Sample Category Title

Markets Remain Relatively Unnerved Around the Looming Shutdown

Markets

A White House meeting between US President Trump and congressional leaders from both political sides to avoid a government shutdown ended without a deal yesterday. Vice-president Vance believes that we’re effectively headed into a shutdown, obviously blaming it on Democrats. They rejected a short-term funding resolution which would have provided funding through November 21st and buy time for negotiations and crafting full-year spending bills. Democrats demand healthcare provisions before engaging their support. The funding bill for the new fiscal year will today again be presented in US Senate, where Republicans’ majority (53-47) is too small to get the notion through without Democratic support (60 votes required). In case of a shutdown, non-essential services will be suspended including the Bureau of Labour Statistics. That means we won’t get weekly jobless claims and especially the payrolls report later this week. If a shutdown runs until mid-October, publications of trade data, retail sales, consumer prices and producer prices are at risk as well. Federal workers will be furloughed with the White House last week suggesting to use the occasion to lay them off rather than allow them to return to work when funding is restored. Markets remain relatively unnerved around the looming shutdown. US Treasuries won ground yesterday, but in a global bull steepening move. We have the impression that end-of-quarter extension buying and lower oil prices (Brent $67.5/b from $69.5/b) related to rumours on another OPEC+ output rate hike next month carried at least as much weight. Daily changes on the US yield curve varied between -2.2 bps (2-yr) and -4.5 bps (30-yr) with German yields closing 0.7 bps (2-yr) to 5.6 bps (30-yr) lower. From a technical point of view, the US 10-yr yield last week bumped into technical resistance at 4.2% (previous support; neck line of triple top formation). Risk sentiment was mildly constructive with main European and US indices closing up to 0.25% higher with the Nasdaq outperforming (+0.5%). EUR/USD is still going nowhere, changing currently hands around 1.1735.

Minutes of the September BoJ meeting this morning showed a broadening view that another rate hike is needed at some stage. Dovish BoJ board member Noguchi yesterday also gave the nod towards an October rate hike, if data permit. The market implied probability of such action increased further to nearly 70% and contributed to today’s weak 2-yr JGB auction. JPY gets some more breathing room away from support levels at USD/JPY 150 and EUR/JPY 175. Apart from above-mentioned themes, today’s eco calendar contains more national EMU inflation numbers, the US JOLTS report and US consumer confidence. We don’t expect them to alter thinking on near term ECB (stable) and Fed (October rate cut) policy. Trump’s peace plan for Gaza gets a lot of media coverage, but doesn’t impact overall trading/risk sentiment so far.

News & Views

Switzerland and the US Treasury yesterday released a joint declaration in which they aligned views on foreign exchange matters. In the rare statement, both promised not to “target exchange rates for competitive purposes” but also recognized that such market interventions are a valid tool for addressing currency volatility or “disorderly” moves. The latter addition is seen as a nod from the US to the Swiss National Bank to act if it deems necessary. That could be the case if inflation threatens to settle below the 0-2% target due to CHF strength and at a time when the policy rate is already 0%. As such, it lowers the risk of the SNB needing to go back into negative rate territory. The Swiss franc yesterday fell, particularly against the euro. EUR/CHF closed around 0.935. In separate news, Switzerland has offered the US to invest in its gold-refining industry as a sweetener in the trade talks aimed at lowering the current 39% import levy. Gold trade with the US, while typically balanced, blew up into a massive surplus in the first quarter of this year amid fears the US administration would levy tariffs on the bullion.

The Reserve Bank of Australia kept the policy rate stead y at 3.6% this morning. The unanimous decision was based on signs that private demand is recovering a little more rapidly than anticipated amid rising real incomes, indications that inflation - while currently within the 2-3% range - may be persistent in some areas and higher than expected in the September quarter and labour market conditions overall remaining stable. The RBA advocates a cautious stance and notes that it is well placed to respond decisively to international developments. It refrained from giving clear hints for the future, saying only that “The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions.” Australian swap rates rose, pulled higher by the front end (up to +6.2 bps). AUD/USD appreciates to above 0.66, keeping the upward sloping trendline intact.

Wait and See

The week started with minor gains in US and European equities, despite fresh tariff threats from Donald Trump and no material progress on talks to avoid a US government shutdown. The S&P 500 and Nasdaq traded flat, just a touch below their all-time highs, while the US 10-year yield fell on safe-haven inflows. A shutdown by tomorrow is a real possibility, though it wouldn’t be the first nor the last time the US government closes on funding issues. A short shutdown wouldn’t have a major impact on US growth expectations or risk appetite.

What’s more worrying for investors is the risk of US data not being released – or being delayed – as government agencies would be mostly closed in case of a shutdown. The lack of data would muddy the Federal Reserve (Fed) outlook. And because the softening Fed outlook and rising rate cut expectations have been a major support to the latest US stock rally, the absence of data could encourage some investors to take profit and move sideways.

