Sample Category Title

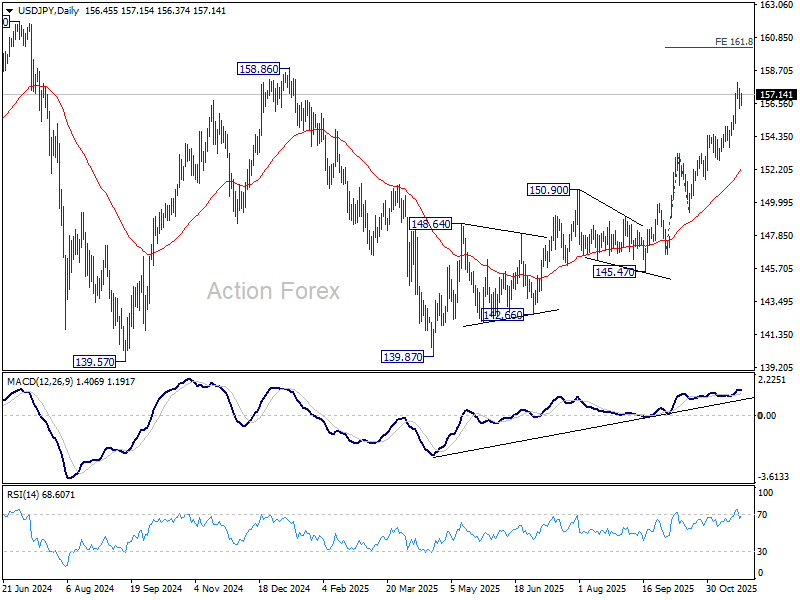

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.90; (P) 156.72; (R1) 157.24; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen below 157.88. Downside of retreat should be contained by 154.47 resistance turned support to bring rebound. On the upside, break of 157.88 will target 161.8% projection of 146.58 to 153.26 from 149.37 at 160.17.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

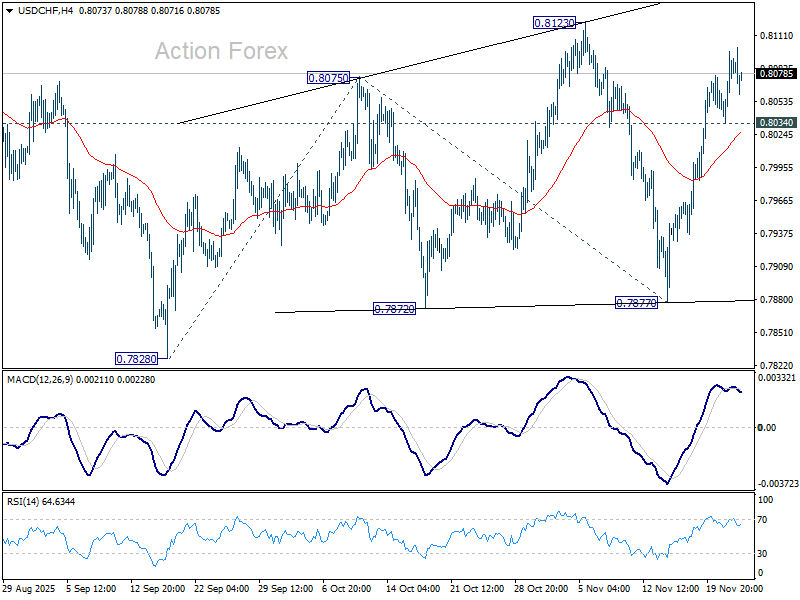

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8047; (P) 0.8073; (R1) 0.8110; More…

Intraday bias in USD/CHF remains mildly on the upside. Corrective pattern from 0.7828 low is still extending. Break of 0.8123 will target 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.8218. On the downside, below 0.8034 minor support will turn intraday bias neutral first.

