Sample Category Title

RBA holds steady at 3.60%, warns Q3 inflation may surprise on upside

The RBA left its cash rate unchanged at 3.60% in a unanimous decision, in line with expectations. The move reflects the Board’s preference to pause while monitoring whether recent economic surprises point to a more persistent inflation challenge.

According to the RBA, recent partial data suggest that September-quarter inflation may come in above projections made in August. At the same time, labor market indicators show conditions have been steady and remain "a little tight", reinforcing the risk that price pressures may not ease as quickly as anticipated.

The Bank outlined two contrasting scenarios for household demand. Stronger consumption may reflect rising real incomes and wealth, potentially allowing firms to raise prices more easily and encouraging further hiring. Alternatively, this consumption rebound may not last if households turn more cautious amid uncertainty around overseas developments.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate unchanged at 3.60 per cent.

The decline in underlying inflation has slowed.

Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and potential supply closer towards balance. Both headline and trimmed mean inflation were within the 2–3 per cent range in the June quarter. Recent data, while partial and volatile, suggest that inflation in the September quarter may be higher than expected at the time of the August Statement on Monetary Policy.

Domestic economic activity is recovering but the outlook remains uncertain.

Data for the June quarter show that private demand is recovering a little more rapidly than expected, taking over from public demand as the driver of growth. In particular, private consumption is picking up as real household incomes rise and measures of financial conditions ease. The housing market is strengthening, a sign that recent interest rate decreases are having an effect. Credit is readily available to both households and businesses.

Various indicators suggest that labour market conditions have been broadly steady in recent months and remain a little tight. Growth in employment has slowed by slightly more than expected, but the unemployment rate was unchanged at 4.2 per cent in August. Measures of labour underutilisation remain at low rates and business surveys and liaison suggest that availability of labour has been little changed of late. Looking through quarterly volatility, wages growth has eased from its peak, but productivity growth has been weak and growth in unit labour costs remains high.

There are uncertainties about the outlook for domestic economic activity and inflation stemming from both domestic and international developments. On the domestic side, stronger-than-expected data on growth and inflation may indicate that households have become more comfortable consuming as real incomes and wealth rise. If this continues, it may make it easier for businesses to pass on cost increases and lead to more demand for labour. Alternatively, the recent growth in consumption might not persist, particularly if households become more concerned about overseas developments.

Uncertainty in the global economy remains elevated. There is a little more clarity on the scope and scale of US tariffs and policy responses in other countries, suggesting that more extreme outcomes are likely to be avoided. Trade policy developments are nevertheless still expected to have an adverse effect on global economic growth over time. Beyond tariffs, a broader range of geopolitical risks remain a threat to the global economy. This could all weigh on growth in aggregate demand and lead to weaker labour market conditions in the domestic economy.

There are also uncertainties regarding the lags in the effect of recent monetary policy easing, the balance between aggregate demand and potential supply for goods and services, conditions in the labour market and the outlook for productivity.

Maintaining price stability and full employment is the priority.

With signs that private demand is recovering, indications that inflation may be persistent in some areas and labour market conditions overall remaining stable, the Board decided that it was appropriate to maintain the cash rate at its current level at this meeting. Financial conditions have eased since the beginning of the year and this seems to be having some impact, but it will take some time to see the full effects of earlier cash rate reductions. The Board judged that it was appropriate to remain cautious, updating its view of the outlook as the data evolve. The Board remains alert to the heightened level of uncertainty about the outlook. It noted that monetary policy is well placed to respond decisively to international developments if they were to have material implications for activity and inflation in Australia.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

Decision

Today’s policy decision was unanimous.

China’s NBS PMI points to easing manufacturing weakness, services soft patch

China’s official PMI data for September signaled tentative improvement in industry but lingering softness in services.The NBS Manufacturing PMI rose to 49.8 from 49.4, its highest since March, though it still pointed to contraction. The gauge has been under 50 since April, reflecting headwinds for large and state-linked producers.

The NBS Non-Manufacturing PMI slipped from 50.3 to 50.0, effectively flatlining and pointing to a loss of momentum in construction and services. That stagnation raises questions about the strength of domestic demand, even as authorities step up stimulus efforts.