If the shutdown lasts a few weeks – which is possible – then growth expectations would start to deteriorate. But that deterioration would boost Fed cut bets. And that “magic mechanism” of dovish Fed expectations would likely put a floor under any potential market sell-off. From a medium-term perspective, I wouldn’t be too worried about a shutdown. Any price pullbacks could be seen as an opportunity to buy the dip.

Now, speaking of data – because today could be the last day of releases before a shutdown, the job openings report (JOLTS) could attract more attention than usual. Job openings are expected to have declined further. A softer-than-expected JOLTS figure today could bolster the Fed doves and weigh further on US yields and the dollar, though it might not boost appetite for equities.

In Asia, appetite for Chinese stocks remains intact after the latest PMI data showed manufacturing activity at its strongest in six months. Export orders rose for the first time in six months, new business expanded at the fastest pace since February, supply conditions improved and input cost inflation accelerated to a 10-month high, driven by higher metal prices. On top, the Chinese government said it will deploy 500bn yuan – the equivalent of about $70bn – to further back investment and boost growth. Appetite is improving as momentum picks up.

Foreign holdings of Chinese assets are expanding for the first time in four years, mostly led by the Chinese technology giants and the AI rally. Alibaba has gained around 130% since the beginning of the year, while the Hang Seng index has rebounded by as much as 43% since January to levels last seen in 2021. But despite these inflows, global investors remain relatively under-exposed to Chinese stocks, leaving further room for the rally to develop. Chinese tech stocks, despite a strong rally this year, still trade at cheaper valuations than their US peers, where stretched multiples are becoming a concern.

High valuations in US Nig Tech haven’t necessarily been a barrier to further gains, but flows suggest that speculative longs may be retreating. Leveraged ETFs – those that double or triple the daily moves in indices or single stocks – saw about $7bn in outflows in September, a warning that hot money could be paring back after the recent push higher.

In Australia, the Reserve Bank of Australia (RBA) kept its policy rate unchanged today, as widely expected. The AUDUSD pushed above 0.66, while the ASX remained under pressure near its 200-day moving average, weighed down by energy stocks. In Japan, the Nikkei was flat, caught between limited risk appetite due to US shutdown uncertainty and support from a softer yen.

In FX, the US dollar is better bid in Asia this morning but remains capped by its 50-day moving average. The EURUSD is consolidating gains above its own 50-DMA, while the USDJPY benefits from a softer US dollar and some safe-haven flows into the yen. The pair is preparing to test its 200-DMA to the downside and could break lower in the event of a US shutdown.

But the real “safe-haven” action is in precious metals. Gold rallied to a fresh record this morning, now trading near $3’864 per ounce, well into overbought territory – though that hasn’t deterred those chasing gold’s ultimate safe-haven status combined with strong momentum. The same is true for silver, which is approaching the $50 per ounce level. That milestone wasn’t reached back in 2011 but could be challenged this time as appetite for precious metals is supported by reduced demand for the US dollar and US Treasuries, waning trust in traditional currencies and stronger demand for hard assets as global inflation expectations rise due to trade frictions.

Elsewhere in metals, copper futures have been trending higher on a mix of supply shock and speculative pressure. A serious accident at Freeport’s Grasberg mine in Indonesia – one of the world’s largest copper mines – forced the company into force majeure, spooking markets over tighter output ahead. Meanwhile, demand expectations remain intact, especially from China, and traders are positioning for a potentially undersupplied copper market. That, combined with a softer dollar and lingering tariff anxieties, keeps the outlook positive.

In energy, crude oil failed to benefit from the softer US dollar or heightened geopolitical tensions in Ukraine. Reports yesterday that OPEC could announce another supply increase in November weighed on sentiment and sent US crude back below $65 per barrel. Consequently, the latest bullish attempt has fizzled, leaving WTI stuck in the $82–85 range and awaiting a meaningful breakout.

US Job Openings and Last-Minute US Shutdown Talks on the Agenda

In focus today

Focus shifts to flash September inflation data from France, Germany and Italy. The core inflation measure will be key, particularly after Spain's data yesterday showed weaker-than-expected core inflation despite a rise in headline inflation. Large base effects from energy prices and travel-related services are likely to drive yearly inflation growth, making monthly price changes the critical metric to watch.

In Sweden, August retail sales will be released at 08:00 CET. While May's data was exceptionally weak, recent months have shown gradual improvement. That said, level-wise July was still below April and the weak overall performance among households over the last few years is the main reason why the Swedish economic recovery has failed to materialize. While the Riksbank moderated its GDP profile, the 2025 estimate at 0.9% y/y rests on the assumption that household consumption picks up sharply in the fourth quarter.

In the US, the August JOLTs labour turnover report is due in the afternoon. The number of job openings is a key measure of labour demand for the Fed, and we will also closely follow the number of involuntary layoffs for potential signs of more acute labour market weakening.

Today is the last opportunity for negotiations to finalise a funding bill before the US government shutdown begins on Wednesday. Limited progress over the weekend and in yesterday's discussions has kept the likelihood of a shutdown high.

