Sample Category Title

OIL CL_F Drops in Wave ((v)) – Minimum Target Hit!

Hello traders. In this technical article we’re going to look at the Elliott Wave charts of Oil commodity (CL_F) published in members area of the website. OIL has recently given us a 3 waves recovery that found sellers as expected. In this discussion, we’ll break down the Elliott Wave forecast.

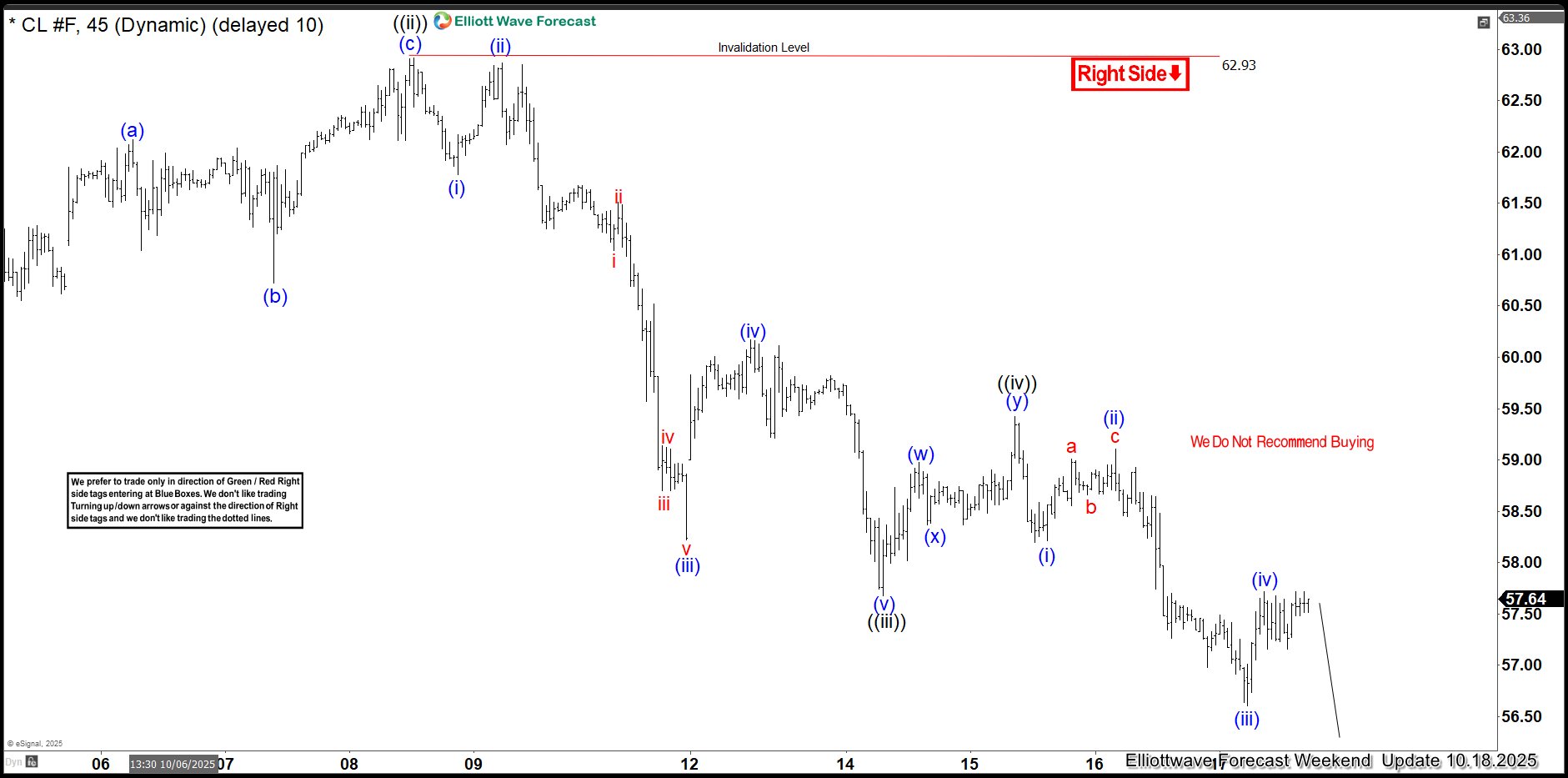

OIL Elliott Wave 1 Hour Chart 10.15.2025

OIL ended a 5-wave decline in the cycle from the 62.93 peak. Currently, the commodity is showing a recovery against that peak: wave ((iv)). We recommend that members avoid buying OIL at this stage and instead favor the short side. As our members know, wave ((iv)) usually ends within the 23.6–38.2% Fibonacci retracement zone, measured from the starting point of wave ((ii)), which in this case is the 62.93 peak. Therefore, we expect OIL to complete its ((iv)) recovery at 58.45–59.21. The price is already within the sellers’ zone, and we anticipate another leg down from this area.

