Sample Category Title

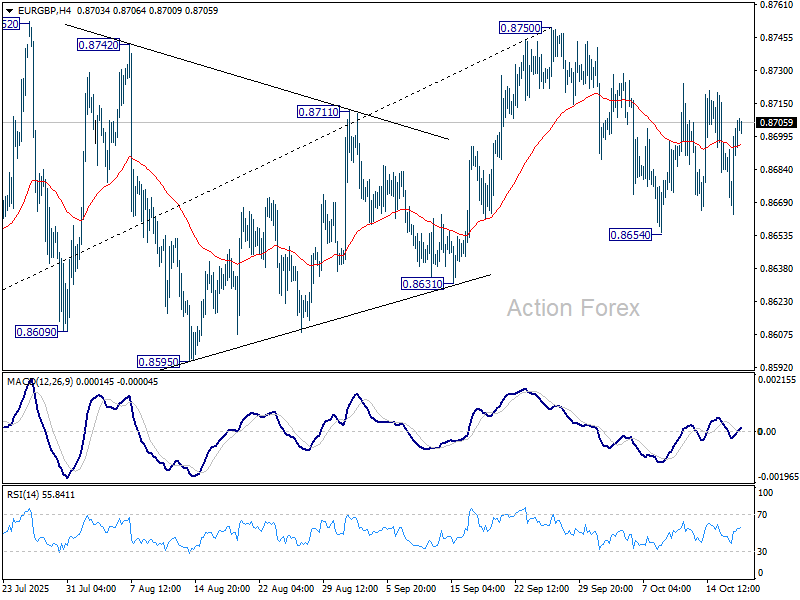

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8674; (P) 0.8689; (R1) 0.8714; More…

Range trading continues in EUR/GBP and intraday bias stays neutral. On the upside, firm break of 0.8750 will resume larger rally towards 0.8867 fibonacci level. On the downside, break of 0.8654 will extend the fall from 0.8750 to 0.8631 support next.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8631 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8550) will confirm, and bring retest of 0.8221 low.

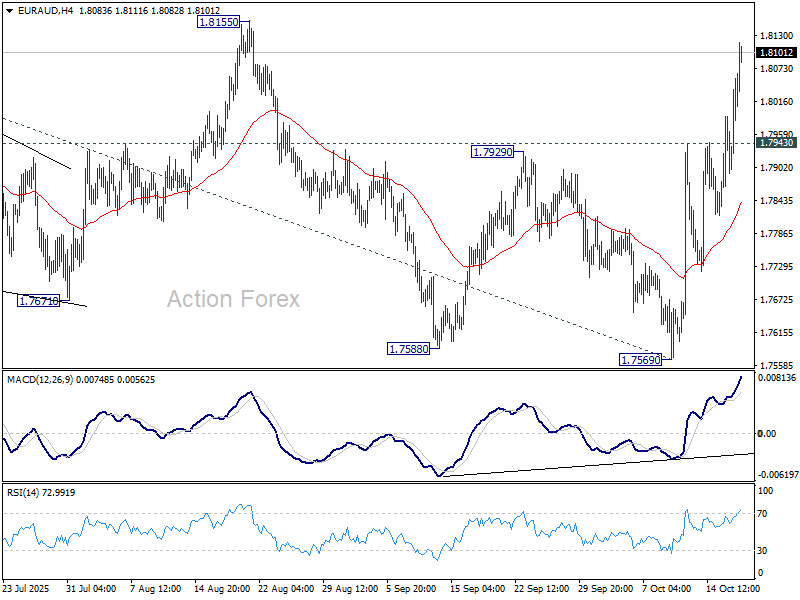

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7910; (P) 1.7984; (R1) 1.8092; More...

EUR/AUD's rally continues today and intraday bias stays on the upside for 1.8155 resistance. Firm break there will argue that whole corrective pattern from 1.8554 has completed with three waves to 1.7569. Further rise should be seen to retest 1.8554 high next. On the downside, below 1.79743 will turn intraday bias neutral first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern, which might have completed already. Firm break of 1.8554 will resume larger up trend from 1.4281 (2022 low), and target 61.8% projection of 1.5963 to 1.8554 from 1.7569 at 1.9170. This will remain the favored case as long as 1.7569 support holds.

