Sample Category Title

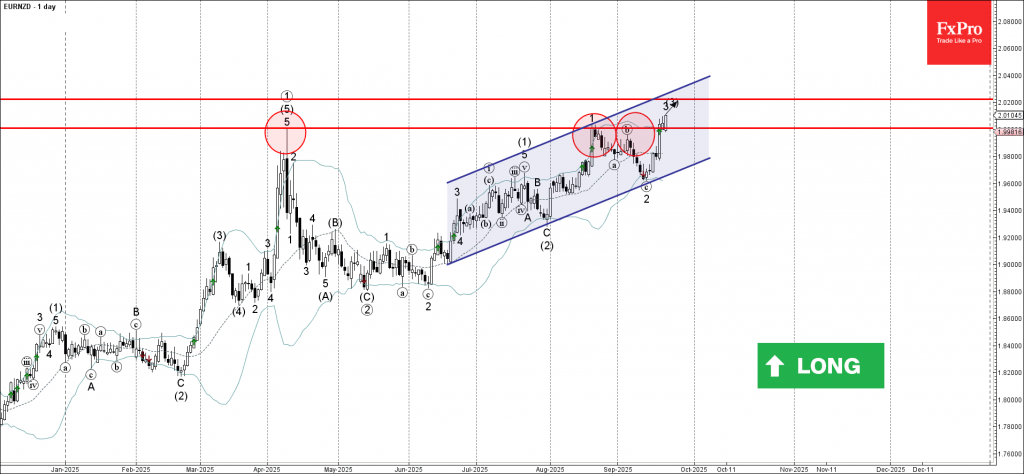

EURNZD Wave Analysis

EURNZD: ⬆️ Buy

- EURNZD broke key resistance level 2.0010

- Likely to rise to resistance level 2.0200

EURNZD currency pair recently broke above the key resistance level 2.0010 (which has been reversing the price from the start of April).

The breakout of the resistance level 2.0010 continues the active impulse waves 3 and (3) – which belong to the long-term upward impulse sequence 3 from May.

Given the clear daily uptrend, EURNZD currency pair can be expected to rise to the next resistance level 2.0200 (target price for the completion of the active impulse wave 3).

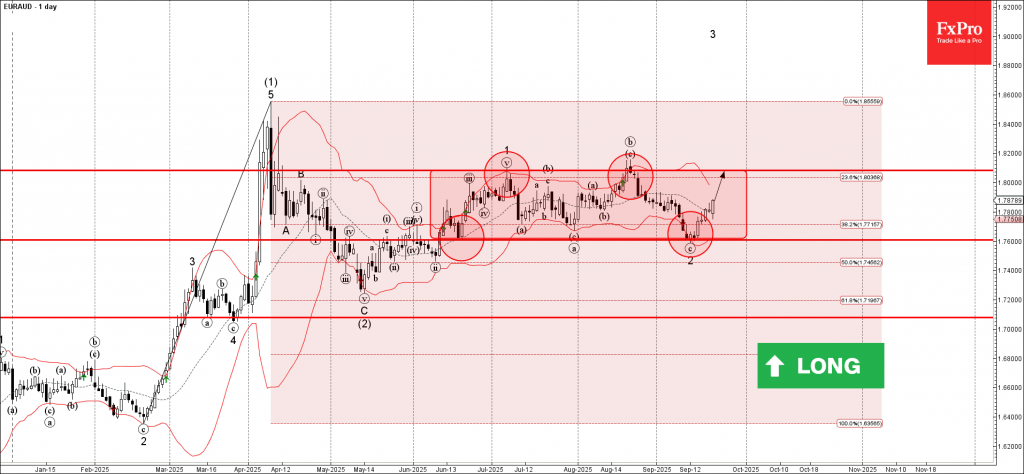

EURAUD Wave Analysis

EURAUD: ⬆️ Buy

- EURAUD reversed from support zone

- Likely to rise to resistance level 1.8085

EURAUD currency pair recently reversed up from the support zone between the support level 1.7600 (lower border of the sideways price range from June) and the lower daily Bollinger Band.

The support level 1.7600 was further strengthened by the 38.2% Fibonacci correction of the sharp upward impulse from February.

Given the bullish euro sentiment seen today, EURAUD currency pair can be expected to rise to the next resistance level 1.8085 (upper border of the active sideways price range).

