Sample Category Title

Canadian GDP Softens in October But Early Data Points to a November Recover

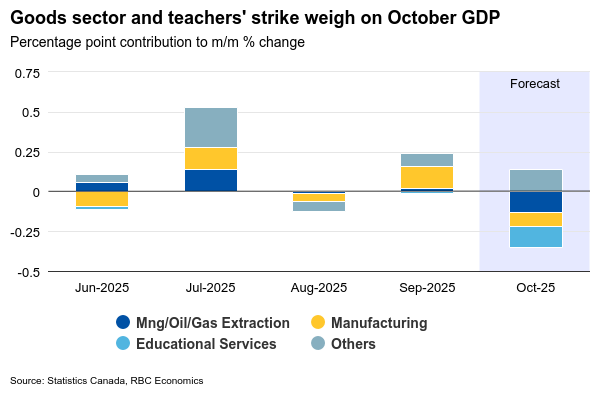

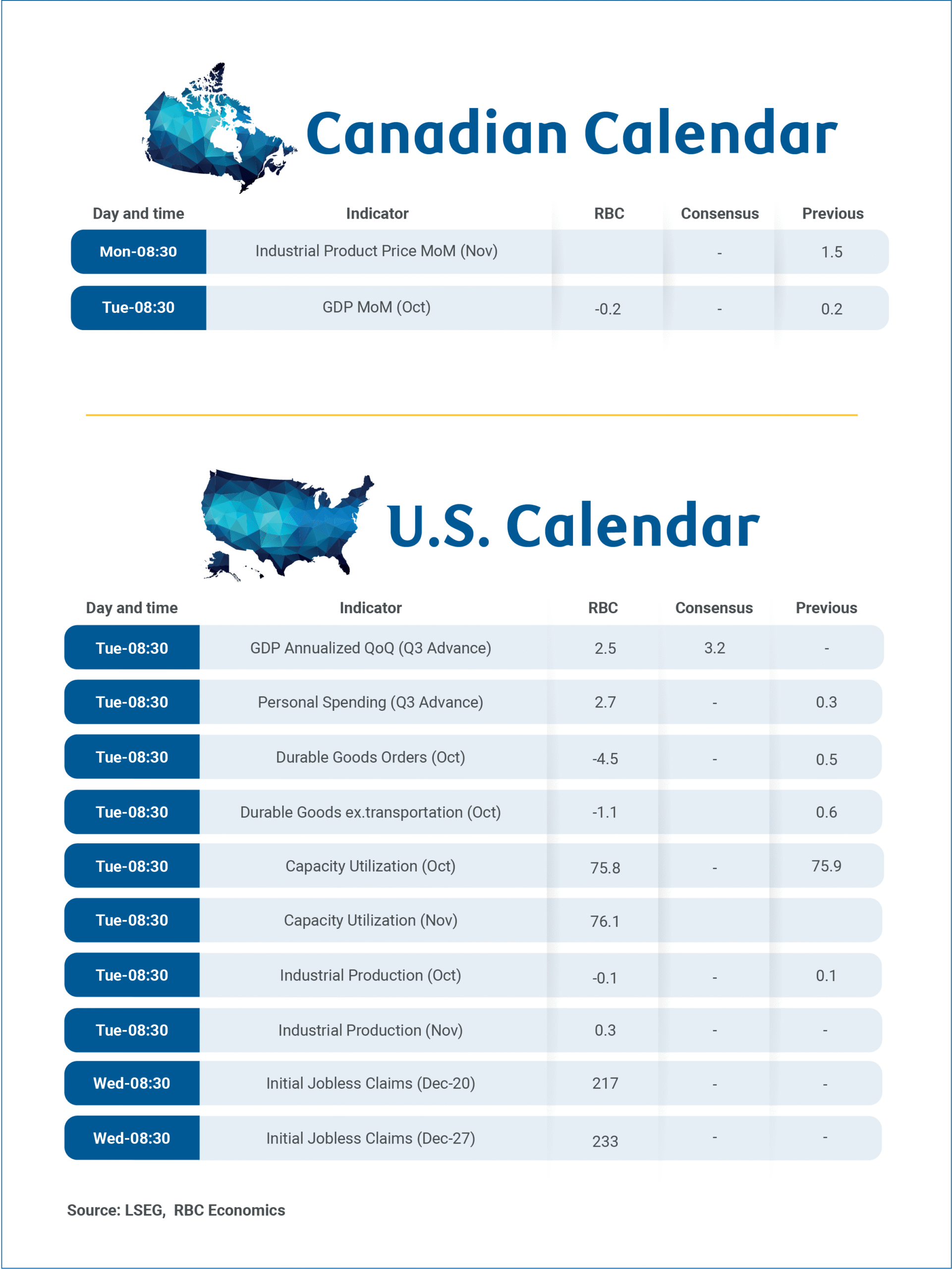

Canada’s gross domestic product report for October on Tuesday will mark Statistics Canada’s final major data release of 2025, and we anticipate a 0.2% decline in growth.

It’s slightly higher than StatsCan’s preliminary estimate released a month earlier for a 0.3% contraction. If October’s decline is realized, it would represent the steepest monthly drop in GDP since February.

Still, early indicators such as hours worked and our tracking of consumer spending suggest a possible recovery in November. We continue to expect a soft 0.5% annualized increase in GDP for Q4.

In October, we see weakness mostly from goods-producing sectors, while output among service industries remained essentially unchanged.

Non-conventional oil production in Alberta contracted sharply (-5%) in October after four consecutive months of expansion. Manufacturing output declined as well, partially reversing September’s gains. StatsCan’s October mineral production data indicated modest recovery in mining output, following declines in the prior two months, helping to cushion some weaknesses in other sectors.

For services, home resales rose 0.8% month-over-month in October, bolstering real estate activity. Arts and entertainment saw a boost from the Blue Jays’ playoff run, although the gain was likely reversed quickly in November. Offsetting stronger activities was the Alberta’s teacher strike temporarily weighing on education services. Wholesale and retail volumes also fell, by 0.7% and 0.6% respectively.

Early November indicators suggest signs of stabilization. Hours worked increased a larger 0.4%, and our tracking of RBC consumer spending data indicates continued strength, especially in discretionary purchases as the holiday shopping season ramps up. This is consistent with StatsCan’s advance retail indicator, which shows sales rebounded by 1.2% in November. Overall, we continue to expect modest growth in Q4.

Week ahead data watch:

Delayed Q3 U.S. GDP report will be released on Tuesday after the U.S. government shutdown. We look for headline GDP growth of an annualized 2.5% quarter-over-quarter—a deceleration from Q2’s 3.8%. Much of Q3’s expansion was driven by household consumption, particularly within services. Excluding volatile net trade, final domestic demand likely remained resilient, albeit growing slightly slower than in Q2.

