Sample Category Title

Sunrise Market Commentary

Markets

Since the conflict in the Middle East, eco data were almost ‘by definition’ considered outdated as markets try to assess the impact of higher energy prices and other supply disruptions as the conflict developed. However, especially US data have regained relevance of late. The combination of a resilient economy (strong ISM’s) and reaccelerating inflation made Fed policy makers and markets pondering whether the next Fed move should be a rate hike. Friday’s May payrolls reinforced that process. The US economy added 172k jobs, almost double the expectations. Figures for March and April were upwardly revised by 93k. This is no longer the “no hire, no fire” stalemate that inspired Fed caution end last year. The strong payrolls turn the focus back to the price stability part of the Fed’s mandate as US May headline CPI (to be published Wednesday) is expected to surpass the 4% mark. US yields added between 10.4 (2-y) and 2.1 (30-y) bps. Markets now (more than) fully discount a Fed rate hike by December meeting. Fed’s Hammack at least also suggested that it might soon be “appropriate to act on rates”. Gains in German yields were understandably more moderate (from +3.1 bps (2-y) to 0.8 bps (30-y)). The sharp rise in (real) US yields came at a difficult time for especially US equity markets. Indices got captured in spiraling down move. The S&P 500 lost 2.64%. Rising (real) yields didn’t help to dent developing doubts on AI-related valuations. The Nasdaq corrected 4.18% following a two-month breathtaking rally. The combo of higher US yields, an outright risk-off and little prospect on a solution to the Middle-east conflict provided a perfect set-up for the dollar. DXY cleared the 99.54 resistance area to close the week at 100.07, the best level since early April. EUR/USD tumbled below the 1.16/1.1575 support area to finish at 1.152. USD/JPY surpassed the 160 barrier (currently 160.3). This is seen as potential intervention territory. Question is how appropriate it is for Japanese authorities to use ammunition to fight what is basically USD strength.

Sentiment in Asia this morning remains outright risk-off. Aside from the payrolls/AI-related sell-off in the US on Friday, a new flaring up in the Iran conflict (especially reciprocal strikes between Iran and Israel) put further pressure on equities (Kospi -7.7%) and bonds (US yields adding 3-4 bps across the curve). Given multiple uncertainties at the start of week there is little reason to fight the trends from end last week (higher yields, stronger dollar, equities in the defensive). Later this week, aside from developments in Iran, the US CPI and the ECB policy decision will take center stage. US headline inflation at 4%+ and core nearing/hitting 3% might further reinforce Fed rate hike bets. The ECB is widely expected to raise the policy rate by 25 bps. Key question is whether/how strong Lagarde will guide to a potential back-to back rate hike already at the July meeting. Last but not least, also keep a close eye at the 3-y/10-y/30-y US Treasury refinancing operation to assess investor appetited at current levels.

News & Views

Permanent placements in the UK declined at the fastest pace since last July, the monthly jobs reports by KMPG, REC and S&P for May said. UK companies blamed low confidence around the outlook and greater cost pressures for the pullback in permanent hiring. Those that did want additional staff often looked to more flexible solutions instead. That supported the strongest rise in temp billings for over three years. Overall vacancies fell by the quickest in three months, driven by the permanent job segment. Demand for temporary workers moved closer to stabilization. Recruitment companies reported redundancies, fewer job opportunities and concerns over current job security to have pushed up the availability of job candidates sharply. That in turn has dampened rates of pay growth in May, together with lower demand for staff and tighter client budgets. Starting wages and temp wages increased modestly at a pace that was slower than in April and well below the historical average.

The seven OPEC+ members that are engaged in the monthly quota adjustments decided yesterday on another modest 188k barrel increase for next month, further restoring the double-layered production curbs introduced in 2023. The decision is merely a symbolically one since much if not all of the additional output isn’t able to leave the Middle East area with the Strait of Hormuz still effectively closed. The price of a barrel of Brent oil remains therefore unaffected, instead eying the recent renewed skirmishes in the region. Brent currently trades around $97.3, up from Friday’s $93 close. In other oil news, Saudi Arabia lowered the price of its flagship Arab Light crude for a second month straight. Asian buyers will pay $6 a barrel less from next month on, reducing the premium over the regional benchmark to $9.50 a barrel, still near the highest in decades, according to Bloomberg. European buyers will pay $10 less for all grades, while varieties for North America were cut by $2 per barrel.

Renewed Iran Uncertainty and Rising Fed Hike Speculations

In focus today

In the euro area, the June Sentix investor confidence index is released today. Markets look for an improvement to -14.6 (May: -16.4), extending last month's positive momentum, although sentiment remains pessimistic amid rising inflation and a weak growth outlook.

In Germany, April industrial orders are due. After the 5.0% m/m surge in March, believed to reflect firms bringing orders forward on concerns over higher costs and supply disruptions, markets now expect a 2.0% m/m decline.

Overnight, China releases trade data, with focus on whether export growth can be sustained amid global headwinds from the war in Iran. Exports have grown at a solid pace of around 15% y/y so far this year, but weaker PMI export orders in April and May suggest momentum is fading.

This week, the main market mover is Thursday's ECB meeting, where we and markets expect a 25bp hike. Ahead of that, Wednesday brings the Bank of Canada rate decision alongside Danish and Norwegian inflation figures, followed on Thursday by Norges Bank's Regional Network Survey, the Central Bank of Turkey's rate decision and final Swedish inflation. The week ends with final euro area inflation on Friday.

Economic and market news

What happened overnight

On the Iran war, Israel carried out overnight air strikes inside Iran after Tehran fired ballistic missiles at northern Israel on Sunday, the first such exchange since the April ceasefire. Iran's attack followed Israeli strikes on Beirut earlier in the day. The escalation hit oil markets this morning, with Brent crude up about 3% to around USD 96/bbl, as hopes fade for a broader regional deal to reopen the Strait of Hormuz. US President Donald Trump said he had told Israel not to respond militarily and insisted the flare-up would not derail a potential US-Iran agreement.

