Sample Category Title

Fed’s Miran says drop in neutral rate increases tightness of policy

Fed Governor Stephen Miran said overnight that the neutral rate of interest has likely declined relative to a year ago, making current policy settings "more restrictive than a couple quarters ago."

Speaking at a conference, Miran warned that such "additional tightness" could pose risks ahead, as the lagged effects of monetary policy start to feed through the economy. While he remained upbeat about near-term conditions, he cautioned that if policy isn’t adjusted appropriately, "I do see some risks lurking there."

He also highlighted the challenge of the ongoing U.S. government shutdown, which has deprived policymakers of critical economic data. Miran noted that private-sector indicators are not a "sufficient replacement" and expressed hope that the government will reopen before the October 28–29 FOMC meeting, allowing the Fed to make a data-informed decision.

Meanwhile, Minneapolis Fed President Neel Kashkari voiced concern that incoming data show stagflationary signals, with a slowing labor market and inflation still near 3%. He said the key uncertainty lies in whether tariff-induced price pressures will fade quickly or prove persistent, adding that it is “too soon to reach a firm conclusion.”

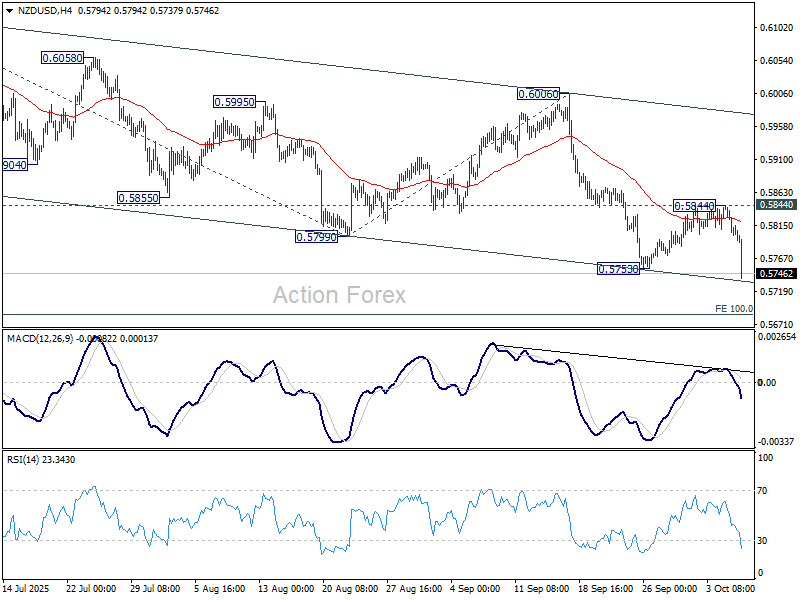

NZD/USD plunges after dovish RBNZ cut; Break below 0.5686 may accelerate losses

NZD/USD tumbled sharply after the RBNZ’s 50bps rate cut to 2.50%, with policymakers retaining an easing bias that signaled scope for further reductions ahead. The policy shift reignited downside momentum in NZD/USD, which broke through 0.5753 support, signaling a renewed leg lower in the ongoing decline from 0.6119.

Technically, near term outlook will stay bearish as long as 0.5844 resistance holds, in case of recovery. The immediate focus is on the bottom of the descending channel near 0.5730, where sustained break would likely drive NZD/USD pair through 100% projection of 0.6119 to 0.5799 from 0.6006 at 0.5686.

Should sellers push beyond 0.5686, NZD/USD could see downside acceleration toward 0.5484 cluster zone, with 161.8% projection at 0.5488. That area is expected to attract strong buying interest to bring rebound. But until then, the path of least resistance remains to the downside.

RBNZ delivers 50bps cut, signals readiness to ease further if needed

RBNZ delivered a larger 50 bps rate cut, lowering the Official Cash Rate (OCR) to 2.50% at today's meeting. The central bank maintained its easing bias, saying it “remains open to further reductions in the OCR” to ensure inflation returns sustainably to 2% over the medium term.

Minutes of the meeting showed the Monetary Policy Committee debated between a 25bps and 50bps move, with the majority favoring a bolder step to mitigate downside risks to medium-term growth and inflation. The Committee judged that prolonged spare capacity warranted a "clear signal" to support consumption and investment, helping anchor expectations amid a slowing economy.

While the Q2 GDP contraction was “considerably larger than expected,” the RBNZ attributed much of the weakness to temporary seasonal factors. It expects the distortion to reverse later in the year and said it does not see the short-term softness as materially altering the broader policy outlook.

The central bank noted that it had only marginally revised down its assessment of spare capacity but acknowledged “some downside risk” to activity. Inflation is projected to converge toward the 2% midpoint in the first half of next year, supported by easing tradables inflation and gradually moderating domestic cost pressures.

