Sample Category Title

Preview of RBNZ: Getting the OCR to Where It Needs to Be

- We expect the RBNZ to cut the OCR by 50bp to 2.5% at its October meeting.

- An easing bias will likely be maintained that’s dependent on data to come.

- Signs of greater than expected excess capacity will be highlighted and the prospect of subdued medium-term inflation pressures will motivate the MPC’s decision.

- The arguments for a “circuit breaking” shift in the OCR to levels more consistent with boosting demand should remain prominent and tip the balance on the MPC.

- Quickly moving the OCR to a stimulatory level will generate confidence and activity ahead of the important Christmas and summer trading period.

RBNZ decision and communication.

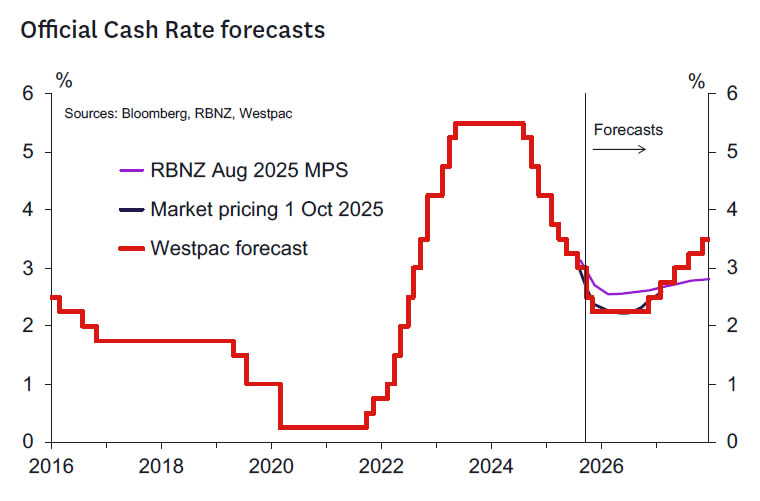

In the August Monetary Policy Statement (MPS) the RBNZ indicated that it expected to reduce the OCR to 2.5% by year end. On balance, the data flow since August – notably the very disappointing June quarter GDP report – has supported the RBNZ’s forecast. Indeed, commentators seem united in the belief that the OCR needs to go to 2.5%, with downside risk beyond. The market has similar views regarding the policy outlook, having quickly moved to price a terminal OCR of 2.25% in the wake of the GDP report.

In our view, there doesn’t seem to be a good reason to delay a move to 2.5%. Quickly moving the OCR to a stimulatory level will boost confidence and activity ahead of the important Christmas and summer trading period. This may also reduce the likelihood that even further monetary policy support is required in the new year – a year in which domestic political uncertainty is likely to grow if opinion polls continue to point to a tight General Election.

In the August MPS, two MPC members voted for a “circuit breaking” shift in the OCR to levels more consistent with boosting demand. Those views should hold even greater sway this meeting, helping to tip the balance on the MPC towards a 50bps cut. Hence, we expect the RBNZ to cut the OCR by 50bp to 2.5% at its 8 October meeting.

We also note that the composition of the MPC has shifted since August. The most hawkish member, Dr Bob Buckle, has ended his term and there is a new member, Hayley Gourley, who may be happy to move with the consensus while getting familiar with the process. Similarly, we expect Governor Christian Hawkesby will give weight to the views of the members of the MPC who will be carrying on post November, since they will be the ones remaining to deal with the consequences of policy decisions taken now. We suspect this might increase the weight the most dovish MPC members carry this time.

We expect the Bank to maintain an easing bias, with the prospect of a further reduction in the OCR at the 26 November meeting conditional on the flow of data to come (which will include the September quarter inflation and labour market reports). We doubt the MPC will want to be seen as delaying stimulus and encouraging the public and businesses to hold back spending, hiring and investment decisions in anticipation of more policy action later. This type of behaviour has been a feature of the easing cycle to date and may have contributed to a slower than ideal response to the 250bp of cuts already implemented.

It’s also worth noting that given current market pricing, it’s probably hard for the RBNZ to cut the OCR by just 25bp and not cause interest rates to rise somewhat. What would be required is a relatively strong commitment to cut rates significantly in November. This would raise the question of why a greater easing wasn’t occurring now? There might also be criticism of the RBNZ in this circumstance that the MPC might be sensitive to.

We think our central scenario of a 50bp cut and an easing bias for November has around a 70% likelihood. There are also other scenarios to be considered.

- A hawkish outcome would be a 25bp cut and indications of another 25bp coming in November (20% chance). This would indicate that the MPC see the path depicted in the August forecasts as remaining reasonable. There would be a decent backup in interest rates given markets currently price the OCR to bottom out around 2.2-2.25% at the time of writing.