Weekly Focus: ECB More Optimistic on Growth Outlook

The last week before Christmas is usually a big central bank week and this year was no exception with central bank meetings in the euro zone, UK, Japan, Norway and Sweden (plus a few others). Most interesting was the ECB meeting. While they kept rates unchanged as expected, the ECB revised up projections for both GDP growth as well as inflation. ECB president Lagarde signalled a neutral outlook for rates at the press conference, though, and bond yields ended broadly unchanged after a short initial spike. The Bank of England delivered a rate cut of 25bp as expected, while Bank of Japan went the other way and raised rates 25bp. They also come from different starting points with rates in Japan now at 0.75% while the cut in UK moved rates to 3.75%. Both Norges Bank and the Riksbank left rates unchanged as expected.

On the data front, Euro zone indicators softened in November with a small decline in the composite PMI from 52.8 to 51.9 (consensus 52.6) and a similar move lower in the German ifo business confidence. The pace of growth thus seemed to moderate a bit towards the end of 2025, but the indicators still underpin continued cruising speed growth in line with our expectations for 2026.

In the US, the most noteworthy data was inflation for November, which showed a big drop to 2.6% y/y from 3.0% y/y in September (inflation for October was not recorded due to the US government shutdown). The data may have been distorted by the shutdown, though. US also released the employment report, which was a mixed bag. The employment picture looked better with job gains around 75k over the past three months outside the government sector, while the unemployment rate increased to the highest level in four years at 4.6%. The increase was due to a lift in the labour force, though. With US GDP growth being robust above 3% in the second half of 2025, we expect the labour market to improve moderately going into 2026. US retail sales showed continued brisk consumer spending with a rise of 0.8% m/m in core sales in November. The data support continued moderate easing by the Fed, and we still look for rate cuts in March and June. It is broadly in line with market pricing, although the market sees the cuts stretched out over a longer period to September.

