Sample Category Title

China Exports Surge 19.4% as US Trade Truce and Tech Demand Fuel Growth

China's trade sector delivered strong performance in May, with exports rising from 14.1% to 19.4% yoy in US dollar terms, beating expectations of 15%. Imports also accelerated from 25.3% to 27.4%, exceeding forecasts and pointing to continued strength in both external and domestic demand. As a result, China's trade surplus widened sharply from USD 84.8B to USD 105.43B, well above the expected USD 88.7B.

A key driver was the continued recovery in trade with the United States following the tariff truce reached last October. Exports to the US surged 35.4% from a year earlier, marking the strongest growth since March 2021, while imports from the US rose 20%. The rebound suggests trade flows have normalized significantly compared with last year's tariff-war disruptions, providing an important boost to China's manufacturing sector.

Technology exports were a standout performer. Shipments of automated data processing equipment surged 66.1% year-on-year, while exports of high-tech products rose 50.9%. Automobile exports also maintained strong momentum, increasing 39%. These figures highlight China's growing competitiveness in higher-value manufacturing sectors and suggest global demand for technology-related products remains resilient despite concerns over slowing economic growth in major markets.

Regional trade data also pointed to strengthening supply-chain activity across Asia. Exports to Southeast Asia rose 24.3%, while imports from the region climbed 28.2%. Imports from South Korea jumped 84% to a record USD 26.7B, making it China's largest import source among major trading partners. The strong rise in intermediate-goods imports suggests Chinese manufacturers are ramping up production to meet both domestic and overseas demand.

