Sample Category Title

AUD/USD Attempts Bounce, But Bulls Face Tough Test Ahead

Key Highlights

- AUD/USD started a fresh decline and traded below 0.6500.

- A bearish trend line is forming with resistance at 0.6470 on the 4-hour chart.

- EUR/USD is consolidating losses above the 1.1480 support.

- GBP/USD is facing a major hurdle near 1.3120 and 1.3140.

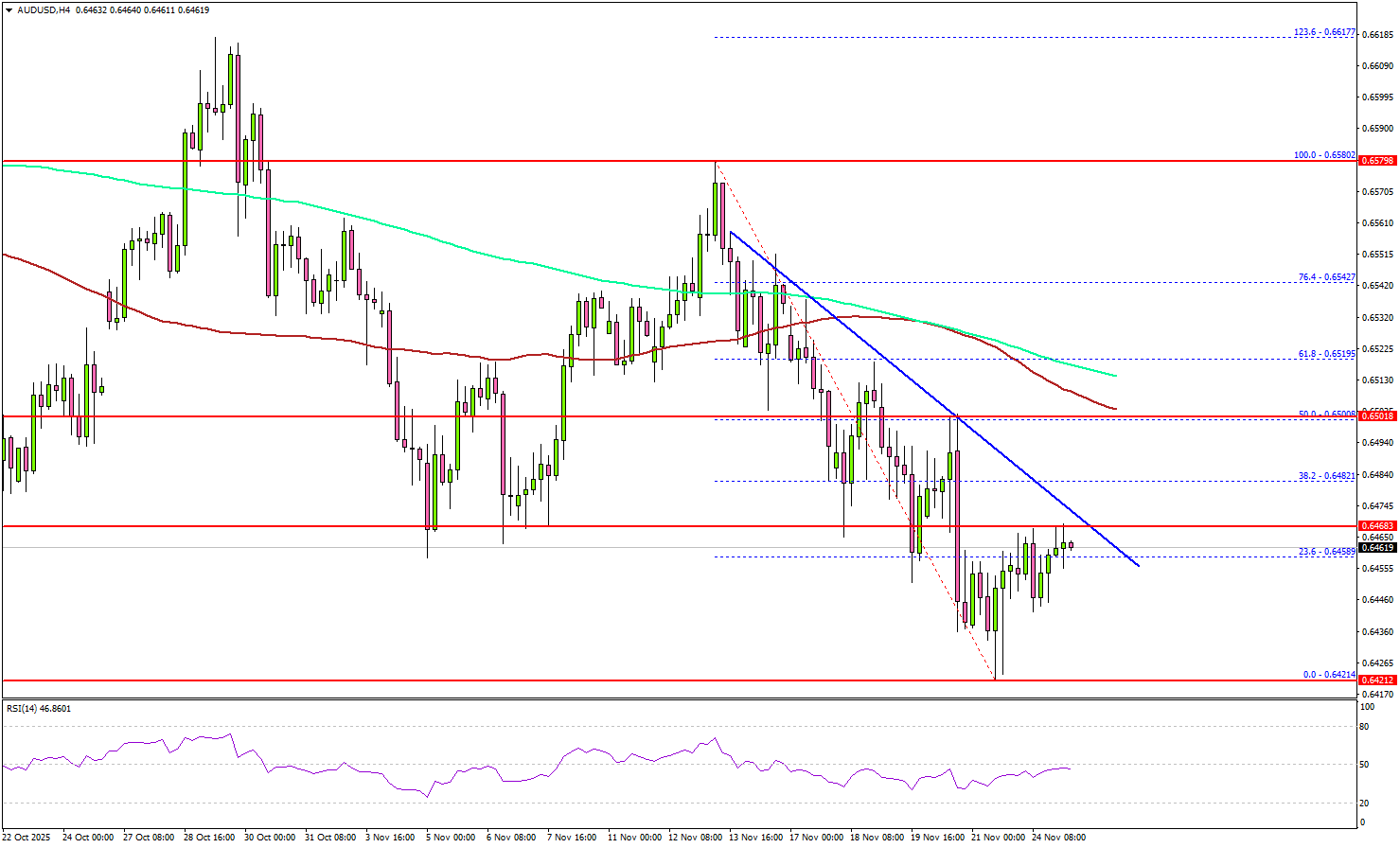

AUD/USD Technical Analysis

The Aussie Dollar declined below 0.6550 and 0.6500 against the US Dollar. AUD/USD tested the 0.6420 zone and is currently attempting to recover.