Gold Price Soars to All-Time High

In focus today

In the euro area, we receive the final inflation print for September. We expect the data to confirm the flash release of headline inflation at 2.2% y/y and core at 2.3% y/y so the print should not be a market mover.

In Sweden, unemployment figures will be published this morning. We expect unemployment to remain largely unchanged at 8.8% (SA). Although the momentum in the labour market is improving, stronger employment in PMI, and an increase in new vacancies from SPES, it is unlikely to be enough to already reflect improvements in the LFS unemployment rate.

In the early hours of Monday, China will release its monthly batch of data for retail sales, housing, etc., as well as GDP data for Q3. GDP growth is expected to slow from the 5.3% rate in the first half to 4.7% in Q3. The monthly data will likely indicate that the domestic economy remains weak, with housing and private consumption continuing to struggle.

Economic and market news

What happened yesterday

In France, premier Lecornu survived the two no-confidence votes in parliament. A total of 271 MPs voted in favour of bringing down the government which was as expected and showed that a handful of Socialists went against the party line as they previously stated they would. This gives some temporary stability in French politics, and the parliament can now work on the 2026 budget. While this is positive in the short term, we eventually expect problems to return as the suspension of the pension reform makes the medium-term fiscal sustainability worse.

In the US, shares of regional banks faced sharp declines following disclosures of problem loans at Zions Bancorp and Western Alliance Bancorp, both of which reported losses tied to alleged fraud involving loans to funds investing in distressed commercial mortgages. Zions dropped 13%, while Western Alliance fell 11%, raising fresh concerns over the stability of the sector. These developments have highlighted investor nervousness despite the S&P 500 Index remaining near record highs.

In geopolitics, following a two-hour phone call with Russian President Putin, President Trump announced plans to meet Putin in Budapest within 'the next two weeks or so' to negotiate an end to the war in Ukraine. Meanwhile, Ukrainian President Zelenskyj is set to meet Trump in Washington today to request additional military support, including long-range missiles. While the White House had recently signalled support for Ukraine, Trump's conciliatory remarks after his call with Putin have raised doubts about the US's next steps.

In commodities, gold reached a record high of USD 4,378 per ounce before retreating slightly, while silver also hit a new peak, topping at USD 54.5. The flight to safety amid renewed US regional banking sector concerns has driven strong demand, with gold set for a weekly gain of 7.6%, the largest since early 2020.

In the UK, the monthly August GDP growth came in at 0.1% as expected. Thus, the less than impressive growth picture continues in the UK. Chancellor Rachel Reeves is facing a GBP20-30bn shortfall in the public budget and a strong rationale to build an additional fiscal buffer on top of that, following years of uncertainty surrounding taxation and spending policies. The Labour Party has promised to freeze income tax rates, National Insurance contributions (social security) and VAT, the three biggest sources of revenue. Most alternative measures, such as reforming property taxation, would prove highly challenging or place significant strain on economic growth. Regardless of the approach, there is a compelling case for addressing the fiscal challenge now, while the next election is still years away. Reeves has acknowledged that she is looking at potential tax increases and spending cuts, and it is hard to see how the fiscal gap can be resolved without breaking some promises. There is no way around an unpopular decision, and we think the Labour government will prioritise addressing the budgetary shortfall in the 26 November budget rather than risk larger tax increases later.

In Norway, Q3 manufacturing confidence dropped from +0.4 to -0.3, pointing to negative growth in the manufacturing sector for the first time in almost 2 years. Details to the weak side as new orders dropped from 48.8 to 47.5 and employment from 54.0 to 53.2. Looking at sectors, the producers of capital goods, a proxy for oil-related sectors, have now turned negative which fits well with our view that oil investments are about to turn into a headwind for the economy. Producers of intermediate goods, a proxy for the export industries, are expecting a very moderate upswing.

