Sample Category Title

Dollar Slips as Fed Cut Bets Surge on ADP, Yen and Sterling Firm

Dollar weakened broadly in early US trade after a sharp miss in the ADP employment report. The data amplified concerns that US job growth is faltering, and rate markets reacted swiftly. A quarter-point Fed cut this month is now fully priced in, while the odds of another cut in December have jumped to nearly 90%.

However, the picture remains incomplete. The more comprehensive nonfarm payrolls report, which could confirm or challenge the ADP signal, may not be released if the US government shutdown persists. The closure — the first since 2018–19 — is going to disrupt data flows. Unless lawmakers strike a funding deal in the coming days, both Friday’s payrolls and Thursday’s weekly jobless claims could be delayed. Such an outcome would leave both the market and Fed officials flying blind, unable to validate the extent of labor market weakness.

In contrast, Yen extended its rally, with speculation intensifying that the BoJ could raise rates at its October 30 meeting. Today's Tankan survey showed resilience in manufacturing despite tariff headwinds, adding weight to the hawkish case. Traders now assign a 40% chance of a quarter-point hike later this month. Attention will turn to speeches by Deputy Governor Shinichi Uchida on Thursday and Governor Kazuo Ueda on Friday. Their tone could be pivotal in confirming whether October is a genuine option, or if markets should expect a move later in the year.

Sterling has also gained ground, buoyed by reports that senior Labour figures are no longer ruling out increases in income tax, VAT, or employee national insurance — traditionally viewed as politically untouchable. Any adjustment here could provide the fiscal headroom needed to stabilize finances. Though, confirmation will have to wait until the November 26 budget.

Overall, Yen leads today’s FX performance, with Kiwi and Pound following. At the bottom,Loonie trails, alongside Swiss Franc and Dollar. Euro and Aussie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.68%, at new record. DAX is up 0.33%. CAC is up 0.37%. UK 10-year yield is down -0.009 at 4.692. Germany 10-year yield is down -0.005 at 2.711. Earlier in Asia, Nikkei fell -0.85%. Hong Kong and China were on holiday. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.002 t o 1.653.

US ADP payrolls drop -32k, small firms bear the brunt

US ADP private payrolls fell by -32k in September, far below expectations for a 50k increase and marking the steepest drop in two and a half years. August’s figures were also revised down to a loss of -3k from an initially reported gain of 54k.

The breakdown showed broad-based weakness. Service providers cut -28k jobs, while goods producers shed -3k. Small businesses were hit hardest, losing -40k positions, whereas large firms with 500 or more employees managed to add 33k.

ADP’s chief economist Nela Richardson said the data “further validates what we’ve been seeing in the labor market, that US employers have been cautious with hiring.”

Despite the slowdown, wage growth held steady. Average pay rose 4.5% yoy in September, little changed from August. However, the pace for job changers eased to 6.6% yoy, down half a percentage point, suggesting wage momentum is beginning to cool alongside weaker employment growth.

BoE’s Mann warns inflation persistence playing out

BoE policymaker Catherine Mann said today that keeping rates on hold is “appropriate for the current period,” and warned that the risk of sticky inflation remains elevated. Speaking to Bloomberg TV, she flagged “drift in inflation expectations” as a key concern, noting that it reinforces the persistence of price pressures.

Mann argued that the scenario outlined earlier this year — one where inflation risk lingers longer than expected — is now “playing out.” She added that the UK’s supply side continues to pose challenges for both the economy and policymakers, making it harder to fully restore price stability.

On trade, Mann said she does not yet see diversion effects feeding through as the “tariff landscape continues to be shifting." “The domestic component is the more important issue that I need to face,” she said.

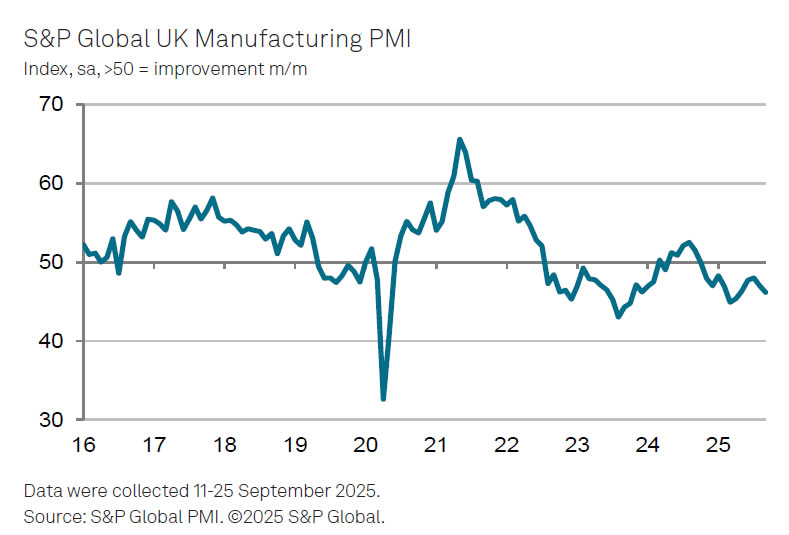

UK PMI manufacturing at 46.2, sector struggles with more worrying news

The UK manufacturing sector slipped further into contraction in September, with the PMI finalized at 46.2, down from 47.0 in August and marking a five-month low. Rob Dobson, Director at S&P Global Market Intelligence, called the results “further worrying news” for industry, pointing to weak demand, fading export orders, and a high-cost environment amplified by rising taxes and labor costs.