| Indicator | April | May | Forecast |

|---|---|---|---|

| Exports Y/Y | 14.1% | 19.4% | 15.0% |

| Imports Y/Y | 25.3% | 27.4% | 25.0% |

| Trade Surplus USD | 84.8B | 105.43B | 88.7B |

| Trade Flow | May Growth Y/Y |

|---|---|

| Exports to US | 35.4% |

| Imports from US | 20.0% |

| Exports to Southeast Asia | 24.3% |

| Imports from Southeast Asia | 28.2% |

| Exports to EU (May) | 7.6% |

| Imports from EU (May) | -1.3% |

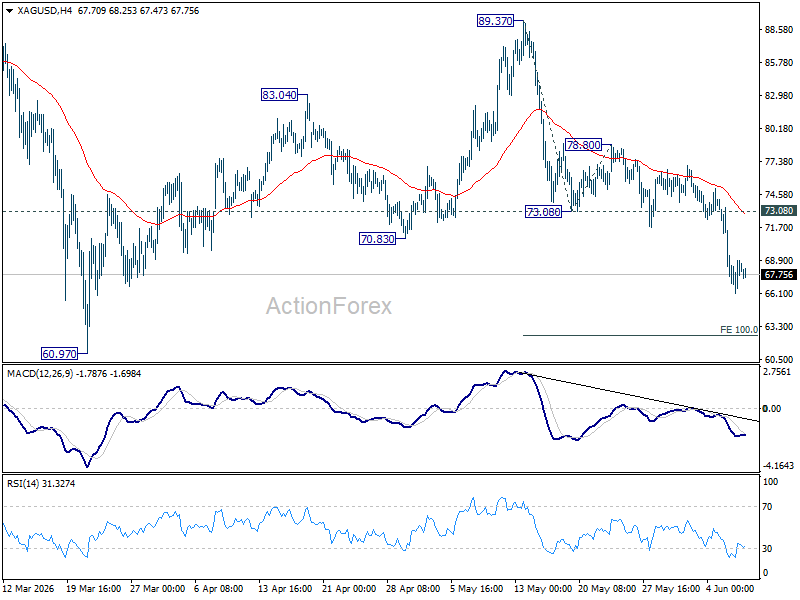

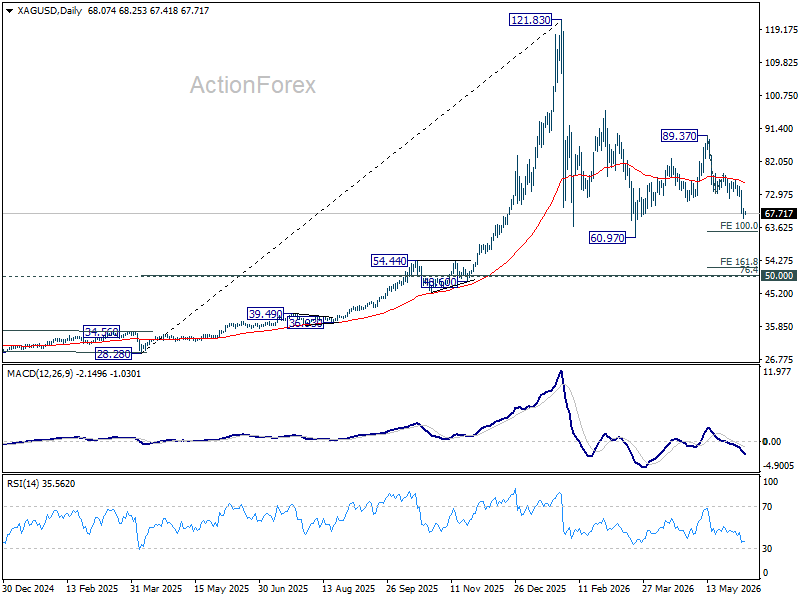

Silver’s $70 Breakdown May Have Changed Everything

Silver's sharp decline this week is about more than rising Fed hike expectations. By breaking decisively below the key $70 level, the metal may have altered one of the market's most widely accepted assumptions. What was previously viewed as a structural floor supported by supply deficits and industrial demand is now at risk of becoming a ceiling.

Like Gold, Silver has come under pressure as investors aggressively reprice the US interest-rate outlook following last week's stronger-than-expected nonfarm payrolls report. A stronger Dollar and growing expectations that Fed may need to tighten policy further have reduced the appeal of precious metals. However, Silver's decline carries broader implications because it occupies a unique position as both a monetary and industrial metal.

The bullish case for Silver rested on two pillars. First, persistent supply deficits were expected to keep physical markets tight. Second, robust industrial demand from sectors such as solar energy and AI-related technologies was seen as providing a durable foundation for prices. Together, these factors fostered a belief that Silver would find strong support around the $70 area even during periods of macroeconomic weakness.

The decisive break below that level now challenges that narrative. Markets can tolerate corrections. What changes sentiment is when a level widely viewed as structural support stops functioning as support. As a result, attention is shifting away from whether Silver can bounce and toward whether it can reclaim the lost ground.

The next phase may prove particularly important from an institutional perspective. In technical analysis, major support levels often undergo a polarity flip after breaking, transforming from floors into ceilings. That process becomes especially significant when large investors use relief rallies back toward the former support area as opportunities to reduce exposure.

In Silver's case, the key level to monitor is now $70 itself. If prices attempt to recover and repeatedly encounter heavy selling around that area, it would suggest institutional distribution rather than accumulation. Such behavior would indicate that the market's long-standing structure is deteriorating and that investors are using strength to exit positions rather than build new ones.

Technically, the near-term outlook remains bearish while 73.08 support-turned-resistance caps any recovery. The next downside target stands at 61.79, representing the 100% projection of 89.37 to 73.08 from 78.80 at 61.79. Strong support is expected between 61.79 and the prior low at 60.97.

That support zone could still trigger a meaningful rebound. However, decisive break below 60.97/61.79 would signal a further acceleration in downside momentum. In that scenario, Silver could extend toward the 161.8% projection at 51.72 and potentially challenge the major psychological level at 50.

For now, the most important question is not how far Silver has already fallen. It is whether the market can reclaim $70 swiftly. If that level has indeed shifted from floor to ceiling, the implications for Silver's medium-term outlook could be far more significant than the current selloff alone suggests.