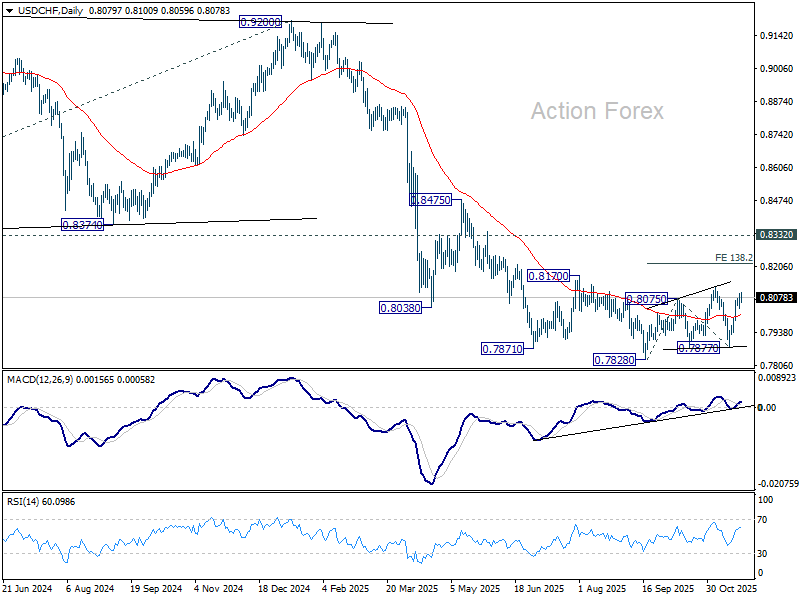

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

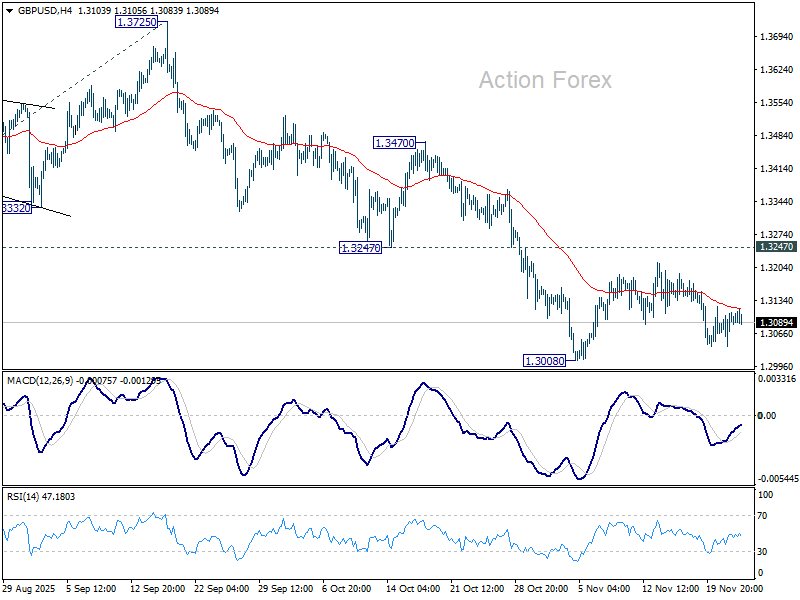

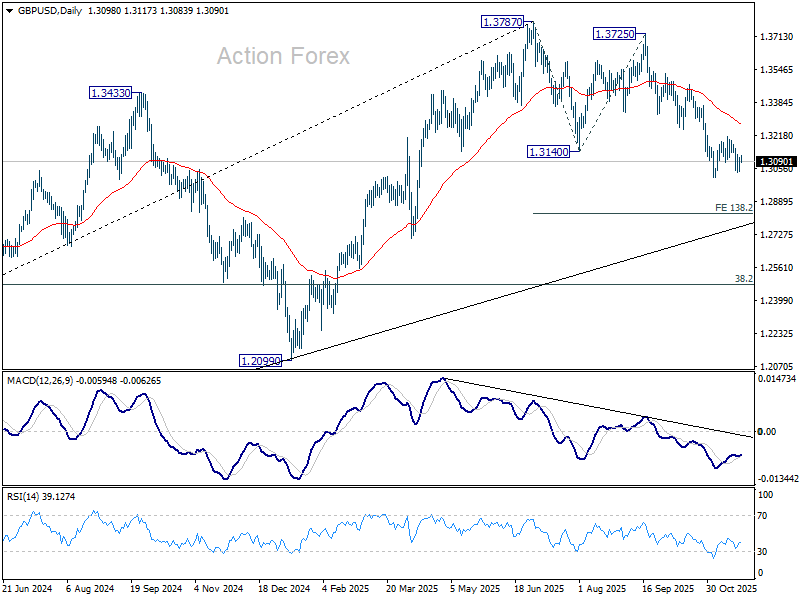

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3055; (P) 1.3083; (R1) 1.3126; More...

Sideway trading continues in GBP/USD and intraday bias remains neutral. With 1.3247 support turned resistance intact, further decline is expected. Break of 1.3008 will resume the fall from 1.3725 to 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

