Sample Category Title

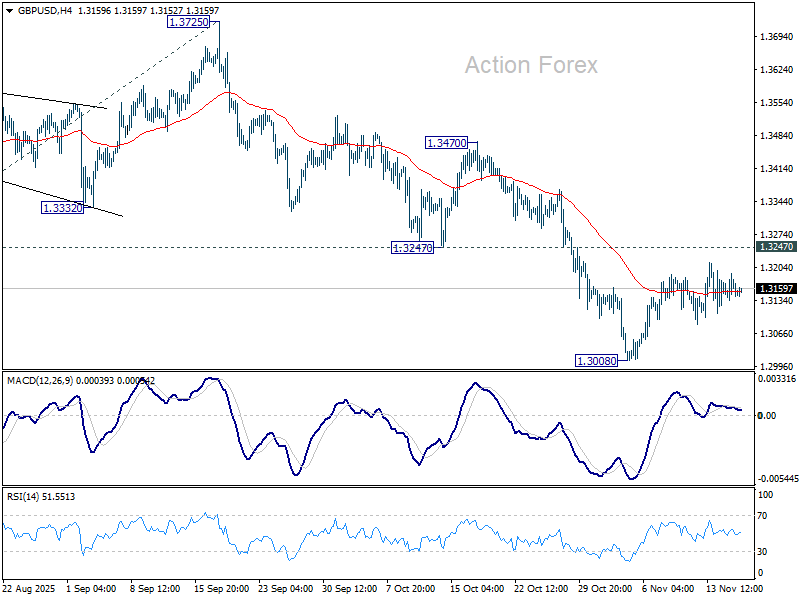

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3130; (P) 1.3161; (R1) 1.3187; More...

No change in GBP/USD's outlook as consolidations continues above 1.3008. Intraday bias stays neutral and further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3182) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

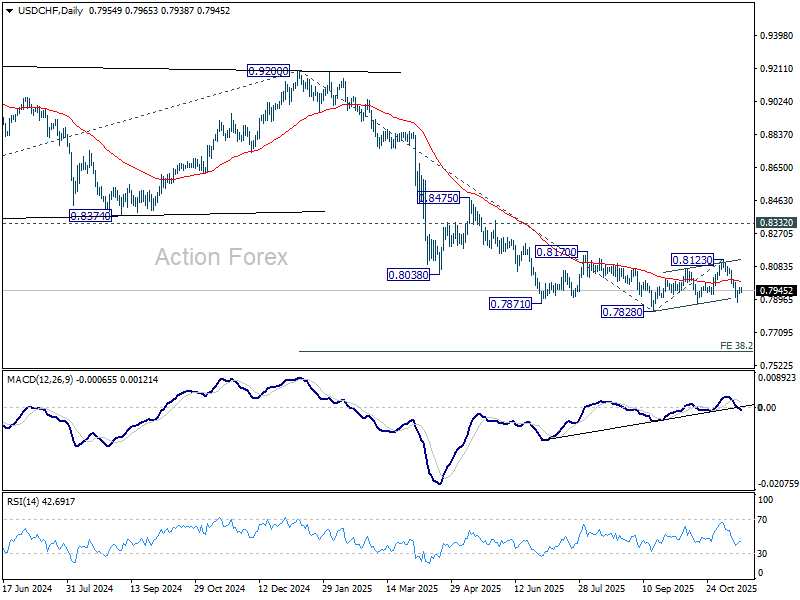

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7953; (R1) 0.7975; More…

No change in USD/CHF's outlook and intraday bias in USD/CHF stays neutral for consolidations above 0.7877. As noted before, corrective rebound from 0.7828 could have completed with three waves up to 0.8123. Break of 0.7872 support will pave the way through 0.7828 to resume the larger down trend. Next near term target is 38.2% projection of 0.9200 to 0.7828 from 0.8123 at 0.7599. However, sustained break of 55 4H EMA (now at 0.7984) will mix up the outlook.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

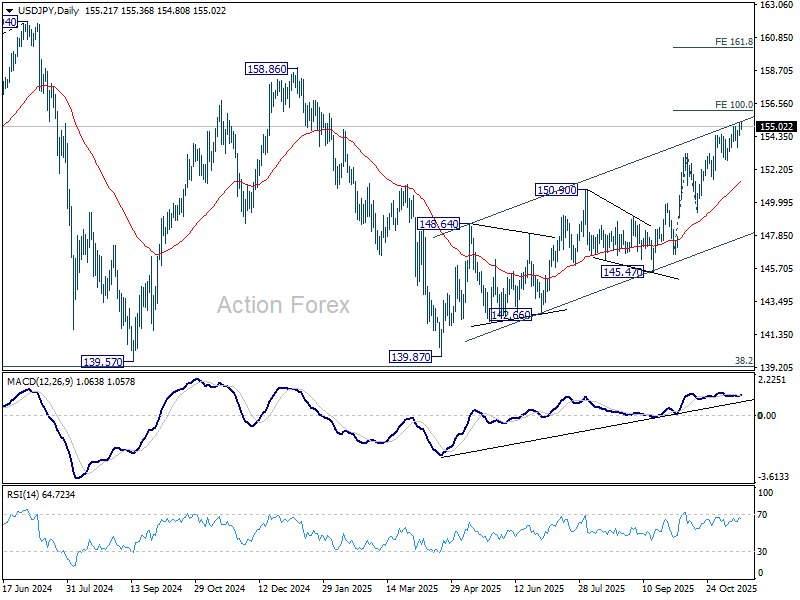

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.43; (P) 154.86; (R1) 155.70; More...