Overnight, the Bank of Japan's quarterly business Tankan survey is released. This is a huge survey holding extensive information about the economy and key input ahead of the 30 October BoJ policy meeting. While PMIs suggest the economy gained momentum in Q3 after a strong H1 with GDP growth above 1.5%, the weaker September PMI signals some loss of steam.

Economic and market news

What happened overnight

In China, PMIs came out better than expected. Both the official and private versions were released and beat expectations with a rise in the official NBS PMI manufacturing from 49.4 to 49.8 (cons: 49.6) and a lift in the RatingDog PMI manufacturing seeing from 50.5 to 51.2 (cons: 50.2). The RatingDog index was the highest since February and the increase was driven by a turn higher in export orders rising from 49.4 to 51.0. Service PMI from RatingDog fell slightly from 53.0 to 52.9. It is still a decent level, though. The numbers suggest that the weakness in PMI over the summer was partly affected by extreme weather. It also confirms that Chinese exports are still coping well despite the higher tariffs from the US. China still suffers from weak domestic demand, though, centred in consumption and construction and there is a need to provide more stimulus to put this part of the economy on a stronger footing if China wants to meet its' goal of stabilising housing and making consumption a stronger growth pillar. The data may lower the sense of urgency, though, for Chinese leaders. Chinese stocks moved higher initially but has come down again to be broadly flat.

In Australia, the RBA maintained rates unchanged, as widely expected. RBA's forward guidance was to the hawkish side, as it did not signal plans for imminent cuts over the coming meetings either. Recovering private demand, still tight labour markets, easing financial conditions and lower trade uncertainty favoured keeping rates at the current level. Markets are now pricing in less than a 40% chance of a rate cut in November, down from around 55% before the meeting. AUD/USD also shifted higher to around 0.66 after the decision, we maintain our 12M forecast at 0.69.

Israel-Palestine conflict, Trump hosted Israeli Prime Minister Netanyahu at the White House to back a US-sponsored 20-point peace plan for ending the Gaza war. Netanyahu endorsed the proposal, citing alignment with Israel's objectives, including staged withdrawal, hostage exchange, and Hamas disarmament. However, with Hamas excluded from the agreement and significant political hurdles remaining, its success is uncertain.

What happened yesterday

In the euro area, Spanish inflation data for September came in below expectations. While headline HICP inflation rose as anticipated to 3.0% y/y (from 2.7% in August), core CPI inflation declined to 2.3% y/y (from 2.4% y/y), contrary to an expected rise to 2.5% y/y. The weaker core inflation print is particularly notable, signalling a dovish outlook for upcoming inflation data from other countries. In contrast, Belgian core inflation rose to 2.6% y/y, highlighting a divergence from Spain's weaker performance. Given the similar historical correlations of euro area inflation with Spain and Belgium, the focus now shifts to French and German data due tomorrow.

In Sweden, the Riksbank minutes showed that the Board remains aligned on the recent rate cut, viewing inflation as likely to abate soon while acknowledging the weak domestic economy. There is little concern about upside inflation risks from the government's budget, and no further rate cuts were discussed, indicating a higher threshold for additional easing. Anna Breman's upcoming departure is expected to shift the board slightly towards a more hawkish stance.

In Norway, retail sales rose by 0.2% m/m in August, following a 0.6 % jump in July, bringing the 3M/3M growth rate down to 0.8%. Supported by higher real wage growth and lower mortgage rates, retail sales appear to remain on an upward trajectory, albeit at a slower pace. These figures do not point to any immediate need for a rate cut but are also not strong enough to challenge expectations of further cuts in 2026.

Equities: Equities extended gains yesterday, in a session dominated by wait-and-see sentiment as we approach 1 October and the US government shutdown deadline. Notably, banks underperformed, while the long end of the curve rallied in both the US and Europe, helped in part by a softer-than-expected Spanish inflation print. Energy was the clear laggard, down sharply as oil sold off 3.5% on renewed expectations that OPEC+ will ramp up production from November. In the US yesterday, Dow +0.2%, S&P 500 +0.3%, Nasdaq +0.5%, Russell 2000 +0.04%. Asian trading this morning shows a mixed picture, with Taiwan and New Zealand in leading advances. US and European equity futures are broadly flat.

FI and FX: EUR/USD starts the week drifting above 1.17 as the USD broadly softens with USD/JPY dropping close to a full figure during yesterday's session to around 148.50. This week, the focus is firmly on US labour market data. With Powell recently stressing that as little as +0-50k job growth may be enough to keep unemployment steady, markets will scrutinise today's JOLTS, the ADP report, weekly claims, and especially Friday's payrolls report for signals on the Fed's next move. US yields started the week on a subdued note, with attention firmly on labour market data and the risk of a US government shutdown. The curve bull flattened as the long end outperformed: the 2Y Treasury yield slipped 1bp, while the 10Y and 30Y yields declined 3bp and 4bp, respectively. In Europe, Bunds mirrored the US dynamic, also undergoing a bull flattening move. The rebound in oil prices last week proved temporary. The price on Brent crude plunged back down below USD68/bbl yesterday. The move looks to have followed indications that OPEC+ this week could agree on further output hikes.