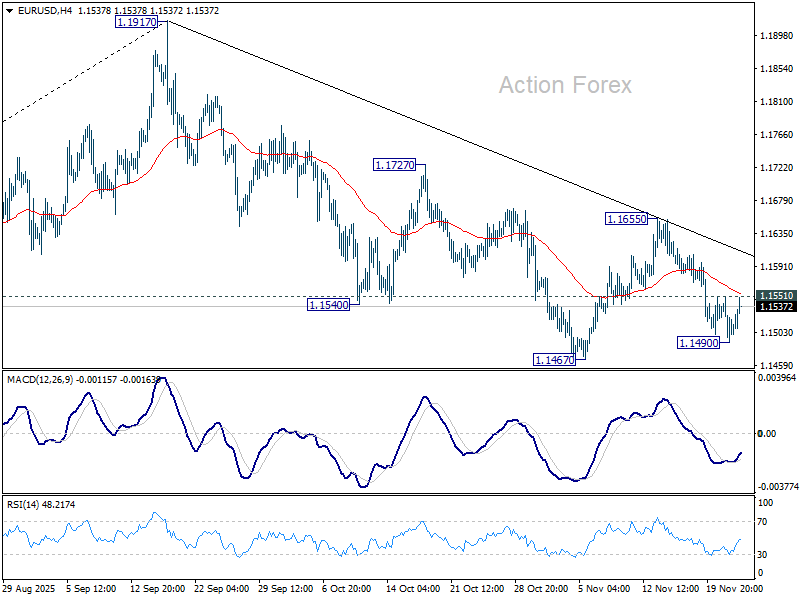

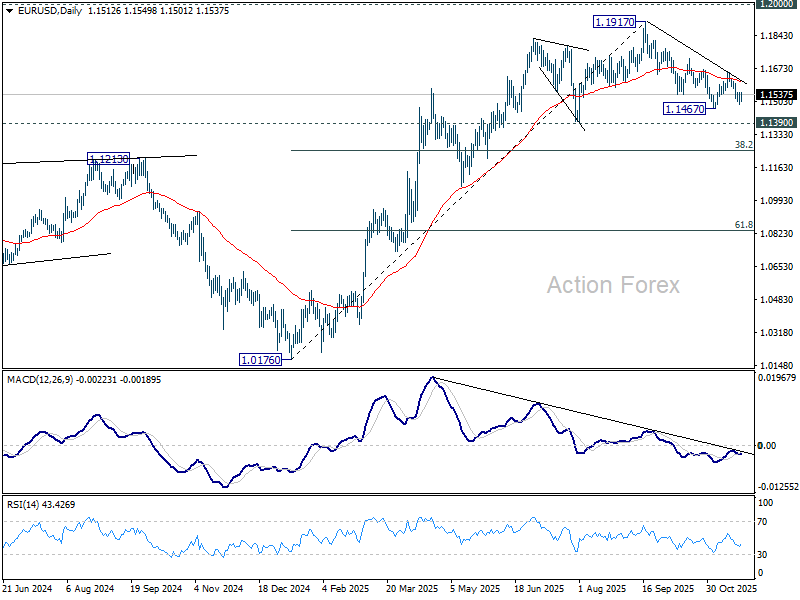

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1485; (P) 1.1519; (R1) 1.1547; More…

Intraday bias in EUR/USD is turned neutral first with today's recovery and some consolidations could be seen above 1.1490. Nevertheless, risk will stay on the downside as long as 1.1655 resistance holds. Below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Dollar Soft as Fed Doves Lift Cut Odds to 75%; Yen Slumps Again

Dollar is trading on the back foot today as markets add to bets on a December Fed rate cut, extending the repricing that began late last week. The shift was triggered by New York Fed President John Williams, who surprised markets last Friday by saying he sees room for a further “near-term adjustment,” reversing the hawkish tone embedded after the FOMC minutes.

Known dove Governor Christopher Waller reinforced the message today, saying a December cut is “appropriate” given continued labor-market softening and easing inflation pressures. He did note that January could be less straightforward due to the flood of delayed data, but markets latched onto the December signal. Fed funds futures now imply more than a 75% chance of a 25bps move next month, putting Dollar on the defensive.

Yen, however, is even weaker, continuing to unwind Friday’s rebound. Traders remain unmoved by verbal intervention efforts, including remarks from Takuji Aida—an influential private-sector member of a key government panel—who told NHK that Japan has “excessive foreign reserves” and should actively tap them for Yen-buying intervention. Markets have heard similar warnings many times recently and continue to fade them.

Meanwhile, a new nationwide Yomiuri Shimbun poll shows strong public backing for Prime Minister Sanae Takaichi. Her cabinet’s approval rating stands at 72%, essentially unchanged from its launch, and 74% of respondents support her pledge for “responsible, active fiscal policy.” High public approval strengthens her political leverage.

That public support makes it even harder for BoJ to push back against Takaichi’s preference to delay rate hikes, even as wage momentum and inflation persistence argue for gradual normalization. Political constraints remain one of the key reasons Yen continues to trade heavy, with markets skeptical that BoJ can accelerate tightening while fiscal stimulus remains the dominant policy tool.

Across the currency markets today, Euro leads the majors, followed by Sterling and Swiss Franc. At the other end, Yen is the weakest performer, with Loonie and Dollar also lagging. Aussie and Kiwi sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is up 0.75%. CAC is up 0.13%. UK 10-year yield is flat at 4.551. Germany 10-year yield is up 0.005 at 2.712. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 1.97%. China Shanghai SSE rose 0.05%. Singapore Strait Times rose 0.62%.

Fed’s Waller backs December cut, says January depends on data flood

Fed Governor Christopher Waller signaled clear support for a December rate cut, saying most private-sector and anecdotal data since the last FOMC meeting show little improvement in economic conditions. He noted that the labor market “is soft” and “continuing to weaken,” with inflation expected to ease, creating an environment where another cut next month is appropriate.

Waller said the January meeting presents more uncertainty, as the Fed will receive a “flood of data” that had been delayed by the government shutdown. If those releases align with recent trends—softening labor conditions and moderating inflation—then a case for another cut could be made. "But if it suddenly shows a rebound in inflation or jobs or the economy's taking off, then it might give concern,"" he added.

Beyond policy, Waller confirmed he met recently with Treasury Secretary Scott Bessent to discuss his potential nomination as the next Fed Chair, as the Trump administration moves to select a successor to Jerome Powell. Waller said the meeting went “great,” and argued that the administration is seeking someone with “merit, experience, and knows what they are doing,” adding, “I think I fit that.”