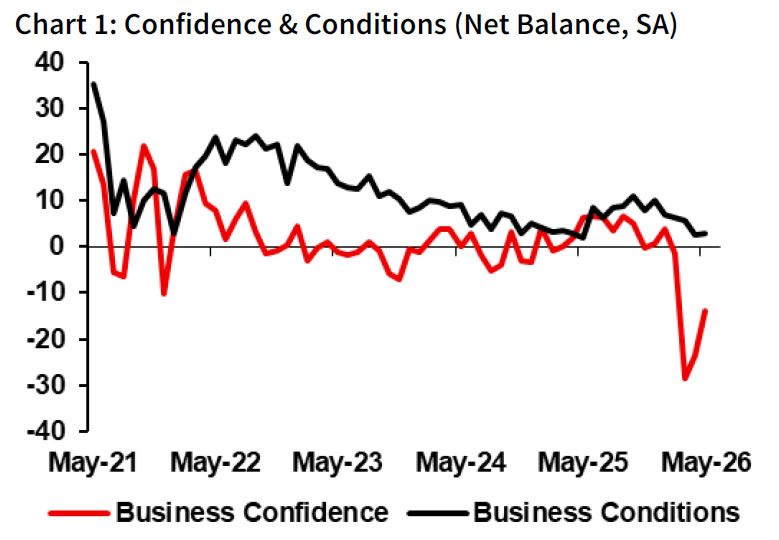

Australia NAB Business Confidence Lifts From Deep Lows as RBA Tightening Bites

Australia's NAB Business Confidence Index improved from -23 to -14 in May, recovering from extremely weak levels as concerns over the economic fallout from the Middle East conflict eased. However, confidence remained firmly negative, highlighting ongoing caution among businesses despite signs that the economy has avoided a more severe slowdown. Business Conditions held steady at 3, with gains in trading and employment offset by weaker profitability.

The survey suggested that activity remains resilient despite higher interest rates and the recent energy price shock. Trading conditions improved from 7 to 8 and employment conditions rose from 1 to 2, while profitability slipped from 0 to -1. NAB said the disruption caused by the Middle East conflict has been less severe than initially feared, particularly with regard to supply chains. According to NAB's Gareth Spence, economic growth has slowed since late 2025 but continues to expand rather than contract, a view supported by spending and transaction data.

Inflation indicators also moved in a more favorable direction. Purchase cost growth slowed from 4.5% to 2.6% in quarterly equivalent terms, labour cost growth eased from 1.7% to 1.5%, while product price growth and retail price growth both halved. The moderation in cost and price pressures adds to evidence that RBA's tightening cycle is cooling the economy. While weak confidence remains a concern for future investment and hiring decisions, the survey points to an economy that is slowing rather than stalling.

| Indicator | April | May |

|---|---|---|

| NAB Business Confidence | -23 | -14 |

| Business Conditions | 3 | 3 |

| Trading Conditions | 7 | 8 |

| Profitability Conditions | 0 | -1 |

| Employment Conditions | 1 | 2 |

| Purchase Cost Growth | 4.5% | 2.6% |

| Labour Cost Growth | 1.7% | 1.5% |

| Product Price Growth | 1.8% | 0.9% |

| Retail Price Growth | 3.1% | 1.5% |

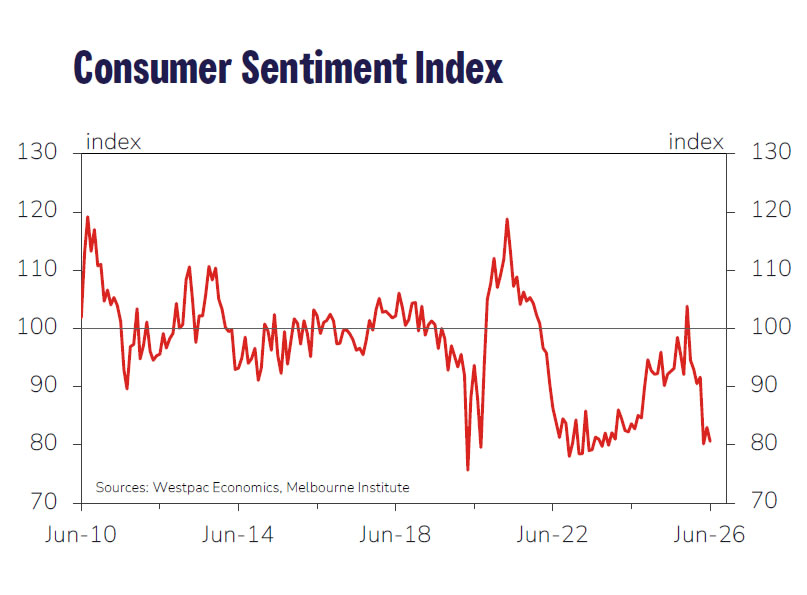

Australian Westpac Consumer Sentiment Falls Back Near Record Lows as Cost-of-Living Pressures Intensify

Australian consumer sentiment deteriorated in June, with the Westpac-Melbourne Institute Consumer Sentiment Index falling -2.9% month-on-month from 83.0 to 80.6. The decline reversed much of May's recovery and left confidence back among the weakest levels recorded in the survey's fifty-year history, highlighting the growing strain on households from higher living costs and rising interest rates.