In the German bond market, upward pressure continued on 30-year bond yields related to changing regulation for Dutch pension funds and record German issuance outlook, while we saw a moderate decline in the short end. US yields traded slightly lower during the week. Equities were on the backfoot the whole week as AI bubble concerns lingered. We continue to see the macro environment as benign for equities in coming quarters with US growth being solid and the euro zone cruising ahead but occasional wobbles related to AI concerns will likely continue given the stretched valuations.

The next interesting data will come on the other side of Christmas with Japanese inflation on 26 December, Chinese PMI on 31 December, Euro Flash CPI on 7 January and the US employment report on 9 January.

Sunset Market Commentary

Markets

Bear steepening is again name of the game today. Two events triggered the selling pressure in core bonds with the long end of the curves underperforming. First there’s the continuation of the Bank of Japan’s policy normalization. The US trade war interfered with the central bank’s semi-annual rate hikes, but with uncertainty reduced and underlying inflation still running above the 2% target, the BoJ picked up where it left things in January. At 0.75%, the policy rate reached its highest level since 1995 with governor Ueda readying more moves in 2026 (“some distance from lower end of neutral range”). The next step higher is discounted by the July policy meeting. Higher Japanese (bond) yields have global implications. By closing the gap with interest rate levels in other parts of the world, there’s an increasing risk of a JPY carry trade unwind with money flowing back into Japan(ese) assets. The Japanese yen is exception to the rule today with USD/JPY surging from 155.70 to 157.30. The Japanese 10-yr yield breached 2% to trade at its highest level since 1999, making JGB’s starting to look attractive after all those years. The Japanese 30-yr yield (3.42%) sits only 10 bps below the German one. Together with the post-Covid monetary framework, there’s the return of risk premia embedded in the long end of the curve as central bank’s unwind their QE-portfolios. Fiscal policy as the new dominant market force is one of our hallmarks together with the notion that Europe will become more reliant on joint debt issuance as a means to prevent a repeat of the 2010-2011 crisis. What started with temporary unemployment support (SURE) and recovery programs during COVID, evolved via upped defense spending to keep the NATO alliance alive and now returns via the €90bn financial loan to Ukraine (which will be borrowed against the bloc’s shared budget). Daily changes on the German yield curve range between + 1 bp (2-yr) and +5 bps (30-yr). The 30-yr yield trades above 3.5% for the first time since 2011. The swap curve moves in parallel fashion with the 10y swap rate testing the 2024 top at 2.95% and the 30y testing the 2023 top at 3.27%. Despite everything what’s going on at bond markets, EUR/USD is unfazed at 1.1720. Changes on stock markets are also minimal.

News & Views

The German Bundesbank today gave a balanced update on its forecasts for the domestic economy. Expected growth for 2026 was slightly downwardly revised to 0.6% (from 0.7% in June). There are signs of an increase in government orders, but it only expects the expansionary spending stance to bolster economic growth more significantly from later on next year. Aside from government spending, the BuBa also expects a resurgence in exports. It sees growth (wda) at 1.3% in 2027 and 1.1% in 2028. The expansionary fiscal policy will only have a limited impact on potential output of the economy (0.4% until 2028) as broader structural reforms are needed. Inflation will decline a little more slowly in the coming years mainly due to expected high wage growth. The Buba sees HICP inflation easing from 2.3% this year to 2.2% next year to reach around 2% in 2027 & 28. Additional spending on defense and infrastructure, tax cuts and larger transfers will be reflected in higher government debt in the coming years. The government deficit ratio will reach 4.8% in 2028, while the debt ratio will have risen to 68%.

Belgian business confidence showed a sharp drop this month (from -8.2 to -11.9). It weakened across all sectors except business-related services. The decline in the trade sector accelerated (-11.8 from -8.9) as business leaders expect demand to drop further and intend to significantly scale back their orders with suppliers. Manufacturing showed a more pessimistic assessment of total order books, employment and demand conditions. Weaker building confidence is due to reduced equipment use and a drop in the order position. Belgian consumer confidence, published yesterday, receded from 2 to -1 after rising since May. There was a particularly sharp downturn in households’ savings intentions (20 from 26). More modest declines were registered for the economic situation in Belgium (-28 from -26), the financial situation of households (-3 from 0) and unemployment.