Looking at the 4-hour chart, the pair recovered a few pips and climbed above 0.6450. There was a move above the 23.6% Fib retracement level of the downward move from the 0.6580 swing high to the 0.6421 low.

However, the pair is still below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). Besides, there is a bearish trend line forming with resistance at 0.6470.

A close above the trend line resistance might call for a steady increase. The first key hurdle sits at 0.6500 and the 50% Fib retracement level of the downward move from the 0.6580 swing high to the 0.6421 low. The next resistance could be 0.6520. Any more gains could set the pace for a steady increase toward 0.6550.

On the downside, there is a key support at 0.6420. The next support is 0.6400, below which the pair could start a steady decline to 0.6365. A close below 0.6365 could start a pullback toward 0.6320.

Looking at EUR/USD, the pair failed to recover steadily and is now at risk of another decline, possibly below the 1.1480 support.

Upcoming Key Economic Events:

- US Pending Home Sales for Feb 2025 (YoY) - Forecast +2.1%, versus -2.8% previous.

- US Retail Sales for Oct 2025 (MoM) – Forecast +0.1%, versus 0% previous.

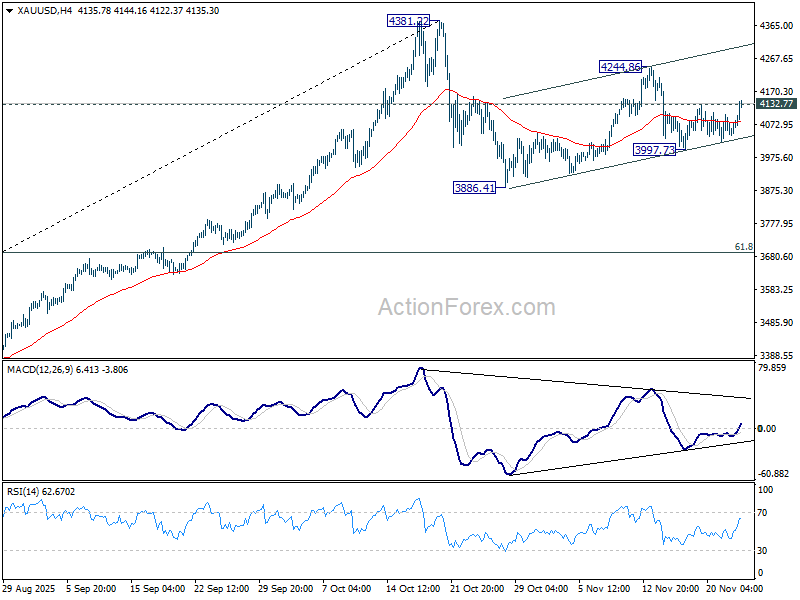

Gold rises towards 4244 as dovish Fed signals drive yields lower

Gold pushed higher this week as markets continued to recalibrate toward a December Fed rate cut. The move come in tandem with notable falling 10-year yield, which provide some tailwinds to the precious metal too. More upside is expected in Gold in the near term, even though a new record is still expected next year, rather than this.

