Sample Category Title

Fed’s Hammack: Inflation seen above target until 2028, restrictive policy needed

Cleveland Fed President Beth Hammack said today she remains concerned about inflation, which she described as still too high across headline, core, and especially services. In a CNBC interview, She reminded that the Fed has missed its 2% mandate for over four years, a persistence that continues to weigh heavily on her outlook.

By contrast, Hammack described the labor market as “reasonably healthy” and broadly balanced, reducing the urgency for further cuts. She warned that inflation may not return to 2% until late 2027 or even early 2028.

Balancing the Fed’s dual mandate, Hammack argued the central bank must maintain a "restrictive stance of policy so that we can get inflation back down to our goal”

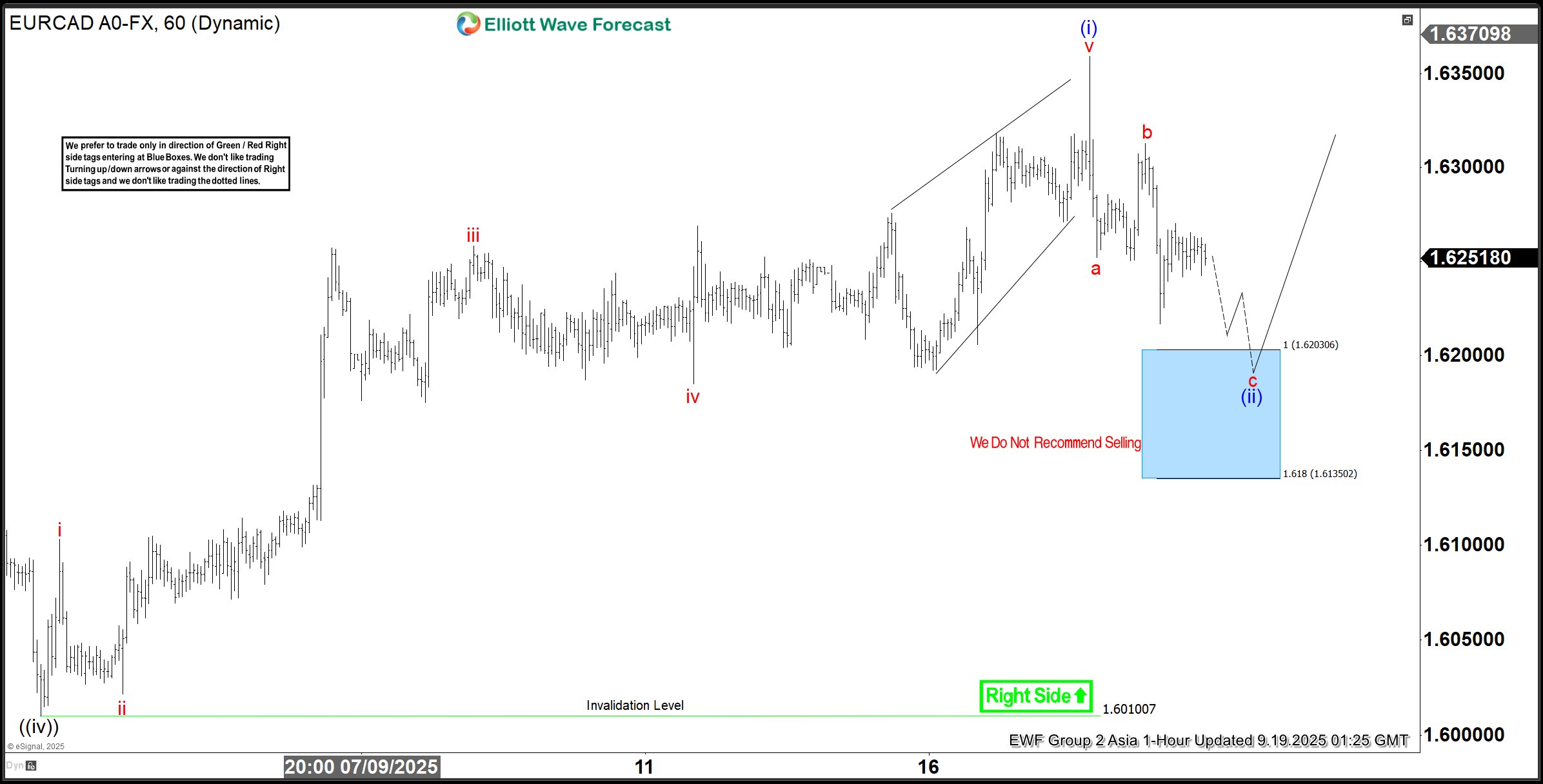

EURCAD Bounces Back: Reaction Higher from Blue Box Area

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of EURCAD. In which, the rally from 02 September 2025 low unfolded as impulse sequence & showed a higher high sequence therefore, called for an extension higher to take place. We knew that the structure in EURCAD should remain supported & extend higher. So, we advised members not to sell the pair & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

EURCAD 1-Hour Elliott Wave Chart From 9.19.2025

Here’s the 1-hour Elliott wave Chart from the 9.19.2025 Asia update. In which, the rally to 1.6359 high completed small wave (i) & made a pullback in wave (ii). The internals of that pullback unfolded as Elliott wave zigzag correction where small wave a ended at 1.6258 low. Then small bounce to 1.6313 high-ended small wave b. Then started the next leg lower in wave c towards 0.6203- 1.6135 blue box area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

EURCAD Latest 1-Hour Elliott Wave Chart From 9.29.2025

This is the latest 1-hour Elliott wave Chart from the 9.29.2025 London update. In which the pair is showing a strong reaction higher taking place, right after ending the correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. However, a break above 1.6359 high is needed to confirm the next extension higher towards 1.6404- 1.6476 area minimum & avoid double correction lower.