Westpac said cost-of-living pressures had returned "with a vengeance", with consumers reporting a significant deterioration in both current and expected family finances. The "family finances versus a year ago" index dropped -7.5% to 67.3, while expectations for family finances over the next 12 months fell -8.5% to 85.1. Although views on the economy over the coming year improved modestly from extremely weak levels, longer-term confidence continued to deteriorate, with the five-year outlook index falling to a three-year low of 86.5.

The survey reinforces the difficult balancing act facing RBA ahead of next week's policy meeting. While the weakening in consumer sentiment highlights the impact of aggressive monetary tightening and higher energy prices, inflation remains the central bank's primary concern. Westpac expects RBA to pause after raising rates at its previous three meetings, giving policymakers time to assess the effects of tightening and the energy shock. However, with underlying inflation still running above the Bank's 2-3% target range, the prospect of further rate increases later this year remains firmly on the table.

| Indicator | May | June | Change m/m |

|---|---|---|---|

| Consumer Sentiment Index | 83.0 | 80.6 | -2.9% |

| Family Finances vs Year Ago | 72.8 | 67.3 | -7.5% |

| Family Finances Next 12 Months | 93.0 | 85.1 | -8.5% |

| Economy Next 12 Months | 74.2 | 77.8 | +4.9% |

| Economy Next 5 Years | 89.4 | 86.5 | -3.2% |

GBP/USD Struggles To Recover As Losses Continue To Linger

Key Highlights

- GBP/USD started a major decline below 1.3450 and 1.3420.

- It traded below a contracting triangle with support at 1.3410 on the 4-hour chart.

- EUR/USD dipped heavily before the bulls appeared near 1.1500.

- Gold extended losses below $4,400 and tested $4,280.

GBP/USD Technical Analysis

The British Pound failed to surpass 1.3520 against the US Dollar. GBP/USD started a fresh decline below 1.3460 and 1.3450 to move into a bearish zone.

Looking at the 4-hour chart, the pair traded below a contracting triangle with support at 1.3410. The pair settled well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

It even tested 1.3300 before the bulls took a stand. The pair is now consolidating losses above 1.3300. On the upside, an immediate resistance could be 1.3375. The next major resistance might be 1.3400.

A close above 1.3400 could open doors for gains. The main hurdle for the bulls could be 1.3420 and the 100 simple moving average (red, 4-hour). If there is a close above 1.3420, the pair could rise toward the 1.3480 level.

Immediate support could be 1.3300. The first major support might be 1.3280. A close below 1.3280 could open the doors for a larger decline toward 1.3220. Any more losses might set the pace for a test of 1.3150.

Looking at EUR/USD, the pair found support near 1.1500, started a consolidation phase, and might soon attempt a recovery wave.

Upcoming Key Economic Events:

- US Existing Home Sales for May 2026 (MoM) - Forecast +0.1%, versus +0.2% previous.