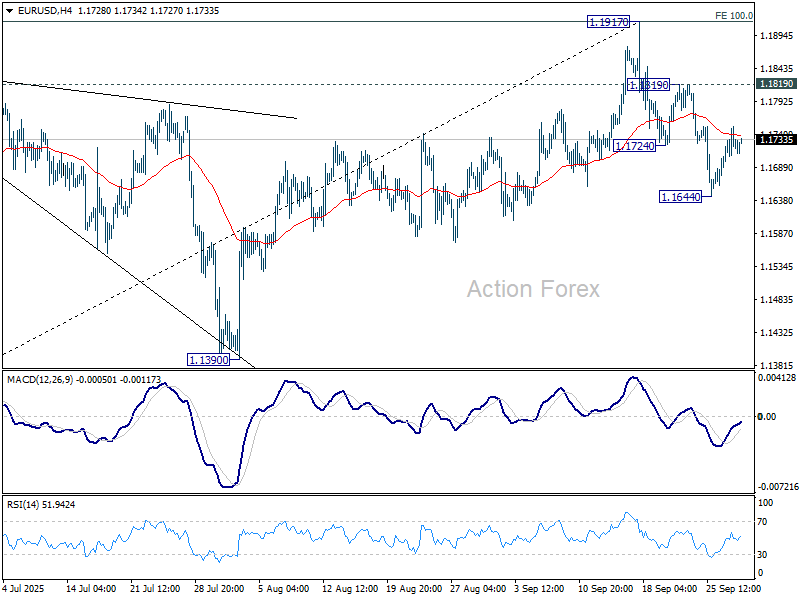

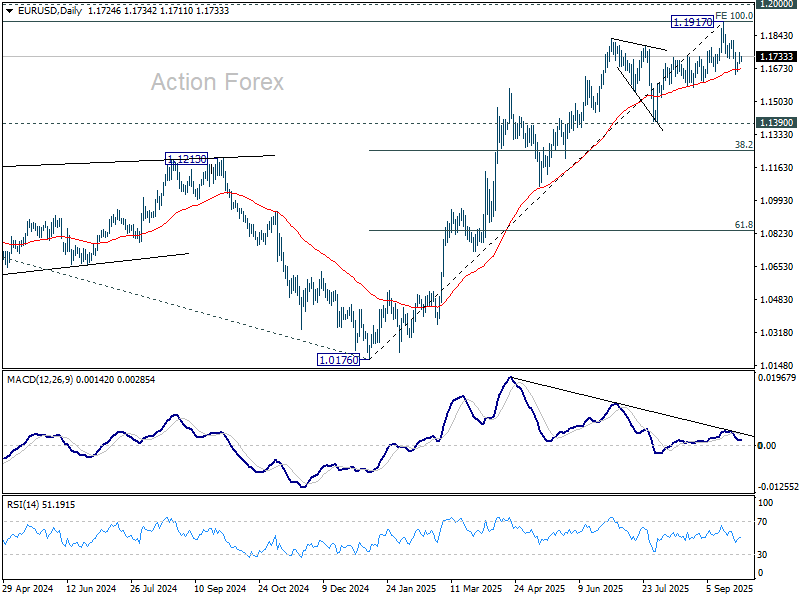

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1700; (P) 1.1728; (R1) 1.1754; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen above 1.1644. Further fall is expected as long as 1.1819 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1670) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

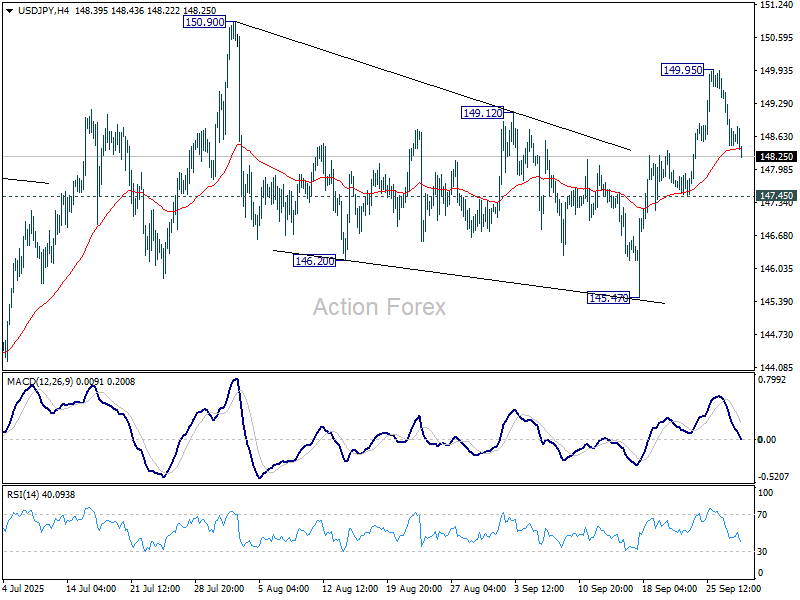

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.15; (P) 148.92; (R1) 149.37; More...