- A dovish outcome would be the RBNZ coupling the 50bp cut at this meeting with a strong presumption of at least a 25bp cut in November (10% chance). This would indicate that the MPC interpret recent data as implying significant downside risks to the timing of the recovery forecast in the second half 2025 and into 2026. Hence this would imply an amping up of the circuit breaking easing discussed in August beyond what we see as more likely right now.

Recent data flow and impact.

Key data and developments that have accumulated since the August MPS include:

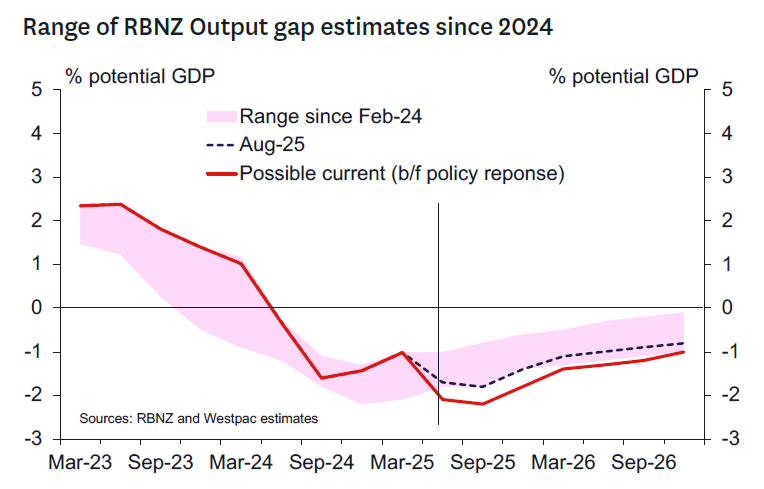

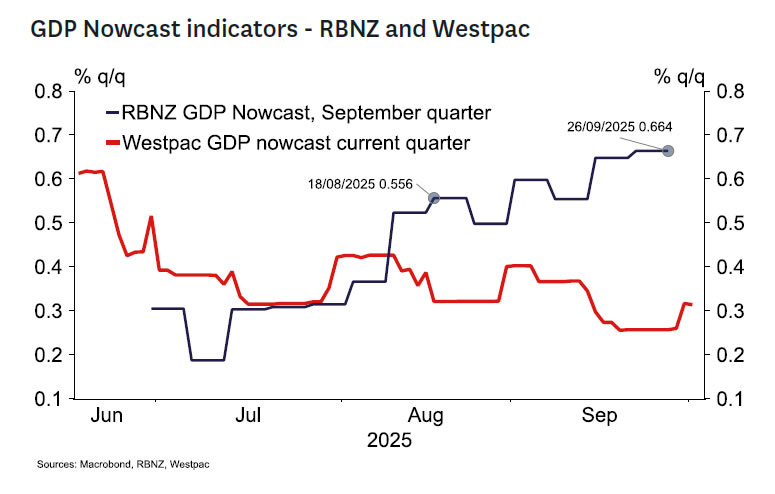

- The June quarter GDP outcome of -0.9%q/q was 0.6ppts weaker than the RBNZ had forecast. While there are reasonable prospects that September quarter GDP growth will exceed the RBNZ’s August MPS forecast of 0.3%q/q, we don’t think growth will be strong enough to offset the June quarter error. As a result, the negative output gap will remain larger than the RBNZ had expected.

- Adjusted for the bias in the latest monthly outcome, filled jobs data from the Monthly Employment Indicator suggests that employment is tracking consistent with the RBNZ’s August forecast of zero growth in the September quarter, which will likely lead to a further modest rise in the unemployment rate. The number of job advertisements remain exceptionally low but have turned factionally higher in recent months.

- High frequency activity indicators, such as the Business NZ PMIs and the ANZ’s past activity indicator have been mixed, but in all cases remain consistent with no more than modest GDP growth.

- House sales have declined slightly in recent months, selling times have remained longer than normal and house prices have been flat at best.

- Sentiment surveys continue to point to firm business optimism, boosted slightly since the RBNZ’s August MPS pivot, but still weak levels of consumer confidence (likely reflecting the weak state of the labour market and pressures on household budgets from higher food and energy prices and sharp increases in council rates).