Equities: Equities were mixed on Thursday, with Europe faring well (Stoxx 600 up 0.7%) while US markets retreated, ending near session lows (S&P 500 -0.6%, small-cap Russell 2000 -2.1%). Financials were the main drag on US markets, weighing particularly on US small caps after renewed concerns over regional bank credit quality. Additionally, underwhelming earnings from insurance companies added to the sector's weakness. The result was a broad risk-off session, with nearly all sectors ending lower. Risk aversion appears to be carrying into Friday, as US futures roughly 0.5% lower pre-market.

Diving deeper, Zions Bancorporation disclosed a 50 million charge-off tied to defaulted commercial loans, reigniting concerns about the health of regional bank balance sheets. This adds to a growing list of developments that have unsettled investors, following two subprime auto lender Tricolor and major auto parts supplier First Brands bankruptcies in September. Shares of Zions and Western Alliance both tumbled more than 10% on the news.

FI and FX: US Treasury bond yields declined on the back of problems with two US regional banks which has been hit by bad loans. France sold some EUR 13bn in nominal bonds and linkers yesterday with a decent bid-to-cover. Hence, there seems to be no problem in selling OATs and linkers at the auctions, which was also seen last year when the political crisis began after European parliament elections.

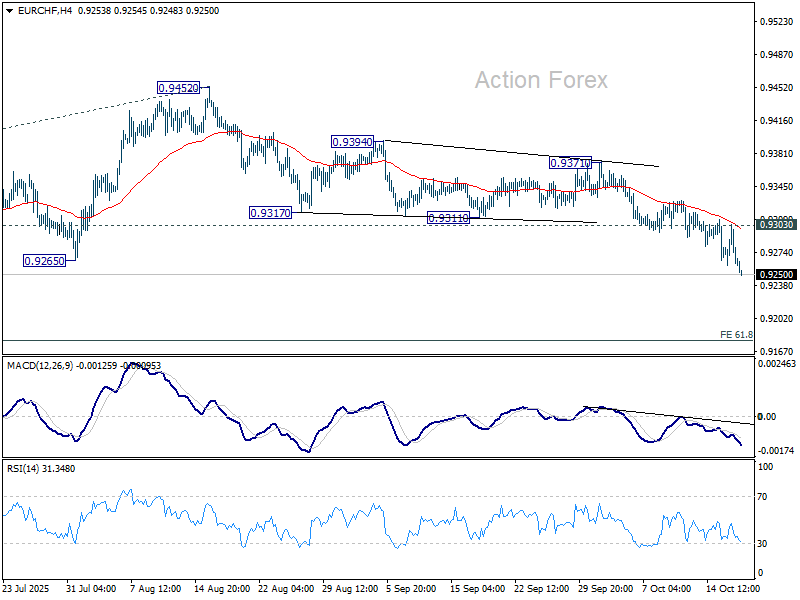

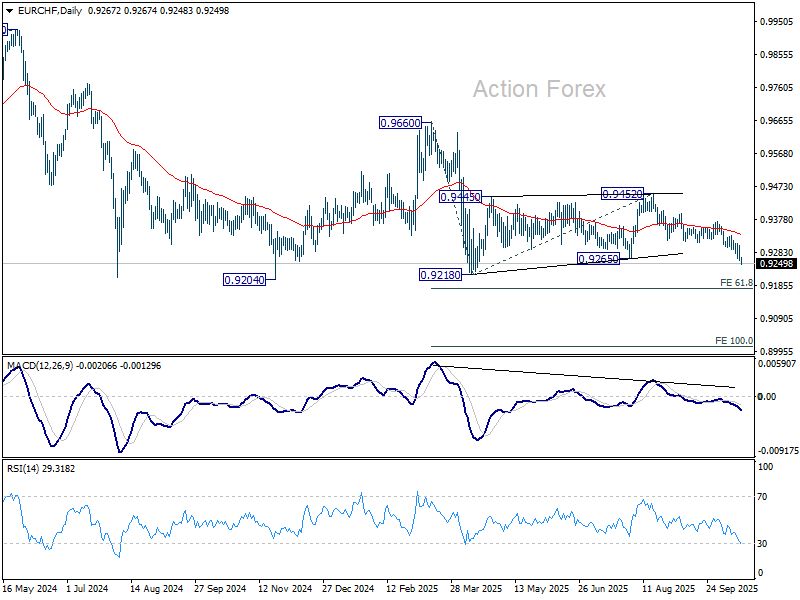

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9249; (P) 0.9277; (R1) 0.9293; More...

