Sample Category Title

Gold Bulls Have No Choice But to Push

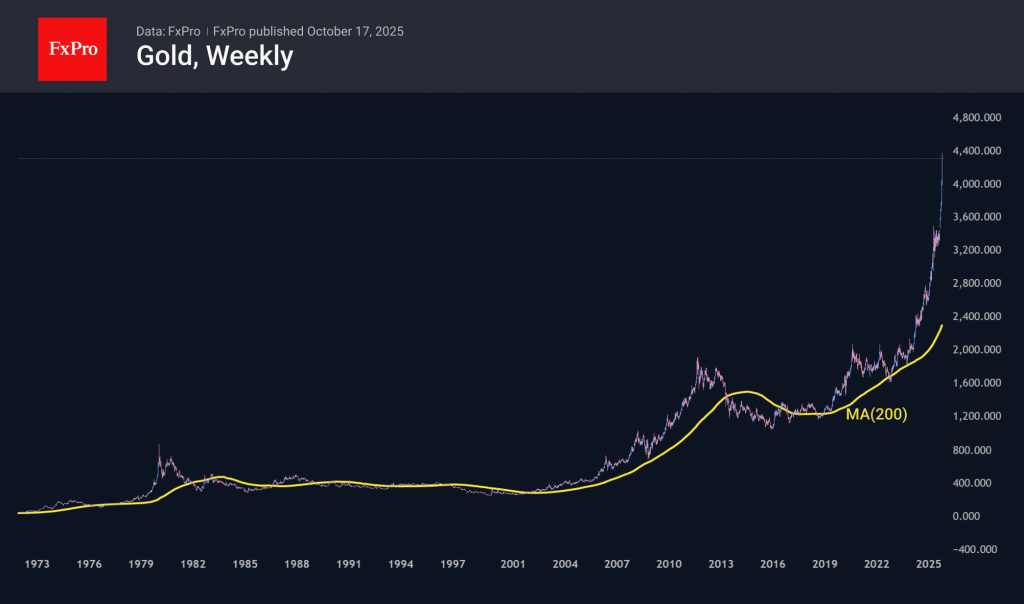

Gold’s rally to record highs above $4,300 per ounce resulted from a debasement trade. Governments cannot cope with budget deficits, are accumulating debt and demanding that central banks cut interest rates, as in the US, or keep them low, as in Japan. As a result, investors are losing confidence in government bonds and currencies. They are looking for alternatives and turning their attention to precious metals.

As a result, gold has been gaining for the last nine weeks, the fifth time in the history of free currency conversion since the 1970s. However, there has never been a 10-week consecutive growth period. The gap from the 200-week moving average also shows the excessiveness of the rally. The spot price at its peak exceeded this line by 90%. There has only been one larger gap once before, in 1980. At the very least, the market needs a technical respite. But historically, its beginning could be the start of a significant multi-year reversal. Now, we are on the side of the bears, but at the same time, we understand that the bulls simply have no choice but to push the price further up, as stopping would ruin the whole game.

Each time, gold finds a new driver of growth. In the summer, there were expectations of a resumption of the Fed’s easing cycle; during September and so far in October, there were political crises in Japan and France, the US shutdown, and the renewed US-China trade war. In November, it will be the turn of the British budget and the court case over Donald Trump’s tariffs. Against this background, Societe Générale’s forecast of precious metal growth to $5,000 per ounce by the end of 2026 seems justified. The company is betting on a consistently high capital inflow into ETFs, a strong appetite for bullion among central banks, and a loosening of the Fed’s monetary policy.

Summary 10/20 – 10/24

Monday, Oct 20, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q3 | 0.80% | 0.50% |

| 21:45 | NZD | CPI Y/Y Q3 | 3.00% | 2.70% |

| 01:00 | CNY | 1-Y Loan Prime Rate | 3.00% | 3.00% |

| 01:00 | CNY | 5-Y Loan Prime Rate | 3.50% | 3.50% |

| 02:00 | CNY | GDP Y/Y Q3 | 4.70% | 5.20% |

| 02:00 | CNY | Industrial Production Y/Y Sep | 5.00% | 5.20% |

| 02:00 | CNY | Retail Sales Y/Y Sep | 2.90% | 3.40% |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Sep | 0.20% | 0.50% |

| 06:00 | EUR | Germany PPI M/M Sep | 0.10% | -0.50% |

| 06:00 | EUR | Germany PPI Y/Y Sep | -2.20% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 22.5B | 27.7B |

| 12:30 | CAD | Industrial Product Price M/M Sep | 0.50% | |

| 12:30 | CAD | Raw Material Price Index Sep | -0.60% | |

| 14:30 | CAD | BoC Business Outlook Survey | ||

| 21:45 | NZD | Trade Balance (NZD) Sep | -1185M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q3 | |

| Forecast: 0.80% | Previous: 0.50% | ||

| 21:45 | NZD | CPI Y/Y Q3 | |

| Forecast: 3.00% | Previous: 2.70% | ||

| 01:00 | CNY | 1-Y Loan Prime Rate | |

| Forecast: 3.00% | Previous: 3.00% | ||

| 01:00 | CNY | 5-Y Loan Prime Rate | |

| Forecast: 3.50% | Previous: 3.50% | ||

| 02:00 | CNY | GDP Y/Y Q3 | |

| Forecast: 4.70% | Previous: 5.20% | ||

| 02:00 | CNY | Industrial Production Y/Y Sep | |

| Forecast: 5.00% | Previous: 5.20% | ||

| 02:00 | CNY | Retail Sales Y/Y Sep | |

| Forecast: 2.90% | Previous: 3.40% | ||

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Sep | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 06:00 | EUR | Germany PPI M/M Sep | |

| Forecast: 0.10% | Previous: -0.50% | ||

| 06:00 | EUR | Germany PPI Y/Y Sep | |

| Forecast: | Previous: -2.20% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | |

| Forecast: 22.5B | Previous: 27.7B | ||

| 12:30 | CAD | Industrial Product Price M/M Sep | |

| Forecast: | Previous: 0.50% | ||

| 12:30 | CAD | Raw Material Price Index Sep | |

| Forecast: | Previous: -0.60% | ||

| 14:30 | CAD | BoC Business Outlook Survey | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Trade Balance (NZD) Sep | |

| Forecast: | Previous: -1185M | ||

Tuesday, Oct 21, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | CHF | Trade Balance (CHF) Sep | 5.22B | 4.01B |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 20.5B | 17.7B |

| 12:30 | CAD | CPI M/M Sep | -0.10% | -0.10% |

| 12:30 | CAD | CPI Y/Y Sep | 1.90% | |

| 12:30 | CAD | CPI Median Y/Y Sep | 3.00% | 3.10% |

| 12:30 | CAD | CPI Trimmed Y/Y Sep | 3.00% | 3.00% |

| 12:30 | CAD | CPI Common Y/Y Sep | 2.60% | 2.50% |

| 23:50 | JPY | Trade Balance (JPY) Sep | -0.09T | -0.15T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | CHF | Trade Balance (CHF) Sep | |

| Forecast: 5.22B | Previous: 4.01B | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | |

| Forecast: 20.5B | Previous: 17.7B | ||

| 12:30 | CAD | CPI M/M Sep | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 12:30 | CAD | CPI Y/Y Sep | |