USD/JPY's rise resumed by breaking through 155.03 temporary top and intraday bias is back on the upside. Current rally from 139.87 should now target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 153.60 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.45).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Risk-Off Strikes Again, Yen Awaits Signals from Takaichi–Ueda Meeting

Swiss Franc and Yen led the forex board in Asian session today, buoyed by a fresh wave of risk aversion. U.S. equities closed notably lower overnight, with pressure concentrated once again in AI-linked megacaps. The weakness spilled quickly into Asia, lifting traditional safe havens and putting renewed strain on high-beta currencies.

Nvidia fell around 2% ahead of Wednesday’s third-quarter earnings report, a release that traders are treating as a barometer of whether the AI-driven equity rally still has structural momentum. The company sits at the center of the debate over whether this year’s surge in AI valuations is still fundamentally sound or dangerously dependent on narrow market leadership. With concerns growing about weak breadth and stretched pricing, traders reduced risk heading into a heavy U.S. data week, including September NFP.

Yen also drew some support from Tokyo’s stepped-up verbal intervention efforts. Japan’s Finance Minister Satsuki Katayama intensified her warnings as USD/JPY crossed 155, describing the latest moves as “extremely one-sided and rapid,” and expressing “deep concern.” The comments helped stabilize the currency intraday, though traders remain skeptical about how far verbal guidance alone can go without policy action.

Indeed, expectations surrounding BoJ policy tightening—not ad hoc remarks—remain the primary driver of Yen’s underlying direction. And on that front, markets are looking to a key meeting today: the first direct discussion between Prime Minister Sanae Takaichi and BoJ Governor Kazuo Ueda. Reports suggest Takaichi is preparing a larger-than-expected economic stimulus package and is unlikely to welcome early or aggressive rate hikes.

The messaging after the meeting could meaningfully shape expectations for whether the next BoJ move comes in December, January, or even later. Any signal that the government prefers policy patience could blunt the impact of today’s intervention rhetoric and leave Yen vulnerable unless risk-off sentiment intensifies.

Risk appetite itself is the Yen’s other major swing factor, and today it is clearly leaning toward caution. Asian equities are deep in the red at the time of writing, with Nikkei down -2.90%, HSI down -1.62%, Shanghai SSE down -0.71%, and STI down -0.45%. Overnight U.S. Indexes also closed lower, with DOW -1.18%, S&P 500 -0.92%, NASDAQ -0.84%, and U.S. 10-year yield slipping -0.015 to 4.133.

Across FX markets, Swiss Franc remains the strongest by a wide margin, followed by Yen and then Euro. At the bottom sits Aussie, despite a relatively hawkish set of RBA minutes. Kiwi is the next weakest, followed by Dollar, while Loonie and Sterling sit squarely in the middle of the pack.

RBA minutes show no clear bias toward next move

RBA minutes from the November 3–4 meeting underscored a Board that sees the economy as “broadly in balance” and saw no justification to adjust the cash rate at this stage. While the central projection remains aligned with the RBA’s employment and inflation objectives, policymakers stressed that the next move in rates is not predetermined. Members agreed it was “not yet possible to be confident” about whether holding steady or easing further would become the more likely scenario.

The minutes outlined several conditions that could support keeping policy unchanged. One is a stronger-than-expected recovery in "demand" that lifts employment. Another is if incoming data suggest the economy’s "supply capacity" is weaker than previously assessed — potentially due to persistently high inflation or softer-than-expected productivity growth. A third is a reassessment of whether monetary policy is still "slightly restrictive". Any of these outcomes, the RBA said, would "limit the scope for further easing".

But the Board also detailed circumstances that could justify another rate cut. A material weakening in the labor market remains the clearest trigger. A second downside risk is if GDP growth disappoints — for example, if households turn "more cautious about spending" than currently assumed. In these cases, excess capacity would likely reappear, cooling inflation and warranting additional support.

Overall, the minutes confirm a central bank in wait-and-see mode. The RBA is not ruling out further easing, but neither is it leaning strongly toward it. The next several months of data — particularly on productivity, inflation persistence, and household spending — will be crucial in determining whether the Board holds steady or reopens the easing path in 2026.

Fed’s Waller backs December cut, Jefferson urges slow approach

Fed Governor Christopher Waller struck a notably dovish tone in a speech overnight, arguing that inflation risks have diminished and that weakening labor conditions now deserve greater attention.

Waller said he is “not worried about inflation accelerating”, adding that after months of cooling job data, it is unlikely that this week’s September employment report—or any incoming releases—would alter his view that “another cut is in order.” He warned that restrictive monetary policy is weighing disproportionately on lower- and middle-income consumers, reinforcing the case for easing.

Waller said a December cut would offer “additional insurance” against further deterioration in the labor market and help move policy closer to a neutral setting.

Separately, Vice Chair Philip Jefferson offered a more balanced perspective in his speech, acknowledging that policy has already been guided closer to neutral rate. He added, "The evolving balance of risks underscores the need to proceed slowly as we approach the neutral rate."