(RBNZ) OCR reduced to 2.5%

Media release

Annual consumers price index inflation is currently around the top of the Monetary Policy Committee’s 1 to 3 percent target band. However, with spare capacity in the economy, inflation is expected to return to around the 2 percent target mid-point over the first half of 2026.

Economic activity through the middle of 2025 was weak. In part, this reflects domestic constraints on the supply of goods and services in some industries, and the impact of global economic policy uncertainty. Household consumption is recovering, partly because of lower interest rates, and elevated commodity prices continue to support the primary sector. House prices are flat, and residential and business investment remain weak.

Economic growth in New Zealand’s trading partners is proving resilient, partly because of strong investment in AI-related activity, but is expected to slow in 2026.

There are upside and downside risks to the inflation outlook in New Zealand. Cautious behaviour by households and businesses could slow the economic recovery, reducing medium-term inflation pressure. Alternatively, higher near-term inflation could prove to be more persistent.

On balance, the Committee reached consensus to reduce the OCR by 50 basis points to 2.5 percent. The Committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2 percent target mid-point in the medium term.

Summary record of meeting — October 2025

Annual consumers price index (CPI) inflation remains within the Monetary Policy Committee’s 1 to 3 percent target band. While inflation is currently near the top of the band, spare capacity is consistent with headline inflation returning towards the target mid-point in the first half of 2026.

Annual CPI inflation is expected to converge to the target midpoint

The Committee considers all economic developments as they relate to its medium-term inflation target. Annual CPI inflation is expected to converge to the mid-point of the target range in the first half of next year as tradables inflation pressures dissipate and spare capacity continues to moderate domestically generated inflation.

The Committee noted that headline inflation is projected to have reached 3.0 percent in the September 2025 quarter, reflecting large increases in administered prices, food prices, and the prices of other tradable goods and services. Excluding the influence of administered prices, quarterly non-tradables inflation has continued to decline and is at levels consistent with price stability.

There is significant spare capacity in the domestic economy

The Committee discussed the contraction in GDP in the second quarter of 2025, which was considerably larger than expected. The Committee noted that an unusually large seasonal balancing item contributed to the weakness in the headline figure. This is expected to be reversed during the remainder of the year and is not assumed to have material implications for monetary policy.

Additionally, some industry-specific factors may have constrained supply. For example, high milk prices and unfavourable weather conditions likely contributed to higher livestock retention and lower meat production. Limited access to domestic energy sources and higher energy prices are likely to have weighed on manufacturing more generally. These factors reflect lower supply capacity, rather than weaker demand.

Consequently, the Committee has revised its assessment of current spare capacity only marginally in response to new GDP and activity data, but note that the new data imply some downside risk.

More timely indicators suggest that economic activity recovered modestly in the September quarter, but there remains significant spare capacity in the New Zealand economy.

Lower interest rates will support a recovery in growth

The Committee discussed the transmission of monetary policy. Wholesale interest rates have fallen since the August Statement, particularly at shorter terms. This has resulted in lower rates on business lending, mortgage lending, and term deposits, supporting new borrowing and investment. The average interest rate on existing mortgages is expected to continue to decline over the coming year as mortgage holders re-fix onto lower rates, reducing debt servicing costs for households.

The Committee discussed the outlook for interest-rate-sensitive parts of the economy. Slow growth in disposable incomes and house prices continue to weigh on economic activity, but lower interest rates are supporting a recovery in consumption. Construction activity is projected to recover from mid-2026 as demand for dwellings recovers and house price growth resumes. The Committee expects this to reduce spare capacity in the economy and support an increase in business investment, even as export prices moderate from elevated levels, and government spending declines as a share of the economy.

Trading partner growth has been resilient but is expected to slow

The Committee discussed the impact of trade restrictions and tariffs on the global economy. Aggregate global trade volumes and economic activity have so far proven resilient. Growth forecasts for 2025 have been revised higher for many of our trading partners, particularly for China, Taiwan, and some other Asian economies. This reflects increased investment in AI-related industries, adaptation of trade flows and global supply chains to new tariffs and trade restrictions, and accommodative fiscal and monetary policy in some economies. However, growth expectations for 2026 have recovered to a lesser extent, with trading-partner growth expected to slow.

Global inflation has continued to decline through 2025. Inflation is especially low throughout Asia, and negative in China. Headline inflation in the United States has increased, but evidence suggests that pass-through of tariffs to consumer prices has so far been weaker than expected. To date, there is little evidence of a material impact of tariffs on the prices of New Zealand’s imports or exports. The Committee continues to expect that the total net effect of global tariffs on the New Zealand economy will be disinflationary.