In Japan, final Q1 GDP was revised slightly lower to 0.45% q/q (prev.: 0.51%, cons.: 0.3%) on weaker capital expenditure, while private consumption, which accounts for approximately 50% of GDP, held steady. The Bank of Japan is expected to stay on its current policy path.

What happened over the weekend

In the US, Friday's May jobs report came in stronger than expected. Nonfarm payrolls rose 172k (Danske: +110k, cons.: +85k) and the unemployment rate printed at 4.3% (Danske: 4.2%, cons.: 4.3%). Previous nonfarm payroll figures were revised up by a sizeable 93k for March-April, and wage sum growth, which is closely correlated with private consumption, accelerated to 4.1% y/y from 3.8%. The labour market strength remains broad-based across sectors, in line with the signal from the ADP report earlier last week. Overall, the report revealed no major weak spots, which led markets to increase the probability of Fed hikes. In the immediate market reaction, EUR/USD moved lower and UST yields rose, with markets now pricing around 40bp of cumulative Fed hikes towards 2027.

Also in the US, the May Challenger report on Thursday showed announced layoffs rising to 97k, the third consecutive monthly increase. Technology led with 38k cuts and AI remained the main stated driver, accounting for about 40% of all announced layoffs.

In Sweden, May flash inflation surprised to the upside. Core inflation printed at 0.5% y/y (Danske: 0.2%, cons.: 0.3%), which pushed up CPIF to 1.5% y/y (Danske: 1.3%, cons.: 1.3%). The surprise stemmed mainly from services, where the limited flash details indicate unusually strong price increases in recreation, up 3.9% m/m in May. From 1 May, the fuel tax was reduced by SEK 1 per litre, which is helping to dampen the rise in energy prices. While the stronger core reading is unlikely to change our expectation that the Riksbank will stay on hold in June, it reinforces the case for tighter policy further ahead. We continue to look for two 25bp rate hikes in September and December.

In the euro area, the third estimate revealed that GDP unexpectedly contracted by 0.2% q/q in Q1 2026, revised down from the previous 0.1% q/q growth estimate and marking the first decline in over three years. The revision mainly reflects a sharp 12.1% q/q drop in Irish GDP, driven by lower exports from multinational pharmaceutical groups. Despite the weaker activity, euro area employment rose 0.1% q/q in Q1 2026.

In Norway, manufacturing production decreased -0.9% m/m in April, taking the underlying trend to 0.4% 3m/3m. Hence, the moderate upswing in manufacturing activity continues, supported by oil-related industries, whereas activity in non-oil industries now is moving sideways.

Equities: Equities sold off sharply on Friday, particularly during the US session, led by tech. Still, it is worth noting that more industries actually finished higher than lower on the day, despite the weakness in the headline US indices. The sell-off was extremely concentrated: US semiconductors were down 8.2%, and semis account for roughly 15% of the S&P 500.

The VIX rose to 21, headline indices were lower, led by Nasdaq, but small caps outperformed. That points to tech-led large-cap underperformance rather than a broad-based risk-off move. Importantly, this had nothing to do with Iran. The Iran headlines came later, and oil was down on Friday. Nor was this caused by stronger jobs data. That may well have been the trigger, but it is a poor explanation for the move. The real reason is that global tech, the largest sector in the world, had risen around 50% in just about two months. After that kind of move, setbacks like Friday's are entirely normal.

Please remember, in the strongest bear markets, we also get days with very powerful equity rallies, and vice versa: in strong bull markets, we also get days with sharp selloffs. That is exactly the kind of environment we are in now.

Even if the Fed were to hike, or if oil were to rise 3% (like this morning), that does not change the outlook for the AI build-out or the extreme earnings growth currently being delivered. Hence, this should not be used as the excuse for why tech sold off on Friday.

Asia is massively lower this morning, especially in markets where tech has driven strong year-to-date performance. That should be seen in the same light. European futures are lower, catching up to Friday's late US weakness, while US futures, especially in the tech space, are higher this morning.

FI and FX

Oil jumped overnight, with Brent at USD 96.5/bbl as the situation in the Middle East escalated with new air strikes between Israel and Iran. EUR/USD plunged towards 1.15 on Friday following the strong US jobs report and yields rose. US yields continue to move higher in overnight trading with 2Y UST now at 4.19%, around 15bp higher compared to before the jobs report was released. The 10Y UST is trading at 4.57%. The strong jobs report weakened risk sentiment on Friday, and this theme continued in Asia overnight. The data calendar is thin for the day, but later this week focus will be on the US CPI report (Wed) and the ECB (Thu). A hike to 2.25% from the ECB is widely expected and priced in, but we do not expect Lagarde to pre-commit to further hikes.

Tech Rout Deepens and Middle East Tensions Fuel Market Tremors

Key Takeaways

- AI-driven equities face their biggest setback in months. A sharp selloff in semiconductor and technology stocks, triggered by valuation concerns and disappointing guidance from key AI-related companies, has halted the nine-week Wall Street rally and raised questions about the sustainability of the AI super cycle.

- Middle East tensions have reignited energy market risks. Fresh Iran-Israel hostilities pushed crude oil prices higher, reviving concerns over global energy supply disruptions and reinforcing inflationary pressures across major economies.

- Strong US labour data has revived expectations of a Fed rate hike. A significantly stronger-than-expected US payrolls report has increased the probability of a Federal Reserve rate hike later this year, driving Treasury yields higher, strengthening the US dollar, and tightening global financial conditions.

- Chart of the day: WTI crude gapped up and rebounded from minor ascending channel support at $91.40/bbl.