Powell’s term ends in May, leaving a narrow window for the White House to finalize its choice.

German Ifo falls to 88.1, firms see little prospect of near-term rebound

Germany’s business mood softened in November as the Ifo Business Climate Index edged down to 88.1 from 88.4, missing expectations of 88.5. The decline was driven mainly by weaker expectations, which dropped from 91.6 to 90.6. Assessment of current conditions improved slightly from 85.3 to 85.6.

Sector details remained broadly negative. Manufacturing slipped further from -12.1 to -12.5, reflecting sustained weakness in global demand and the lingering impact of U.S. tariff. Services eased from 2.9 to 2.6, hinting at a moderation in domestic resilience. Trade deteriorated from -20.4 to -21.4 and construction fell from -14.4 to -15.7. Together, these readings signal a still-fragile backdrop with limited catalysts for improvement heading into year-end.

Ifo noted that sentiment among German firms has deteriorated as companies grow more pessimistic about the medium-term outlook. While current conditions improved slightly, businesses “have little faith that a recovery is coming anytime soon.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1485; (P) 1.1519; (R1) 1.1547; More…

Intraday bias in EUR/USD is turned neutral first with today's recovery and some consolidations could be seen above 1.1490. Nevertheless, risk will stay on the downside as long as 1.1655 resistance holds. Below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

