Sample Category Title

USD/JPY Technical: USD Strength Capped (Again) Below 148.95 Range Resistance, BoJ Keeps Rate Hike Hopes Alive

The USD/JPY dropped further on Wednesday, 17 September 2025, with an initial intraday loss of -0.7% to print an intraday low of 145.48 before it reversed up higher ex-post FOMC to close higher and erased all its initial losses, reinforced by Fed Chair Powell’s “less dovish” press conference.

The USD/JPY has managed to survive at the 145.95 medium-term support (the lower boundary of the “Ascending Wedge” range configuration) in place since the 22 April 2025 low of 139.89 and rallied by 1.9% in the past two days, from the 17 September 2025 low of 145.48 to the 18 September 2025 high of 148.27.

The 18 September 2025 high of 148.27 of the USD/JPY is just below a key minor range resistance of 148.75/148.95 that keeps the US dollar bulls in check since 12 August 2025.

US dollar’s intraday bearish reversal against the JPY, 2 BoJ officials favoured a rate hike

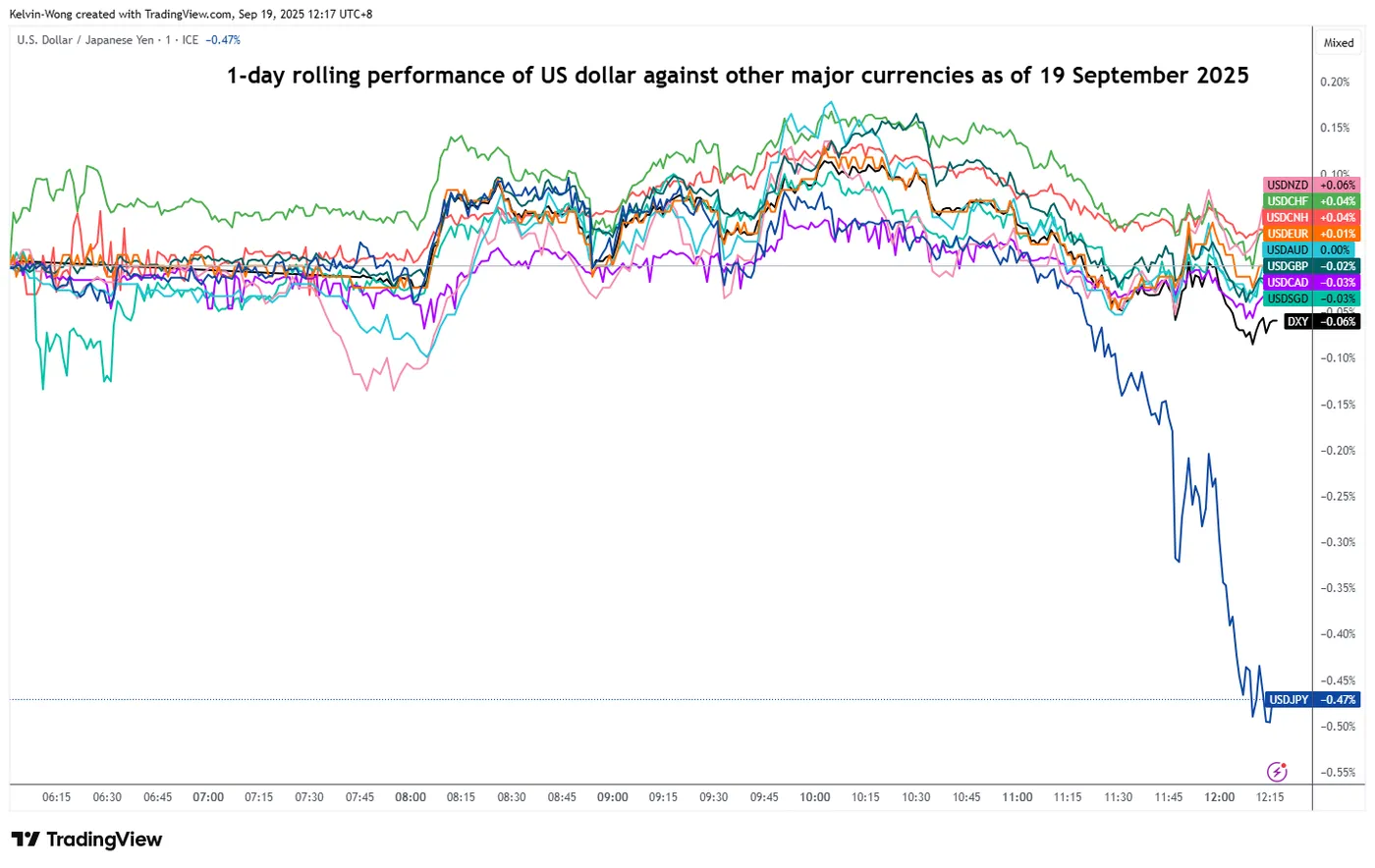

Fig. 1: 1-day rolling performances of the US dollar against major currencies as of 19 Sep 2025 (Source: TradingView)

Interestingly, the USD/JPY shed by -0.5% after the Bank of Japan (BoJ)’s monetary policy decision to keep its short-term policy interest rate unchanged at 0.5% as expected for the fifth consecutive meeting (see Fig. 1).