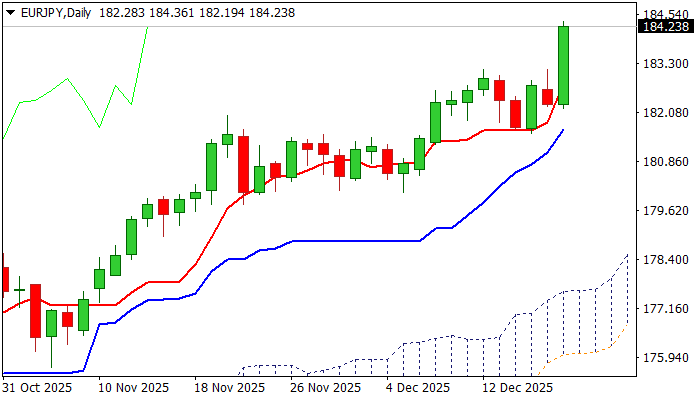

EURJPY Hits New All-Time High

EURJPY hit new record high following 1.1% advance in post BoJ rate decision trading.

Japanese yen weakened across the board after the Bank of Japan raised interest rates by 25 basis points to 0.75% (the highest in three decades) and left the door opened for further tightening.

The pair is in steep ascend in past 10 months, which is the part of larger uptrend since mid-2020, with today’s move, marking the biggest daily gain since Apr 7.

Fresh move into uncharted territory eyes targets at 185.00 (round figure) and 185.93 (Fibo 150% projection of the rally from 154.40), though shallow correction should be anticipated as daily RSI is approaching overbought territory.

Dips should ideally find firm ground above 183.00 support zone, to mark positioning for fresh push higher.

Only break and close below 182.00 zone (today’s low / rising 10DMA) would sideline bulls.

Res: 185.00; 185.93; 187.00; 188.41

Sup: 184.00; 183.15; 182.20; 181.70

Natural Gas Prices Fell in Late December

On 4 December, while analysing the XNG/USD chart, we highlighted the rally in natural gas prices towards a three-year high and noted that the price had entered a resistance zone formed by:

→ the upper boundary of a broad descending channel (shown in red);

→ the $4.800/MMBtu level, near which a peak was formed in March;

→ the psychological $5.000/MMBtu mark.

As indicated by the arrow:

→ this resistance cluster proved effective, and after an attempt to break above the $5.000 psychological level, the uptrend reached its climax;

→ following the appearance of a bearish gap on 8 December, selling pressure took control, leading to a break below the orange ascending trend line and a decline in US natural gas prices.

From a fundamental perspective, the pullback has been driven by several factors:

→ Seasonality. Weather forecasts for the US holiday period point to above-average temperatures, reducing demand for heating and power generation.

→ Rising production. According to Trading Economics, natural gas output in the continental United States reached 109.7 billion cubic feet per day in December, maintaining the record levels seen in November. In addition, EIA data show that gas inventories remain 0.9% above the current five-year average.

It is worth noting that today natural gas prices are trading:

→ near a support zone created by the bullish gap formed in the second half of October;

→ close to the median of the aforementioned descending channel, an area where supply and demand often come back into balance.

Taking this into account, it is reasonable to assume that:

→ after a sharp drop of around 30% from the early-December peak, sellers may look to lock in profits ahead of the holidays;

→ the market could enter a consolidation phase.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Crypto Market Updating Lows But Avoiding Sharp Changes

Market Picture

The crypto market set another trap for bulls yesterday afternoon, jumping to $3T and then falling to $2.85T. However, on Friday morning, it is once again flirting with buyers, trading at the same level of $2.95T, where it has remained since the beginning of the week.

On Thursday, Bitcoin replayed Wednesday’s micro-drama, soaring towards $90K, only to soon fall below its previous local lows. As a result, by the end of the day, the intraday low had fallen back to $84K, which we last saw almost five weeks ago. However, on Friday morning, the price is back at the $87K level, around which it has been trading for the last four days.