The report noted that the tough backdrop is eroding business confidence. Firms have now shed jobs for 11 consecutive months, with many cutting back on purchasing and non-essential spending. Sentiment about the year ahead remains subdued.

There were some glimmers of hope. Firms highlighted that lean inventories and potential easing in global trade tensions could lift output in the months ahead. Input costs are also rising at a slower pace, which may give the BoE scope to cut rates later this year.

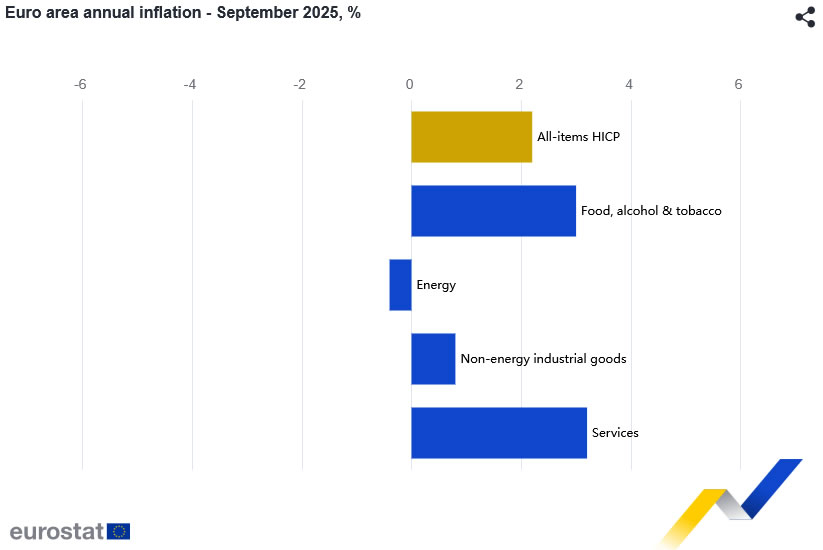

Eurozone inflation ticks higher to 2.2%, core steady 2.3%

Eurozone headline inflation edged up in September, with CPI rising to 2.2% yoy from 2.0% yoy in August, in line with expectations. Core CPI, which excludes energy, food, alcohol and tobacco, held steady at 2.3% yoy, suggesting underlying price pressures remain sticky even as the energy drag eases.

By component, services posted the highest annual inflation at 3.2%, slightly higher than August’s 3.1%. Food, alcohol and tobacco slowed to 3.0% from 3.2%. Non-energy industrial goods were unchanged at 0.8%. Energy prices continued to decline, though the contraction moderated to -0.4% from -2.0%.

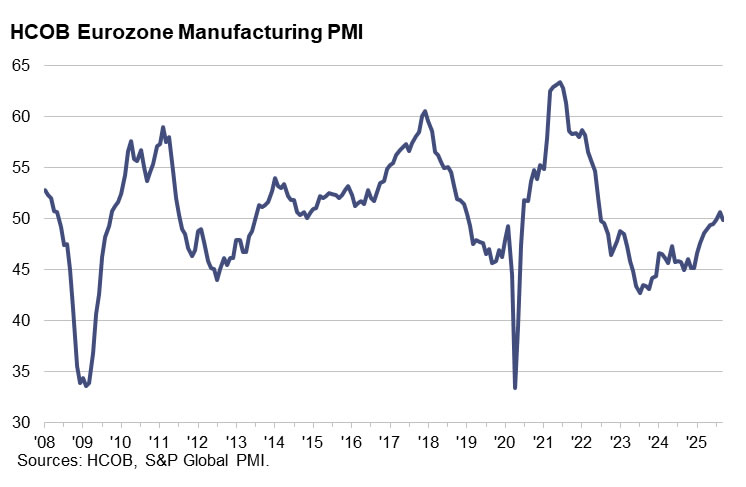

Eurozone PMI manufacturing at 49.8, stagnation can be viewed positively

Eurozone manufacturing activity edged back into contraction in September, with the PMI finalized at 49.8, down from August’s 50.7. Output slowed as well, with the production index falling from 52.5 to 50.9, pointing to weaker factory momentum across the bloc.

Country data painted a mixed picture. The Netherlands stood out with a 38-month high of 53.7, while Ireland and Greece also held above 50. Spain remained in expansion at 51.5 but slowed to a three-month low. Germany, France, and Italy — the region’s largest economies — all stayed below 50, signaling their industrial recessions are easing but not yet over.

Cyrus de la Rubia of Hamburg Commercial Bank said the “stagnation observed in the manufacturing sector can also be viewed positively,” given headwinds from US tariffs, political uncertainty in France and Spain, and high energy costs. He noted the sector is “holding up surprisingly well,” though confidence remains lower than the decade average.

Japan's Tankan shows resilience, supports BoJ tightening outlook

Japan’s Q3 Tankan survey showed large manufacturers growing more confident, with the index rising from 13 to 14, in line with expectations and the highest since Q4 2024. While the manufacturing outlook held steady at 12, suggesting some softening ahead, sentiment remains resilient despite trade headwinds.