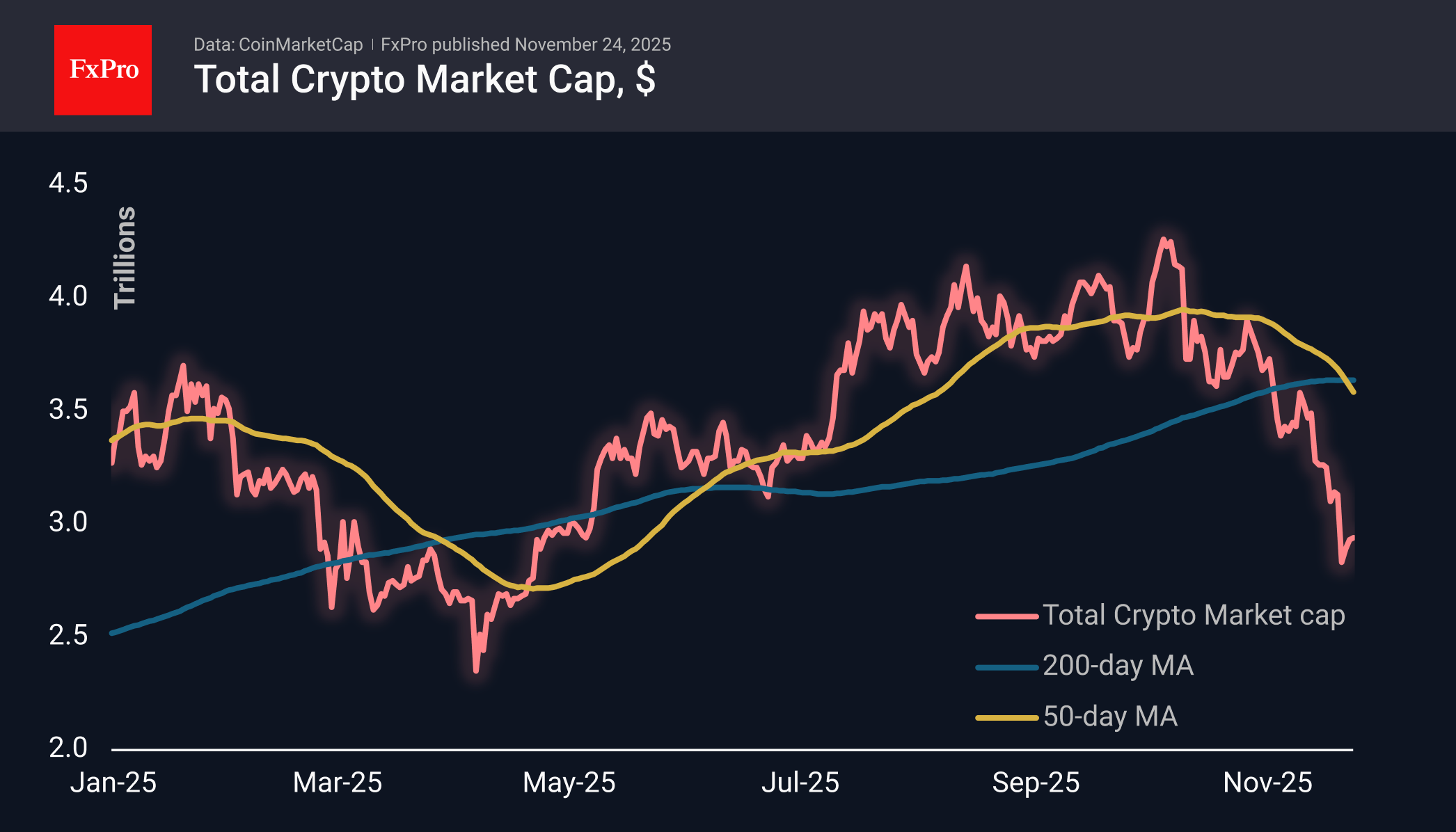

Crypto Market Rebounds After Collapse

Market Overview

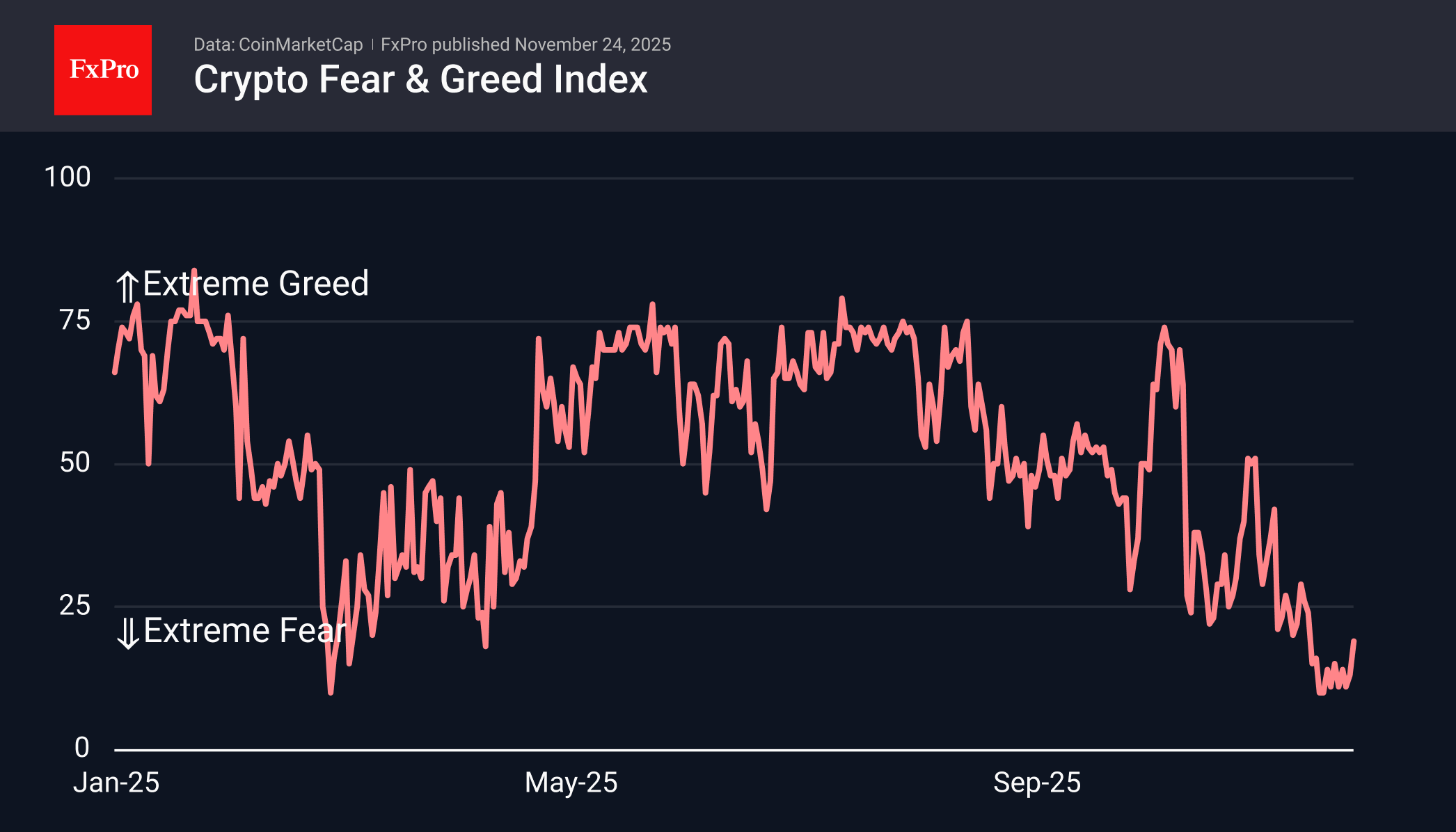

The crypto market appears to have found a foothold last Friday, adding 5% to its lows and recovering to $2.94 trillion. At the same time, the market is now more than 9% lower than it was seven days ago. This is a timid rebound after a devastating collapse. But in this situation, we can see some green shoots for the near future.

The sentiment index rose to 19, remaining in the territory of extreme fear but breaking out of the narrow range where it had been trading for ten days since November 13th. All this looks like a good, but short-term signal to buy in anticipation of a rebound after excessive overselling.

