Sample Category Title

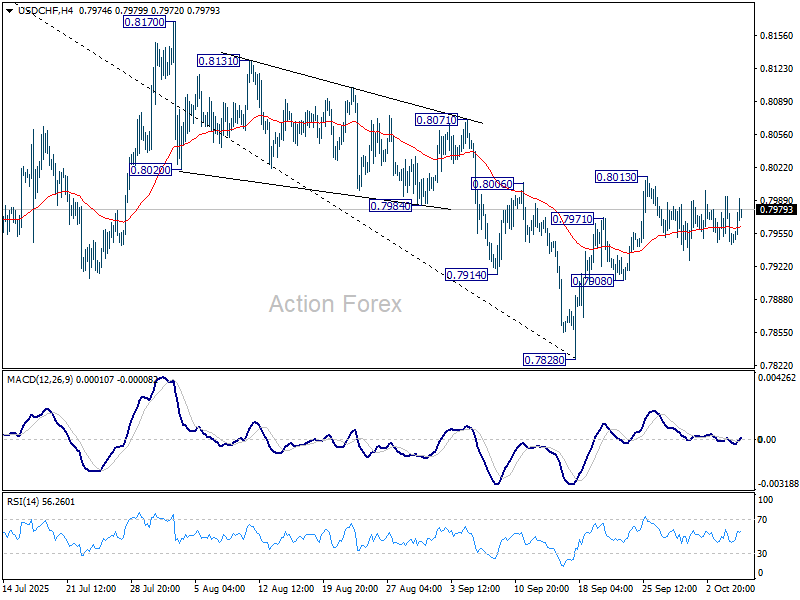

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7932; (P) 0.7963; (R1) 0.7979; More…

Intraday bias in USD/CHF stays neutral as range trading continues. On the upside, sustained trading above 55 D EMA (now at 0.8004) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

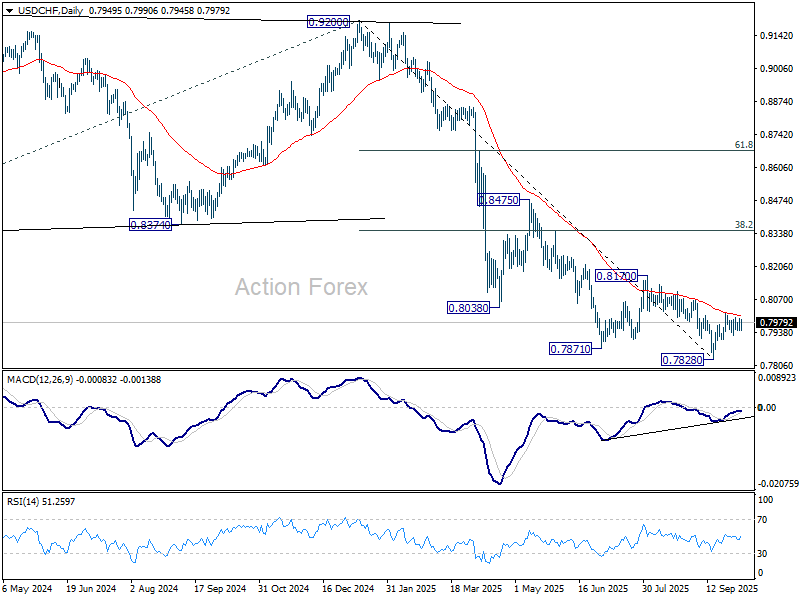

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

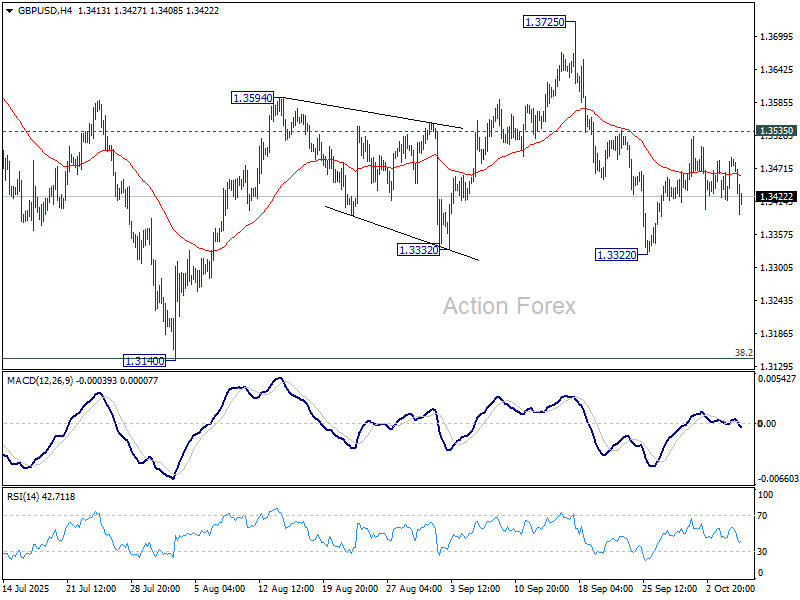

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3437; (P) 1.3464; (R1) 1.3511; More...

Range trading continues in GBP/USD and intraday bias stays neutral. With 1.3535 resistance intact, further decline is mildly in favor. On the downside, break of 1.3322 will resume the fall from 1.3725 to 1.3140 support. On the upside, though, firm break of 1.3535 will argue that pullback from 1.3725 has already completed, and bring stronger rise to retest 1.3725/87 key resistance zone.