Economic activity in New Zealand has been subdued relative to other economies, resulting in a lower exchange rate. This, together with high commodity export prices, is providing some support to the domestic economy in the very near term, particularly in rural and exporting regions of New Zealand. If sustained, a lower exchange rate may limit the pass-through of lower international prices for imported goods to New Zealand.

There are upside and downside risks to the global growth outlook

The Committee discussed whether recent global developments presented upside or downside risk to inflationary pressure in New Zealand. On the upside, global economic activity has been stronger than anticipated and measures of uncertainty have fallen. In the near term, resilient global demand and a low New Zealand dollar exchange rate may provide more support than expected for New Zealand exports and growth, as well as higher inflation.

On the downside, there is uncertainty about how long elevated equity prices and increased investment activity in the AI technology sector will be sustained. In addition, political and institutional uncertainty in some economies and heightened geopolitical risk may contribute to higher term premia and increased volatility in bond markets. Furthermore, resilient global growth in 2025 may represent a difference in the timing, rather than the extent, of the negative impacts of trade restrictions on growth.

There are upside and downside risks to domestic inflationary pressure

The Committee discussed upside risks to domestic inflation. Businesses continue to face cost pressures from administered prices, such as local council rates, and some energy charges. The Committee’s central expectation is that inflation reached 3.0 percent in the September quarter. Given the two-sided uncertainty around any forecast, there is a material possibility that September quarter inflation was outside the target band. If inflation was to remain higher for longer than expected, there is a risk that this influences inflation expectations and wage- and price-setting behaviour over the medium term.

The Committee discussed the risk that potential output growth could slow by more than currently expected. Growth in potential output is being constrained by subdued investment, low productivity, and low population growth through net immigration. This limits the rate of growth the economy can sustain without generating additional inflationary pressure. In an environment of constrained supply, inflation could stay elevated for longer as demand recovers.

The Committee discussed downside risks to domestic demand and inflation. There remains a risk that excess precaution from households and businesses dampens consumption and investment by more than currently assumed. There is also a risk that declines in short-term interest rates may not provide sufficient support for growth. Borrowing and investment decisions are influenced by interest rates across the entire yield curve, and interest rates at the 5-year tenor have not fallen as far as rates at shorter maturities.

The Committee agreed to reduce the OCR by 50 basis points to 2.5 percent

In light of recent economic developments and the balance of risk, the Committee discussed the options of reducing the OCR by 25 basis points or by 50 basis points at this meeting.

The case for reducing the OCR by 25 basis points emphasised that past reductions in the OCR continue to transmit through the economy and there are signs of recovery in consumption and employment growth. Some members highlighted that constrained supply and cost pressures on businesses present upside risks to inflation. Financial conditions are influenced by the current level and expected future path of the OCR. Reducing the OCR by 25 basis points at this meeting, and signalling that further easing is likely in November, could be sufficient to deliver a sustained economic recovery while giving the Committee confidence that inflation will converge quickly to the 2 percent target mid-point.

The case for reducing the OCR by 50 basis points emphasised prolonged spare capacity and the associated downside risk to medium-term activity and inflation. Domestic inflationary pressures have continued to moderate as projected, giving the Committee more confidence that inflationary pressures are contained. Some members continue to put relatively more weight on the risk that excess precaution by households and businesses and, therefore, subdued economic activity and employment persists. A larger reduction in the OCR could mitigate this risk by providing a clear signal that supports consumption and investment.

On balance, on Wednesday 8 October the Committee reached consensus to reduce the OCR by 50 basis points to 2.5 percent. The Committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2 percent target mid-point in the medium term.

MPC Members: Christian Hawkesby (Chair), Carl Hansen, Hayley Gourley, Karen Silk, Paul Conway, Prasanna Gai

Treasury Observer: James Beard

MPC Secretary: Evelyn Truong

Dow Jones (DJ30) Cools Off All-Time Highs as US Government Shutdown Rumbles on – Potential Targets and Price Forecast

Cooling from all-time highs, the Dow Jones (DJ30) trades 0.33% lower in today’s session, at around $46,594.

Having found support early August, US equities have staged a formidable rally since, despite a somewhat questionable cocktail of macroeconomic themes.

As always, let’s review some macro themes impacting US equity markets, and importantly, consider some potential price targets for this week’s trading.

Dow Jones (DJ30): Key takeaways 07/10/2025

- Staging an impressive rally despite a dubious fundamental outlook, the Dow Jones is retracing from all-time highs in today’s trading, with Caterpillar (CAT), Nike (NKE), and Salesforce (CRM) amongst the worst-performing constituents.

