Sample Category Title

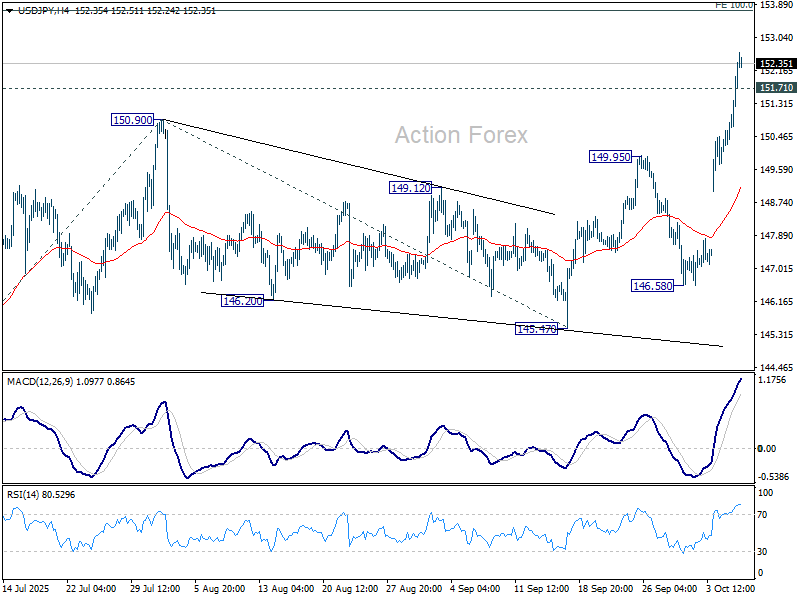

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.72; (P) 151.39; (R1) 152.55; More...

USD/JPY's rally accelerates higher today and intraday bias remains on the upside. Next near term target is 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. On the downside, below 151.71 minor support will turn bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 suggests that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

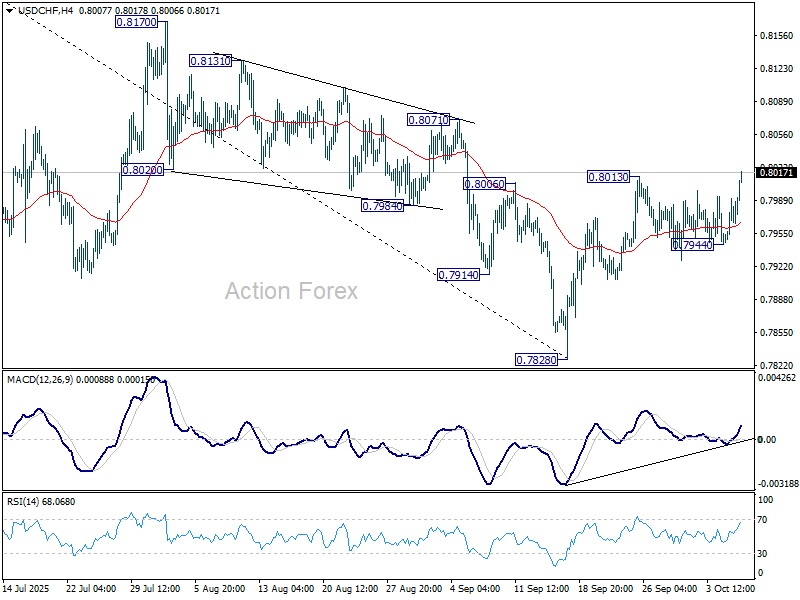

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7956; (P) 0.7974; (R1) 0.8000; More…

USD/CHF's rebound from 0.7828 resumed by breaking through 0.8013 resistance and intraday bias is back on the upside. Sustained trading above 55 D EMA (now at 0.8004) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. For now, risk will stay on the upside as long as 0.7944 support holds, in case of retreat.