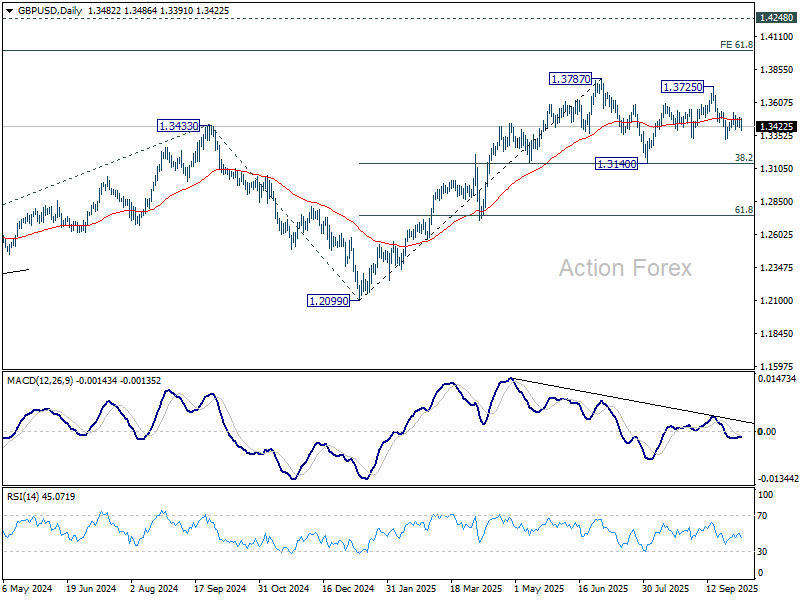

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3176) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

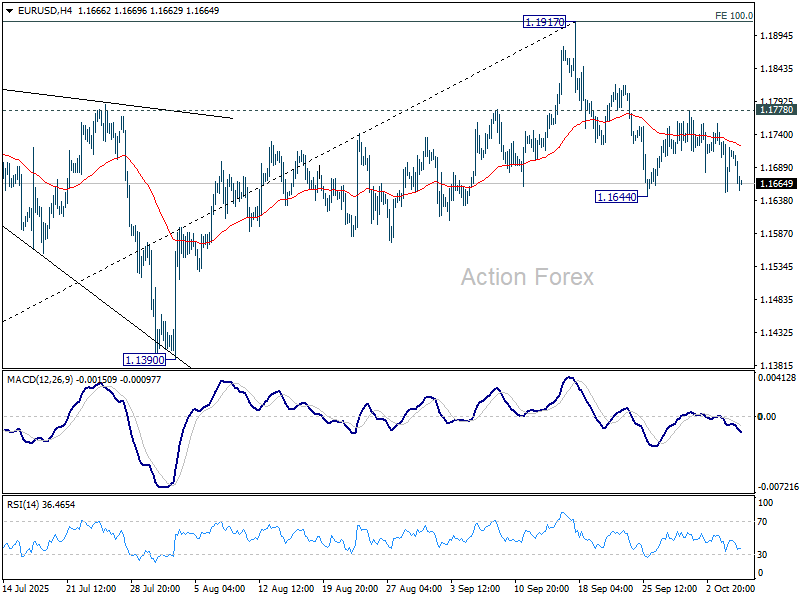

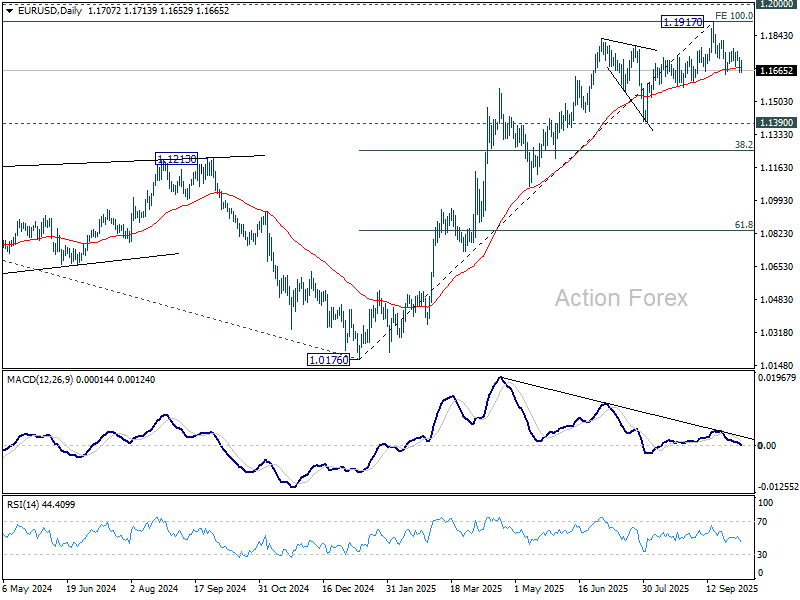

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1668; (P) 1.1699; (R1) 1.1747; More...

EUR/USD is still holding in range above 1.1644 and intraday bias remains neutral. Further decline is mildly in favor as long as 1.1778 resistance holds. On the downside, break of 1.1644 and sustained trading below 55 D EMA (now at 1.1679) will indicate medium term topping at 1.1917, on bearish divergence condition in D MACD. Further fall should then be seen to 1.1390 support. Nevertheless, break of 1.1778 resistance will retain near term bullishness and bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265).

Dollar Steady Ahead of Fed Speeches, RBNZ Decision Looms

Dollar firmed modestly as markets transitioned into early US session. Despite the resilience, it remain skeptical whether the greenback could stage a breakout. While Dollar continues to outperform the struggling Yen, its strength against other currencies is refrained. Against Loonie, the greenback is losing traction as oil prices stabilize. Similarly, Dollar remains range-bound versus Euro Sterling, and Swiss Franc, indicating a lack of fresh catalysts.

A lineup of Fed officials is due to speak later today, including Governors Michelle Bowman and Stephen Miran, who are expected to strike a dovish tone. However, given the elevated uncertainty surrounding growth, tariffs, and fiscal disruptions, other policymakers are unlikely to offer any clear signal on the timing of the next rate cut.

The U.S. government shutdown has entered its seventh day, with Senate Republicans again failing to advance a funding bill. The standoff requires at least eight Democratic votes to clear the procedural hurdle, but negotiations remain deadlocked. The White House has toughened its rhetoric. NEC Director Kevin Hassett said President Donald Trump may soon “take sharp measures” if Congress continues to block funding, warning that extended shutdown could lead to large-scale government layoffs.