Intraday bias in USD/JPY remains neutral at this point. Further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall back to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

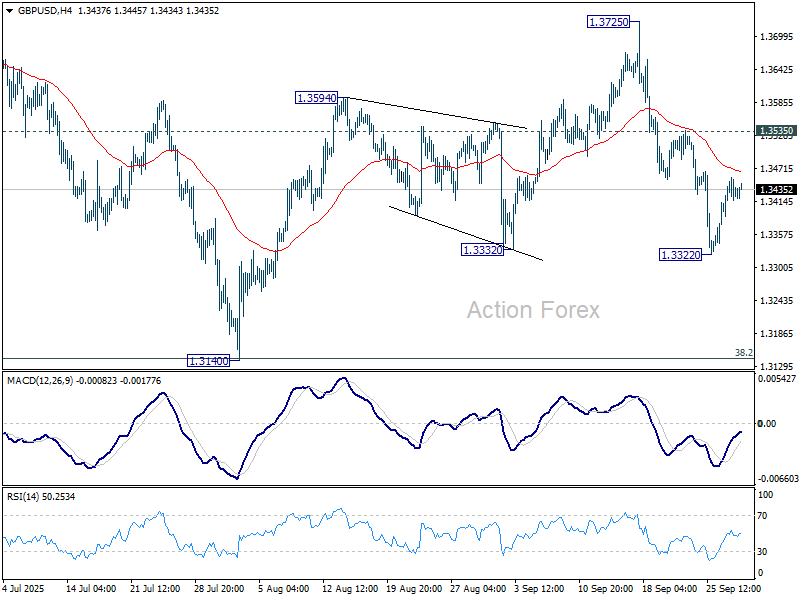

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3394; (P) 1.3426; (R1) 1.3458; More...

Intraday bias in GBP/USD stays neutral and more consolidations could be seen above 1.3322. But further decline is expected as long as 1.3535 resistance holds. Break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

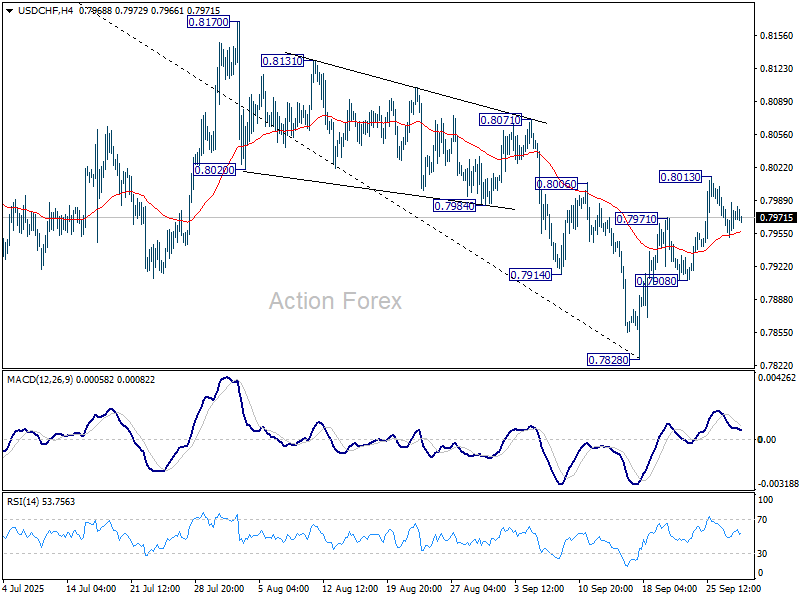

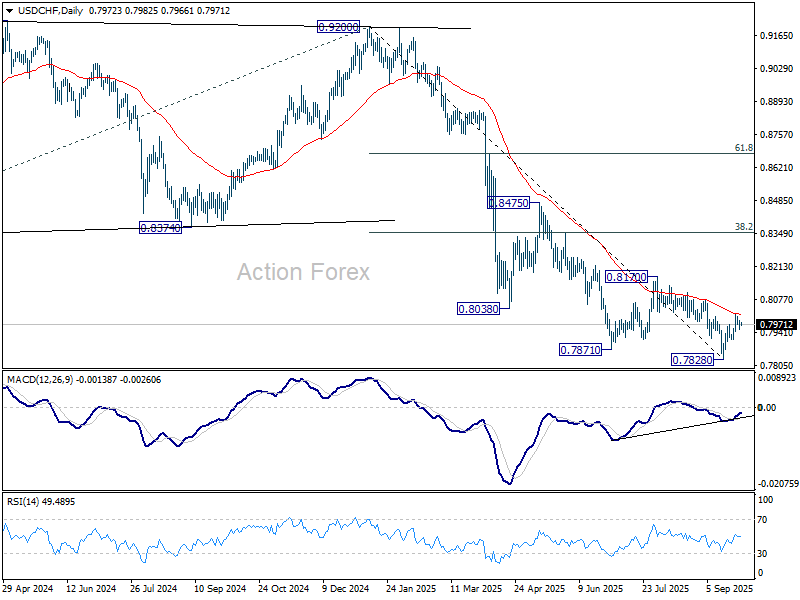

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7957; (P) 0.7972; (R1) 0.7993; More…