- Despite some downside in today’s session, sentiment on US equities remains generally positive, with complications to Fed monetary policy brought about by the US government shutdown positive for equity markets, somewhat counterintuitively.

- Otherwise, political uncertainty in major world economies, most notably Japan and France, is encouraging risk-averse investors to seek alternative forms of investment, somewhat benefiting US equities

Dow Jones 30 (US30USD), S&P 500 (SPX500USD) and Nasdaq-100 (NAS100USD) YTD, OANDA, TradingView, 07/10/2025

Dow Jones 30 retraces from all-time highs, snapping a six-day bullish streak

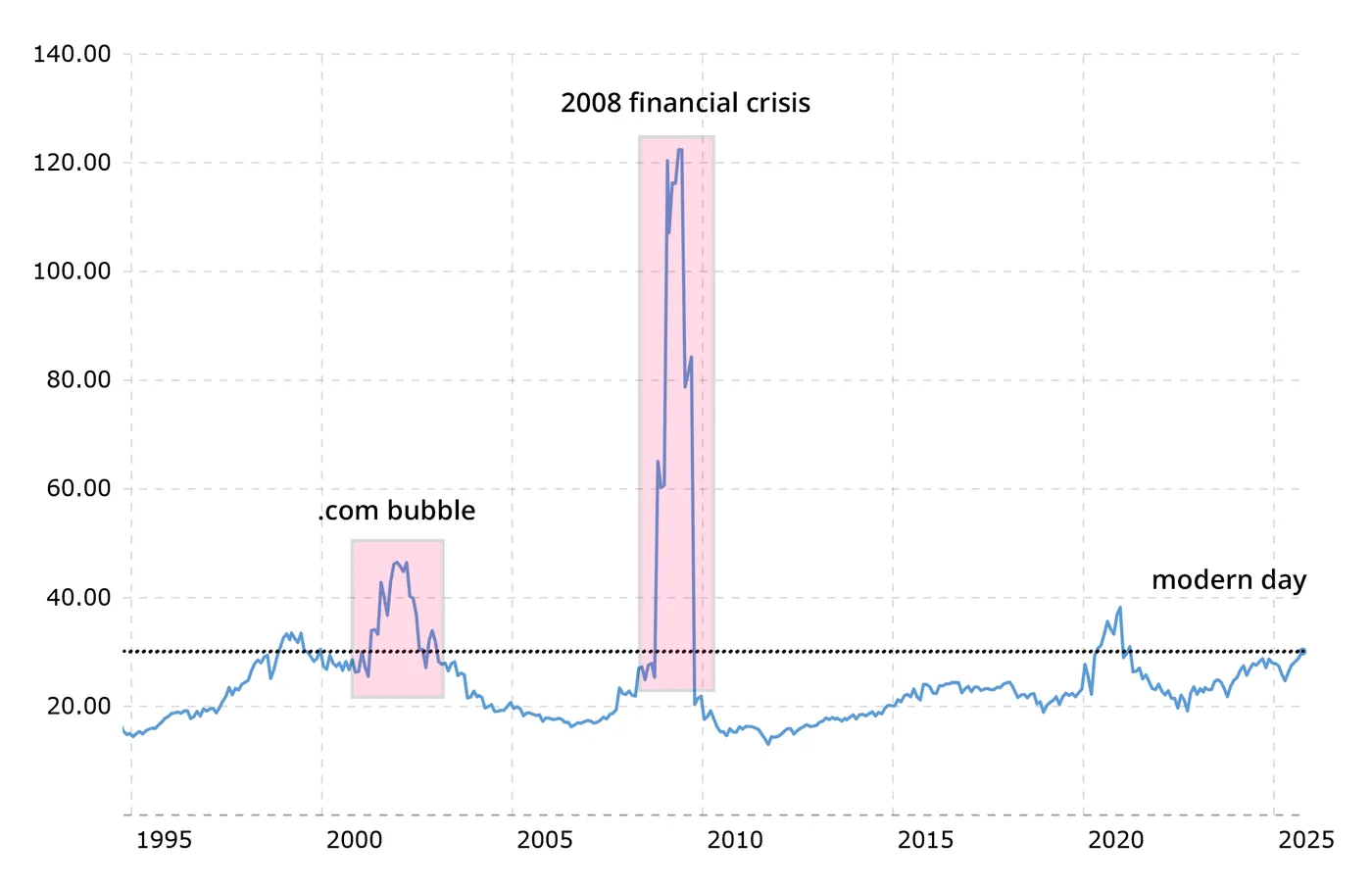

Despite the best efforts of ballooning sovereign debt, an ongoing government shutdown, and stock valuations rivalling the .com bubble, US equities remain at the highs

While the hive mind of the market is not typically known for its ultimate rationality in decision-making, the recent rally in US equity prices, including the Dow Jones, cannot be ignored.