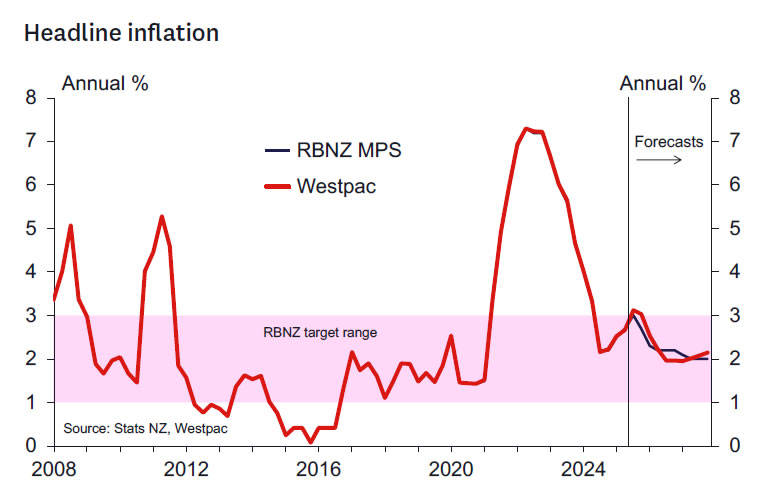

- Monthly price data continues to suggest that the CPI will sit close to the top of the RBNZ’s 1-3% target range in the September quarter, as the RBNZ forecast in the August MPS.

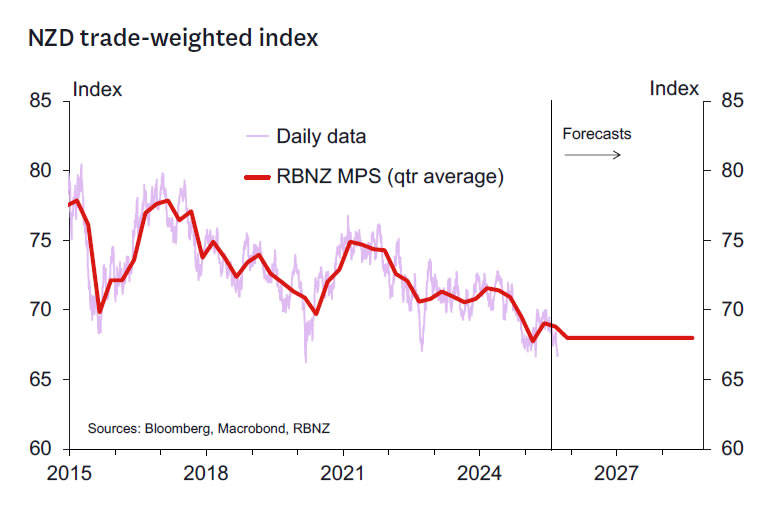

- The trade-weighted exchange rate has fallen around 2% below the RBNZ’s August MPS assumption, reflecting the market’s reaction to the weak June quarter GDP data and the pricing of a 2.25% terminal rate for the OCR.

- The RBNZ will also be watching the upcoming QSBO survey (out 7 October) closely. This survey has tended to be one of the more reliable gauges of economic activity and inflation pressures in New Zealand, and will provide a timely update on how the economy has been tracking following the weaker than expected June quarter GDP result.

Kelly’s take.

A 50bps cut at this meeting is appropriate. In the past few meetings, I’ve been counselling a more cautious approach consistent with the end of the easing cycle potentially getting nearer. But events have overtaken that view as it was predicated on growth broadening and strengthening in the second half of 2025 in the context of an inflation rate that’s too high and unlikely to fall into the lower half of the 1-3% target range.

Where we stand now is a situation where the level of excess capacity has grown instead of shrunk in the last 3-6 months. And while the primary sector and rural economies look strong enough, the flow through to the urban economies and critically the services sector seems sufficiently weak to imply its far from assured that at OCR around 3% will deliver above trend growth quickly.

It’s reasonable to assume that inflation will moderate from the 3%-plus level we expect to print in the September and December quarters. The level of excess capacity seems sufficient to achieve an inflation rate closer to 2% in time – although I don’t expect inflation to move significantly below 2%, especially since the exchange rate seems likely to remain weak given low growth and widening interest rate differentials.

The biggest medium-term concern is the risks of monetary policy overshooting. Given where underlying growth momentum appears to be, my sense is that the OCR would need to fall below 2% before those risks become material. And it’s easy enough to take back some stimulus at some stage in 2026 should growth quickly accelerate and bring the OCR back closer to the 3.75% level I continue to see as broadly neutral. Indeed, that scenario would likely be a quality problem I suspect.

A sub-2% OCR would be an entirely different story and not one that’s in the thinking right now. We would need to see some kind of problem – domestic or global – to emerge to justify an OCR below 2%. And questions should be asked of fiscal policy in those circumstances also.

Right now, the concern should be to get the OCR set by Christmas at a level where the MPC can be confident of seeing trend to above trend growth outcomes in the New Year. Doing less now and then having to promise more in February, as was the case at the end of 2024, risks extending unduly the timeframe where growth resumes and the labour market strengthens.