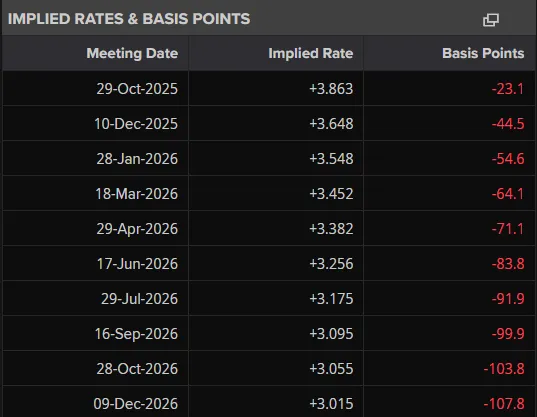

Focus is now turning to New Zealand, where the RBNZ meets early Wednesday. A rate cut is fully priced in, but the size is uncertain. Weak domestic data and subdued business confidence have kept pressure on policymakers to act decisively to restore momentum.

A majority of economists surveyed by Bloomberg (15 of 25) anticipate a 25bps cut to 2.75%, while the rest forecast a 50bps reduction to 2.50%. Given the Q2 GDP contraction, some analysts believe the MPC could opt for a larger move to front-load easing. With uncertainty high and a number of possible outcomes, Kiwi is set for heightened volatility.

For the week so far, Dollar is staying on the top of the performance ladder, followed by Loonie, and then Aussie. Yen is sitting at the bottom, followed by Euro, and then Sterling. Swiss Franc and Kiwi are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.23%. DAX is up 0.13%. CAC is up 0.21%. UK 10-year yield is up 0.007 at 4.748. Germany 10-year yield is up 0.013 at 2.736. Earlier in Asia, Nikkei rose 0.01%. Hong Kong and China were on holidays. Singapore Strait Times rose 1.14%. Japan 10-year JGB yield rose 0.001 to 1.681.

Australia Westpac consumer sentiment slumps to firmly pessimistic level, RBA November cut not assured

Australian consumer sentiment dropped -3.5% mom to 92.1 in October, according to the Westpac-Melbourne Institute survey, erasing all gains seen between May and August when rate cuts briefly lifted confidence. The index has returned to “firmly pessimistic” territory, signaling renewed caution among households.

Westpac said consumers were unsettled by recent inflation updates, with partial indicators suggesting annual price growth has edged back toward the top of the RBA’s 2–3% target range. Signs of stronger consumer demand and a reviving housing market have also stoked speculation that the RBA may not ease policy as quickly as previously expected.

With the RBA meeting scheduled for November 3–4, Westpac noted that a rate cut is “far from assured, though not off the table.” The bank added that the longer the RBA holds off on further easing, the greater the likelihood of deeper cuts later.

NZIER sees two more RBNZ cuts despite signs of inflation pick-up

The New Zealand Institute of Economic Research maintained its forecast for two additional 25bps cuts by the RBNZ at the October and November meetings, despite a mild uptick in inflation pressures during Q3.

In its latest Quarterly Survey of Business Opinion (QSBO), NZIER said a net 11% of firms raised prices, compared with 1% reporting price cuts in the previous quarter, suggesting that cost pressures are firming again. NZIER expects annual CPI inflation to rise slightly above 3% in the near term but sees it drifting back toward the 2% midpoint of the RBNZ’s target range as excess capacity continues to weigh on domestic demand.

Business sentiment, however, softened, with 15% of firms expecting economic improvement, down from 26% in Q2, while 14% reported weaker trading activity in their own businesses. The survey also pointed to declining hiring and investment intentions, as 23% of firms cut staff and a majority plan to reduce capital spending over the coming year.

The mixed picture—firmer inflation but softer demand—supports NZIER’s view that the RBNZ will deliver further easing to stabilize growth, even as it remains alert to temporary inflation volatility.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1668; (P) 1.1699; (R1) 1.1747; More...

EUR/USD is still holding in range above 1.1644 and intraday bias remains neutral. Further decline is mildly in favor as long as 1.1778 resistance holds. On the downside, break of 1.1644 and sustained trading below 55 D EMA (now at 1.1679) will indicate medium term topping at 1.1917, on bearish divergence condition in D MACD. Further fall should then be seen to 1.1390 support. Nevertheless, break of 1.1778 resistance will retain near term bullishness and bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265).

EUR/USD Slides on French Political Turmoil and USD Rebound, Lagarde/Fed Speakers Up Next

EUR/USD continued its slide this morning as a combination of US Dollar strength and concerns around the French political drama rambled on.

The most recent news indicates that President Macron has given the outgoing Prime Minister, Sebastien Lecornu, until Wednesday evening to try and get the divided parliament to agree on a new prime minister.

It is unclear what will happen if Lecornu is unsuccessful, but the likely choices would be either appointing someone who is an expert but not a politician (a technocrat) or calling for early elections.

Resurgent US Dollar Keeps EUR/USD on the Back Foot

The US Dollar has surprised many by its resilience over the past two weeks. What could be the driving force of the Greenback stubbornness at the moment? Let us take a look.

One of the reasons benefitting the US Dollar may be down to the one-week interest rate which is rather expensive. The current rate rests near 4.15%. With a lack of high impact US data, market participants appear to be staying away from the loading up on US Dollar short positions.

Market participants may have also changed their outlook due to an IMF report last week. The prevailing theory of late was that Central Banks were the sellers of US Dollars in April and May, however the IMF data showed the dollar’s share in bank reserves remained about 57% in the second quarter of 2025. That suggests something else could be at work and maybe it was the private sector dumping US Dollar during Q2.

The US Government shutdown has not had the impact many market participants had hoped it would. I think many expected the US Dollar to slide if the shutdown drags on.

The latest predictions show that people are slightly less worried that this shutdown will become the longest ever (which would be more than 35 days); the chance of that happening is now down to 22%.

Nevertheless, markets are scheduled to hear from several officials from the Federal Reserve today, including Bostic, Bowman, and Miran, all speaking between 4:00 PM and 4:30 PM Central European Time (CET).

However, I don't expect their comments to significantly change the market's strong belief that the Fed will cut interest rates two more times before the end of the year.

As things stand, markets are still pricing in around 44.5 bps of rate cuts through December 2025.

Source: LSEG

Technical Analysis - EUR/USD

From a technical standpoint, EUR/USD is approaching a key confluence level which could prove key to the pair's next move.