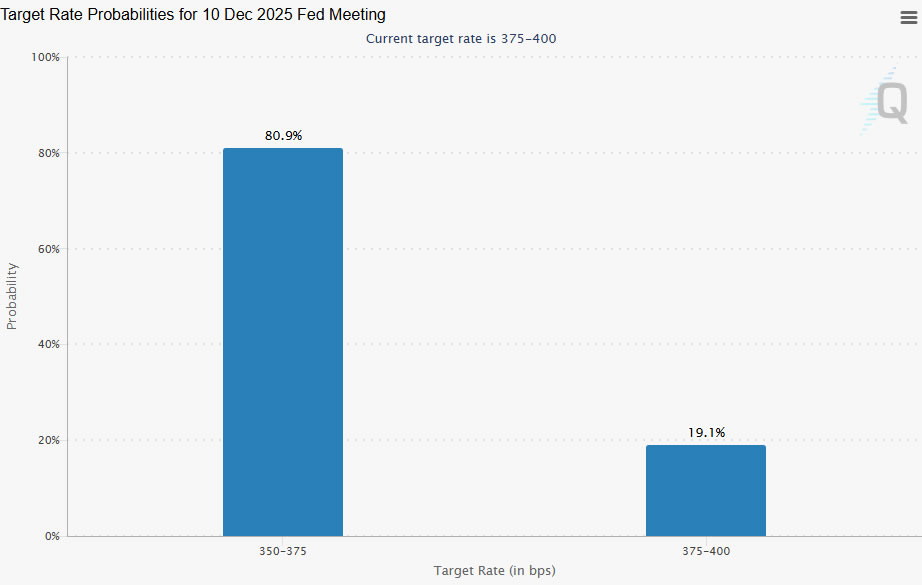

The Fed’s internal balance has moved noticeably toward the dovish camp. Mary Daly, in her WSJ interview, argued that labor-market fragility now poses a greater risk than inflation and said she supports easing next month. While not a vote, her comments—combined with John Williams’ earlier pivot—validates that the center of the Fed’s spectrum has shifted meaningfully towards easing. That has driven expectations for a December cut to around 80%.

Technically, 10-year yield's break of 4.056 support suggests that corrective rebound from 3.947 has completed at 4.162, after hitting falling channel resistance that started at 4.629 (May high). Further decline would now be seen towards 3.947 low.

Gold’s breakout above 4,132.77 indicates that pullback from 4,244.86 bottomed at 3,997.73. The rally from 3,886.41, as the second leg of the broader corrective pattern from 4,381.22, remains in progress. Further rise is expected to 4,244.86 and higher, as support by weakness in yield. But strong resistance should emerge from 4,381.22 high to cap upside to bring the third leg of the pattern.

Fed’s Daly backs December cut, warns job market risks outweigh inflation

San Francisco Fed President Mary Daly signaled clear support for a rate cut at next month’s FOMC meeting, telling the Wall Street Journal that the Fed now faces greater risk from a sudden deterioration in the labor market than from another inflation flare-up.

She said the job market is “vulnerable enough now” that the risk of a sharp, "nonlinear" weakening is rising, leaving policymakers with less room to react if they wait too long. Daly emphasized that she no longer feels confident the Fed can “get ahead of” labor-market weakening, arguing that the damage from a sudden drop in hiring would be harder to manage than moderating inflation.

On inflation, Daly said the chance of a meaningful reacceleration appears limited, pointing to softer-than-expected tariff-related cost increases this year.

Crypto Bloodbath Stalls: Is a Bottom In?

The relentless crypto bloodbath appears to have finally stalled, and signs suggest the market may have already posted a definitive bottom.

Bearish acceleration had driven prices to stark troughs, with Bitcoin grazing the $80,000 level and altcoins suffering even steeper declines. XRP plunged below $2.00, Ethereum tested levels near $2,800, and Solana dropped to trade near $125.

However, as key technical areas and Fibonacci retracements triggered interest from both opportunistic investors and algorithms, dip-buying has brought the Crypto Market higher to start the week. Bitcoin is now testing the $88,000 level, while Ethereum is climbing back towards the $3,000 psychological level.

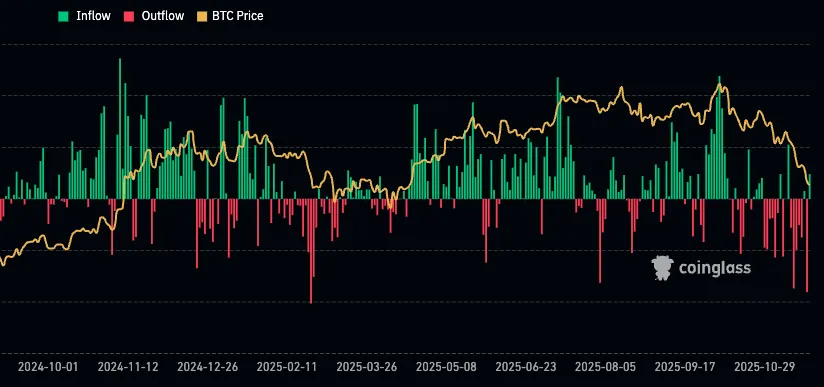

ETF Inflows and Outflows in 2025 – Source: Coinglass

Crucially, institutional flows are signaling a shift. Bitcoin and Ethereum ETFs are seeing their first renewed inflows after a painful 6-week streak of net outflows that reflected general deleveraging across digital assets.