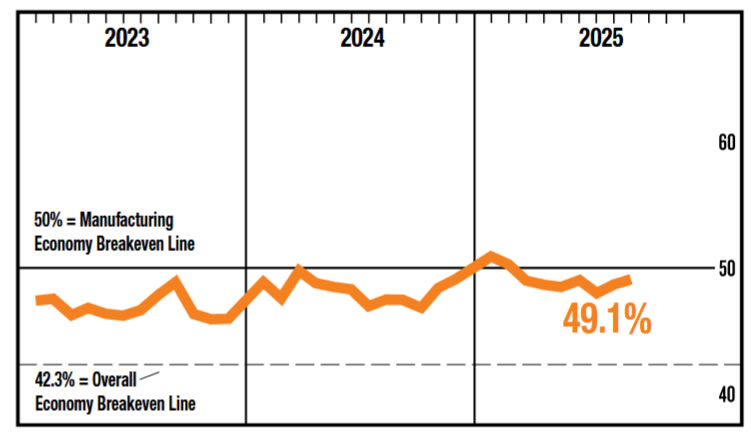

US: ISM Manufacturing Index Shows Seventh Consecutive Month of Contraction

The ISM Manufacturing Index rose to 49.1 in September, up from 48.7 in August, but remaining in contractionary territory.

Only five of 18 industries reported growth last month, down from seven in August. Similar to August, roughly 70% of manufacturing GDP contracted in August.

Demand conditions worsened in September, after showing signs of turning a corner in August. The new orders index fell 2.5 points to 48.9, reversing a short-lived trip into expansionary territory in August. The new export orders index fell by 3.6 points to 43.0, also reversing an uptick in the month prior.

The production index entered expansionary territory, increasing to 51.0 from 47.8, but the employment index remained in contractionary territory.

Price gains decelerated in September, coming in at 61.9 vs. 63.7 in August. However, the prices index continued to fluctuate near a three-year high.

Key Implications

Manufacturing activity contracted at a slower pace in September as domestic demand expanded, the decline in foreign demand slowed, and expectations for lower interest rates increased. The details of the report clearly show stagnation in the manufacturing sector, but as a small silver living, we may be seeing less stagflation. The production index entered expansionary territory, and the prices index pointed to slower, but still increasing, price pressures. If this is a sign of moderating price pressures accompanied by economic weakness, it simplifies the decision-making of the Federal Reserve.

Sentiment relayed by survey respondents continued to be negative and points to broad expectations that the weakness in the index will persist for some time. Several comments pointed to a large impact from tariffs, such as products being held at the border and tariffs pushing up their costs. Others point to tariffs as dragging down customer orders and leading to flat revenue expectations for the year. Without a major change in the economic environment, it seems likely that the contraction in manufacturing will be continuing.

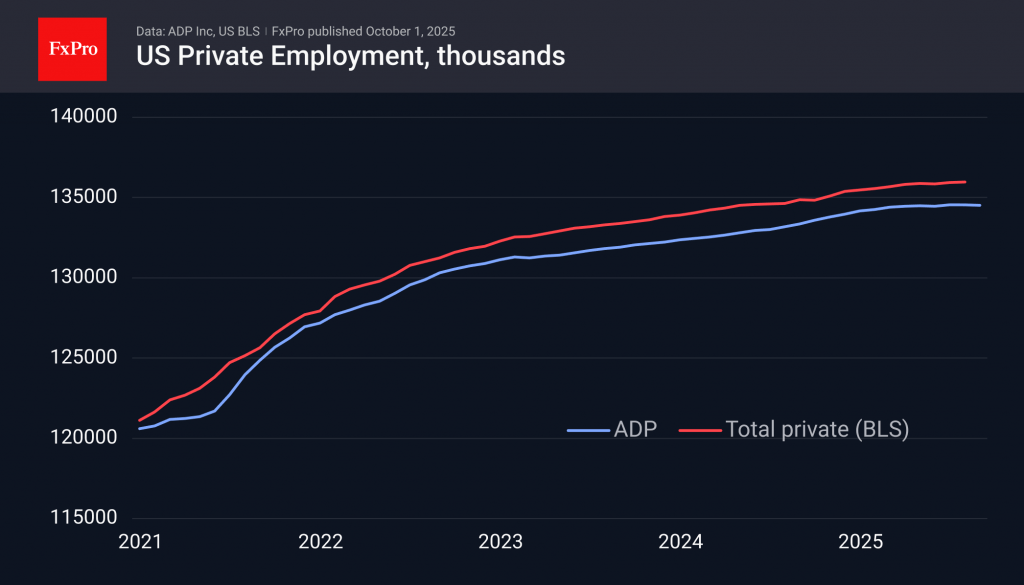

ADP Reports Two Consecutive Months of Job Losses in Private Sector

Independent data provider ADP reported a decline of 32k jobs in the US private sector in September. The data was significantly worse than the expected growth of 50k. Moreover, August figures were revised down from +54k to -3k. ADP thus paints a very bleak labour market picture, while recent revisions to official figures suggested that June was the worst point since the beginning of the year, followed by slight growth.