USD/CHF is staying in consolidations below 0.8013 and intraday bias remains neutral. On the upside, sustained trading above 55 D EMA (now at 0.8014) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

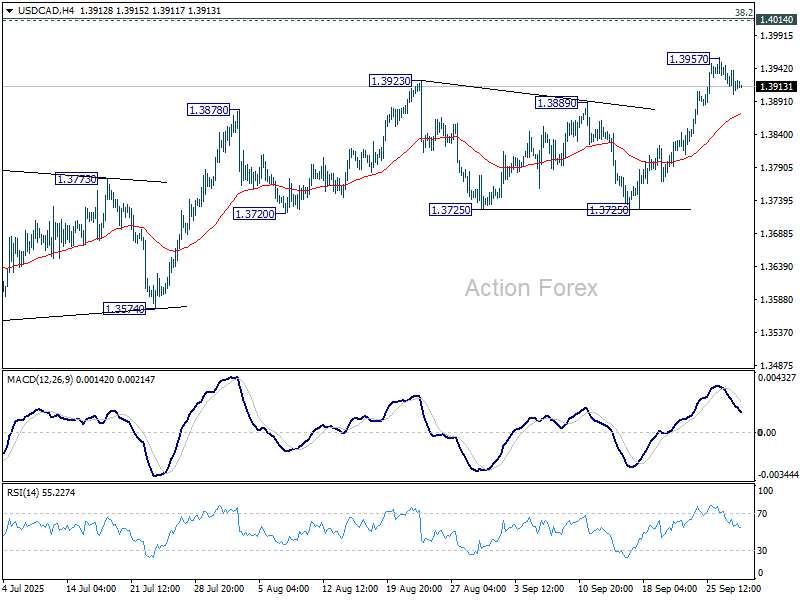

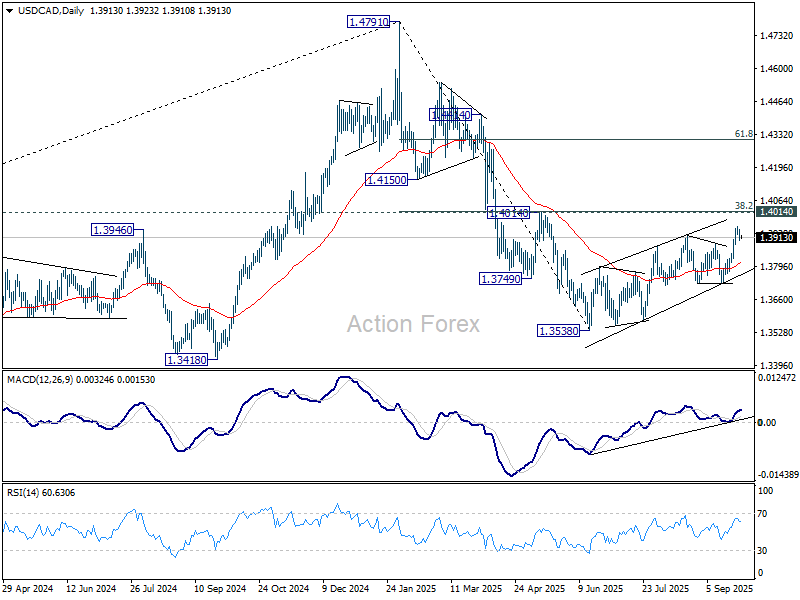

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3896; (P) 1.3922; (R1) 1.3940; More...

Intraday bias in USD/CAD remains neutral and more consolidations could be seen below 1.3957. On the upside, break of 1.3.957 will resume the corrective rebound from 1.3538. But upside should be limited by 1.4014 cluster resistance to bring reversal. Meanwhile, sustained trading below 55 4H EMA (now at 1.3870) will bring deeper fall back to 1.3725 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