| Forecast: | Previous: 1.90% | ||

| 12:30 | CAD | CPI Median Y/Y Sep | |

| Forecast: 3.00% | Previous: 3.10% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Sep | |

| Forecast: 3.00% | Previous: 3.00% | ||

| 12:30 | CAD | CPI Common Y/Y Sep | |

| Forecast: 2.60% | Previous: 2.50% | ||

| 23:50 | JPY | Trade Balance (JPY) Sep | |

| Forecast: -0.09T | Previous: -0.15T | ||

Wednesday, Oct 22, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | CPI M/M Sep | 0.30% | |

| 06:00 | GBP | CPI Y/Y Sep | 4.00% | 3.80% |

| 06:00 | GBP | Core CPI Y/Y Sep | 3.70% | 3.60% |

| 06:00 | GBP | RPI M/M Sep | 0.40% | |

| 06:00 | GBP | RPI Y/Y Sep | 4.70% | 4.60% |

| 06:00 | GBP | PPI Input M/M Sep | 0.80% | |

| 06:00 | GBP | PPI Input Y/YS ep | -0.10% | |

| 06:00 | GBP | PPI Output M/M Sep | 0.50% | |

| 06:00 | GBP | PPI Output Y/Y Sep | 0.30% | |

| 06:00 | GBP | PPI Core Output M/M Sep | 0.30% | |

| 06:00 | GBP | PPI Core Output Y/Y Sep | 1.50% | |

| 14:30 | USD | Crude Oil Inventories (Oct 17) | 3.5M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | CPI M/M Sep | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | CPI Y/Y Sep | |

| Forecast: 4.00% | Previous: 3.80% | ||

| 06:00 | GBP | Core CPI Y/Y Sep | |

| Forecast: 3.70% | Previous: 3.60% | ||

| 06:00 | GBP | RPI M/M Sep | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | RPI Y/Y Sep | |

| Forecast: 4.70% | Previous: 4.60% | ||

| 06:00 | GBP | PPI Input M/M Sep | |

| Forecast: | Previous: 0.80% | ||

| 06:00 | GBP | PPI Input Y/YS ep | |

| Forecast: | Previous: -0.10% | ||

| 06:00 | GBP | PPI Output M/M Sep | |

| Forecast: | Previous: 0.50% | ||

| 06:00 | GBP | PPI Output Y/Y Sep | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | PPI Core Output M/M Sep | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | PPI Core Output Y/Y Sep | |

| Forecast: | Previous: 1.50% | ||

| 14:30 | USD | Crude Oil Inventories (Oct 17) | |

| Forecast: | Previous: 3.5M | ||

Thursday, Oct 23, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 12:30 | CAD | Retail Sales M/M Aug | 1.00% | -0.80% |

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | 1.50% | -1.20% |

| 14:00 | USD | Existing Home Sales Sep | 4.06M | 4.00M |

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | -15 | -15 |

| 14:30 | USD | Natural Gas Storage (Oct 17) | 80B | |

| 22:00 | AUD | Manufacturing PMI Oct P | 51.4 | |

| 22:00 | AUD | Services PMI Oct P | 52.4 | |

| 23:01 | GBP | GfK Consumer Confidence Oct | -20 | -19 |

| 23:30 | JPY | National CPI Y/Y Sep | 2.70% | |

| 23:30 | JPY | National CPI Core Y/Y Sep | 2.90% | 2.70% |

| 23:30 | JPY | National CPI Core-Core Y/Y Sep | 3.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 12:30 | CAD | Retail Sales M/M Aug | |

| Forecast: 1.00% | Previous: -0.80% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | |

| Forecast: 1.50% | Previous: -1.20% | ||

| 14:00 | USD | Existing Home Sales Sep | |

| Forecast: 4.06M | Previous: 4.00M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | |

| Forecast: -15 | Previous: -15 | ||

| 14:30 | USD | Natural Gas Storage (Oct 17) | |

| Forecast: | Previous: 80B | ||

| 22:00 | AUD | Manufacturing PMI Oct P | |

| Forecast: | Previous: 51.4 | ||

| 22:00 | AUD | Services PMI Oct P | |

| Forecast: | Previous: 52.4 | ||

| 23:01 | GBP | GfK Consumer Confidence Oct | |

| Forecast: -20 | Previous: -19 | ||

| 23:30 | JPY | National CPI Y/Y Sep | |

| Forecast: | Previous: 2.70% | ||

| 23:30 | JPY | National CPI Core Y/Y Sep | |

| Forecast: 2.90% | Previous: 2.70% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Sep | |

| Forecast: | Previous: 3.30% | ||

Friday, Oct 24, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Oct P | 48.6 | 48.5 |

| 00:30 | JPY | Services PMI Oct P | 53.3 | |

| 06:00 | GBP | Retail Sales M/M Sep | -0.20% | 0.50% |

| 07:15 | EUR | France Manufacturing PMI Oct P | 48.4 | 48.2 |

| 07:15 | EUR | France Services PMI Oct P | 48.9 | 48.5 |

| 07:30 | EUR | Germany Manufacturing PMI Oct P | 49.6 | 49.5 |

| 07:30 | EUR | Germany Services PMI Oct P | 51.1 | 51.5 |

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | 49.9 | 49.8 |

| 08:00 | EUR | Eurozone Services PMI Oct P | 51.4 | 51.3 |

| 08:30 | GBP | Manufacturing PMI Oct P | 46.9 | 46.2 |

| 08:30 | GBP | Services PMI Oct P | 51.4 | 50.8 |

| 12:30 | CAD | New Housing Price Index M/M Sep | 0.20% | -0.30% |

| 12:30 | USD | CPI M/M Sep | 0.40% | 0.40% |

| 12:30 | USD | CPI Y/Y Sep | 3.10% | 2.90% |

| 12:30 | USD | CPI Core M/M Sep | 0.30% | 0.30% |

| 12:30 | USD | CPI Core Y/Y Sep | 3.10% | 3.10% |

| 13:45 | USD | Manufacturing PMI Oct P | 51.9 | 52 |

| 13:45 | USD | Services PMI Oct P | 53.5 | 54.2 |

| 14:00 | USD | UoM Consumer Sentiment Oct F | 55 | 55 |

| 14:00 | USD | UoM 1-Yr Inflation Expectations Oct F | 4.60% | 4.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Oct P | |

| Forecast: 48.6 | Previous: 48.5 | ||

| 00:30 | JPY | Services PMI Oct P | |

| Forecast: | Previous: 53.3 | ||

| 06:00 | GBP | Retail Sales M/M Sep | |

| Forecast: -0.20% | Previous: 0.50% | ||

| 07:15 | EUR | France Manufacturing PMI Oct P | |

| Forecast: 48.4 | Previous: 48.2 | ||

| 07:15 | EUR | France Services PMI Oct P | |

| Forecast: 48.9 | Previous: 48.5 | ||

| 07:30 | EUR | Germany Manufacturing PMI Oct P | |

| Forecast: 49.6 | Previous: 49.5 | ||

| 07:30 | EUR | Germany Services PMI Oct P | |

| Forecast: 51.1 | Previous: 51.5 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | |

| Forecast: 49.9 | Previous: 49.8 | ||

| 08:00 | EUR | Eurozone Services PMI Oct P | |

| Forecast: 51.4 | Previous: 51.3 | ||

| 08:30 | GBP | Manufacturing PMI Oct P | |

| Forecast: 46.9 | Previous: 46.2 | ||

| 08:30 | GBP | Services PMI Oct P | |

| Forecast: 51.4 | Previous: 50.8 | ||

| 12:30 | CAD | New Housing Price Index M/M Sep | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 12:30 | USD | CPI M/M Sep | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 12:30 | USD | CPI Y/Y Sep | |

| Forecast: 3.10% | Previous: 2.90% | ||

| 12:30 | USD | CPI Core M/M Sep | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | CPI Core Y/Y Sep | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 13:45 | USD | Manufacturing PMI Oct P | |

| Forecast: 51.9 | Previous: 52 | ||

| 13:45 | USD | Services PMI Oct P | |

| Forecast: 53.5 | Previous: 54.2 | ||

| 14:00 | USD | UoM Consumer Sentiment Oct F | |

| Forecast: 55 | Previous: 55 | ||

| 14:00 | USD | UoM 1-Yr Inflation Expectations Oct F | |

| Forecast: 4.60% | Previous: 4.60% | ||

Week Ahead – CPI and PMI Data Flood the Agenda, Earnings Also in Focus

- US CPI and PMI data to test dovish Fed cut bets.

- UK inflation figures may impact chances of another BoE cut in 2025.

- Canadian and Japanese CPI numbers are also due out.

- Eurozone flash PMIs could revive ECB rate cut expectations.

Investors maintain dovish Fed cut bets

The dollar began the week on a strong footing, buoyed initially by US President Trump’s weekend remarks aimed at tempering concerns over a potential escalation in US-China trade tensions. However, the greenback quickly relinquished its gains after Fed Chair Jerome Powell struck a dovish tone, reinforcing investors’ expectations of aggressive rate cuts down the road.

The Fed Chief observed that the labor market remained subdued, adding that the assessment was based on private-sector data in light of the ongoing government shutdown and the resulting lack of official releases. While he suggested that sufficient information may still be available to support an informed policy decision at the upcoming meeting, he cautioned that a prolonged shutdown could further obscure the economic outlook.

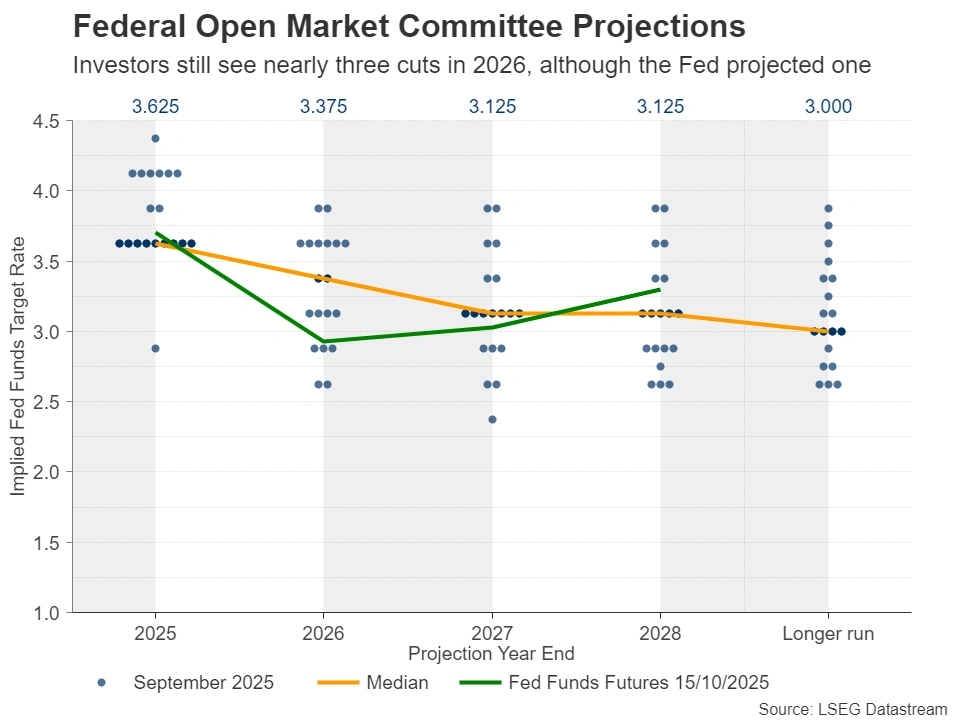

His comments allowed market participants to maintain expectations of two additional quarter-point rate cuts this year, while nearly fully factoring in another three in 2026. This stands in sharp contrast to the Fed’s latest dot plot, which indicated only a single cut next year, and underscores the potential for heightened volatility should forthcoming data tilt sentiment in either direction.

In addition to acknowledging labor market weakness, Powell noted that the economy appears to be “on a somewhat firmer trajectory than expected”, implying that they may not proceed as forcefully as markets anticipate, particularly if data continues to indicate economic resilience and the government reopens.

US CPI and PMI data enter the spotlight

With this context in mind, dollar traders may turn their attention to next Friday’s US CPI data for September – set to be released on Friday even if the government shutdown persists – alongside the S&P Global PMIs for October.

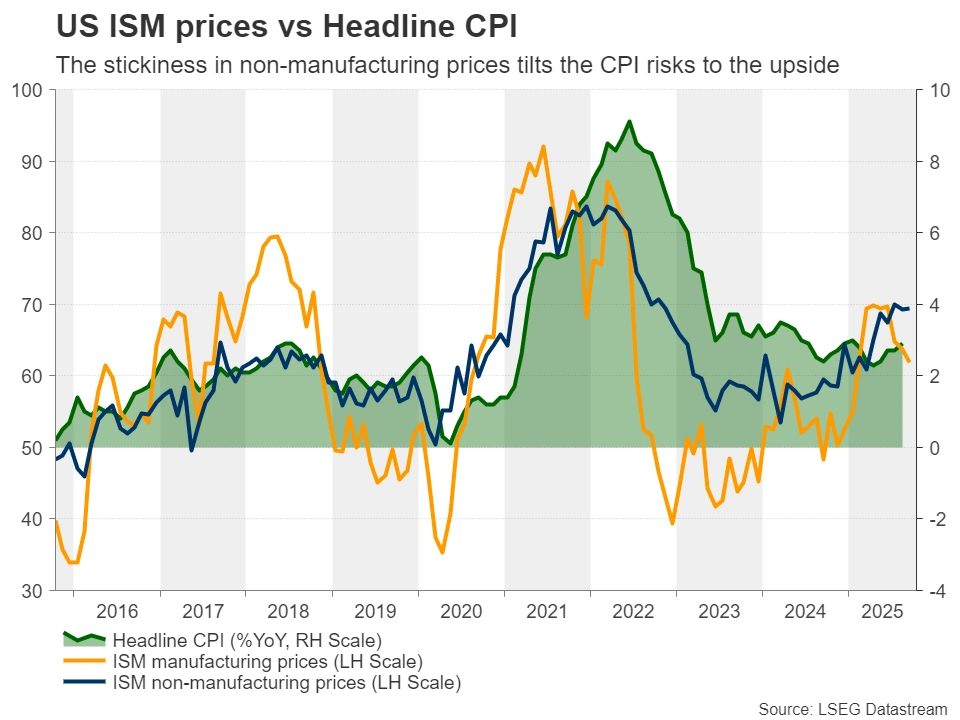

According to the ISM PMI reports for September, prices charged in the manufacturing sector continued to decelerate, but the corresponding non-manufacturing subindex saw a modest uptick. Given that non-manufacturing activity represents roughly 90% of US GDP, Friday’s inflation data may exhibit some persistence. Indeed, the Cleveland Fed CPI Nowcast model pointed to a 3% y/y inflation rate, slightly above August’s 2.9%.