ADP data has lost much of its influence on the markets in recent years, proving to be a weak predictor of Friday’s official release, as originally intended. But this time, there is a risk that the official release will not be published on Friday at all due to the US government shutdown. The funding freeze has a significant impact on statistical services, which are considered less of a priority than courts, the military, and doctors.

Weak labour market indicators increase the chances of a consistent reduction in the Fed’s key rate. The probability of two more cuts before the end of the year rose to 91% on Wednesday after the ADP release, compared to 77% the day before and 40% a month ago.

Policy easing is bad news for the dollar, as long as we see a moderate decline. It would take a sharp decline in employment to trigger a wave of carry trade unwinding, which leads to impulsive sell-offs in stocks and commodities, attracting capital to short-term government bonds, which is good for the USD. However, until that point is reached, the prevailing pattern for equities remains “bad news is good news.”

Sunset Market Commentary

Markets

The jobs report coming from ADP is usually a mere appetizer ahead of the official payrolls report scheduled for release two days later. This time around, though, it’s the main dish. The US government shutdown means economic data coming from the Department of Labour (payrolls, CPI, jobless claims …) are suspended for who knows how long. The ADP version therefore gains in significance as a labour market gauge, temporarily at the very least. Private Job creation fell well below the 51k consensus view, in fact printing a negative 32k. The August reading saw a sharp downward revision to a minus 3k from +54k. ADP noted that the annual rebenchmarking resulted in a reduction of 43k jobs last month compared to the pre-benchmarked data. Looking at the broader underlying trend however, the company said that nothing had changed and “job creation continued to lose momentum across most sectors” with US employers being cautious in hiring. The report triggered a kneejerk market reaction with US yields down across the curve, led by the front end. Net daily changes vary between -2.8 (30-yr) and -7 bps (2-5-yr bucket). A Fed October cut is fully priced in now, even though the central bank – as things currently stand – will literally have zero new (critical) information compared to the September policy meeting. A follow-up move in December is discounted for around 90%. German/European rates gapped higher at or shortly after the market open before changing course afterwards. They extended the decline in sympathy with the US but are down less than <1.5 bps across the curve. The US dollar obviously trades in the defensive, in particular against the yen. Solid business confidence (Q3 Tankan) is adding to conviction of a new Bank of Japan rate hike later this month, diverging with the direction the Fed is going. USD/JPY slides to 146.8, more or less the lower bound of this summer’s sideways trading range. EUR/JPY is leaving the recent 175 highs further behind (172.5). EUR/USD ekes out a small gain to 1.175. The pair remains stuck from a technical point of view. Sterling is enjoying a strong day. Other than a constructive risk environment, we’ve seen no particular trigger. Bank of England’s Mann at a Bloomberg conference said she puts more weight on inflation, calling for a longer hold on rates. While higher rates are theoretically positive for a currency, it’s different when you’re in a stagflationary environment the sorts the UK is facing. Either way, EUR/GBP tumbles to a two-week low around the 0.87 big figure. Cable (GBP/USD) tries to settle back north of 1.35. European stocks add 0.6% with the EuroStoxx50 closing in on a record high. Wall Street opens day 1 of the shutdown slightly lower.

News & Views

A renewed drop in new orders drove the overall decline in the Czech manufacturing PMI in September (49.2 from 49.4). New sales decreased for the first time in four months. Firms continued to highlight subdued international and domestic demand conditions, alongside challenges from competition. Czech manufacturers saw a small decline in monthly output and lowered their workforce numbers again. Backlogs of work are nevertheless increasing with business confidence rising to a 3-month high. Cost burdens increased at the slowest pace YtD. Where an increase was reported, it was mostly linked to energy and foodstuff. Czech goods producers cut their selling prices at the end of the third quarter, extending a four-month decline. Prices components are consistent with 2.5% Y/Y CPI-growth in September, according to S&P global. Data will be published next Monday. CZK is still trading near best levels since end 2023 at EUR/CZK 24.27.

The Hungarian Association of Logistics, Purchasing and Inventory Management (HALPIM) said that the country’s manufacturing PMI rose from 49.1 to 51.5, moving back above the 50 boom/bust level. New orders and production volumes also returned to expansionary levels while the pace of job shedding slowed. A new increased of purchased inventories points to restocking. The improving PMI and stubborn inflation both strengthen the view that the MNB will be sidelined for longer. EUR/HUF today tested the YtD low at 389.

US ISM manufacturing rises to 49.1, improvement negligible

US ISM Manufacturing PMI inched up from 48.7 to 49.1 in September, just shy of expectations at 49.2, marking the seventh straight month in contraction. The modest uptick reflected stronger production, which rose from 47.8 to 51.0, and a slight improvement in employment from 43.8 to 45.3.