Chart of the Day – WTI Crude Erased Last Friday’s Losses

Fig. 1: West Texas Oil CFD minor trend as of 8 Jun 2026 (Source: TradingView). The information presented is historical information, and past performance is not indicative of future performance.

The price action of the West Texas Oil CFD (a proxy for the WTI crude oil futures) gapped up by 3.3% in today’s Asia opening session to trade at $95.10 per barrel at this time of writing, erasing last Friday’s loss of 3%.

Near-term technicals have flipped bullish, as the hourly RSI momentum indicator exited oversold territory and broke out above its former descending resistance.

Watch the 91.40 key short-term pivotal support, and a clearance above 95.45 would see the intermediate resistance at 100.00 (also close to the 20-day and 50-day moving averages) in the first step.

However, a break and an hourly close below 91.40 would signal a retest of the 29 May 2026 minor swing low at 89.00. Below it extends losses towards the next intermediate support at 85.50.

Top Macro Headlines

- Tech deflates in brutal Wall Street reversal: Wall Street’s historic nine-week winning streak ground to a violent halt on Friday as a massive tech-led selloff intensified. The Nasdaq 100 Index plunged 4.8%, and a broad gauge of chipmakers tumbled 10% in its worst single-session routing in months, as growing anxiety over AI overvaluation triggered widespread institutional profit-taking.

- Geopolitical escalation as Iran fires on Israel: Middle East tensions exploded over the weekend. Following an Israeli strike on Beirut, Iran directed a massive salvo of missiles targeting Israeli territory. WTI and Brent crude futures immediately spiked 2.8% to hit at $92.70 and $95.40 a barrel in today’s Asia opening session, though gains moderated slightly after President Trump said the flare-up would not derail the overarching regional peace framework negotiations.

- Hot US jobs report shifts Fed target: The US labour market showed unexpected, robust resilience, with May nonfarm payrolls adding 172,000 positions, shattering the consensus forecast of 85,000. While the unemployment rate held at 4.3%, the red-hot hiring numbers prompted Fed funds futures traders to immediately price in a 60% probability of a Federal Reserve interest rate hike as early as October 2026.

Key Macro Themes

- The Great AI narrative fray: The unyielding “AI-drives-everything” bull market faced its harshest reality check over the weekend. A combination of hot macroeconomic data and localised tech earnings disappointment (e.g., Broadcom) has investors fiercely debating whether the current AI market cap demands a tactical correction, particularly as blockbuster private listings such as SpaceX threaten to drain liquidity from broader equity markets.

- The Mega-IPO liquidity drain: Wall Street trading desks are highly anxious over an unprecedented wave of massive capital calls coming to market. Elon Musk’s SpaceX has locked in a fixed $135/share price targeting a record-shattering $75 billion public raise this week, while generative AI giant Anthropic just filed confidentially for an IPO targeting a near 1$ trillion valuation. Capital allocators are actively selling existing liquid equities to free up space for these generational private tech entries.

- Sovereign bond yield resurgence: The combination of an inflationary energy supply shock and an unrelenting US jobs landscape has completely crushed any remaining expectations for central bank rate cuts. Two-year Treasury yields surged 10 basis points on Friday to 4.15%, signalling a profound multi-month repricing of global cost of capital.

Global Markets Impact

Equities: S&P 500 futures fell 0.3%, and Nasdaq 100 futures slipped 0.2% in early Asian trade before easing towards a slight gain of 0.01% and 0.35%, after Friday’s steep losses, where the S&P 500 sank 2.6%. The medium-term uptrend, which began late March 2026, has officially stalled.

Fixed Income: US Treasuries tumbled; two-year yields closed Friday up 10 bps to 4.15%. The 10-year Treasury yield extended its gains by another 4 bps to 4.57% in early Monday trading, maintaining immense upward pressure.

FX: The US Dollar Index gained aggressively against all G-10 peers on a cocktail of safe-haven flows and the hawkish Fed rate adjustment. The Euro flattened out at $1.1519, a 2-month low, while the British Pound hovered defensively at $1.3317, near a 1-month low. In addition, the AUD tumbled to around a 2-month low of 0.7022, and the JPY grinded lower towards the recent intervention zone of 160.45/65 per US dollar.

Commodities: Brent crude gapped higher by 2.8% to trade at $95.40/bbl on the back of Iranian missile deployment. Spot Gold extended its losses from Friday, slipping to $4,315/oz as expectations of higher-for-longer global interest rates diminished its non-yielding appeal.

Asia Pacific Impact

- Regional AI stocks routed: Tech-heavy Asian benchmarks bore the brunt of global tech contagion on Monday morning. South Korea’s Kospi index, the world’s top-performing gauge this year due to its exposure to memory and AI chips, tumbled 5.5% on Friday and opened 7% lower today. The Nikkei 225 also posted steep losses of 5%. Blood baths are seen in other Asia-Pacific benchmark stock indices: Hang Seng Index (-1.7%), China A50 (-1.6%), CSI 300 (-2.4%), ASX 200 (-0.7%), and STI (-1.4%).

- Currency interventions in play: The South Korean won slid to its weakest valuation framework since 2009 to an intraday high of 1,559 per US dollar in today’s Asia opening session, forcing the Seoul government to deploy an emergency series of curbs to support the currency. The Japanese Yen also remains deeply pinned, trading weakly at 160.30 per US dollar, keeping Bank of Japan intervention flags fully raised.

- Trade sentiment frozen: Early regional performance is further muted by traders waiting on major Chinese trade balance data later this week, as regional supply chains undergo structural realignment and linger amid lingering tariff anxieties.

Top 2 Events to Watch Today

- New York Fed 1-YR Inflation Expectations (May) – 11.00 pm SGT

Impact: USD, US Treasuries, US stock indices - US-Iran peace talks/ceasefire developments

Impact: All asset classes

US CPI Leads High-Stakes Week as Fed Hike Expectations Build; ECB and BoC Meet

Three major events dominate the week ahead, but they all revolve around a single question: how much of the recent oil shock will ultimately feed into inflation and alter the policy outlook?