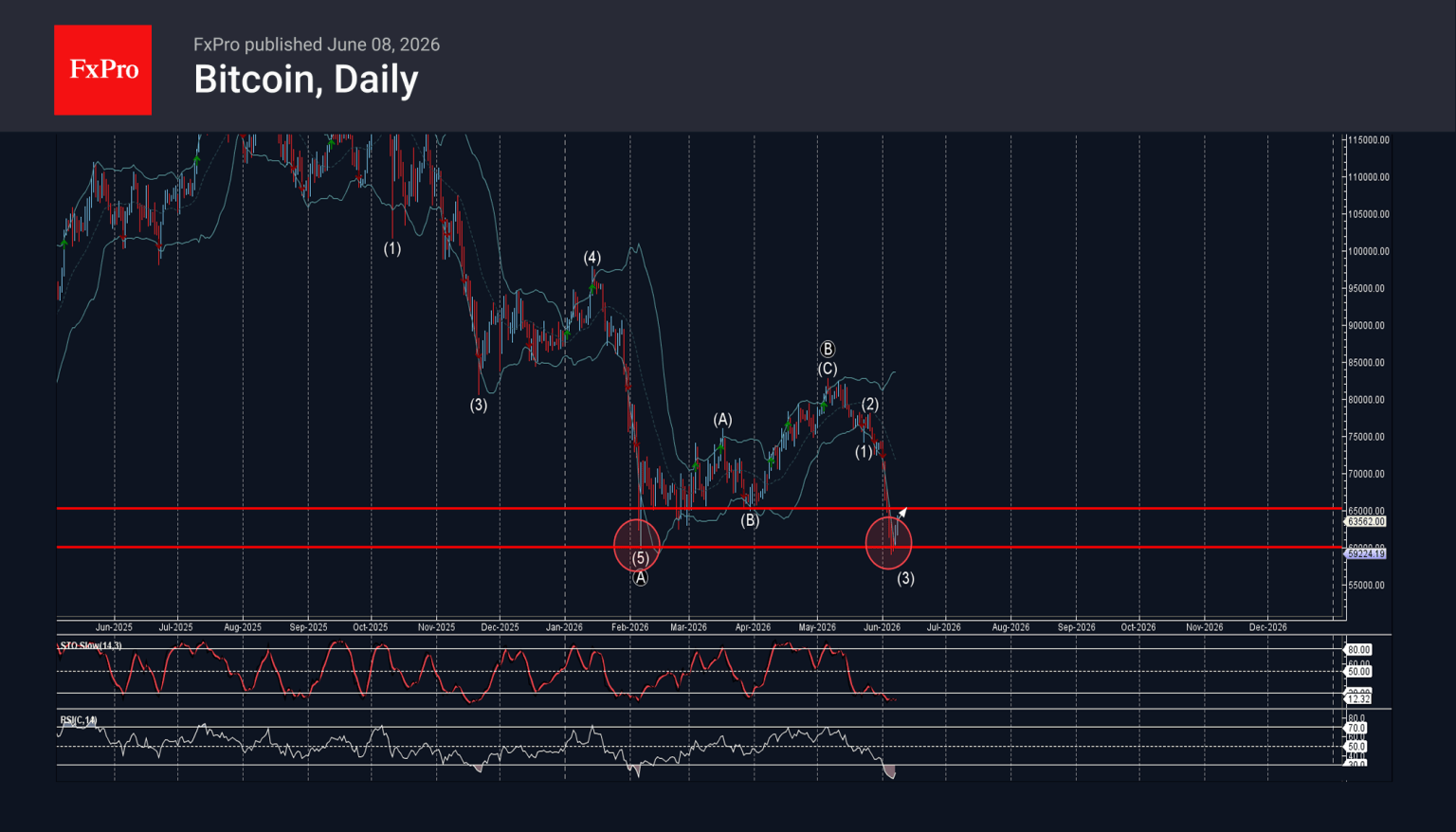

Bitcoin Wave Analysis

Bitcoin: ⬆️ Buy

- Bitcoin reversed from powerful support level 60000.00

- Likely to rise to resistance level 65000.00

Bitcoin cryptocurrency recently reversed up from the powerful support level 60000.00 (which stopped the previous sharp downward impulse wave (A) at the star of February).

The support zone near the support level 60000.00 was strengthened by the lower daily Bollinger Band

Given the strength of the support level 60000.00 and the oversold daily Stochastic and RSI indicators, Bitcoin cryptocurrency can be expected to rise to the next resistance level 65000.00 (former support from March).