Bitcoin eyes temporary support at 92k; broader downside risks stretch to 84k or even 70k

Bitcoin’s downturn has accelerated last week, dragging the cryptocurrency back toward levels last seen at the end of 2024. The retreat is striking: despite surging to a fresh record above 126k earlier this year, the entire advance has now been unwound.

For now, the pace of selloff has slowed, and some signs of stabilization are emerging. Bitcoin is approaching potential technical support near 92k, a level that aligns with measured projection of the current decline. Still, the broader technical picture suggests that this latest leg lower may be part of a correction within a much larger, multi-year uptrend rather than a simple dip to be bought.

History also matters, and a deeper drop could change behavior quickly. Bitcoin has repeatedly seen corrections of more than 50% during major down cycles, and any renewed acceleration lower may reawaken those memories among investors. Panic selling is an unmistakable risk if the decline extends sharply from here, especially given how quickly sentiment has turned since the October peak.

This downturn is not happening in isolation. The slide from the record high has been driven by a confluence of factors: widespread profit-taking by long-term holders, steady institutional outflows, and the forced liquidation of leveraged longs. Adding to the pressure, broader market sentiment has softened as uncertainty over a December Fed rate cut lingers. That policy hesitation has weighed on risk assets broadly, cryptocurrencies included.

Technically, short-term indicators reflect loss of downside momentum. 4H MACD is showing early signs of stabilization, and Bitcoin may find a floor near 100% projection of 126,289 to 101,896 from 116,405 at 92,012. Break of 97,351 minor resistance would signal near-term bottoming and allow for consolidation. However, any rebound is likely to be capped below 10,7493 resistance, keeping the bias tilted toward another decline.

The longer-term chart carries deeper implications. The entire uptrend from 15,452 (2022 low) may have completed as a five-wave rise to 126,289. Bearish divergence in W MACD supports this interpretation, and last week’s break below 55 W EMA (now at 98,483) reinforces the prospect of a broader correction.

From a structural perspective, 38.2% retracement of 15,452 to 126,289 at 83,949 is the minimum medium term downside target for the correction. However, given the combination of momentum loss and macro headwinds, a deeper decline toward 50% level at 70,870 — where a notable support cluster sits — cannot be ruled out.

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.43; (P) 154.86; (R1) 155.70; More...

USD/JPY's rise resumed by breaking through 155.03 temporary top and intraday bias is back on the upside. Current rally from 139.87 should now target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 153.60 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.45).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Bitcoin eyes temporary support at 92k; broader downside risks stretch to 84k or even 70k

Bitcoin’s downturn has accelerated last week, dragging the cryptocurrency back toward levels last seen at the end of 2024. The retreat is striking: despite surging to a fresh record above 126k earlier this year, the entire advance has now been unwound.

For now, the pace of selloff has slowed, and some signs of stabilization are emerging. Bitcoin is approaching potential technical support near 92k, a level that aligns with measured projection of the current decline. Still, the broader technical picture suggests that this latest leg lower may be part of a correction within a much larger, multi-year uptrend rather than a simple dip to be bought.

History also matters, and a deeper drop could change behavior quickly. Bitcoin has repeatedly seen corrections of more than 50% during major down cycles, and any renewed acceleration lower may reawaken those memories among investors. Panic selling is an unmistakable risk if the decline extends sharply from here, especially given how quickly sentiment has turned since the October peak.

This downturn is not happening in isolation. The slide from the record high has been driven by a confluence of factors: widespread profit-taking by long-term holders, steady institutional outflows, and the forced liquidation of leveraged longs. Adding to the pressure, broader market sentiment has softened as uncertainty over a December Fed rate cut lingers. That policy hesitation has weighed on risk assets broadly, cryptocurrencies included.

Technically, short-term indicators reflect loss of downside momentum. 4H MACD is showing early signs of stabilization, and Bitcoin may find a floor near 100% projection of 126,289 to 101,896 from 116,405 at 92,012. Break of 97,351 minor resistance would signal near-term bottoming and allow for consolidation. However, any rebound is likely to be capped below 10,7493 resistance, keeping the bias tilted toward another decline.

The longer-term chart carries deeper implications. The entire uptrend from 15,452 (2022 low) may have completed as a five-wave rise to 126,289. Bearish divergence in W MACD supports this interpretation, and last week’s break below 55 W EMA (now at 98,483) reinforces the prospect of a broader correction.

From a structural perspective, 38.2% retracement of 15,452 to 126,289 at 83,949 is the minimum medium term downside target for the correction. However, given the combination of momentum loss and macro headwinds, a deeper decline toward 50% level at 70,870 — where a notable support cluster sits — cannot be ruled out.