Although Bitcoin has buyers stopping really sharp declines, other top altcoins are gradually drifting down. It appears that large holders have been quietly exiting them over the last three to five months. This is clearly visible in Ethereum, XRP, and Solana. Zcash, in its traditional manner, soars sharply on signs of a reversal in larger coins, but then falls just as dramatically.

News background

The options market is hedging against the risk of Bitcoin falling below $85K, according to Derive.xyz. Market participants anticipate an increase in volatility at the end of the year. The situation is exacerbated by unstable inflows into ETFs and a decline in liquidity ahead of the holidays.

BTC’s growth is also being hindered by investor doubts about the return on investment in the American artificial intelligence (AI) sector, amid a liquidity shortage. Bitcoin’s correlation with the Nasdaq has strengthened due to the influx of large investors.

BitcoinForCorporations predicts an outflow of up to $15 billion from DAT companies accumulating cryptocurrency if MSCI decides to exclude them from its indices. Eighteen firms are at risk of exclusion.

In 2025, Bitcoin’s volatility was lower than that of Nvidia’s shares, according to Bitwise. The emergence of spot ETFs and other traditional instruments caused the ‘fundamental reduction in risk’ of the asset.

An increase in the number of users and an expansion of the gas limit has led to the ‘inflation’ of the Ethereum blockchain, which negatively affects the operation of nodes, warned the Ethereum Foundation (EF) team, proposing several possible solutions. Ethereum co-founder Vitalik Buterin called for Ethereum to be simplified. In his opinion, the complexity of using the ecosystem of the second-largest cryptocurrency by capitalisation hinders its mass adoption.

Canada: Retail Sales Fall Again in October, But November Flash Points to Rebound

Retail sales declined for a second consecutive month in October, slipping 0.2% month-on-month (m/m), undershooting Statistics Canada's advanced estimate for a flat reading. After adjusting for inflation, sales volumes fell a steeper 0.6% m/m.

Auto sales partially reversed September's losses, rising 0.6% m/m in October.

Receipts at gas stations and fuel vendors fell 0.8% m/m, driven by weaker demand, with volumes also down 0.9% m/m.

Core sales – excluding auto sales and receipts at gas stations – were weak for a second straight month, declining 0.5% m/m.

- Weakness was concentrated in food and beverage stores (-2.0% m/m) with more than a 10.6% drop at beer, wine and liquor retailers coinciding with a labour dispute in British Columbia. Sales at clothing and clothing accessories (-0.7% m/m) and health and personal care stores (-0.3% m/m) also fell in October.

- Gains at furniture, home furnishings stores (+2.3% m/m) partially offset the weakness.

E-commerce sales declined by 0.3% m/m in October.

Statistics Canada's advanced estimate points to a rebound with 1.2% gain in November.

Key Implications

The holiday shopping season got off to a flat start. Despite November's rebound, the underlying trend in real sales remains negative. Only a handful of discretionary categories – clothing and electronics – continue to show positive momentum. This lines up with our TD credit & debit card data, which show relatively resilient services spending growth outpacing goods

Looking ahead, our outlook for Q4 real consumption growth remains subdued, tracking close to 1.0% (quarter-on-quarter, annualized). This below-trend pace is consistent with the Bank of Canada’s assessment that the economy is still working to gain traction and that monetary policy is appropriately positioned.

Yen Selling Persists as BoJ Normalization Seen as Slow and Shallow

Yen selling remains the dominant theme heading into the weekend, with the currency staying as the weakest performer. The renewed slide comes despite the BOJ lifting interest rates to their highest level since 1999. The problem for Yen bulls is not the direction of policy, but the pace. BoJ normalization is widely expected to remain slow and cautious, with policymakers clearly unwilling to risk choking off fragile momentum in growth and wages.

Market consensus has now converged on the view that the next BoJ hike is unlikely to arrive until mid-2026. Even then, policy rates would only move toward the lower bound of the estimated neutral range, roughly between 1.00% and 2.50%. Some investors are already questioning whether the cycle will go any further. There is growing speculation that 1.00% could ultimately mark the terminal rate of the current tightening phase, limiting the scope for sustained Yen appreciation.

While there is theoretical room for rates to move deeper into neutral, that would require tangible evidence of stronger domestic demand. In particular, markets will look for results from Prime Minister Sanae Takaichi’s fiscal stimulus efforts, alongside clear proof that wage growth can be sustained into 2026.