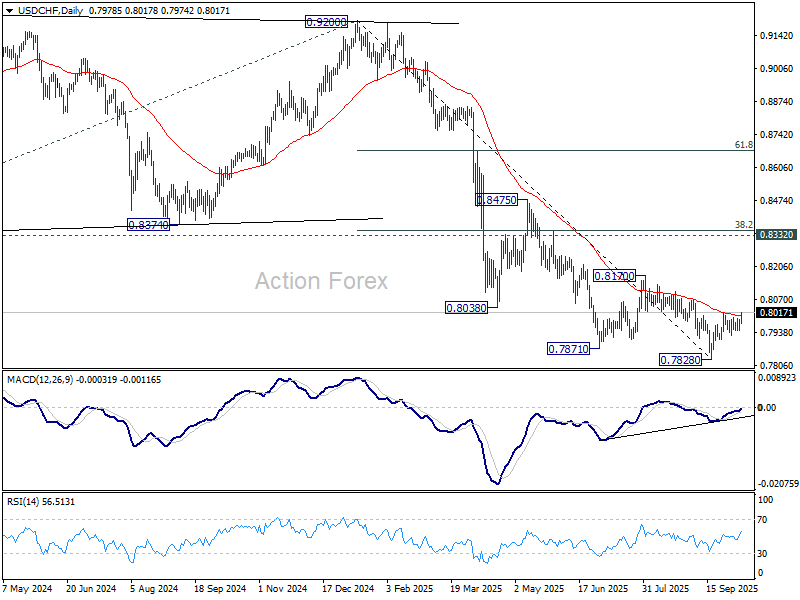

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

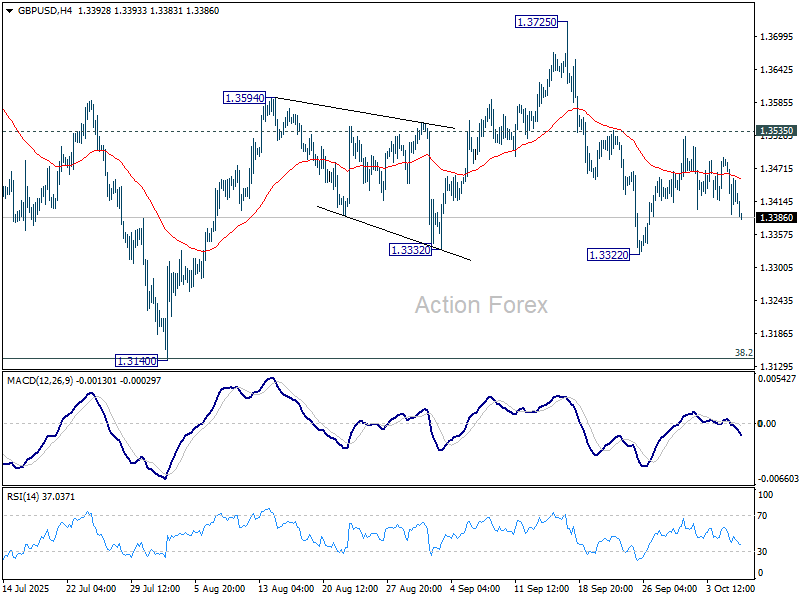

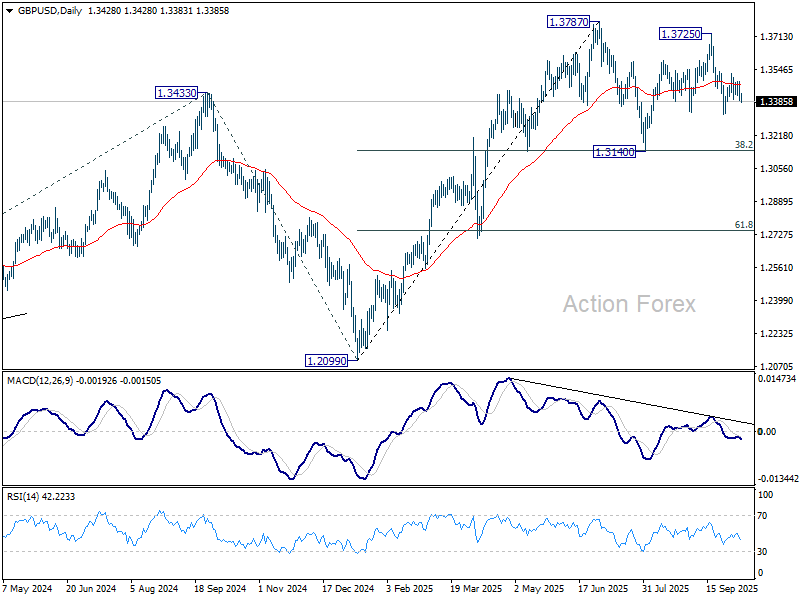

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3382; (P) 1.3435; (R1) 1.3478; More...

GBP/USD is still staying above 1.3322 support despite current dip. Intraday bias stays neutral at this point. With 1.3535 resistance intact, further decline is mildly in favor. On the downside, break of 1.3322 will resume the fall from 1.3725 to 1.3140 support. On the upside, though, firm break of 1.3535 will argue that pullback from 1.3725 has already completed, and bring stronger rise to retest 1.3725/87 key resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3176) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

USD Gains on Weak Euro, Yen

Investors took a breather from buying US stocks yesterday, near all-time highs, as a report showing Oracle’s profit margins were much lower than expected dampened the euphoria that followed the OpenAI and AMD announcements earlier in the week. According to The Information, Oracle made roughly $900 million in revenue in the three months to August by renting servers powered by Nvidia chips, but it only reported a gross profit of $125 million (and a $100 million loss from Nvidia’s Blackwell chip rentals). This is because Oracle operates in a capital-intensive business with high maintenance costs, and its services may still be underutilized.

But data-center demand is expected to rise exponentially through 2030 — largely driven by AI. McKinsey projects global data-center capacity to surge from about 60 GW today to 170–220 GW by 2030, implying 19–27% annual growth. That outlook helps explain why dip-buyers stepped in as Oracle shares fell to around $270.

And that small bump will likely be forgotten quickly, with this morning’s news that Nvidia is considering investing $20bn in Elon Musk’s xAI. Nasdaq futures are up this morning. The AI tide is too strong to swim against — telling ya!