EUR/USD had broken above a descending trendline from the YTD high, before pushing lower. However, it is approaching the medium term ascending trendline which coincides with a retest of the descending trendline and the 100-day MA around the 1.1626 handle.

A break of this level could see the start of a deeper pullback toward the trendline touch and swing low on August 1, resting just below the pivot price of 1.1450.

Before that, there is support at 1.1584 and 1.1528 which could come into play and provide some short-term relief.

A move higher from here faces resistance at 1.1700 before the 1.1800 swing high and YTD high at 1.1918 comes into focus.

EUR/USD Daily Chart, October 7, 2025

Source: TradingView.com (click to enlarge)

Client Sentiment Data - EUR/USD

Looking at OANDA client sentiment data and market participants are short on the EUR/USD Index with 61% of traders net-short. I prefer to take a contrarian view toward crowd sentiment and thus the fact that so many traders are short means EUR/USD could rise in the near-term.

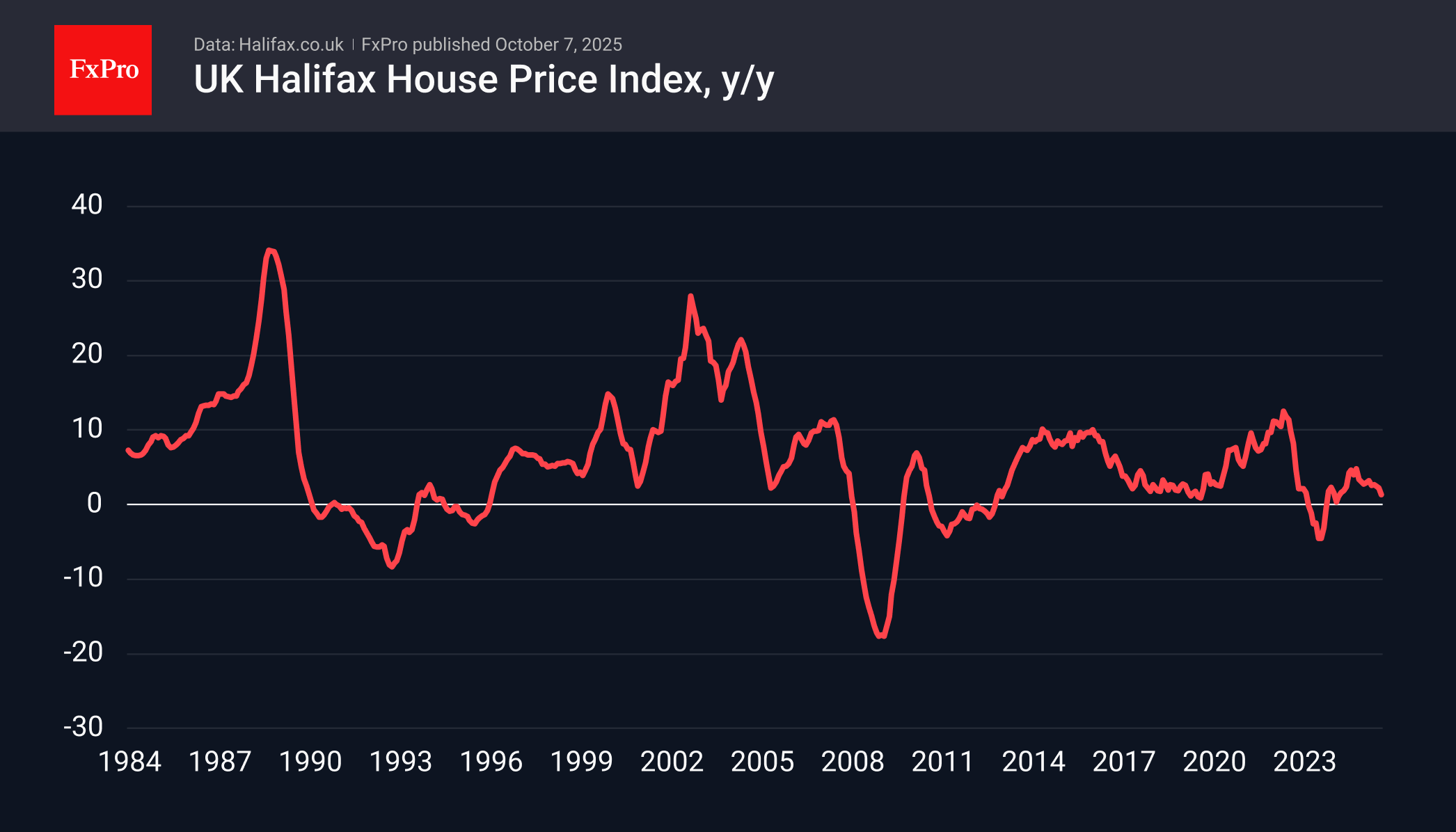

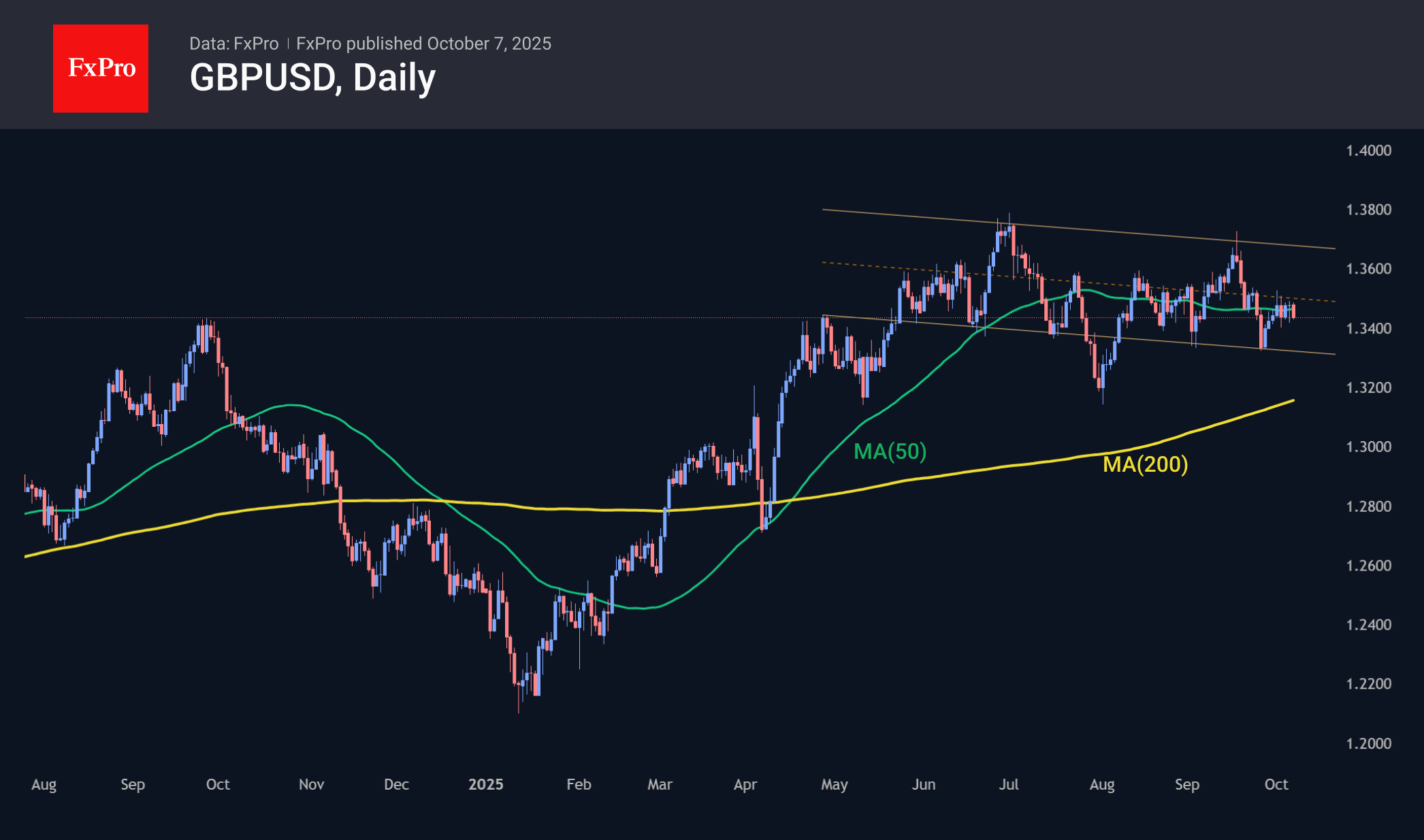

UK House Prices Lag CPI

House prices fell by 0.3% in September after rising by the same amount in August, Halifax reported in its monthly market report. Since the beginning of the year, prices for typical homes have risen by 0.3%, while the annual growth rate has slowed to 1.3%. Compare this with the 2.7% rise in the overall consumer price index since the start of the year and 3.8% year-on-year, and there is little doubt that the UK housing market is not in the best shape. The housing market is often a barometer of consumer demand, and its current state allows the Bank of England to continue easing policy, as the economy is far from overheating.

Against the backdrop of such news, it is not surprising that the pound has weakened, accelerating its decline against the dollar at the start of the day and giving up some of its Monday gains against the euro. Politics has been playing an unusually strong role in currency market dynamics recently. The UK has its own budgetary difficulties, which are deterring investors from capital markets, but so far, they are not as acute as in the US or the eurozone.