The main trigger of the US dollar's weakness against the Japanese yen was the BoJ officials’ voting patterns. In today’s BoJ’s monetary policy decision meeting, for the first time in 2025, two officials (Takata and Tamura) voted for an interest rate hike to 0.75%, citing that price stability (2% long-term inflation trend target in Japan) had been achieved, and the risks to prices becoming more skewed to the upside.

Let’s now examine fundamental factors.

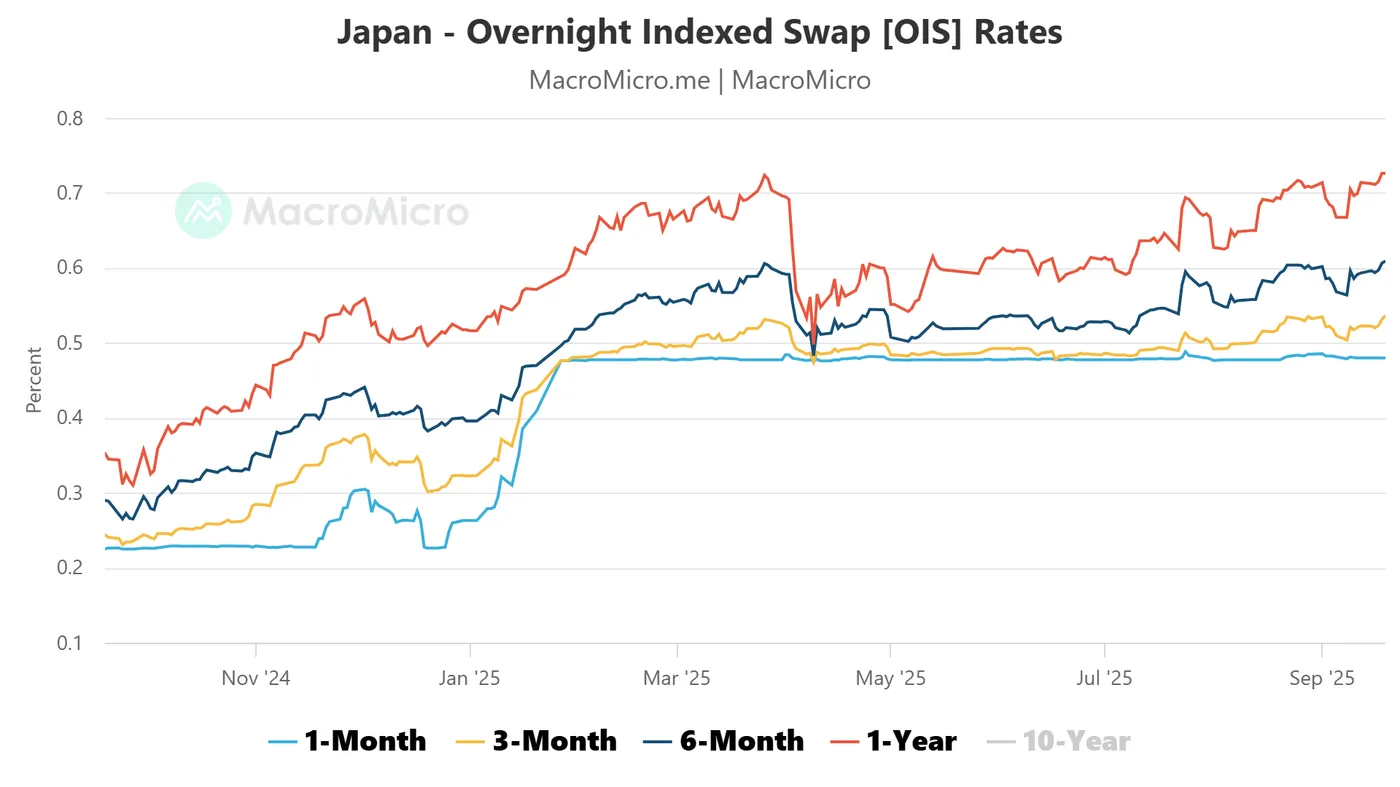

Fig. 2: Japan overnight interest rate swaps as of 19 Sep 2025 (Source: MacroMicro)