So we’re back to the same conclusion: chips, data centers, energy and cybersecurity are all needed to power AI models. The real question isn’t whether AI will grow, but whether market pricing has run ahead of itself. And no — I don’t buy for a second that AI models won’t generate revenue. There will certainly be losers, but also major winners.

As for valuations — whether markets go up, down, or sideways — the question of a bubble looms. Evercore ISI, in a note titled A Big Beautiful Bubble, argues that while the S&P 500 is indeed in bubble territory, it likely has room to expand — possibly pushing the index to 9’000 by the end of next year with a 33% probability. Eye-popping, yes, but they argue that rate cuts, improving sentiment, stronger earnings, reduced uncertainty and productivity gains from AI could keep investors piling in before the bubble eventually bursts. Their advice: buy the dips rather than close long positions.

There’s also still ample room for leveraged investors to join the rally, given that net short positions in the S&P 500 remain deeply negative. The takeaway? Don’t fear the bubble — play along.

Now, speaking of energy, Shell jumped to its highest level in more than a year in London yesterday after a strong Q3 trading update, boosted by significantly higher gas trading and solid upstream production. Full results are due later this month, but the update offered a sweet taste for investors — even as oil prices remain under pressure. As per oil, the barrel of US crude is back above the $62pb level, but last week’s selloff tilted outlook to the downside, suggesting that the price rallies will likely bump into top sellers with first strong resistance seen into the 50-DMA that currently stands at $63.90 but declining fast.

In FX, UD dollar gains accelerated as investors sold the euro and yen. In Europe, the French political drama widened the France–Germany 10-year yield spread to 86 bps, while in Japan, the yen weakened as markets dialled back Bank of Japan (BoJ) rate-hike expectations on Takaichi’s preference for easy policy. As such, the EURUSD fell below its 50-DMA yesterday and the 100-DMA this morning, with downside potential toward 1.15, while the USDJPY broke above 152, reigniting the once-popular short yen trade. Rising Japanese yields could, however, limit appetite for further yen shorts — and the BoJ is unlikely to turn dovish just because Takaichi wants it to when it remains on a normalization path to balance inflation.

Elsewhere, the US government remains shut, but the FOMC will still release its latest minutes. The delay in jobs data doesn’t help doves hoping for weaker prints, but according to Carlyle Group, the US economy added about 17K jobs in August — modest and enough to keep the doves in charge and equities supported. The US dollar, however, looks set to benefit from further euro and yen weakness for now.

FOMC Minutes Take Centre Stage

In focus today

In the US, minutes from the FOMC's September meeting will be released, with markets closely watching for clues on the timing of the next rate cut. We revised our call yesterday and now expect the Fed to lower rates in October, followed by quarterly reductions until July 2026.

In Sweden, preliminary inflation figures for September are released. Inflation is expected to start declining y/y after the increase over the summer. We will not get any details today (they will be published next Wednesday), but there are still some summer-season-related components expected to decrease. Our forecast is close to the Riksbank's, and we are slightly below consensus. We predict CPIF excluding energy to be 2.7% (prior: 2.9%), and CPIF to be 3.1% (prior: 3.2%).

In Poland, the National Bank of Poland (NBP) concludes its monetary policy meeting. The decision will be a close run, with the market split between a rate cut and a hold. We expect the central bank to keep the policy rate unchanged at 4.75%. The NBP cut rates by 25bp in September, taking a data-dependent stance while emphasising risks to inflation from loose fiscal policy and elevated wage growth. Nonetheless, Governor Glapiński has indicated a 'cautious will' within the Board to cut rates further, and we expect at least one more cut during Q4.

Economic and market news

What happened overnight

In Japan, wage data surprised to the downside with a mere 1.5% y/y increase in total cash earnings for August (prior: 3.4%). In real terms, this corresponds to a decline of 1.4% y/y, marking the fastest drop in 3 months. This contrasts with expectations of a stronger wage pickup following spring negotiations. The weak data adds to the Bank of Japan's challenges ahead of its 29-30 October policy meeting, as sustained wage increases remains a prerequisite for further rate hikes.

In New Zealand, the Reserve Bank of New Zealand (RBNZ) announced a 50bp rate cut overnight, bringing the official cash rate to 2.5% and signalling further easing to come. The decision was a close call, with analyst consensus leaning towards a smaller 25bp cut. Markets reacted by trading the NZD lower, while interest rate swaps also declined. The dovish stance is likely to be a welcome relief for the government, as policymakers aim to address economic struggles. We expect the NZD/USD to rise over the coming year, with a 12M target of 0.63.

In the commodities space, gold surged past USD4000.00 per troy ounce for the first time, marking a historic milestone with gains exceeding 50% year to date. The rally is fuelled by geopolitical uncertainty, soaring debt levels, and central banks diversifying away from the dollar. Other precious metals, including silver, platinum, and palladium, also saw notable gains.

What happened yesterday

In the US, several Fed officials were on the wire, offering mixed signals ahead of the October meeting. Miran advocated for aggressive rate cuts, citing a declining neutral rate and subdued inflation risks. Kashkari was more cautious, warning against stagflation signals amid a slowing job market and persistent inflation around 3%. Lastly, Bostic downplayed recent labour market weaknesses, attributing them to structural factors such as reduced immigration.