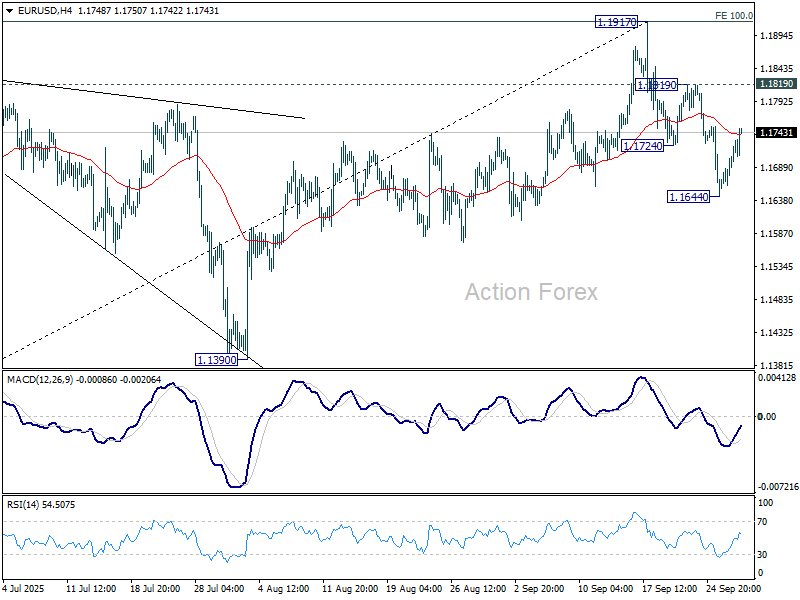

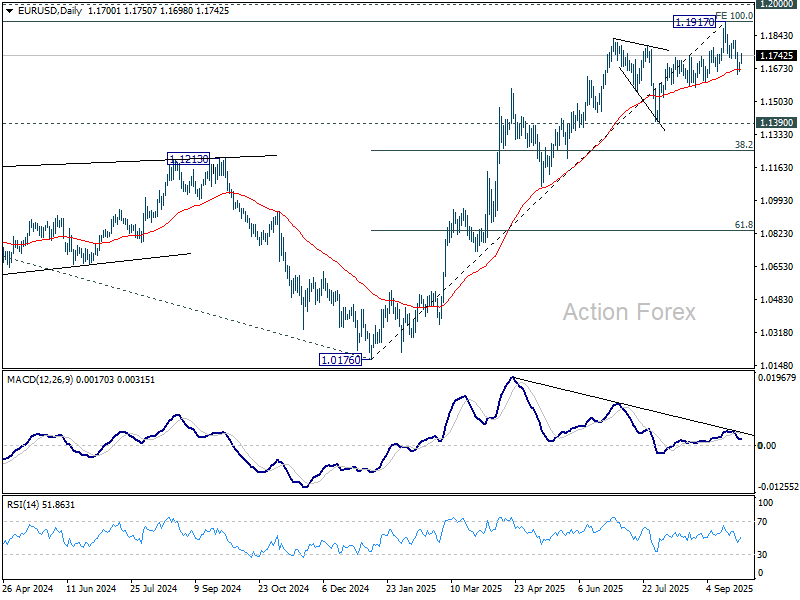

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1670; (P) 1.1688; (R1) 1.1719; More...

Intraday bias in EUR/USD stays neutral at this point. More consolidations could be seen above 1.1644. Further fall is expected as long as 1.1819 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1670) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