Elsewhere, Dollar trading has steadied after New York Fed President John Williams reinforced skepticism around November’s CPI data. His remarks that the report was likely distorted validated market hesitation to push Dollar lower earlier in the week. As a highly influential Fed voice, Williams’ comments were taken seriously and helped anchor expectations that policy repricing will remain limited in the near term, probably until the December NFP data after holidays.

For the week so far, Kiwi sits at the bottom of the FX performance table, followed by Yen and Aussie. Swiss Franc leads, ahead of Sterling and Dollar, while Euro and Loonie remain positioned in the middle as markets.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.19%. CAC is down -0.06%. UK 10-year yield is up 0.041 at 4.531. Germany 10-year yield is up 0.044 at 2.897. Earlier in Asia, Nikkei rose 1.03%. Hong Kong HSI rose 0.75%. China Shanghai SSE rose 0.36%. Singapore Strait Times fell -0.02%. Japan 10-year JGB yield rose 0.057 to 2.024.

Fed’s Williams flags CPI distortions, plays down urgency to cut again

New York Fed President John Williams said today that November’s inflation data were likely distorted by "technical factors", cautioning against overinterpreting the downside surprise. He estimated that such distortions may have pushed the CPI reading down by around a tenth of a percentage point.

Williams said it remains difficult to fully assess the size of the impact until December data become available, which should provide a clearer picture of how much the technical effects influenced November’s figures.

On policy, Williams struck a measured tone, saying he does not feel a "sense of urgency" to lower interest rates further. He argued that the cuts already delivered have positioned the Fed well to continue easing inflation pressures while also supporting a labor market that is cooling in an orderly fashion.

Canada retail sales fall -0.2% mom in October, November rebound eyed

Canada’s retail sales edged down by -0.2% mom to CAD 69.4B in October, extending signs of soft consumer demand. Sales declined in four of nine subsectors, led by weakness at food and beverage retailers, pointing to ongoing pressure on discretionary spending.

Underlying momentum was weaker than the headline suggested. Core retail sales, excluding autos and gasoline, fell -0.5% mom. Sales volumes declined -0.6% mom.

Statistics Canada’s advance estimate points to a 1.2% mom rebound in November. While the estimate is based on a lower-than-usual response rate of 60%, it hints at a potential stabilization in consumption as financial conditions ease, though confirmation will depend on the final data.

BoJ raises rates to 0.75%, keeps tightening bias intact

The BoJ raised its policy rate by 25bps to 0.75%, as widely expected, marking another step in its gradual normalization process. Despite the hike, the BoJ emphasized that financial conditions remain highly accommodative, with real interest rates still “significantly negative.”

In its statement, the BoJ reaffirmed a tightening bias. If the outlook laid out in the October 2025 Outlook Report is realized, the Bank said it will "continue to raise the policy interest rate". Policymakers also expressed increased confidence that the likelihood of realizing the outlook "has been rising".

At the post-meeting press conference, Governor Kazuo Ueda stressed future adjustments will depend on incoming data on economic, price, and financial conditions, with policy decisions reassessed at every meeting rather than following a preset path.

On the neutral rate, Ueda acknowledged substantial uncertainty. He described the estimate as sitting within a wide range and said they would assess how the economy and prices respond to each rate move. "We will seek to produce new estimates on Japan's neutral rate, if needed, though I don't think that will help us narrow the range that much," he added.

NZ trade deficit narrows to ND -163m on 9.2% yoy exports surge

New Zealand’s trade balance surprised to the upside in November, with the deficit narrowing sharply to NZD -163m, far smaller than expectations for a shortfall of around NZD -1.2B. The improvement was driven by a solid pickup in exports, which rose 9.2% yoy, or NZD 588m, to NZD 7.0B.

Export performance was mixed by destination. Shipments to Australia surged by 31% yoy, while exports to the EU also rose strongly by 51% yoy. By contrast, exports to China slipped modestly by -0.7%yoy, while shipments to the US fell sharply by -17% yoy, and Japan by -1.9% yoy.

Imports rose at a more moderate pace of 4.4% yoy to NZD 7.2B. Gains were led by stronger inflows from the US (36% yoy), EU (17% yoy) and South Korea (20% yoy). Imports from China rose a modest 1.7% yoy. Imports from Australia declined (-7.7% yoy).