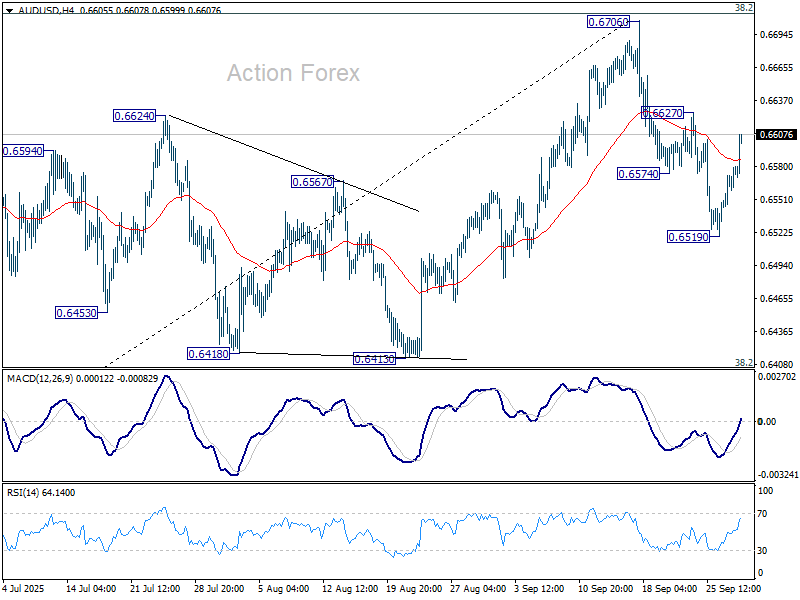

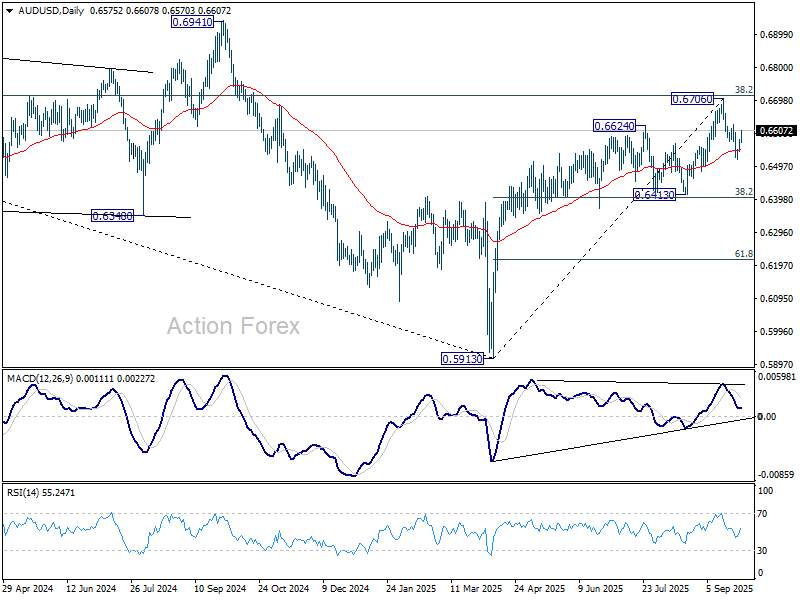

AUD/USD Daily Report

Daily Pivots: (S1) 0.6555; (P) 0.6568; (R1) 0.6589; More...

Focus is back on 0.6627 resistance in AUD/USD with current extended rebound. Break there will suggest that pullback from 0.6706 has completed as correction, after drawing support from 55 D EMA (now at 0.6546). That will keep the larger rally from 0.5913 alive and bring retest of 0.6706 high. However, on the downside, sustained trading below 55 D EMA will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

Aussie Surges on RBA Hawkish Tilt, Yen Supported Despite Data Weakness

Aussie rallied broadly after the RBA left policy unchanged at 3.60% but issued a statement that leaned hawkish. Traders were quick to note the Bank’s warning that Q3 inflation may come in stronger than projected in August, a reminder that the disinflation path remains far from assured.

The RBA’s tone suggested that the widely expected November cut is far from a done deal. Policymakers appear keen to leave flexibility in case inflation surprises higher, especially if robust consumption and firm labour markets give businesses scope to pass on costs. More importantly, scope for a deeper easing cycle is now more limited than markets had assumed. Even if the RBA delivers one cut in November, follow-up moves may prove difficult.

Meanwhile, Yen also stayed firm, supported by the BoJ’s Summary of Opinions, which revealed growing calls for rate hikes within the board. A number of board members argued that the time for action may be near, adding momentum to expectations of policy normalization.

Yet Japanese data continue to cast doubt on how soon that shift can occur. Industrial production contracted more than expected in August, and retail sales posted their first drop in 42 months. For now, the majority of the Board remains cautious, waiting for more evidence before endorsing a move.

Doves remain in the majority in the BoJ for now, and there is little hard evidence yet to tip the balance decisively toward an imminent hike. The next test will be the quarterly Tankan survey due tomorrow, which will provide a clearer read on business sentiment and capital expenditure plans.

In terms of weekly performance, Aussie is leading the pack for now, followed by Yen and Kiwi. Dollar sits at the bottom, trailed by Swiss Franc and Euro, while Sterling and the Loonie are holding in the middle of the field.

Elsewhere, Asian equities traded mixed after Wall Street’s modestly higher close overnight. Quarter-end lull and caution ahead of key US data — notably ISM Manufacturing tomorrow and non-farm payrolls on Friday — are keeping traders restrained, ensuring a steady but cautious tone across markets.

In Asia, at the time of writing, Nikkei is up 0.01%. Hong Kong HSI is down -0.13%. China Shanghai SSE is up 0.40%. Singapore Strait Times is up 0.40%. Japan 10-year JGB yield is down -0.013 at 1.634. Overnight, DOW rose 0.15%. S&P 500 rose 0.26%. NASDAQ rose 0.48%. 10-year yield fell -0.046 to 4.140.

RBA holds steady at 3.60%, warns Q3 inflation may surprise on upside

The RBA left its cash rate unchanged at 3.60% in a unanimous decision, in line with expectations. The move reflects the Board’s preference to pause while monitoring whether recent economic surprises point to a more persistent inflation challenge.