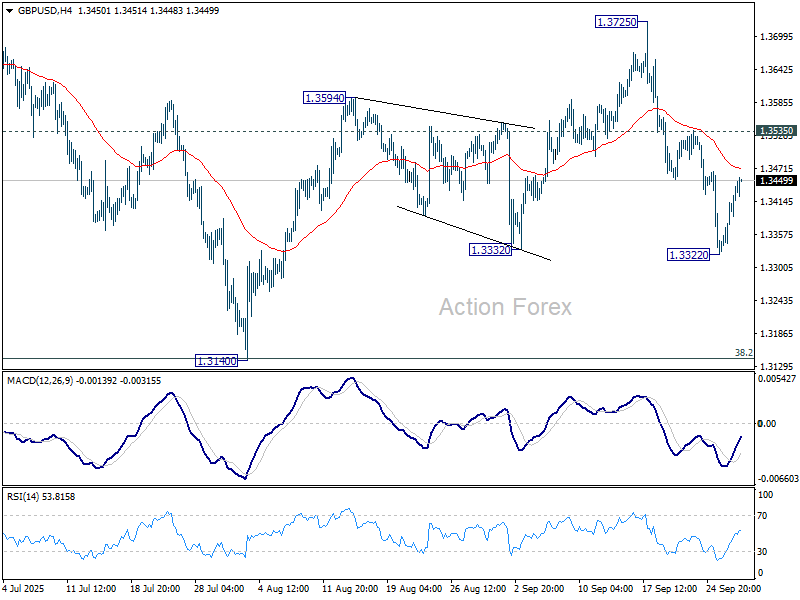

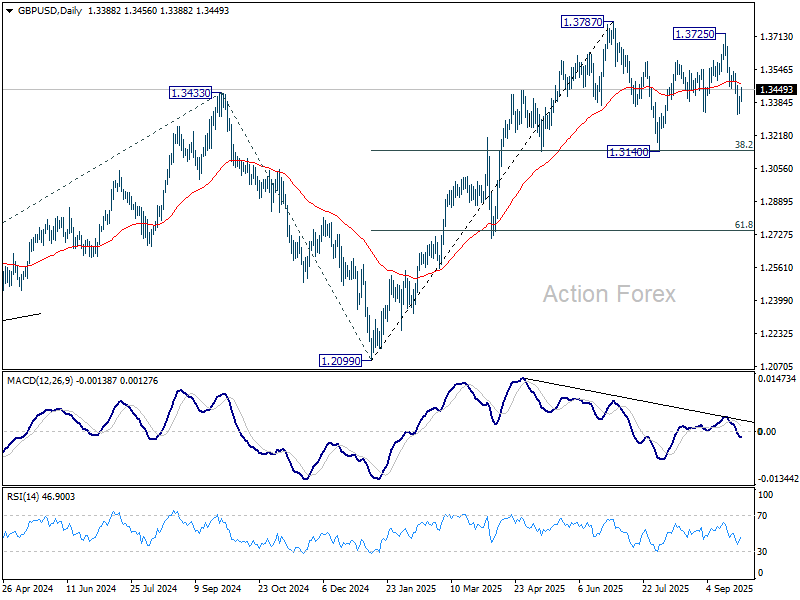

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3347; (P) 1.3380; (R1) 1.3430; More...

Intraday bias in GBP/USD remains neutral for the moment. More consolidations could be seen above 1.3322. But further decline is expected as long as 1.3535 resistance holds. Break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

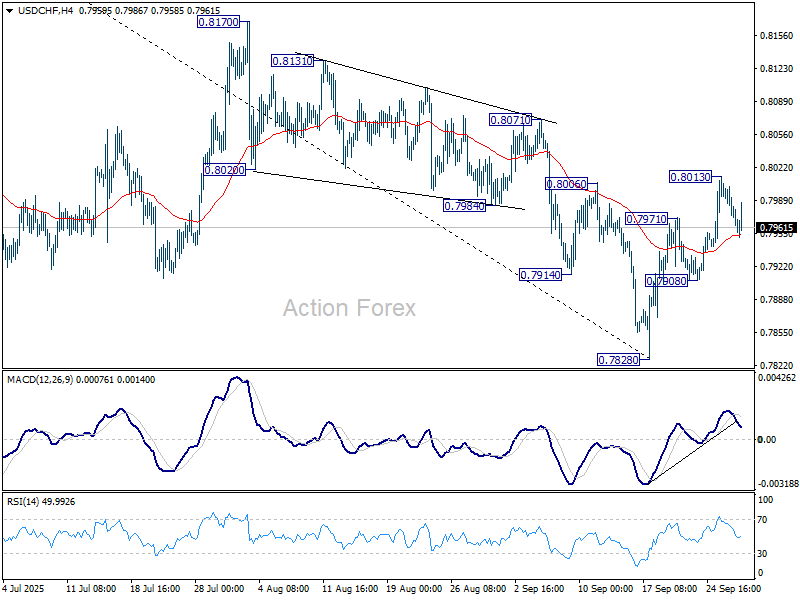

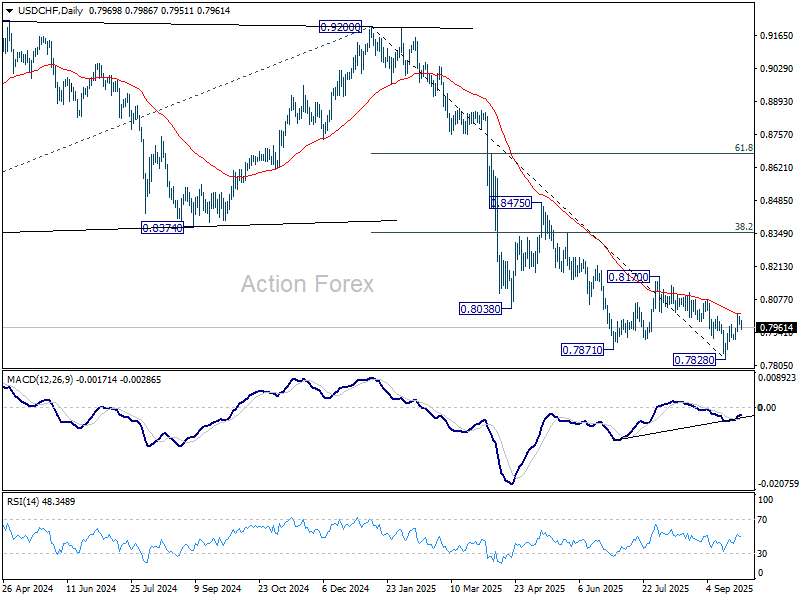

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7953; (P) 0.7984; (R1) 0.8026; More…

Intraday bias in USD/CHF remains neutral and some more consolidations could be seen below 0.8013. On the upside, sustained trading above 55 D EMA (now at 0.8014) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