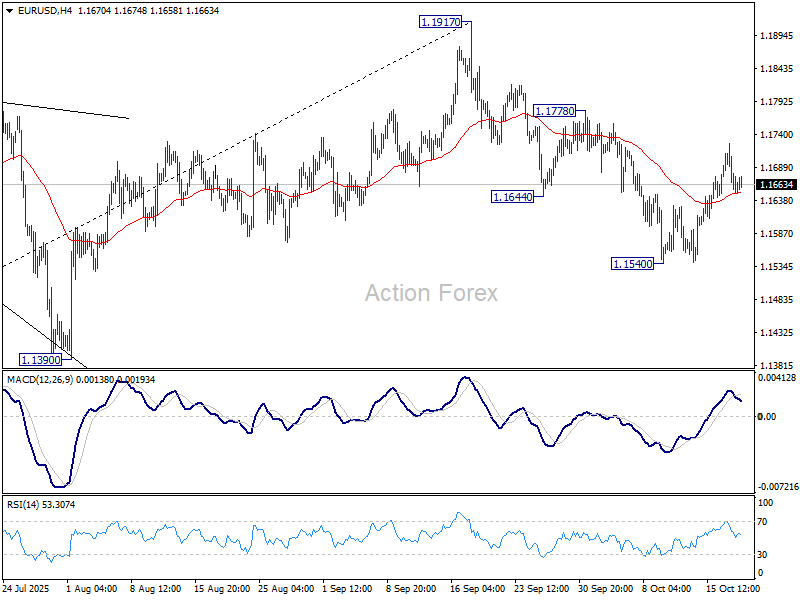

OIL Elliott Wave 1 Hour Chart 10.18.2025

The commodity ended wave ((iv)) within the mentioned zone as expected. We got decline toward new lows as expected. The price is currently in wave ((v)) which has already reached the minimum target at 56.82-56.15. We got this target by measuring inverse 1.236-1.618 fib extension zone of wave ((iv)). However, short term structure in wave ((v)) looks incomplete at this moment. So we believe another low still can be seen before bounce takes place in OIL.

Asian Markets Start the Week on Positive Note with Japan Outperforming

Markets

Ongoing trade tensions between the US and China and a spike in uncertainty related to US regional banks (fraud-linked) undermined risk sentiment last week. Credit tensions in Europa were temporary mitigated as old/new French Prime Minister Lecornu on Thursday survived two no-confidence votes, allowing him to work on a 2026 government budget. Even so, rating agency S&P on Friday stripped the country from its AA status, suggesting that the topic of (French) debt sustainability is here to stay. The multiple sources of uncertainty supported a solid bid for core bonds lately with US yields (temporary?) dropping below key support levels (2y 3.45% area, 10y 4% area) and markets even pondering whether there was a good reason for the Fed to consider a faster path of easing than the two additional 25 bps steps seen this year as the by default scenario. German yields also ceded some important technical levels (2y 1.9% area, 10y 2.6% area) and in a weekly perspective even outperformed Treasuries. On Friday, decent results from some other (regional) US banks and some comforting comments from President Trump on the US-Chine trade war, finally soothed sentiment going into the weekend. US yields rebounded 2 bps (30y) to 4.5 bps (5y), returning above the mentioned support levels. German yields managed to close 1-2 bps higher despite a steep initial decline. US equites finished with modest gains (0.5%). The dollar regained some ground after (bank-related) losses on Thursday. (DXY closed at 98.43 from 98.33). EUR/USD reversed Thursday’s rebound north of 1.17 to close the week at 1.1655.

Asian markets start the week on a positive note with Japan outperforming (Nikkei +2.9%). The LDP party reached a collation agreement with the Japan Innovation party (Ishin), building the case for a growth-supportive policy. Short-term Japanese yields are rising 3-4 bps (2-10-y sector). The yen shows no clear trend (USD/JPY 150.65). The eco calendar is again very thin today. European investors will look out for the fall-out from the S&P downgrade of France. After easing a few bps last week, futures suggest again some further French spread widening this morning. For now, the there is little additional damage for the euro (EUR/USD 1.1665). On interest rate markets, we look out whether last week’s lows might turn into some kind of support with the earnings season and headlines on US-China trade still potential risk factors to unsettle sentiment. For now, the dollar shows no clear momentum with EUR/USD again firmly within the 1.155/1.19 trading range.