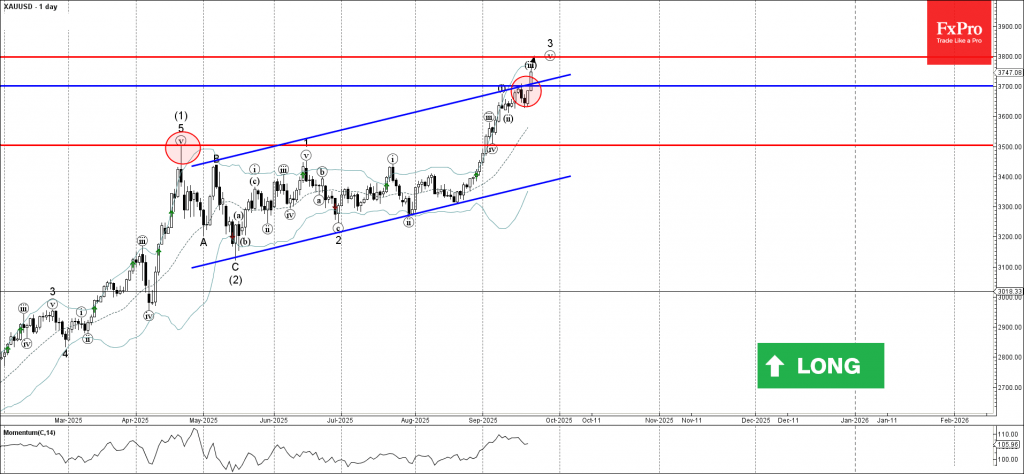

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold broke resistance zone

- Likely to rise to resistance level 3800.00

Gold recently broke the resistance zone between the resistance level 3700.00 and the resistance trendline of the daily up channel from April.

The breakout of this resistance zone accelerated the active impulse wave v of the impulse wave 3 from the end of June.

Given the strong daily uptrend, Gold can be expected to rise to the next resistance level 3800.00 (target price for the completion of the active impulse wave 3).

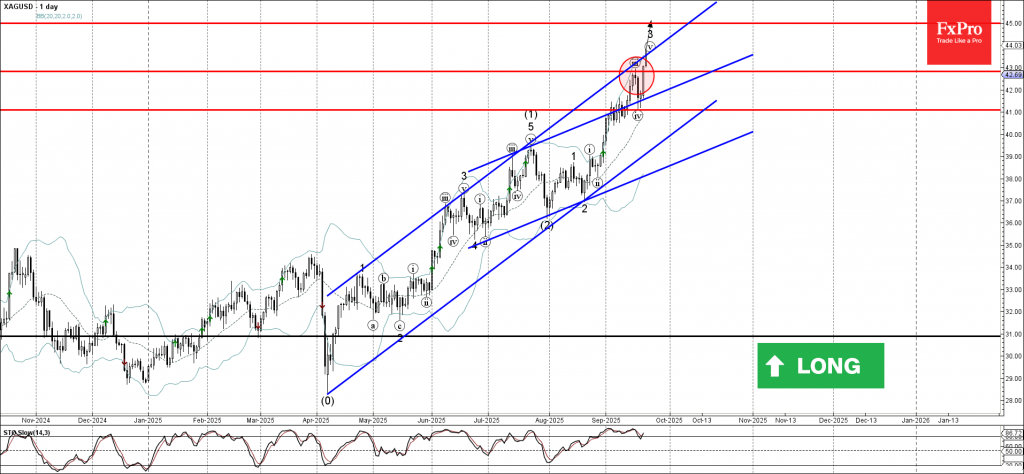

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver reversed from support zone

- Likely to rise to resistance level 45.00

Silver recently reversed from the support zone between the support level 41.00 and the upper trendline of the recently broken up channel from June (acting as the support after it was broken at the start of September).

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Morning Star – which started the active impulse wave v.

Given the clear daily uptrend, Silver can be expected to rise to the next resistance level 45.00 (target price for the completion of the active impulse wave v).

Fed’s Musalem: Rate cut was precautionary, scope for easing limited

St. Louis Fed President Alberto Musalem said he supported last week’s 25bps rate cut as a "precautionary move" to protect the labor market from further weakening. He emphasized in a speech, however, that there is only “limited room for easing further” before monetary policy risks becoming “overly accommodative.”

He stressed that while the Fed can provide insurance against labor market softness, it must also “lean against persistence in above-target inflation.”

Musalem added that he will continue to update his economic outlook in the months ahead to strike the right balance between employment and inflation.