Although prices have cooled somewhat, seemingly due to technical selling, all three major US indices, the Dow Jones 30, S&P 500, and Nasdaq-100, have recently posted all-time highs.

Let’s take a look at the major fundamental themes at play this week:

US government shutdown: As a precursor to the following theme, the US government shutdown should, at least in a vacuum, spell trouble for the current rally in equity pricing. Adding to market uncertainty, undermining confidence in the US government, and suspending non-essential government services, none of these outcomes would typically be viewed as a reason to hold US equities over an alternative.

S&P 500 historical price-to-earnings (P/E) ratio, Macrotrends, 07/10/2025

Fair to say, however, this has not been the case since Tuesday’s shutdown announcement, with prices renewing all-time highs since.

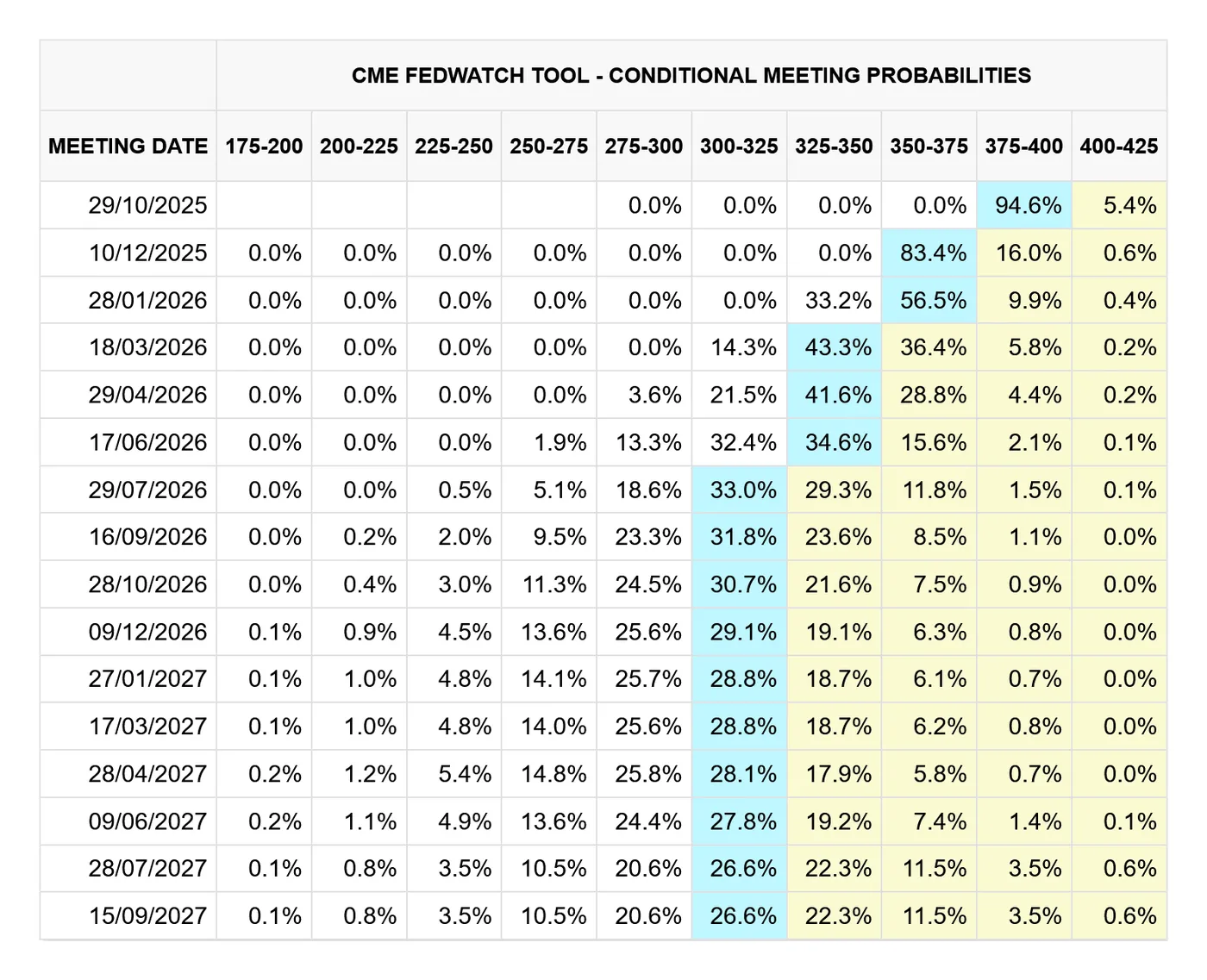

Market conviction on Federal Reserve easing path: While the notion that the Federal Reserve is becoming increasingly dovish is a pre-existing narrative, one of the many knock-on effects of the US government shutdown is further complications to Fed monetary policy.