Therefore, sticky inflation, coupled with PMIs supporting Powell’s view that the economy continues to fare well, may lead investors to temper their aggressive rate cut bets and scale back anticipated reductions for next year. This could prove positive for the US dollar. The opposite may be true in case inflation decelerates.

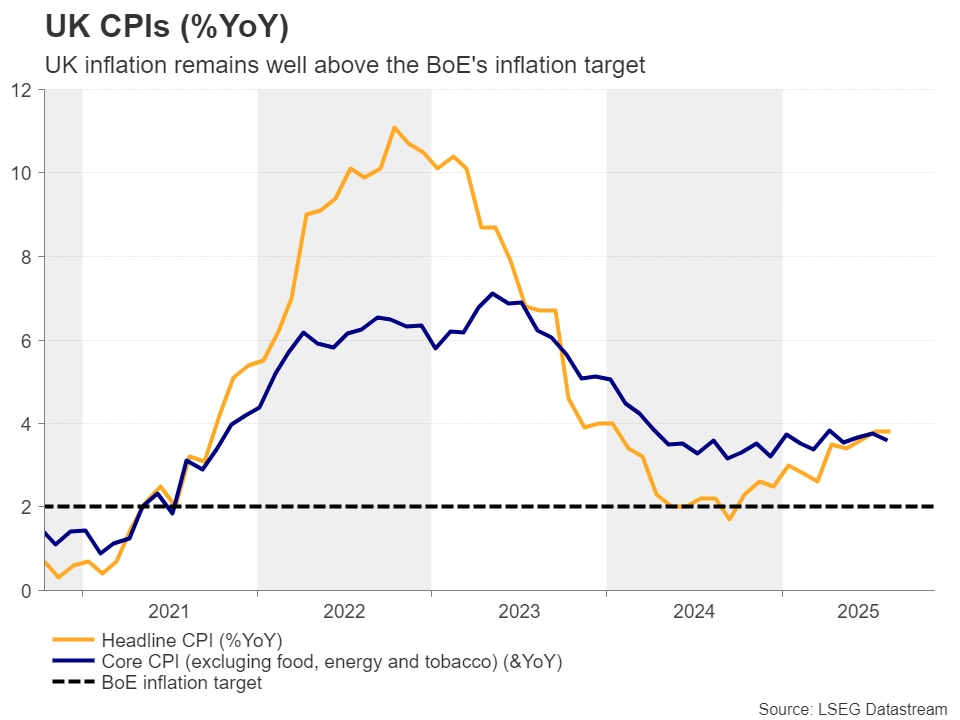

Did UK inflation accelerate as the BoE projected?

Pound traders are also facing a busy week, with September’s CPI data slated for release on Wednesday, followed by retail sales for the same month and the preliminary S&P Global PMIs on Friday.

At its latest gathering, the Bank of England maintained its Bank Rate at 4% via a 7-2 vote, with the two dissenters advocating a 25bps reduction. The accompanying statement highlighted that the Bank’s monetary policy stance has become less restrictive and that a gradual and careful approach to further easing remains appropriate. Although officials acknowledged ongoing underlying disinflation, they noted that there was greater progress in easing wage pressures than prices.

Indeed, this week’s employment data revealed that average earnings excluding bonuses continued to ease, though the y/y rate remained elevated at 4.7%. The unemployment rate rose to 4.8% from 4.7%, prompting market participants to assign a nearly 50% chance of another 25bps rate cut by December. Such a policy move is nearly fully priced in for February, while one more same-sized reduction is anticipated by the end of 2026.

What may have also influenced the latest dovish tilt in market expectations were remarks by UK Chancellor Rachel Reeves, who indicated that she is considering tax increases and spending cuts in the autumn budget, scheduled for announcement on November 26.

Tighter fiscal policy creates room for a more accommodative stance, yet the BoE’s next steps will hinge largely on next week’s inflation data. The Bank itself projected that inflation is expected to increase slightly in September from 3.8% y/y in August. Should Wednesday’s CPI report confirm this, investors may scale back their rate cut bets, thereby injecting fuel into the pound’s engines. A set of encouraging retail sales and PMIs may add extra credence to the idea that policymakers should not rush into lowering borrowing costs.

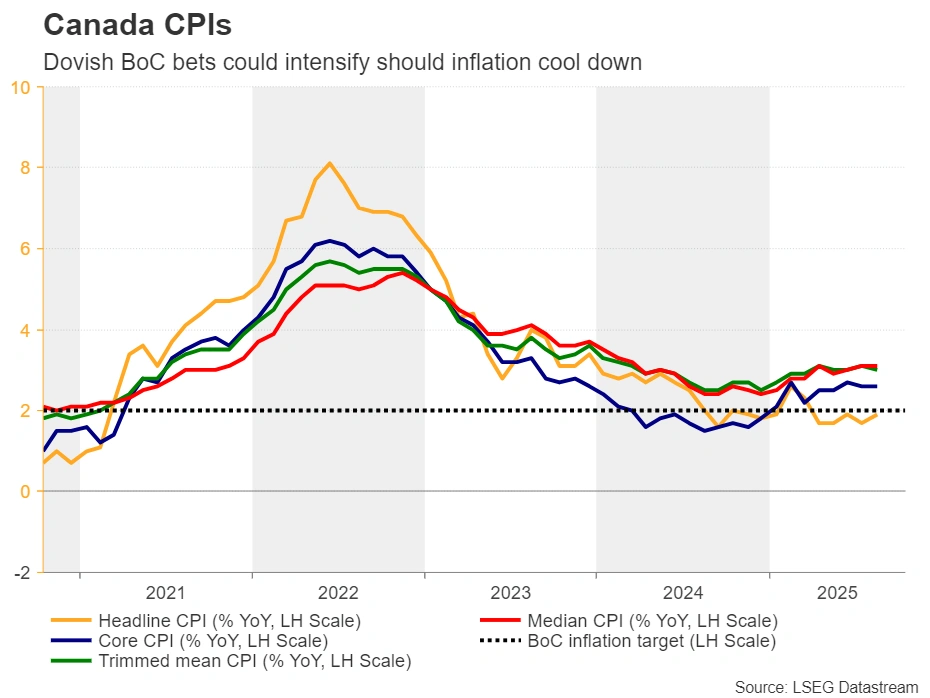

Canada and Japan CPI figures to shape BoC and BoJ expectations

CPI figures will be released from Canada and Japan as well, on Tuesday and Friday, respectively.