EUR/CHF's is still in progress and intraday bias stays on the downside. Current development suggests that consolidation from 0.9218 has completed with three waves to 0.9452, and larger down trend is resumption. Further fall should be seen through 0.9204/18 support zone to 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179 next. On the upside, above 0.9303 minor resistance will turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. Bearishness is reaffirmed by rejection at 55 W EMA (now at 0.9405). Firm break of 0.9204 will confirm down trend resumption. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851.

Safe Havens Surge as Market Nerves Deepen Ahead of Weekend

Safe-haven demand is dominating global markets as traders head into the final trading day of the week. Gold has surged past 4,300 mark to a new record high, putting it on track for its best weekly performance in five years, while the Swiss Franc is rallying sharply across the board. The flight to safety reflects deepening concerns about financial stability and the global outlook as investors seek shelter from mounting geopolitical and economic uncertainty.

The latest catalyst came from a renewed wave of anxiety over the U.S. regional banking sector, after a string of lenders disclosed rising bad loans. The headlines have revived memories of the mini banking crisis in 2023, which began with the collapse of Silicon Valley Bank, followed soon after by Signature Bank and First Republic Bank. The unease comes just as markets grapple with a series of unresolved macro risks that continue to weigh on sentiment.

Among those, U.S.–China trade tensions remain front and center, with no visible progress toward de-escalation before the November 1 deadline for 100% tariffs. Both sides have hardened their rhetoric, leaving investors uncertain about whether negotiations will resume or break down completely. The lack of clarity is amplifying volatility across equities and commodities, while reinforcing demand for traditional safe havens.

Adding to the fog, the U.S. government shutdown continues with no resolution in sight, delaying key economic data releases and leaving policymakers and investors without a reliable read on the economy—especially on the labor market. The blackout has made it harder for traders to assess whether growth is holding up or slipping, further encouraging defensive positioning in the absence of clear signals.

For the week so far, Swiss Franc leads as the strongest major currency, rebounding after a brief pullback yesterday. Euro and Yen also gained on safe-haven flows. Loonie lags behind, hit by weaker risk appetite and falling oil prices. Dollar, Aussie, and Kiwi are also under pressure, with Sterling trading mid-pack. Sentiment is not yet in freefall, but with nerves running high and multiple risks unresolved, markets are increasingly vulnerable to a sharper turn south.

In Asia, at the time of writing, Nikkei is down -1.58%. Hong Kong HSI is down -1.84%. China Shanghai SSE is down -1.27%. Singapore Strait Times is down -0.55%. Japan 10-year JGB yield is down -0.033 at 1.624. Overnight, DOW fell -0.65%. S&P fell -0.63%. NASDAQ fell -0.47%. 10-year yield fell -0.070 to 3.976.

US 10-year yield breaks 4% on bank fears, watch 3.9% as market stress builds

U.S. 10-year Treasury yield tumbled decisively below the 4.00% mark overnight, hitting its lowest level since April and flashing renewed signs of market stress. The next key support lies at around 3.9%, where some stabilization should occur. However, decisive break below 3.9% would be a serious warning signal that could trigger an accelerated decline toward 3.70%, signaling a sharp escalation in risk aversion.

The sharp drop was driven by flight to safety following unsettling developments in the U.S. regional banking sector. Shares of Zions Bancorporation and Western Alliance plunged after both lenders revealed unexpected bad loans, igniting fears of loose credit standards and potential contagion across smaller financial institutions. The news came on the heels of two recent auto industry-related bankruptcies, which have amplified concerns about tightening credit conditions and balance sheet vulnerabilities.

Markets now turn to Friday’s wave of regional bank earnings, seen as the next test of sector stability. Investors will be watching closely to gauge whether the problem is contained or spreading. A weak showing could deepen risk aversion and accelerate the rush into Treasuries, further suppressing yields.