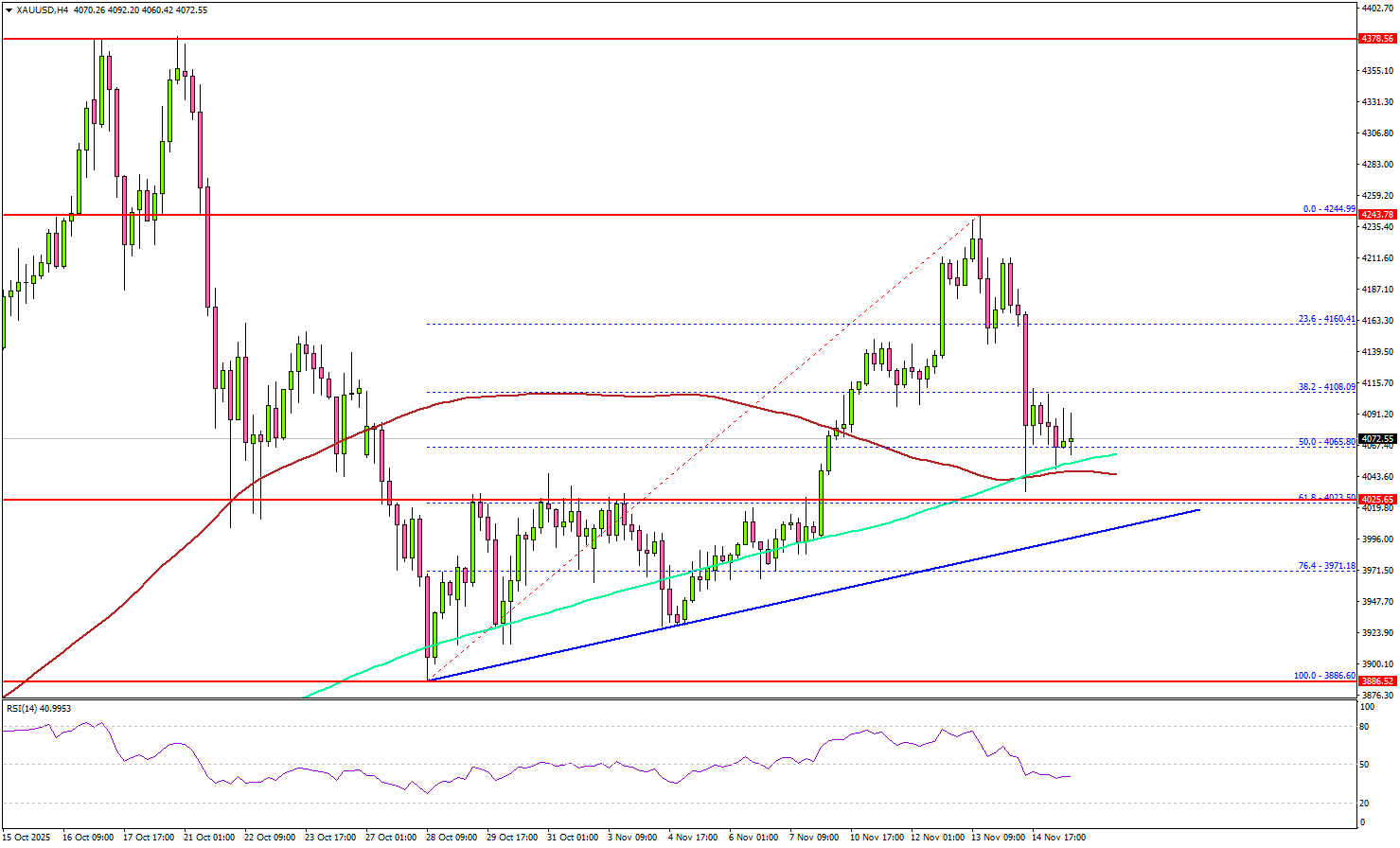

Gold Tests Crucial Support as Traders Watch for Signs of a Bounce

Key Highlights

- Gold started a downside correction from the $4,245 zone.

- A key bullish trend line is forming with support at $4,020 on the 4-hour chart.

- WTI Crude Oil prices could struggle to recover above $61.20.

- Bitcoin extended losses and might dip further below $90,000.

Gold Price Technical Analysis

Gold prices corrected some gains and traded below $4,200 against the US Dollar. It traded below the $4,150 pivot level to enter a consolidation phase.

The 4-hour chart of XAU/USD indicates that the price dipped below the 50% Fib retracement level of the upward move from the $3,886 swing low to the $4,244 high. However, the bulls were active near the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

Besides, there is a key bullish trend line forming with support at $4,020 on the same chart. The next major support is near the $4,000 level. A downside break below $4,000 might call for more downsides. The next key zone to watch could be $3,880.

On the upside, immediate resistance is near the $4,120 level. The next major resistance sits near the $4,150 level. A clear move above $4,150 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $4,185.

Looking at WTI Crude Oil, the price attempted a decent recovery wave, but the bears remained active below the $61.20 level.

Economic Releases to Watch Today

- US Import Price Index for Oct 2025 (MoM) – Forecast +0.1%, versus +0.3% previous.

- US Export Price Index for Oct 2025 (MoM) – Forecast +0.1%, versus +0.3% previous.

RBA minutes show no clear bias toward next move

RBA minutes from the November 3–4 meeting underscored a Board that sees the economy as “broadly in balance” and saw no justification to adjust the cash rate at this stage. While the central projection remains aligned with the RBA’s employment and inflation objectives, policymakers stressed that the next move in rates is not predetermined. Members agreed it was “not yet possible to be confident” about whether holding steady or easing further would become the more likely scenario.

The minutes outlined several conditions that could support keeping policy unchanged. One is a stronger-than-expected recovery in "demand" that lifts employment. Another is if incoming data suggest the economy’s "supply capacity" is weaker than previously assessed — potentially due to persistently high inflation or softer-than-expected productivity growth. A third is a reassessment of whether monetary policy is still "slightly restrictive". Any of these outcomes, the RBA said, would "limit the scope for further easing".