Non-manufacturing confidence also stayed firm, with the index unchanged at 34, beating forecasts, and the outlook improving to 28 from 27.

Large firms signaled robust investment plans, projecting a 12.5% increase in capital expenditure for the fiscal year to March 2026, up from June’s forecast of 11.5%.

The results suggest Japan’s economy is weathering tariff pressures and steady domestic demand continues to support activity. For the Bank of Japan, the data bolster expectations that further tightening is coming — the debate is less about if and more about when policymakers will move.

Japan PMI manufacturing finalized at 48.5, weak demand from China and US

Japan’s manufacturing sector contracted further in September, with the PMI finalized at 48.5, down from August’s 49.7. S&P Global’s Annabel Fiddes said the sector ended Q3 “on a weaker note,” as output and new orders declined at a faster pace, driven by softer demand across key markets such as China and the drag from US tariffs.

Weaker demand weighed on business confidence, leading firms to scale back activity. Employment expanded at the slowest pace since February, while purchasing activity dropped at the second-steepest rate since early 2024. The cautious stance underscores concern that the sector may “struggle to see much growth in the near term.”

Price dynamics offered some relief, with cost pressures “less pronounced” than earlier in the year. Still, selling prices rose at a "historically strong pace" as firms sought to protect margins.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3418; (P) 1.3442; (R1) 1.3471; More...

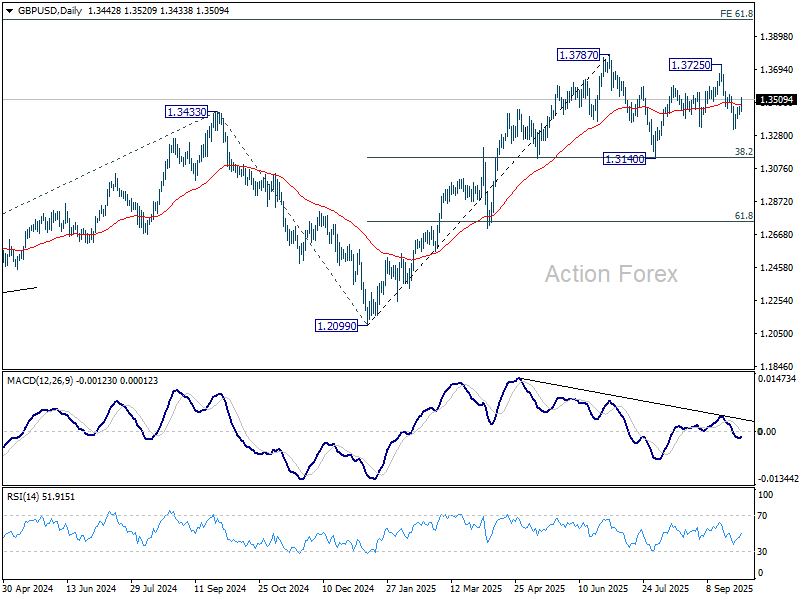

Focus is back on 1.3535 resistance in GBP/USD with today's extended rebound. Firm break there will target 1.3725/87 key resistance zone. On the downside, though, break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

US ADP payrolls drop -32k, small firms bear the brunt

US ADP private payrolls fell by -32k in September, far below expectations for a 50k increase and marking the steepest drop in two and a half years. August’s figures were also revised down to a loss of -3k from an initially reported gain of 54k.

The breakdown showed broad-based weakness. Service providers cut -28k jobs, while goods producers shed -3k. Small businesses were hit hardest, losing -40k positions, whereas large firms with 500 or more employees managed to add 33k.

ADP’s chief economist Nela Richardson said the data “further validates what we’ve been seeing in the labor market, that US employers have been cautious with hiring.”

Despite the slowdown, wage growth held steady. Average pay rose 4.5% yoy in September, little changed from August. However, the pace for job changers eased to 6.6% yoy, down half a percentage point, suggesting wage momentum is beginning to cool alongside weaker employment growth.

EUR/USD: Euro Bulls Ignite as US Government Shuts Down

Key takeaways

- The US government shutdown, the first in nearly seven years, heightens political uncertainty ahead of the 2026 midterm elections.

- Past shutdowns show the US dollar tends to weaken during and after such impasses, with the 2018 episode triggering a 2% decline.

- Rising unemployment and Trump’s threat of mass layoffs increase bets for Fed rate cuts in October and December 2025.

- The Eurozone/US policy rate spread is steepening, reinforcing upside momentum in EUR/USD.

The US government has officially entered a shutdown in nearly seven years today, 1 October 2025, after Senate Republican and Democratic leaders remained locked in a stalemate over health care subsidies and engaged in brinkmanship maneuvers to frame the 2026 midterm elections.

The previous shutdown occurred in late December 2018 during President Trump’s first term, which lasted for 34 days, the longest US government shutdown in history since 1976.

Based on the data compiled by Bloomberg for the last three shutdowns, in 2013, early 2018, and late 2018, the US dollar drifted lower (Bloomberg Dollar Spot Index) both during the impasse and in the aftermath of the shutdowns.

The late 2018 episode produced the most pronounced bout of US dollar weakness; the greenback shed around -2% during the shutdown period of 34 days.

Right now, let's examine one key macro factor that is likely to support the ongoing medium-term uptrend phase of the EUR/USD in light of the latest US government shutdown.