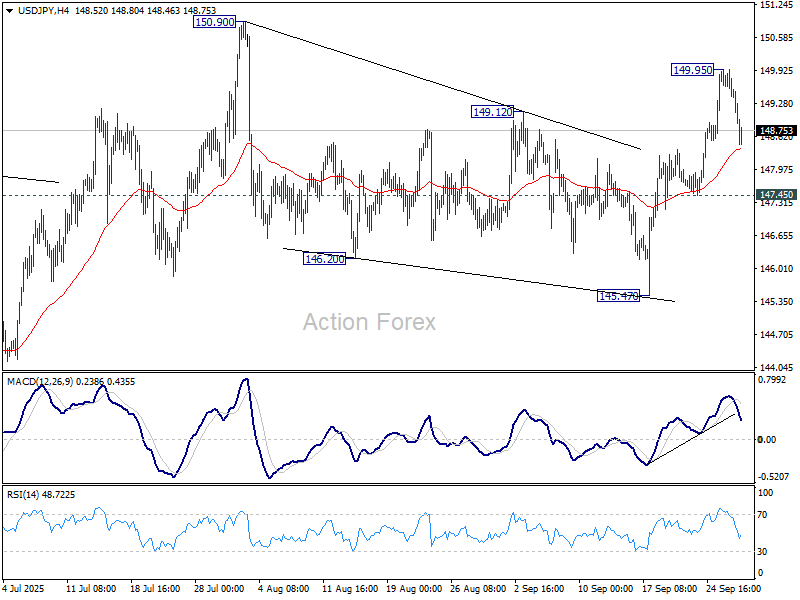

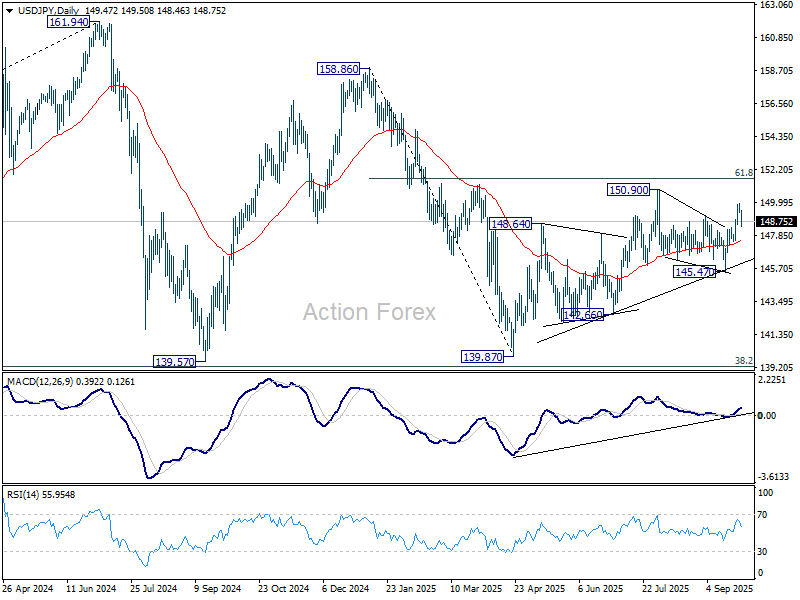

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.28; (P) 149.62; (R1) 149.83; More...

Intraday bias in USD/JPY stays neutral for the moment and some more consolidations could be seen below 149.95 temporary top. Further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall back to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Yen Leads as BoJ Hawkish Signals Build, Focus Turns to RBA

Yen held firm as the strongest performer heading into the US session, supported by mounting speculation that the BoJ is moving closer to a rate hike. Traders seized on a hawkish shift from a known dove on the Policy Board, a sign that internal momentum is building for further normalization.

This shift in tone from the BoJ was partly balanced by a cautious note from the Japanese government. In its September monthly report, the Cabinet Office kept its basic economic assessment unchanged, describing the recovery as “moderate” while highlighting the drag from US trade policies, particularly in the automotive sector. Officials also warned that attention should remain on downside risks linked to external headwinds.

Still, the currency’s next major driver will be global risk sentiment. Heavyweight US releases this week — highlighted by Friday’s non-farm payrolls — will be decisive for both stocks, bonds and currencies. Any data surprise strong enough to sway Fed expectations will inevitably spill over into USD/JPY and broader Yen crosses.

In the upcoming Asian session, attention is shifting to the RBA’s policy decision. The RBA is expected to keep rates on hold at 3.60%, but the outcome carries added weight after August CPI accelerated to 3.0% from 2.8%. While consensus sees a year-end rate of 3.35%, a handful of analysts have delayed their calls for a November cut in light of the firmer inflation print.

Australia’s largest banks are split: ANZ, CBA, and Westpac forecast a 25bps reduction in November, while NAB expects no easing until May. A Reuters poll found more than 80% of respondents still see a cut to 3.35% by year-end, though the number expecting no change has risen since August.

For the day so far, Dollar is the weakest major currency, followed by Swiss Franc and Loonie. Yen sits at the top of the ladder, ahead of Sterling and Aussie, with the Kiwi and Euro trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.54%. DAX is up 0.02%. CAC is up 0.26%. UK 10-year yield is down -0.038 at 4.72. Germany 10-year yield is down -0.023 at 2.731. Earlier in Asia, Nikkei fell -0.69%. Hong Kong HSI rose 1.89%. China Shanghai SSE rose 0.90%. Singapore Strait Times rose 0.09%. Japan 10-year JGB yield fell -0.013 to 1.647.