Last week's stronger-than-expected US employment report reinforced the view that Fed can afford to keep its focus squarely on inflation. With labor market concerns fading into the background, investors are increasingly debating whether higher energy prices could eventually force another rate hike later this year.

Against that backdrop, Wednesday's US CPI report stands as the week's most important event, carrying the greatest potential to move Treasury yields, currencies and global equities. The ECB meeting follows closely behind, though the focus is likely to be on updated forecasts rather than the widely anticipated rate increase. Meanwhile, the Bank of Canada faces a very different challenge as policymakers balance recessionary conditions at home against what they continue to view as a temporary, oil-driven rise in inflation.

The US inflation report is likely to set the tone for global markets. Following three consecutive months of solid payroll growth, the labor market is no longer providing an argument for easier monetary policy. Instead, the resilience in employment gives Fed officials greater flexibility to focus on inflation developments and the pass-through effects of higher energy prices.

Consensus forecasts point to headline CPI accelerating from 3.8% year-on-year to 4.2% in May, while core CPI is expected to edge up from 2.8% to 2.9%. While a rise in headline inflation is largely anticipated due to energy costs, markets will pay closer attention to the core reading. Any upside surprise in core inflation would likely reinforce expectations that the Fed may need to tighten policy further, pushing Treasury yields and Dollar higher while weighing on equity valuations.

The market reaction function has changed significantly over the past month. Rate cuts are effectively off the table, and Fed funds futures now imply nearly a 75% probability of at least one additional rate increase by year-end. The CPI report will therefore serve as a critical test of whether those expectations are justified.

For the ECB, a 25 basis point increase in the deposit rate to 2.25% is widely expected. Because the decision itself is fully priced, investors will focus instead on President Christine Lagarde's guidance and, more importantly, the updated staff projections. Recent PMI surveys have painted an increasingly challenging picture for Eurozone growth, raising concerns that the region may be drifting toward recession even as inflation pressures intensify.

Nevertheless, Lagarde is likely to maintain a balanced tone, acknowledging upside inflation risks while emphasizing growing concerns about economic activity. Markets should not expect strong forward guidance. Instead, the new projections may provide the clearest policy signal. Upward revisions to near-term inflation forecasts combined with downgrades to 2026 growth projections toward the 0.3% to 0.5% range would reinforce the stagflation narrative currently emerging across Europe.

While a Reuters survey found that more than 60% of economists expect one additional ECB rate increase later this year, likely in September, conviction remains limited. Confirmation of weaker growth prospects could cap Euro gains even if policymakers retain a tightening bias.

The Bank of Canada enters the week from a markedly different position. Canada's economy has already recorded two consecutive quarters of contraction, meeting the technical definition of recession. As a result, the central bank's policy framework differs substantially from that of both Fed and ECB.

Recent employment data have provided policymakers with some breathing room. Strong May job growth reduced pressure for immediate policy easing and supports the Bank's decision to keep rates steady. At the same time, officials have repeatedly indicated a willingness to look through temporary inflation increases driven by energy prices, arguing that domestic economic weakness should absorb part of the shock.

A hold at 2.25% is widely expected. According to Reuters polling, more than 80% of economists expect rates to remain unchanged through the end of the year. The policy statement and press conference are likely to reinforce the view that the Bank remains on hold, though uncomfortably, as it balances recession risks against temporary inflation pressures.

Highlights for the week:

| Date | Currency | Event |

| Tue, June 9 | AUD | Consumer & Business Confidence |

| Wed, June 10 | CNY | China CPI & Trade Balance |

| Wed, June 10 | USD | US Consumer Price Index (CPI) |

| Wed, June 10 | CAD | BoC Rate Decision |

| Thu, June 11 | EUR | ECB Rate Decision |

| Thu, June 11 | USD | US Producer Price Index (PPI) |

| Fri, June 12 | GBP | UK GDP |

| Fri, June 12 | USD | U. of Michigan Consumer Sentiment (Prelim) |

Japan Growth Downgraded to 1.8% as Capital Spending Weakens

Japan's economic expansion in Q1 was weaker than initially estimated, as a sharp downward revision to corporate investment offset improvements in consumption and trade. Revised government figures showed real GDP grew at an annualized 1.8% pace in January-March, down from the preliminary estimate of 2.1%, while quarter-on-quarter growth was revised from 0.51% to 0.45%.

The key drag came from business spending. Capital investment was revised from a 0.3% gain to a -0.7% contraction, raising questions about corporate confidence amid a broader environment of rising inflation and expectations for further Bank of Japan policy normalization. The downgrade also reduced nominal GDP growth to an annualized 2.5% from the previously reported 3.4%.

However, the overall picture was not uniformly weak. Consumer spending was revised higher to 0.35% growth from 0.27%, suggesting household demand remained supportive. Housing investment was also stronger than first reported, while exports rose 1.8%, slightly above the preliminary estimate. Together, the revisions point to an economy still expanding at a healthy pace, though one increasingly reliant on consumers and external demand rather than corporate investment.