News & Views

Rating agency S&P cut France’s rating into single A territory end last week. S&P wasn’t supposed to review France until November 28, making Friday’s decision all the more remarkable. France now enjoys an A+ rating with a stable outlook that balances rising government debt and weak political consensus against the country’s credit strengths. The rating agency said “France is experiencing its most severe political instability since the founding of the Fifth Republic in 1958” and added that even if snap elections would produce a clear majority there’s no guarantee for credible medium-term fiscal consolidation or economic reform implementation. It expects next year’s budget deficit to only marginally narrow from 5.4% to 5.3% and comes with the disclaimer of huge uncertainty ahead of the 2027 presidential elections. French PM Lecornu repeatedly said that bringing it back to below 5% in 2026 is key. S&P projects government debt to climb to 121% by 2028 vs 112% last year. With two (Fitch, S&P) out of the three major rating agencies now having a single A rating, some funds with strict investment criteria may be forced to offload French OATs. OAT futures this morning lose ground. Rating agency Moody’s (Aa3, stable outlook) has a review scheduled this Friday.

Chinese GDP grew by 1.1% q/q in the previous quarter, in line with Q2’s 1% and better than the 0.8% expected. The economy is 4.8% larger in y/y terms and 5.2% bigger YtD. Accompanying monthly data showed retail sales grinding slower from 3.4% y/y to just 3% but industrial activity (export) jumping to 6.5% from 5.2%. Investment dropped by -0.5% y/y YtD, a rare decline mainly caused by the ailing real estate sector. China after the data release said they remain on track to hit the 5% growth target for 2025. While the outcome was in line to slightly below expectations, markets are looking through and draw comfort from signs of easing trade tensions. They are also on the lookout for today’s start of the Fourth Plenum, during which the next 5-year plan is being worked out. China’s yuan stabilizes around USD/CNY 7.12.

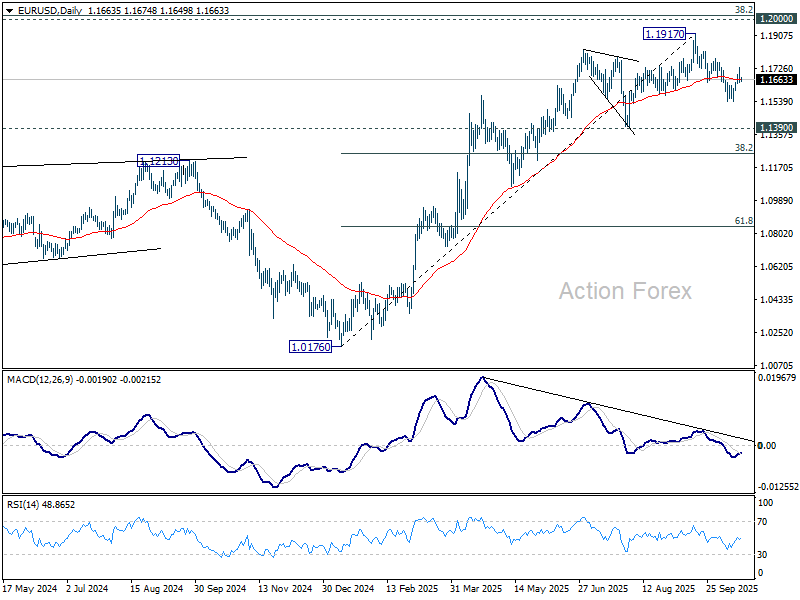

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1627; (P) 1.1677; (R1) 1.1705; More…

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Further decline is in favor as long as 1.1778 resistance holds. Break of 1.1540 will resume the decline from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, through, break of 1.1778 will target retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

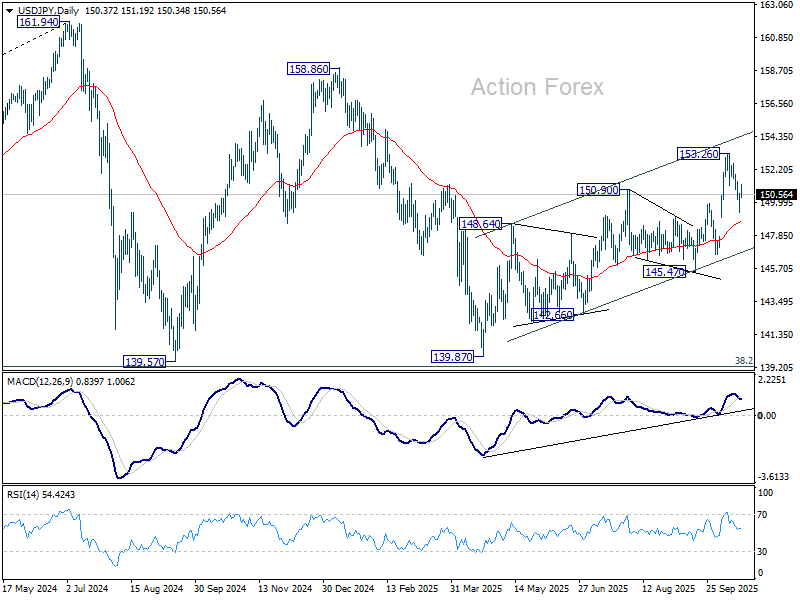

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.79; (P) 150.22; (R1) 151.05; More...