Equities: Equities pulled back slightly yesterday after a long stretch of steady gains. There were no major macroeconomic or political catalysts behind the move, rather it looked like a classic case of profit-taking following an extended rally.

The "profit-taking" approach also visible with in the sector rotation as cyclical sectors underperformed, where investors locked in profits, while more defensive areas such as consumer staples outperformed after being massively underperforming in the rally the last six months.

What's worth highlighting is that volatility has been gradually rising, with the VIX now above 17. Considering the current macro backdrop, that's not extreme, but it's notably higher than in recent weeks.

This uptick reflects growing investor awareness that valuations have reached levels rarely seen in recent years, prompting some to hedge exposures in what remains a strong equity environment. Adding to this, the ongoing U.S. government shutdown is limiting the flow of key macro data, leaving markets to navigate somewhat "blindly" for now.

Asian equities are lower this morning, with particular weakness in tech, while U.S. futures are slightly higher and Europe is broadly unchanged.

FI and FX: French politics and the US government shutdown remain in focus in foreign exchange and fixed income markets, together with the strong depreciation of the Yen. As for the latter, the question arises if we could see interventions in the foreign exchange market from the BoJ. In Sweden we get the preliminary inflation numbers for September, and the Debt Office is issuing substantial amount of ten-year government bonds. Norway taps its 4y and 15y bonds.

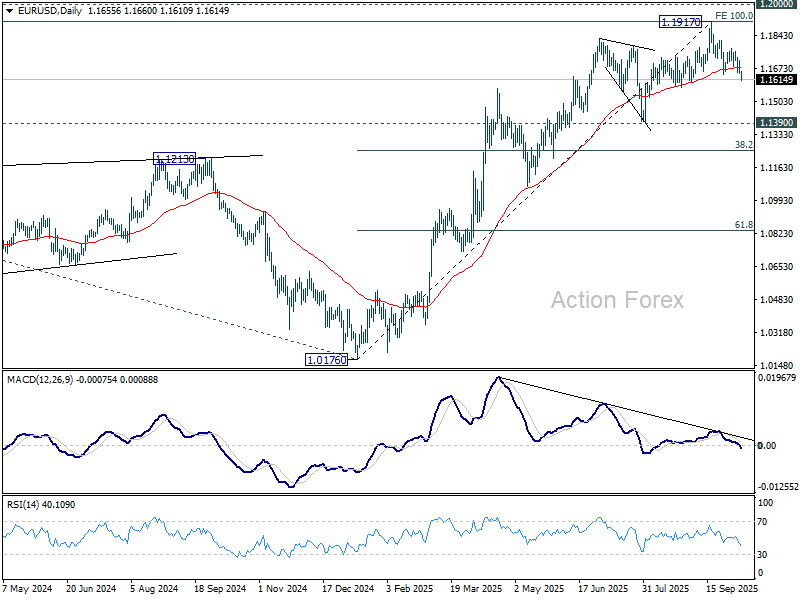

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1632; (P) 1.1675; (R1) 1.1701; More...

EUR/USD's fall from 1.1917 resumed by breaking through 1.1644 and intraday bias is back on the downside. Also, the break of 55 D EMA (now at 1.1679) suggests that a medium term top was already formed on bearish divergence condition D MACD. Deeper fall should be seen to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1682 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1778 resistance holds, in case of recovery.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265) and below.

RBNZ Sparks Kiwi Selloff, Yen and Euro Weakness Persists

The New Zealand Dollar fell across the board after the RBNZ surprised some with a 50bps rate cut and adopted an even more dovish tone than markets anticipated. The cut itself was not a shock—markets had speculated for weeks that a half-point move was possible—but positioning in the lead-up helped amplify the reaction.

Some traders had pared back expectations earlier in the week after the NZIER shadow board recommended only a 25bps reduction. The mismatch between those softer expectations and the RBNZ’s decision sparked a knee-jerk selloff in the Kiwi, pushing NZD/USD to new multi-month lows.

Several major banks quickly shifted expectations. Westpac now forecasts a follow-up 25 bps cut in November, taking the OCR to 2.25%, and ANZ echoed that view.

Despite the Kiwi’s sharp losses, the Japanese Yen remained the weakest performer for the week, still weighed down by optimism surrounding Sanae Takaichi’s victory to become Japan’s next prime minister. Traders increasingly believe her preference for monetary accommodation will encourage the BoJ to delay any further rate hikes until next year.

Euro also stayed under pressure, hurt by the deepening political crisis in France. Outgoing prime minister Sébastien Lecornu is making a last-minute attempt to forge cross-party cooperation after his short-lived government collapsed. He is due to meet with the socialists, greens, and communists on Wednesday in an effort to break the deadlock.

Meanwhile, President Emmanuel Macron faces growing pressure even from former allies to resolve the crisis quickly. Calls for him to resign or call early elections are mounting after his first prime minister urged him to step down for the good of the country.