GBPUSD is currently at 1.3440, trading in the middle of the range where the pair has been since May, but the upward trend began a gradual reversal in July. The current dynamics resemble consolidation with a wait for the next move, which could be very significant given how long the pair has been moving without a trend. In such conditions, there is a slightly higher chance of a downward reversal. The targets for a deep correction may again be the 1.32 area, where 61.8% of the rally since the beginning of the year and the 200-day moving average coincide. However, in the event of a full-fledged dollar offensive, the pair may roll back to 1.27 by the end of the year, targeting 1.20 by mid-2026.

Nikkei 225: Rallied Above 48,000, Key Levels to Watch Next as New Japanese PM Ignites Bulls

Key takeaways

- Nikkei 225 hits new record high, rising 6.5% since 23 September 2025 amid optimism over Japan’s incoming Prime Minister, Sanae Takaichi.

- Expansionary fiscal policy expected, with higher government spending and increased JGB issuance to boost wages and corporate profits.

- Steepening JGB yield curves continue to correlate positively with the Nikkei 225’s bullish momentum.

- Medium-term bullish bias remains intact, with key support at 45,930 and potential targets between 50,090 and 51,220.

Price actions of the Japan 225 CFD Index (a proxy of the Nikkei 225 futures) have shaped the expected bullish move. All in all, it rallied by 6.5% to hit a fresh intraday all-time high of 48,668 on Monday, 6 October 2025’s US session from 23 September 2025.

The bullish tone has been reinforced by the weekend election of fiscal and monetary dove Sanae Takaichi as the leader of the LDP ruling party in Japan, and she is likely to become Japan's new prime minister.

Let’s now focus on one key macro factor that can further boost the ongoing major and medium-term uptrend phases of the Nikkei 225.

Further steepening of the JGB yield curve

Fig. 1: JGGs yield curve with Nikkei 225 major trends as of 7 October 2025 (Source: TradingView)

The incoming new Japanese premier, Takaichi, a protegée of the late former Prime Minister Shinzo Abe, is considered a pro-fiscal stimulus conservative who is likely to embark on an expansionary fiscal policy to increase Japanese workers’ wages and corporate profits.

Aggressive fiscal expansion is going to be financed by higher Japanese Government Bonds (JGB) issuance, especially via the long-dated JGBs such as the 30-year tenure.

The major bullish breakout (steepening conditions) of the JGB yield curves (both 10-year and 30-year against the 2-year) since June 2022 has a direct correlation with the movements of the Nikkei 225 (see Fig. 1).