But the Board also detailed circumstances that could justify another rate cut. A material weakening in the labor market remains the clearest trigger. A second downside risk is if GDP growth disappoints — for example, if households turn "more cautious about spending" than currently assumed. In these cases, excess capacity would likely reappear, cooling inflation and warranting additional support.

Overall, the minutes confirm a central bank in wait-and-see mode. The RBA is not ruling out further easing, but neither is it leaning strongly toward it. The next several months of data — particularly on productivity, inflation persistence, and household spending — will be crucial in determining whether the Board holds steady or reopens the easing path in 2026.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 3 and 4 November 2025

Members present

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor and Deputy Chair), Marnie Baker AM, Renée Fry-McKibbin, Ian Harper AO, Carolyn Hewson AO, Iain Ross AO, Alison Watkins AM, Jenny Wilkinson PSM

Others present

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

Brad Jones (Assistant Governor, Financial System), Andrea Brischetto (Head, Financial Stability Department), James Greenwood (Deputy General Counsel) and David Wakeling (Senior Manager, Financial Stability Department) for discussion of the item on exceptional liquidity assistance

Financial conditions

Members commenced their discussion of financial conditions by considering central bank policy settings in advanced economies. The US Federal Reserve (Fed) and the Bank of Canada (BoC) had both cut their official rate by 25 basis points at their October meetings, as expected, while the Reserve Bank of New Zealand (RBNZ) had cut its official rate by 50 basis points. Members noted that inflation remained above target in these economies. The BoC and RBNZ expected inflation to decline to their targets over the period ahead, given significant spare capacity in their economies. The Fed had responded to weaker labour market conditions, while noting that inflation was expected to moderate over time but with risks still tilted to the upside.

In many advanced economies, market expectations were for policy rates to be cut further over the coming year as economic conditions weaken. However, policy rates were expected to be steady in Canada, where policy had already been eased significantly, and in the euro area, where the unemployment rate remained low and inflation was close to target. The Bank of Japan was expected to raise its policy rate further in response to persistent inflationary pressures, despite ongoing weak growth.

Members noted that the Fed had announced in October that it would conclude its balance sheet runoff. This reflected a judgement that reserves were reaching ‘ample’ levels, given signs of pressure in a range of US money market rates.

Sovereign bond yields had fallen noticeably in the United States, Canada and New Zealand over preceding months, as expectations for the future path of policy rates had declined. In the United States, market measures of short-term inflation compensation had also fallen, though longer term measures had remained relatively stable. Long-term government bond yields in Australia were little changed.

In corporate funding markets, risk premia across equity and corporate bond markets remained low as investors continued to price in an outlook of relatively benign macroeconomic outcomes and positive earnings growth in several economies. US financial markets, in particular, were likely being buoyed by expectations of policy easing by the Fed, robust corporate earnings and optimism around the potential impact of artificial intelligence on company profits. Overall, markets appeared to be placing little weight on risks to growth or inflation stemming from the US administration’s policies. Members noted that a reassessment of these or other risks could prompt a sharp tightening in global financial conditions.

In China, the property sector remained a headwind to economic growth and borrowing. Growth in total social financing was still weak, with growth in credit to households particularly low despite the measures taken by authorities to support lending.

Members noted that Australian financial conditions had eased over the course of the year as the cash rate had been reduced. Cuts in the cash rate had been passed through to banks’ funding costs and lending rates. Growth in housing prices and housing credit had picked up. This was most notable for housing credit to investors, which tends to be more responsive to interest rate cuts than housing credit to owner-occupiers. Business debt had continued to grow strongly.

In light of the easing in financial conditions, members considered their assessment of whether financial conditions overall were still restrictive. A range of indicators painted a mixed picture, in contrast to the clear signals apparent in 2024.

The market-implied path for the cash rate was within the range of model-based estimates of the neutral cash rate, though these estimates are imprecise and do not provide any direct guide to monetary policy.

Some other indicators suggested that financial conditions could be on the accommodative side: risk premia in capital markets were low; funding was readily available; and the spread to the cash rate for both bank funding costs and lending rates was notably below pre-pandemic levels. These all implied that a given level of the cash rate was less restrictive than was the case a few years earlier, consistent with some estimates of the neutral interest rate having risen.

However, other indicators were consistent with financial conditions still being a little restrictive. Scheduled mortgage payments remained historically high as a share of household disposable incomes, and households were continuing to make extra mortgage payments into offset and redraw accounts at an above-average rate. The ratio of household debt to household disposable income had continued to fall, when adjusted for offset balances. Business indebtedness had risen, but members noted that this was probably less about funding to increase investment and more about balance sheet and cash flow management (as has historically been the case).

The Australian dollar had appreciated slightly on a trade-weighted basis since early August, but not enough to alter financial conditions materially. The modest appreciation had been associated with a small rise in the interest rate differential between Australia and its major trading partners. The exchange rate remained within the range of staff estimates of its equilibrium level.

Members noted that market expectations for the policy rate in Australia had shifted significantly higher since the August Statement on Monetary Policy. This had occurred progressively over the period, as inflation data for the July to September period came in stronger than expected and more than offset the response to weaker-than-expected labour force data. The market pricing used to condition the November forecasts implied no further cuts in the cash rate in 2025, and one further cut of 25 basis points by late 2026. More than half of market economists projected that there would be no further cuts in the cash rate in 2025 or 2026.