In contrast, the RatingDog (S&P Global) surveys offered a more optimistic take. Manufacturing improved to 51.2 from 50.5, the strongest since May, suggesting that private and export-focused companies are benefiting from external demand. Services edged down slightly from 53.0 to 52.9 but remained firmly in growth territory.

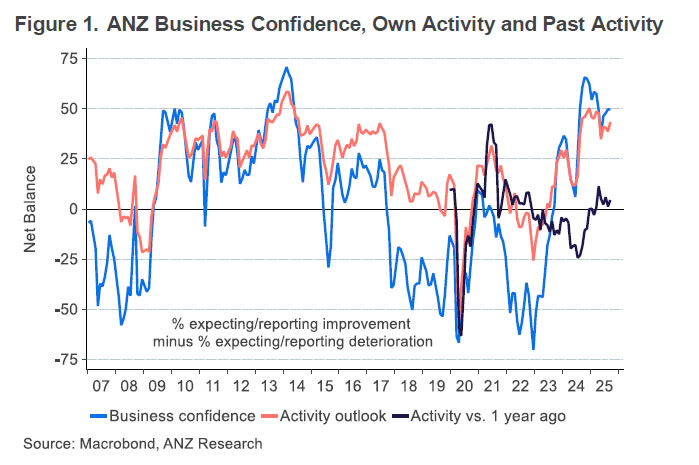

NZ ANZ business confidence ticks down, but activity outlook improves

New Zealand’s ANZ Business Confidence edged slightly lower in September, slipping from 49.7 to 49.6. Though, Own Activity Outlook improved to 43.4 from 38.7.

Inflation pressures ticked mildly higher. One-year-ahead inflation expectations rose to 2.71% from 2.63%,. The share of firms expecting to raise prices in the next three months climbed to 46%. Cost expectations also edged up, with 75% of respondents seeing higher input costs.

ANZ noted that the RBNZ is positioned to support growth with a lower Official Cash Rate. While the exact path of policy easing remains uncertain, the bank said the OCR will ultimately reach the level required to ensure the recovery takes hold.

Gold Hits New Record – Could Bulls Drive Price Toward Next Milestone?

Key Highlights

- Gold extended its rally and traded to a new record high above $3,850.

- A key bullish trend line is forming with support at $3,785 on the 4-hour chart.

- WTI Crude Oil prices failed to recover above $66.50 and trimmed gains.

- EUR/USD could struggle to clear the 1.1780 and 1.1800 resistance levels.