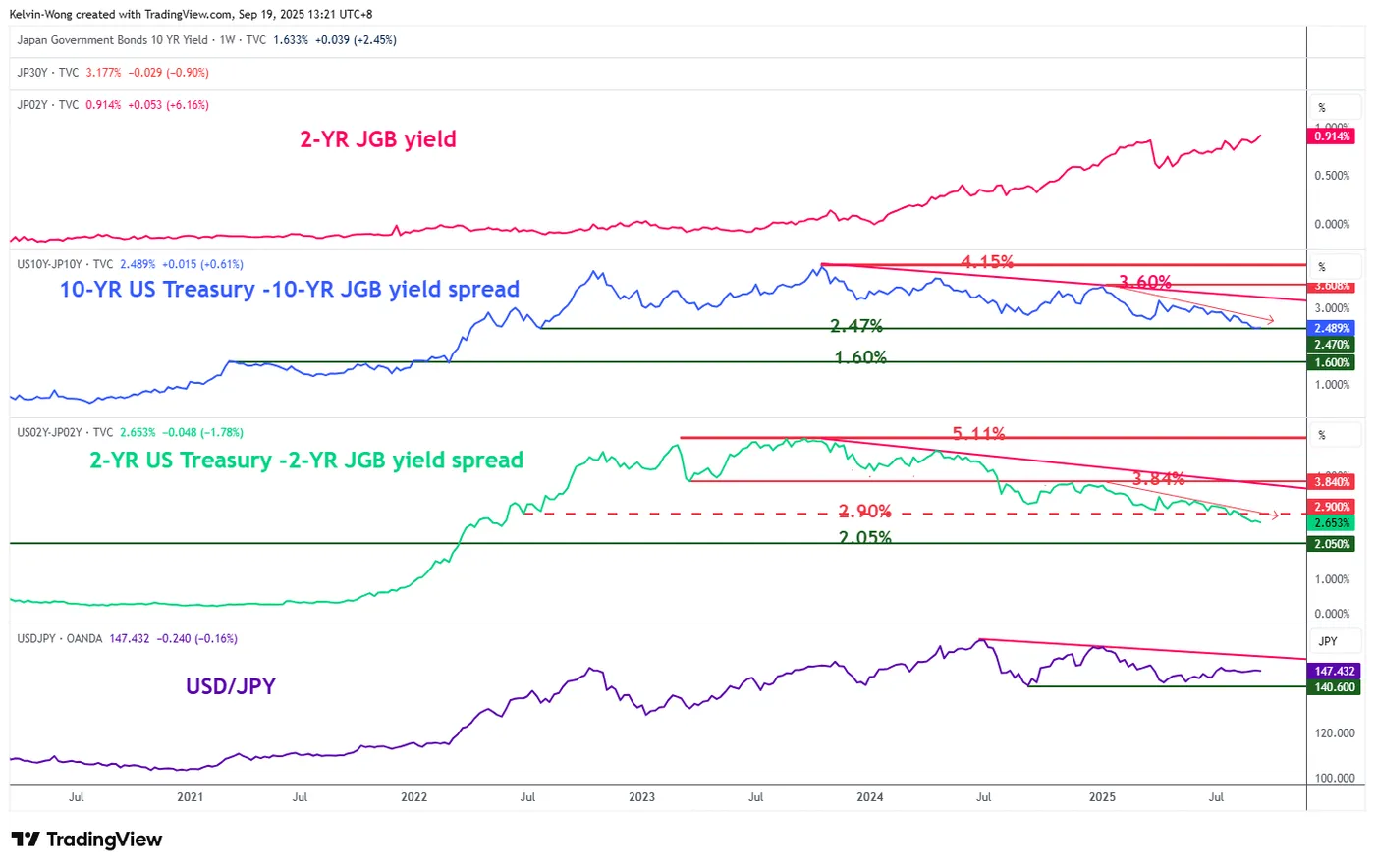

Fig. 3: Yield spreads of US Treasury/JGB with major trend of USD/JPY as of 19 Sep 2025 (Source: TradingView)

The overnight index swaps (OIS) market for Japan’s short-term interest rates is still pricing in a 25 basis points (bps) hike to the short-term overnight policy interest rate to 0.75% before 2025 ends.

The 3-month, 6-month, and 1-year OIS rates have continued to widen over the 1-month OIS rates in the past two weeks, where the 1-year OIS rate has increased from 0.67% on 8 September 2025 to 0.73% on Friday, 19 September 2025 at the time of writing (see Fig. 2).

The 2-year Japanese Government Bond (JGB) yield, which is sensitive to changes to the BoJ’s monetary policy stance, has continued its upward trajectory and climbed by to 0.91%, its highest level since 2008.

Hence, the yield premium between the 2-year US Treasury note and the 2-year Japanese Government Bond has continued to narrow steadily since the start of the year. The bearish breakdown of the 2.90% former major support on the week of 18 August 2025 is likely to add impetus for a further potential narrowing of the yield premium towards the next support at 2.05% (see Fig. 3).

This ongoing narrowing process suggests that 2-year US Treasuries have become relatively less attractive versus 2-year JGBs, reducing the yield premium in favour of the dollar. As a result, this dynamic may exert downside pressure on USD/JPY.

Let’s now examine the USD/JPY from a technical analysis perspective to determine its latest short-term (1 to 3 days) trend bias and key technical levels to watch.