Technically, 10-year yield’s fall from the recent peak of 4.629 resumed with conviction after breaking below 3.992 support. Next near term target lies at 61.8% projection of 4.493 to 4.205 from 4.200 at 3.891. Some stabilization should emerge there, at least on the first attempt.

However, decisive break below 3.891 would raise the risk of a deeper slide toward 100% projection at 3.699. A bounce from the 3.900 area could still restore some calm — but failure to hold that line risks triggering a deeper wave of safe-haven buying across the Treasury curve.

Fed's Kashkari sees inflation as stubborn but not dangerous

Minneapolis Fed President Neel Kashkari said overnight that the balance of risks in the U.S. economy has shifted, with greater danger of a labor market slowdown than of a sharp rebound in inflation. Neveretheless, he added that while policymakers may be leaning toward the view that the economy is weakening, “we’re more likely betting that the economy is really slowing more than it really is.”

Kashkari downplayed fears of inflation reaccelerating to 4% or 5%, noting that the arithmetic of tariff effects does not support such a scenario. Instead, he described the main concern as “persistence”, with price pressures potentially staying near 3% for "an extended period" rather than spiking.

He also addressed the impact of the ongoing government shutdown, saying that while the lack of official data complicates decision-making, Fed officials still have access to timely private indicators and feedback from business outreach.

“We can make our way through while the shutdown is happening,” Kashkari said. “But the longer it goes on, the less confidence I have that we are reading the economy appropriately.”

ECB's Lagarde: Well positioned to weather future shocks

Speaking at an IMF event, ECB President Christine Lagarde said the Eurozone economy has reached a point of relative stability, with inflation now close to the ECB’s 2% goal. “We are in a good place, and we are well positioned to face future shocks,” she said.

Lagarde cautioned, however, that several unpredictable risks remain on the horizon, from trade-related frictions to the continuing conflict in Ukraine. She said that while uncertainty is still elevated, some feared disruptions “were not as bad as we had anticipated.”

Ueda signals watchful patience as BoJ weighs October policy options

BoJ Governor Kazuo Ueda reiterated overnight that the central bank will consider rate hikes "if our confidence in hitting the outlook increases”. He added that he intends to continue gathering informations before making any decisions at the October 29–30 policy meeting.

Ueda observed that G20 members regard the world economy as broadly stable but facing persistent risks, from trade disputes to geopolitical frictions. "Many institutions and observers still factor them into their outlooks, or at least treat them as downside risks when assessing the global and U.S. economies,” he said.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9249; (P) 0.9277; (R1) 0.9293; More...

EUR/CHF's is still in progress and intraday bias stays on the downside. Current development suggests that consolidation from 0.9218 has completed with three waves to 0.9452, and larger down trend is resumption. Further fall should be seen through 0.9204/18 support zone to 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179 next. On the upside, above 0.9303 minor resistance will turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. Bearishness is reaffirmed by rejection at 55 W EMA (now at 0.9405). Firm break of 0.9204 will confirm down trend resumption. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851.

