Sample Category Title

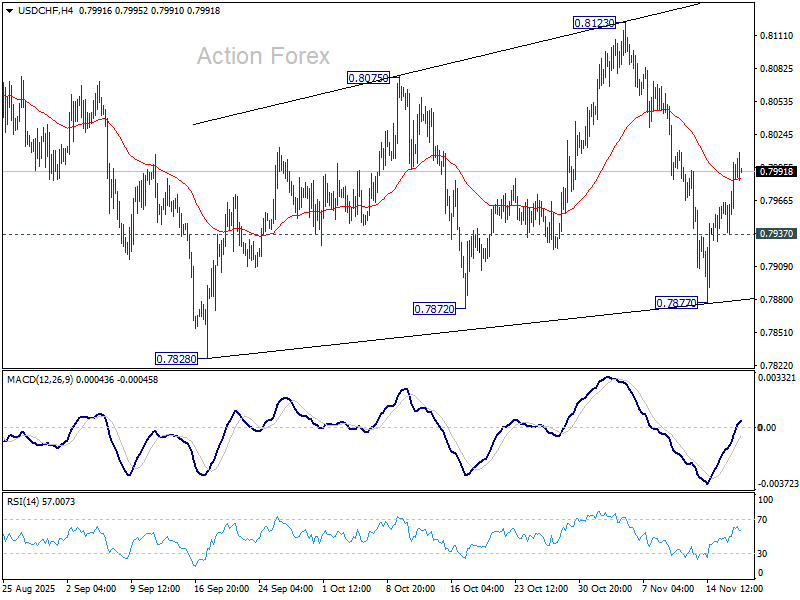

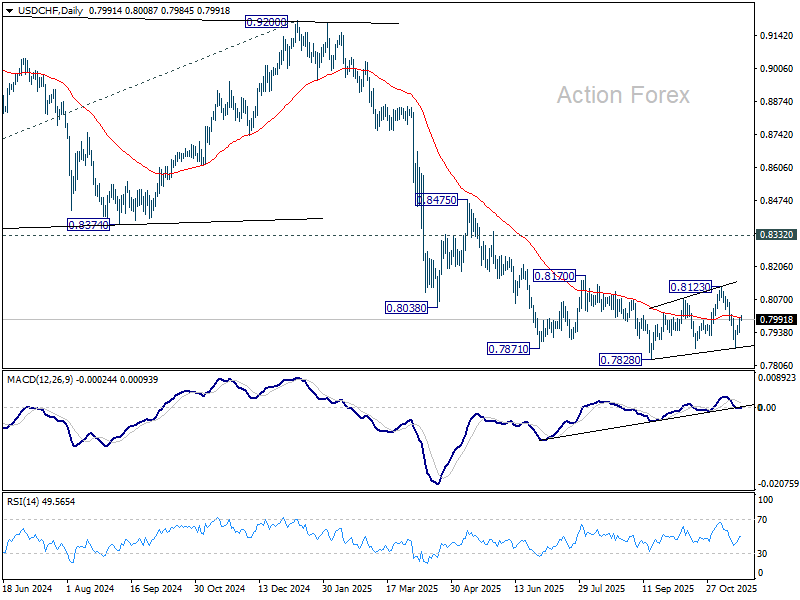

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7956; (P) 0.7979; (R1) 0.8019; More…

USD/CHF's extended rebound and break of 55 4H EMA (now at 0.7986) argues that corrective pattern from 0.7828 low is still extending. Intraday bias is back on the upside for 0.8123 resistance. On the downside, below 0.7937 minor support will turn bias neutral first. Break of 0.7877 will bring retest of 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