Eurozone economic sentiment inches higher to 95.5, jobs outlook softer

Economic sentiment in the Eurozone improved slightly in September, with the Economic Sentiment Indicator rising 0.2 points to 95.5. The broader EU also gained 0.6 points to the same level. Despite the uptick, sentiment remains below the long-term average of 100.

The modest gains were driven by stronger confidence in industry, services, and among consumers, offset partly by weaker retail sentiment and stable conditions in construction.

By contrast, labor market expectations slipped, with the Employment Expectations Indicator dropping -0.9 points in the EU and -1.3 points in the euro area, suggesting hiring momentum is fading.

Country-level trends were uneven. Spain led with a notable 3-point jump, followed by Italy (+0.7), while sentiment weakened in the Netherlands (-0.7) and Germany (-0.4). France (+0.3) and Poland (+0.1) saw little change.

BoJ dove Noguchi signals hawkish shift

BoJ board member Asahi Noguchi, long seen as one of the most dovish voices on the Board, struck a notably hawkish tone today. He argued that Japan is making steady progress toward its 2% inflation goal, citing stronger wage momentum and greater corporate willingness to pass on rising costs.

Noguchi said the “need to adjust the policy interest rate is increasing more than ever,” highlighting that upside risks to prices and growth now outweigh the downside. He noted the labor market is "close to full employment" and the output gap has "almost reached zero", warranting a shift in policy perspective to address rising inflation risks.

His comments mark a significant departure from his usual stance, adding to expectations that the BoJ could deliver another rate hike in the near future. Noguchi did caution that U.S. tariffs remain a source of downside risk, but the overall message suggests growing consensus within the Board for normalization.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.28; (P) 149.62; (R1) 149.83; More...

Intraday bias in USD/JPY stays neutral for the moment and some more consolidations could be seen below 149.95 temporary top. Further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall back to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

BoJ dove Noguchi signals hawkish shift

BoJ board member Asahi Noguchi, long seen as one of the most dovish voices on the Board, struck a notably hawkish tone today. He argued that Japan is making steady progress toward its 2% inflation goal, citing stronger wage momentum and greater corporate willingness to pass on rising costs.

Noguchi said the “need to adjust the policy interest rate is increasing more than ever,” highlighting that upside risks to prices and growth now outweigh the downside. He noted the labor market is "close to full employment" and the output gap has "almost reached zero", warranting a shift in policy perspective to address rising inflation risks.

His comments mark a significant departure from his usual stance, adding to expectations that the BoJ could deliver another rate hike in the near future. Noguchi did caution that U.S. tariffs remain a source of downside risk, but the overall message suggests growing consensus within the Board for normalization.

EUR/USD Gains on US Shutdown Fears and Data Watch

The EUR/USD pair extended gains for a second consecutive session, trading around 1.1727. The move reflects market concerns over a potential US government shutdown and caution ahead of key economic releases due this week.

A partial shutdown of US federal agencies could begin as early as Wednesday if Congress fails to pass a funding bill before the fiscal year ends on Tuesday. President Donald Trump is scheduled to meet with congressional leaders in an effort to reach a compromise.

Investor attention is also focused on upcoming US data, including the September non-farm payrolls report, JOLTS job openings, the ADP private employment survey, and the ISM manufacturing index. Strong indicators last week have tempered expectations for aggressive Fed easing, with markets now pricing in roughly 40 basis points of rate cuts by year-end.

Broad-based US dollar weakness has provided additional support for the euro.