Getting the ball rolling with Canada, on September 17, the Bank of Canada lowered interest rates by 25bps – the first reduction since March – citing a weaker economy and a rising unemployment rate. The market was quick to price in at least one additional rate cut for the foreseeable future, assigning a 60% probability to a move on October 29. A slowdown in the CPIs could take that probability higher and perhaps hurt the loonie.

In Japan, the likelihood of a Bank of Japan rate hike at the turn of the year has risen again to 65% amid political deadlock. Fiscal dove Sanae Takaichi, recently elected leader of the Liberal Democratic Party (LDP), has reportedly lost support from Komeito, the coalition partner, adding uncertainty to the policy outlook.

Takaichi’s election initially raised speculation that the BoJ may delay its rate hike process, but the stalemate has led investors to restore their rate hike bets. Combined with the risk-aversion triggered by the renewed trade tensions between the US and China, these factors allowed the yen to recover decent ground. That said, for the Japanese currency to continue its upside trajectory, Friday’s inflation data may have to surprise to the upside, something that could increase the probability of a BoJ rate hike in the coming months even further.

China GDP in focus amid US-China trade frictions

Speaking of China, on Monday, the world’s second largest economy will release GDP data for Q3, alongside industrial production, fixed asset investment, retail sales, and the unemployment rate, all for September.

Consumer prices fell more than expected in September and although producer prices improved, they remained in deflationary territory, highlighting weak domestic demand and trade anxiety. Another set of data suggesting that the economy is struggling could intensify calls for more stimulative measures by Chinese authorities – especially following the latest trade spat with the US – and could thereby weigh on aussie and kiwi, given that China is the main trading partner of both Australia and New Zealand.

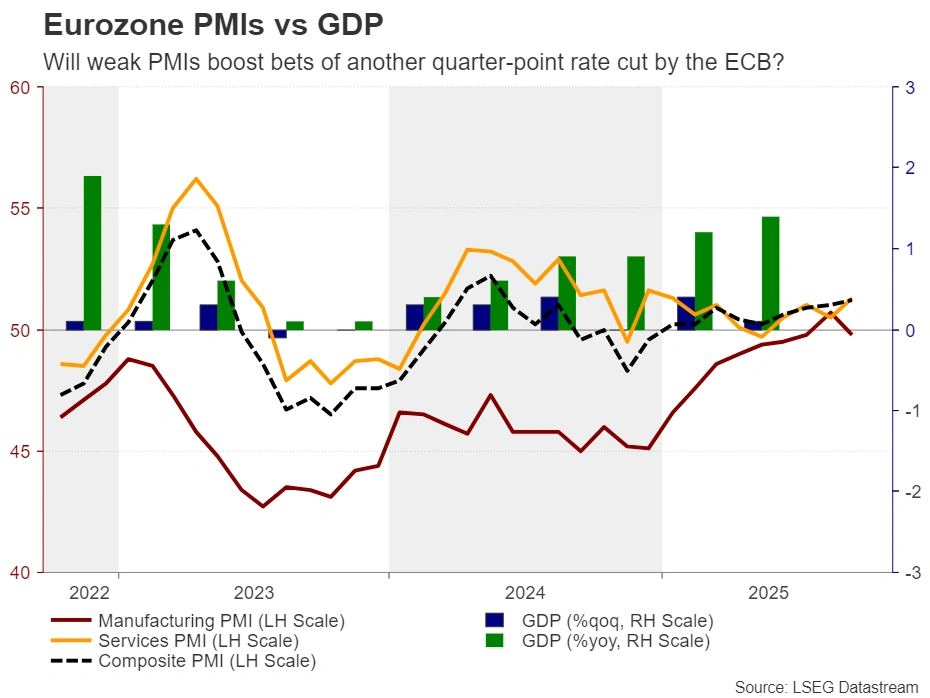

Will the EZ PMIs confirm that the ECB is done cutting rates?

In the Eurozone, the preliminary S&P Global PMIs for October may set the tone for the euro, which took a hit lately following the gridlock in French politics. However, in terms of ECB monetary policy, the market is not fully factoring in any additional rate cuts. There is nearly a 70% chance of another 25bps reduction by July 2026, which means that some investors believe the ECB is done with easing policy.

Indeed, several ECB policymakers have emphasized that there is no reason to adjust rates in the coming months. That said, Governing Council member Villeroy said this week that the Bank’s next move is likely to be a cut rather than a hike. Combined with previous remarks by Vice President de Guindos regarding the NEER euro rate, which is hovering at record highs, this suggests that any signs that a strong euro is affecting trade and the broader economy could spark speculation of a contingency cut in the foreseeable future, and thereby take euro/dollar lower. Soft PMIs could trigger the first wave of such concerns.

Earnings season continues with Netflix and Tesla results

Besides the aforementioned macro data, next week’s agenda includes earnings results from Netflix and Tesla.

Netflix will draw particular attention following Elon Mask’s call for his followers to cancel their subscriptions over controversy regarding an animated show and its creator. Nonetheless, the backlash might not be a big headache for the streaming giant, as Mask’s remarks came too late to meaningfully impact subscriber counts. What’s more, the fourth quarter of 2024 marked the last reporting of this metric before the company shifted priority to revenue over user growth.

As for Musk’s own company, the results are likely to center around vehicle deliveries and auto profit margins. The firm has already announced a record 497,099 vehicle deliveries in Q3 2025, which marks a 7% increase from the same quarter last year. Based on that, strong revenue metrics may be reported, likely providing support for the company’s stock price.