CME FedWatch, 06/10/2025

Nailing their colours to the mast in 2025 and committing to following objective data when making rate decisions, the current government shutdown has suspended all collection and reporting of economic data by federal agencies, putting the Federal Reserve in a difficult position.

Naturally, it’s challenging to balance the dual mandate of stable pricing and employment when the most recent figures, particularly regarding their reaction to September’s 25-basis-point cut, are entirely unknown.

Ultimately, markets are predicting that a lack of economic data will force the Fed’s hand into performing a second back-to-back interest rate cut, especially considering that September’s NFP report left much to be desired, an outcome Fed Chair Powell will be keen to avoid repeating.

This holds true especially when considering that ADP payrolls, serving as our most recent and reliable private sector gauge of the US labor market, painted a less-than-stellar picture, losing 32,000 jobs in September.

As for US equities, we can consider any suggestion that rates will be lowered in upcoming decisions as positive for pricing, adding some rationale to recent upside.

Rising political uncertainty in major economies: As a brief aside, the change of leadership in Japan and the recent resignation of the French prime minister are contributing to global political uncertainty.

While I’m hesitant to say the United States equity market has entirely maintained its prestige as a global safe haven in recent memory, we can expect substantial political changes in key world economies to inspire risk-averse investors to seek alternative forms of investment, offering a minor boost to US equity pricing.

Dow Jones 30 (US30USD), Nikkei 225 (JP225USD) and CAC 40 (FR40EUR), OANDA, TradingView, 07/10/2025

Dow Jones 30 (DJ30): Technical Analysis 07/10/2025

Let’s now direct our focus to market technicals, starting with the daily, and then concluding with the four-hourly.

Dow Jones 30 (DJ30): Daily (D1) chart analysis (07/10/2025):

Dow Jones 30 (US30USD) D1, OANDA, TradingView, 07/10/2025

With a crossover of the 9 and 21-period moving averages marking the start of the current uptrend, the Dow Jones trades are almost 4.00% higher since.

While the price trades above the current trend line, we are approaching the upper limits of the 20-period Bollinger band, which, so far, correctly suggested that the price needs to retrace towards the baseline before a move higher.

From a technical perspective, if support can be maintained at $46,650, further upside can be expected in the near term.

Price targets and support/resistance levels:

- Price target 1: 78.6% Fib: $47,100

- Support 1: Previous high: $46,450

- Support 2: Consolidation: $45,642

Dow Jones 30 (DJ30): Four-hourly (H4) chart analysis (07/10/2025):

Dow Jones 30 (US30USD) H4, OANDA, TradingView, 07/10/2025

For those with a passion for technical analysis, the H4 Dow Jones chart is a textbook example of a stairstep pattern, providing those with a keen eye plenty of opportunity to get long.

Price targets and support/resistance levels:

- Price target 1: All-time high: $47,102

- Support 1: Previous swing high: $46,508

- Support 2: Bottom of consolidation: $46,157

At current, price looks for support at the trendline, but may slide lower to the lower limit of the 20-period Bollinger band if support can not be found.

To the upside, a clear target would be the previous high of $47,102, although some may view $47,000 as a logical exit point.

USDJPY Wave Analysis

USDJPY: ⬆️ Buy

- USDJPY broke key resistance level 151.00

- Likely to rise to resistance level 153.00

USDJPY currency pair recently broke above the key resistance level 151.00 (former strong resistance from July, which stopped the previous impulse wave 1).

The breakout of the resistance level 151.00 continues the active short-term impulse wave 3 from the middle of September.

Given the clear daily uptrend and the strongly bullish US dollar sentiment seen today, USDJPY currency pair can be expected to rise to the next resistance level 153.00.

