Sample Category Title

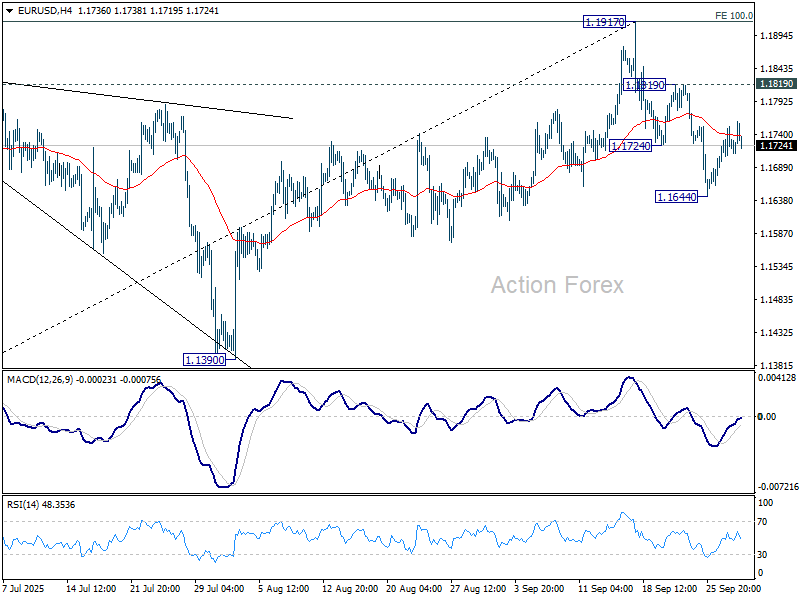

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1700; (P) 1.1728; (R1) 1.1754; More...

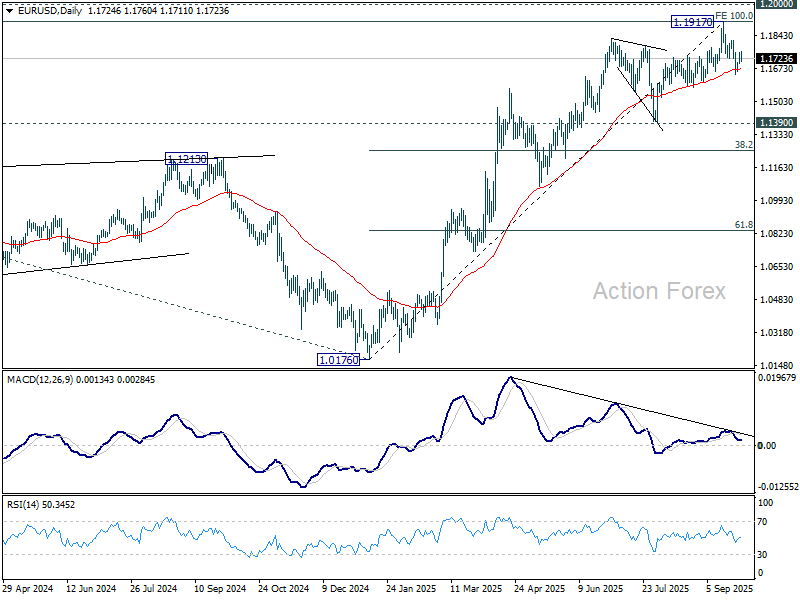

Intraday bias in EUR/USD stays neutral for the moment. Further fall is expected as long as 1.1819 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1670) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