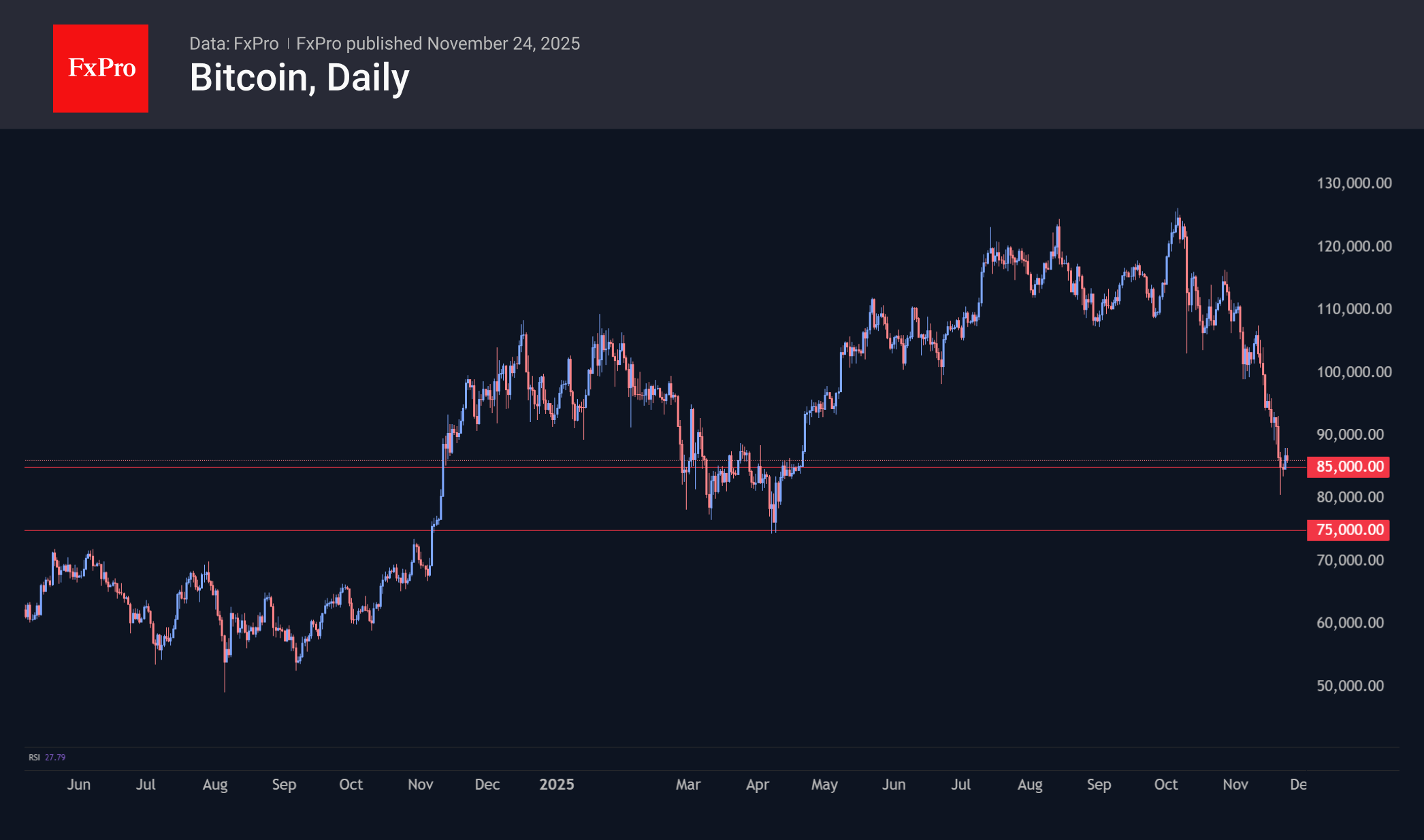

Bitcoin rose to $88K at the start of the day, then corrected to $86K during European trading. The first cryptocurrency slipped to $80.5K on Friday but found buyers to form a rebound, leaning on a recovery in risk appetite in stocks as the chances of a rate cut in December shot to 75% from 28%. BTCUSD received active support in the same $75-85K range in March and April, so it may linger there for some time.

News Background

Outflows from spot Bitcoin ETFs in the US have continued for the fourth consecutive week. According to SoSoValue, net outflows from spot BTC ETFs reached $1.22 billion last week. Total outflows over the five weeks amount to $5.13 billion, bringing the total cumulative inflows since the approval of Bitcoin ETFs in January 2024 to $57.64 billion.

Outflows from spot Ethereum ETFs in the US have continued for the third consecutive week, and for five out of the last six weeks. Net outflows from ETH ETFs totalled $500.3 million, reducing the total inflow since the ETFs’ launch in July 2024 to $12.63 billion. Over the past five weeks, investors have withdrawn $2.28 billion from ETFs.

Inflows into the recently launched Solana spot ETFs in the US have continued for four consecutive weeks. Net inflows rose to $120.2 million last week. Total inflows since the SOL ETF launched on 28 October have increased to $510.3 million (+33.5% over the week).

Inflows into the recently launched spot XRP ETFs in the US have continued for six consecutive trading sessions. During this time, investors have invested $422.7 million in the funds.

The options market is not yet signalling that Bitcoin has bottomed out and is pointing to the risks of a more profound decline, Glassnode notes. The total volume of bets on put options has reached 67.6%.

The volume of realised losses on Bitcoin has reached levels last seen during the collapse of the FTX crypto exchange, Glassnode notes. Experts have called this a sign of capitulation — a cleansing of the market of ‘weak hands’.