NZ ANZ business confidence hits 30-year high as cyclical recovery gathers pace

New Zealand business confidence surged in December, with the ANZ headline index jumping from 67.1 to 73.6. Firms’ own activity outlook rose sharply from 53.1 to 60.9. Both readings are the strongest in 30 years, pointing to a broad-based improvement in sentiment as the economic cycle turns.

Inflation indicators ticked up modestly but remain contained. The share of firms expecting to raise prices in the next three months rose one point to 52%, while those anticipating cost increases climbed two points to 76%. Inflation expectations, however, were unchanged at 2.69%, suggesting confidence is improving without triggering a renewed inflation scare.

ANZ said “things are clearly looking up,” noting that the earlier slowdown was deliberately engineered by tight monetary policy. With that restraint easing, interest rates and the exchange rate both well below their peaks, and the RBNZ signaling no intention to hike rates any time soon, cyclical forces appear firmly supportive of recovery.

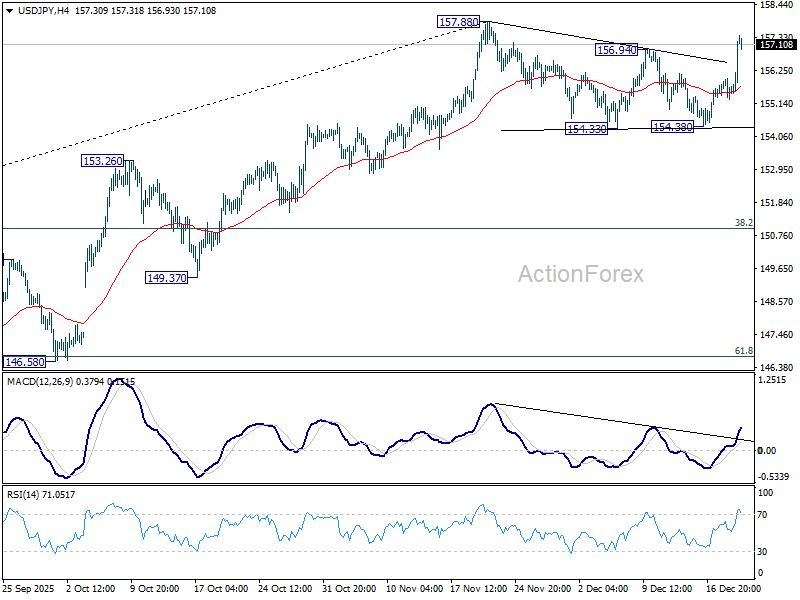

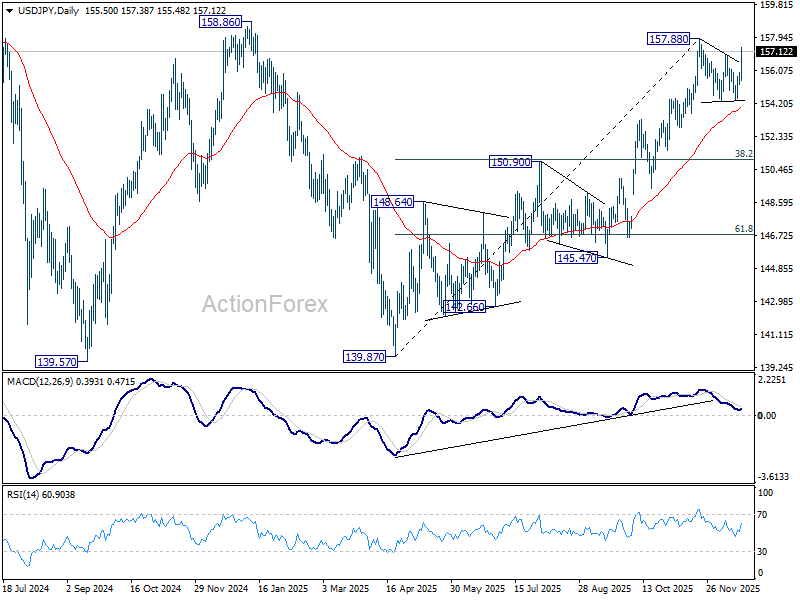

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.23; (P) 155.61; (R1) 155.93; More...