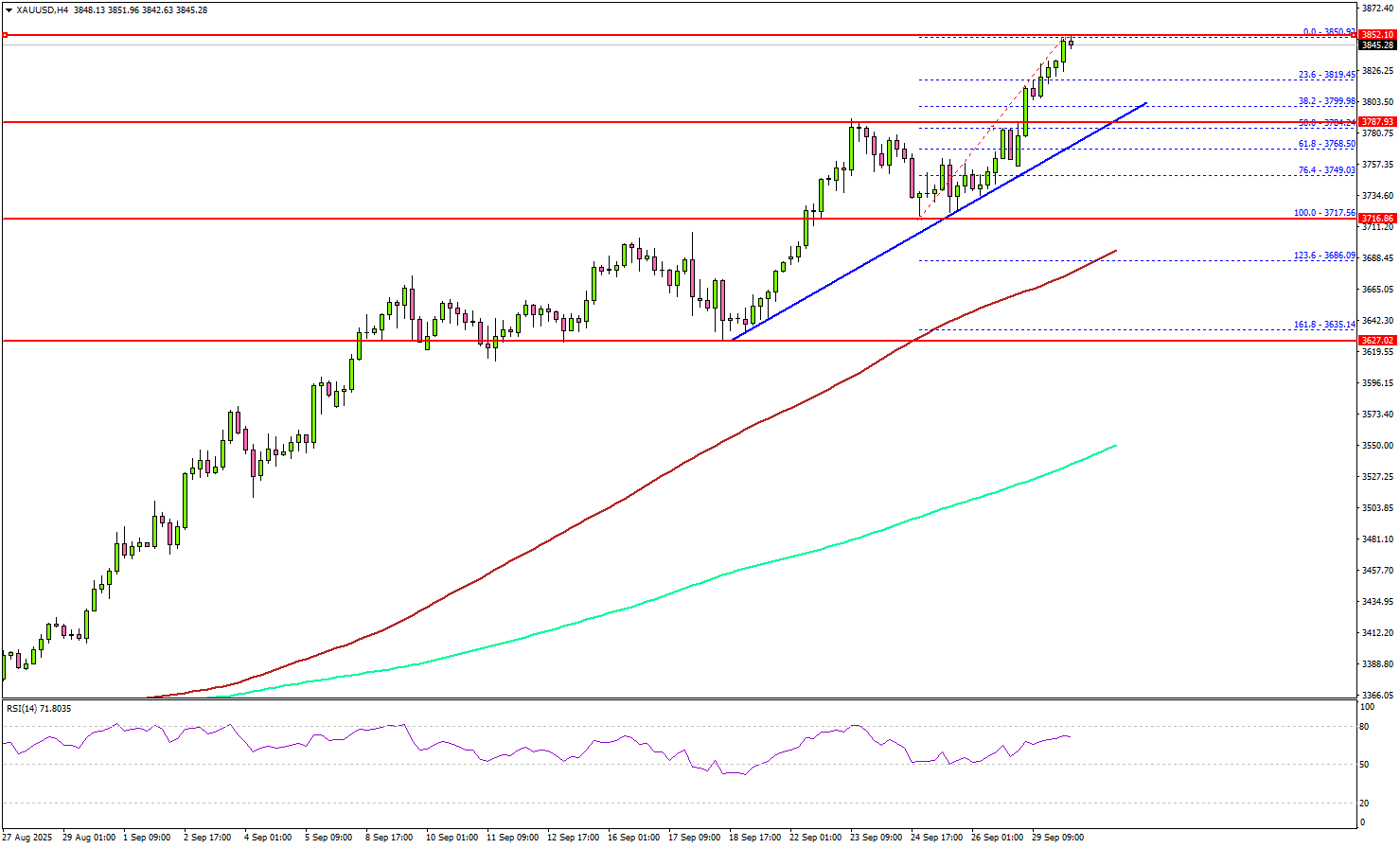

Gold Price Technical Analysis

Gold prices formed a base above $3,720 and started a fresh increase against the US Dollar. It cleared many hurdles near $3,750 and $3,800.

The 4-hour chart of XAU/USD indicates that the price settled above the $3,800 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours). The upward move was such that the price spiked above $3,850.

Gold traded to a new record high near $3,851 and might continue to rise. On the upside, immediate resistance is near the $3,855 level. The next major resistance sits near the $3,865 level.

A clear move above $3,865 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $3,900, above which the price could rally toward the milestone level of $4,000.

On the downside, initial support is near the $3,800 level. The first key support is $3,785. There is also a key bullish trend line forming with support at $3,785 on the same chart. The next major support is near the $3,750 level.

A downside break below $3,750 might call for more downsides. The next key zone to watch could be $3,690 and the 100 Simple Moving Average (red, 4 hours).

Looking at WTI Crude Oil, the price attempted a decent recovery wave, but the bears remained active near the $66.50 level.

Economic Releases to Watch Today

- US Housing Price Index for July 2025 (MoM) - Forecast +0.1%, versus -0.2% previous.

- ECB's Nagel speech.

- Fed's Goolsbee speech.

Japan’s industrial output falls -1.2% mom in August, retail sales contracts

Japan’s latest data painted a downbeat picture of economic momentum in August. Industrial production slipped -1.2% mom, falling short of the expected -0.8%. Of the 15 industrial sectors, 12 including metal products, and inorganic and organic chemicals, saw output decreases.

METI maintained its description of output as "fluctuates indecisively". Officials stressed that firms remain highly cautious in their production planning. Still, manufacturers surveyed see output rising 4.1% in September and another 1.2% in October.

Household demand faltered at the same time, with retail sales tumbling -1.1% yoy, marking the first decline in 42 months.

BoJ summary reveals rising hawkish pressure, but board still divided

The BoJ’s September Summary of Opinions revealed that members debated the feasibility of raising interest rates in the near term, with some arguing that conditions were aligning for another move. The release underscores a growing hawkish tilt inside the Board, even as the majority voted to hold steady at 0.50%.