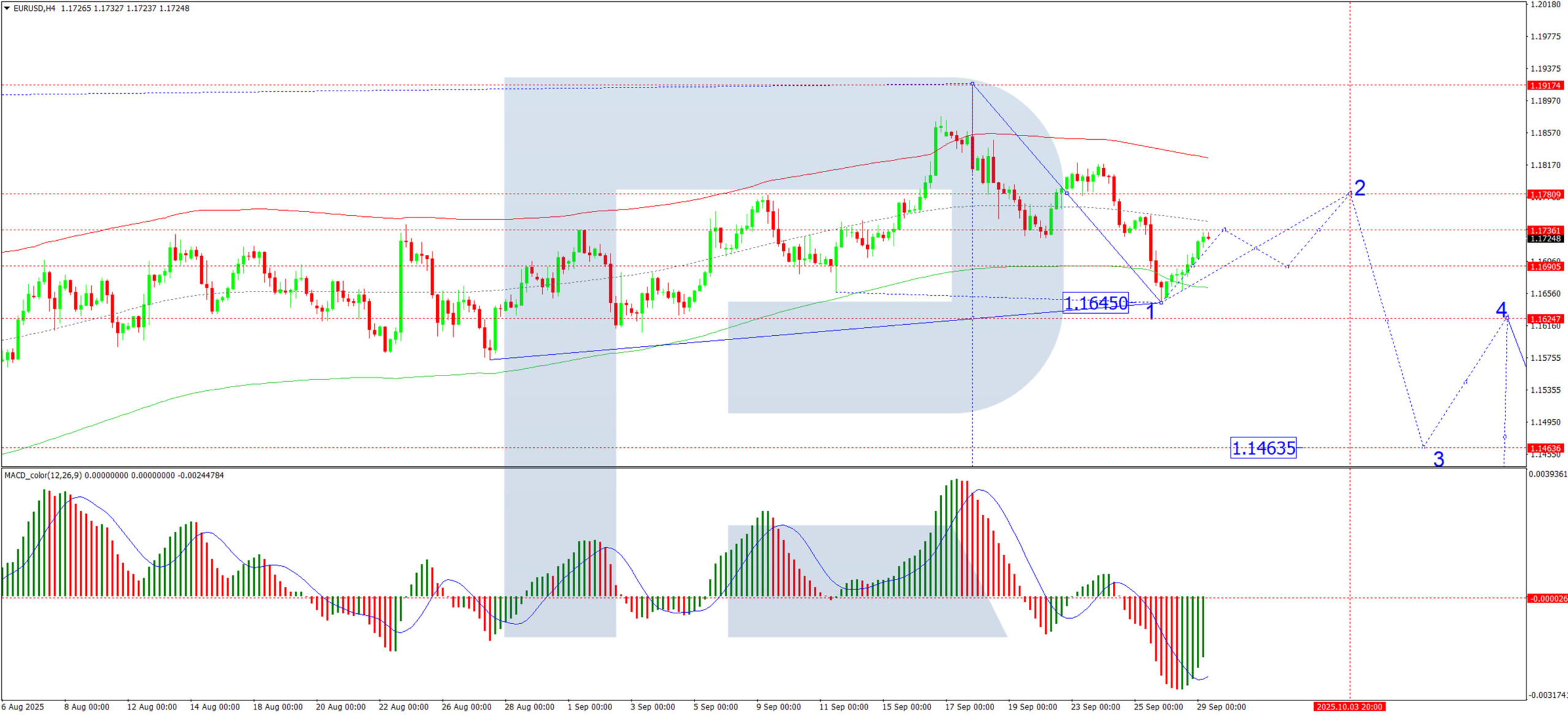

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, EUR/USD established a consolidation range above 1.1645 before breaking upward into a corrective phase. We expect the pair to advance toward 1.1730, followed by a pullback to 1.1695. A subsequent rise toward 1.1780 is anticipated, at which point the corrective potential is likely to be exhausted. A new decline toward 1.1625 may then develop. The MACD indicator supports this view, with its signal line below zero but exiting the histogram zone—suggesting potential upward momentum toward the zero line.

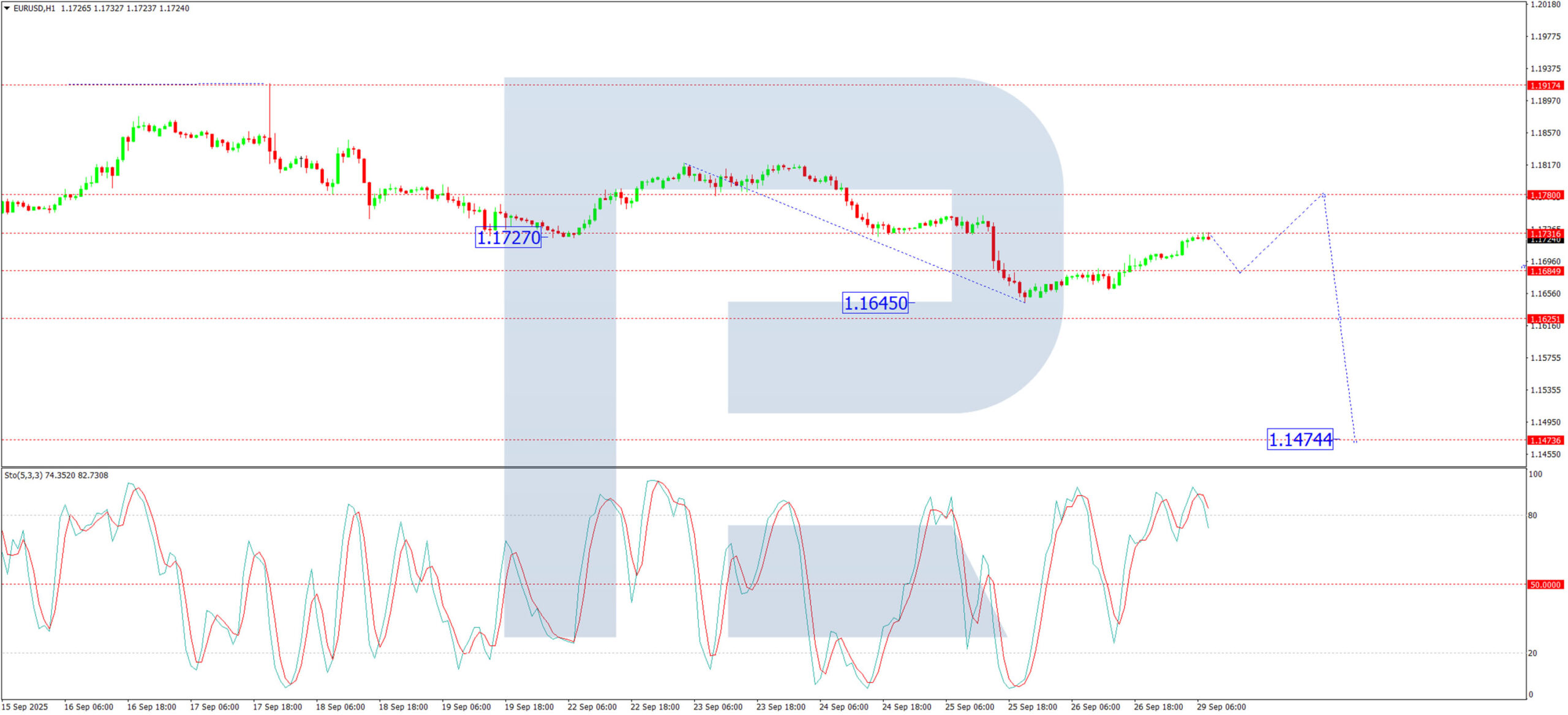

H1 Chart:

The H1 chart shows the completion of a decline to 1.1645, followed by the formation of a corrective structure. The initial advance to 1.1730 appears complete. A dip toward 1.1695 is possible before another rise toward 1.1780. Once this correction concludes, a new decline toward 1.1625 is expected. A break below this level could open the way toward 1.1470. The Stochastic oscillator aligns with this outlook, with its signal line above 80 and turning downward toward 20.