Risk of a spike in the US employment rate leads to a more dovish Fed

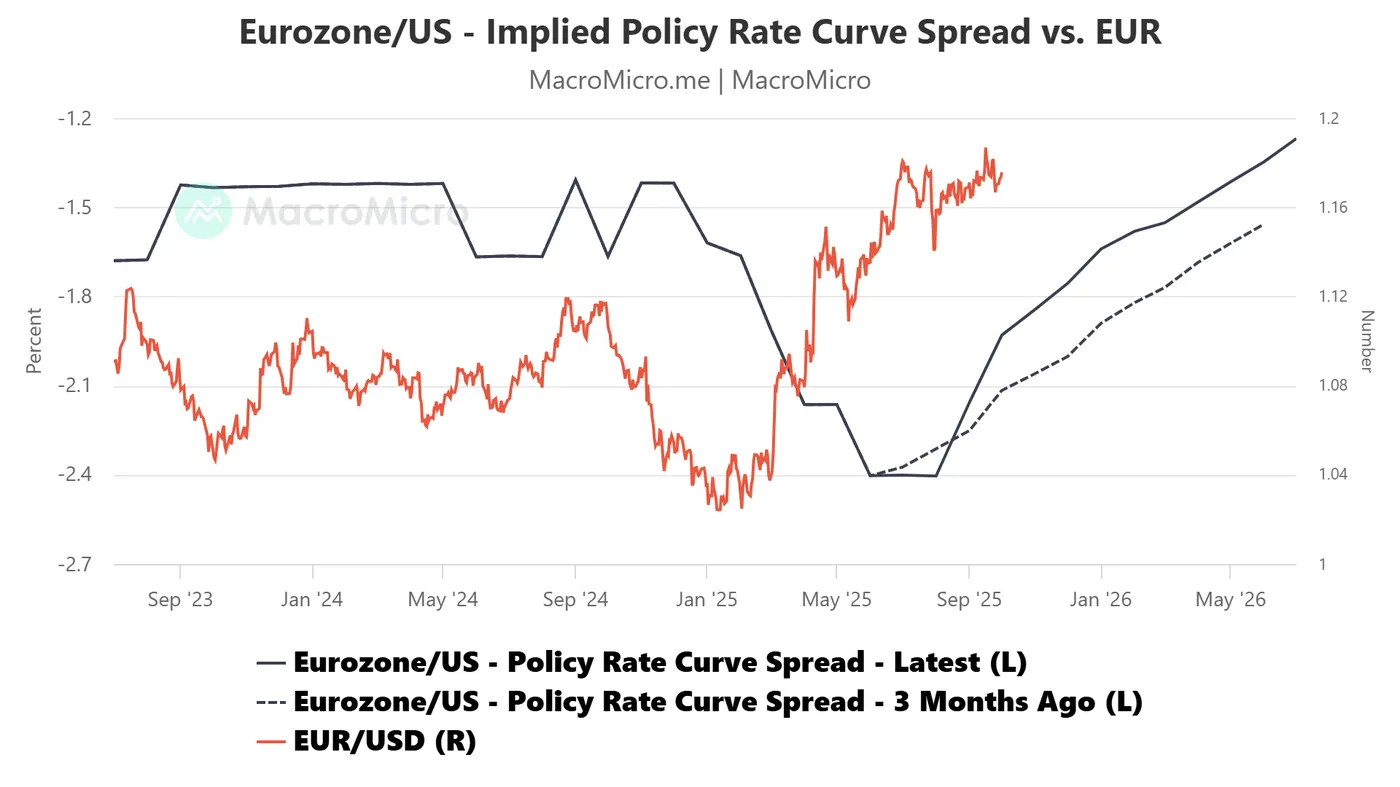

Fig. 1: The Eurozone/US implied policy interest rate curve spread with EUR/USD as of 30 Sep 2025 (Source: MacroMicro)

To heighten brinkmanship ahead of the 2026 US midterm elections, President Trump suggested his administration could leverage the shutdown to pursue mass layoffs of government employees, going beyond the temporary furloughs already affecting an estimated 750,000 personnel.

The current unemployment rate in the US has increased to 4.3% in August 2025 from 4.2% in July, its highest level since October 2021. Hence, the unemployment rate could spike higher if the shutdown lasts for more than a week, with the mass layoffs proposed by Trump.

The Fed funds futures market has started to price in a bleak US labour market condition that triggers an increase in bets for two more Fed rate cuts in the October and December FOMC meetings before 2025 ends

Based on the latest data from the CME FedWatch tool, the odds of a 25 basis points (bps) cut to reduce the Fed funds rate to 3.75%-4.00% on the 29 October FOMC meeting have increased to 95% from 90% a day ago.

Also, the odds have risen to a 75% chance of another 25 bps rate cut in the 12 December 2025 FOMC meeting to bring the Fed funds rate lower to 3.50%-3.75% from around 58% chance recorded previously ex-post 17 September 2025 FOMC meeting.

All in all, the increase in Fed rate cut bets has led to the Eurozone/US implied policy interest rate curve spread to inch higher to -1.84% in November 2025 from -1.93% in October 2025 and rose steadily in the next few months to be at -1.55% by March 2026. Also, the curve spread has shifted upwards from three months ago (see Fig. 1).