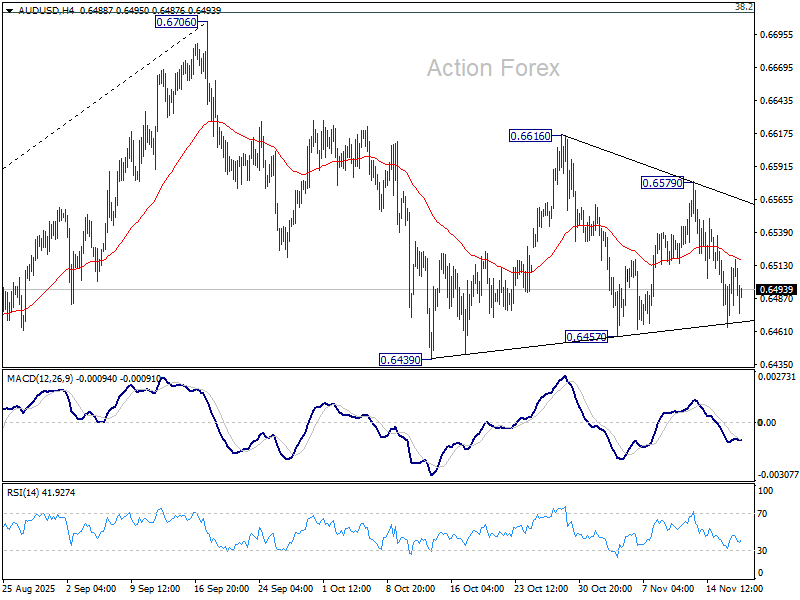

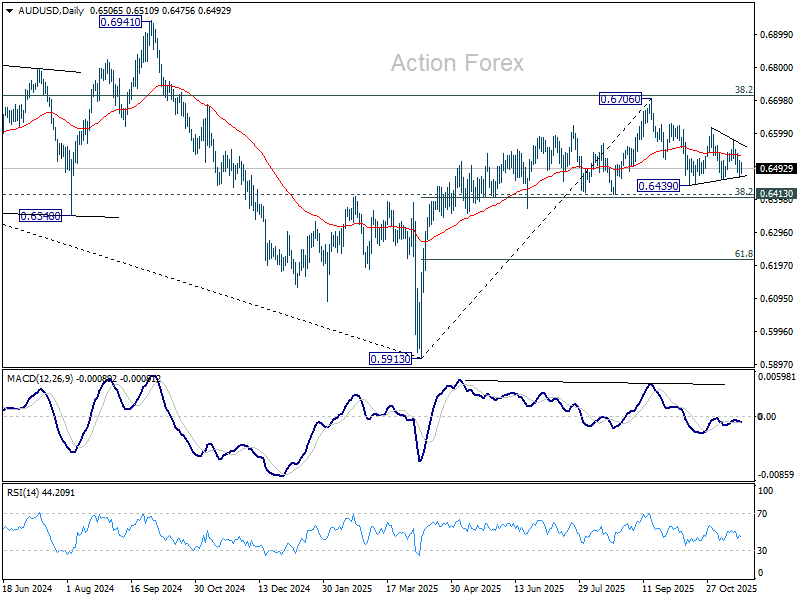

AUD/USD Daily Report

Daily Pivots: (S1) 0.6476; (P) 0.6498; (R1) 0.6530; More...

AUD/USD is still bounded in range of 0.6457/6579 and intraday bias remains neutral. On the downside, break of 0.6457 will target 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403). Decisive break there will carry larger bearish implications. On the upside, break of 0.6579 will bring stronger rise to 0.6616 resistance. Firm break there will target a retest of 0.6706 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