The currency leaderboard now shows Yen, Kiwi, and Euro as the week’s weakest performers. By contrast, Dollar leads gains, extending its advance with stronger momentum. Loonie ranks second-strongest, helped by a more constructive trade backdrop, while is also firm. Sterling and Swiss Franc are mid-range.

On the trade front, U.S. President Donald Trump struck a conciliatory tone toward Canada, promising to “treat Canada fairly” in ongoing negotiations over U.S. tariffs. After meeting Prime Minister Mark Carney, both sides described the discussions as positive and substantive, though Canadian Trade Minister Dominic LeBlanc said a final deal remained out of reach. “We have momentum now that we didn’t have this morning,” he told reporters, signaling cautious optimism without declaring victory.

In Asia, at the time of writing, Nikkei is down -0.30%. Hong Kong HSI is down -0.86%. China is still on holiday. Singapore Strait Times is down -0.47%. Japan 10-year JGB yield is up 0.019 at 1.700. Overnight, DOW fell -0.20%. S&P 500 fell -0.38%. NASDAQ fell -0.67%. 10-year yield fell -0.035 to 4.127.

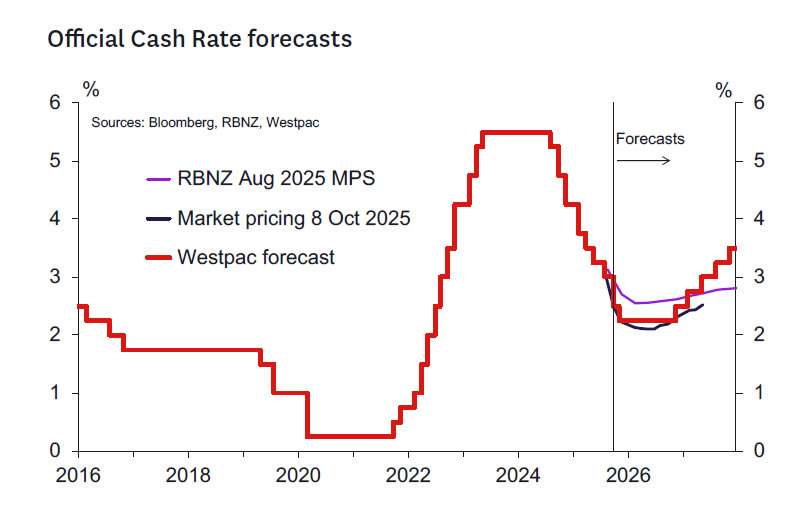

RBNZ delivers 50bps cut, signals readiness to ease further if needed

RBNZ delivered a larger 50 bps rate cut, lowering the Official Cash Rate (OCR) to 2.50% at today's meeting. The central bank maintained its easing bias, saying it “remains open to further reductions in the OCR” to ensure inflation returns sustainably to 2% over the medium term.

Minutes of the meeting showed the Monetary Policy Committee debated between a 25bps and 50bps move, with the majority favoring a bolder step to mitigate downside risks to medium-term growth and inflation. The Committee judged that prolonged spare capacity warranted a "clear signal" to support consumption and investment, helping anchor expectations amid a slowing economy.

While the Q2 GDP contraction was “considerably larger than expected,” the RBNZ attributed much of the weakness to temporary seasonal factors. It expects the distortion to reverse later in the year and said it does not see the short-term softness as materially altering the broader policy outlook.

The central bank noted that it had only marginally revised down its assessment of spare capacity but acknowledged “some downside risk” to activity. Inflation is projected to converge toward the 2% midpoint in the first half of next year, supported by easing tradables inflation and gradually moderating domestic cost pressures.

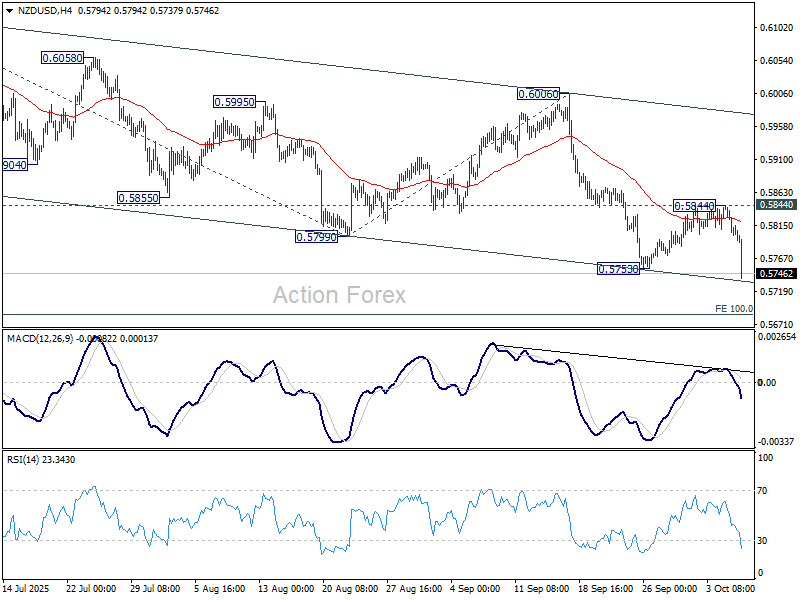

NZD/USD plunges after dovish RBNZ cut; Break below 0.5686 may accelerate losses

NZD/USD tumbled sharply after the RBNZ’s 50bps rate cut to 2.50%, with policymakers retaining an easing bias that signaled scope for further reductions ahead. The policy shift reignited downside momentum in NZD/USD, which broke through 0.5753 support, signaling a renewed leg lower in the ongoing decline from 0.6119.