USD/JPY's rally continues today and the break of 156.94 solidify that case that corrective pattern from 157.88 has completed with three waves to 154.38. That is, rally form 139.87 is ready to resume. Intraday bias is back to the upside for 157.88 and above. Firm break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 158.85 high. Risk will now stay on the upside as long as 154.38 support holds, in case of retreat.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

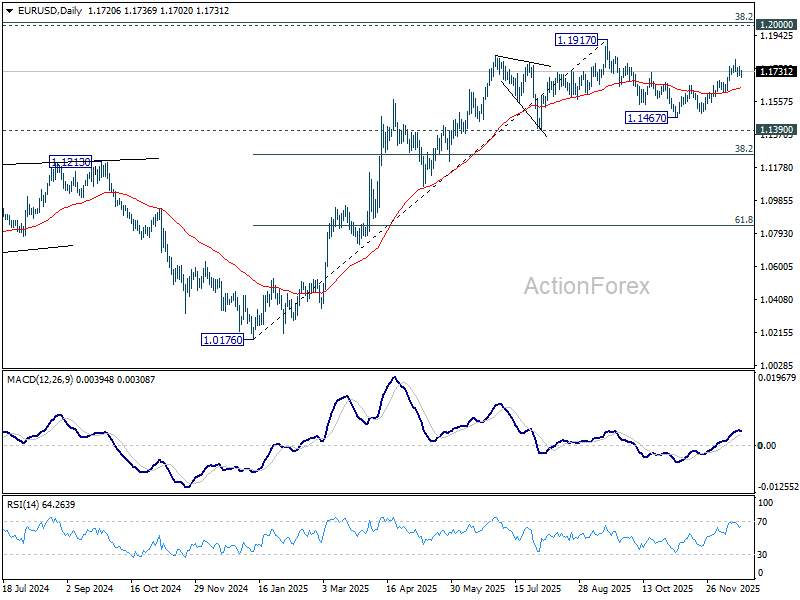

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1704; (P) 1.1734; (R1) 1.1754; More….

EUR/USD is still bounded in range below 1.1803 and intraday bias stays neutral. On the upside, break of 1.1803 will resume the rally from 1.1467 to retest 1.1917 high. Decisive break there will resume larger up trend. On the downside, however, firm break of 55 D EMA (now at 1.1640) will turn bias back to the downside for 1.1467 support, to extend the corrective pattern form 1.19717 with another falling leg.

In the bigger picture, as long as 55 W EMA (now at 1.1373) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

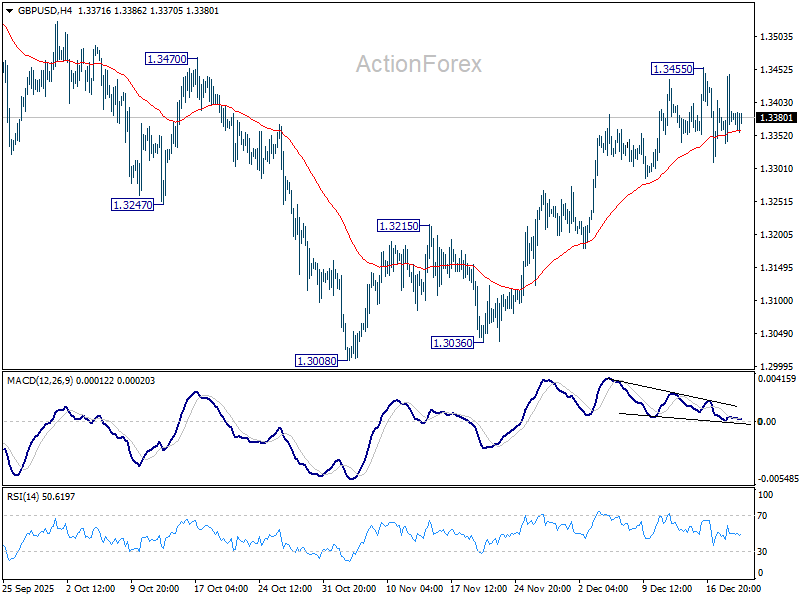

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3333; (P) 1.3390; (R1) 1.3439; More...

GBP/USD is still bounded in tight range below 1.3455 and intraday bias stays neutral. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3298) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.