Intraday bias in USD/JPY is turned neutral with current recovery. On the downside, below 149.37 will target 55 D EMA (now at 148.78). Sustained break there will target 145.47 support next. Nevertheless, firm break of 151.38 minor resistance will argue that pullback from 153.26 short term top has completed, and bring retest of this high.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

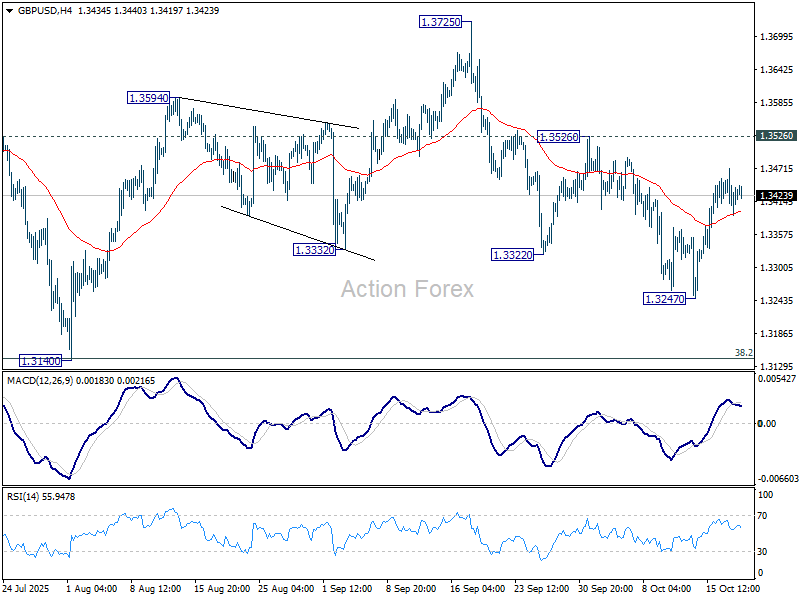

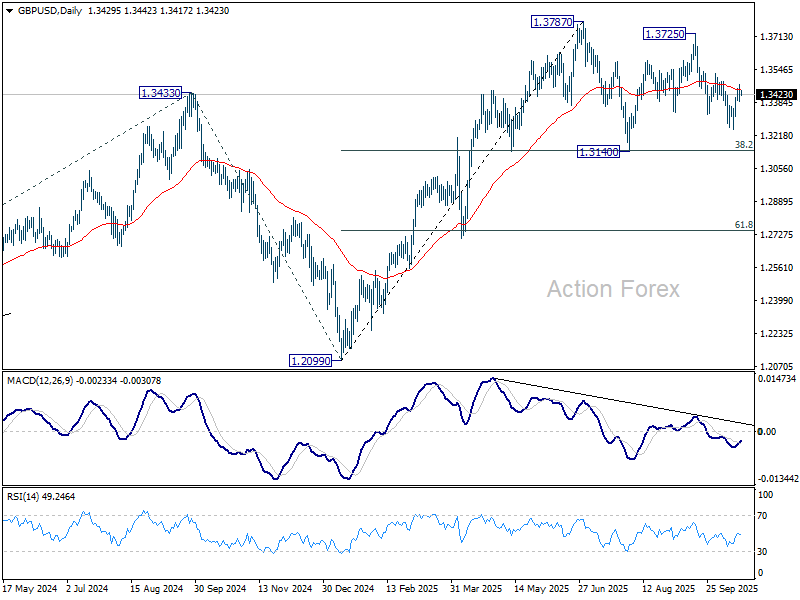

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3388; (P) 1.3430; (R1) 1.3468; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. On the downside, break of 1.3247 will target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3526 will target 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