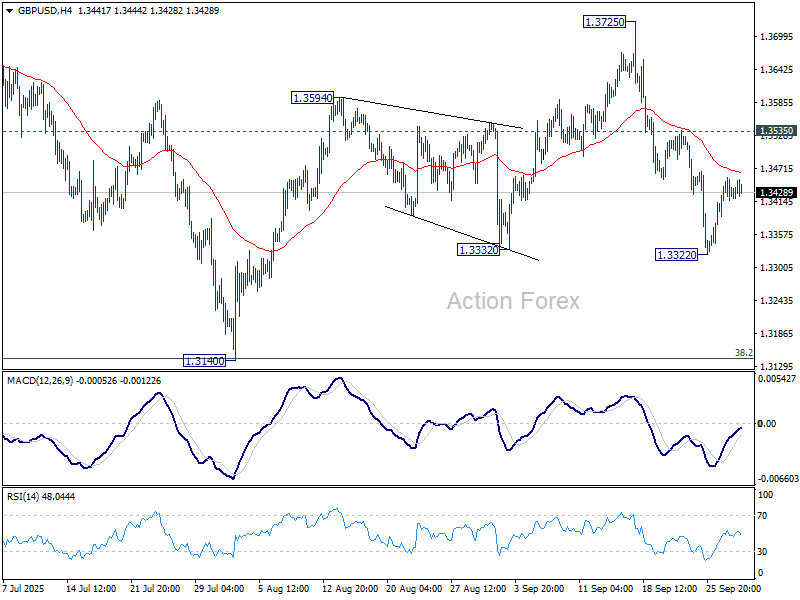

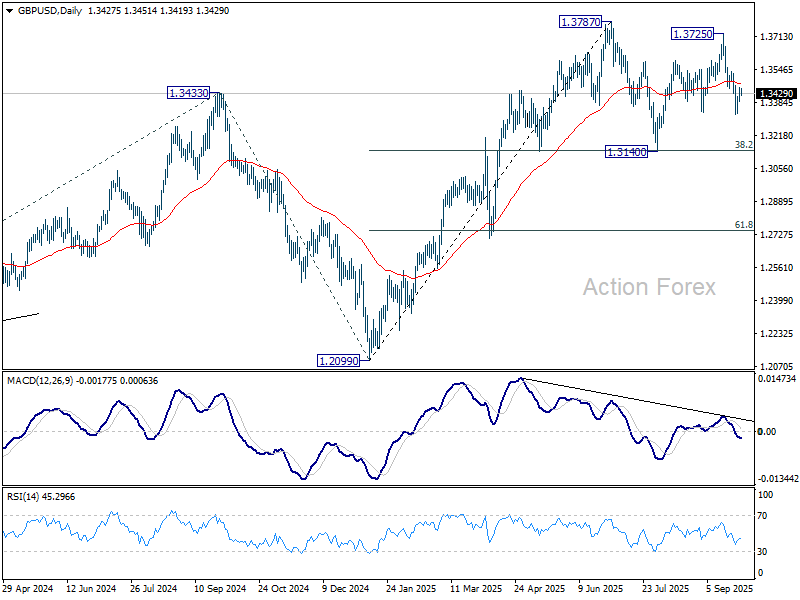

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3394; (P) 1.3426; (R1) 1.3458; More...

Intraday bias in GBP/USD remains neutral for the moment. Further decline is expected as long as 1.3535 resistance holds. Break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

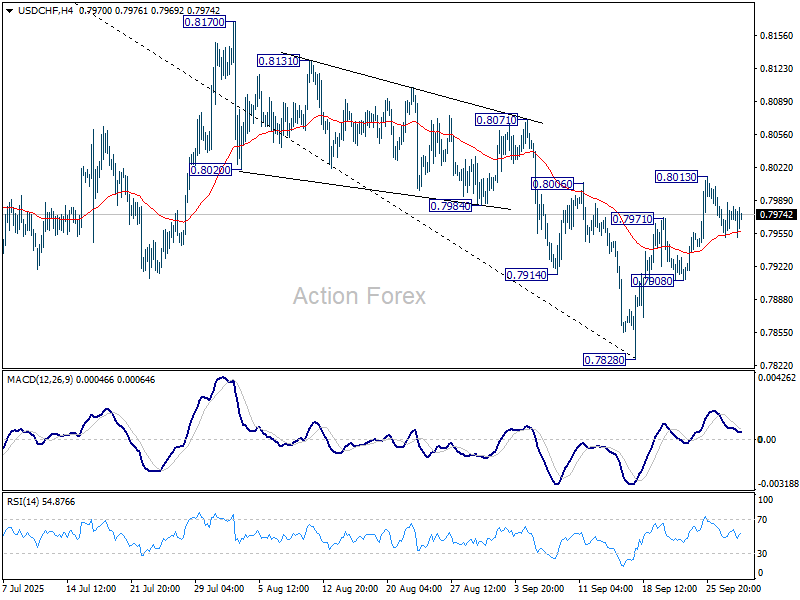

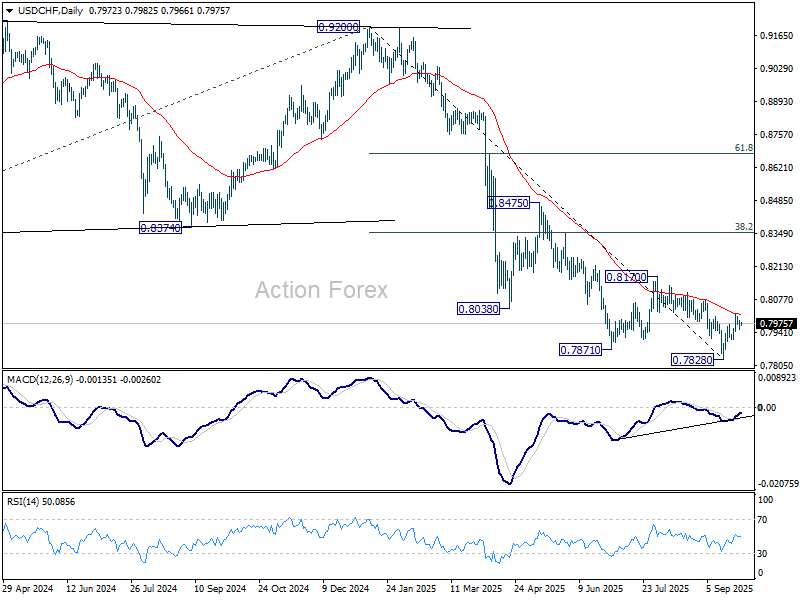

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7957; (P) 0.7972; (R1) 0.7993; More…

Intraday bias in USD/CHF remains neutral for the moment. On the upside, sustained trading above 55 D EMA (now at 0.8014) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