The major uptrend phases of the JGB yield curves' steepening remain intact so far, and since Friday, 3 October 2025, the 30-year/2-year JGB yield curve has steepened further by 16 basis points (bps) to 2.38% on Tuesday, 7 October 2025. In addition, the 10-year/2-year JGB yield curve steepened by a lower magnitude of 8 bps to 0.77%.

The continuation of a further steepening of the JGB yield curves is likely to trigger another round of a positive feedback loop in the Nikkei 225.

We shall now turn our attention to the medium-term (1 to 3 weeks) trajectory, key elements, and key levels to watch on the Japan 225 CFD Index from a technical analysis perspective.

Fig. 2: Japan 225 CFD Index medium-term trend as of 7 Oct 2025 (Source: TradingView)

Preferred trend bias (1-3 weeks)

Bullish bias with risk of a minor corrective pull-back to cover Monday, 6 October 2025’s gapped up for the Japan 225 CFD Index.

Medium-term pivotal support at 45,930 for the next potential bullish impulsive up move sequence to materialize for the next medium-term resistances to come in at 50,090/50,220 and 51,030/51,220 (Fibonacci extension clusters) (see Fig. 2).

Key elements

- The price actions of the Japan 225 CFD Index have continued to oscillate within a medium-term ascending channel since the April 2025 low. The upper boundary of the medium-term ascending channel is projected to act as a resistance zone at 50,090/51,220.

- The 45,930 key medium-term pivotal support also confluences closely with the rising 20-day moving average.

- The 4-hour RSI momentum indicator of the Japan CFD Index has reached an extreme overbought level of 87.50 on Monday, 6 October 2025. It's highest overbought level in four years since 6 September 2021. These observations highlight an increased risk of an imminent minor corrective pull-back sequence in the price actions of the Japan 225 CFD Index.

Alternative trend bias (1 to 3 weeks)

A break below the 45,930 key medium-term support for the Japan 225 CFD Index put the bulls on the backseat for a deeper corrective pull-back sequence to unfold to expose the next medium-term supports at 44,485 and 43,210 (also the 50-day moving average).

Yen Hits Two-Month Lows, DXY Continues Advance, Gold Retreats. DAX Eyes Return to Support

Asia Market Wrap - Asian Stocks Advance

Asian stocks advanced as tech stocks continue to drive the rally. It seems the deal between Advanced Micro Devices and OpenAI gave investors a boost.

The MSCI Asian‑Pacific Index was up about 0.3 percent, touching a record level. Japanese shares kept climbing, while worldwide markets also nudged toward peaks. Yet worries about a US government shutdown and turmoil in France seemed to push some people toward safe assets. Gold and Bitcoin both hit fresh highs. A sign that concerns still linger?

Tech firms still anchor the global rise. The AMD‑OpenAI partnership could be another data‑center project this year. It follows Nvidia’s earlier promise to spend up to $100 billion on OpenAI, a move that appears aimed at meeting growing AI demand.

European Session - Shell Jumps as Energy Shares Gain

European stock markets were mostly unchanged on Tuesday, as losses in the industrial and healthcare sectors were balanced out by gains in energy companies and luxury stocks.

The main STOXX 600 index was steady at 570.2 points. French stocks also stabilized after their sharp drop yesterday following the sudden resignation of the Prime Minister. The outgoing Prime Minister is holding final talks with political parties today and tomorrow.

On the downside:

Healthcare stocks fell 0.6%, with major companies like Germany's Bayer and Denmark's Novo Nordisk both dropping around 2%.

Top defense companies, including Rheinmetall and BAE Systems, also lost about 1%.

Helping to support the market:

Oil and gas stocks were boosted, rising 1.9%. Energy giant Shell saw its shares climb after it predicted higher production and better trading results for liquefied natural gas in the third quarter.

Luxury goods companies LVMH and Kering saw their shares rise by 1.8% and 2.2% respectively, after Morgan Stanley upgraded its rating on them.

In company news, discount retailer B&M fell sharply by about 15% after predicting a 28% drop in its core earnings for the first half of the year, leading to a forecast of lower annual profit.

Shares of the major oil company Shell rose 1.9% to 2790.5 pence, making it the second-biggest gainer on the FTSE 100. The company announced several updates. The company raised its forecast for the third quarter's production of Liquefied Natural Gas (LNG) to between 7.0 and 7.4 million metric tons. It also expects that its trading results for the integrated gas division in the third quarter will be significantly higher than they were in the second quarter.

However, Shell also stated it will take a $600 million financial hit due to the cancellation of its Rotterdam biofuels project. Even with this loss, the company's stock has performed well this year, having climbed over 10.5% year-to-date as of its last closing price

On the FX front, the Japanese yen continued to weaken on Tuesday, falling to its lowest level against the dollar in two months.

The yen slid 0.1% to 150.46 per dollar (after touching a low of 150.62). It also hit a fresh all-time low against the euro at 176.35 before regaining some ground. This move comes as attention in Japan shifts to who the new pro-stimulus party leader, Sanae Takaichi, will name to her government.

Meanwhile, the US dollar index edged up 0.1% to 98.23. The euro slipped 0.1% to trade at 1.1694, extending its losses from the previous day. The British pound also weakened 0.1% to 1.3463.

In commodity currencies, the Australian dollar fell 0.1% to 0.6608, and the New Zealand dollar dropped 0.3% to 0.5822.

In the cryptocurrency market, Bitcoin declined 0.7% to 124,334.94, while Ether rose 0.5% to 4,713.78.