Economic conditions

Members began their discussion of current economic conditions by discussing the stronger-than-expected outcome for inflation in the September quarter. They noted that the outcomes for both headline and underlying inflation were significantly higher than had been forecast in August, though some of this had already become apparent from the monthly indicators ahead of the September meeting. Both headline and trimmed mean inflation stood at or above 3 per cent.

Members observed that part of the increase in underlying inflation was accounted for by volatile expenditure items (such as fuel and travel) or one-off factors (such as council rates) and was therefore expected to be temporary. However, inflation had also been higher than expected across a range of categories for which inflation is typically more persistent. This included categories such as new dwelling costs and market services, both of which tend to reflect domestic cost pressures. Taken together, these observations suggested that there could be a little more underlying inflationary pressure than previously assessed.

Members observed that a range of other price indices had been signalling higher inflation in the first half of 2025 than had been recorded in the Consumer Price Index. This included measures from the national accounts that captured a broader span of economic activity, such as the output price deflator (excluding agriculture and mining, given their limited influence on final prices) and the consumption deflator. Similar developments had also been seen on the costs side: growth in the national accounts measure of average earnings had been significantly higher than growth in the Wage Price Index; and growth in unit labour costs had also remained high.

Members considered whether the apparently stronger growth in costs than in consumer prices could be explained by a compression of some firms’ margins in late 2024 and early 2025, and whether any such compression might have eased somewhat in the September quarter. They noted that such an explanation would be consistent with the emerging recovery in private demand. It would also be consistent with underlying inflation prior to the September quarter having been close to the staff forecasts in November 2024 but with growth in unit labour costs having been stronger than the staff had expected. There was also direct evidence from the housing construction industry of an earlier margin squeeze, and liaison had suggested retailers’ margins were not under quite as much downward pressure as earlier in the year. However, earlier margin compression was not clearly apparent from aggregate data on profits. Overall, members concluded that the conflicting evidence did not allow for a clear assessment of the evolution of margins.

Recent data pointed to a further, and slightly faster-than-expected, easing in labour market conditions. The unemployment rate had increased in September and both the employment-to-population ratio and the participation rate had edged lower over prior months. The unemployment rate for young people, which tends to be more cyclical, had also risen. Members noted signs that it was a little more difficult to find jobs. And the changing composition of growth in activity – with slower growth in public demand and stronger growth in private demand – was likely to have constrained growth in aggregate employment somewhat. However, there were also signs that part of the easing in employment and the participation rate had reflected softer labour supply, as incentives to enter or remain in the labour force had diminished with cost-of-living pressures becoming less acute. Taking a slightly longer perspective, members observed that the employment-to-population ratio had remained high and strikingly stable by both historical and international standards. Timely indicators of labour demand pointed to a broadly stable outlook for the labour market.

Members turned to consider what these data implied for capacity pressures in the economy. They noted that the inflation outcome added weight to the possibility (identified in the August Statement) that there was slightly more capacity pressure in the economy than previously assessed. Members also noted that a range of indicators of capacity in the labour market still pointed to some remaining tightness, notwithstanding the recent easing in the data. These included the low underemployment rate, high level of job vacancies and the above-average share of firms reporting difficulties finding workers. In addition, the layoffs rate had trended down and the ‘quits rate’ (the share of employees voluntarily leaving their job) had increased recently, both of which often signal tighter conditions. Business surveys showed that firms continued to report persistent pressures on capacity utilisation. Members added that the possibility that capacity pressures overall in the economy were slightly more than had been assumed was supported by findings from the annual review of the staff forecasts. That review found that GDP growth had been a little weaker than expected a year earlier but underlying inflation had been very close to expectations, which would be consistent with supply capacity having been less than expected.

Members’ discussion of trends in economic activity began with developments overseas. Global growth had so far proved more resilient than expected despite the ongoing uncertainty about global policy measures and the rise in US tariffs. GDP growth in Australia’s major trading partners (including the United States) had exceeded expectations in the first half of the year, trade patterns appeared to be adjusting quite rapidly and there were signs that various tariff exemptions were reducing the cost for exporters of the announced tariffs. In China, GDP growth had been stronger than expected in the September quarter, as a rise in net exports more than offset weaker domestic demand, including a marked slowdown in investment growth. The authorities had announced new policy measures to support infrastructure investment and lift domestic demand. Iron ore and coking coal prices had increased a little, supported by resilient underlying demand from Chinese steel mills and the announced stimulus.

In Australia, GDP growth had picked up in the June quarter and there was further evidence of the anticipated shift in the composition of growth from public to private demand. Recent indicators pointed to a further modest increase in year-ended growth in the September quarter, to around its potential rate. The pick-up had been underpinned by a resumption in growth in real income as inflation eased and the Stage 3 tax cuts took effect. Members noted that the easing in monetary policy in 2025 was unlikely to have contributed materially to the pick-up in GDP growth at this stage. However, they observed that the impact of the easing in monetary policy would become more material from late 2025.

Outlook

Turning to the latest projections, global growth was still expected to slow a little over the second half of 2025 and into 2026, as higher tariffs weigh on global activity. However, the likelihood of a severe downside scenario had diminished. The staff’s expectation was that policy support from Chinese authorities would largely offset any further slowing in domestic demand growth in China. Inflation in most advanced economies was expected to return to around central bank targets over the coming year or so.