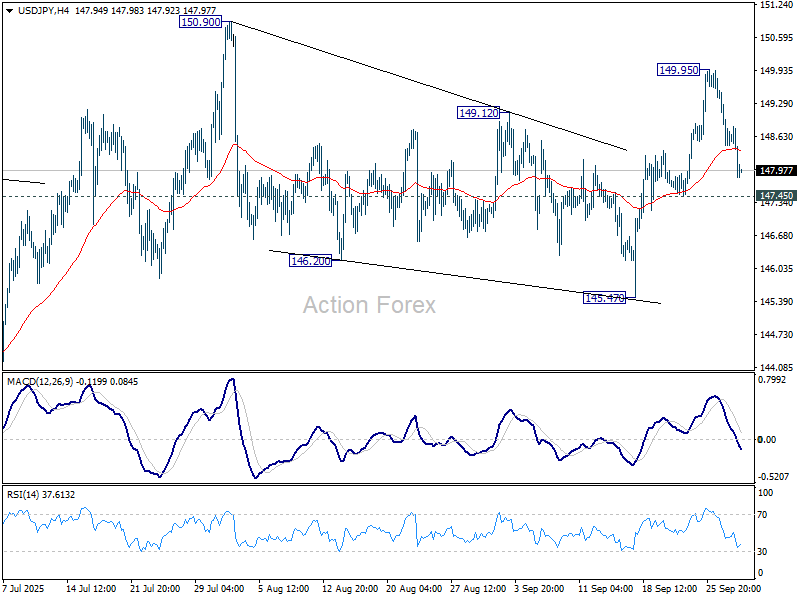

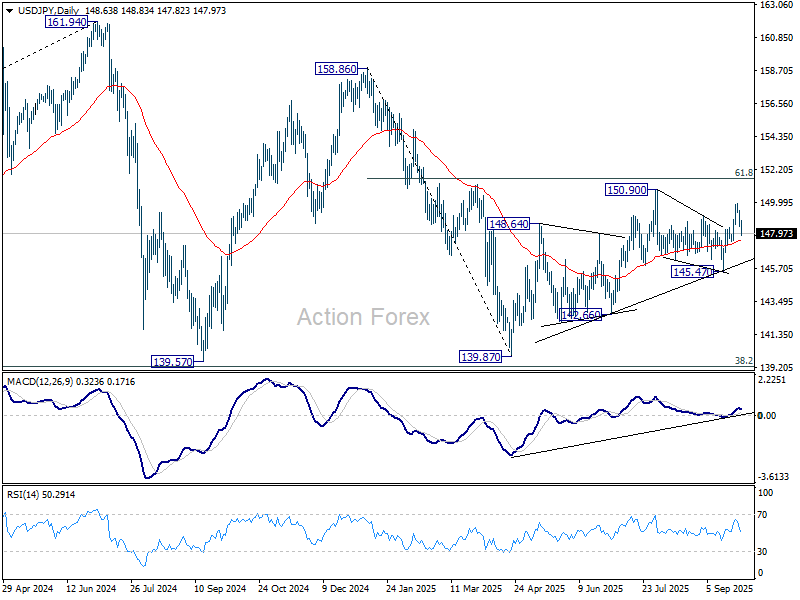

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.15; (P) 148.92; (R1) 149.37; More...

No change in USD/JPY's outlook and intraday bias stays neutral first. Further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall back to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