However, the details painted a mixed picture. New orders slipped back into contraction at 48.9 (down from 5.14) after briefly turning positive. Prices paid eased from 63.7 to 61.9, suggesting input cost pressures are cooling.

ISM noted that the gains in production were offset by declines in new orders and inventories, leaving the overall PMI improvement “negligible.”

According to ISM, the September reading historically corresponds to a 1.9% annualized increase in US GDP. That suggests the factory sector remains a drag but not a collapse.

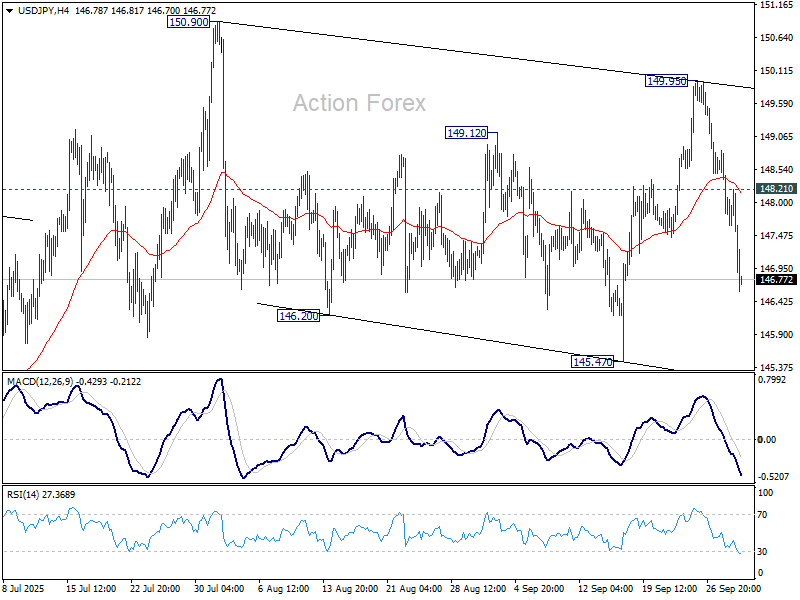

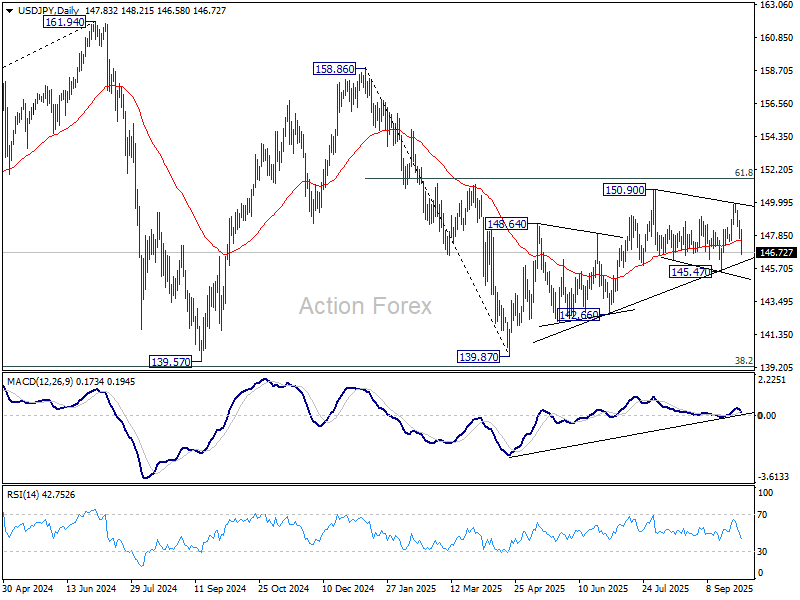

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.44; (P) 148.15; (R1) 148.64; More...

Intraday bias in USD/JPY remains on the downside for for 145.47 support. Strong support from there will keep the pattern from 150.90 corrective. That is, rise from 139.87 would still be in favor to resume at a later stage. However, decisive break of 145.47 will indicate near term reversal, and bring deeper fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