According to the RBA, recent partial data suggest that September-quarter inflation may come in above projections made in August. At the same time, labor market indicators show conditions have been steady and remain "a little tight", reinforcing the risk that price pressures may not ease as quickly as anticipated.

The Bank outlined two contrasting scenarios for household demand. Stronger consumption may reflect rising real incomes and wealth, potentially allowing firms to raise prices more easily and encouraging further hiring. Alternatively, this consumption rebound may not last if households turn more cautious amid uncertainty around overseas developments.

BoJ summary reveals rising hawkish pressure, but board still divided

The BoJ’s September Summary of Opinions revealed that members debated the feasibility of raising interest rates in the near term, with some arguing that conditions were aligning for another move. The release underscores a growing hawkish tilt inside the Board, even as the majority voted to hold steady at 0.50%.

One member argued that “judging solely from the perspective of Japan’s economic conditions, it may be time to consider raising the policy interest rate again,” noting that more than six months have passed since the last hike. Another highlighted easing concerns from U.S. tariffs, suggesting external impact on inflation had "abated" and that the BoJ could “return to its stance to raise the policy interest rate.”

At the same time, caution was evident. Some warned against surprising markets with a hike, stressing that Japan’s domestic demand remains vulnerable to external shocks. The view was that it would be better to wait for more hard data before making another adjustment.

At the September 18–19 meeting, the BoJ left rates at 0.50%, though two members dissented in favor of a hike to 0.75%.

Japan's industrial output falls -1.2% mom in August, retail sales contracts

Japan’s latest data painted a downbeat picture of economic momentum in August. Industrial production slipped -1.2% mom, falling short of the expected -0.8%. Of the 15 industrial sectors, 12 including metal products, and inorganic and organic chemicals, saw output decreases.

METI maintained its description of output as "fluctuates indecisively". Officials stressed that firms remain highly cautious in their production planning. Still, manufacturers surveyed see output rising 4.1% in September and another 1.2% in October.

Household demand faltered at the same time, with retail sales tumbling -1.1% yoy, marking the first decline in 42 months.

China's NBS PMI points to easing manufacturing weakness, services soft patch

China’s official PMI data for September signaled tentative improvement in industry but lingering softness in services. The NBS Manufacturing PMI rose to 49.8 from 49.4, its highest since March, though it still pointed to contraction. The gauge has been under 50 since April, reflecting headwinds for large and state-linked producers.

The NBS Non-Manufacturing PMI slipped from 50.3 to 50.0, effectively flatlining and pointing to a loss of momentum in construction and services. That stagnation raises questions about the strength of domestic demand, even as authorities step up stimulus efforts.

In contrast, the RatingDog (S&P Global) surveys offered a more optimistic take. Manufacturing improved to 51.2 from 50.5, the strongest since May, suggesting that private and export-focused companies are benefiting from external demand. Services edged down slightly from 53.0 to 52.9 but remained firmly in growth territory.

NZ ANZ business confidence ticks down, but activity outlook improves

New Zealand’s ANZ Business Confidence edged slightly lower in September, slipping from 49.7 to 49.6. Though, Own Activity Outlook improved to 43.4 from 38.7.

Inflation pressures ticked mildly higher. One-year-ahead inflation expectations rose to 2.71% from 2.63%,. The share of firms expecting to raise prices in the next three months climbed to 46%. Cost expectations also edged up, with 75% of respondents seeing higher input costs.

ANZ noted that the RBNZ is positioned to support growth with a lower Official Cash Rate. While the exact path of policy easing remains uncertain, the bank said the OCR will ultimately reach the level required to ensure the recovery takes hold.

Fed’s Williams: Makes sense to ease policy a little bit to support jobs

New York Fed President John Williams said overnight that it made sense for the central bank to ease policy “a little bit” to reduce restrictiveness to support the labor market while maintaining downward pressure on inflation.

Williams acknowledged progress toward the 2% inflation target but cautioned that more work remains. He underscored the Fed’s dual mandate, stressing the need to avoid “undue harm” to employment at a time when job creation has been gradually weakening. “I don’t want to see that go too far,” he said.

Encouragingly, Williams noted that some inflation worries have eased ""The tariff effects have been smaller than most people thought, and there doesn't seem to be any signs of inflationary pressures building," he noted.

Fed’s Musalem open to cuts but urges cautions

St. Louis Fed President Alberto Musalem said monetary policy is now “somewhere between modestly restrictive and neutral.”

Musalem, who votes on policy this year, said he is “open minded” to further rate cuts but stressed that caution is needed. With limited room before policy turns "overly accommodative", he signaled the Fed should proceed carefully.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6555; (P) 0.6568; (R1) 0.6589; More...

Focus is back on 0.6627 resistance in AUD/USD with current extended rebound. Break there will suggest that pullback from 0.6706 has completed as correction, after drawing support from 55 D EMA (now at 0.6546). That will keep the larger rally from 0.5913 alive and bring retest of 0.6706 high. However, on the downside, sustained trading below 55 D EMA will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.