| Indicator | Previous Estimate | Revised Estimate |

|---|---|---|

| Real GDP (Annualized) | 2.1% | 1.8% |

| Real GDP (Q/Q) | 0.51% | 0.45% |

| Capital Spending | +0.3% | -0.7% |

| Private Consumption | +0.27% | +0.35% |

| Public Investment | +1.4% | +1.5% |

| Housing Investment | +0.5% | +0.9% |

| Exports | +1.7% | +1.8% |

| Imports | +0.5% | +0.4% |

| Nominal GDP (Annualized) | +3.4% | +2.5% |

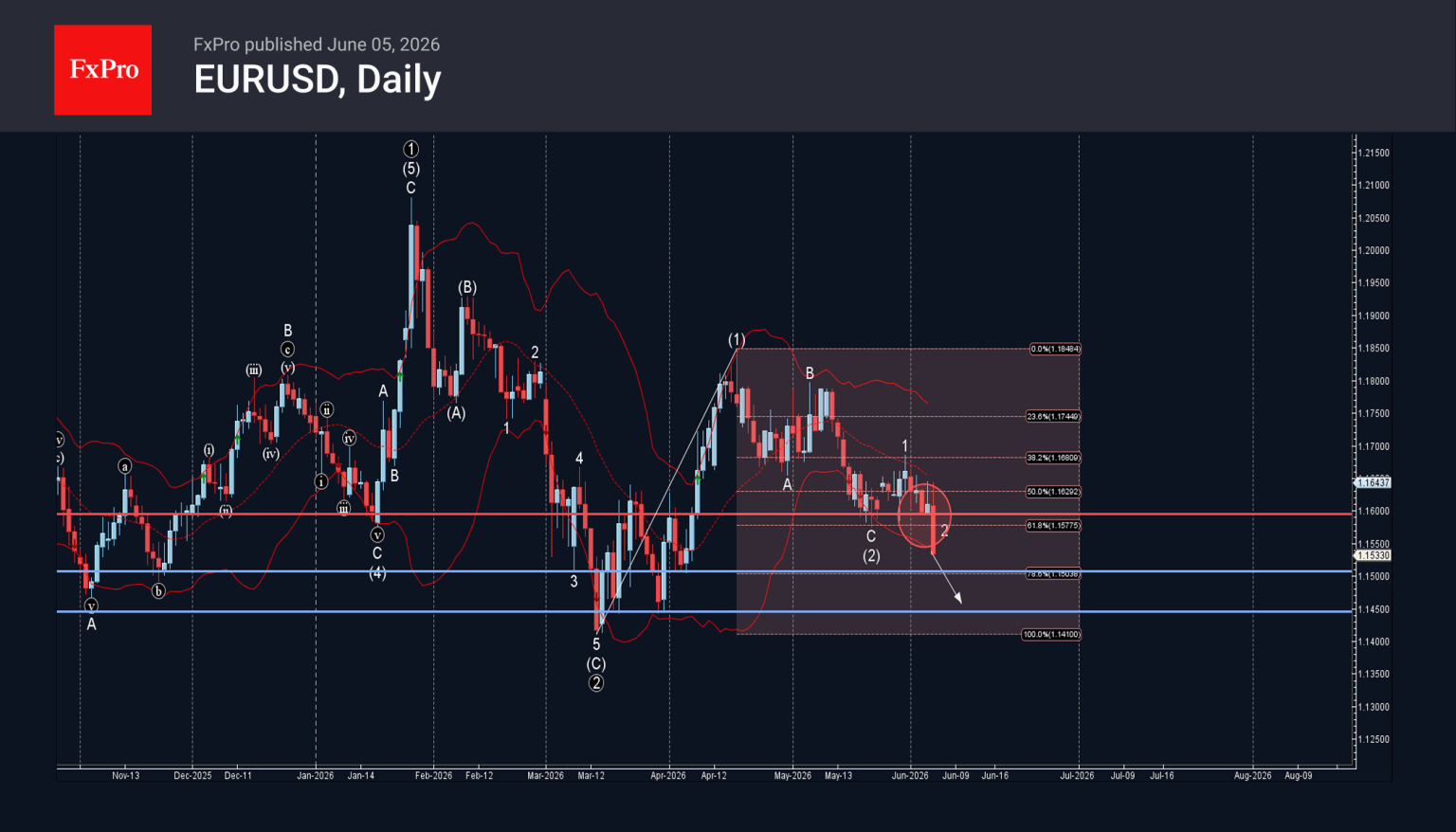

EUR/USD Stumbles Again—Is A Bigger Drop Around The Corner?

Key Highlights

- EUR/USD started a major decline below 1.1600 and 1.1580.

- It traded below a contracting triangle with support at 1.1595 on the 4-hour chart.

