Sample Category Title

USD/JPY Mid-Day Outlook

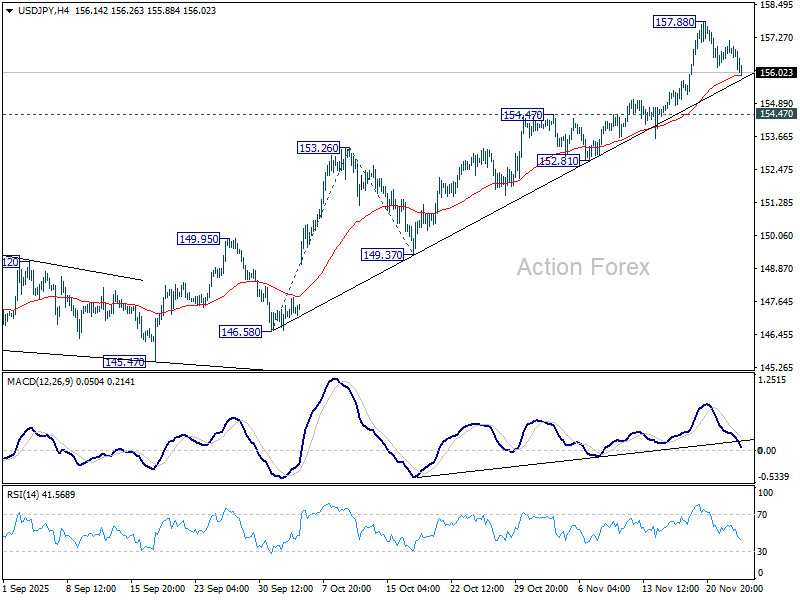

Daily Pivots: (S1) 156.46; (P) 156.82; (R1) 157.30; More...

USD/JPY's pullback from 157.88 extends lower today but stays well above 154.47 resistance turned support. Intraday bias remains neutral and further rally is expected. On the upside, break of 157.88 will resume the whole rally from 139.87, and target 161.8% projection of 146.58 to 153.26 from 149.37 at 160.17.