The market is entering the final phase of seller exhaustion, according to Swissblock. Bitcoin will remain under pressure unless there is a significant recovery in institutional or retail demand, according to an EgyHash analyst.

Fed’s Waller backs December cut, says January depends on data flood

Fed Governor Christopher Waller signaled clear support for a December rate cut, saying most private-sector and anecdotal data since the last FOMC meeting show little improvement in economic conditions. He noted that the labor market “is soft” and “continuing to weaken,” with inflation expected to ease, creating an environment where another cut next month is appropriate.

Waller said the January meeting presents more uncertainty, as the Fed will receive a “flood of data” that had been delayed by the government shutdown. If those releases align with recent trends—softening labor conditions and moderating inflation—then a case for another cut could be made. "But if it suddenly shows a rebound in inflation or jobs or the economy's taking off, then it might give concern,"" he added.

Beyond policy, Waller confirmed he met recently with Treasury Secretary Scott Bessent to discuss his potential nomination as the next Fed Chair, as the Trump administration moves to select a successor to Jerome Powell. Waller said the meeting went “great,” and argued that the administration is seeking someone with “merit, experience, and knows what they are doing,” adding, “I think I fit that.”

Powell’s term ends in May, leaving a narrow window for the White House to finalize its choice.

Euro’s Fight Back

- The eurozone economy is stable, and Ukraine’s de-escalation is helping EURUSD.

- The Fed may still cut rates in December, and Japan has announced fiscal stimulus measures.

As ECB President Christine Lagarde said, Europe’s vulnerabilities are linked to a growth model focused on a world that is gradually disappearing. The Ukrainian military conflict and trade wars have worked against the euro. However, there are positive developments in both areas, allowing us to look to the future of the regional currency with optimism.

The latest statistics on European business activity indicate the eurozone’s resilience to tariffs, and there are signs of accelerating GDP growth in the final quarter of the year. In 2026, Germany’s fiscal stimulus and EU defence spending are expected to support the economy. The markets see the plan presented by the US and Russia as a step forward towards ending the war in Ukraine, which supports hopes for a recovery in the EURUSD uptrend.

The picture is different in the US. The lack of data makes it hard to be sure about the future. A leading indicator from the Federal Reserve Bank of Atlanta signals an acceleration in GDP from 3.8% to 4.2% in the third quarter. Experts at the Wall Street Journal say it will slow to 3%. However, due to the shutdown, high tariffs, and the White House’s anti-immigration policy, fourth-quarter figures may deteriorate sharply.

Unsurprisingly, New York Fed President John Williams argues that the federal funds rate could be cut in the near future. The futures market reacted by increasing the chances of monetary policy easing in December to 71% from a modest 28% after the publication of the minutes of the October FOMC meeting.

The return of the topic of rate cuts has dealt a blow to the dollar. EURUSD is rushing into battle, and even USDJPY has fallen below key support at 156.7. The principle of ‘buy the rumour, sell the fact’ has come to the aid of the bears. For a long time, the pair rose on expectations of fiscal stimulus from Sanae Takaichi. The stimulus package amounted to ¥17.7 trillion, which was more than the ¥14-15 trillion expected by investment banks. However, this figure was enough for investors to begin taking profits on their short yen positions.

Yen Under Sustained Pressure, Igniting Intervention Fears

The USD/JPY pair is trading firmly around 156.56 on Monday, keeping the Japanese yen in a deeply weak position. Markets remain on high alert as they assess a chorus of verbal interventions from Japanese officials aimed at stemming the decline of the national currency.

The warnings intensified on Sunday when Takuji Aida, an adviser to Prime Minister Sanae Takaichi, stated that Tokyo is prepared to intervene directly in the currency market if the yen's weakness begins to inflict significant harm on the economy.

This follows similar expressions of concern from Bank of Japan Governor Kazuo Ueda and Finance Minister Satsuki Katayama last week. Their comments have significantly heightened expectations of potential market intervention, with many analysts identifying the 160.00 level as a critical line in the sand, recalling that this zone prompted official action during previous episodes of yen weakness.

The yen's sell-off, which drove it to a ten-month low last week, was initially triggered by the new cabinet's substantial stimulus package. The plan raised alarms over Japan's fiscal health, while the administration's continued insistence on ultra-loose monetary policy has provided a fundamental backdrop for further currency depreciation.