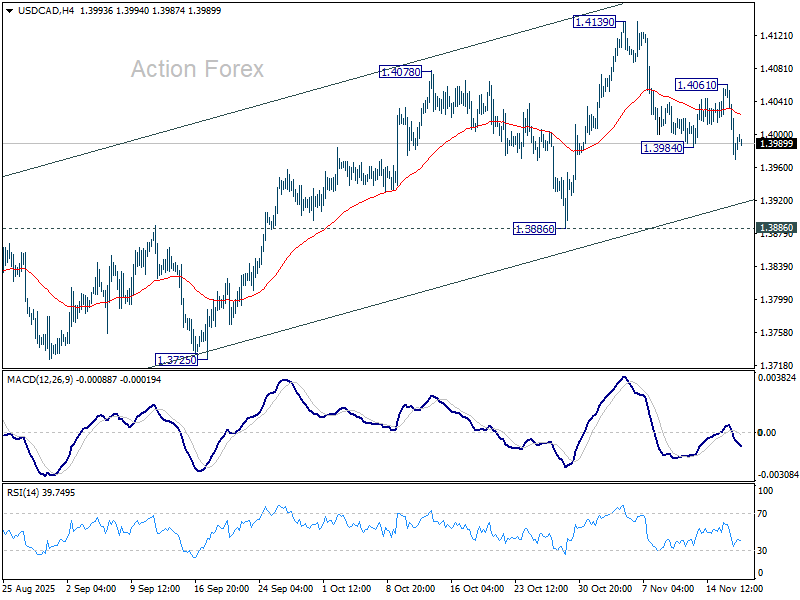

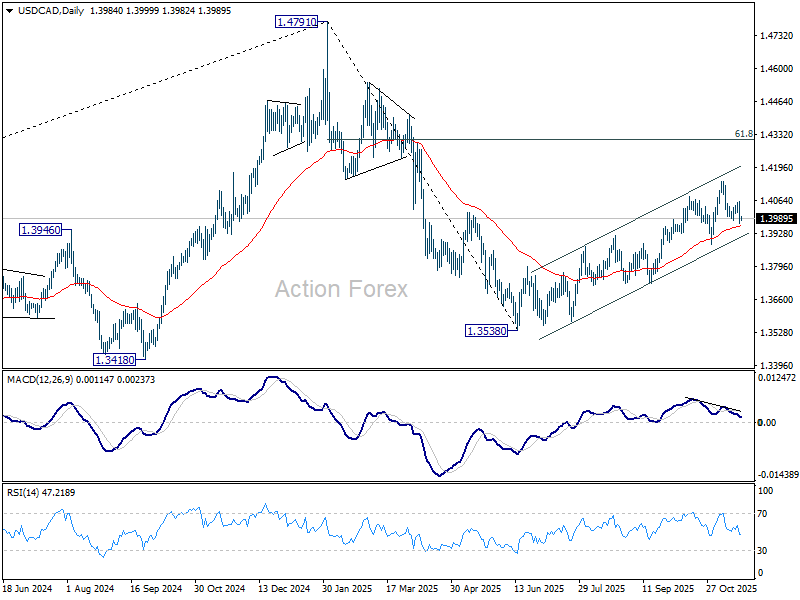

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3954; (P) 1.4008; (R1) 1.4045; More...

USD/CAD's pullback from 1.4139 resumed by breaking through 1.3984 and intraday bias is back on the downside. Deeper fall would be seen towards 1.3886 support. But strong rebound should be seen there to preserve the whole rally from 1.3538. On the upside, above 1.4061 will turn bias to the upside for retesting 1.4139.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