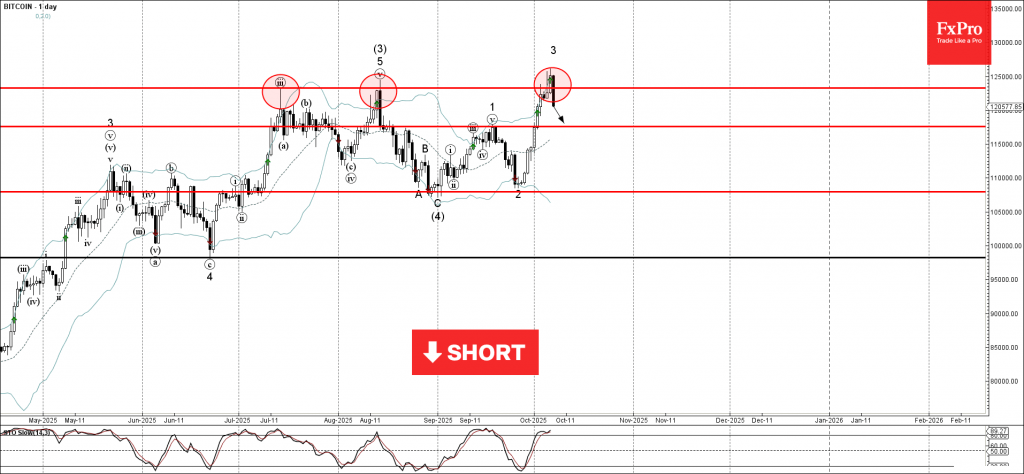

Bitcoin Wave Analysis

Bitcoin: ⬇️ Sell

- Bitcoin reversed from the resistance zone

- Likely to fall to support level 117620.00

Bitcoin cryptocurrency recently reversed down from the resistance zone between the key resistance level 123240.00 (former strong resistance from July and August) and the upper daily Bollinger Band.

The downward reversal from this resistance zone stopped the earlier short-term impulse wave 3 from the end of September.

Given the strength of the resistance level 123240.00 and the overbought daily Stochastic, Bitcoin cryptocurrency can be expected to fall to the next support level 117620.00 (former top of wave 1 from September).

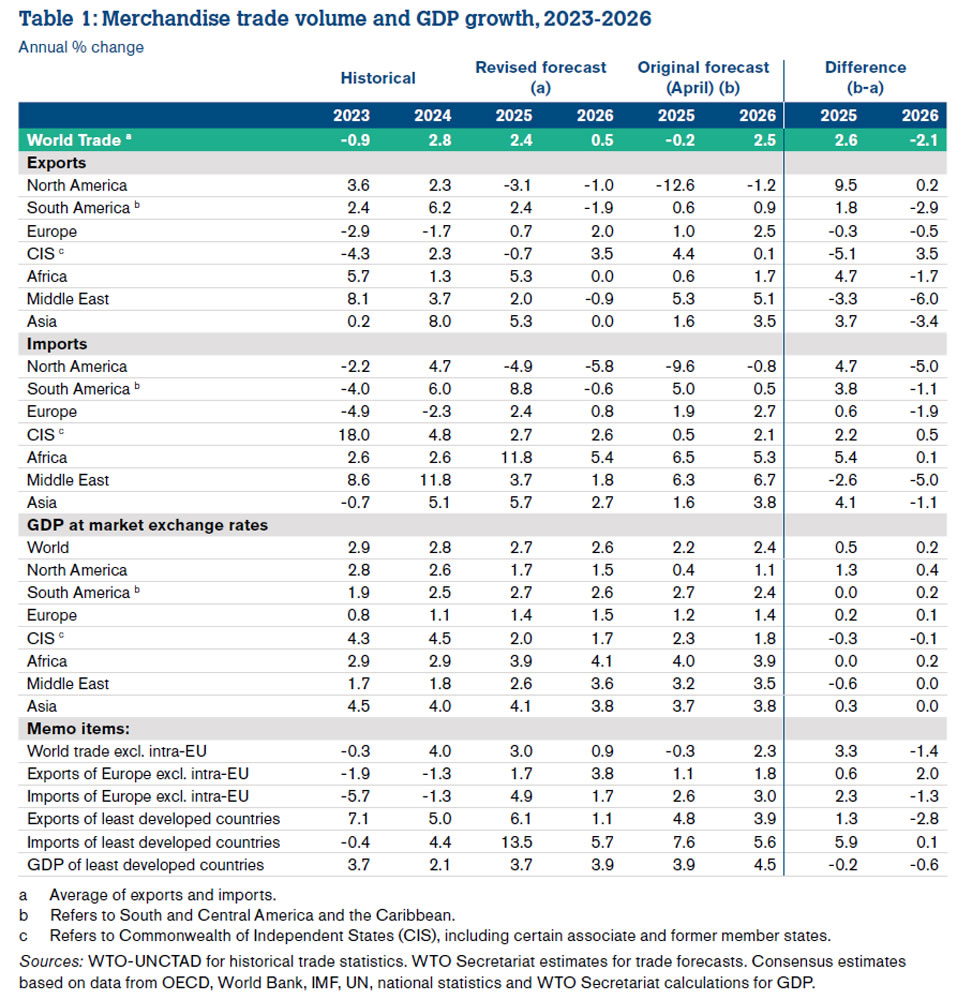

WTO raises 2025 trade growth forecast on AI demand and South-South momentum

The World Trade Organization said today that global merchandise trade outpaced expectations in the first half of 2025, buoyed by strong demand for AI-related products, a surge in North American imports ahead of tariff increases, and resilient trade among emerging economies.