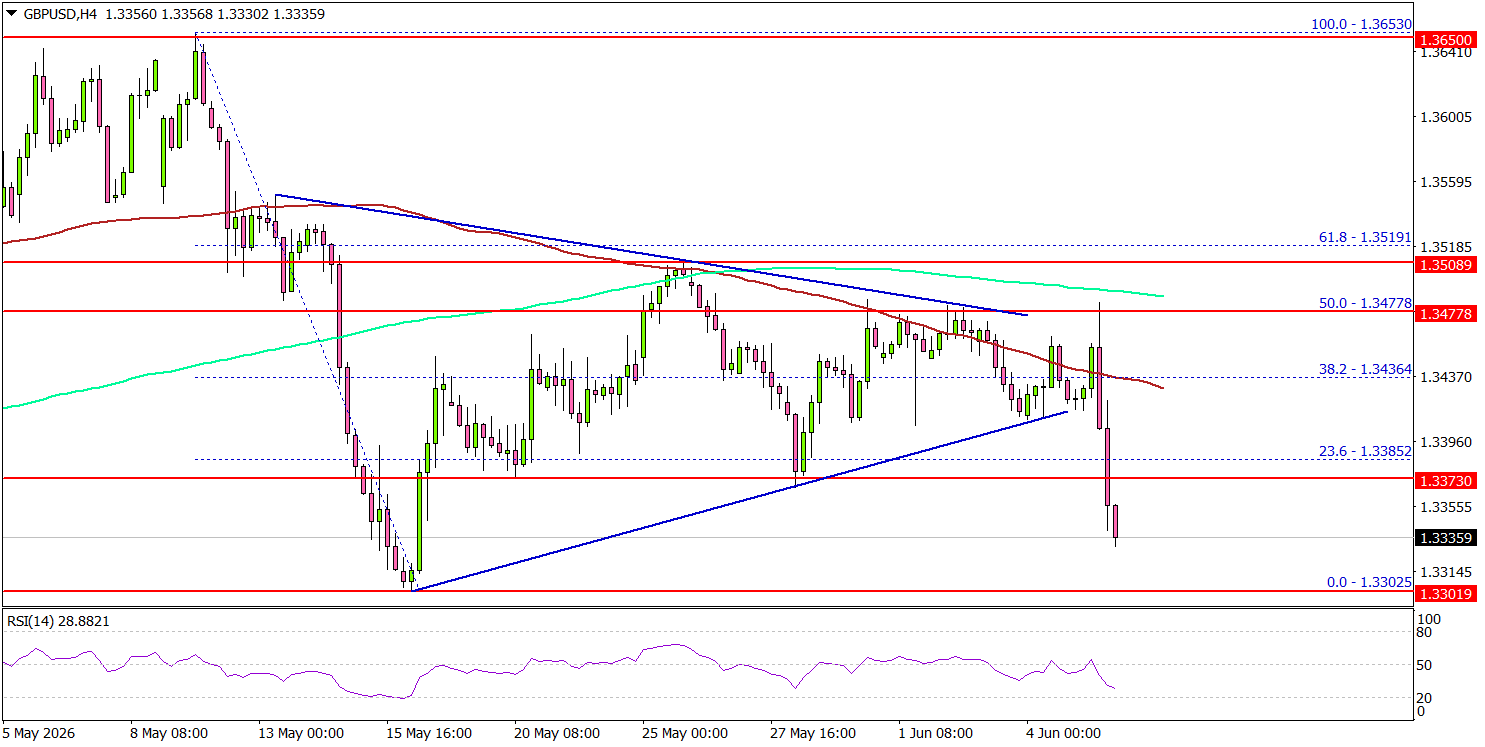

- GBP/USD is again moving lower from the 1.3500 resistance zone.

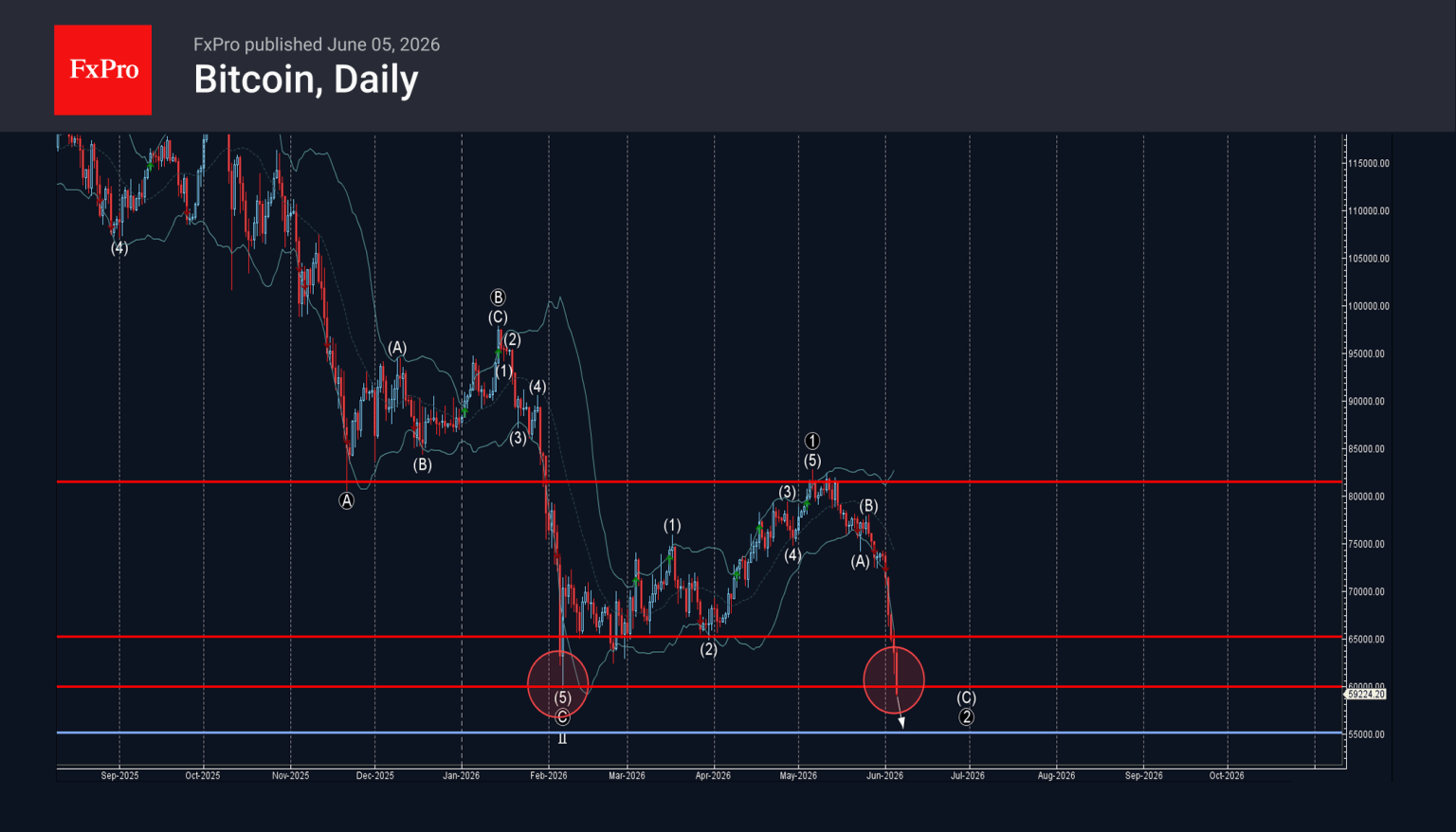

- Bitcoin extended losses and tested the $60,000 support.