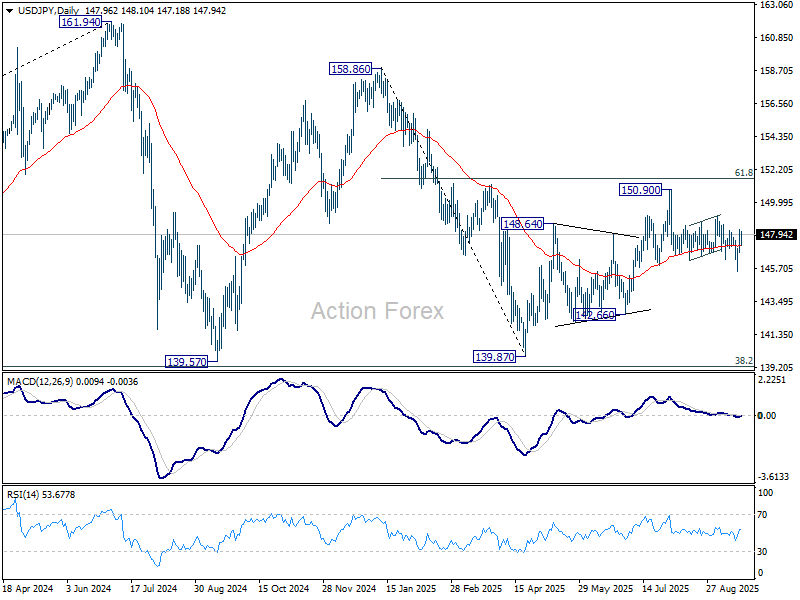

Fig. 4: USD/JPY medium-term trend as of 19 Sep 2025 (Source: TradingView)

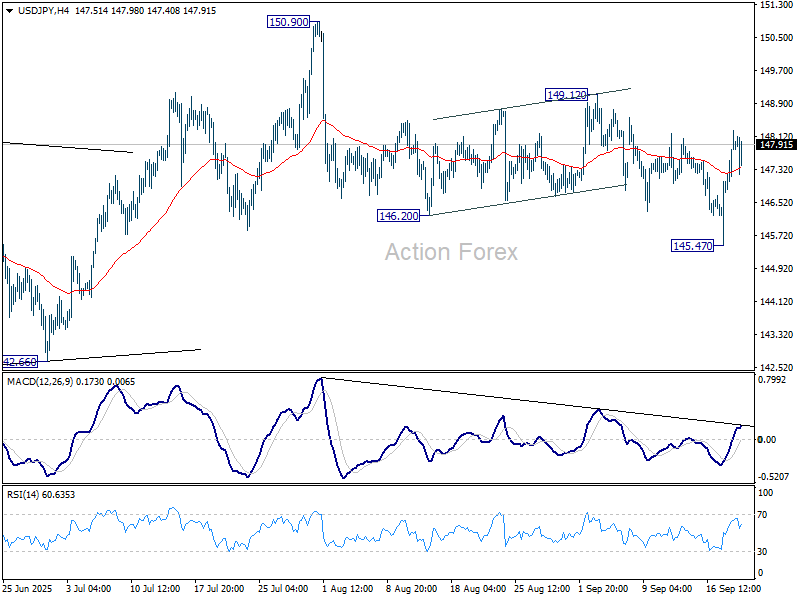

Fig. 5: USD/JPY minor trend as of 19 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

Bearish bias below 148.75/148.95 short-term pivotal resistance for USD/JPY within its range configuration for the next intermediate support to come in at 146.30, followed by the medium-term “Ascending Wedge” range support at 145.95 (see Fig. 5)

Only a break with a daily close below 145.95 on the USD/JPY is likely to trigger the start of a medium-term (multi-week) Japanese yen strength against the greenback.

Key elements

- The daily RSI momentum indicator of the USD/JPY has continued to hover below its resistance at the 60 level and printed a “lower high”. These observations suggest the lack of medium-term bullish momentum (see Fig. 4).

- The 148.75/148.95 short-term pivotal resistance of the USD/JPY has also coincided with the key 200-day moving average that has capped dollar bulls' strength since 1 August 2025 (see Fig. 4).

- The hourly RSI momentum indicator has exited from its overbought level after it flashed out a bearish divergence condition (see Fig. 5).

Alternative trend bias (1 to 3 days)

A clearance above 148.95 invalidates the bearish scenario for the USD/JPY and sees a squeeze up towards the key medium-term resistance of 149.70/149.90 (the upper boundary of the “Ascending Wedge”).