The steepening of the Eurozone/US implied policy interest rate curve spread is likely to assert upside pressure in the EUR/USD.

Let’s now examine the latest technical factors on the EUR/USD to determine the next potential short-term (1 to 3 days) trajectory and its key levels to watch.

Fig. 2: EUR/USD minor trend as of 1 Oct 2025 (Source: TradingView)

Fig. 3: EUR/USD medium-term & major trends as of 1 Oct 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

Bullish bias with key short-term pivotal support at 1.1680 for the EUR/USD. A clearance above 1.1760 increases the odds of a new minor bullish impulsive up move sequence for the next intermediate resistances to come in at 1.1820, 1.1860, and 1.1910 in the first step (see Fig. 2).

Key elements

- The EUR/USD exited from the minor descending channel resistance on Monday, 29 September 2025, and traded back above its 50-day moving average. These observations suggest that the minor corrective decline sequence from its 17 September 2025 ex-post FOMC high to 25 September 2025 low of 1.1645 is likely to have ended (see Fig. 2).

- The hourly RSI momentum indicator of the EUR/USD has managed to hover above a horizontal support at the 46 level, which suggests a potential build-up of short-term bullish momentum (see Fig. 2).

- The yield spread between the 2-year German Bund and the US Treasury note has just staged a bullish breakout on Tuesday, 29 September 2025, at the time of writing. It narrowed to -1.57% as of Wednesday, 1 October 2025, at the time of writing, from -1.7% printed on 25 September 2025 (see Fig. 2).

- This development indicates a relative decline in the yield attractiveness of the 2-year US Treasury versus its German counterpart, which in turn exerts downside pressure on the US dollar against the euro (see Fig. 2).

- The EUR/USD has continued to oscillate above a medium-term ascending trendline in place since the 3 February 2025 low, coupled with a recent bullish momentum reading seen in its daily RSI momentum indicator. These observations support the ongoing medium-term uptrend phase of the EUR/USD (see Fig. 3).

Alternative trend bias (1 to 3 days)

Failure to hold at the 1.1680 short-term key support invalidates the bullish scenario on the EUR/USD to expose the next intermediate supports at 1.1630/1.1615 and 1.1570 (the medium-term pivotal support).