Sunset Market Commentary

Markets

Markets take a very calm start of the week. Sentiment is slightly risk off, resulting in some modest losses on equity markets. Core bond yields trade little changed between -2 bps and +2 bps, with some minor outperformance by German bunds vs USTs. Italian BTP’s show no particular outperformance following Fitch’s rating upgrade last Friday, meaning the move was already priced in before. That’s obvious from the strong BTP bull run since April of this year. Italian credit risk premia as a result is now considerably closer to and even below some semi-core peers. Italy’s upgrade, along with Spain’s and Portugal’s a few weeks earlier, in a broader perspective highlights the tidal shift going on between the now-former underperforming periphery and the northern part of the euro area. France serves as a prime example, carrying a higher premium than Italy since last week. But Belgium is showing similar French traits with its credit risk premium having topped Portugal’s in September of last year and closing in on Spain’s (the difference is a mere 1.5 bps). Swapspreads of countries such as the Netherlands and Germany have been flatlining in 2025 but saw a material rise from the depths in 2022. UK gilts strengthen a tad after facing some budget deficit-driven selling pressure by the end of last week, especially at the very long end of the curve. In terms of market themes, the looming potential US government shutdown is gaining some attention. The current US fiscal year ends September 30 and Congress must pass annual spending bills to keep the government running in the next. But Capitol Hill is currently deadlocked with the Republican plan which foresaw to keep the government funded through Nov 21 (and which passed the House) failing in the Senate. A Democratic alternative was later rejected as well. The US dollar loses some ground in FX markets, awaiting some potential market moving comments from Fed policymakers including Williams & Marin on monetary policy. EUR/USD bounces off the short-term upward sloping trendline to turn to but remain below the 1.18 big figure. DXY never came to an actual test of the 98 lever and is currently slightly down on the day at around 97.4. USD/JPY is going nowhere within this summer’s narrow sideways trading range of roughly 146-150. UK’s pound steadies against the euro around EUR/GBP 0.872 but ekes out a gain against an overall weaker dollar. Cable (GBP/USD) tops 1.35 again.

News & Views

Confidence indicators published today by the National Bank of Belgium show that consumer confidence in the country continued to rise in September. At -1 (from -2 in August) the overall indicator improved to the best level this year. Still, consumers’ fears about a rise in unemployment increased slightly (2 from 1). On the positive side, household expectations for the for the general economic situation rose solidly from -26 to -23. On a personal level, households have slightly upgraded their expectations regarding their own financial situation (0 from -1). At the same time, they intend to save more (22 from 21).

Statistics Poland reported that retail sales (constant prices) were by 3.1% higher in August than the year before (was +4.8% Y/Y in July). Compared with July 2025, sales were reported 0.4% lower, coming after a monthly gain of 4.4%. In the period of January-August 2025 sales increased y/y by 3.6%. Overall, the data were close to expectations. Details showed that sales were higher Y/Y in most groups of enterprise activity. High increases (Y/Y) were reported for “textiles, clothing, footwear” (by 18.9%), “furniture, radio, TV and household appliances” (by 13.9%). Sales also rose in the groups “motor vehicles, motorcycles, parts” (by 9.4%), “fuels” (by 6,1%), and “pharmaceuticals, cosmetics, orthopedic equipment” (by 3.3%). However, sales in “food, beverages and tobacco products” declined 3.4%. The value of retail sales via internet (current prices) rose 4.9% Y/Y. Today’s data probably won’t change the assessment of the National Bank of Poland on monetary policy. The NBP cut the policy rate by 25 bps 4.75% early this month. At 2.9% Y/Y, inflation in August was again in the NBP target range (2.5% +/- 1%pt), but governors recently remained cautious on (the pace of) further easing due to ongoing high wage growth and a supportive fiscal policy, amongst others. Recent NBP comments suggested that there might still be room for one additional 25 bps rate cut by the end of the year. EUR/PLN (4.255 area) holds a tight sideways consolidation pattern. In this respect, the zloty recently underperformed the forint and the Czech koruna.

Gold Bulls Notch Another Record High

- Gold at fresh all-time high; aims for another move higher.

- Short-term risk positive, but overbought conditions threaten five-week rally.

Gold started the week on positive note, edging softly up to unlock a new record high of 3,719 thanks to Friday’s quick rebound near the 3,630 support area.