Eco Data 6/9/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturingles Q1 | 2.80% | -0.50% | 0.80% | |

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y May | 3.40% | -3.40% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 2.50% | 2.30% | ||

| 00:30 | AUD | Westpac Consumer Confidence Jun | -2.90% | 3.50% | ||

| 01:30 | AUD | NAB Business Confidence May | -14 | -24 | ||

| 01:30 | AUD | NAB Business Conditions May | 3 | 3 | ||

| 03:00 | CNY | Trade Balance (USD) May | 105.4B | 88.7B | 84.8B | |

| 06:00 | EUR | Germany Industrial Production M/M Apr | 0.40% | 0.50% | -0.70% | -0.10% |

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | 14.5B | 15.4B | 14.3B | 14.7B |

| 10:00 | USD | NFIB Business Optimism Index May | 95.3 | 96 | 95.9 | |

| 12:30 | CAD | Trade Balance (CAD) Apr | 2.7B | 2.5B | 1.8B | |

| 12:30 | USD | Trade Balance (USD) Apr | -55.9B | -55.5B | -60.3B | -56.6B |

| 14:00 | USD | Existing Home Sales May | 4.17M | 4.05M | 4.02M |

| 22:45 | NZD |

| Manufacturingles Q1 | |

| Actual | 2.80% |

| Consensus | |

| Previous | -0.50% |

| Revised | 0.80% |

| 23:01 | GBP |

| BRC Like-For-Like Retail Sales Y/Y May | |

| Actual | 3.40% |

| Consensus | |

| Previous | -3.40% |

| 23:50 | JPY |

| Money Supply M2+CD Y/Y May | |

| Actual | 2.50% |

| Consensus | |

| Previous | 2.30% |

| 00:30 | AUD |

| Westpac Consumer Confidence Jun | |

| Actual | -2.90% |

| Consensus | |

| Previous | 3.50% |

| 01:30 | AUD |

| NAB Business Confidence May | |

| Actual | -14 |

| Consensus | |

| Previous | -24 |

| 01:30 | AUD |

| NAB Business Conditions May | |

| Actual | 3 |

| Consensus | |

| Previous | 3 |

| 03:00 | CNY |

| Trade Balance (USD) May | |

| Actual | 105.4B |

| Consensus | 88.7B |

| Previous | 84.8B |

| 06:00 | EUR |

| Germany Industrial Production M/M Apr | |

| Actual | 0.40% |

| Consensus | 0.50% |

| Previous | -0.70% |

| Revised | -0.10% |

| 06:00 | EUR |

| Germany Trade Balance (EUR) Apr | |

| Actual | 14.5B |

| Consensus | 15.4B |

| Previous | 14.3B |

| Revised | 14.7B |

| 10:00 | USD |

| NFIB Business Optimism Index May | |

| Actual | 95.3 |

| Consensus | 96 |

| Previous | 95.9 |

| 12:30 | CAD |

| Trade Balance (CAD) Apr | |

| Actual | 2.7B |

| Consensus | 2.5B |

| Previous | 1.8B |

| 12:30 | USD |

| Trade Balance (USD) Apr | |

| Actual | -55.9B |

| Consensus | -55.5B |

| Previous | -60.3B |

| Revised | -56.6B |

| 14:00 | USD |

| Existing Home Sales May | |

| Actual | 4.17M |

| Consensus | 4.05M |

| Previous | 4.02M |

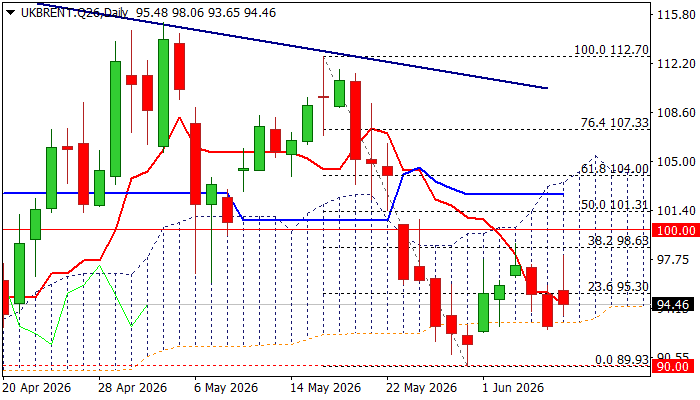

BRENT OIL – Daily Cloud Base Came Under Increased Pressure Again After Short-Lived Recovery Attempts

Brent oil price jumped on Monday morning following an escalation in the Middle East (Israel attacked Iran’s energy infrastructure and Iran responded by a wave of attacks on Israel) but gains were short-lived, as the price fell on Iran’s announcement of an end to attacks that calmed the markets.