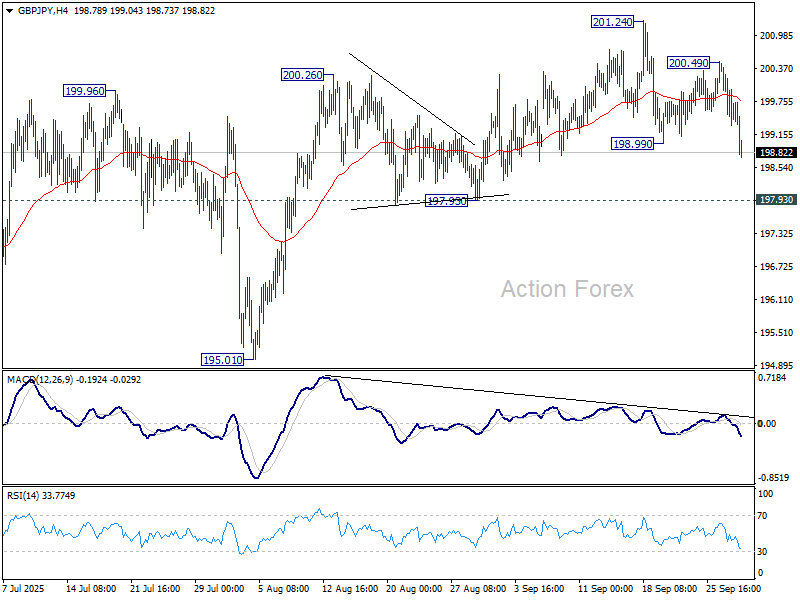

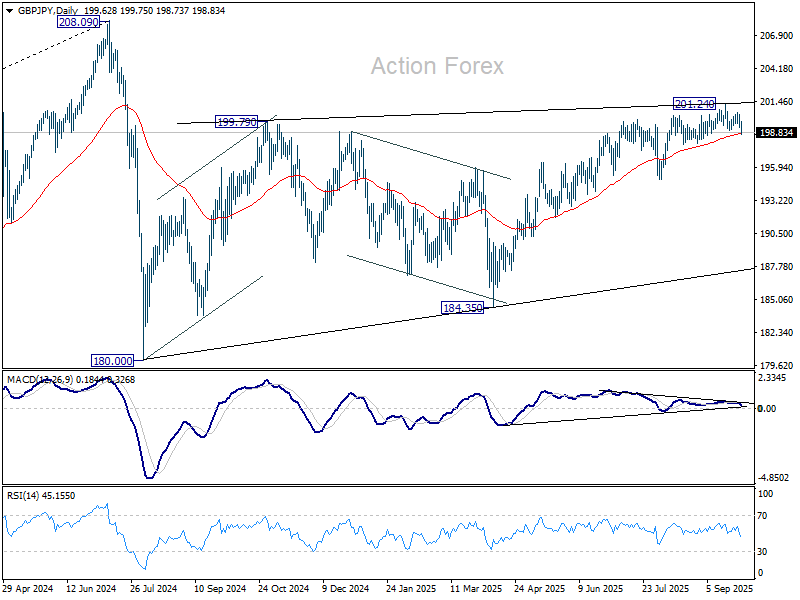

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 199.10; (P) 199.82; (R1) 200.30; More...

Intraday bias in GBP/JPY is back on the downside with break of 198.99. A short term top should be formed at 201.24, on bearish divergence condition in 4H MACD. Deeper fall should be seen to 197.93 support first. Firm break there will argue that whole rise from 184.35 has completed too and target 195.01 support next. For now, risk will stay on the downside as long as 200.49 support holds, in case of recovery.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Markets Cautious at Quarter-End, Aussie and Yen Lead FX

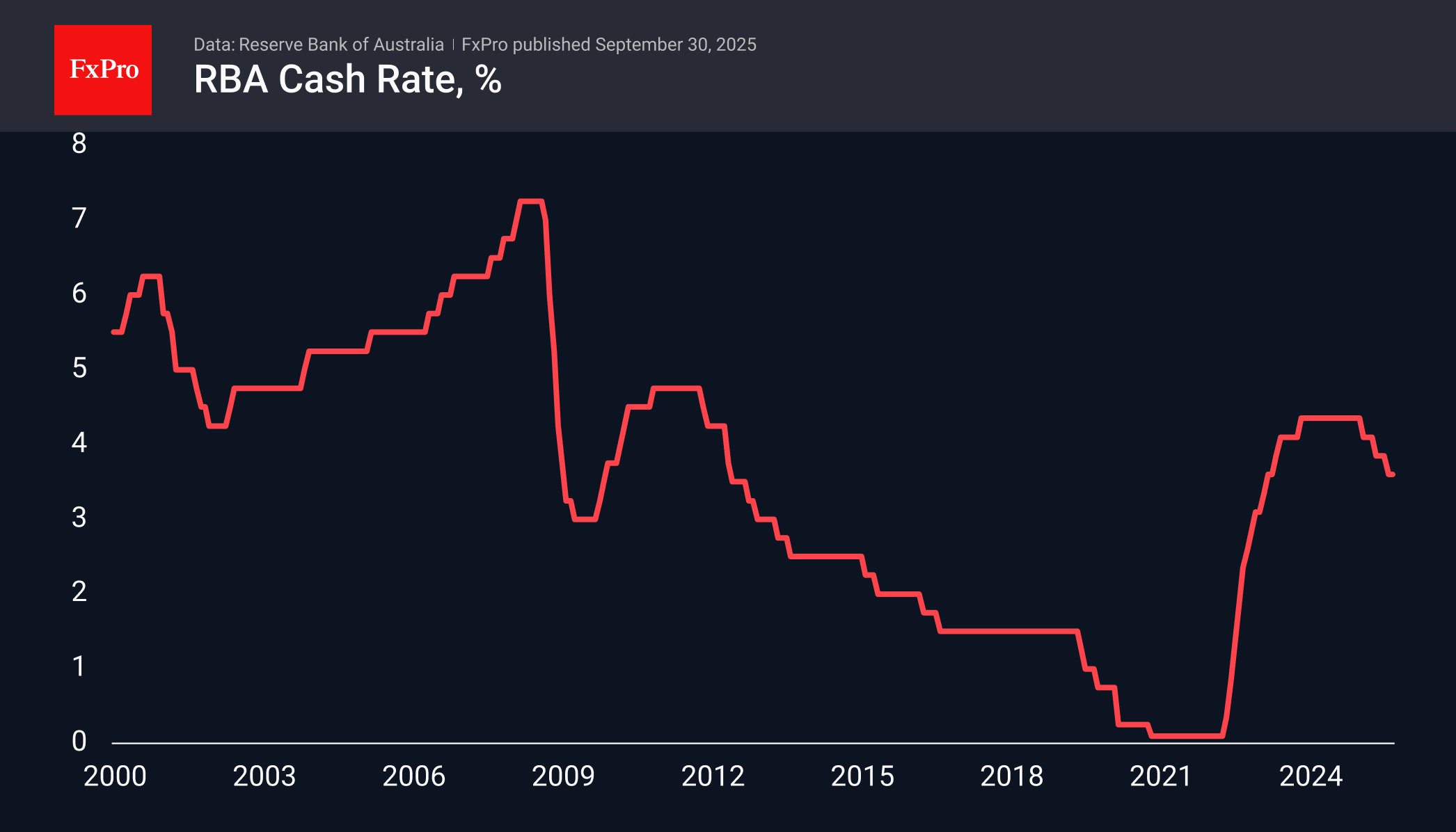

Australian Dollar is staying the day’s top performer, rallying after the RBA kept its cash rate unchanged but leaned hawkish in tone. Later at the press conference, Governor Michele Bullock avoided any firm guidance on future cuts, telling reporters she would not “predict what the interest rate is going to be in the next three to six months.”