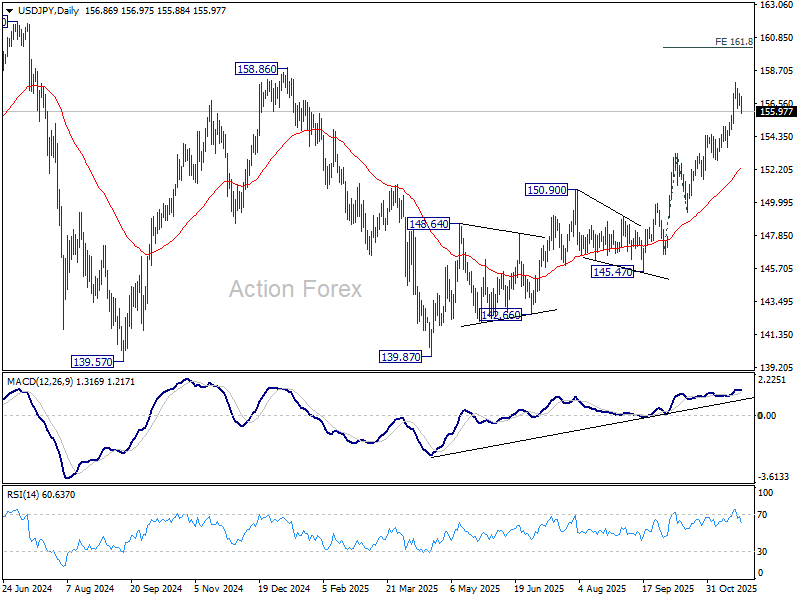

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

USD/CHF Mid-Day Outlook

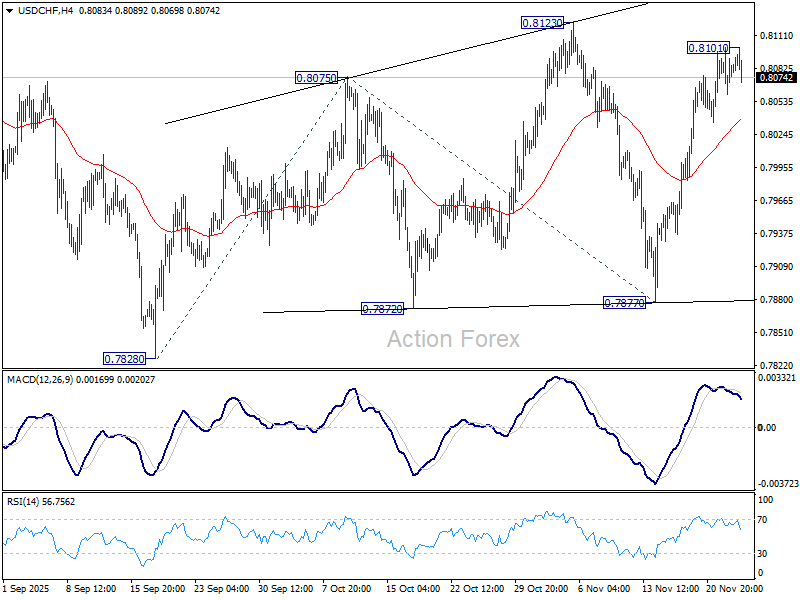

Daily Pivots: (S1) 0.8063; (P) 0.8082; (R1) 0.8104; More…

A temporary top should be in place at 0.8101 in USD/CHF, and intraday bias is turned neutral first. Current rise from 0.7877 is still seen as the third leg of the corrective pattern from 0.7828 low. Above 0.8101 will target 0.8123 resistance, and then 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.8218. However, sustained break of 55 D EMA (now at 0.8011) will bring deeper fall back to 0.7877 support instead.