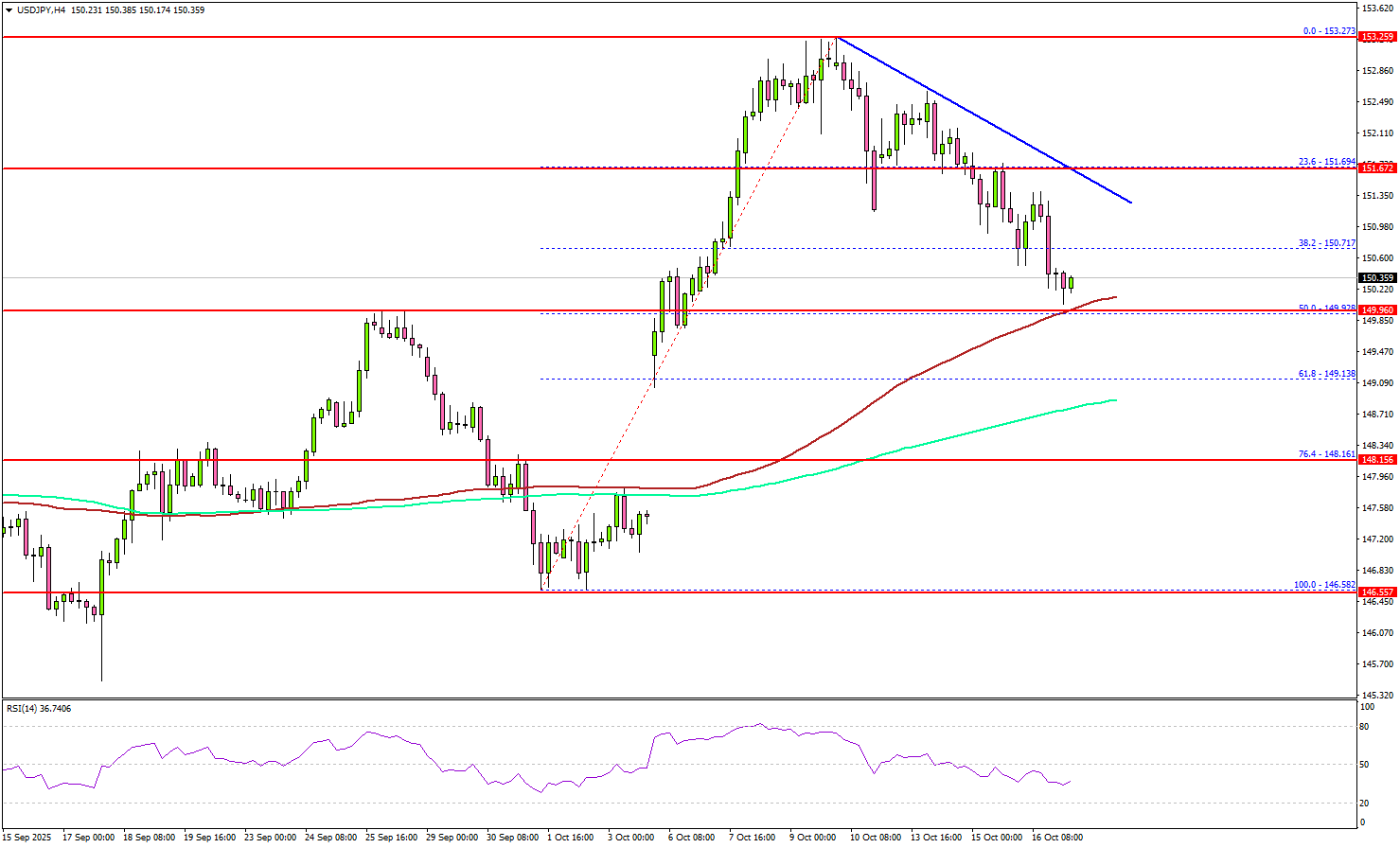

USD/JPY Pulls Back From Recent Highs — Support Test In Focus

Key Highlights

- USD/JPY started a downside correction from the 153.25 zone.

- A key bearish trend line is formed with resistance at 151.70 on the 4-hour chart.

- EUR/USD started a recovery wave above 1.1600 but faces hurdles.

- Gold rallied to a fresh all-time high above $4,260 and seems unstoppable.

USD/JPY Technical Analysis

The US Dollar failed to stay above 153.00 against the Japanese Yen and corrected gains. USD/JPY traded below 152.50 and 152.00.

Looking at the 4-hour chart, the pair traded below the 38.2% Fib retracement level of the upward move from the 146.58 swing low to the 153.27 high. Besides, there is a key bearish trend line formed with resistance at 151.70.

On the downside, the pair might find support at 150.00 and the 100 simple moving average (red, 4-hour). It coincides with the 50% Fib retracement level of the upward move from the 146.58 swing low to the 153.27 high.

The main support might be 149.00 and the 200 simple moving average (green, 4-hour). A close below 149.00 could start a major pullback toward 148.20. Any more losses might open the doors for a test of 146.50.