Bullock emphasized that the current backdrop is “quite a positive situation,” pointing to inflation within the 2–3% target band and employment hovering around full employment. While monthly CPI has been volatile, she reiterated that the RBA continues to focus on the quarterly trimmed mean as its preferred measure of inflation. Her comments reinforced market expectations that November is a live meeting and that a cut is far from certain.

Meanwhile, Yen also strengthened broadly, supported by a cautious risk tone as the US edges closer to a partial government shutdown. At the same time, speculation is intensifying that the BoJ is preparing to hike rates in Q4. December appears the more likely timing, but October cannot be ruled out given the central bank’s track record of surprising markets. Importantly, the October meeting will include new economic projections that could provide the justification for an earlier move.

Some traders may already be positioning for a hawkish shift, particularly as BoJ officials have turned more vocal about the risks of sustained inflation. The Tankan survey and further guidance from policymakers will be critical in shaping expectations.

By performance, the Aussie leads FX, followed by Yen and Kiwi. Loonie lags at the bottom alongside Dollar and Swiss Franc, while Euro and Sterling are trading mid-pack.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.13%. CAC is down -0.26%. UK 10-year yield is up 0.004 at 4.709. Germany 10-year yield is up 0.009 at 2.721. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 0.87%. China Shanghai SSE rose 0.52%. Singapore Strait Times rose 0.71%. Japan 10-year JGB yield rose 0.004 to 1.651.

Fed's Jefferson sees labor market vulnerable if unsupported

Fed Vice Chair Philip Jefferson said in a speech today while tariffs have added to price pressures, the impact has been "lower than what many forecasters predicted" this spring. Encouragingly, short-term expectations have eased from Q2 highs, while long-term expectations remain anchored. As a result, he expects the disinflation process to "resume after this year" and inflation to eventually return to the Fed’s 2% target "in the coming years".

On the labor side, Jefferson highlighted softening conditions. He warned that the job market could "experience stress” if left unsupported, and said this was a key reason he backed a 25bp rate cut at the last FOMC meeting.

Looking ahead, Jefferson stressed that policy will remain data-dependent, with the Fed monitoring both economic indicators and government policies.

Swiss KOF barometer rises to 98.0, outlook still subdued

Switzerland’s KOF Economic Barometer rose to 98.0 in September from 96.2, beating expectations of 97.3. The improvement marks a rebound after last month’s dip, though the indicator still lingers below its long-term average, underscoring a "subdued" outlook.

According to KOF, the uptick was driven by stronger signals from manufacturing as well as financial and insurance services. These production-side sectors showed notable improvement, suggesting some resilience in key parts of the economy.

However, demand-side indicators were less encouraging. Foreign demand weakened, while the outlook for private consumption remained unchanged.

RBA holds steady at 3.60%, warns Q3 inflation may surprise on upside

The RBA left its cash rate unchanged at 3.60% in a unanimous decision, in line with expectations. The move reflects the Board’s preference to pause while monitoring whether recent economic surprises point to a more persistent inflation challenge.

According to the RBA, recent partial data suggest that September-quarter inflation may come in above projections made in August. At the same time, labor market indicators show conditions have been steady and remain "a little tight", reinforcing the risk that price pressures may not ease as quickly as anticipated.

The Bank outlined two contrasting scenarios for household demand. Stronger consumption may reflect rising real incomes and wealth, potentially allowing firms to raise prices more easily and encouraging further hiring. Alternatively, this consumption rebound may not last if households turn more cautious amid uncertainty around overseas developments.

BoJ summary reveals rising hawkish pressure, but board still divided

The BoJ’s September Summary of Opinions revealed that members debated the feasibility of raising interest rates in the near term, with some arguing that conditions were aligning for another move. The release underscores a growing hawkish tilt inside the Board, even as the majority voted to hold steady at 0.50%.

One member argued that “judging solely from the perspective of Japan’s economic conditions, it may be time to consider raising the policy interest rate again,” noting that more than six months have passed since the last hike. Another highlighted easing concerns from U.S. tariffs, suggesting external impact on inflation had "abated" and that the BoJ could “return to its stance to raise the policy interest rate.”

At the same time, caution was evident. Some warned against surprising markets with a hike, stressing that Japan’s domestic demand remains vulnerable to external shocks. The view was that it would be better to wait for more hard data before making another adjustment.

At the September 18–19 meeting, the BoJ left rates at 0.50%, though two members dissented in favor of a hike to 0.75%.

Japan's industrial output falls -1.2% mom in August, retail sales contracts

Japan’s latest data painted a downbeat picture of economic momentum in August. Industrial production slipped -1.2% mom, falling short of the expected -0.8%. Of the 15 industrial sectors, 12 including metal products, and inorganic and organic chemicals, saw output decreases.