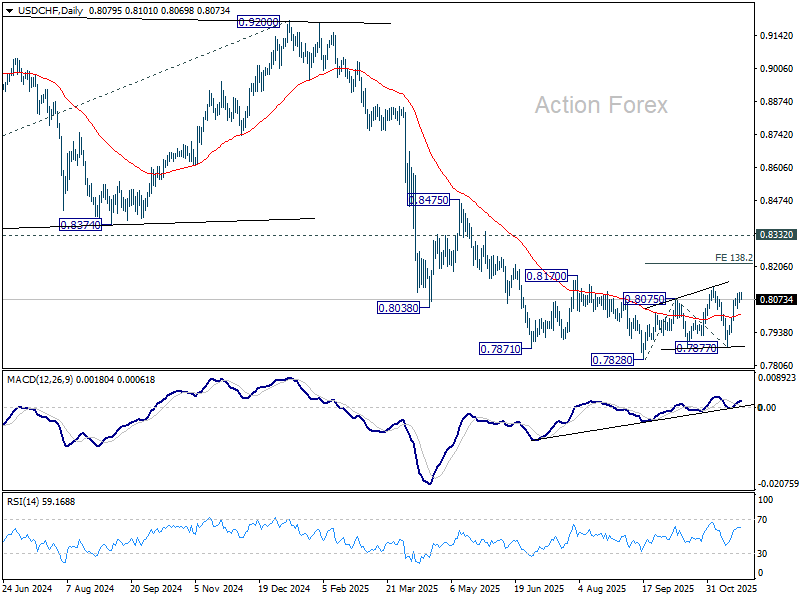

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

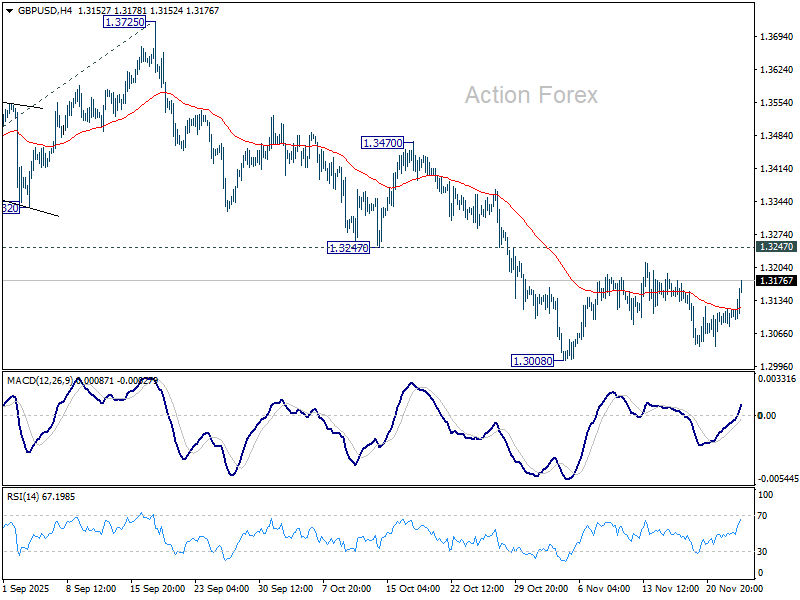

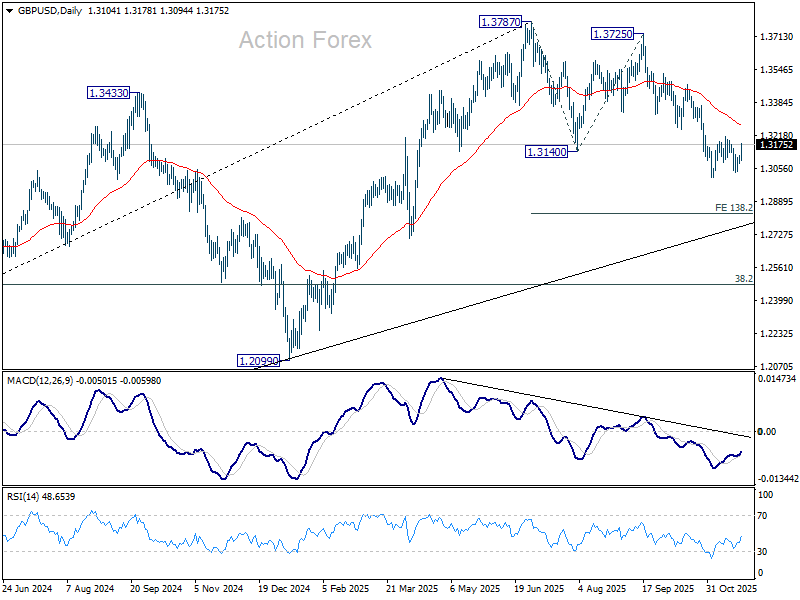

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3083; (P) 1.3101; (R1) 1.3121; More...

GBP/USD rebounds notably today but stays in range of 1.3008/3247, and intraday bias remains neutral. With 1.3247 support turned resistance intact, further decline is expected. On the downside, break of 1.3008 will resume the fall from 1.3725 to 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

US: Retail Sales Slow in September

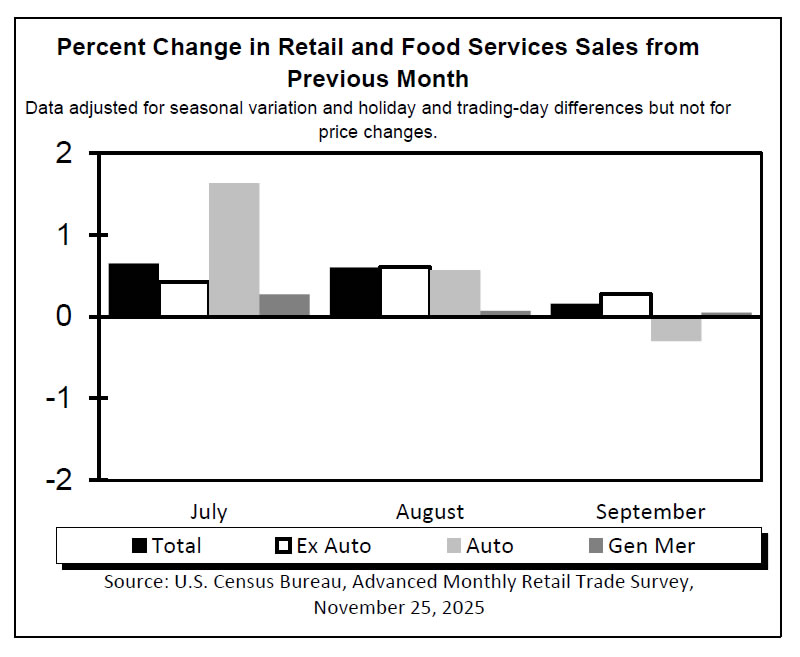

The delayed retail sales report showed retail sales rising by 0.2% month-over-month (m/m) in September. Spending growth decelerated from a 0.6% m/m pace seen in each of the prior two months and was slightly weaker than consensus expectations which called for a 0.3% gain.