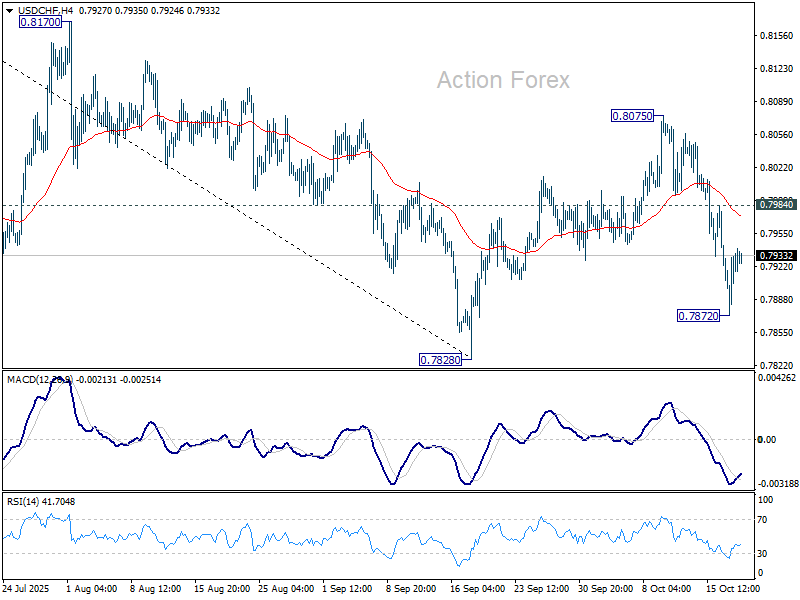

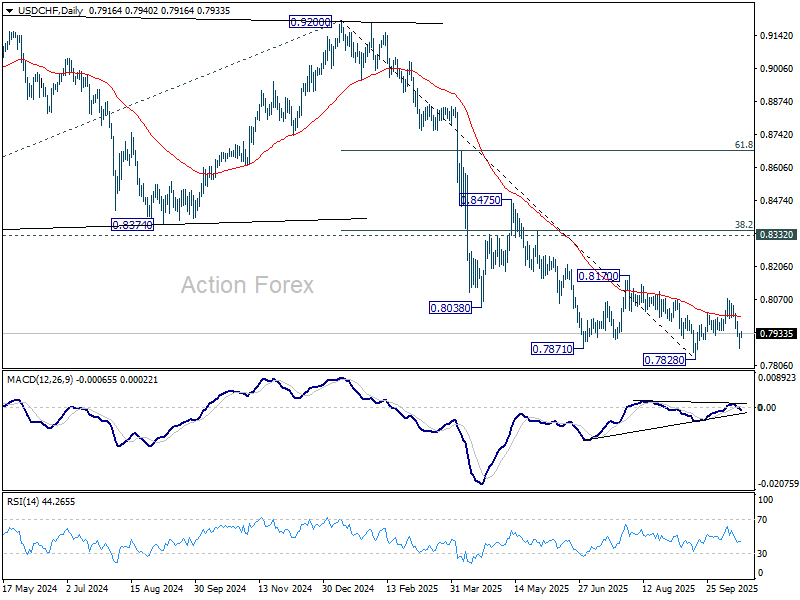

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7893; (P) 0.7916; (R1) 0.7958; More…

Intraday bias in USD/CHF remains neutral for some consolidations. But further decline is expected as long as 0.7984 resistance holds. On the downside, below 0.7872 will bring retest of 0.7828. Firm break there will resume larger down trend. However, break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