METI maintained its description of output as "fluctuates indecisively". Officials stressed that firms remain highly cautious in their production planning. Still, manufacturers surveyed see output rising 4.1% in September and another 1.2% in October.

Household demand faltered at the same time, with retail sales tumbling -1.1% yoy, marking the first decline in 42 months.

China's NBS PMI points to easing manufacturing weakness, services soft patch

China’s official PMI data for September signaled tentative improvement in industry but lingering softness in services. The NBS Manufacturing PMI rose to 49.8 from 49.4, its highest since March, though it still pointed to contraction. The gauge has been under 50 since April, reflecting headwinds for large and state-linked producers.

The NBS Non-Manufacturing PMI slipped from 50.3 to 50.0, effectively flatlining and pointing to a loss of momentum in construction and services. That stagnation raises questions about the strength of domestic demand, even as authorities step up stimulus efforts.

In contrast, the RatingDog (S&P Global) surveys offered a more optimistic take. Manufacturing improved to 51.2 from 50.5, the strongest since May, suggesting that private and export-focused companies are benefiting from external demand. Services edged down slightly from 53.0 to 52.9 but remained firmly in growth territory.

NZ ANZ business confidence ticks down, but activity outlook improves

New Zealand’s ANZ Business Confidence edged slightly lower in September, slipping from 49.7 to 49.6. Though, Own Activity Outlook improved to 43.4 from 38.7.

Inflation pressures ticked mildly higher. One-year-ahead inflation expectations rose to 2.71% from 2.63%,. The share of firms expecting to raise prices in the next three months climbed to 46%. Cost expectations also edged up, with 75% of respondents seeing higher input costs.

ANZ noted that the RBNZ is positioned to support growth with a lower Official Cash Rate. While the exact path of policy easing remains uncertain, the bank said the OCR will ultimately reach the level required to ensure the recovery takes hold.

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 199.10; (P) 199.82; (R1) 200.30; More...

Intraday bias in GBP/JPY is back on the downside with break of 198.99. A short term top should be formed at 201.24, on bearish divergence condition in 4H MACD. Deeper fall should be seen to 197.93 support first. Firm break there will argue that whole rise from 184.35 has completed too and target 195.01 support next. For now, risk will stay on the downside as long as 200.49 support holds, in case of recovery.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Fed’s Jefferson sees labor market vulnerable if unsupported

Fed Vice Chair Philip Jefferson said in a speech today while tariffs have added to price pressures, the impact has been "lower than what many forecasters predicted" this spring. Encouragingly, short-term expectations have eased from Q2 highs, while long-term expectations remain anchored. As a result, he expects the disinflation process to "resume after this year" and inflation to eventually return to the Fed’s 2% target "in the coming years".

On the labor side, Jefferson highlighted softening conditions. He warned that the job market could "experience stress” if left unsupported, and said this was a key reason he backed a 25bp rate cut at the last FOMC meeting.

Looking ahead, Jefferson stressed that policy will remain data-dependent, with the Fed monitoring both economic indicators and government policies.