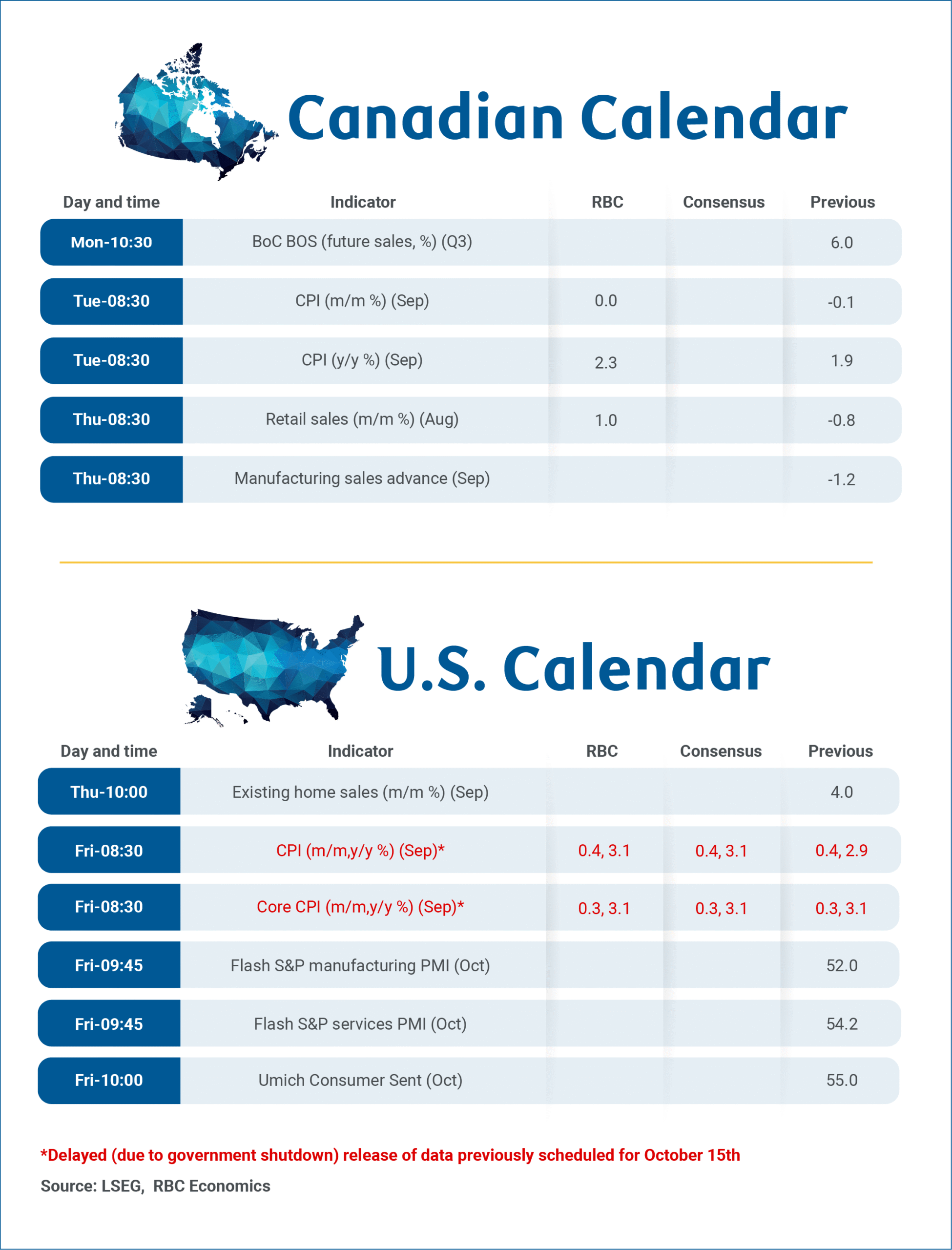

Forward Guidance: Inflation and Retail Data to Guide Next BoC Interest Rate Move

The Bank of Canada will be closely watching September’s consumer price index report, August’s retail sales data as well as its own Q3 Business Outlook Survey in the coming week ahead of an interest rate decision on Oct. 29.

It is unlikely that policymakers cut rates in September expecting that just one 25 basis point reduction would be sufficient. We expect them to follow with another 25 basis point cut in Q4, most likely later this month.

The BoC did leave additional rate reductions contingent on economic data, and inflation not surprising significantly to the upside. We don’t think details of a firmer-than-expected jobs report in September alone is enough to derail another rate cut, and we expect inflation trends look broadly similar in September to August.

We expect headline CPI growth of 2.3% year-over-year in September, up from 1.8% in August as the pace of energy price declines slowed. That would leave inflation tracking close to our Q3 base case assumption of a 2% quarterly average. Food price growth likely eased last month, but underlying price pressures appear to have firmed.

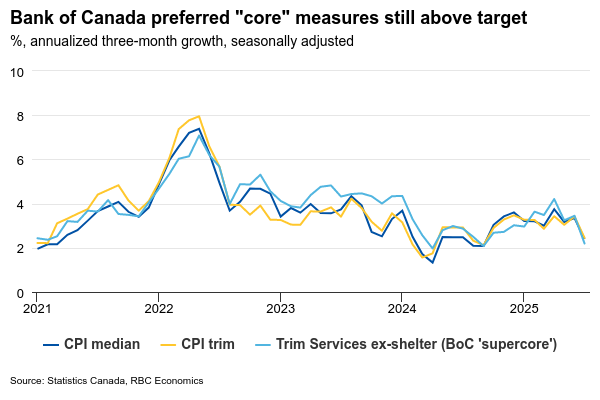

We look for inflation excluding food and energy to rise to 2.6% from 2.4% in August, suggesting modest upward pressure in other categories. The BoC’s preferred core inflation measures continue to hover near 3% year-over-year, and about 2.5% on a three-month rolling average. Both are still running above the BoC’s 2% inflation target, but are similar to the month earlier.

Stabilizing business sentiment

The Business Outlook Survey on Monday will offer a more qualitative check on the pulse of the economy. We expect it to show further signs of stabilizing business sentiment after a period of heightened uncertainty earlier this year when U.S. trade tensions were most intense. Earlier data from the Canadian Federation of Independent Business suggests the recovery is already underway. Their Small Business Confidence Index rose again in September, and now sits slightly above the breakeven threshold.

Meanwhile, a preliminary estimate of retail sales for August from Statistics Canada pointed to a 1% rebound following a July dip. September’s flash estimate on Thursday will be closely watched for signs of continued resilience in consumer spending. RBC’s card spending data showed relatively firm momentum in September, though Q3 quarterly spending growth has slowed from Q2.

Week ahead data watch:

The U.S. government shutdown is disrupting the release of several economic indicators, particularly from public sector agencies, but the Bureau of Labor Statistics has confirmed the CPI report will be released on Oct. 24. September CPI data is expected to show both headline and core inflation rising 3.1% year-over-year, reflecting the onset of core goods price pressures as tariff pass-through effects finally begin to emerge.

Weekly Focus – Market Jitters on New US Regional Banking Worries

Trade war has once again been a dominant theme in markets, after US president Trump threatened an additional 100% tariff on Chinese goods last week. We see it primarily as a negotiation tactic, but even if the threat takes effect on 1 November, the economy would be much better prepared than six months ago. Equity markets rebounded on expectations that trade disputes will be solved.

With no official US data in on account of the government shutdown, bond markets have taken their clues from Fed chair Powell's worries about the labour market and his take that tariffs, rather than broader inflationary pressures are driving elevated goods prices. His remarks pushed global bond yields lower and the move was further exacerbated by renewed concerns over regional bank credit quality in the US following the disclosure of problematic loans at Zions Bancorp and Western Alliance Bancorp. It adds to a growing list of investors' worries and the news also weighed heavy on equity markets and caused a big spike in the VIX index.

The private NFIB business sentiment did offer some interesting insights into how small US businesses see the outlook, while we wait for official data. Optimism declined on rising concern of tariff-related issues. At the same time, price plans edged higher, which has historically led changes in the official CPI by few months.

On our own continent, the French Prime Minister Lecornu survived two no-confidence votes after caving in to the Socialists' demand to suspend the pension reform, which led to OAT-Bund spread tightening. While positive in the short term, a complete reversal of the pension reform will place additional strain on France's already weak public finances. In fact, Moody's has France up for review next week.

Next week kicks off with the monthly batch of Chinese data, which will likely show that the domestic economy is still weak with housing and private consumption struggling. Elsewhere in Asia, negotiations to form a new Japanese government are ongoing and things are more unpredictable than seen in many years. There are different opinions on the right extent of fiscal as well as monetary stimulus. That said, the ruling Liberal Democrats sit on 42% of the parliamentary seats and it remains most likely they will continue to govern, although not without serious concessions to a potential coalition partner. A parliament vote for prime minister is scheduled for Tuesday.

In the euro area, PMI data stands out on the agenda. We expect the euro area economy to be close to stagnant in the second half of 2025, which aims with composite PMI close to unchanged just above the 50-thresshold.