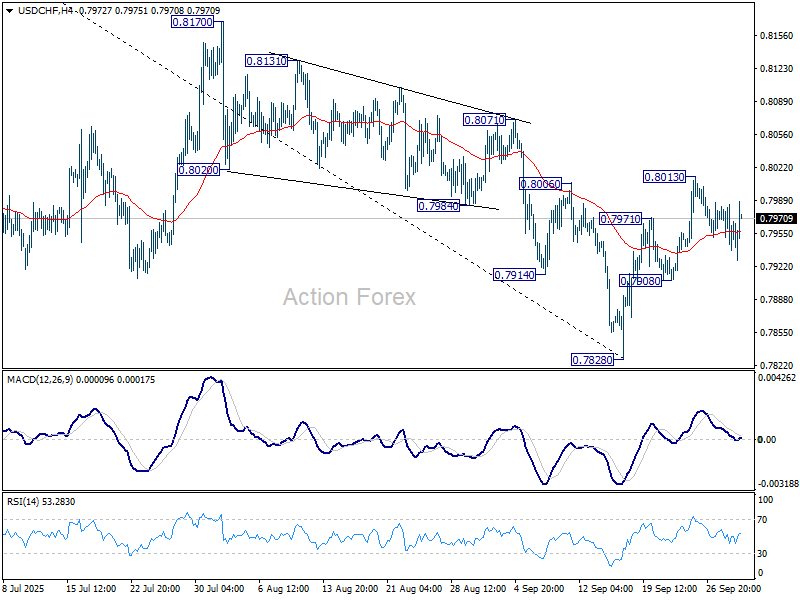

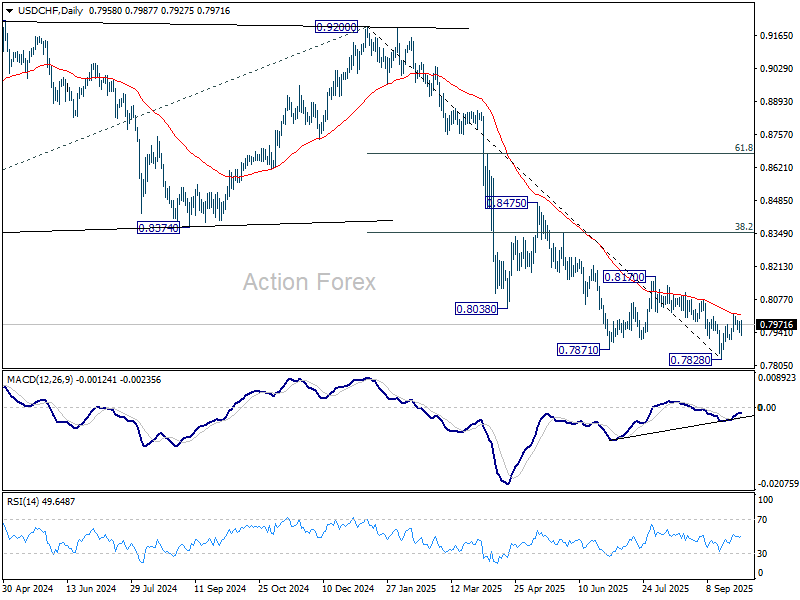

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7963; (R1) 0.7988; More…

Intraday bias in USD/CHF remains neutral at this point. On the upside, sustained trading above 55 D EMA (now at 0.8014) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