As a result, WTO economists raised 2025 global merchandise trade growth forecast to 2.4%, up from 0.9% projected in August. However, growth is expected to slow sharply to just 0.5% in 2026, reflecting the delayed impact of trade restrictions and slowing global demand. WTO added that services trade is also set to cool, with export growth projected to ease from 6.8% in 2024 to 4.6% in 2025 and 4.4% in 2026.

Director-General Ngozi Okonjo-Iweala credited the improved near-term outlook to countries’ “measured response to tariff changes” and the growth potential of AI, noting that global supply chains are adapting to geopolitical realignments rather than retreating from them.

Okonjo-Iweala highlighted that South-South trade—commerce among developing economies—rose 8% year-on-year in value terms during the first half of 2025, outpacing the 6% increase in overall world trade. Excluding China, South-South flows expanded even faster, up around 9%.

Sunset Market Commentary

Markets

Wherever you look, there’s serious political risk with public finances as the common root cause. A cost of living crisis in Japan and public discontent with the government’s response (ie. relief measures) triggered the demise of the LDP’s majority in both houses of parliament. LDP leader and PM Ishiba had to give way for a fiscal dove, Takaichi, who argued for tax cuts earlier despite the country’s explosive debt situation. The US Congress meanwhile is divided over the continuing resolution to bring an end to the shutdown, which entered its seventh day today. Support of Senate Democrats is needed but they are using their leverage to roll back some of the social security spending cuts Republicans had planned. And then there’s France, home to textbook political unwillingness and/or inability to address a rapidly deteriorating budget situation. Back in the days, when the ECB was still accumulating sovereign bonds en masse, markets weren’t particularly worried about government debt. One pandemic and a structurally changed interest rate environment later, they are way less forgiving for those still living in the past. Outgoing prime minister Lecornu has talks planned with parties today and tomorrow to see what is still possible. But chances for him to find a solution of any kind are extremely slim. It’s merely buying president Macron time to ponder his options. None of them are appealing. The most drastic one, early presidential elections (scheduled for 2027), seems to be the most unlikely one, although pressure is mounting. Edouard Philippe, a former PM and close ally of Macron, suggested during an interview with RTL radio that’s what the president should do. New parliamentary elections on the other hand hold a “terrible risk” of still resulting in a hung assembly and prolonging the crisis. The French swapspread continues to march higher towards the 2025 multiyear high, but in a move shared by European peers. German yields add up to 2 bps at the long end in quiet trading. Treasuries and gilts lack inspiration and trade basically flat on the day. The euro underperforms against an overall stronger USD but recoups some of yesterday’s losses against GBP. EUR/USD eases to 1.167, EUR/GBP advances to but remains below 0.87. Both European stocks and WS eke out slight gains. France’s CAC40 adds 0.2%.

News & Views

Hungarian industrial production in August declined 2.3% M/M (SA and WDA) and was 4.6% lower compared to the same month last year. In the first eight months of the year industrial production was 3.9% lower than in the same period of 2024. The statistical office indicates that production volumes decreased in the manufacturing subsections - except for one - compared to the same month of the previous year. Out of the subsections having the largest weight a significant decrease was observed in the manufacture of transport equipment, while the manufacture of computer, electronic and optical products grew. In the meantime, the disappointing growth performance causes the government to put some pressure on the National Bank of Hungary (MNB) to shift to a more growth supportive policy. Yesterday, Prime Minister Orban already indicated that he saw room for lowering the MNB policy rate. His call today was reinformed by comments from Economy Minister Nagy who assessed that rates are too high and that there is room to lower them even as the MNB aims to reduce inflation and still allowing a stable forint. Despite the ‘growing political pressure’, the MNB director of Monetary policy, Adam Banai, this afternoon repeated that a tight monetary policy is still warranted. Even so, the 2-y Hungarian swap rate today declines 8 bps (to 6.18%). The forint made a step backward currently trading near EUR/HUF 392 compared to a below EUR/HUF 389 this morning.

According to UK Mortgage lender Halifax, house prices in the country in September declined 0.3% M/M. This reduced the Y/Y-growth rate to 1.3%, the slowest pace since April 2024. Halifax said that “This slight monthly dip in house prices reflects a housing market that has remained broadly stable, prices are up +0.3% since the start of the year’. Halifax indicates that affordability remains a challenge, but a relative lower mortgage rate environment and steady wage growth are seen helping support buyer confidence.