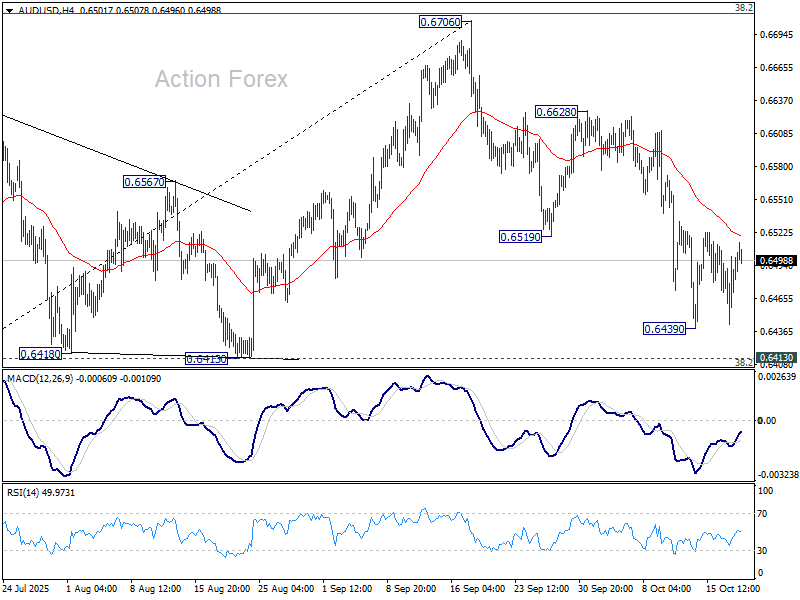

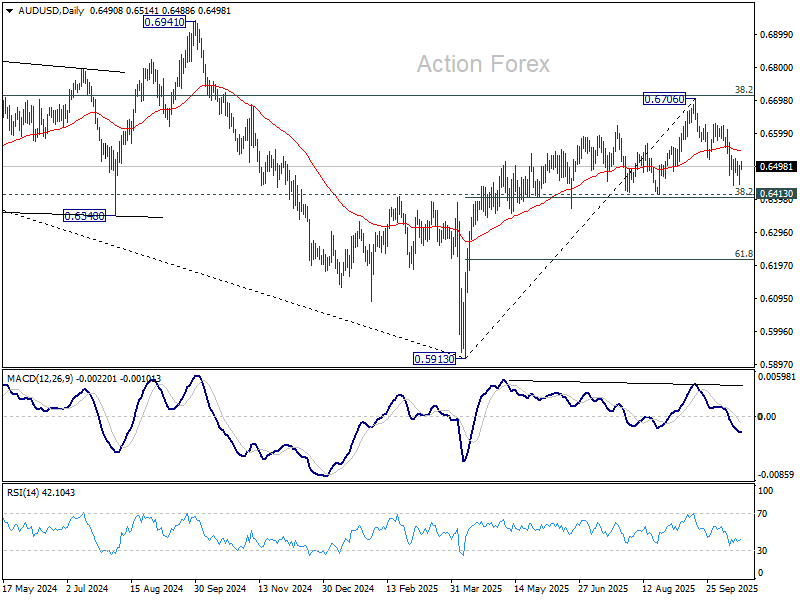

AUD/USD Daily Report

Daily Pivots: (S1) 0.6458; (P) 0.6480; (R1) 0.6516; More...

Intraday bias in AUD/USD stays neutral and more consolidations could be seen above 0.6439. Further decline is in favor as long as 55 D EMA (now at 0.6543) holds. Below 0.6439 will target 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403. Decisive break there will indicate bearish reversal after rejection by 0.6713 fibonacci level. Nevertheless, sustained trading above 55 D EMA will keep the rise from 0.5913 intact, and bring retest of 0.6706 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

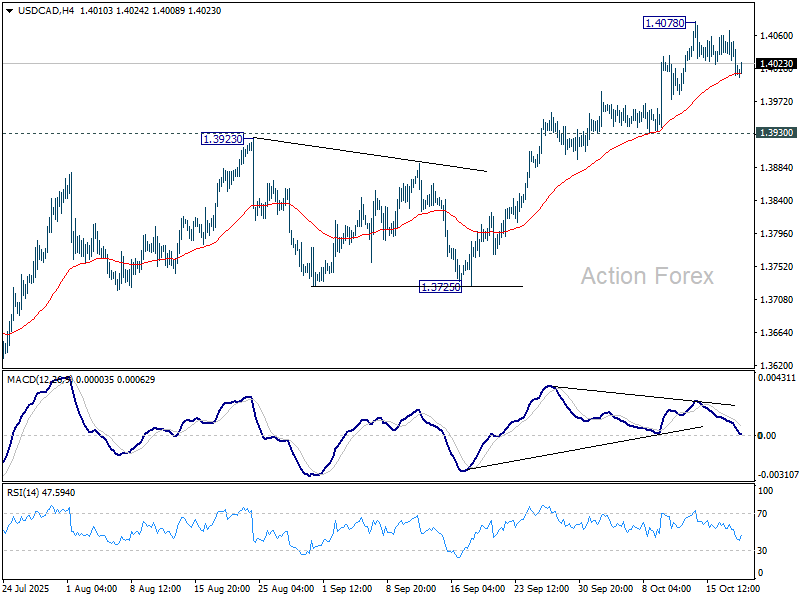

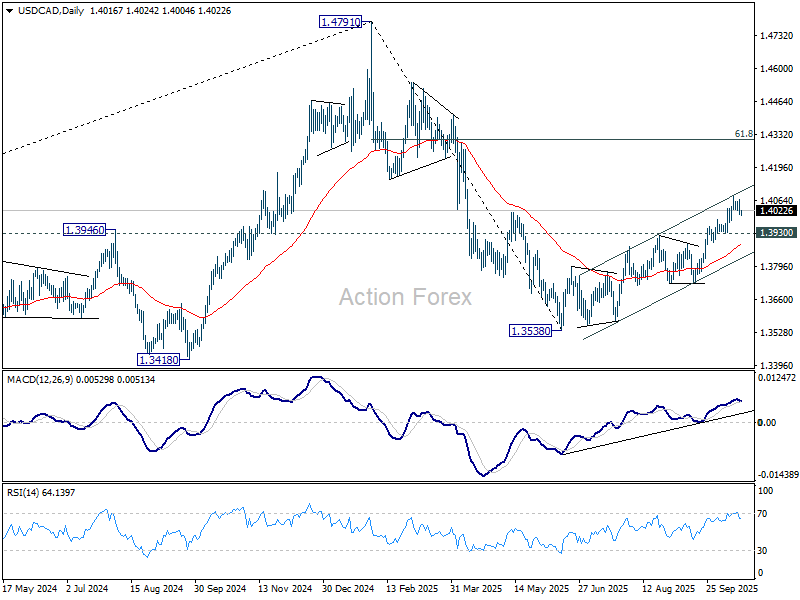

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3998; (P) 1.4033; (R1) 1.4057; More...