In the US, focus will be on trade negotiations and of course the delayed September CPI print. We see core CPI at 0.3% mom for a third consecutive month with risks to the upside but also the bar for Fed skipping its planned rate cut on 29 October as very high. US PMI data might also catch more attention than usual. US data will probably continue to be scarce, with prediction markets assigning roughly an 80% probability that the shutdown will extend into November.

Sunset Market Commentary

Markets

In a market devoid of hard economic data, yesterday’s credit-driven risk off from the US also fully hit European markets. European equities (Eurostoxx 50) opened >1.5% lower, an even bigger loss than the close in major US indices yesterday. Bunds extended their recent rally with the German 10-y yield at 2.53% testing the lowest level since end June. Money markets also further raised the chance of an additional ECB interest cut next year to about 75%. However, sentiment gradually turned less negative, especially as US traders joined. A series of US (regional) banks reported earnings with no unexpectedly high credit provisions. Also before the open of US markets, investors took comfort from some headlines from a Fox Business interview with president Trump, as he indicated that the current high tariffs on China were not sustainable. Recent threats might again be considered as some kind of ‘tactical’ (TACO?). Even so, both topics can still cause some ‘glass half full, glass half empty’ market swings going forward. After an initial decline this morning, both US and European yields have currently recouped initial declines. US yields are rebounding between 2 bps(5-y) and 1 bp (30-y). Key technical levels across the whole US yield curve that were broken yesterday (including 3.43/3.5% area for the 2-y, 4% for the 10-y) are still at risk. Money markets for now have left the idea of a potential 50 bps step at some of the two remaining Fed meetings this year and again are pricing two 25 bps steps at the end October and December meetings. German yields are currently marginally higher (30-y + 1 bp) after a decline at the open. Even so, in a broader perspective, both US and EMU bonds easily consolidate recent strong gains. The EuroStoxx 50 ‘limits’ the daily loss at the moment to 0.7%. US indices open little changed (Dow) to 0.5% lower (Nasdaq). The Vix volatility index jumped to the highest level since end-April, but eased as the US trading session proceeds. The dollar tracked the intensity of the’ US risk-off’ intraday, with DXY testing to low 98 area this morning before returning to 98.45. EUR/USD failed to maintain gains north of 1.17 (currently again 1.1675). USD/JPY after touching the 149.4 area, rebounds back to 150+ levels.

Aside from potential market moving headlines on trade and on credit, the eco calendar is backloaded next week. US data releases mostly are still suspended due to the government shutdown, but on Friday the BLS will publish (delayed) US September CPI data which still serve as input for the October 29 FOMC meeting. In this respect, the blackout period for FOMC members to comment on monetary policy starts tomorrow. Also on Friday next week, the US and EMU PMI’s will provide some insight on the economic momentum on both sides of the Atlantic. In the UK, September CPI data on Wednesday are key input for the November 6 BoE policy meeting. EMU bond investors look forward to credit rating reviews next Friday for the likes Belgium, France and Slovakia as well.

News & Views

The Hungarian National Bank (MNB) is widely expected to keep its base rate unchanged at 6.5% at next week’s policy meeting, accompanied by ongoing hawkish language. The MNB is facing stubborn inflation with CPI not expected to fall within the 2-4% tolerance band before the end of the year and strong services inflation creating second-round risks. The central bank is also wary of the government’s expansionary fiscal policy with new initiatives such as a 14th pension payment floated ahead of next year’s parliamentary elections. The Hungarian forint meanwhile has strengthened in recent weeks, bringing some comfort for the central bank through its disinflationary impact. The HUF rally, however, is now stalling around EUR/HUF 390 and signaling rate cuts of any kind risks triggering a reversal. KBC Economics sees little scope for monetary easing prior to early next year and even that depends on inflation having fallen to around 3% y/y and EUR/HUF more or less stable around the current levels.

Chinese finance ministry officials said that fiscal revenue has been picking up in September from August despite signs the economy could be losing momentum. September 2.6% increase compares to the 2% in the month before. For the first three quarters of the year, fiscal revenue grew 0.5% y/y, the officials said, adding that they’ll continue frontloading the bonds from 2026’s new local government debt quota in an attempt to further jumpstart the economy. On a related note, China’s Communist Party next week is holding its fourth Plenum in which they’ll map out the country’s next five-year vision (2026-2030). High-tech manufacturing is seen as being high on the priority list, together with a further shift towards private consumption. Chinese Q3 GDP growth numbers are also on tap next week with consensus expecting YtD GDP growth having slowed from 5.3% in Q2 to 5.1% last quarter..

WTI Oil: Bears May Take a Breather to Position for Fresh Push Lower

WTI Oil price fell further on Friday, remaining on track for the third consecutive weekly loss and the second straight weekly close below $60 mark.

Oil remains under pressure from darkened demand outlook, with the latest forecast from International Energy Agency about growing supply surplus, news about potential meeting between US and Russian Presidents, and growing US-China trade tensions, contributing to current picture.

Oil price fell to the lowest in five months and eyes key supports at $55.40/12 (2025 lows posted in Apr/May) which also formed a double bottom, ahead of subsequent strong rally.

Daily studies are in full bearish setup, but oversold conditions,14-d momentum indicator turning north from the depth of negative territory and anticipated profit taking at the end of the week, suggest that we may see some consolidation or limited correction.

Broken $60 level reverted to initial resistance (reinforced by falling 10DMA), followed by broken Fibo 76.4% ($60.71) and $61.50 zone (former range floor and higher base, reinforced by 20DMA), where stronger upticks should be capped to keep larger bears in play.

Res: 58.37; 59.74; 60.00; 60.71.

Sup: 56.58; 55.40; 55.12; 53.87.