One member argued that “judging solely from the perspective of Japan’s economic conditions, it may be time to consider raising the policy interest rate again,” noting that more than six months have passed since the last hike. Another highlighted easing concerns from U.S. tariffs, suggesting external impact on inflation had "abated" and that the BoJ could “return to its stance to raise the policy interest rate.”

At the same time, caution was evident. Some warned against surprising markets with a hike, stressing that Japan’s domestic demand remains vulnerable to external shocks. The view was that it would be better to wait for more hard data before making another adjustment.

At the September 18–19 meeting, the BoJ left rates at 0.50%, though two members dissented in favor of a hike to 0.75%.

Fed’s Musalem open to cuts but urges cautions

St. Louis Fed President Alberto Musalem said monetary policy is now “somewhere between modestly restrictive and neutral.”

Musalem, who votes on policy this year, said he is “open minded” to further rate cuts but stressed that caution is needed. With limited room before policy turns "overly accommodative", he signaled the Fed should proceed carefully.

Fed’s Williams: Makes sense to ease policy a little bit to support jobs

New York Fed President John Williams said overnight that it made sense for the central bank to ease policy “a little bit” to reduce restrictiveness to support the labor market while maintaining downward pressure on inflation.

Williams acknowledged progress toward the 2% inflation target but cautioned that more work remains. He underscored the Fed’s dual mandate, stressing the need to avoid “undue harm” to employment at a time when job creation has been gradually weakening. “I don’t want to see that go too far,” he said.

Encouragingly, Williams noted that some inflation worries have eased ""The tariff effects have been smaller than most people thought, and there doesn't seem to be any signs of inflationary pressures building," he noted.

Aussie Grinds It Out in the Mid-0.65s

AUD/USD starts the week on slightly steadier ground (0.6570). The looming risk of a US government shutdown from 1 Oct has seen the USD open the week with a broadly softer tone. Negotiations over a short-term bill to keep the federal government funded through to mid-Nov are ongoing. US Sept payrolls on Friday headlines the global calendars, but the release depends entirely on whether the US government stays open. Locally, the focus is on the RBA policy meeting tomorrow.

Aussie grinds it out in the mid-0.65s

AUD/USD starts the week on slightly steadier ground (0.6570). The looming risk of a US government shutdown from 1 Oct has seen the USD open the week with a broadly softer tone. Negotiations over a short-term bill to keep the federal government funded through to mid-Nov are ongoing. US Sept payrolls on Friday headlines the global calendars, but the release depends entirely on whether the US government stays open. Locally, the focus is on the RBA policy meeting tomorrow.

AUD/USD's pullback from its mid-Sept 0.6707 highs extended a little further last week, the pair touching a low of 0.6521, mostly due to a round of constructive US data at the back end of the week. The AUD-side of the equation is doing just fine. In fact, local markets are walking back RBA rate cut expectations. But this is not enough to sustain AUD/USD while US data is also beating expectations.

The third and final update to US Q2 GDP was revised up notably, to a punchy 3.8% annualised pace, on account of stronger private services consumption and business investment (AI/data centers). On the same day US jobless claims fell to 218k, pretty much the lowest reading of the year, while durable goods orders rose by more than expected.

This mix of data soothed jitters about an economy that is facing a significant tariff impost and a material reduction in immigration. If sustained, this kind of data has the potential to make amends and subdue a lot of bearish medium term USD thinking.

But the US labour market isn't showing anywhere near the same kind of momentum. Job openings have been trending lower and hiring intentions have cooled a lot. The consensus for this week's US Sept payrolls is for a +50k increase. That would be pretty much in line with the pace of the last 6 months - soft - and well down from the trend pace back in Q1, which was closer to +175k. The unemployment rate commands as much, if not more attention. Immigration restrictions have dramatically slowed the growth of the US labour force, so even with soft employment growth, the unemployment rate isn't rising much. If a US government shutdown is not averted, this marquee release will be delayed.

Last week's (August) monthly CPI indicator produced a commotion for local markets - not for the first time, even though it is less detailed and representative than the full quarterly CPI survey. Australia's monthly CPI YoY gauge printed stronger-than-expected at 3.0% (vs exp 2.9%) driven by lifts in fuel, dwelling and services prices which were somewhat offset by falling electricity prices.