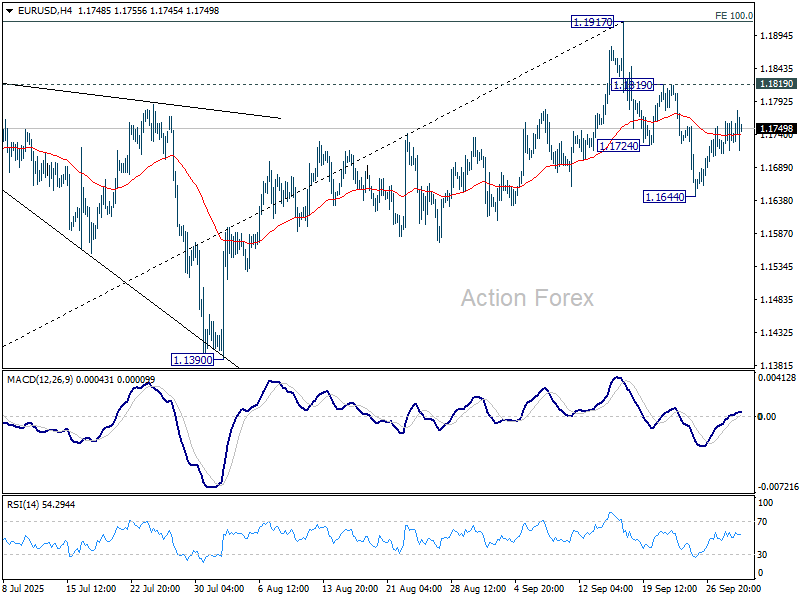

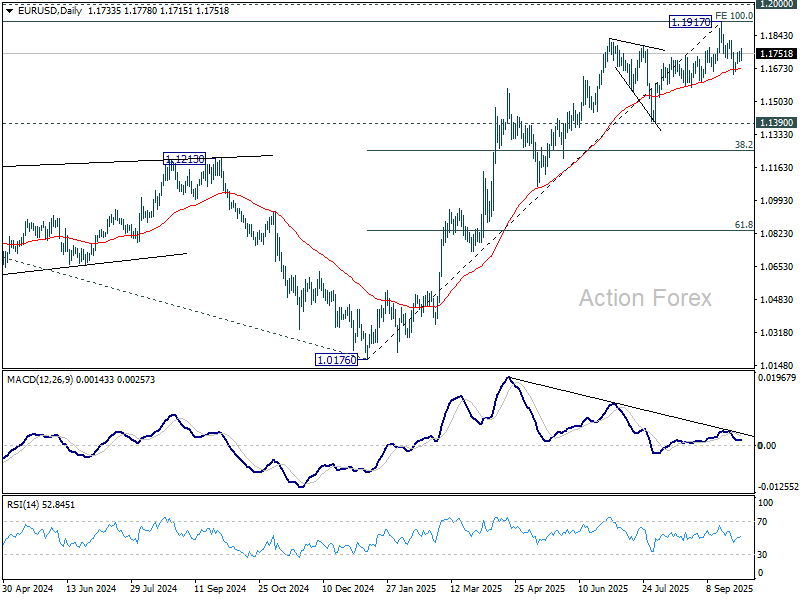

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1709; (P) 1.1736; (R1) 1.1759; More...

No change in EUR/USD's outlook and intraday bias stays neutral. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1675) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next. Nevertheless, break of 1.1819 will bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

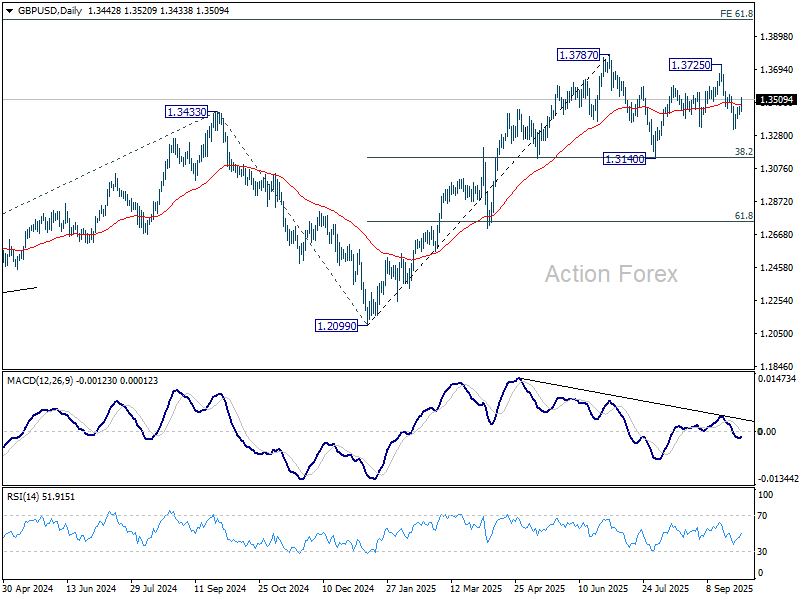

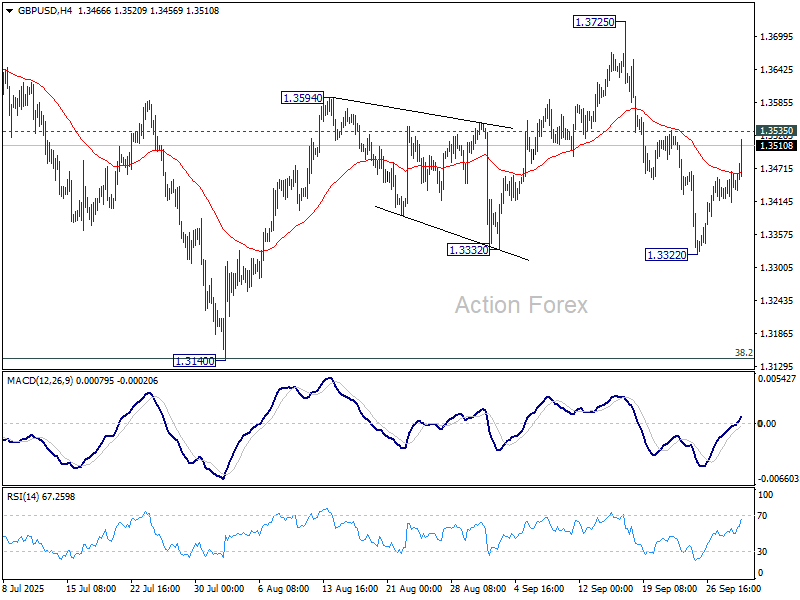

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3418; (P) 1.3442; (R1) 1.3471; More...

Focus is back on 1.3535 resistance in GBP/USD with today's extended rebound. Firm break there will target 1.3725/87 key resistance zone. On the downside, though, break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.