The Fed has opened the door to two more 25bps rate cuts by the end of the year. However, this scenario is not fully priced in and the central bank’s communication could provide some direction this week along with the core PCE inflation figures, as policymakers are scheduled to take to the podium. Coupled with elevated geopolitical tensions over the war in Ukraine and falling Treasury yields, gold may have scope to achieve new milestones.

The area around 3,727 could act as immediate resistance as the RSI and the Stochastic oscillator are sloping upwards but are still close to overbought territory, warning that the five-week bullish streak may have limited upside in the short term. Should the price find new buyers, the 3,800 and 3,900 psychological marks could next come on the radar ahead of the all-important 4,000 level.

On the downside, the 3,600-3,630 zone may keep buffering downside pressures. If not, the 20-day simple moving average (SMA) could come to the rescue at 3,590 for the first time in a month. Failure to pivot there could expose the 3,500 region.

Summing up, gold is setting the tone for another push higher. A sustained break above 3,730 could generate fresh buying interest.

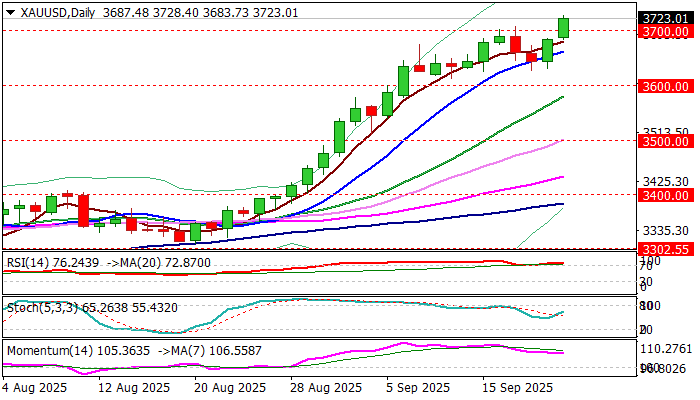

XAU/USD: Gold at New Record Highs Above $3,700

Acceleration through key $3700 resistance zone pushed gold price to new record high on Monday (price was up 1.1% since opening).

Shallow pullback from previous peak did not harm larger bulls and was just positioning for fresh push higher, as it reversed well above $3600 lower breakpoint.

Revived optimism of more Fed rate cuts (despite less dovish than expected post-FOMC comments from chief Powell) brightened the sentiment, along with complicating geopolitical situation after a few countries recognized the State of Palestine, that resulted in fresh rise in safe haven demand.

In addition, sustained physical buying by central banks continues to underpin yellow metal’s price.

Daily studies remain firmly bullish and supportive for further advance, with immediate targets at $3734 and $3750, guarding $3789/$3800 zone.

Daily close above $3700 is needed to validate positive signal, generated on completion of bullish continuation pattern on daily chart.

Meanwhile, bulls may face headwinds from overbought conditions on hourly and 4-hr charts, with limited dips expected to find firm ground at $3700 zone (reverted to solid support).

Res: 3734; 3750; 3789; 3800.

Sup: 3707; 3700; 3663; 3627.

USDCHF Elliott Wave Analysis Shows Fresh Sell-Off From Bluebox

Hello traders. Welcome to a new blog post where we discuss recent trade setups from the blue box to the Elliottwave-forecast members. In this one, the spotlight will be on the USDCHF currency pair.

The USDCHF currency pair remains clearly bearish. This trend is driven by dollar weakness since September 2022 and more recently January 2025. When analyzing this pair, we focus heavily on the dollar. The dollar has been in a bearish cycle since September 2022. It follows a clear A-B-C corrective structure. Wave C of this 3-swing pullback began in January 2025.

Since it is a simple zigzag, wave C has unfolded as an impulse. However, the September 2022 cycle has not yet reached its target zone. Moreover, all bounces so far have been corrective. Therefore, we continue to favor a “sell the bounce” strategy. This approach has delivered strong profits across dollar pairs, including USDCHF.

For USDCHF specifically, the bearish cycles began in October 2022 and January 2025. Since January, we have sold bounces at the extremes of 3, 7, or 11 swings. We highlight these extreme zones with blue boxes on our charts. For example, there was a clean 7-swing corrective bounce from July 1, 2025. When that bounce matured, we marked the blue box zone for selling. This setup was shared with members on August 9, 2025. From the August blue box, USDCHF fell over 330 pips. We wrote about it; read here. It even broke below the July low where the bounce started. As a result, we prepared for another corrective bounce to sell from.