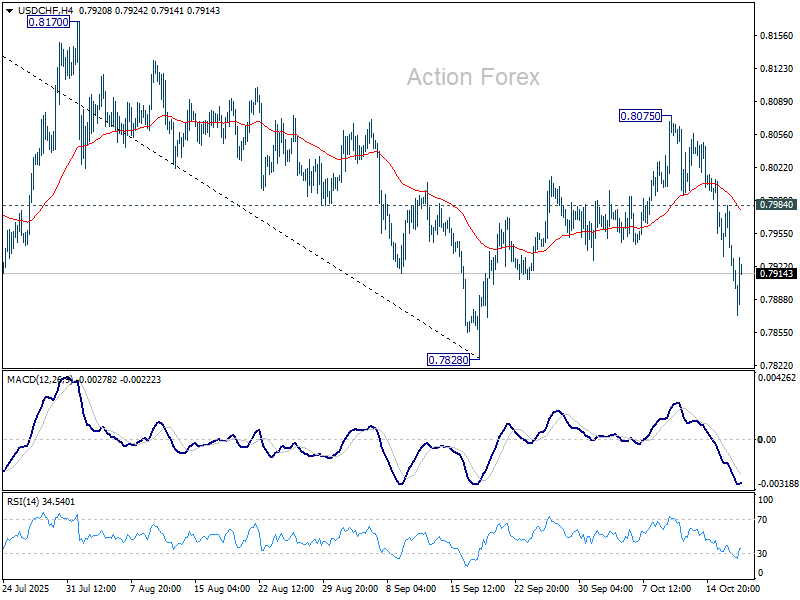

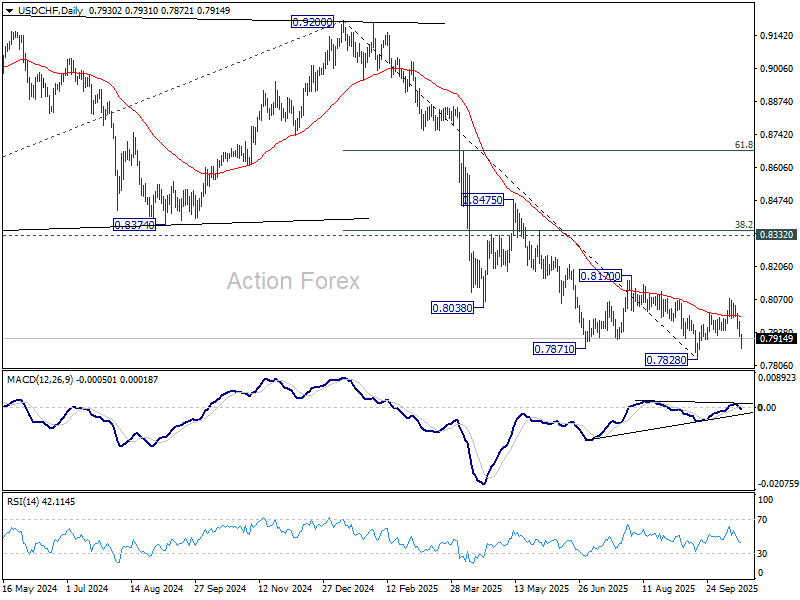

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7907; (P) 0.7946; (R1) 0.7968; More…

Intraday bias remains mildly on the downside for retesting 0.7828 low. Decisive break there will resume larger down trend. For now, risk will stay on the downside as long as 0.7984 minor resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

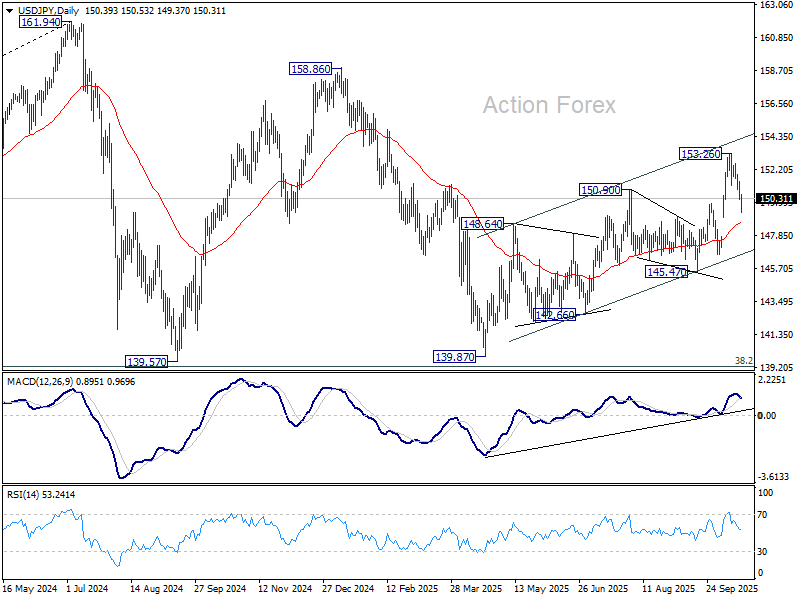

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.97; (P) 150.68; (R1) 151.16; More...

Intraday bias in USD/JPY stays mildly on the downside at this point. Fall from 153.26 short term top would target 55 D EMA (now at 148.58) instead. Sustained break there will raise the chance of bearish reversal and target 145.47 structural support next. On the upside, above 151.38 minor resistance will turn intraday bias neutral again first.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

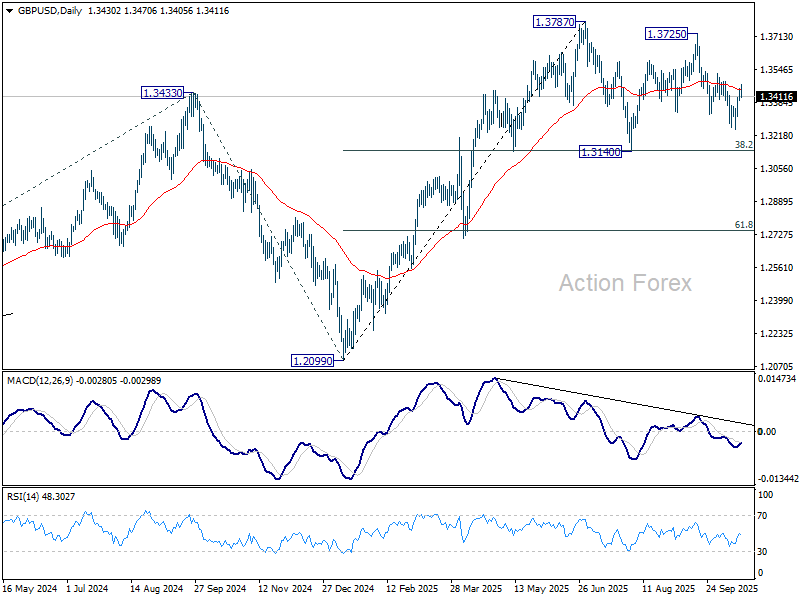

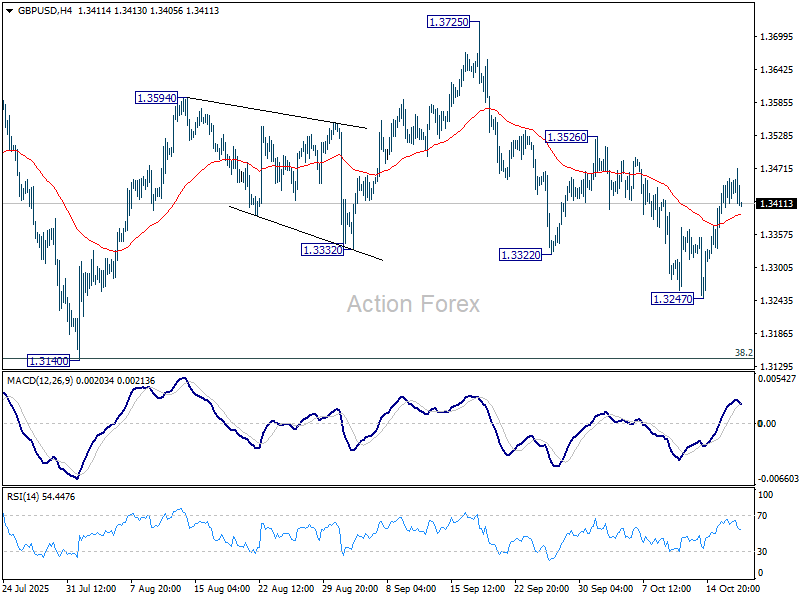

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3399; (P) 1.3427; (R1) 1.3462; More...

GBP/USD's recovery lost momentum well above of 1.3526 resistance and intraday bias remains neutral. Fall from 1.3725 could still extend lower through 13247. But even in that case, strong support is expected from 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142) to complete the corrective pattern from 1.3787. On the upside, break of 1.3526 will bring stronger rally back to 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.