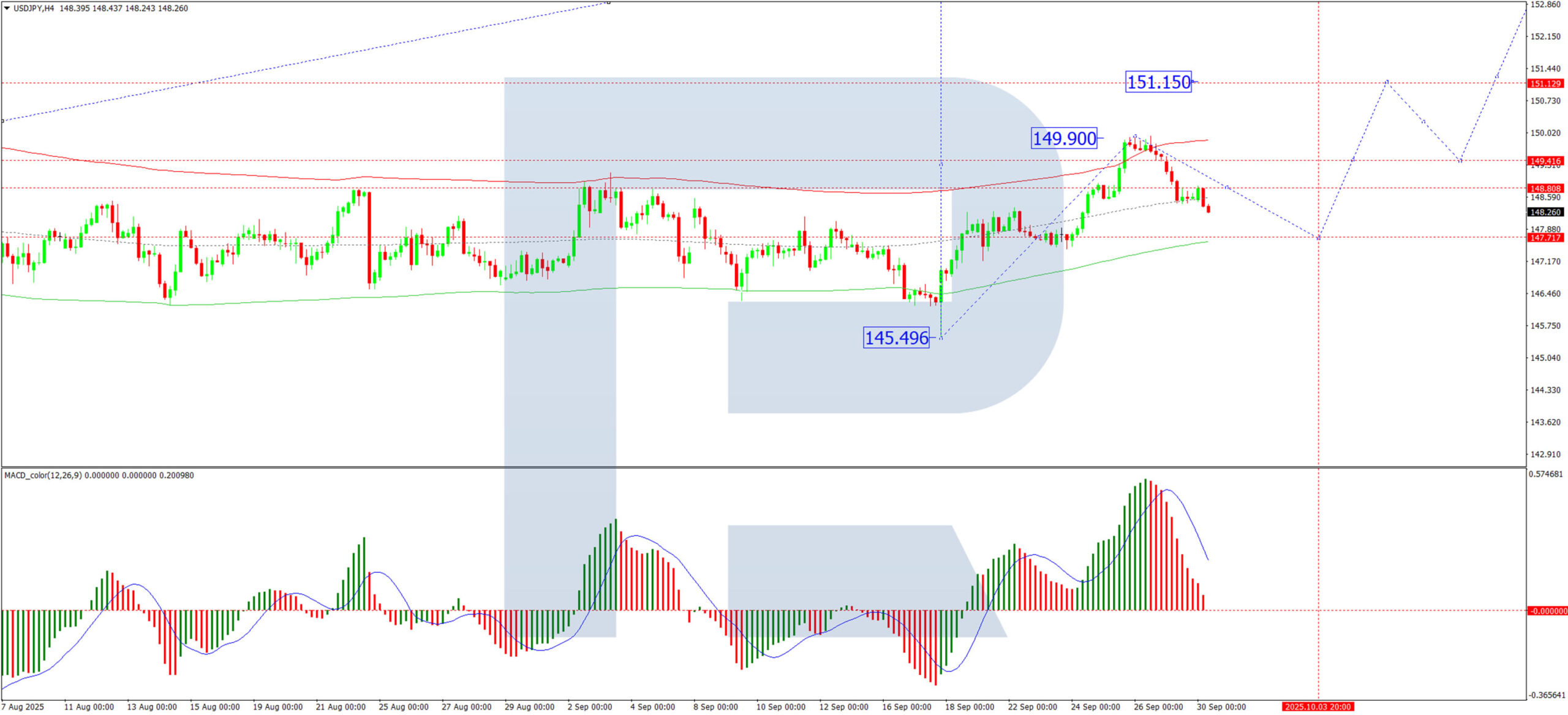

USD/JPY Under Pressure: All Eyes on Bank of Japan Rhetoric

The USD/JPY pair fell to 148.49, marking a third consecutive day of declines as markets digest mixed signals from the Bank of Japan.

The recently published summary of opinions from the September meeting revealed a divided policy committee. Some members advocated for further rate hikes, assuming current growth and inflation forecasts hold. Others, however, argued for maintaining low rates to help cushion the economy from the impact of new US tariffs.

Further highlighting the internal debate, one board member emphasised a wait-and-see approach, stressing the need to monitor global trade policy, the yen's exchange rate, and domestic price and wage dynamics. In contrast, another member noted that with over six months having passed since the last policy shift, it was time to consider another increase.

Weakening Japanese economic data added to the downward pressure. August retail sales fell 1.1%, missing forecasts for 1.0% growth and marking the first decline since February 2022. Industrial production figures also came in worse than expected.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY formed a tight consolidation range around 148.80. Today's downside breakout has extended the correction, with the next target at 147.72. Upon reaching this level, we anticipate a potential new growth wave towards 149.95. This scenario is technically confirmed by the MACD indicator, whose signal line is above zero but pointing firmly downward.

H1 Chart:

The H1 chart shows the pair completed a decline to 148.80 and consolidated around this level. The subsequent downside breakout has confirmed the continuation of the bearish wave structure towards 147.72. The Stochastic oscillator supports this view, with its signal line below 50 and falling sharply towards 20.

Conclusion

USD/JPY remains under pressure amid divergent signals from the BoJ and soft domestic data. While the near-term technical bias is bearish, the current decline is viewed as a correction within a broader uptrend, with the potential for a renewed upward move upon completion of the current wave.

Silver (XAG/USD): Minor Mean Reversion Decline in Progress Below US$47.17

Key takeaways

- Silver’s stellar run: XAG/USD surged 16.1% in September and 27.5% in Q3 2025, marking its strongest quarter since Q3 2020.

- Short-term pullback risk: Price stalled at US$47.17 resistance with bearish RSI divergence, signalling potential mean reversion decline.

- Upside scenario: A breakout above US$47.17 could extend gains toward US$48.14/49.45 in the near term.

Silver (XAG/USD) has delivered a stellar performance, surging 16.1% month-to-date and 27.5% in Q3 as of 30 September 2025, its strongest quarterly gain since Q3 2020.

Over the same period, Silver has outpaced Gold (XAU/USD), which posted comparatively smaller advances of 10.4% month-to-date and 15.5% for the quarter.

Let’s now focus on the short-term trajectory (1 to 3 days), key elements, and key levels to watch on Silver (XAG/USD) from a technical analysis perspective.

Fig. 1: Silver (XAG/USD) minor trend as of 30 Sep 2025 (Source: TradingView)

Fig. 2: Silver (XAG/USD) long-term trend as of 30 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

Potential minor mean reversion decline in progress for Silver (XAG/USD) within its medium-term uptrend phase.

Bearish bias below US$47.17 short-term pivotal resistance for a potential drop towards the intermediate supports at 45.22, 43.75, and 43.10/42.95 (also the 20-day moving average).

Key elements

- The price actions of Silver (XAG/USD) have oscillated within a medium-term ascending channel in place since the 20 August 2025 low and continued to trade above its 20-day and 50-day moving averages (see Fig. 1).

- The recent push-up seen in Silver (XAG/USD) on Monday, 29 September 2025, has stalled at the upper boundary of the medium-term ascending channel at the US$47.17 level, which confluences with a Fibonacci extension (see Fig. 1).

- The hourly RSI momentum indicator of Silver (XAG/USD) has flashed out a bearish divergence condition at its overbought region (above the 70 level) before its exit from it, which increases the odds of a minor mean reversion decline scenario (see Fig. 1).

