interest rate differential offers near-term support, the technical structure appears bearish. A decisive break below the current consolidation range could trigger a renewed move towards the 1.1650–1.1645 support zone.

Gold Price Breaks Above $4,400 for the First Time

As the XAU/USD chart shows, gold has climbed above $4,400 today, setting a new all-time high.

On Friday, when analysing the gold chart, we highlighted a triangle formation and noted strong selling pressure near the previous record high around $4,380, set in October.

However, over the weekend geopolitical tensions intensified following reports that the United States detained an oil tanker linked to Venezuela. At the turn of the week, this resulted in a clear triangle breakout (as indicated by the arrow):

→ during the second half of Friday’s session, gold moved above the upper boundary of the pattern;

→ at the Asian open, the price turned higher after retesting that level, with former resistance acting as support.

As a result, concerns about a potential armed conflict involving the US have shifted the balance of supply and demand decisively higher.

The bullish momentum has justified the construction of an ascending channel. It is worth noting that the RSI indicator is currently in overbought territory. Intraday trading during the US session could therefore bring some corrective pullback, with potential support coming from:

→ the lower boundary of the newly formed channel;

→ the area between the previous peak at $4,380 and the psychological $4,000 level.

According to Goldman Sachs analysts, structural demand from central banks combined with falling interest rates could drive gold prices towards $4,900 by the end of 2026.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Breaks to Record High as WTI Crude Seeks Rebound

Gold price started a fresh surge above $4,350 and traded to a new all-time high. Crude oil is recovering and might rise toward the $58.50 resistance zone.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price rallied to a new all-time high and traded above $4,395 against the US Dollar.

- A key bullish trend line is forming with support at $4,334 on the hourly chart of gold at FXOpen.

- WTI Crude oil is recovering losses and trading above $56.20.

- There was a break above a major bearish trend line with resistance at $56.00 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price formed support near $4,240. The price remained in a bullish zone and started a fresh increase above $4,300, as mentioned in the previous analysis.

The bulls pushed the price above $4,360 level and the 50-hour simple moving average. Finally, it traded to a new all-time high at $4,397. The price is still showing bullish signs above $4,380, and the RSI is above 70.

Initial support on the downside is near the 23.6% Fib retracement level of the upward move from the $4,271 swing low to the $4,397 high at $4,365. The next area of interest might be near a key bullish trend line at $4,335 and the 50% Fib retracement.

A downside break below the trend line might send the price to $4,300. If the bulls fail to protect $4,300, the price could start a larger downside correction. In the stated case, Gold could drop toward $4,240.

The next area for the bulls might be $4,220. A daily close below $4,220 could spark bearish moves and send the price to $4,150.

If there is a fresh increase, the price could face resistance at $4,400. The next sell zone might be $4,420. An upside break above the $4,420 resistance could send Gold price toward $4,465. Any more gains may perhaps set the pace for an increase to $4,500.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price found support near $54.85 against the US Dollar. The price formed a base and started a recovery wave above $55.50 and the 50-hour simple moving average.

The bulls were able to push the price above the 23.6% Fib retracement level of the downward move from the $58.80 swing high to the $54.84 swing low. Besides, there was a break above a major bearish trend line with resistance at $56.00.

The hourly RSI is above the 60 level, and the price is attempting to close above the 50% Fib retracement. The next hurdle could be $57.85. A clear move above $57.85 could send the price toward $58.50. Any more gains might open the doors for a test of $58.80.

Conversely, the price might start a fresh decline from $57.30 or $57.85. Immediate support sits near $56.45 or the 50-hour simple moving average. The key breakdown zone on the WTI crude oil chart might be $55.55.

If there is a downside break, the price might decline toward $54.85. Any more losses might encourage the bears for a push toward $54.00.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.