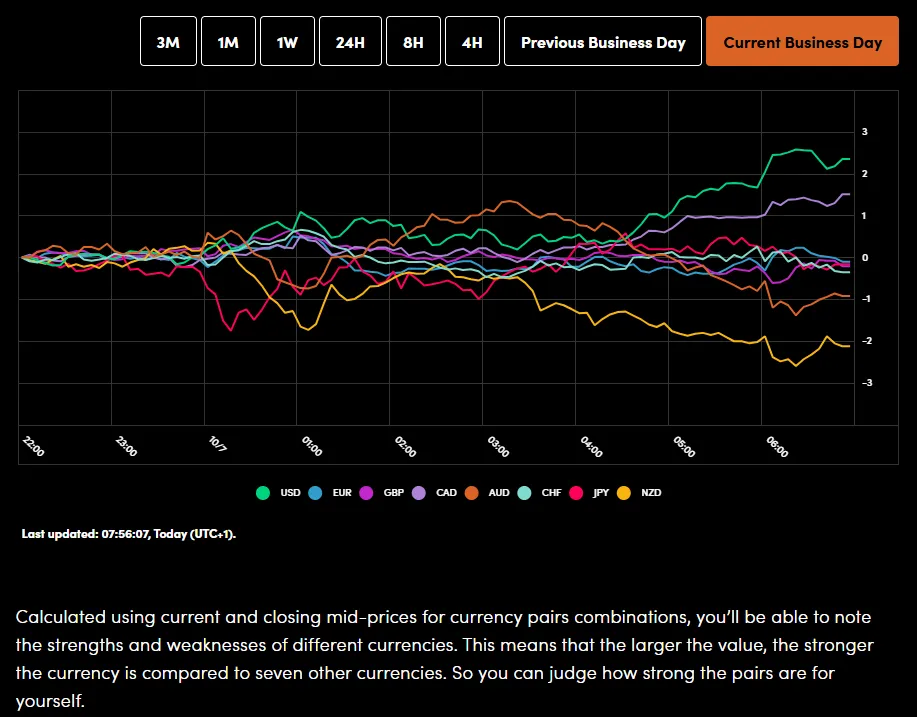

Currency Power Balance

Source: OANDA Labs

Oil prices continued to rise on Tuesday. The rise in Oil prices are largely down to the fact that the OPEC+ group announced a smaller production increase for November than expected, which eased some of the worries about the market having too much supply.

Specifically, Brent crude increased by 0.29% to 65.66 a barrel, and US West Texas Intermediate (WTI) crude climbed 0.31% to reach 61.88 a barrel.

For more on the OPEC + output hike and Oil prices, read OPEC + Delivers Modest Output Hike, Brent Crude Rises 1.7%. What Next for Oil Prices?

Gold prices reached another record high on Tuesday. This surge is due to two main reasons: the ongoing US government shutdown, which shows no sign of ending, and the near certainty that the US Federal Reserve will cut interest rates this month.

Spot gold rose 0.1% to trade at 3,962.63 per ounce, after earlier setting a new all-time high of 3,977.19. US gold futures for December delivery also gained 0.2% to reach $3,985.30.

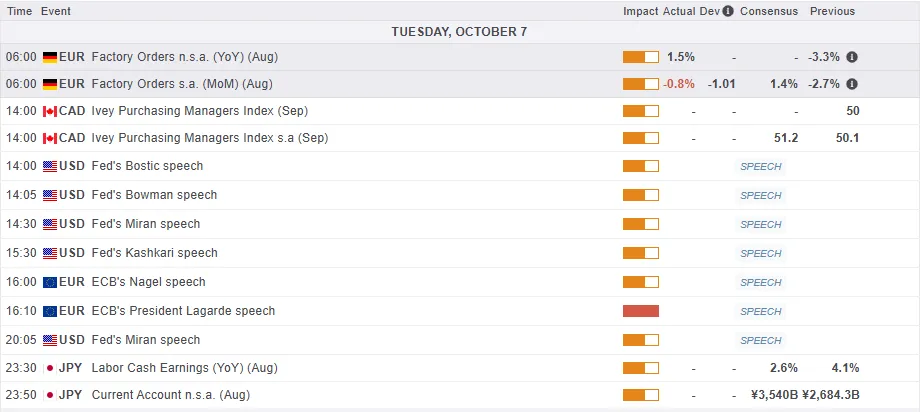

Economic Calendar and Final Thoughts

Looking at the economic calendar, it is a rather quiet day from a data perspective for both the US and European sessions.

The day will be dominated by a host of Central Bank speakers with ECB President Christine Lagarde and the Feds Stephen Miran's comments likely to get the most attention.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - DAX Index

From a technical standpoint, the DAX index has pulled back to the top of the channel it broke out of last week.

This sets the index up for a potential 900 point rally to the upside.

Given that global equities have started the week on the front foot, European equities are lagging which could bode well for the DAX if price can hold above the 24200 level in the early part of the week.

Yesterday we saw a hammer candlestick close on the daily timeframe which does support further upside. However, this morning we are seeing a pullback in the DAX which may present a better risk-to-reward opportunity for would be longs.

Immediate upside resistance for now rests at 24500 before the 24665 swing high from July 10 comes into focus.

A move to the downside will face support at 24200 before the confluence area around 24000 comes into focus.

DAX Index Daily Chart, October 7. 2025

Source: TradingView.com (click to enlarge)

EUR/USD Edges Lower Amid Heightened Political Uncertainty

The EUR/USD pair declined to 1.1706 on Tuesday, weighed down by a confluence of adverse political developments. In the US, the federal government shutdown entered its seventh day, with the Senate once again failing to pass competing funding bills proposed by Democrats and Republicans.

The political stalemate deepened after Democratic leader Chuck Schumer rejected President Donald Trump's claims that negotiations with Democrats were ongoing.

From a monetary policy perspective, recent economic data have reinforced market expectations for further easing by the Federal Reserve. Traders are now almost fully pricing in a 25-basis-point rate cut in October, with another expected in December.

Market participants are awaiting fresh guidance from central bank officials, including scheduled speeches by Governing Council member Stephen Miran on Wednesday and Chair Jerome Powell on Thursday.

The US dollar found additional support from the weakness of its major counterparts. The euro was pressured by political uncertainty in Europe, while the yen softened on the election of a new, moderate prime minister in Japan, who is known to advocate for further accommodative stimulus measures.

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, the pair completed a downward impulse to 1.1652, followed by a corrective rebound to 1.1720. A subsequent decline towards 1.1685 is now forming. Later today, another rise towards 1.1723 is possible; however, the broader bearish structure suggests this will be followed by a further decline to 1.1650. A decisive break below this support level would open the potential for a move down to 1.1600, with a longer-term prospect of 1.1530. This bearish scenario is technically confirmed by the MACD indicator, whose signal line lies below zero and is pointing firmly downwards.