In addition, OPEC+ approved a fourth increase in oil output to stabilize oil markets that added pressure on prices.

Brent price was down 4.5% on Thursday and Friday with strong fall being contained by daily Ichimoku cloud base ($93.14) which continues to provide solid support (probe below cloud base on May28 / June1 period resulted in a false break).

Daily studies remain predominantly bearish and contribute (in addition to weakening fundamentals) to scenario of renewed attack at cloud base, firm break of which to generate fresh bearish signal and open way towards $90 zone (psychological / May 29 low / 100DMA).

Near-term bias is expected to remain with bears while the price stays below significant barrier at $98.63 (Fibo 38.2% of $112.70/$89.93) which has so far capped two attempts and guards another important resistance at $100 (psychological).

Caution on potential repeated failure at cloud base that may keep near term action in extended sideways mode.

Res: 97.41; 98.63; 99.70; 100.00

Sup: 93.14; 91.76; 90.81; 89.93

Bank of England Preview – On Hold Amid Growing Policy Divide

- We expect the Bank of England on hold, but hawkish voices are growing louder.

- Data has come in on the soft side since the April meeting, but the inflation risks remain pronounced.

- Data releases ahead of the meeting could push more votes back in the hawkish camp but are not likely to change the hold decision.

Since the April meeting, data has supported our call for maintaining Bank Rate unchanged. That said, it remains too early to make any conclusions on inflation spillovers. We get fresh inflation and labour market data ahead of the meeting.

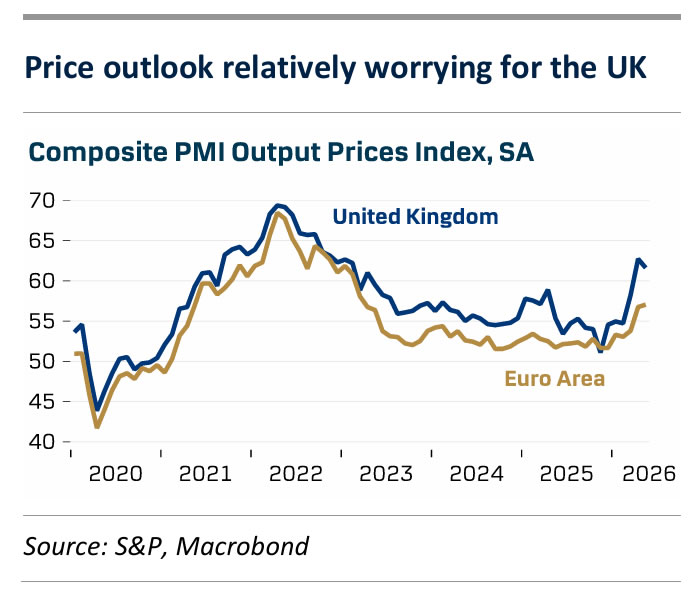

May PMI data suggest the economy came to a marked slowdown following a solid April print, as the service sector index took its steepest decline in four years. The manufacturing sector on the other hand remains quite solid with sustained growth in output and orders. Q1 growth was relatively high at 0.6%, although uncertainty on the seasonal pattern suggests momentum might be weaker. Retail sales reflected the deteriorating consumer sentiment in April with the biggest monthly decline in a year.

Job loss accelerated to -100K in April and the unemployment rate increased to 5.0%. At the same time, wage pressures remain on a weakening trend and according to the BoE decision maker panel (DMP), firms also expect slower wage growth going forward, which is key to the prospects of sustaining service inflation at acceptable levels. CPI inflation was lower than expected in April as core inflation continues lower. Producer prices, on the other hand, are on the rise and the PMI survey suggests businesses are raising prices, particularly in the manufacturing sector but also in service. Reported price increases are much steeper than in the euro area. According to the DMP, businesses largely expect compressed margins, though, suggesting more modest feed through of energy costs.