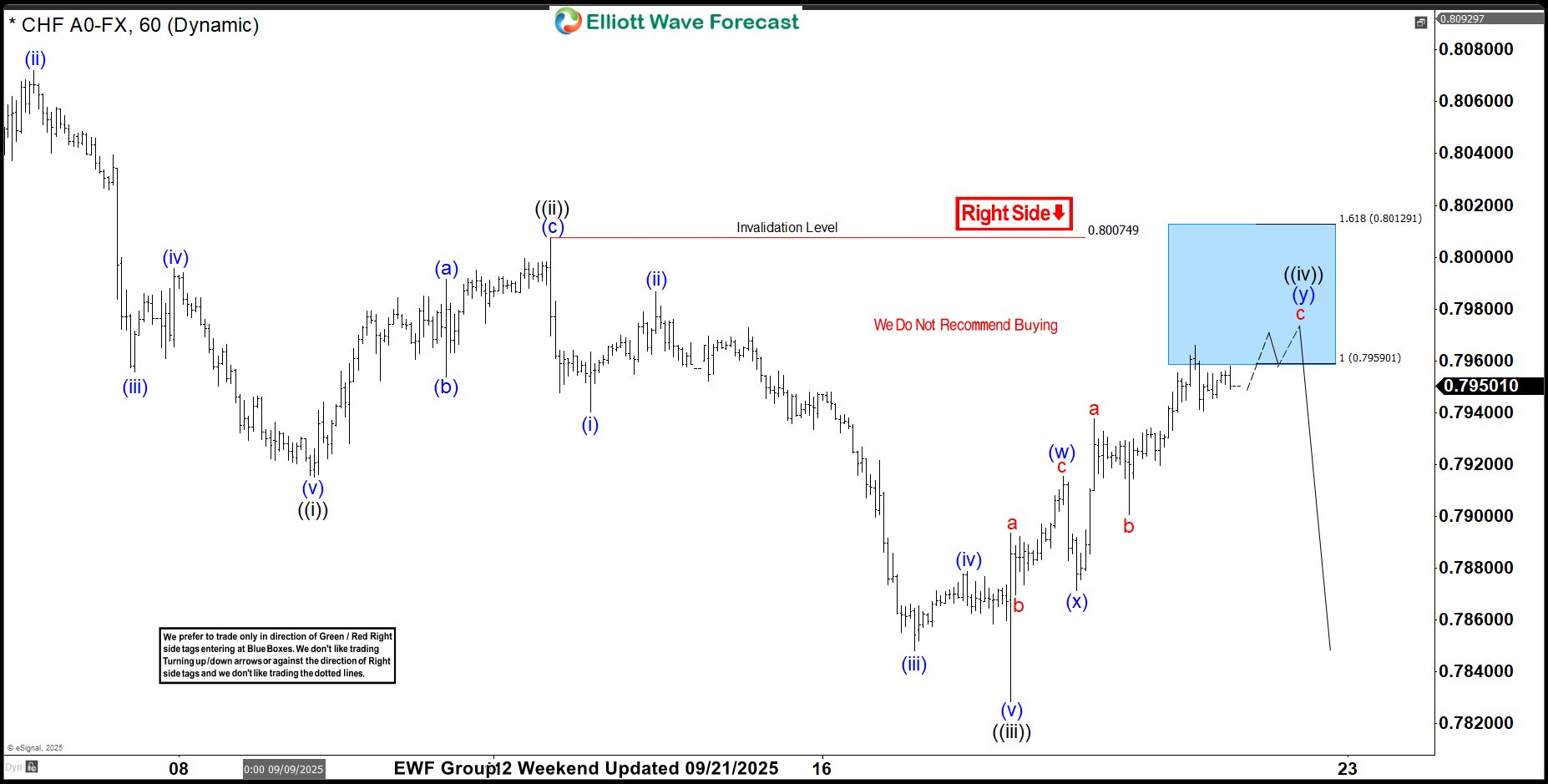

USDCHF Elliott Wave Setup: 9.21.2025 Update

Shortly after the 17th September FOMC, the pair breached the July 1st low and then turned upside to correct August cycle. Thus, we prepared to sell from the blue box. We shared the H1 chart below with members on the 21st September 2025.

The chart above highlighted the 0.7959-0.8012 blue box zone for short opportunities. From the blue box, we expected wave ((v)) to start and continue lower to break the current September low. Alternatively, if not an impulse, then at least a 3-swing dip to happen. A 3-swing dip will put sellers in risk-free position. The chart shows price already triggered the blue box. Thus members are in an open short position.