The Total Market Cap, which posted lows around $2.74T just last Friday, is also staging a recovery.

Buoyed by a broadly more positive mood in markets—fueled by a dovish repricing for the Fed's December meeting, strong beats on Nvidia earnings, and potential trade reopening talks with China—the total valuation is once again breaking back above the pivotal $3T mark.

This level will be extremely important to hold as it equates to the 2021 Bull Market peak.

Screenshot 2025-11-24 at 2.28.05 PM

Crypto Total Market Cap – Bouncing at the lows of its Channel. November 24, 2025 – Source: TradingView

The Picture is Green after many Red days

Daily overview of the Crypto Market (14:30 ET), November 24, 2025 – Source: Finviz

Bitcoin and Ethereum 2-timeframe Analysis

Bitcoin Weekly Chart

Bitcoin (BTC) Weekly Chart, November 24, 2025 – Source: TradingView

A ruthless 37% descent for the pioneer Crypto has taken a break as multiple confluences of Technical Supports are coming through.

The 61.8% retracement of the entire move from the 2023 ($15,500!) lows has brought some interest, as this Fibonacci level tends to generate traction among Traders and Investors.

This also comes at an imperfect touch of the 2023 trendline, which presents one of the most important technical support on the long-run.

Breaking this line will let the $75,000 Liberation Day as an emergency lifeline but after that, there isn't much before the $60,000 Monthly Support.

Bitcoin Intraday (8H) Chart and Technical Levels

Bitcoin (BTC) 8H Chart, November 24, 2025 – Source: TradingView

A Bullish divergence on the 8H Timeframe also helped the shorter-timeframe buyers to step in quite aggressively.

A precedingly downside-broken Bear Channel pointed to extreme fear which wasn't followed by momentum accumulation, which tends to create Bullish divergences on the RSI.

These are strong setups for mean-reversion, however not much says for how long things will rebound.

Therefore, keep an eye on the Channel lows for Short-term support (if it breaks, more bearish).

On the other hand, holding the Channel after a fakeout could lead to a $102,000 higher bound test.

Levels of interest for BTC trading:

Support Levels:

- $90,000 to 93,000 major support turned Pivot

- Current Weekly Lows $89,340

- $85,000 mid-term Support (+/- $1,500)

- $75,000 Key long-term support

Resistance Levels:

- $90,000 to 93,000 major support turned Pivot

- $98,000 to $100,000 Main Support, now Pivot (MA 50 at $100,000)

- $102,000 Bear Channel Highs

- Resistance at previous ATH $106,000 to $108,000

- Current ATH Resistance $124,000 to $126,000

Ethereum (ETH) Weekly Chart

Ethereum (ETH) Weekly Chart, November 24, 2025 – Source: TradingView

The $2,700 Level mentioned in our very recent ETH analysis was used as a trampoline for Buyers.

The next test will be to break and hold above $3,000, which also corresponds with the mid-lane of the Channel. Above this, breakout odds greatly increase.

Ethereum Intraday (8H) Chart and Technical Levels

Ethereum (ETH) 8H Chart, November 24, 2025 – Source: TradingView

Levels of interest for ETH trading:

Support Levels:

- $2,500 to $2,700 June Key Support (recent rebound)

- $2,620 Session and weekly Lows

- $2,100 June War support

- $1,385 to $1,750 2025 Support

- 2025 Lows $1,384

Resistance Levels:

- $3,000 to $3,200 Major momentum Pivot (Test of the $3,000)

- $3,500 (+/- $50) Resistance and Descending Channel highs

- $3,800 September lows

- $4,000 to Dec 2024 top Higher timeframe Resistance zone

- $4,950 Current new All-time highs

Safe Trades!