Sales of autos & parts declined by 0.2%, while sales at the gasoline stations rose 2% alongside higher prices at the pump. Sales at building materials and garden equipment & supplies stores edged higher (+0.2% m/m) but were down 2.4% from its year-ago level.

Sales in the "control group", which excludes the three volatile components mentioned above (i.e., autos, gasoline and building supplies) were little changed on the month (-0.1%). Significant declines were reported by online retailers (-0.7%), though that comes after a string of solid gains in three months prior. Sales were also lower at clothing and accessories stores (-0.7%), electronics (-0.5%) and sporting goods (-2.5%). On the other hand, spending rose at miscellaneous store retailers (+2.9%) and furniture stores (+0.6%), with modest gains elsewhere.

Sales at bars and restaurants – the only service category in the report – had another strong month, rising by 0.7% and were up 6.7% from the year ago.

Key Implications

The delayed retail sales report showed some cooling in spending growth in September, following strong gains the two months prior. We will get a more complete picture of consumer spending in Q3 – including spending on services – on Dec 5th once data for consumer spending and income in September are released. At present, our tracking suggests a robust performance, with annualized growth around 3.3%. This marks an acceleration from the 2.5% pace seen in Q2 and represents a notable improvement compared to our earlier forecast.

Looking ahead to the fourth quarter, spending growth is expected to slow during the holiday season, with an annualized rate of growth of around 1%. Consumer sentiment has weakened in recent months, as households have become more concerned about the softening labor market, impacts from the government shutdown, and lingering inflation worries. Both the Conference Board and University of Michigan measures of consumer confidence have been declining since August.