Fed’s Dovish Stance Buoyed Stock Market

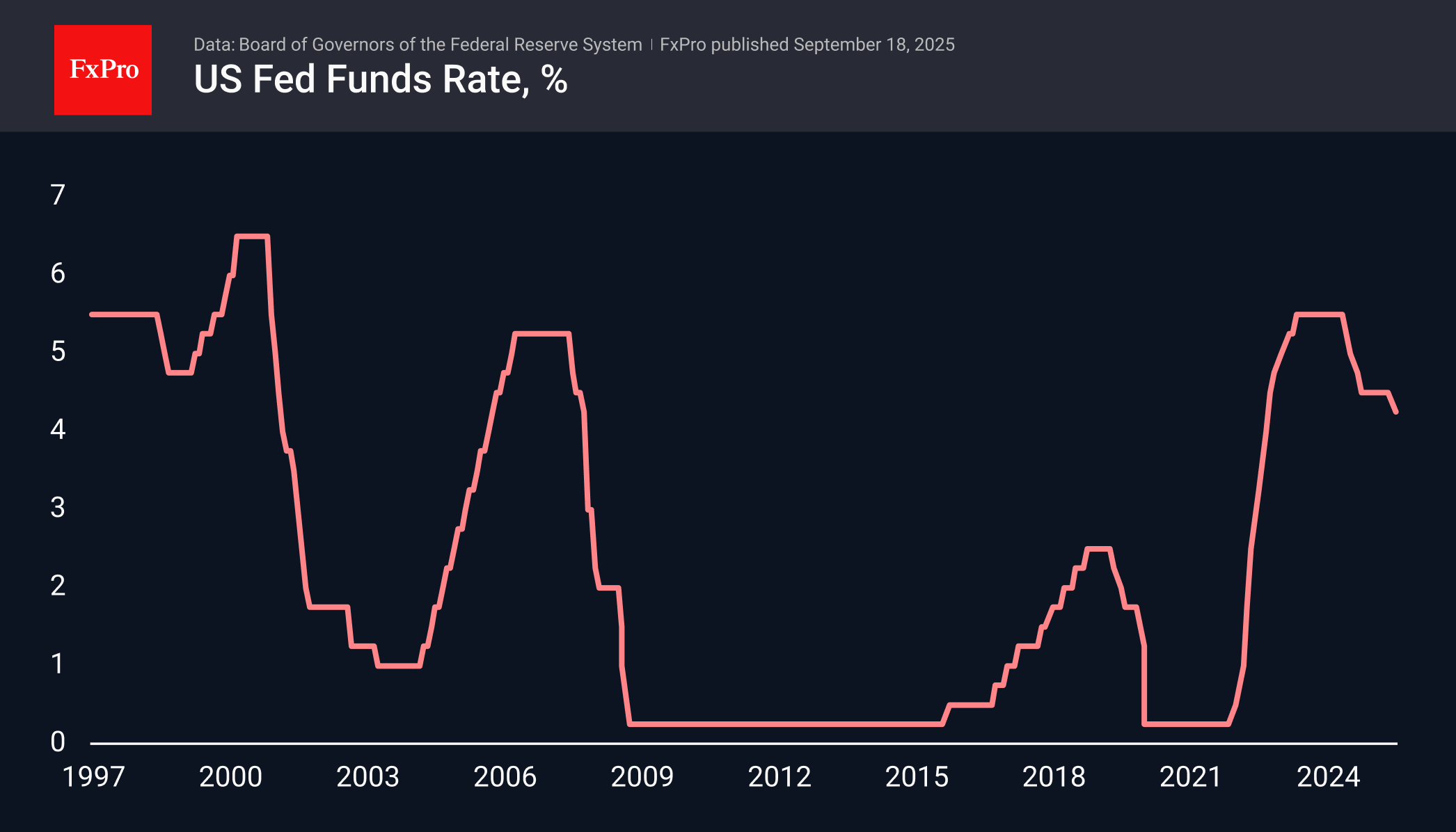

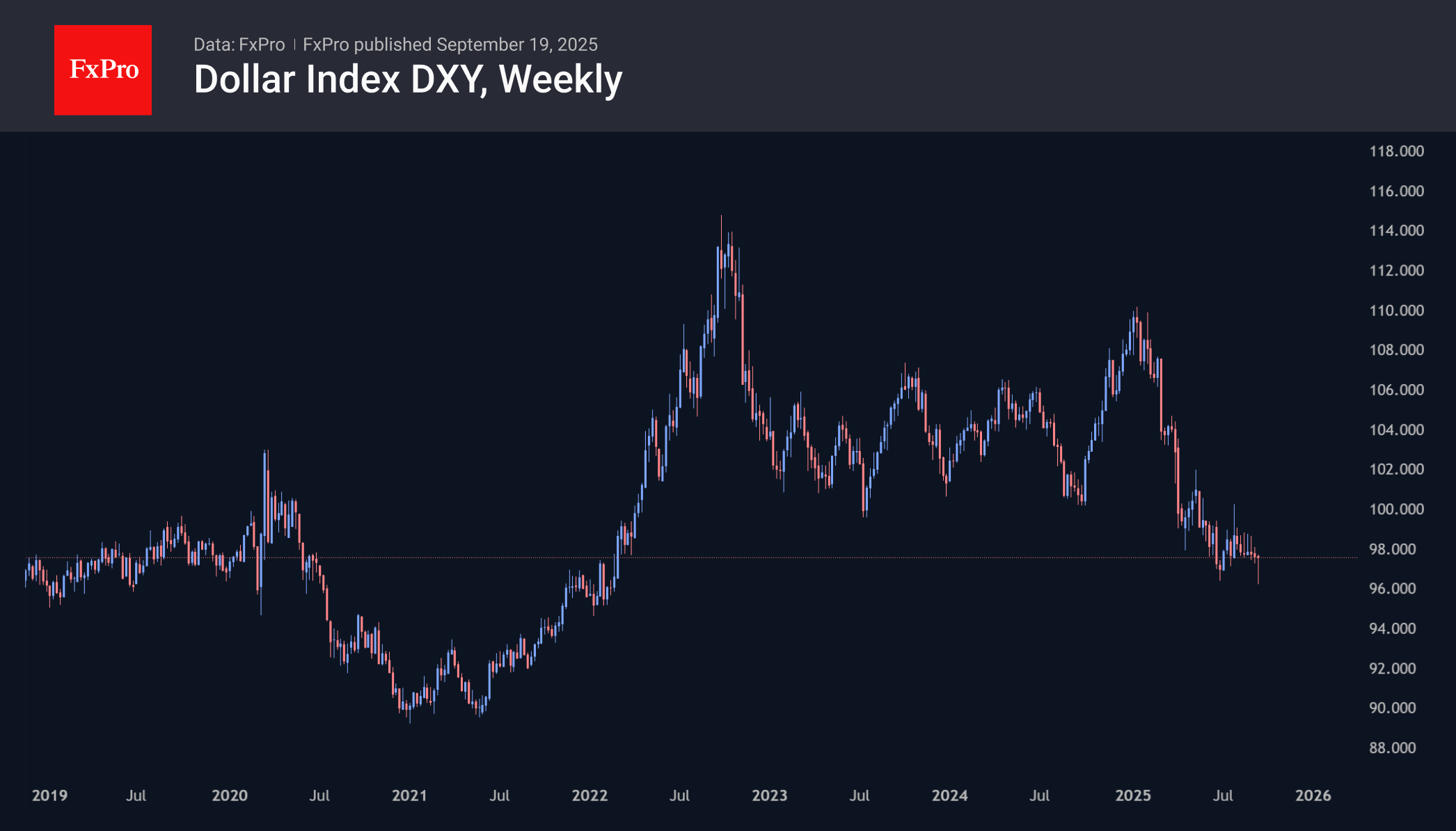

Buy the rumours, sell the facts. The US dollar was actively sold ahead of the announcement of the Fed meeting results. Investors expected the central bank to cut rates, with the FOMC’s updated forecasts showing two more acts of monetary expansion before the end of 2025, and the number of dissenters increasing from two in July to three.

In reality, only the first two expectations were met. The September forecast did indeed include two more rate cuts this year. The Fed lowered the rate by 25 basis points to 4.25% with 11 votes out of 12. Only the recently appointed president, Stephen Miran, voted for a 50 bp cut. However, after the initial downward impulse, the USD index went on a counterattack.

The US dollar’s success is primarily due to the closing of short positions. Fundamentals still do not favour the dollar. The Fed, as it did at the end of last year, will cut rates. The ECB and the Bank of England will leave them unchanged, while the Bank of Japan may raise them. Divergence in monetary policy encourages a strategy of selling the dollar’s rebounds.

Stock indices

Buying the dips in the S&P 500 is the most popular strategy in 2025. Bulls are lining up to pick up American stocks after the broad stock index fell following the September FOMC meeting and Jerome Powell’s comments. According to him, the Fed cannot avoid taking risks in a bilateral risk environment.

Over the past 50 years, the S&P 500 has risen in 13 out of 16 cases over a 6-week horizon if two conditions were met. The Fed cut rates, and the broad stock index was within 1% of its record high. History inspires bulls in US stocks.

At the same time, it is not wise to talk about a bubble. Over the past 12 months, the S&P 500 Information Technology Index has risen 27%, and the profits of its constituent issuers have risen 26.9%. For the rest of the broad stock index, these figures are 13% and 6.4%. If the market is overbought, it is outside of technology companies.