We continue to see Governor Bailey's stance as the key to pin down the policy outlook. His remarks have been mostly dovish leaning as he has argued that allowing inflation to run above target is justified given the uncertainty about the impact of the Iran war on the economy and the weak pace of growth. We could quickly be back in a situation with a completely split MPC with recent hawkish remarks not least from Meghan Greene, who is more worried about second round price effects than what the official BoE risk scenarios imply.

BoE call. Hiking rates will have to be weighed against a considerable risk of exacerbating a looming economic contraction. We think it is most likely the BoE will remain sidelined for the foreseeable future, but the vote split could soon be back where only a slim majority stands in the way of hiking rates.

Market reaction. We will keep a close eye on the updated views of MPC members and the vote split. The relatively weak UK growth outlook and our dovish stance on BoE compared to market pricing weighs on our GBP call. We forecast EUR/GBP to move higher towards 0.89 on a 6-12-month horizon.

Sunset Market Commentary

Markets

The Iran headline roulette has been doing overtime the past days. Over the weekend, it spit out news about fighting between Israel and Hezbollah which triggered retaliation by Iran against Israel and afterwards the other way around. The escalation prompted a complete ban by Houthis (part of the “axis of resistance”) on Israel in the Red Sea mainly by control over de Bab-el-Mandeb straight. Brent crude jumped from a $93/close last week to $98/b, before US president Trump stepped in. He claimed that he is calling all shots and that Israel and Iran would look for an immediate cease-fire. Later, both Israel and Iran declared an end to military operations which pulled the oil price back towards $94/b. However, Israel simultaneously indicated that it hasn’t reached its objectives towards dismantling Hezbollah suggesting that the risk of escalation remains extremely high. Intraday moves in oil prices drove action on other markets with core bonds yields initially adding up to 5 bps. As US trading gets going, changes on yield curves are negligible. EUR/USD tested the 1.15 big figure following Friday’s break below 1.16 before rebounding to 1.1544 as oil prices drop and Friday’s equity market correction didn’t continue after the opening bell. The EuroStoxx 50 started over 1% weaker following Friday’s heavy AI-correction, but is currently flat. US equities open up to 1.5% for the Nasdaq with investors apparently taking Nvidia CEO Jensen Huang’s advise to “buy the dip”. For the time being, we err on the side of a more profound correction especially if this week’s US inflation numbers (Wednesday) trigger more hawkish Fed repositioning bets. The US mid-month refinancing operation (3, 10, 30) is another risk factor. Today and tomorrow’s empty eco calendars nevertheless leave space for more headline-swings with the impact of Friday’s SpaceX IPO also added to the equation. They provide some kind of smoke screen to underlying economic developments.

News & Views

Czech industrial production and orders continued to grow slightly in April. Industrial production in real terms increased by 1.4% M/M and 1.5% Y/Y. The increase was driven by manufacturing of motor vehicles and their spare parts and by computer, electronics and optical products amongst others. A negative impact on production was registered from mining and quarrying, and repair and installation of equipment and in Food and beverages production. The value of new orders at current prices increased by 3.3% M/M and 2.7% Y/Y. New non-domestic orders increased by 3.5% Y/Y. Domestic new orders recorded an increase by 1.1%. The average registered number of employees in industry decreased by 1% Y/Y. At the same time, construction activity remained in strong April rising 0.6% M/M and 7.7% Y/Y. The number of building permits granted increased by 14.7% and the number of started dwellings even increased by 89.7% Y/Y.

In an interview with Reuters, National Bank of Hungary (MNB) deputy governor Kurali indicated that the central bank received better-than expected inflation data of late together with an improvement in risk premia. "As a result, potentially the required rate to achieve and maintain price stability might be lower.". At the same time, Kurali said that the prospect of major central banks (ECB, Fed, Bank of Japan) raising interest rates remains a reason for caution. As the MNB evaluates the potential trajectory of policy rates, it will have to uphold positive real rates to achieve and maintain price stability. Asked whether any easing would be a one-off or the start of a cycle, the deputy governor indicated that it's difficult to talk about cycles in this environment. Kurali also said that the MNB will launch a regular review of its 3% medium term inflation target in the summer as the government aims to meet euro adoption criteria by 2030. The review is said to examine the impact of a lower target closer to euro zone levels, and the strategy and timing for any change, which could come in one or two steps. The MNB expects this analysis to be fully prepared and discussed by autumn.