Technically, near term outlook will stay bearish as long as 0.5844 resistance holds, in case of recovery. The immediate focus is on the bottom of the descending channel near 0.5730, where sustained break would likely drive NZD/USD pair through 100% projection of 0.6119 to 0.5799 from 0.6006 at 0.5686.

Should sellers push beyond 0.5686, NZD/USD could see downside acceleration toward 0.5484 cluster zone, with 161.8% projection at 0.5488. That area is expected to attract strong buying interest to bring rebound. But until then, the path of least resistance remains to the downside.

Fed's Miran says drop in neutral rate increases tightness of policy

Fed Governor Stephen Miran said overnight that the neutral rate of interest has likely declined relative to a year ago, making current policy settings "more restrictive than a couple quarters ago."

Speaking at a conference, Miran warned that such "additional tightness" could pose risks ahead, as the lagged effects of monetary policy start to feed through the economy. While he remained upbeat about near-term conditions, he cautioned that if policy isn’t adjusted appropriately, "I do see some risks lurking there."

He also highlighted the challenge of the ongoing U.S. government shutdown, which has deprived policymakers of critical economic data. Miran noted that private-sector indicators are not a "sufficient replacement" and expressed hope that the government will reopen before the October 28–29 FOMC meeting, allowing the Fed to make a data-informed decision.

Meanwhile, Minneapolis Fed President Neel Kashkari voiced concern that incoming data show stagflationary signals, with a slowing labor market and inflation still near 3%. He said the key uncertainty lies in whether tariff-induced price pressures will fade quickly or prove persistent, adding that it is “too soon to reach a firm conclusion.”

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1632; (P) 1.1675; (R1) 1.1701; More...

EUR/USD's fall from 1.1917 resumed by breaking through 1.1644 and intraday bias is back on the downside. Also, the break of 55 D EMA (now at 1.1679) suggests that a medium term top was already formed on bearish divergence condition D MACD. Deeper fall should be seen to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1682 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1778 resistance holds, in case of recovery.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265) and below.

RBNZ Review: OCR Reduced by 50bps to 2.5%, as Expected

- As we expected, the RBNZ cut the OCR by 50bps to 2.50%.

- The decision was reached by consensus, with no vote required.

- The Bank’s commentary suggests further easing is likely in November reflecting significant excess capacity pushing down medium-term inflation.

- Westpac expects a 25bp cut at the 26 November MPS meeting. Further cuts beyond November remain a possibility but not our base case.

- Ahead of the 26 November meeting, the focus will be on the Q3 CPI and labour market reports, and high frequency indicators covering spending, activity and the housing market.

Today the RBNZ’s MPC announced that it had decided to lower the OCR by 50bps to 2.5%. The decision was made by consensus, so no vote was required. This means that the members who voted for a 25bp cut in August shifted to the 50bp camp this time while the new MPC member also shared their view. The MPC’s discussion canvassed two options: a 25bp cut and the 50bp cut.

The RBNZ emphasised signs of significant excess capacity in the economy that give them comfort that medium-term inflation will be well under control. The RBNZ marginally increased their estimate of the degree of excess capacity considering the weak Q2 GDP data but emphasised that a number of one-off or supplydriven factors also drove that weak result. Nevertheless, in line with their message from August, the MPC has little appetite for increased excess capacity – hence the relatively dovish reaction here – especially considering that the RBNZ’s appears to only expect that “…economic activity recovered modestly in the September quarter.”

The RBNZ was notably more positive on the global economic outlook than they have been in recent meetings. This makes sense given the run of more positive data and the general dialling down of concerns around the impact that US tariffs will have on global economic activity. Nevertheless, the RBNZ remains cautious about the global growth outlook next year.

Guidance for the future indicates that further easing seems likely in November – and perhaps beyond given the reference to future “reductions” in the OCR. The degree of guidance is equivocal, and hence further easing will be data dependent. But the language in the final sentence of the Media Release tells us a November easing is more likely than not.

“The Committee remains open to further reductions [our emphasis] in the OCR as required for inflation to settle sustainably near the 2 percent target mid-point in the medium term.”

With the market less than 50% priced for a 50bp easing today, and the RBNZ’s commentary also leaning dovish, the front end of the interest rate curve has rallied (1Y swap falling 12bps; 2Y swap falling 7bps). The NZ dollar has fallen about 1% to 0.5740 and NZD/AUD have fallen around 0.8% to 0.8750. At the time of writing, the market is pricing 27bps of easing for the 26 November meeting.

Westpac expects a 25bp rate cut at the 26 November meeting.