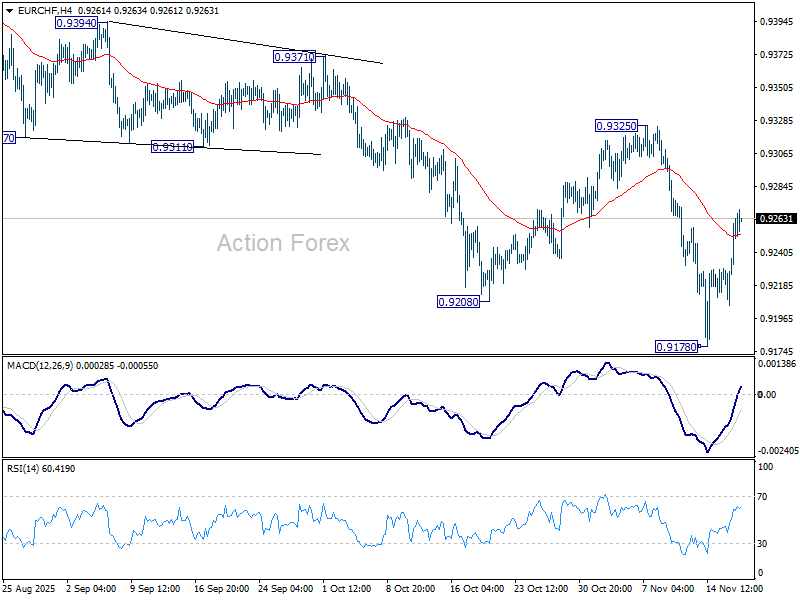

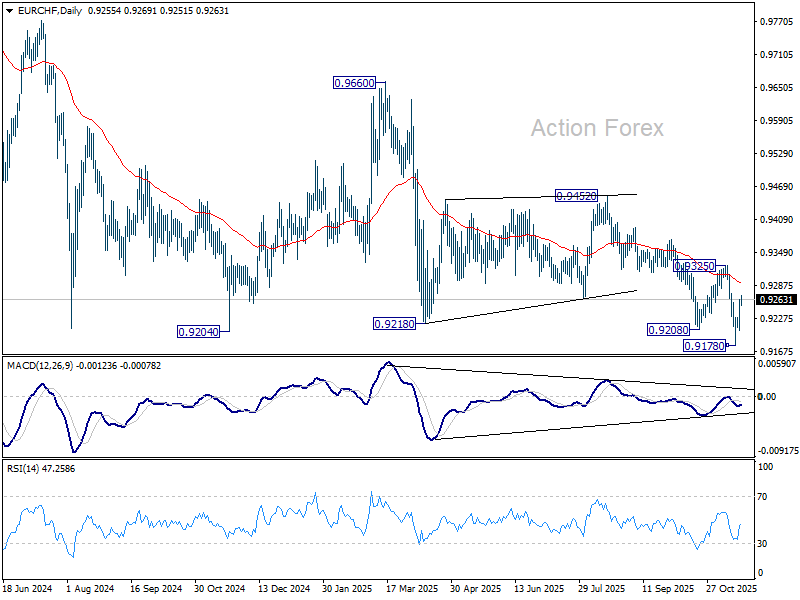

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9222; (P) 0.9244; (R1) 0.9280; More....

EUR/CHF's extended rebound suggests that a short term bottom was already formed at 0.9178, and lengthier consolidations would be seen. Still, outlook will remain bearish as long as 0.9325 resistance holds. Firm break of 0.9178 will resume larger down trend.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9377). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