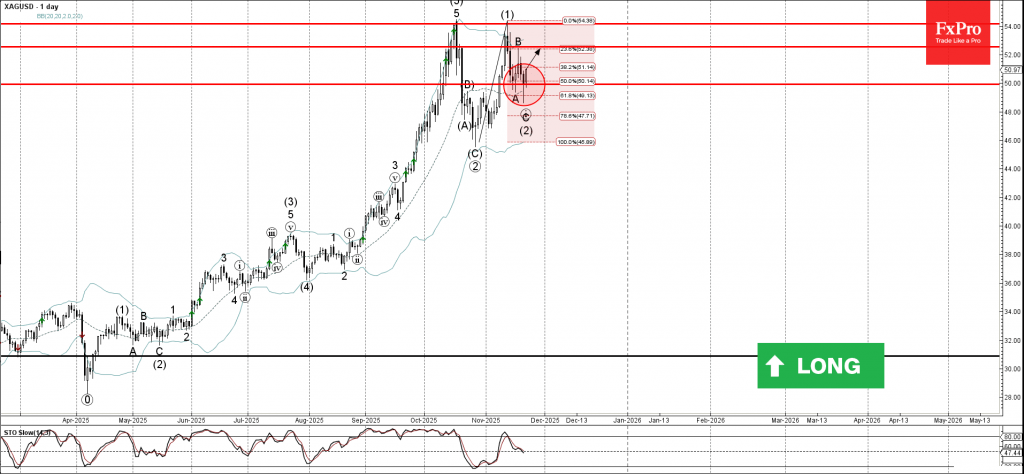

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver reversed from support area

- Likely to rise to resistance level 52.50

Silver recently reversed from support area between the round support level 50.00 (which was set as the likely downward target in our earlier report for this instrument), 20-day moving average and the 50% Fibonacci correction of the upward impulse (1) from October.

The upward reversal from this support area started the active intermediate impulse wave (3).

Given the overriding daily uptrend, Silver can be expected to rise to the next resistance level 52.50 (top of the previous wave B).

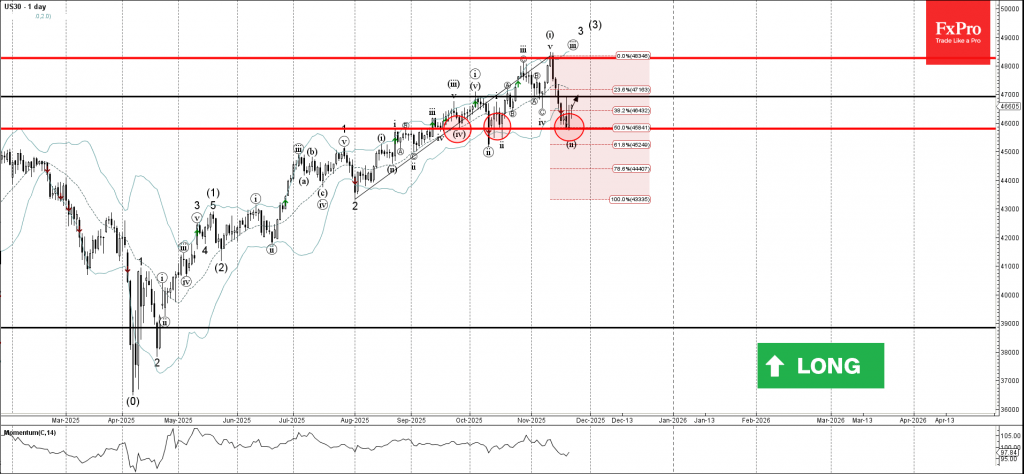

Dow Jones Wave Analysis

Dow Jones: ⬆️ Buy

- Dow Jones reversed from support area

- Likely to rise to resistance level 47000.00

Dow Jones index recently reversed from support area between the key support level 45800.00 (which has been reversing the price from September), lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from July.

The upward reversal from this support area stopped the previous short-term ABC correction 2.