Members noted that GDP growth in Australia was forecast to stabilise around its potential growth rate from late 2025, supported by the easing in monetary policy. This forecast was conditioned on market expectations for around 30 basis points of additional easing in the cash rate over the year ahead, around 30 basis points less than had been assumed in the August forecasts. The expected level of GDP at the end of the forecast period was little changed from the August Statement, with an upgrade to private demand offset by a downward revision to public demand. Members noted that there were risks to the outlook for GDP growth in both directions.

The unemployment rate was forecast to be close to 4½ per cent throughout the forecast period, consistent with GDP growth settling around its potential rate. This forecast took account of the suite of leading indicators of labour demand, which pointed to a broadly stable near-term outlook for labour market conditions. Members noted, however, that there were risks on both sides of this central path. Recent monthly outcomes for employment and the uncertain economic environment created some downside risk to the labour market forecasts. On the other hand, the possibility of stronger-than-expected activity or persistent weakness in productivity posed some upside risk. Members also considered the implications of potential developments in labour supply for future capacity pressures in the labour market.

Members noted that these forecasts imply there is unlikely to be significant further easing in capacity pressures over the forecast period if the cash rate follows the market path.

The forecast for underlying inflation over the year ahead had been revised higher since the August Statement. This followed the strong September quarter inflation outcome and the assessment that there was slightly more capacity pressure than previously assessed. While the staff did not expect quarterly inflation to be as strong in the December quarter as in the September quarter – as some of the recent increase was judged to be due to temporary factors – underlying inflation was now expected to be above 3 per cent until the second half of 2026. Headline inflation was expected to be higher than underlying inflation over this time, as earlier electricity rebates end. Both headline and underlying inflation were then forecast to be slightly above the midpoint of the target range in 2027. Members noted that this forecast was also predicated on 30 basis points of reduction in the cash rate and that an alternative staff projection based on the assumption of no further change in interest rates had inflation settling closer to the midpoint. The staff viewed the risks around the inflation outlook as balanced.

Considerations for monetary policy

Turning to considerations for the monetary policy decision, members identified three judgements that were particularly pertinent: the implications of the recent rise in inflation; the outlook for the labour market; and whether monetary policy was still restrictive.

Regarding inflation, members noted that the increase in the September quarter had been a little larger than expected at the September meeting and materially larger than expected in the August Statement. They agreed that some part of the increase in underlying inflation was likely to be temporary. However, strength in several components pointed to the possibility that some part of the increase might prove persistent. Members acknowledged that this could imply that there was less capacity in the economy than they had previously judged, perhaps masked by a narrowing of margins in late 2024 and early 2025.

In relation to the labour market, members noted the rise in the unemployment rate in September and the associated slowing in employment growth. At the same time, they observed that forward-looking indicators were consistent with employment growing over coming months and that the emerging recovery in economic activity would provide some support to employment growth if sustained. A wide range of indicators suggested that the labour market was still a little tight but there continued to be significant uncertainty about this judgement. Members noted the staff’s forecast for the unemployment rate to be broadly stable over the coming two years.

Members also considered the current extent of monetary policy restriction. They noted that financial conditions had eased because of the 75 basis points of reduction in the cash rate this year, and that there had been a contraction in bank lending spreads and risk premia in financial markets over a longer period. The effects of the monetary policy easing earlier in the year was not yet apparent in the data on economic activity. Members observed that there were some tensions in the signals coming from various other indicators of the tightness of financial conditions. On balance, members judged that financial conditions were still slightly restrictive but that it was also possible this was no longer the case.

Members noted that the Board’s strategy over the prior year had been to ensure its decisions were guided by the incoming data and their implications for the evolving assessment of the outlook and risks, while remaining cautious. The Board had agreed at the September meeting that such a strategy could imply a more gradual easing in policy than had been assumed in the August forecasts if certain conditions were to materialise. Those conditions included growth in aggregate demand proving stronger than had been forecast, members’ assessment of the economy’s supply capacity being lowered or members’ judgement about the extent of monetary policy restriction being reduced. Members noted that the information received since the previous meeting had increased the probability of each of these scenarios materialising, though there was not yet enough information to be certain. They observed that the updated staff forecasts, which incorporated these developments and the assumption of one further reduction in the cash rate target, were for the labour market to remain a little tight and for inflation to be above target for a time before returning to slightly above the midpoint of the target range by 2027.

In light of these considerations, members agreed there was no need to adjust the cash rate target at this meeting. They noted that the central projection was for the economy to remain broadly in balance, and hence consistent with the Board’s objectives, over coming years. There were nevertheless significant uncertainties on both sides of this baseline projection. Given that, members determined that they could afford to be patient while assessing what the incoming data reveal about their judgements on the extent of spare capacity, the outlook for the labour market and the degree of restrictiveness of monetary policy.

Members discussed the developments that could materially influence their decisions at future meetings, noting that these decisions would be driven by how the incoming data alter the outlook for the economy.

They noted several factors that could lead them to hold the cash rate target at its current level. One such factor was if the incoming data signalled that the emerging recovery in demand was stronger than expected, further supporting employment growth. Members noted that such a scenario could emerge in several ways, including if global growth continued to be more resilient than forecast or if the strengthening in household income and wealth, combined with easier monetary policy than a year earlier, resulted in a larger-than-expected recovery in household spending. Another factor was if the incoming data caused the Board to lower its judgement about the supply capacity of the economy. Members observed that this could happen if inflation remained high over coming months or if productivity growth proved to be weaker than expected. A third factor was if the Board changed its assessment that monetary policy was still slightly restrictive. Members noted that any of these scenarios could limit the scope for further monetary easing, particularly with inflation having been above its target for much of the preceding few years.