H1 Chart:

On the H1 chart, the market completed a corrective wave towards 1.1720. We anticipate a drop to 1.1680 today, followed by a potential rise to 1.1723. The overall trajectory, however, is expected to resume downwards, targeting 1.1650. A breach of this level would signal the potential for a downward wave to 1.1600, and if that level is breached, a third wave of decline towards 1.1530. This outlook is supported by the Stochastic oscillator, whose signal line is currently below 50 and is trending sharply downwards towards the 20 level.

Conclusion

The EUR/USD remains under pressure, caught between a resilient US dollar supported by Fed policy expectations and its own domestic political concerns. The technical structure remains predominantly bearish, suggesting further losses are likely if key support levels are breached.

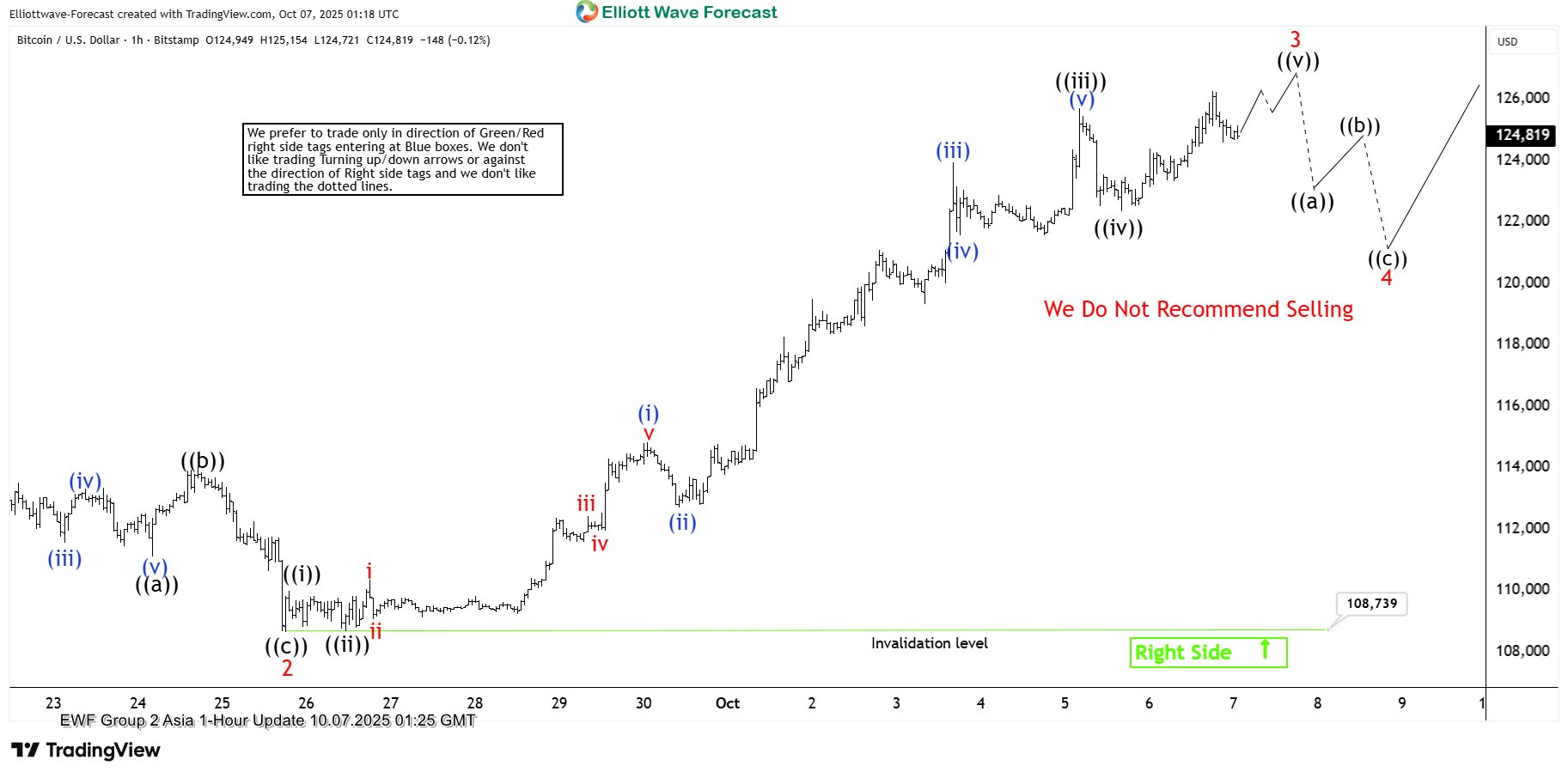

Elliott Wave Forecast: Where Is Bitcoin (BTCUSD) Headed After Record Highs?

The short-term Elliott Wave analysis for Bitcoin (BTCUSD) indicates a five-wave impulse cycle unfolding from the September 1, 2025 low. Wave 1 reached $117,968, and wave 2 corrected to $108,739. Bitcoin then surged to a new all-time high, advancing in wave 3. Within wave 3, sub-wave ((i)) peaked at $109,995. Sub-wave ((ii)) pulled back to $108,676. The rally progressed, with sub-wave ((iii)) hitting $125,725. Sub-wave ((iv)) found support at $122,355, maintaining the bullish structure.

Sub-wave ((v)) is nearing completion, finalizing wave 3 on a higher degree. Following this, wave 4 should correct the rally from the September 25, 2025 low. The uptrend will likely resume in wave 5. As long as the pivot low at $108,676 from September 25 remains intact, dips should find support in a 3, 7, or 11 swing pattern. This support will facilitate further upside. After wave 4 concludes, traders can project the wave 5 target using the 123.6–161.8% inverse Fibonacci retracement of wave 4. This calculation will provide a precise target for Bitcoin’s next rally. The cryptocurrency’s price action reflects strong bullish momentum, suggesting continued growth in the near term.

(Bitcoin) BTCUSD – 60 Minute Elliott Wave Technical Chart:

BTCUSD – Elliott Wave Technical Video:

https://www.youtube.com/watch?v=We0nSMWPv3A