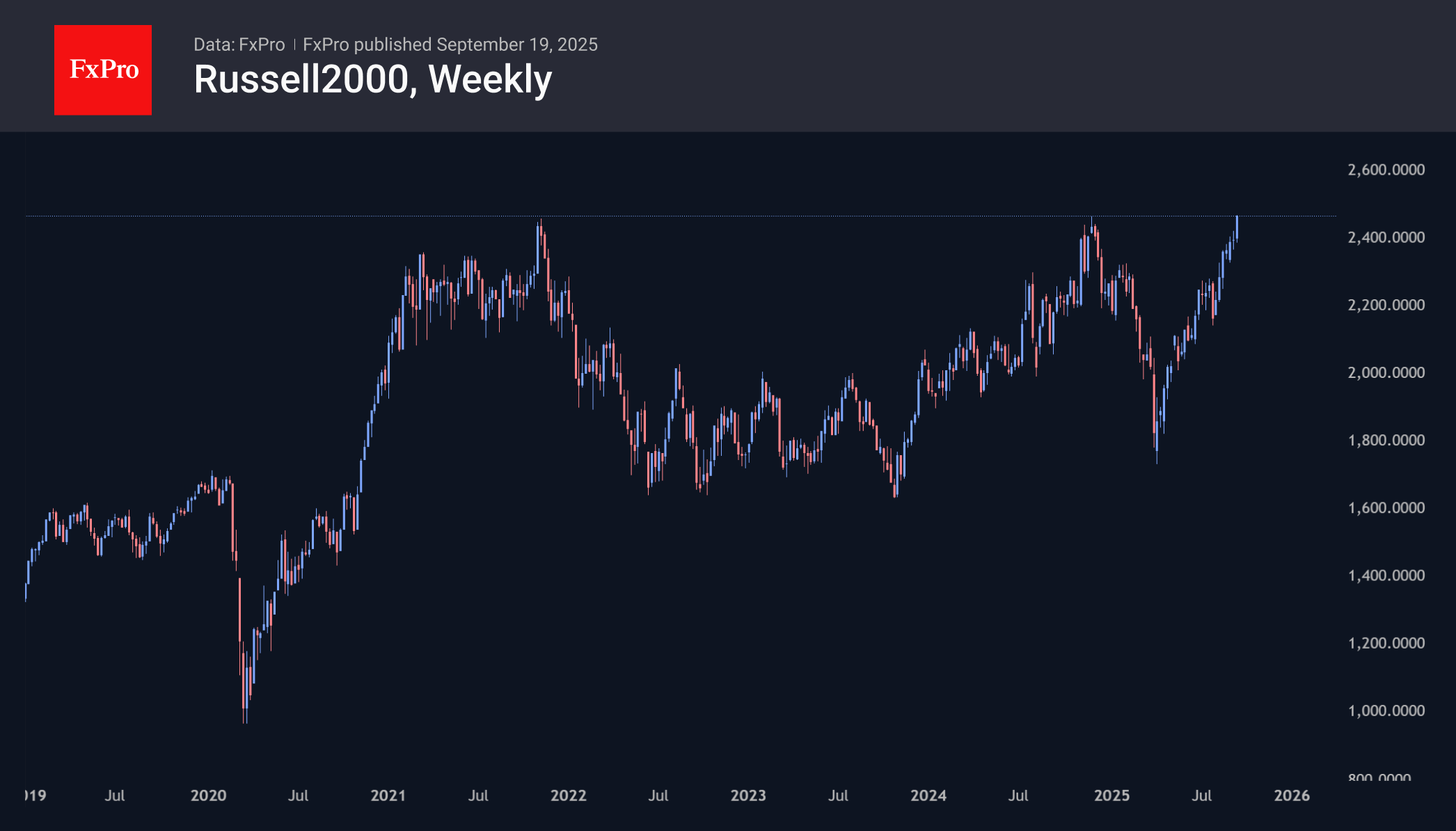

For the first time since November last year, the Russell 2000, an index of small-cap companies, has broken its historical record. It has borne the brunt of trade isolationism combined with the Fed’s restrictive monetary policy. The current peak is 0.3% above the highs of November 25, which were also only 0.3% above the peak of November 8, 2021. For comparison, the S&P 500 is now up 10.6% and 41% from those dates, and the Nasdaq 100 is up 17% and 49.7%, respectively. The main question for investors now is whether the Russell 2000 is sending a new signal of a market reversal by touching these highs, or whether it will catch up with the leaders.

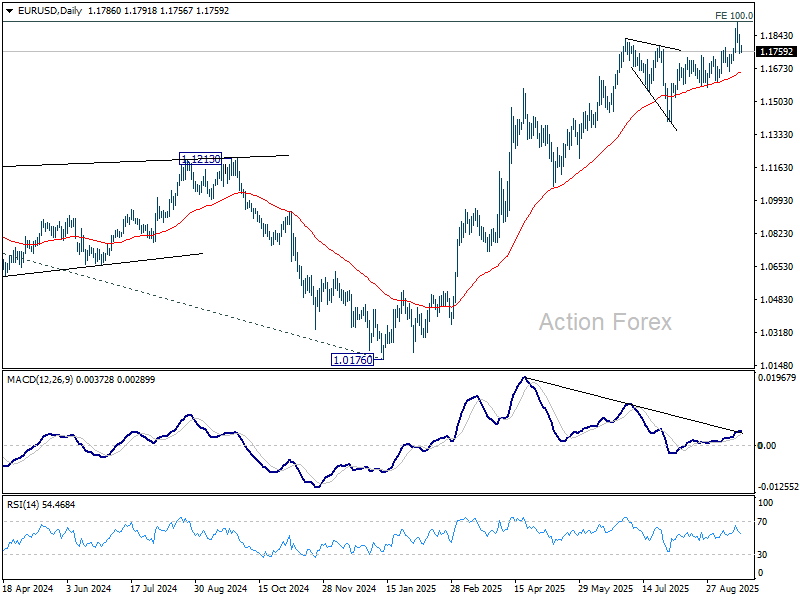

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1743; (P) 1.1795; (R1) 1.1841; More...

Intraday bias in EUR/USD stays neutral at this point. Further rise will remain in favor as long as 1.1741 resistance turned support holds. Above 1.1917 will resume larger up trend to 1.2 psychological level. However, firm break of 1.1741 should confirm short term topping, and turn bias back to the downside for 1.1573 support.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Sustained break of 1.2 psychological level will carry larger bullish implications. Next target is 138.2% projection at 1.2581. This will remain the favored case as long as 55 W EMA (now at 1.1215) holds.

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.09; (P) 147.68; (R1) 148.59; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, break of 149.12 resistance will suggest that pullback from 150.90 has completed as a correction, and rise from 139.87 is still in progress. Further rise should then be seen back to retest 150.90 next. On the downside, below 145.47 will resume the fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3505; (P) 1.3583; (R1) 1.3631; More...