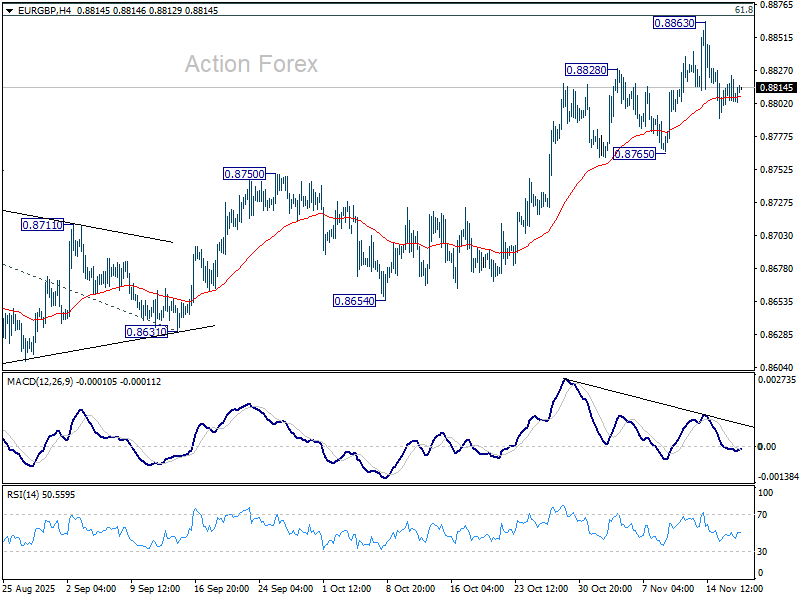

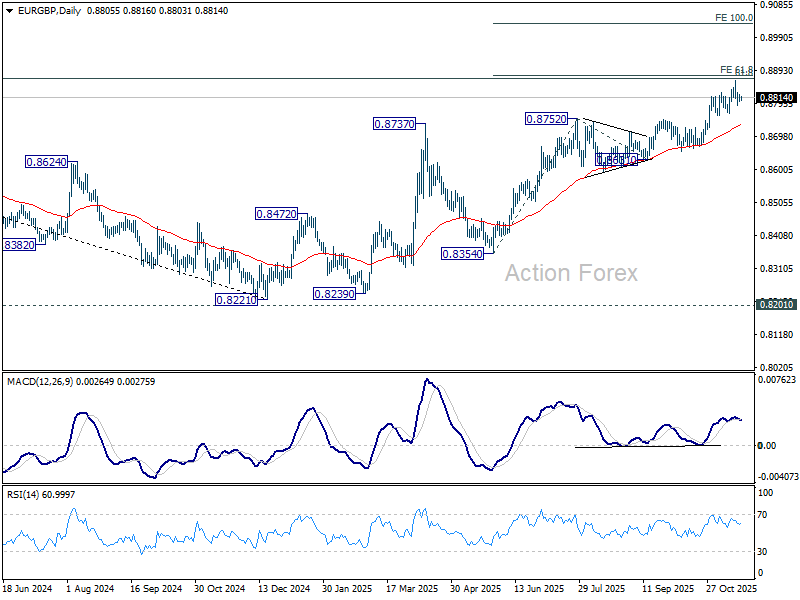

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8800; (P) 0.8812; (R1) 0.8820; More…

Intraday bias in EUR/GBP stays neutral as sideway trading continues. Considering bearish divergence condition in 4H MACD, firm break of 0.8765 support will confirm short term topping. Deeper fall should then be seen back to 55 D EMA (now at 0.8734) even still as a correction. On the upside, however, sustained trading above 0.8867 fibonacci level will carry larger bullish implications. Next near term target will be 100% projection of 0.8354 to 0.8752 from 0.8631 at 0.9029.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8589) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