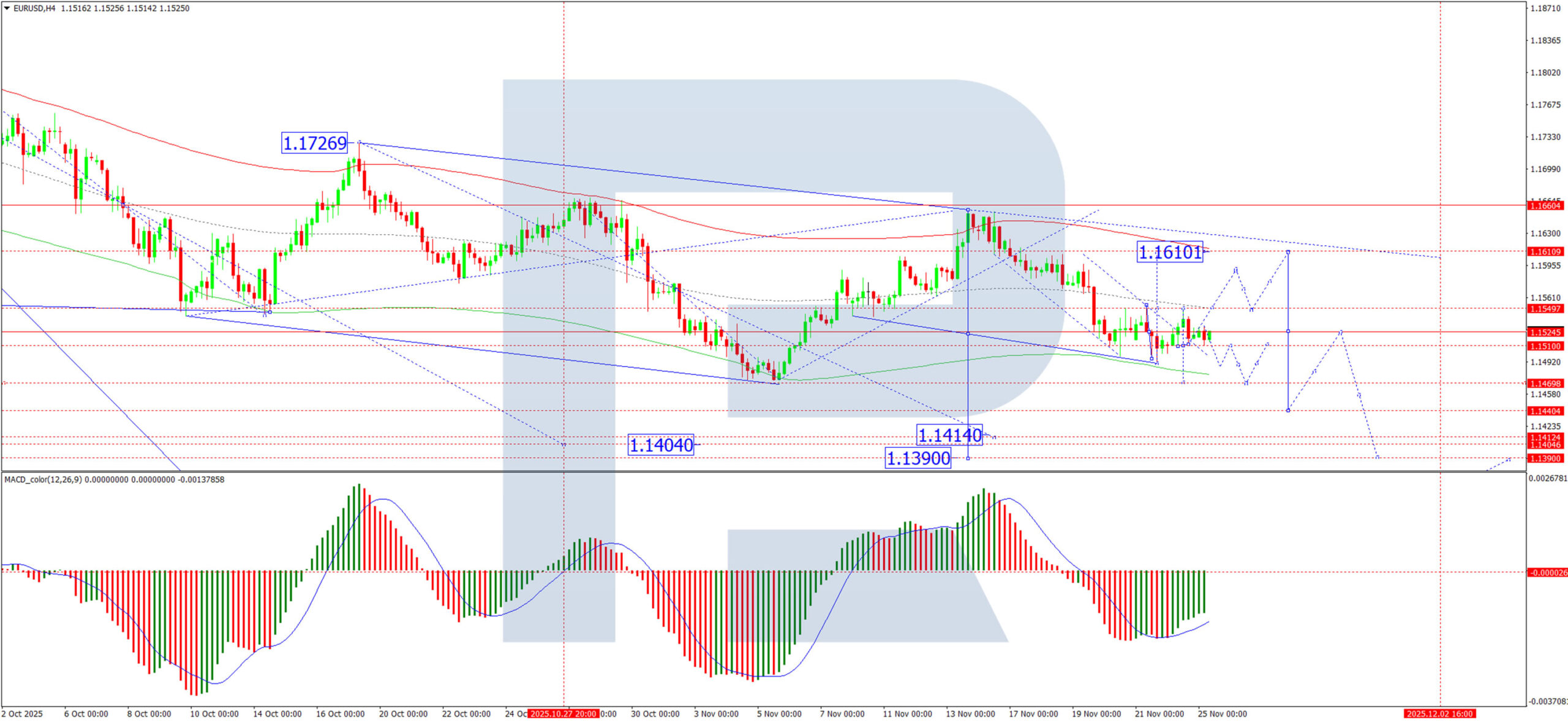

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1499; (P) 1.1524; (R1) 1.1547; More…

EUR/USD recovers further today but stays well below 1.1655 resistance. Intraday bias remains neutral and further decline is still in favor. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Dollar Softens Further on Dovish Repricing; Bessent Signals Fed Chair Decision Near

Dollar weakened notably against Euro and Yen in early U.S. session, tracking another leg lower in Treasury yields as markets absorbed softer-than-expected September retail sales. While the report was backward-looking, it reinforced the direction of travel for consumption and added incremental weight to the view that demand is steadily cooling. PPI, meanwhile, was nor alarming.

The easing narrative continues to strengthen. Fed funds futures now imply nearly an 85% probability of a 25bps cut in December, with investors leaning heavily on the growing chorus of key Fed officials highlighting labor-market risks over inflation concerns. Dollar’s dip reflects that shift, though reactions across asset classes are uneven. Equity futures were broadly steady in pre-market trade.

Meanwhile, U.S. Treasury Secretary Scott Bessent told CNBC that President Donald Trump is likely to announce his choice for the next Fed Chair before Christmas. He emphasized that the timeline ultimately rests with the president but described the selection process as “moving along very well.”

The shortlist remains broad. Candidates believed to be under consideration include NEC Director Kevin Hassett, former Fed Governor Kevin Warsh, BlackRock’s Rick Rieder, and current Fed Governors Christopher Waller and Michelle Bowman. Bessent also hinted at a philosophical shift in how the administration views the Fed’s role. He suggested the central bank should “move back into the background” and play a less dominant role over the economy and markets than it has since the financial crisis.

In daily performance terms, Yen leads the majors, followed by Sterling and Euro. Kiwi is the weakest performer, trailed by Swiss Franc and Aussie, while Euro and Loonie sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.44%. DAX is up 0.71%. CAC is up 0.66%. UK 10-year yield is down -0.037 at 4.507. Germany 10-year yield is down -0.014 at 2.680. Earlier in Asia, Nikkei rose 0.07%. Hong Kong HSI rose 0.69%. China Shanghai SSE rose 0.87%. Singapore Strait Times fell -0.24%. Japan 10-year JGB yield rose 0.016 to 1.804.

US retail sales miss at 0.2% mom growth in September

US retail sales rose 0.2% mom to USD 733.3B in September, falling short of the 0.4% forecast. Ex-auto sales performed slightly better at 0.3% mom, in line with expectations. Ex-gasoline sales were flat.

On a longer view, sales for the July–September period were still up 4.5% yoy, indicating that overall demand remains broadly supported.