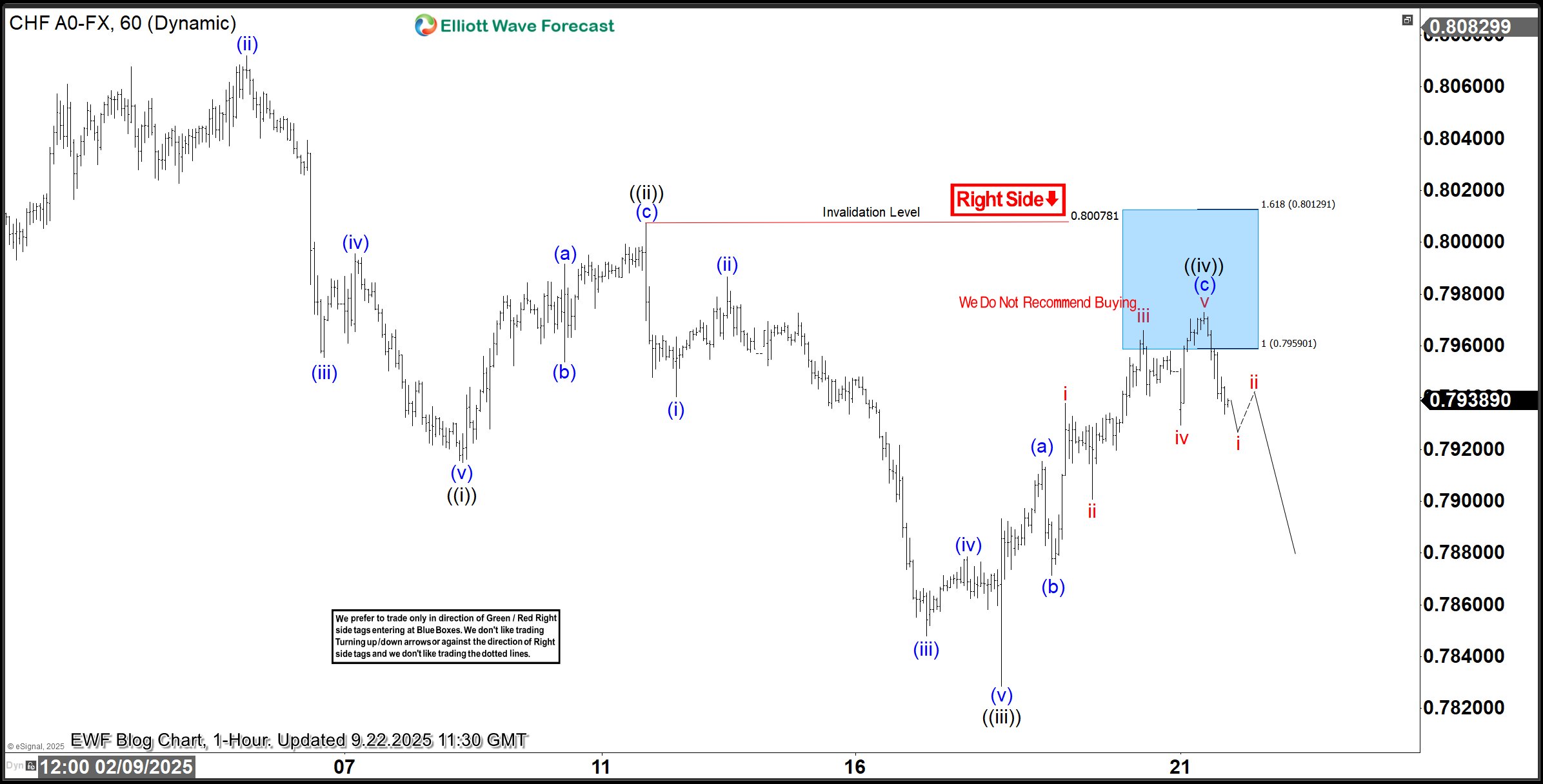

USDCHF Elliott Wave Setup: 9.22.2025 Update

The chart above shows the H1 price action leaving the blue box after it triggered it. Price separation is ongoing and we expect it to extend to at least the 50% of wave (c) of ((iv)), where they can take the first profit and run a risk-free trade. This is another typical example of our blue box entry system we use for all the 78 market we cover across all the time frames.