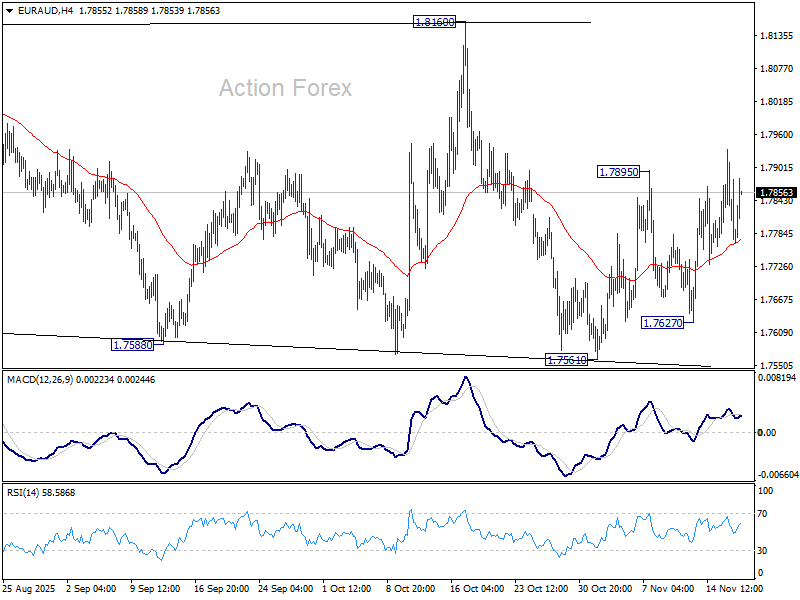

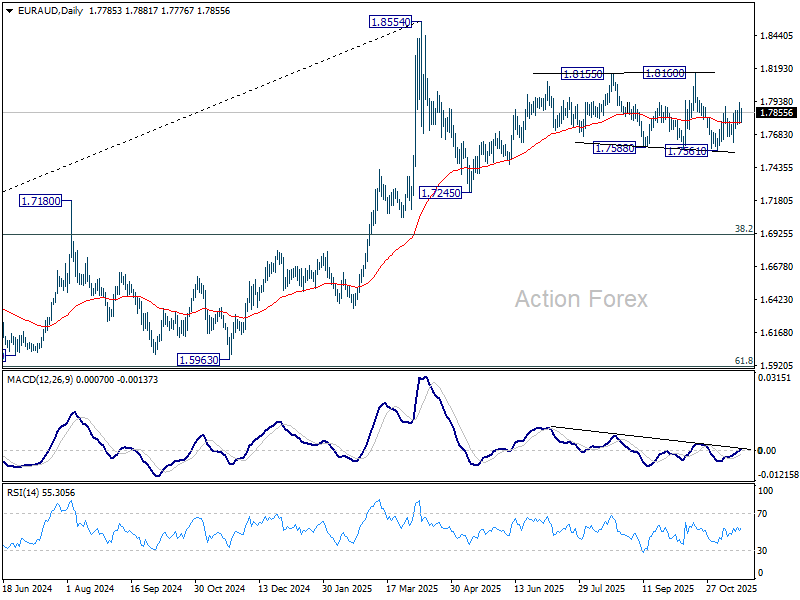

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7729; (P) 1.7833; (R1) 1.7895; More...

Intraday bias in EUR/AUD remains mildly on the upside at this point. Rebound from 1.7561 would target 1.8150 resistance. Firm break there will resume the rally from 1.7245. On the downside, however, break of 1.7627 will turn bias back to the downside for 1.7561 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7426) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound from 55 W EMA will likely bring resumption of the up trend sooner.

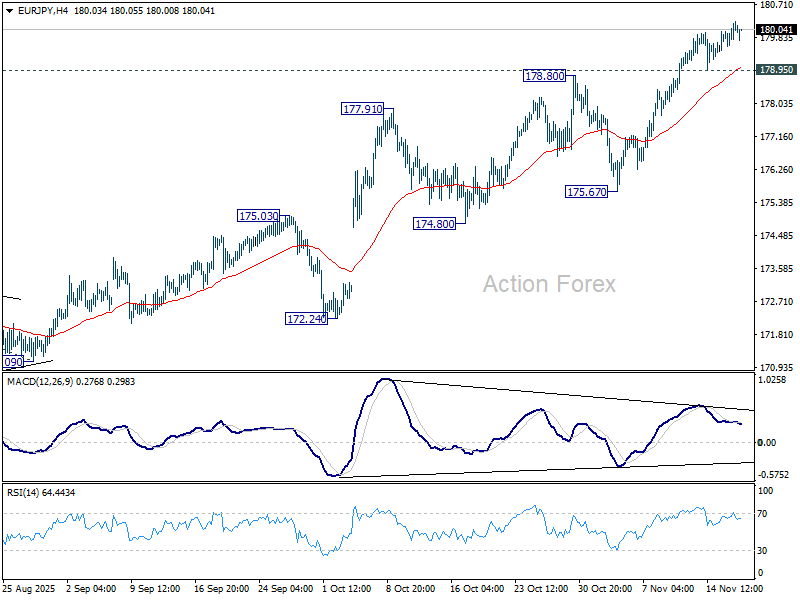

EUR/JPY Daily Outlook

Daily Pivots: (S1) 179.70; (P) 180.00; (R1) 180.38; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Next target is 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, considering bearish divergence condition in 4H MACD, firm break of 178.95 support should confirm short term topping, and turn bias to the downside for 175.67 support.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.00) holds, even in case of deep pullback.