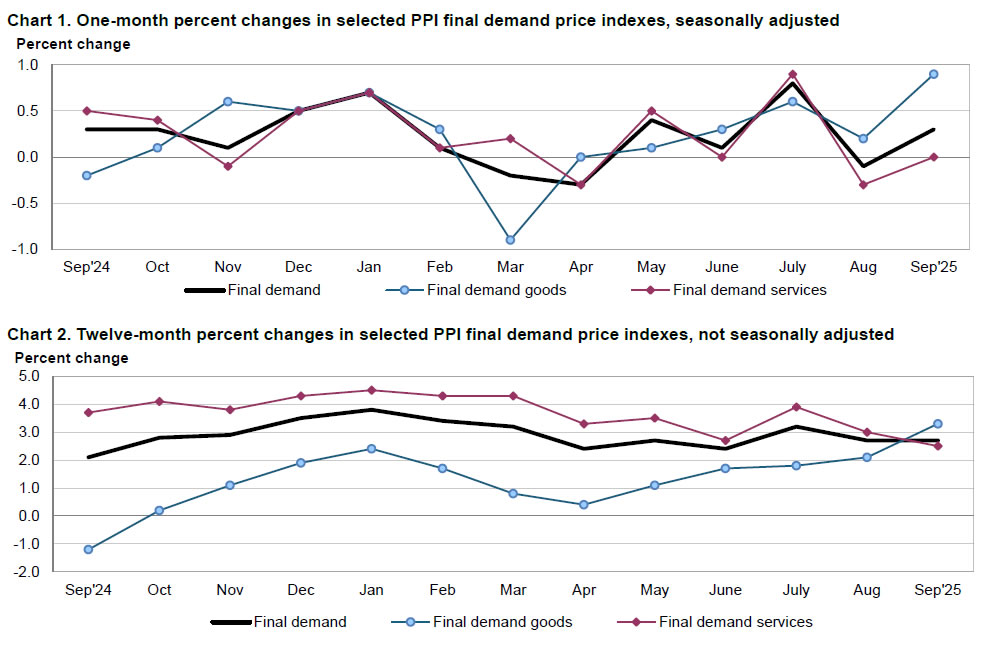

US PPI rises 0.3% mom in September, core pressure eases

US PPI rose 0.3% mom and 2.7% yoy in September, matching expectations. The entire monthly advance came from goods, where prices jumped 0.9%, while services were flat.

PPI final demand less food, energy, and trade—edged up just 0.1% mom after a firmer 0.3% mom reading in August. On a 12-month basis, core rose 2.9%.

UK retail sentiment hits 17-year low ahead of Autumn Budget

UK retail sentiment deteriorated sharply in November, with the CBI’s quarterly Distributive Trades Survey showing confidence plunging to its worst level in 17 years. Firms expect their business situation to worsen over the coming quarter, with the index sliding to -35% from -10% in August.

Sales volumes also contracted at a faster pace, with the year-to-November balance dropping to -32% from -27% in October. Retailers expect the decline to moderate slightly next month, but the outlook remains bleak, pointing to another weak patch heading into the key holiday period. Even modest stabilization would leave activity at depressed levels by historical standards.

CBI Deputy Chief Economist Alpesh Paleja said retailers are still grappling with "a long spell of weak demand". He added that uncertainty surrounding the forthcoming Autumn Budget is causing businesses to delay investment and hiring decisions.