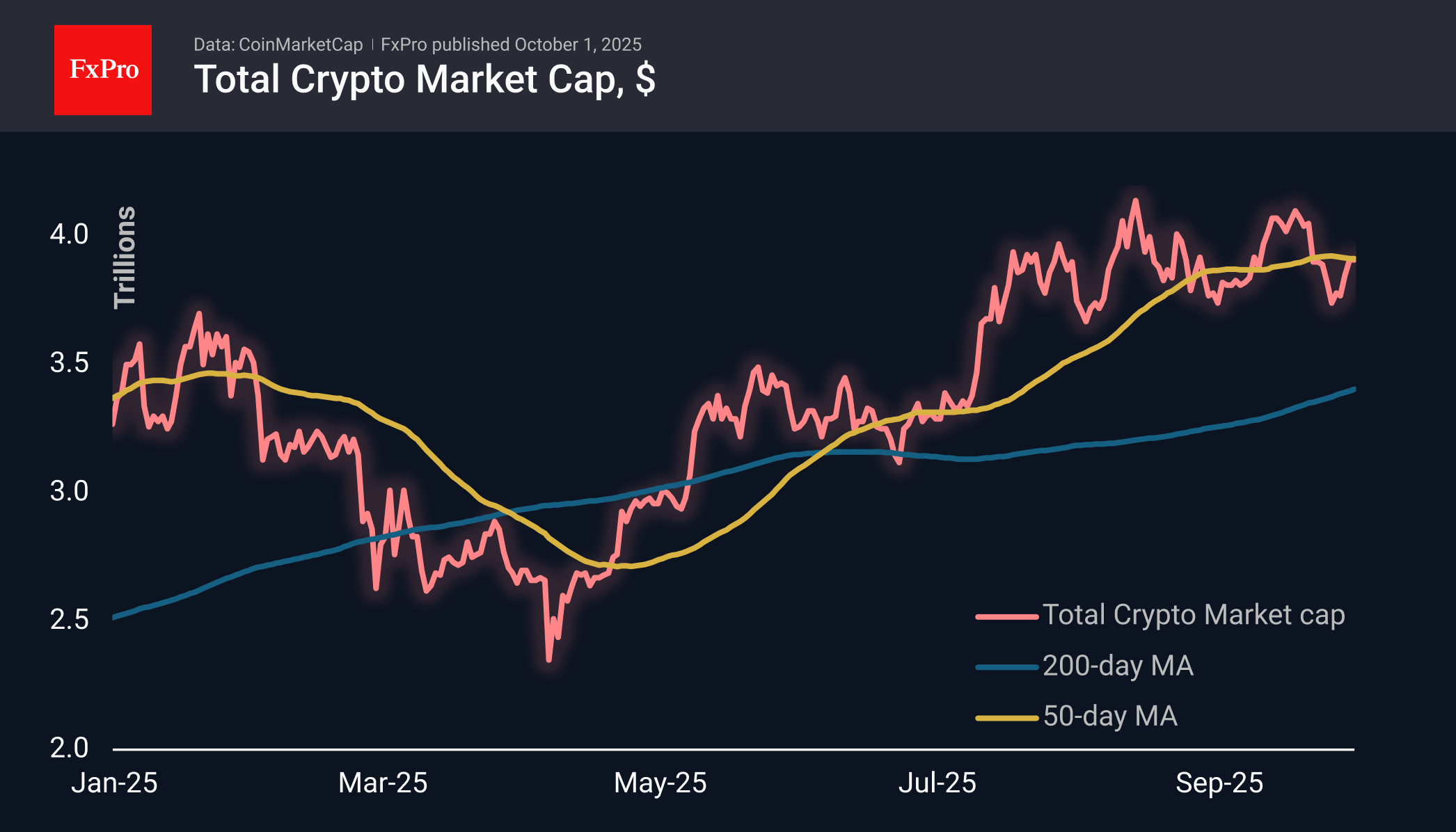

Crypto Market Rebounds from Low Point, But Further Signals Needed

Market Picture

The crypto market capitalisation has remained virtually unchanged over the past 24 hours, staying close to $3.91 trillion and the 50-day moving average. The market has moved away from local lows but prefers to wait for the next catalyst to determine its direction. Labour market data and the resolution of the US shutdown issue promise to help in this regard.

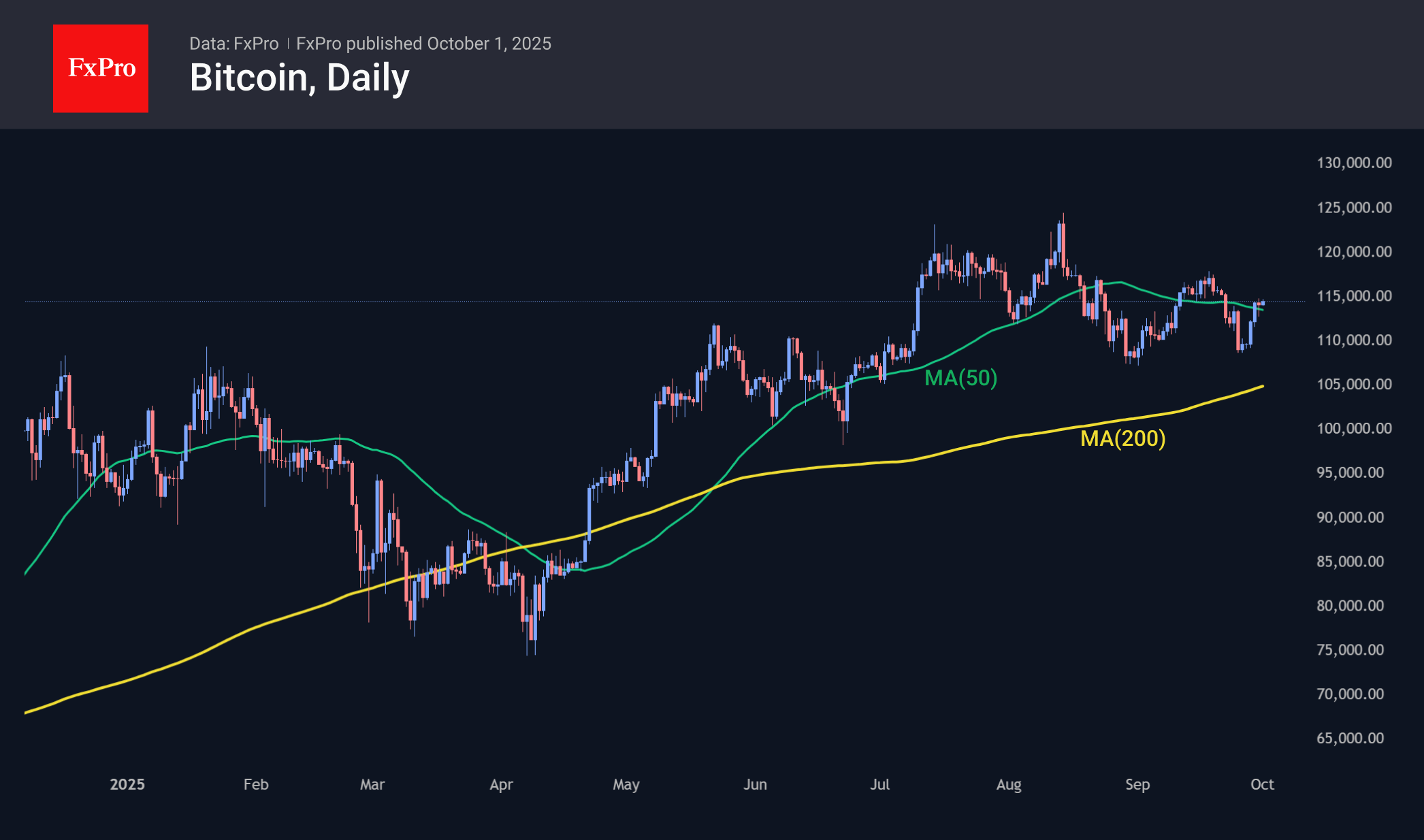

Bitcoin is trading above $114.4k, trying to consolidate above its 50-day moving average. The first cryptocurrency is much worse than gold and silver at exploiting the narrative of US financial problems, showing very indecisive growth. Cryptocurrencies are being weighed down by pressure on the stock markets, for which the shutdown is a negative factor.