On the other hand, members pointed to scenarios in which monetary policy may need to be eased further. One scenario was if the labour market were to weaken materially from its current state. Members observed that many indicators of the labour market had softened over the prior year. They noted the risk that employment growth in the market sector remains soft, which could occur if the uncertain economic outlook reduces firms’ willingness to hire or if an emerging focus on cost-cutting results in layoffs. Alternatively, members noted that the recovery in GDP growth could prove to be weaker than expected if households are more cautious about spending than had been assumed. In both scenarios, excess capacity was likely to emerge and dampen inflationary pressures. If so, it would likely be appropriate to ease monetary policy to keep inflation at target and the labour market around full employment.

Members agreed that it was not yet possible to be confident about which of these scenarios was more likely. They affirmed that it was appropriate in this environment for the Board’s decisions to remain cautious and data dependent. In finalising their statement, members committed to continue paying close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board will remain focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

The decision

The Board decided unanimously to leave the cash rate target unchanged at 3.60 per cent.

Exceptional liquidity assistance

As part of a series of discussions at recent meetings on the RBA’s financial stability policies, following the amendments to the Reserve Bank Act 1959, members discussed the RBA’s arrangements for exceptional liquidity assistance (ELA). The capacity to provide ELA to eligible financial institutions that are experiencing acute liquidity difficulties but remain solvent has been a longstanding responsibility of central banks. It reflects that, while each financial institution is responsible for managing its own liquidity, extreme situations can arise when the provision of liquidity to a specific institution by the central bank can be necessary to help preserve financial stability. Given the robust regulatory frameworks for authorised deposit-taking institutions and clearing and settlement facilities in Australia, the provision of ELA is envisaged to be exceptionally rare – as has been the historical experience.

Members agreed that the operational arrangements for ELA would remain as before. However, a key criterion for the Board deciding to provide ELA would be its judgement that doing so was needed to contribute to the stability of the Australian financial system. This aligns the arrangements to the recently updated legislated responsibilities of the RBA and the Monetary Policy Board.

Members agreed that the information on ELA arrangements provided on the RBA’s website would be updated accordingly.

Fed’s Waller backs December cut, Jefferson urges slow approach

Fed Governor Christopher Waller struck a notably dovish tone in a speech overnight, arguing that inflation risks have diminished and that weakening labor conditions now deserve greater attention.

Waller said he is “not worried about inflation accelerating”, adding that after months of cooling job data, it is unlikely that this week’s September employment report—or any incoming releases—would alter his view that “another cut is in order.” He warned that restrictive monetary policy is weighing disproportionately on lower- and middle-income consumers, reinforcing the case for easing.

Waller said a December cut would offer “additional insurance” against further deterioration in the labor market and help move policy closer to a neutral setting.

Separately, Vice Chair Philip Jefferson offered a more balanced perspective in his speech, acknowledging that policy has already been guided closer to neutral rate. He added, "The evolving balance of risks underscores the need to proceed slowly as we approach the neutral rate."

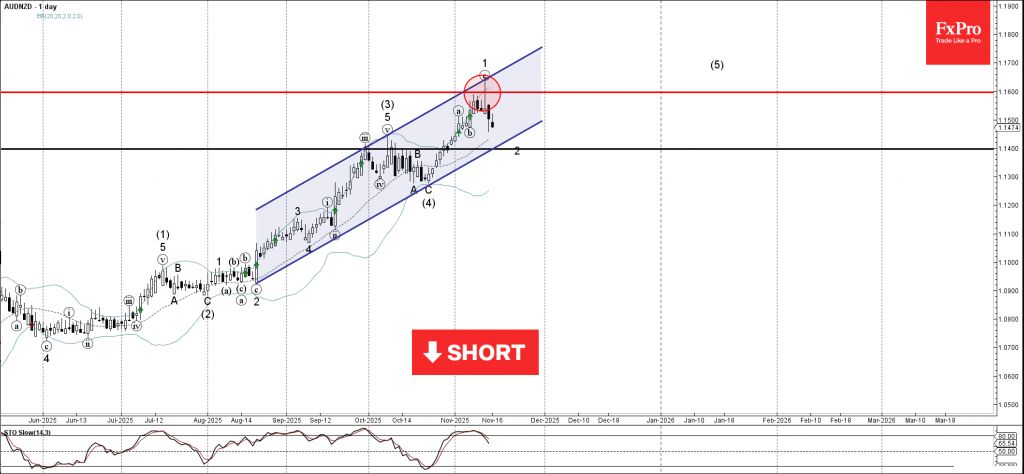

AUDNZD Wave Analysis

AUDNZD: ⬇️ Sell

- AUDNZD reversed from resistance level 1.1600

- Likely to fall to support level 1.1400

AUDNZD currency pair recently reversed down from the key resistance level 1.1600, coinciding with the upper daily Bollinger Band and the resistance trendline of the daily up channel from August.

The downward reversal from the resistance level 1.1600 created the daily Japanese candlesticks reversal pattern Shooting Star.

AUDNZD currency pair can be expected to fall further in the active minor correction 2 to the next support level 1.1400 (target for the completion of the active wave 2).