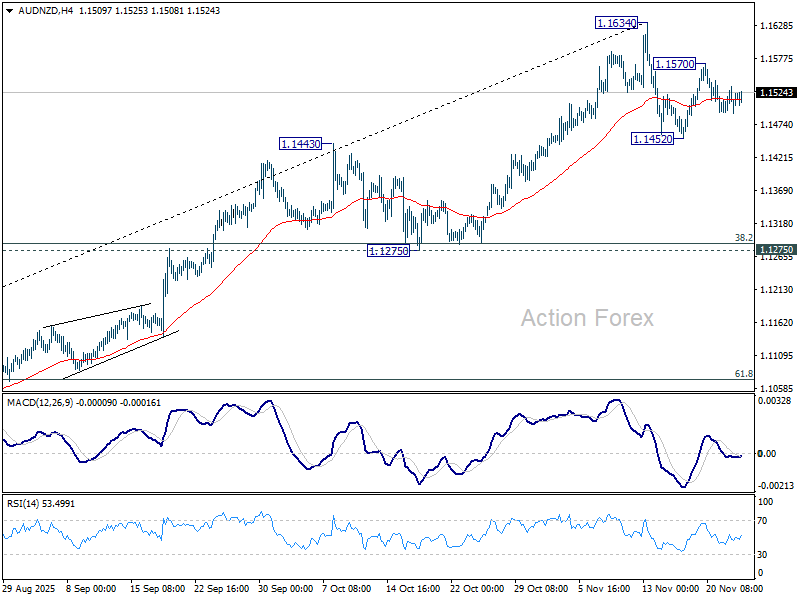

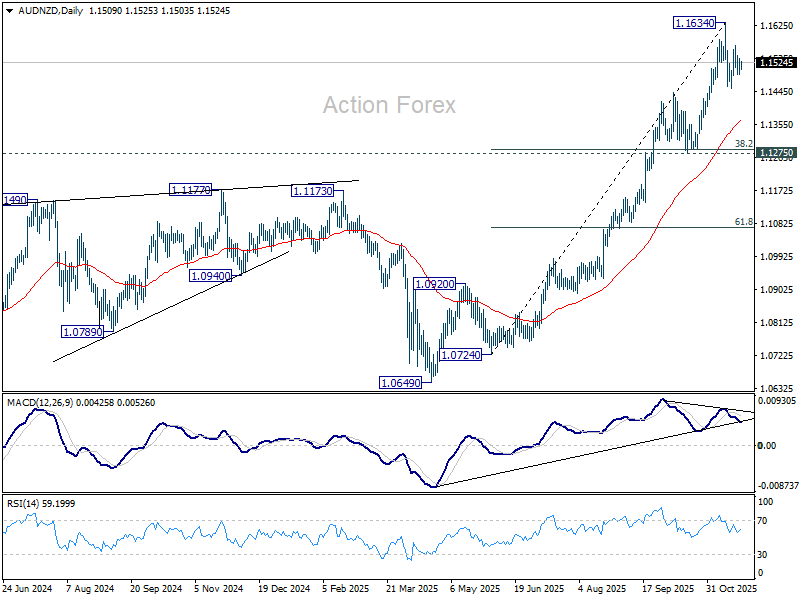

Two-way risks for AUD/NZD as RBNZ cut meets rising Australia CPI

AUD/NZD is shaping up for an active week, with two major catalysts—RBNZ’s rate announcement and Australia’s monthly CPI—set to hit on Wednesday.

RBNZ is widely expected to cut the OCR by 25bps to 2.25%. The NZIER Monetary Policy Shadow Board also endorsed a quarter-point reduction, arguing that although the economy is beginning to recover from a low base, excess capacity remains and a small additional cut is justified. Some members, however, warned against pushing stimulus too far, citing the risk of reigniting inflation—highlighting a cautious undercurrent within the broader policy debate.

On the medium-term path, the Shadow Board’s views clustered around an OCR of 2.25%–2.50% in a year, implying broad consensus that only limited easing will be required beyond November. While a minority still consider the risk of a larger, front-loaded cut—particularly given the long three-month gap until the next meeting—the Board’s recommendations may help stabilize expectations at a standard 25bps move.

In Australia, CPI is expected to rise again, from 3.5% to 3.6% for October, the fourth consecutive acceleration from June’s trough of 1.9%. A trend like this keeps the RBA firmly on hold for the remainder of the year, with any upside surprise diminishing the likelihood of a February rate cut. Sticky inflation would strengthen AUD by reinforcing Australia’s higher-for-longer stance relative to New Zealand’s easing cycle.

Technically, AUD/NZD carved out a short-term top at 1.1634 earlier this month and has since turned sideway. For now, it’s seen as in a brief near term correction. Break of 1.1570 minor resistance will solidify this case and bring retest of 11634 high.

However, on the downside, break of 1.1452 support will indicate that deeper decline is underway, as fall from 1.1634 could be correcting whole rise from 1.0724. But even so, downside should be contained by 1.1275 cluster support (38.2% retracement of 1.0724 to 1.1634 at 1.1286) or even higher at 55 D EMA (now at 1.1362).