EUR/USD Technical Analysis

The Euro failed to surpass 1.1650 against the US Dollar. EUR/USD started a fresh decline below 1.1620 and 1.1600 to move into a bearish zone.

Looking at the 4-hour chart, the pair traded below a contracting triangle with support at 1.1595. The pair shows bearish signs below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

Immediate support could be 1.1500. The first major support might be 1.1470. A close below 1.1470 could open the doors for a larger decline toward 1.1420. Any more losses might set the pace for a test of 1.1350.

On the upside, an immediate resistance could be 1.1550. The next major resistance might be 1.1580. A close above 1.1580 could open doors for gains. The main hurdle for the bulls could be 1.1620 and the 100 simple moving average (red, 4-hour). If there is a close above 1.1620, the pair could rise toward the 1.1650 level.

Looking at GBP/USD, the pair failed to continue higher above 1.3500, started a fresh decline, and might move below the 1.3320 support.

Upcoming Key Economic Events:

- Euro Zone Sentix Investor Confidence for June 2026 - Forecast -15.5, versus -16.4 previous.

Strong U.S. Employment Data Raises U.S. Rate Fears

For most of the week, markets continued their recent trends. Equities and the U.S. dollar moved higher, while oil traded mostly sideways as traders watched developments around Iran. Bitcoin was the most volatile market and remained under pressure as investors looked for better returns elsewhere.

Friday’s U.S. employment data was almost double expectations, and previous months were also revised higher. This strong data, together with ongoing inflation concerns, made markets focus on the possibility that the Fed may need to raise rates again. USD/JPY rose above 160 as the Bank of Japan did not intervene, and the U.S. dollar strengthened against other major currencies.

Gold came under pressure, while equities sold off sharply. The Nasdaq fell more than 4%, and the S&P 500 had its worst day of the year. Other data during the week also pointed to continued strength in the U.S. economy and ongoing inflation pressure, while Bank of Japan Governor Kazuo Ueda’s comments increased expectations of a possible June rate hike.

Markets This Week

U.S. Stocks

The Dow did not fall as much as the Nasdaq or S&P 500, but the weekly close below the 10-day moving average suggests selling pressure could continue this week. U.S. inflation data will be important for both the short-term and medium-term direction. For now, looking for selling opportunities may be the better approach as markets adjust to higher U.S. interest rate expectations. Resistance levels are at 51,500 and 52,000. Support is seen at 50,000, 49,500, 49,000, 48,500 and 48,000.

Japanese Stocks

The Nikkei 225 hit a record high during the week, but Japanese equities fell sharply on Friday night along with U.S. stocks. In the short term, the market may be oversold, and demand for Japanese equities remains strong. However, the medium-term outlook looks more sideways to lower, as the Bank of Japan appears more likely to raise interest rates, which could be negative for Japanese stocks. Resistance is seen at 67,000, 68,000, 69,000 and 70,000, while support is at 64,000, 62,000, 61,000, 60,000 and 59,000.

USD/JPY

The lack of intervention from the Bank of Japan allowed USD/JPY to slowly move higher and test the 160 level for most of the week. Strong U.S. employment data increased expectations for higher U.S. interest rates, helping the pair close above 160. The Bank of Japan may also raise interest rates this month, which could put pressure on USD/JPY, but for now the uptrend remains in place within a narrow range. Short-term trading is still difficult, as the pair could continue higher, but there is also a risk of a quick drop if Japan intervenes. Resistance is at 160.50, 162.00 and 165.00, while support is seen at 159.00, 158.00, 157.00, 156.00, 155.50 and 155.00.

Gold

Renewed talk of higher U.S. interest rates, along with continued U.S.-Iran negotiations, kept gold under pressure throughout the week. Strong U.S. employment data was also negative for gold, pushing prices to close near the lows. It was a disappointing week as the fundamental outlook weakened, although central bank demand may still support prices on larger falls. For this week, waiting for a rebound before looking for selling opportunities may be the better strategy. Resistance is at $4,500, $4,600, $4,665, $4,750 and $4,900, while support is at $4,300, $4,200, and $4,100.

Crude Oil

WTI crude oil traded sideways as hopes for a quick return of Middle East oil supply faded, pushing prices higher early in the week toward $100. However, resistance held, and the stronger U.S. dollar later pushed WTI back close to its weekly opening levels. With the 10-day moving average still bearish and Friday’s close looking weak, focusing on selling opportunities may be the better short-term strategy. Resistance is at $95, $100, $105, $110 and $120, while support is at $90, $80, $75, $70, and $67.50.

Bitcoin

Bitcoin suffered a very large weekly loss and hit new lows for 2026 as ETF outflows and institutional selling added pressure. Bitcoin has disappointed investors this year, with some moving money into AI and technology stocks instead. In the short term, support near the yearly lows is still holding, so there may be a short-term buying opportunity with a small stop loss. However, the medium-term outlook remains negative, so waiting for a rebound closer to the 10-day moving average may be the better strategy. Resistance is at $65,000, $75,000, $80,000, $85,000, and $90,000, while support is at $60,000, $55,000 and $50,000.

This Week’s Focus

- Monday: Australia GDP and Current Account

- Tuesday: U.S. Trade Balance and Existing Home Sales

- Wednesday: Australia Building Approvals, China CPI and PPI, U.S. CPI

- Thursday: E.U. ECB Interest Rate Decision, U.S. PPI

- Friday: Japan Industrial Production, U.K. Trade Balance and Industrial Production, U.S. Michigan Consumer Expectations

After the large market moves caused by the strong U.S. employment data, volatility may stay high as traders adjust to the growing possibility that the Fed may need to raise interest rates again. U.S. CPI and PPI inflation data will be the main focus this week, along with the ECB interest rate decision. Equities have performed strongly this year, so stronger-than-expected inflation data could increase the risk of further falls.