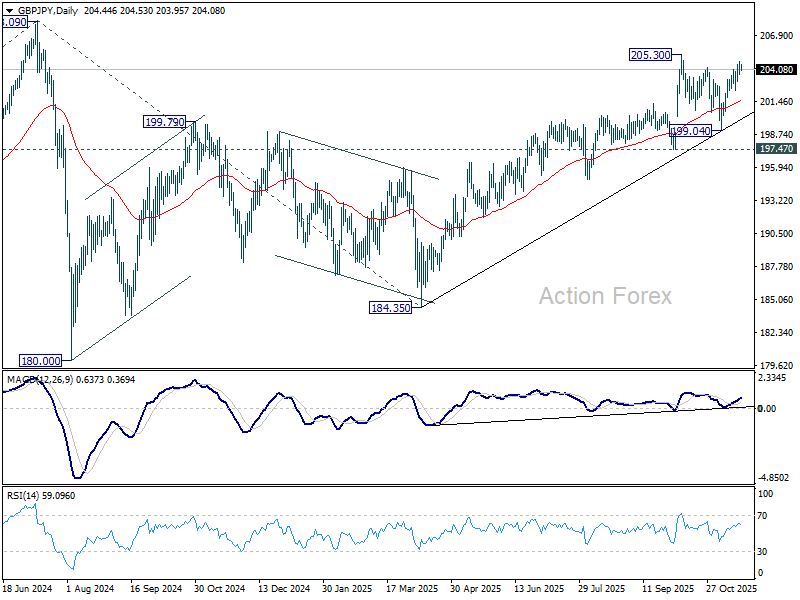

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.87; (P) 204.31; (R1) 204.92; More...

GBP/JPY's rally is still in progress and intraday bias stays on the upside for 205.30 resistance. Firm break there will resume whole rise from 185.43 and target 208.09 high. For now, further rise is expected as long as 102.31 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

Yen Fails to Rally in Risk-Off Trade as BoJ Hike Slips Further Out

Risk-off sentiment continues to drive global markets this week, but the traditional safe-haven Yen is gaining little traction from the turbulence. The currency’s inability to capitalize on the broad defensive tone reflects an overriding theme: expectations that the BoJ’s long-awaited rate hike will be pushed back once again.

Political pressure from the new government has already all but ruled out a move in December. However, the market’s base case of a January hike is now being questioned too. Former BoJ board member Goushi Kataoka, who now serves on Prime Minister Sanae Takaichi’s flagship economic panel, openly urged the central bank to wait even longer.

Kataoka argued it would be “premature” for the BoJ to lift rates to 0.75% in December or January and said the central bank should wait until March or April. He stressed the need for policymakers to assess the impact of the government’s upcoming stimulus package—expected to exceed JPY 20 trillion, according to Kyodo—and to gather more information on next year’s wage negotiations. His comments carry weight given his history as one of the most dovish voices on the BoJ board from 2017 to 2022.

The timing debate will get fresh attention today as BoJ Governor Kazuo Ueda meets with key government ministers, including Finance Minister Satsuki Katayama. Markets are watching closely for any subtle signals on how strongly the administration intends to lean on the central bank to avoid premature tightening.

In Europe, UK CPI data is the main macro highlight for the session. Headline inflation is expected to dip from 3.8% to 3.5% in October, with core slipping from 3.5% to 3.4%. Unless there is a major surprise, the release is unlikely to shift expectations for a December BoE rate cut. The real swing factor remains next week’s Autumn Budget, where uncertainty still hangs over whether the government will resort to tax hikes to plug the fiscal shortfall.

The FOMC minutes from the October meeting will be closely parsed too. Markets will look for clues on how close the Fed came to another rate cut, especially with futures now pricing less than 50% chance of easing in December. Still, the biggest catalyst for expectations may be Thursday’s delayed September non-farm payrolls report, now set to land after weeks of data blackout during the government shutdown.

Overall in the currency markets this week, Kiwi is currently the weakest performer, followed by Aussie and then Swiss Franc. At the top of the table sits Loonie, followed by Dollar and then Sterling, while Euro and Yen are holding the middle ground.