Given our expectations for the data flow over the coming weeks (see below) a further 25bp reduction in the OCR seems more likely than not at the 26 November meeting. This is consistent with our existing forecast.

It is possible that a case could be made for both no change or a 50bp cut in November, depending on the data flow between now and then. The no-change option would come into play should the short-term indicators improve markedly between now and late November. The RBNZ noted in the statement of record that they see the transmission mechanism as still working but needing time. They also noted that indicators of activity recovered “modestly” in the September quarter, which tells us that they would need to see a lot more stronger data before thinking about no change in the OCR in November. A much higher than expected Q3 CPI reading might also prompt a reassessment.

The 50bp option looks more interesting and seems a higher probability should data disappoint. There will be the issue of the long gap between the November and February meetings. If there remains some doubt about the economy’s forward momentum, it is possible that the MPC will elect to insure against the possibility of continued below-trend growth performance over the summer trading period.

Key quotes from the RBNZ’s commentary.

The press statement and record of meeting contained the following notable remarks:

- “The Committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2 percent target midpoint in the medium term.”

- “While inflation is currently near the top of the band, spare capacity is consistent with headline inflation returning towards the target mid-point in the first half of 2026.”

- “There are upside and downside risks to the inflation outlook in New Zealand. Cautious behaviour by households and businesses could slow the economic recovery, reducing mediumterm inflation pressure. Alternatively, higher nearterm inflation could prove to be more persistent.”

- “…the Committee has revised its assessment of current spare capacity only marginally in response to new GDP and activity data, but note that the new data imply some downside risk.”

- “More timely indicators suggest that economic activity recovered modestly in the September quarter, but there remains significant spare capacity in the New Zealand economy.”

- “Slow growth in disposable incomes and house prices continue to weigh on economic activity, but lower interest rates are supporting a recovery in consumption.”

- “Aggregate global trade volumes and economic activity have so far proven resilient... However, growth expectations for 2026 have recovered to a lesser extent, with trading-partner growth expected to slow.”

Things to watch ahead of the 26 November meeting.

Looking ahead to the 26 November MPS, the key domestic economic indicators to watch are:

- The Q3 CPI (released 20 October) and October Selected Prices (17 November). We currently expect CPI inflation to rise to 3.1%y/y in Q3, compared to the RBNZ’s August forecast of 3.0%y/y. The October Selected Prices data will cast light on whether this is likely to be the peak.

- The Q3 labour market surveys (released 5 November). We currently forecast a broadly flat quarter for employment, leading the unemployment rate to nudge up to 5.3%. Our forecast is in line with the RBNZ’s August MPS forecast.

- The Q4 RBNZ Survey of Expectations (released 11 November), Q4 RBNZ Survey of Household Expectations (17 November) and the Q4 RBNZ Survey of Business Expectations (released 18 November). The particular emphasis will be on how inflation expectations are evolving with actual inflation close to 3%y/y.

In addition to these major quarterly releases, we expect the RBNZ will pay close attention to the developments in the BusinessNZ PMIs, consumer spending, the housing market and migration (out in mid-October and mid- November). The various activity and inflation indicators contained in the ANZ business and consumer confidence surveys (released late October) will also be of interest. Aside from domestic economic data, developments in US tariff policy and any clarity regarding how this is impacting the outlook for trading partner growth and inflation will also have an impact on the RBNZ’s deliberations at the November meeting. Movements in world prices for New Zealand’s key commodity exports, alongside movements in the exchange rate, will be important in gauging the extent to which international conditions are impacting the New Zealand economy.