Bitcoin rose 6.1% in September to $114.6k, defying the seasonal trends of one of the two worst months of the year. In recent days, BTC has managed to approach the highs of the middle of the month.

From a seasonal perspective, October is one of the three best months of the year, which is why it is called ‘Uptober.’ Over the past 14 years, Bitcoin has ended this month with growth in 10 cases. The average growth was 27.4%, and the average decline was 15.3%.

News Background

According to Bitwise, the current situation may indicate the end of the decline phase. Sellers appear to be ‘increasingly depleted.’ Upcoming SEC decisions on spot ETFs could be catalysts for growth, according to Bitget Research.

The share of altcoins in the volume of futures trading on Binance reached a historic high of 82.3%, exceeding the peak values of the 2021 altseason, according to CryptoQuant. Traders are increasingly shifting their attention to more volatile assets in anticipation of higher profits.

DePIN tokens of decentralised physical infrastructure networks are not securities and are therefore outside the SEC’s oversight. This is stated in a letter from the regulator addressed to the DoubleZero project.

EUR/USD Aims Fresh Increase While USD/CHF Corrects Lower

EUR/USD started a fresh increase above 1.1700. USD/CHF declined from 0.8000 and is now struggling to stay above 0.7945.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro started a decent upward move from 1.1650 against the US Dollar.

- There was a break above a key bearish trend line with resistance at 1.1700 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF declined below the 0.7985 and 0.7965 support levels.

- There is a major bearish trend line forming with resistance near 0.7965 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from 1.1650. The Euro cleared 1.1685 to decrease bearish pressure and move into a bullish zone against the US Dollar.

There was a break above a key bearish trend line with resistance at 1.1700. The bulls pushed the pair above the 50-hour simple moving average and 1.1720. It opened the doors for a move above the 50% Fib retracement level of the downward move from the 1.1818 swing high to the 1.1645 low.

The pair is now struggling to gain pace for a move above 1.1750 and the 61.8% Fib retracement. The first key hurdle on the EUR/USD chart is near 1.1780. An upside break above 1.1780 might send the pair toward 1.1820. The next major area of interest for the bears might be 1.1850. Any more gains might open the doors for a move toward 1.1880.

Immediate support on the downside is near the 50-hour simple moving average and 1.1730. A close below 1.1730 could spark more bearish moves and send the pair toward 1.1685. The next major hurdle for the bears might be 1.1650. Any more losses might send the pair into a bearish zone toward 1.1550.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a fresh decline after it failed to stay above 0.8000. The US Dollar dropped below 0.7985 to move into a negative zone against the Swiss Franc.

There was a move below the 50% Fib retracement level of the upward move from the 0.7902 swing low to the 0.8014 high. The bears pushed the pair below the 50-hour simple moving average and 0.7965.

Finally, the pair tested the 61.8% Fib retracement at 0.7945. It is now consolidating losses and facing resistance near the 50-hour simple moving average and a major bearish trend line at 0.7965. A clear move above the trend line could send the pair to 0.7985.

The next major barrier for the bulls might be 0.8015, above which the pair could test the 0.8050 level. If there is a clear break above 0.8050, the pair could start another increase. In the stated case, it could even surpass 0.8100.

On the downside, immediate support on the USD/CHF chart is 0.7945. The first major area of interest could be 0.7925. Any more losses may possibly open the path for a move toward the 0.7900 level in the coming sessions.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Pound Faces Challenges: Weak Data and External Pressures Mount

The GBP/USD pair is trading near 1.3445 on Wednesday, with the pound closing September with its first monthly decline against the US dollar since July.

Short-term price action remains under pressure from the looming US government shutdown, which threatens to delay the release of key US macroeconomic data, injecting uncertainty into the market.

Domestic economic figures from the UK offered a mixed picture. Second-quarter GDP growth was confirmed at 0.3% quarter-on-quarter, matching forecasts. However, the current account deficit widened significantly to £28.9 billion, or 3.8% of GDP, up from 2.8% in the previous quarter and well beyond expectations.

The pound is also contending with substantial domestic headwinds. The UK continues to grapple with the highest inflation rate among major developed economies (around 4%) and elevated borrowing costs. Bank of England Deputy Governor Sarah Breeden emphasised that inflation remains excessively high, noting two-sided risks. She warned that prices for food and services could keep inflation stubbornly elevated, despite emerging signs of a slowdown in wage growth.

Further pressure stems from fiscal policy, with Chancellor of the Exchequer Rachel Reeves preparing the budget for 26th November. Tax rises are seen as almost inevitable to cover a fiscal gap estimated in the tens of billions of pounds.

In summary, the pound is caught between external risks—such as the US shutdown and global capital flows—and domestic challenges, including a high deficit, persistent inflation, and the prospect of fiscal tightening.