Conclusion

EUR/USD is drawing support from US fiscal uncertainty and a softer dollar, though the broader technical structure remains corrective. Traders are likely to remain cautious ahead of critical US employment and activity data, which may determine the near-term direction for the pair.

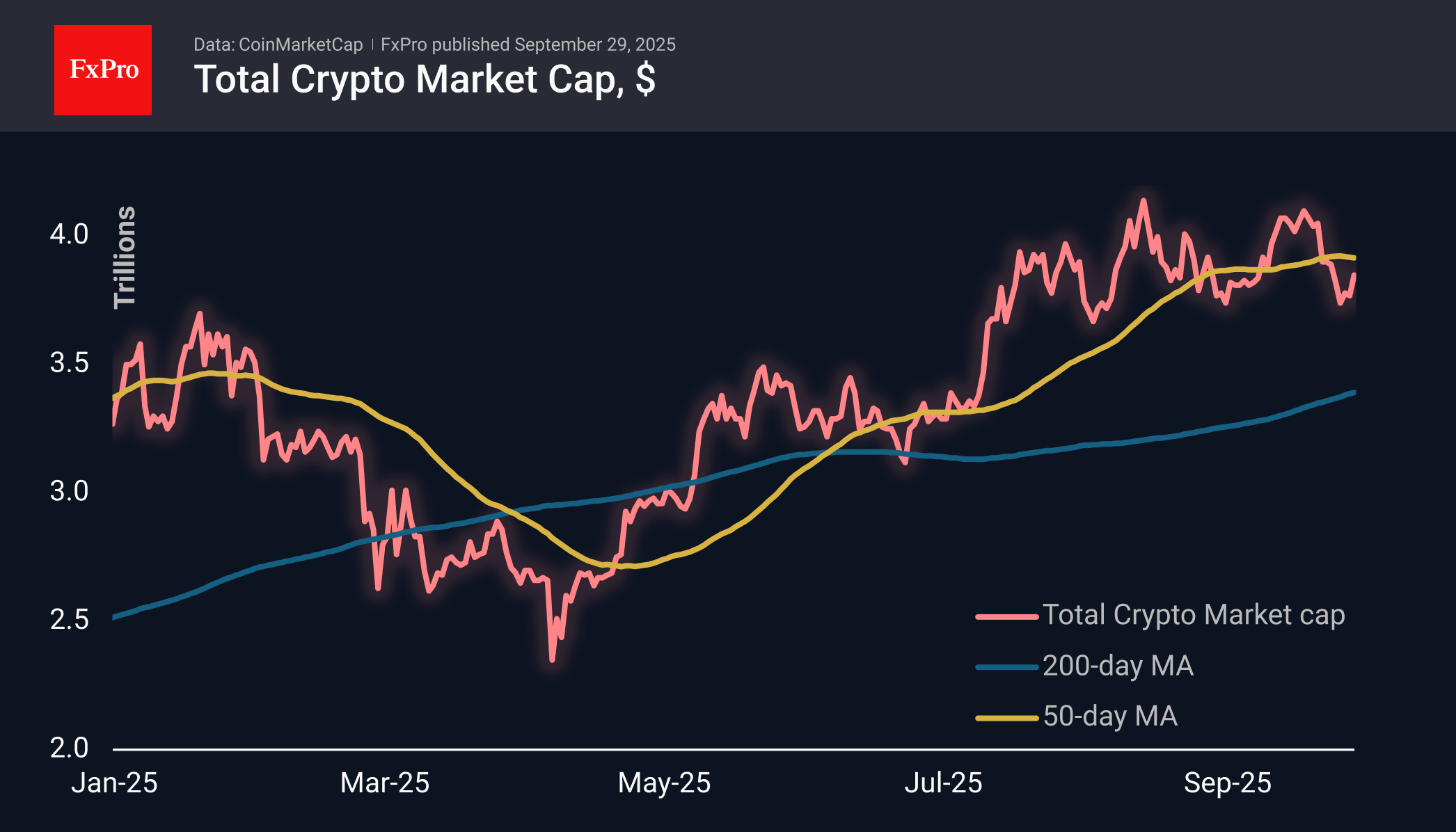

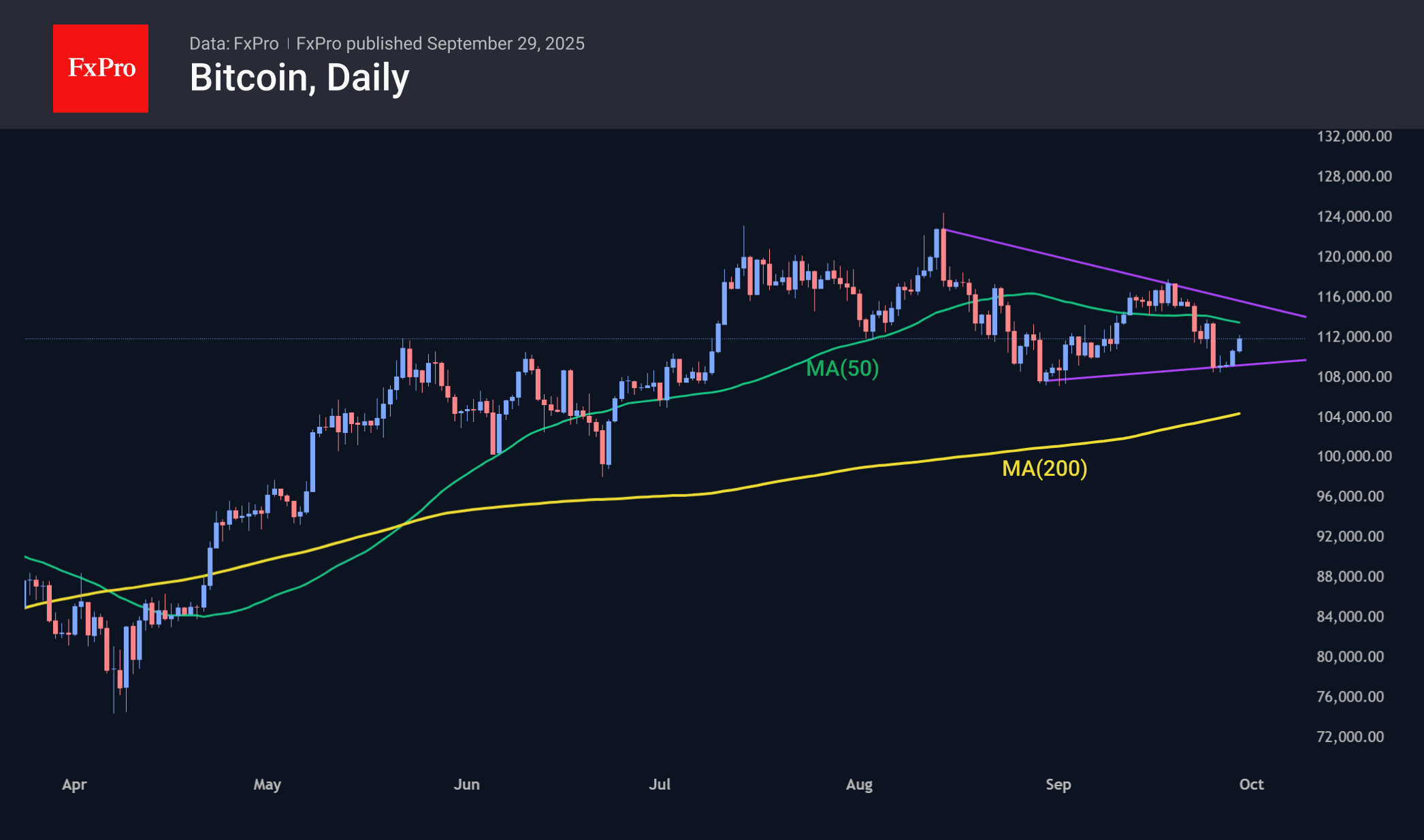

Crypto Market Attempts to Form a Double Bottom

Market Picture

The crypto market has been gaining since the start of the day on Friday, adding 3.5% during this time to $3.85 trillion, but still 1.3% below the level of a week earlier. The rebound is coming from roughly the same levels as in early September. Once again, altcoins are recovering stronger than BTC. Such outperformance in the early stages of recovery often indicates the future winners of the race, which in this case are altcoins.

The sentiment index fell to 28 on Friday but recovered to 50 by Monday. The approach to the extreme fear zone seems to have activated optimists, who began to buy back the drawdown. However, cautious traders will likely prefer to wait for the results of the 50-day moving average test, which is currently passing through $3.92 trillion.

At the end of last week, Bitcoin found support at $109K. It was bought at roughly the same levels as the end of August and even slightly higher, which is positive for the bulls. On the other hand, September’s local high is lower than the previous one, which generally indicates a decrease in volatility and a stronger movement towards a breakout beyond the $108-118K range. Movements within the range can give many false short-term signals.

News Background

Santiment has recorded a surge in mentions of “buy on dip,” which may indicate the likelihood of an imminent rebound. In addition, whales continue to accumulate BTC, and the supply of Bitcoin on exchanges is declining.

However, Glassnode warns of a continued correction, given growing selling pressure from long-term holders and declining institutional demand for ETFs. The first Ethereum ETF with a staking feature from REX Shares and Osprey Funds has launched in the US. Investors will receive monthly payments for supporting the ETH network. Applications from BlackRock and Fidelity are still being reviewed by the SEC.

Ethereum has begun to show signs that a local bottom has likely been reached, notes analyst Mikybull Crypto. The RSI oscillator on daily charts has fallen to its lowest levels since April, when ETH was trading around $1,400.

According to the Wall Street Journal, US regulators are investigating cases of potential insider trading involving companies that accumulate cryptocurrencies in their reserves. The SEC and FINRA have already sent inquiries to a number of companies.

Rating agency Moody’s warns that the rapid expansion of cryptocurrencies’ use in developing countries, including stablecoins, poses risks to monetary sovereignty and financial stability.