Bitcoin Wave Analysis

Bitcoin: ⬇️ Sell

- Bitcoin broke support level 60000.00

- Likely to fall to support level 55000.00

Bitcoin cryptocurrency recently broke the support level 60000.00 (which stopped the previous sharp downward impulse wave (5) at the star of February).

The breakout of the support level 60000.00 follows the earlier breakout of the support level 65000.00 (low of the previous correction (2)).

Given the overriding daily downtrend, Bitcoin cryptocurrency can be expected to fall to the next support level 55000.00 – target for the completion of the active impulse wave (C).

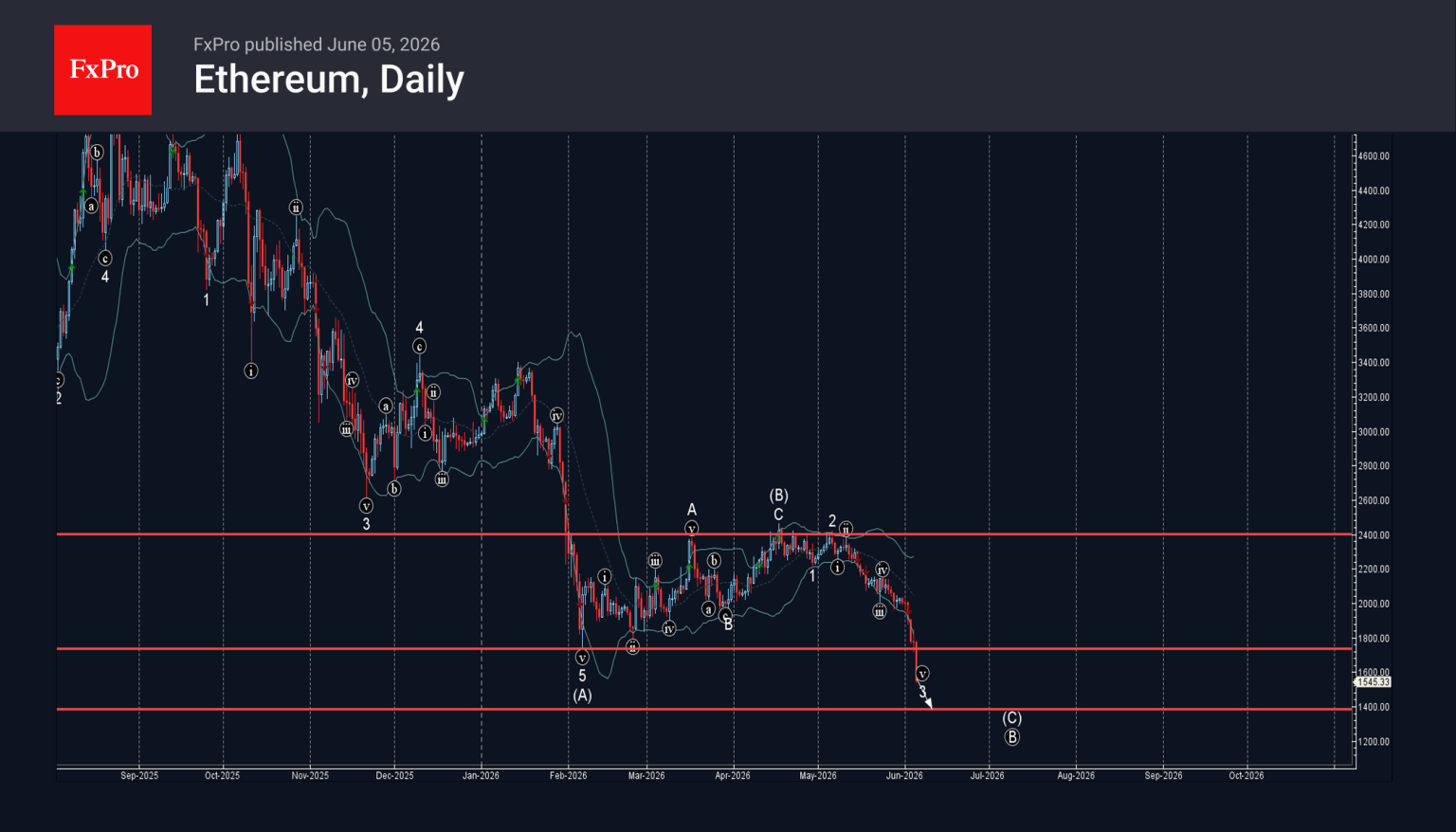

Ethereum Wave Analysis

Ethereum : ⬇️ Sell

- Ethereum broke strong support level 1735.00

- Likely to fall to support level 1400.00

Ethereum cryptocurrency recently broke below the strong support level 1735.00 (which stopped earlier sharp downward impulse wave (A) at the start of February).

The breakout of the support level 1735.00 – if the price closes this week below this level- should greatly accelerate the active impulse waves 3 and (C).

Given the strongly bearish sentiment seen across the crypto markets today, Ethereum cryptocurrency can be expected to fall to the next support level 1400.00.

EURUSD Wave Analysis

EURUSD: ⬇️ Sell

- EURUSD broke support zone

- Likely to fall to support levels 1.1500 and 1.1450

EURUSD currency pair recently broke the support zone between the support level 1.1600 (which stopped earlier correction (2)) and the 61.8% Fibonacci correction of the upward impulse (1) from March.

The breakout of this support zone accelerated the active impulse waves 3 and (3).

Given the strongly bullish US dollar sentiment seen today, EURUSD currency pair can be expected to fall to the next support levels 1.1500 and 1.1450.