Technical Analysis: GBP/USD

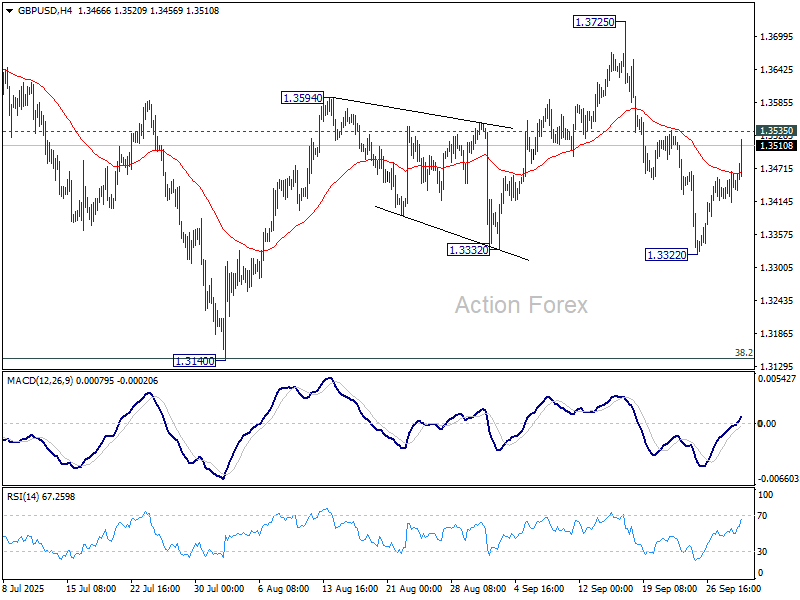

H4 Chart:

On the H4 chart, GBP/USD formed a tight consolidation range around 1.3434. Following an upward breakout, the pair is now developing a corrective wave towards 1.3550. Once this correction is complete, we anticipate the start of a new decline towards 1.3434, with a longer-term prospect of extending the downtrend to 1.3330. This outlook is technically confirmed by the MACD indicator, whose signal line is below zero but is rising steadily.

H1 Chart:

The H1 chart shows the pair forming a consolidation range around 1.3418 before breaking upwards. It is now continuing a growth wave towards a local target of 1.3490. Following this, a decline back to 1.3418 (testing it as support from above) is expected. Subsequently, another upward structure could develop, targeting at least 1.3508, with a potential extension to 1.3550. The Stochastic oscillator supports this view, with its signal line above 50 and rising sharply towards 80.

Conclusion

The pound is navigating a complex landscape of domestic economic weaknesses and external uncertainties. While a short-term technical correction is underway, the broader fundamental and technical picture suggests the downward trajectory is likely to resume after the current upward move is exhausted.

Eurozone inflation ticks higher to 2.2%, core steady 2.3%

Eurozone headline inflation edged up in September, with CPI rising to 2.2% yoy from 2.0% yoy in August, in line with expectations. Core CPI, which excludes energy, food, alcohol and tobacco, held steady at 2.3% yoy, suggesting underlying price pressures remain sticky even as the energy drag eases.

By component, services posted the highest annual inflation at 3.2%, slightly higher than August’s 3.1%. Food, alcohol and tobacco slowed to 3.0% from 3.2%. Non-energy industrial goods were unchanged at 0.8%. Energy prices continued to decline, though the contraction moderated to -0.4% from -2.0%.

UK PMI manufacturing at 46.2, sector struggles with more worrying news

The UK manufacturing sector slipped further into contraction in September, with the PMI finalized at 46.2, down from 47.0 in August and marking a five-month low. Rob Dobson, Director at S&P Global Market Intelligence, called the results “further worrying news” for industry, pointing to weak demand, fading export orders, and a high-cost environment amplified by rising taxes and labor costs.

The report noted that the tough backdrop is eroding business confidence. Firms have now shed jobs for 11 consecutive months, with many cutting back on purchasing and non-essential spending. Sentiment about the year ahead remains subdued.

There were some glimmers of hope. Firms highlighted that lean inventories and potential easing in global trade tensions could lift output in the months ahead. Input costs are also rising at a slower pace, which may give the BoE scope to cut rates later this year.

BoE’s Mann warns inflation persistence playing out

BoE policymaker Catherine Mann said today that keeping rates on hold is “appropriate for the current period,” and warned that the risk of sticky inflation remains elevated. Speaking to Bloomberg TV, she flagged “drift in inflation expectations” as a key concern, noting that it reinforces the persistence of price pressures.

Mann argued that the scenario outlined earlier this year — one where inflation risk lingers longer than expected — is now “playing out.” She added that the UK’s supply side continues to pose challenges for both the economy and policymakers, making it harder to fully restore price stability.

On trade, Mann said she does not yet see diversion effects feeding through as the “tariff landscape continues to be shifting." “The domestic component is the more important issue that I need to face,” she said.

Eurozone PMI manufacturing at 49.8, stagnation can be viewed positively

Eurozone manufacturing activity edged back into contraction in September, with the PMI finalized at 49.8, down from August’s 50.7. Output slowed as well, with the production index falling from 52.5 to 50.9, pointing to weaker factory momentum across the bloc.

Country data painted a mixed picture. The Netherlands stood out with a 38-month high of 53.7, while Ireland and Greece also held above 50. Spain remained in expansion at 51.5 but slowed to a three-month low. Germany, France, and Italy — the region’s largest economies — all stayed below 50, signaling their industrial recessions are easing but not yet over.

Cyrus de la Rubia of Hamburg Commercial Bank said the “stagnation observed in the manufacturing sector can also be viewed positively,” given headwinds from US tariffs, political uncertainty in France and Spain, and high energy costs. He noted the sector is “holding up surprisingly well,” though confidence remains lower than the decade average.