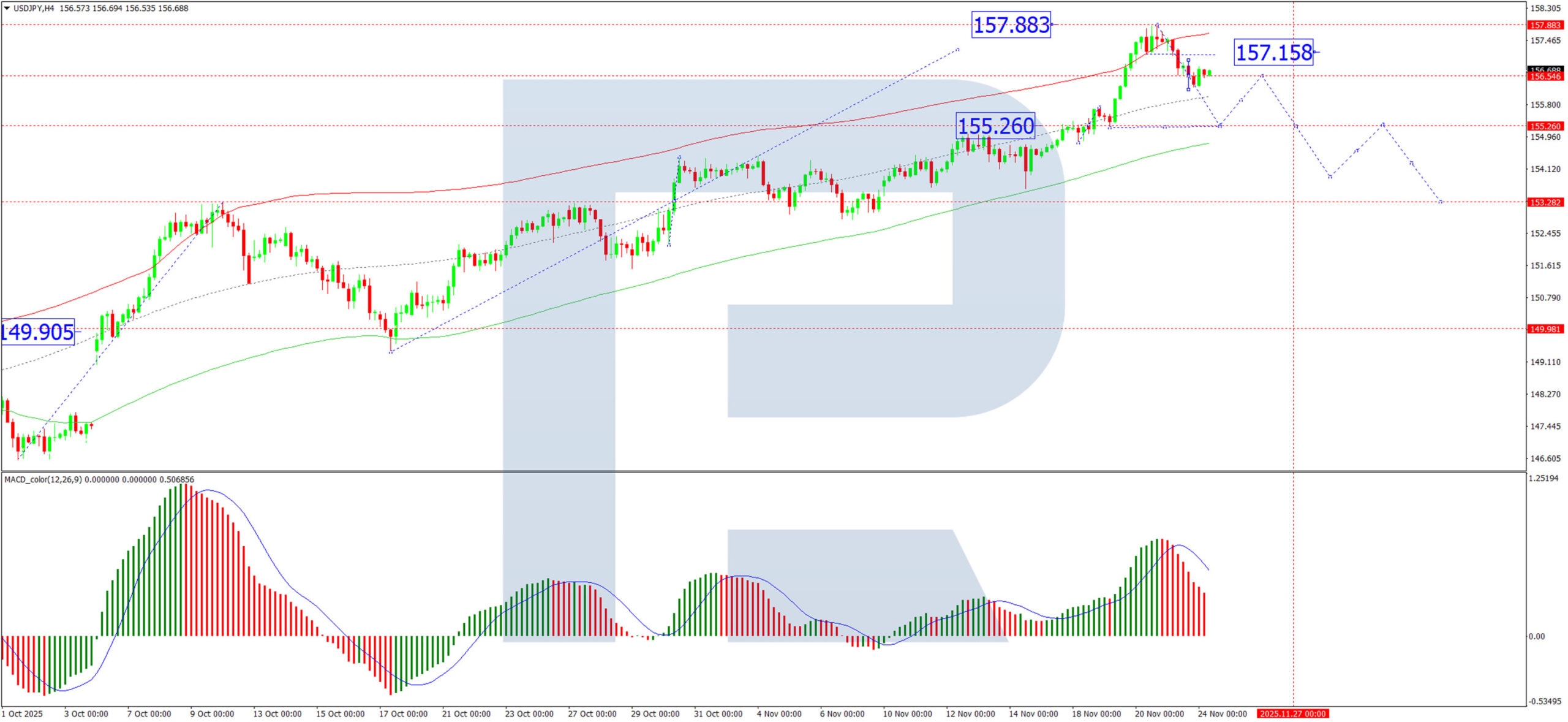

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY completed its first downward impulse to 156.19 and is now forming a consolidation range around 156.55. An upward breakout from this range is expected to trigger a corrective rally towards 157.15. Following this correction, we anticipate the resumption of the bearish move, initiating a new downward impulse with an initial target at 154.00. A break below this level would open the path for a deeper correction towards 153.30. This scenario is technically supported by the MACD indicator. Its signal line is above zero but is pointing decisively downward, suggesting that while the pair is correcting from overbought conditions, the underlying momentum is shifting bearish.

H1 Chart:

On the H1 chart, the pair completed a downward wave to 156.20. We are now observing a corrective phase for this move, with an initial target set at 157.13. Upon completion of this upward correction, we expect the next leg of the downtrend to develop, targeting 154.44. The Stochastic oscillator confirms this near-term view. Its signal line is above 50 and rising towards 80, indicating that short-term buying pressure is driving the correction before the larger bearish trend reasserts itself.

Conclusion

The yen remains caught between fundamental pressures from domestic policy and escalating verbal intervention from authorities. Technically, the USD/JPY pair is completing a corrective bounce within a newly established short-term downtrend. While a rise towards 157.15 is likely in the near term, this should be viewed as a corrective move within a broader bearish structure that targets a decline towards 154.00 and potentially 153.30. All eyes remain on the 160.00 level, widely viewed as the threshold for potential official intervention.

German Ifo falls to 88.1, firms see little prospect of near-term rebound

Germany’s business mood softened in November as the Ifo Business Climate Index edged down to 88.1 from 88.4, missing expectations of 88.5. The decline was driven mainly by weaker expectations, which dropped from 91.6 to 90.6. Assessment of current conditions improved slightly from 85.3 to 85.6.

Sector details remained broadly negative. Manufacturing slipped further from -12.1 to -12.5, reflecting sustained weakness in global demand and the lingering impact of U.S. tariff. Services eased from 2.9 to 2.6, hinting at a moderation in domestic resilience. Trade deteriorated from -20.4 to -21.4 and construction fell from -14.4 to -15.7. Together, these readings signal a still-fragile backdrop with limited catalysts for improvement heading into year-end.

Ifo noted that sentiment among German firms has deteriorated as companies grow more pessimistic about the medium-term outlook. While current conditions improved slightly, businesses “have little faith that a recovery is coming anytime soon.”