Given the clear daily uptrend, Dow Jones index can be expected to rise to the next resistance level 47000.00 (top of the previous wave B).

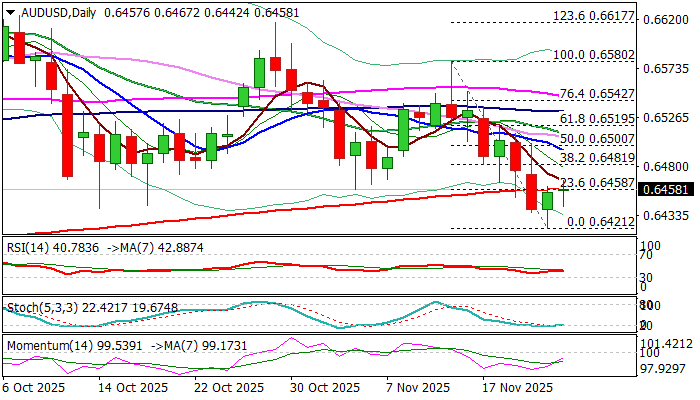

AUDUSD: Bounce from New Three-Month Low So Far Limited

AUDUSD – Last Friday’s bounce from new three-month low (bears were contained by the top of thick weekly Ichimoku cloud) was repeatedly obstructed by broken 200DMA (0.6458 – reverted to resistance)

Monday’s action is moving within limited range and shaped in long-legged Doji candle and signals indecision.

Conflicting fundamental signals (the latest dovish comments from Fed official revived expectations of December rate cut but countered by still prevailing concerns about inflation that may keep the central bank’s rates on hold next month) contribute to the current situation.

Investors also focus on Australia’s inflation report (due on Wednesday and the first time to be released on monthly basis, replacing old system of quarterly reports).

Technical picture remains bearishly aligned on daily chart (MA’s in bearish setup / negative momentum), with reaction on 200DMA to provide fresh signal.

Close above the moving average (0.6458, also Fibo 23.6% of 0.6580/0.6412) to add fresh optimism, though more work at the upside (lift above 0.6500 zone) needed to verify signal.

Conversely, repeated close below 200DMA to keep the downside at increased risk of violation of Aug 21 low (0.6414) and nearby Fibo 38.2% of larger 0.5914/0.6706 (0.6404).

Res: 0.6467; 0.6481; 0.6500; 0.6520

Sup: 0.6421; 0.6414; 0.6372; 0.6350

Sunset Market Commentary

Markets

Natural gas prices showed some of the larger daily moves today. They dropped below €30/MWh (Dutch TTF) for the first time since May 2024. Prices have been slowly grinding lower over the last couple of months on a combination of amongst others strong LNG imports and mild weather so far. But the trigger for today’s break originated from the US spearheading talks to end Russia’s war in Ukraine. It revived them with its 28-now-reduced-to-19-point peace plan and stability in the region could affect global supplies. The US is pushing for Ukraine to accept the deal and some senior officials have reported “meaningful progress” but some bullet points are (too?) hard to swallow for Ukraine, but also for the EU. These are mostly related to territorial concessions and a cap on Ukraine’s military size. In return, the US would offer security guarantees. President Trump had imposed a November 27 deadline for Ukraine to accept (or lose US military and intelligence support) but Secretary of State Rubio over the weekend clarified talks could go into next week. Oil prices also lose ground today but are off the intraday lows. Brent trades around $62.7/b. Movements in other corners of the market are limited. US Treasuries marginally outperform Bunds by shedding 1.2-2.8 bps in the 5-30yr bucket. US money markets crept a little bit further in the direction of a Fed rate cut next month. The market implied probability now stands at 72%. Fed governor Waller, still in the race to become the next chair, called for another reduction in an interview today, referring to weak labour market data. The flurry of economic releases that’ll come in after December 10 could make the decision for January trickier, Waller said. German yields trade flat on the day. Spreads vs swap narrow slightly, even in France where parlement rejected a first (partial) reading of the 2026 budget. Belgium outperforms a tad, the result of the government having agreed on a €9.2bn deficit-reducing multiannual budget through 2029. The European Commission warned last week that Belgium’s budget shortfall would rise from an expected -5.3% of GDP this year to -5.9% in 2027 in an unchanged-policy scenario. UK gilts hold their breath going into Wednesday’s release of the government’s Autumn Budget. Yields marginally ease at the long end of the curve. The euro is holding a minor upper hand in FX markets against most global peers. EUR/USD rises to 1.1532. The November lows just below 1.15 are still lurking though. EUR/GBP bounces back above 0.88. US stock markets kick off the holiday-shortened week in good spirits. The tech-heavy Nasdaq rises 1.5%. European equities limit gains to just 0.2%.