Alternative trend bias (1 to 3 weeks)

A clearance above the US$47.17 key short-term resistance for Silver (XAG/USD) invalidates the bearish tone for a continuation of the bullish impulsive up move sequence for the next intermediate resistances to come in at 48.14, 48.90 and 49.45.

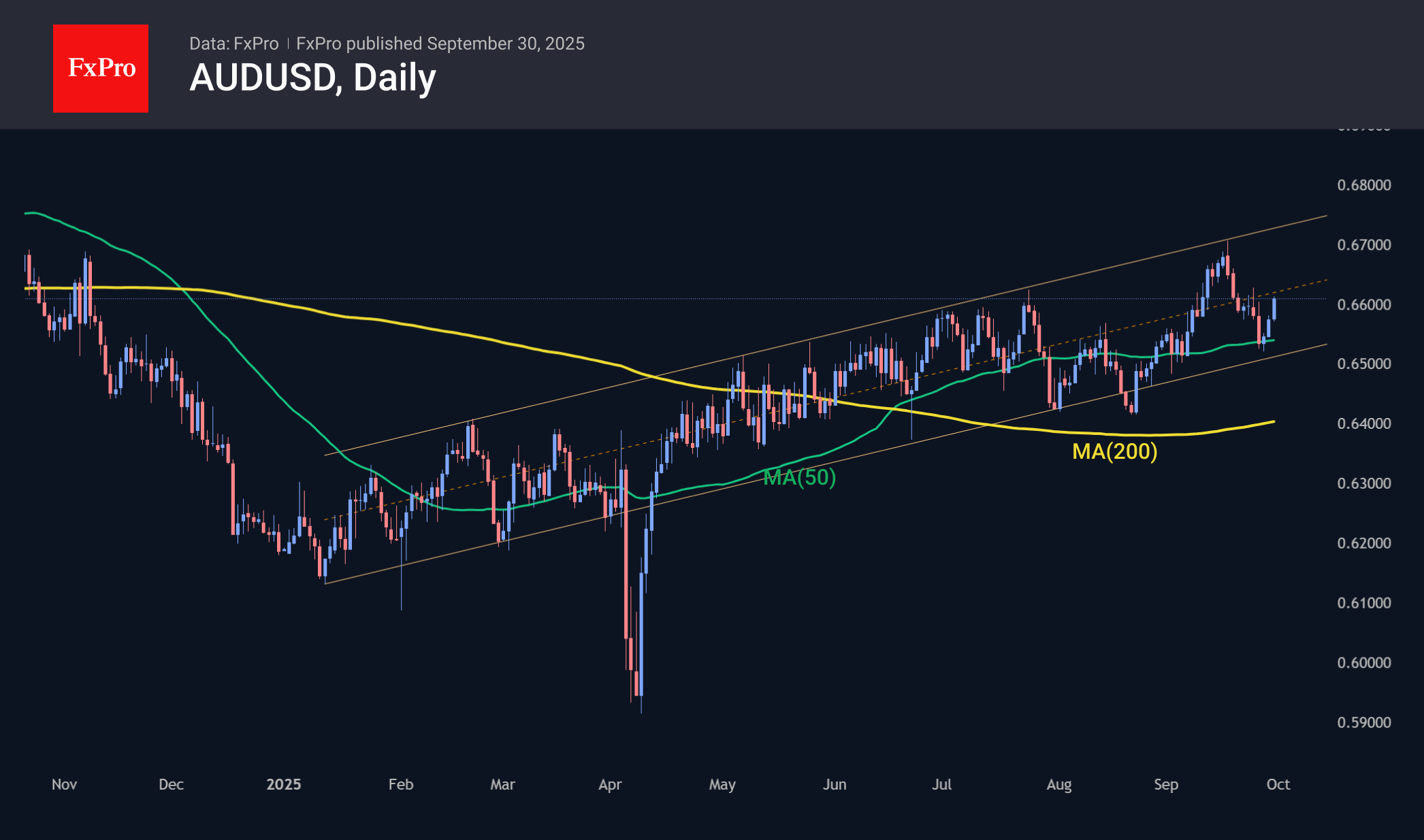

Uncertainty Benefits AUD, While Shutdown Hurts USD

The Australian dollar gained for the third trading session, accelerating its growth to 0.5% on Tuesday after the Reserve Bank of Australia decided to keep its key rate at 3.60%. Analysts widely anticipated the decision, but the official commentary on the decision contained hawkish notes, which played into the hands of the AUD.

The RBA noted that September inflation may be higher than previously expected and pointed to a recovery in economic activity. When the economy does not require emergency support and inflation is likely to pick up, central banks are more inclined to pause and assess the dynamic. In contrast, there are increasing signs in the US that monetary policy needs to be eased.

Taken together, this creates a divergence between Australian and US monetary policy in favour of the Australian dollar.

At the end of last week, AUDUSD found support at the 50-day moving average and reversed to growth at the 200-day average. The pair has been moving upwards within a range since the beginning of the year, from which it only fell during the shock of ‘America’s Liberation Day’ in early April.

The Aussie touched the upper limit of this channel on 17 September, briefly exceeding 0.6700, but the looming US government shutdown halted the strengthening of the USD on the Fed’s cautious comments. This exceptionally short-term and speculative story (a compromise was always found sooner or later) nevertheless undermines long-term confidence in the dollar, preventing it from reversing the downward trend that began at the start of the year.