There should be one more up leg through 1.1634 before the whole five-wave up trend from 1.0649 (April low) completes.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1499; (P) 1.1524; (R1) 1.1547; More…

EUR/USD recovers further today but stays well below 1.1655 resistance. Intraday bias remains neutral and further decline is still in favor. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

US PPI rises 0.3% mom in September, core pressure eases

US PPI rose 0.3% mom and 2.7% yoy in September, matching expectations. The entire monthly advance came from goods, where prices jumped 0.9%, while services were flat.

PPI final demand less food, energy, and trade—edged up just 0.1% mom after a firmer 0.3% mom reading in August. On a 12-month basis, core rose 2.9%.

US retail sales miss at 0.2% mom growth in September

US retail sales rose 0.2% mom to USD 733.3B in September, falling short of the 0.4% forecast. Ex-auto sales performed slightly better at 0.3% mom, in line with expectations. Ex-gasoline sales were flat.

On a longer view, sales for the July–September period were still up 4.5% yoy, indicating that overall demand remains broadly supported.

UK retail sentiment hits 17-year low ahead of Autumn Budget

UK retail sentiment deteriorated sharply in November, with the CBI’s quarterly Distributive Trades Survey showing confidence plunging to its worst level in 17 years. Firms expect their business situation to worsen over the coming quarter, with the index sliding to -35% from -10% in August.

Sales volumes also contracted at a faster pace, with the year-to-November balance dropping to -32% from -27% in October. Retailers expect the decline to moderate slightly next month, but the outlook remains bleak, pointing to another weak patch heading into the key holiday period. Even modest stabilization would leave activity at depressed levels by historical standards.

CBI Deputy Chief Economist Alpesh Paleja said retailers are still grappling with "a long spell of weak demand". He added that uncertainty surrounding the forthcoming Autumn Budget is causing businesses to delay investment and hiring decisions.

EUR/USD Extends Losses as Dollar Strength Questioned

The EUR/USD pair declined further on Tuesday, edging towards 1.1512. This downward movement persists despite a recent bout of US dollar weakness, which was triggered by a series of dovish comments from Federal Reserve officials that significantly increased the likelihood of an imminent rate cut.

The shift in sentiment was led by Governor Christopher Waller, who expressed support for a December cut, citing mounting risks to the labour market. Other officials, including Mary Daly and John Williams, echoed his stance. Waller also emphasised that policy decisions in 2026 will be contingent upon a large volume of delayed economic data, which agencies are now beginning to publish following the end of the government shutdown.

This coordinated messaging has caused a dramatic repricing in interest rate futures. The market-implied probability of a 25-basis-point cut in December has surged to 81%, a substantial increase from just 42% a week ago.

Despite this dovish tilt, the US dollar has demonstrated resilience. Investor focus is now shifting to a slew of upcoming data releases, including reports on retail sales, PPI, durable goods orders, and weekly jobless claims, which will provide a clearer picture of the US economy's health.

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, EUR/USD is forming a tight consolidation range above the key support at 1.1510. The current structure suggests a high probability of a technical correction towards 1.1588, with the potential to extend this rebound to 1.1616. However, a decisive downward breakout from this range would signal the resumption of the primary downtrend, activating the next bearish impulse with an initial target at 1.1488. The MACD indicator technically supports this scenario. Its signal line is below zero but is pointing upwards, indicating building momentum for a short-term correction within the broader bearish environment.

H1 Chart:

On the H1 chart, the pair completed a growth wave to 1.1549 before declining to 1.1510, forming a consolidation range around 1.1530. An upward breakout could initiate another leg higher towards 1.1568, potentially extending to 1.1616. It is crucial to view any such strength as a corrective rally before the larger downtrend resumes, targeting a move back towards 1.1500. Conversely, a downward breakout would directly activate the bearish potential for a decline to 1.1488, a level that could mark the completion of the first phase of the third wave within the broader downward trend. The Stochastic oscillator aligns with the near-term corrective view, as its signal line has turned up from the 20 level, suggesting room for a bounce towards 80.

Conclusion

While dovish Fed rhetoric has injected volatility and capped the dollar's gains, the EUR/USD remains in a fragile technical position. The immediate outlook hinges on the pair's ability to hold the 1.1510 support. A break higher would trigger a corrective rally towards 1.1616, offering a potential selling opportunity. However, a failure to hold this level would open the path for a more pronounced decline towards 1.1488 and possibly lower, reaffirming the underlying bearish trend.