In Asia, at the time of writing, Nikkei is down -0.16%. Hong Kong HSI is down -0.70%. China Shanghai SSE is down -0.17%. Singapore Strait Times is down -0.06%. Japan 10-year JGB yield is up 0.013 at 1.762. Overnight, DOW fell -1.07%. S&P 500 fell -0.83%. NASDAQ fell -1.21%. 10-year yield fell -0.010 to 4.123.

Australia wage price index rises 0.8% qoq in Q3, private sector underperforms

Australia’s wage price index rose 0.8% qoq in Q3, matching expectations and holding the same pace as Q2. The headline stability masks a mild divergence across sectors: private-sector wages increased 0.7% qoq while public-sector wages climbed 0.9% qoq, continuing their recent outperformance.

On an annual basis, wage growth came in at 3.4% yoy, unchanged from Q2. Public-sector pay rose 3.8% yoy, edging up from last year’s 3.7%. Private-sector wage growth slowed to 3.2% yoy from 3.5% in September 2024. This marks the third consecutive quarter in which public wages have grown faster than their private counterparts.

Barkin says Fed flying blind as data blackout ends

Richmond Fed President Thomas Barkin said the U.S. central bank is facing pressure on both sides of its mandate, with inflation still above target and job growth clearly slowing. However, he noted that the picture is not one-directional, as consumers are increasingly resisting price increases while a contraction in labor supply has kept the unemployment rate stable.

Barkin described the Fed’s current environment as akin to “docking a boat at night without a lighthouse,” highlighting the difficulty of judging policy in the absence of timely government data during the shutdown. The upcoming release of delayed reports, he said, will offer much-needed clarity on both inflation and labor market dynamics.

“I think we have a lot to learn between now and then,” Barkin added, suggesting that the December decision remains highly data-dependent as policymakers wait for the first full set of figures since the government reopened.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.87; (P) 204.31; (R1) 204.92; More...

GBP/JPY's rally is still in progress and intraday bias stays on the upside for 205.30 resistance. Firm break there will resume whole rise from 185.43 and target 208.09 high. For now, further rise is expected as long as 102.31 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

GBP/USD Aims Higher Ahead of Key UK CPI Report Release

Key Highlights

- GBP/USD started a recovery wave above 1.3100.

- A major bearish trend line is forming with resistance at 1.3165 on the 4-hour chart.

- EUR/USD is consolidating above the 1.1565 support.

- The UK CPI could increase 3.5% in Oct 2025 (YoY).

GBP/USD Technical Analysis

The British Pound found support at 1.3000 and started a recovery wave against the US Dollar. GBP/USD climbed above 1.3050 and 1.3085.

Looking at the 4-hour chart, the pair settled above 1.3100 and the 23.6% Fib retracement level of the downward move from the 1.3471 swing high to the 1.3009 low. The pair tested the 100 simple moving average (red, 4-hour).

On the upside, the pair faces resistance near the 1.3170 zone. There is also a major bearish trend line forming with resistance at 1.3165. The first key hurdle sits at 1.3200. A close above 1.3200 might send the pair higher toward 1.3240 and the 50% Fib retracement level of the downward move from the 1.3471 swing high to the 1.3009 low.

The next resistance could be 1.3290 and the 200 simple moving average (green, 4-hour). Any more gains could set the pace for a steady increase toward 1.3350.

On the downside, there is a key support at 1.3110. The next support is 1.3080, below which the pair could start a steady decline to 1.3000. A close below 1.3000 could start a pullback toward 1.2850. Any more losses might open the doors for a test of 1.2740.

Looking at EUR/USD, the pair started a recovery wave above 1.1600 and now faces tough resistance near 1.1650.

Upcoming Key Economic Events:

- UK Consumer Price Index for Oct 2025 (YoY) – Forecast +3.5%, versus +3.8% previous.

- UK Core Consumer Price Index for Oct 2025 (YoY) – Forecast +3.4%, versus +3.5% previous.