News & Views

Czech consumer confidence surged for a third consecutive month in November, from 107.4 to 111.7, its highest level since January 2019. Most consumers expected the overall economic situation in Czechia to improve over the next twelve months. The share of households expecting an improvement in their financial situation over the next twelve months increased compared to last month. At the same time, the share of respondents who assess their current financial situation as worse than in the previous twelve months decreased. The number of respondents who do not plan to make any major purchases in the next twelve months decreased slightly. Czech business confidence disappointed, falling from a more than 3-yr high at 103.4 to 99.9. On a sectoral level, confidence in the economy increased only in trade while declining in construction, industry, and to a lesser extent in selected service sectors. Weaker business sentiment carried the bigger weight in the composite confidence indicator, which corrected from the highest level since February 2008 (104) to 101.9. The Czech koruna strengthens today (EUR/CZK 24.15) with CE FX in general performing better against the background of Ukraine peace talks in Geneva.

Belgian business confidence rebounded slightly in November after a modest decline in October. Confidence improved in the business-related services sector (more positive assessment of current level of activity) and in manufacturing (significant improvement in demand expectations) while declining in building (drop in orders and reduced optimism about future demand) and trade (fear of significant drop in demand and in their orders to suppliers) sectors. Belgian consumer confidence, published last week, hit the highest level since October 2021.

Dollar Index (DXY) Technical Outlook: Pivotal Week for Dollar as Acceptance Above 100.00 Remains Key

Market participants are eyeing the US Dollar Index (DXY) as it hovers above the crucial 100.00 barrier. The greenbacks recent rally has been impressive but may fail to gain traction unless acceptance is achieved beyond the 100.00 psychological level.

A break above the 100.00 psychological level is no surprise to market participants as we have seen two forays beyond this handle in recent weeks. Having broken below the 100.00 mark in May of 2025, the DXY has attempted two recoveries prior to the current one.

The result? A significant materialized each time the DXY attempted a push higher beyond the 100.00 mark. Is history set to repeat itself?

From a technical standpoint, the Daily chart below appears to have printed a potential double-top pattern which hints at a deeper pullback.

The 200-day MA rests just below the 100.00 psychological level which could serve as dynamic support if price moves lower.

A break of the 200-day MA would be needed for a deeper correction to take place.

Acceptance above the 100.00 mark may find resistance at 100.61 before the 102.16 handle comes onto focus.

US Dollar Index (DXY) Daily Chart, November 24, 2025

Source: TradingView.com (click to enlarge)

Macroeconomic Backdrop

This week, which is shorter due to the Thanksgiving holiday in the U.S. on Thursday, a lot of attention will be on peace talks concerning Ukraine. Recent reports suggest the U.S. is becoming less supportive of Russia's maximum demands, and Ukrainian President Volodymyr Zelenskyy might travel to Washington later this week for direct talks with U.S. President Donald Trump. While specifics from the current Geneva peace talks are few, the overall mood is tentatively hopeful.

Aside from politics, the U.S. dollar's performance this week will be largely driven by upcoming U.S. economic data and the release of the Federal Reserve's Beige Book report on Wednesday evening. Tomorrow's retail sales data for September is expected to be strong, but the market is likely more interested in the Beige Book. Any informal information within that report from the Fed's regions indicating that the recent slowing in job growth is spreading could quickly renew the discussion about a potential Federal Reserve interest rate cut in December. This possibility was recently highlighted on Friday by comments from New York Fed President John Williams favoring another December rate cut, which caused the market's expectation for a December cut to jump back up to 75%. This high probability of a cut leads to the question of why the dollar is not weaker this morning.