On the upside, the pair faces resistance near the 151.50 level. The next hurdle could be near the trend line at 151.70. A close above the trend line resistance might push the pair to 152.50.

Looking at EUR/USD, the pair started a recovery wave, but the bears might remain active near the 1.1700 and 1.1720 levels.

Upcoming Key Economic Events:

- US Housing Starts for Sep 2025 (MoM) – Forecast 1.330M, versus 1.307M previous.

- US Building Permits for Sep 2025 (MoM) – Forecast 1.340M, versus 1.312M previous.

US 10-year yield breaks 4% on bank fears, watch 3.9% as market stress builds

U.S. 10-year Treasury yield tumbled decisively below the 4.00% mark overnight, hitting its lowest level since April and flashing renewed signs of market stress. The next key support lies at around 3.9%, where some stabilization should occur. However, decisive break below 3.9% would be a serious warning signal that could trigger an accelerated decline toward 3.70%, signaling a sharp escalation in risk aversion.

The sharp drop was driven by flight to safety following unsettling developments in the U.S. regional banking sector. Shares of Zions Bancorporation and Western Alliance plunged after both lenders revealed unexpected bad loans, igniting fears of loose credit standards and potential contagion across smaller financial institutions. The news came on the heels of two recent auto industry-related bankruptcies, which have amplified concerns about tightening credit conditions and balance sheet vulnerabilities.

Markets now turn to Friday’s wave of regional bank earnings, seen as the next test of sector stability. Investors will be watching closely to gauge whether the problem is contained or spreading. A weak showing could deepen risk aversion and accelerate the rush into Treasuries, further suppressing yields.

Technically, 10-year yield’s fall from the recent peak of 4.629 resumed with conviction after breaking below 3.992 support. Next near term target lies at 61.8% projection of 4.493 to 4.205 from 4.200 at 3.891. Some stabilization should emerge there, at least on the first attempt.

However, decisive break below 3.891 would raise the risk of a deeper slide toward 100% projection at 3.699. A bounce from the 3.900 area could still restore some calm — but failure to hold that line risks triggering a deeper wave of safe-haven buying across the Treasury curve.

Fed’s Kashkari sees inflation as stubborn but not dangerous

Minneapolis Fed President Neel Kashkari said overnight that the balance of risks in the U.S. economy has shifted, with greater danger of a labor market slowdown than of a sharp rebound in inflation. Neveretheless, he added that while policymakers may be leaning toward the view that the economy is weakening, “we’re more likely betting that the economy is really slowing more than it really is.”

Kashkari downplayed fears of inflation reaccelerating to 4% or 5%, noting that the arithmetic of tariff effects does not support such a scenario. Instead, he described the main concern as “persistence”, with price pressures potentially staying near 3% for "an extended period" rather than spiking.

He also addressed the impact of the ongoing government shutdown, saying that while the lack of official data complicates decision-making, Fed officials still have access to timely private indicators and feedback from business outreach.

“We can make our way through while the shutdown is happening,” Kashkari said. “But the longer it goes on, the less confidence I have that we are reading the economy appropriately.”

Ueda signals watchful patience as BoJ weighs October policy options

BoJ Governor Kazuo Ueda reiterated overnight that the central bank will consider rate hikes "if our confidence in hitting the outlook increases”. He added that he intends to continue gathering informations before making any decisions at the October 29–30 policy meeting.

Ueda observed that G20 members regard the world economy as broadly stable but facing persistent risks, from trade disputes to geopolitical frictions. "Many institutions and observers still factor them into their outlooks, or at least treat them as downside risks when assessing the global and U.S. economies,” he said.

ECB’s Lagarde: Well positioned to weather future shocks

Speaking at an IMF event, ECB President Christine Lagarde said the Eurozone economy has reached a point of relative stability, with inflation now close to the ECB’s 2% goal. “We are in a good place, and we are well positioned to face future shocks,” she said.

Lagarde cautioned, however, that several unpredictable risks remain on the horizon, from trade-related frictions to the continuing conflict in Ukraine. She said that while uncertainty is still elevated, some feared disruptions “were not as bad as we had anticipated.”