Intraday bias in USD/CAD remains neutral and more consolidations could be seen below 1..407. But further rally is expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

Sentiment Improves Before US-China Trade Talks

I was off last week and couldn’t believe the amount of news that landed on the headlines in just a week.

First, trade tensions between the US and China are fully back after China restricted rare earth metal exports to the US and the US threatened China with 100% tariffs — before Scott Bessent said later in the week that there could still be a trade truce for another three months. Bessent will meet Chinese leaders this week — hopefully to ease the latest flare-up.

Meanwhile, China kept its rates unchanged today and printed a set of stronger-than-expected production and GDP figures. Yet, growth expanded at the slowest pace in a year, while retail sales grew at the weakest pace in a year. Chinese equities kicked off the week with a small rebound from Friday on optimism over the upcoming trade talks, while the HSI is up 2.4%, led higher by a solid rebound in tech stocks this Monday, with Alibaba up 5% in Hong Kong at the time of writing.

Elsewhere in tech, TSMC is testing all-time highs in Taiwan after posting — last week — a fresh quarterly profit record and improved outlook on sustained AI demand. ASML in the Netherlands also printed strong earnings, further backing the AI rally and lofty valuations. Then, there was a fresh deal between OpenAI and Oracle, while Applied Materials was hit by new export restrictions toward China — a reminder that trade risks are never too far. But remember that Nvidia expects to make more than $54 bn in revenue last quarter, excluding China. So, Chinese risks — though present — are largely priced in. Plus, the prospects of lower Federal Reserve (Fed) rates continue to support valuations.

Speaking of which, Fed Chair Powell gave a fresh hint last week about an upcoming rate cut by the end of this month — and his words were the only solid indication of what the Fed might do in the absence of economic data as the US government remains shut. The probability of a 25 bp cut by month-end is now seen as nearly 100%. The good news is that the US Bureau of Labor Statistics will release September CPI data on Friday, giving investors something to rely on before the late-October Fed decision. The headline CPI is expected to have rebounded past the 3% mark, while the core CPI figure will likely remain steady above 3% - higher than the Fed’s 2% inflation target. But, because the Fed is now believed to have unofficially shifted its inflation comfort zone closer to 3%, and assuming the US jobs market continues to weaken, that 3% inflation shouldn’t derail expectations for a Fed cut this month, even less so as credit worries are somehow building under the rug.

Big US banks announced strong — even record — quarterly results last week on robust trading revenue and rising deal-making, but rising credit concerns weighed heavier. Zions and Western Alliance, two regional US banks, said they were victims of suspected fraud on loans tied to distressed property funds. The news landed after last month’s implosion of auto lender Tricolor and the bankruptcy of parts supplier First Brands. JPMorgan Chase CEO Jamie Dimon seized the opportunity to add fuel to the fire by comparing these failures to cockroaches, warning that “there are probably more.” But don’t panic just yet: the credit exposures of banks are thought to be sufficiently isolated to avoid sector- or system-wide risk. And three regional banks reported results on Friday — and no new cockroaches, phew. As such, Thursday’s sell-off in bank stocks eased on Friday, keeping the KBW index above its 100-day moving average, and US futures are positive at the time of writing following a strong open in Asia on trade-truce hopes between the US and China this week.

It was however amusing to see that — contrary to popular fear — Big Tech wasn’t behind last week’s volatility; banks and credit worries were! Still, the S&P 500 closed the week 1.7% higher, supported by tech stocks, as the Nasdaq 100 rallied almost 2.5%. In the absence of major data — and hopefully with easing credit fears — attention will remain on earnings: Netflix, Coca-Cola, GM, P&G and Intel are due to report in the US, while STMicroelectronics, UBS, Barclays and Dassault Systèmes will be ones to watch in Europe.

On the political front, the US government remains shut. In Japan, the ruling LDP’s nearly 13-year coalition with Kōmeitō ended last week, but the Ishin party is joining forces with the LDP to pave Takaichi’s way toward the top seat — a development that could keep the USDJPY above the 150 mark.