The big question is whether this signals a stronger underlying inflation pulse. We'll find out when Q3 CPI is released 29 Oct. At the very least, the widespread view is that a benign looking 0.7% q/q increase in the trimmed mean quarterly CPI is much less likely. Westpac has revised its forecast up to 0.8% and other forecasters have pencilled in higher forecasts.

Rates markets trimmed expectations for the RBA's November meeting in the wake of the monthly CPI indicator, taking down the probability of a cut to almost a line-ball 50-50 call. The next full RBA rate cut is not priced until Feb 2026 and the terminal rate is priced around 3.28%.

That's quite a step change from where things stood a few weeks ago, when markets were confidently predicting a Nov RBA rate cut (pricing it at -22bp), anticipating a follow up in Feb 2026 and the terminal rate was priced below 3.00%.

How is the RBA going to play it this week? There's a pretty good chance that the Bank will note that private consumption is on surer footing. Governor Bullock will likely repeat her comments to Parliament last week that, "Since the August meeting, domestic data have been broadly in line with our expectations or if anything slightly stronger". Assistant Governor Hunter was a little bolder, describing the economy in a “cyclical upturn” at the same appearance.

This kind of language doesn't amount to a "hawkish pivot", not even close. But it sure seems to imply a higher bar for cuts. At the same time, the Governor will no doubt stress that Q3 CPI Oct 30 will be determinative. All told, this speaks to a Bank that will continue with a cautious and gradual approach to policy, as it has long underscored.

AUD had been quietly ceding ground on crosses (ex-AUD/JPY and AUD/NZD) in the days prior to the monthly CPI release. AUD/EUR and AUD/JPY were testing 1 and 2 week lows respectively. The stronger monthly CPI produced good sized rebounds for both, though the gains have not really stuck. AUD/EUR is at 0.5600 to start the week, while AUD/JPY trading around 97.65.

AUD/NZD continued to extend its already impressive run, taking out 1.1300 last week and settling in the mid-1.13s, its highest levels in 3 years. Both legs of this cross want to run in opposite directions and the net result is that the AUD/NZD cross has been breaking higher impulsively in recent weeks.

Private domestic demand appears to be on surer ground in Australia and RBA rate cut expectations have been trimmed. However across the Tasman, fledging activity green shoots have come a cropper. Q2 GDP a few weeks ago contracted a lot more than expected and markets are giving a non-negligible chance for a larger 50bp RBNZ rate cut in early October.

For a good part of September, US equities were printing record highs almost daily. But the tide turned a little last week, with the S&P500 down almost 1%. US 10-year yields trailed higher over the week up from 4.13% to 4.17%.

Gold continued its impressively surge higher capping out just under $3800/oz last week, up almost 9% over the month as steady inflation numbers increased expectations of further Fed easing. Copper marked its largest weekly gain in 3-months climbing by over 4% last week to just under $10500 on the back of global supply shortage concerns

Japan's ruling Liberal Democratic Party is scheduled to elect a new leader following the resignation of Shigeru Ishiba. The two favoured candidates are Shinjiro Koizumi and Sanae Takaichi, with the former larger leading the latter in polls conducted among LDP voters.

China will also be commencing its Golden Week Holiday this week (Oct 2-8) which should see fairly neutral price action across Iron ore futures.

Tuesday

- China Sep Manufacturing & Non-manufacturing PMI

- Australia Aug Building Approvals

- RBA Monetary Policy Meeting

- UK Q2 GDP (Final)

- US Aug JOLTS Job Openings

- Fedspeak; Logan, Goolsbee

Wednesday

- China Golden Week Holiday commences (1 - 8 Oct)

- Australia, Japan, UK, Eurozone, US Sep Manufacturing PMIs (Final)

- Australia Sep Cotality Home Value

- Eurozone Sep CPI (Prelim.)

- US Sep manufacturing ISM survey

Thursday

- Australia Aug Trade Balance, Household Spending

- RBA Semi-Annual Financial Stability Review

- Fedspeak; Logan

Friday

- Australia, Japan, Eurozone, UK & US Sep Services PMIs (Final)

- US Sep Non-farm payrolls, ISM services

Saturday

- Japan's ruling LDP party to elect new Leader/PM (Oct 4)