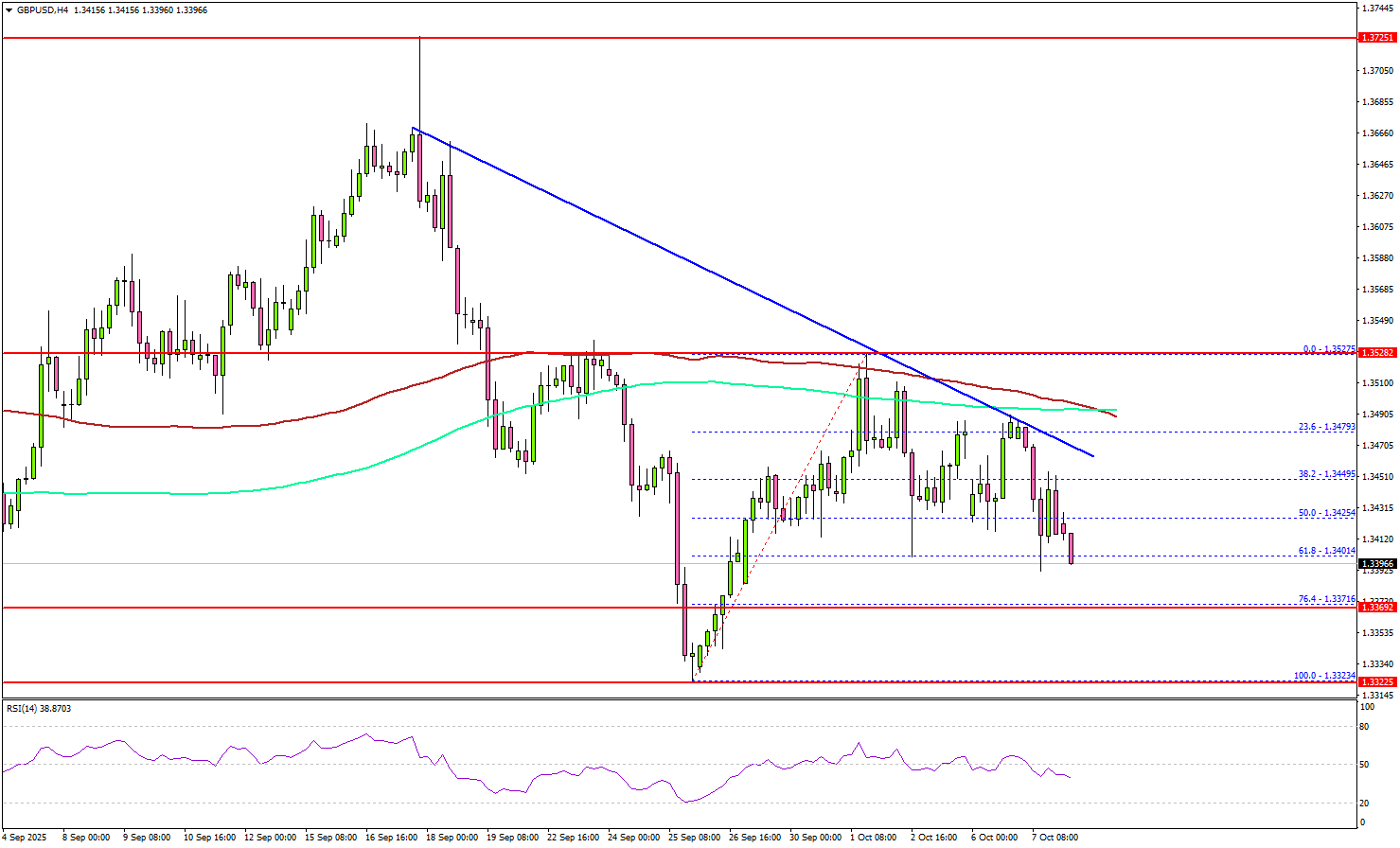

GBP/USD Weakens – Is The Pair Entering A New Downtrend Phase?

Key Highlights

- GBP/USD is struggling to recover above 1.3500.

- A major bearish trend line is forming with resistance near 1.3470 on the 4-hour chart.

- EUR/USD is moving lower and might drop below 1.1620.

- Gold extended gains and rallied to a new record high above $3,980.

GBP/USD Technical Analysis

The British Pound attempted a recovery wave above 1.3450 against the US Dollar. GBP/USD seems to be struggling to settle above 1.3500 and 1.3525.

Looking at the 4-hour chart, the pair traded as high as 1.3527 and recently corrected gains. There was a move below the 1.3480 support. The pair dipped below the 50% Fib retracement level of the upward move from the 1.3323 swing low to the 1.3527 high.

The pair is now trading well below 1.3500, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). Besides, there is a major bearish trend line forming with resistance near 1.3470.

To start a decent increase, GBP/USD must settle above the trend line and 1.3500. The main hurdle could be near 1.3525. A close above 1.3525 could open the doors for a fresh increase. If not, the pair could decline again.

On the downside, there is key support at 1.3370 and the 76.4% Fib retracement level of the upward move from the 1.3323 swing low to the 1.3527 high. The next area of interest might be 1.3350. The main support could be 1.3320. Any more losses might increase selling pressure and send the pair toward 1.3200.

Looking at EUR/USD, the pair attempted to recover, but the bears are still active below the 1.1750 resistance level.

Upcoming Key Economic Events:

- FPC Meeting Minutes.

- FPC Statement.

- Fed's Logan speech.

- FOMC Minutes.

- Fed's Kashkari speech

Fed’s Miran says drop in neutral rate increases tightness of policy

Fed Governor Stephen Miran said overnight that the neutral rate of interest has likely declined relative to a year ago, making current policy settings "more restrictive than a couple quarters ago."

Speaking at a conference, Miran warned that such "additional tightness" could pose risks ahead, as the lagged effects of monetary policy start to feed through the economy. While he remained upbeat about near-term conditions, he cautioned that if policy isn’t adjusted appropriately, "I do see some risks lurking there."

He also highlighted the challenge of the ongoing U.S. government shutdown, which has deprived policymakers of critical economic data. Miran noted that private-sector indicators are not a "sufficient replacement" and expressed hope that the government will reopen before the October 28–29 FOMC meeting, allowing the Fed to make a data-informed decision.

Meanwhile, Minneapolis Fed President Neel Kashkari voiced concern that incoming data show stagflationary signals, with a slowing labor market and inflation still near 3%. He said the key uncertainty lies in whether tariff-induced price pressures will fade quickly or prove persistent, adding that it is “too soon to reach a firm conclusion.”