In Europe, French PM Sébastien Lecornu survived two no-confidence votes by shelving pension reform last week. But that move will necessarily force the French government to find savings elsewhere — all with a deteriorating credit rating, as S&P Global downgraded France to A+ from AA-. The EURUSD will likely remain under pressure.

And in the UK, Rachel Reeves was relieved to see gilt yields fall amid last week’s flight to safety — making her think that, if she improves the narrative around Britain, she might just improve the country’s fortunes. But wait before buying the story — and sterling — ahead of the Autumn Budget announcement.

Focus on PMIs and Inflation

In focus the week

Today is quiet on the data front. The week ahead will focus on inflation, with the UK print on Wednesday likely being a deciding factor for whether a Bank of England rate cut is on the table in November. On Friday, the euro area October flash PMI report will be released, followed by the delayed US September CPI reading and US October flash PMIs.

Economic and market news

What happened overnight

In Japan, newly elected LDP president Sanae Takaichi looks to have found her new coalition government. With the support from the Japan Innovation Party (Ishin), Takaichi should have enough votes to secure another LDP-led government in a parliamentary vote tomorrow. Ishin wants social security reform, lower VAT and a smaller parliament. LDP staying in power means that the largest opposition party, The Constitutional Democratic Party, which has previously advocated for the Bank of Japan to lower its inflation target and hike interest rates faster, will not gain influence. The yen weakened on the outlook of a dovish PM, a move also supported by global risk-on sentiment this morning.

In China, the monthly data release showed Q3 GDP growth slowing to 4.8% y/y from Q2 5.2% y/y in line with consensus expectations. Industrial output growth was the main surprise at 6.5% y/y (cons: 5.0%) from 5.2% in August. The domestic economy remains weak, with house prices down by 2.2% y/y and private consumption continuing to struggle.

What happened over the weekend

In the Middle East, Israel stuck Hamas targets in Gaza in retaliation for an armed attack which killed two Israeli soldiers. Israel has halted incoming aid until Monday, and the truce remains uneasy. Hamas announced its commitment to the ceasefire and stated it was unaware of any attacks in the region where the Israeli soldiers were killed.

In the euro area, the final HICP print confirmed the flash release of 2.2% y/y in September while core inflation was revised up slightly to 2.35% y/y from 2.34% y/y. The uptick in headline inflation in September was mainly due to energy base effects. We expect it to fall back to 2.0% y/y in the final quarter of the year as the energy outlook remains soft, while core inflation is expected to stay at 2.3% y/y.

In Sweden, the September labour force survey was slightly weak. The labour force declined to 5.238M from 5.320M in August, while the unemployment rate fell by 0.1% to 8.7% m/m. Earlier last week, labour market data from SPES offered some encouraging signs. SPES figures for September showed lower unemployment and an improvement in labour demand, while redundancy notices increased only slightly and continued to trend downwards.

Equities: Equities rebounded in the US on Friday to close out a volatile week dominated by earnings and renewed concerns around potential credit losses in the US banking sector. Financials were at the centre of attention, notably, insurance was the weakest performing industry of the week, while banks did better, backed by solid results from the large US banks. Those earnings helped stabilize sentiment and provided some support to the sector overall, even as worries linger around smaller regional lenders. In the US on Friday, Dow +0.5%, S&P 500 +0.5%, Nasdaq +0.5%, Russell 2000 -0.6%. Asian equities are trading notably higher this morning, led by cyclical and export-oriented names after more conciliatory comments from Trump ahead of renewed US-China trade discussions this week. In Japan, markets are rallying close to 3% as an LDP-led government under Takaichi looks increasingly likely, notably, without any material yen reaction so far this morning. Futures are pointing higher in both the US and Europe.

FI and FX: US yields generally edged higher on Friday, despite a downward trend through most of last week, as markets showed signs of relief with risk assets rebounding following recent concerns around regional banks' credit exposure. Despite several sources of uncertainty, markets continue to perform notably well. In the days ahead, attention will turn to another round of US-China trade talks, led by Vice Premier He Lifeng and Treasury Secretary Scott Bessent. On the data front, the continued absence of key government releases due to the shutdown will see one notable exception - Friday's September CPI print. The US repo market came under pressure last week. Most noticeably, the SOFR fixing rose outside the Federal Reserve's target range for the EFFR. EUR/USD fell below 1.17 after trending higher for most of the week amid broad USD weakness. EUR/CHF broke firmly below 0.93 during Friday's session as concerns about US regional banks surfaced. Markets are still digesting the announcement of central bank certificates in Norway. As expected, the primary reaction has been in basis markets and so far, the FRA/Nowa widening has been close to our expectations.