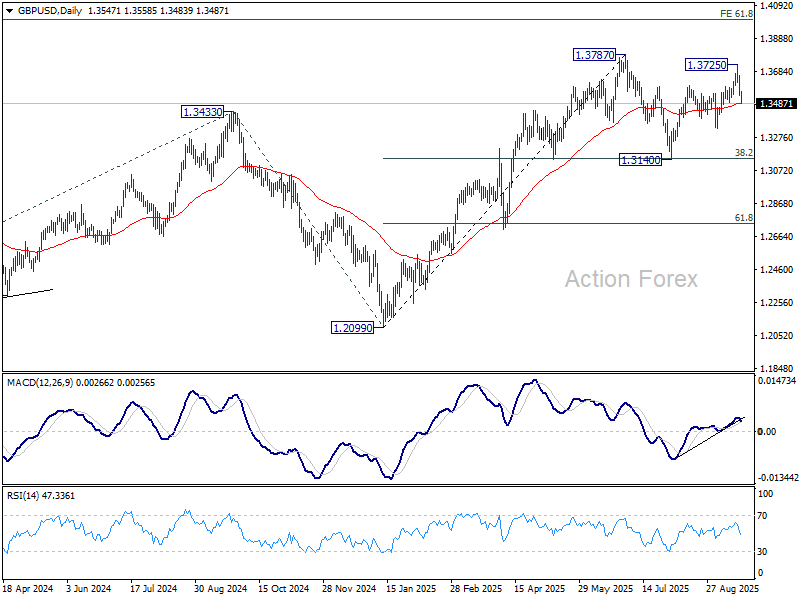

GBP/USD's fall from 1.3725 accelerates lower today, and immediate focus is now on 55 D EMA (now at 1.3488). Sustained break there will suggest that rebound from 1.3140 has completed as the second leg of the corrective pattern from 1.3787 high. The third leg has already started. Deeper fall should then be seen to 1.3332 support first. Break will target 1.3140 next. On the upside, break of 1.3725 will bring retest of 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

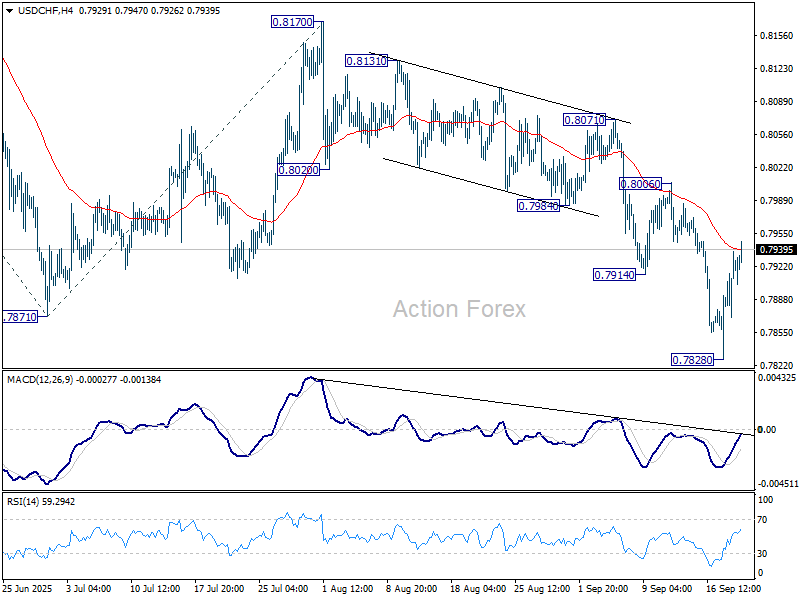

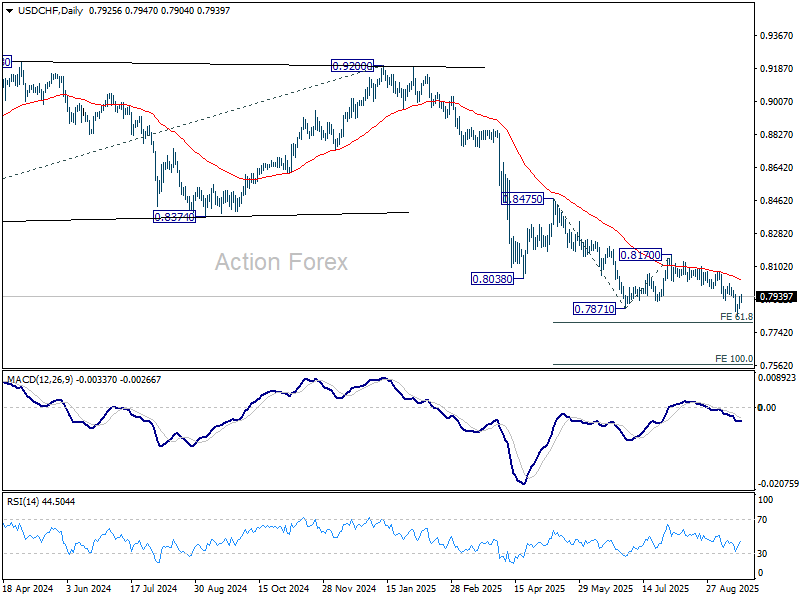

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7885; (P) 0.7912; (R1) 0.7951; More….

Intraday bias in USD/CHF remains neutral at this point. While rebound from 0.7828 might extend higher, outlook will stay bearish as long as 0.8006 resistance holds. On the downside, break of 0.7828 will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

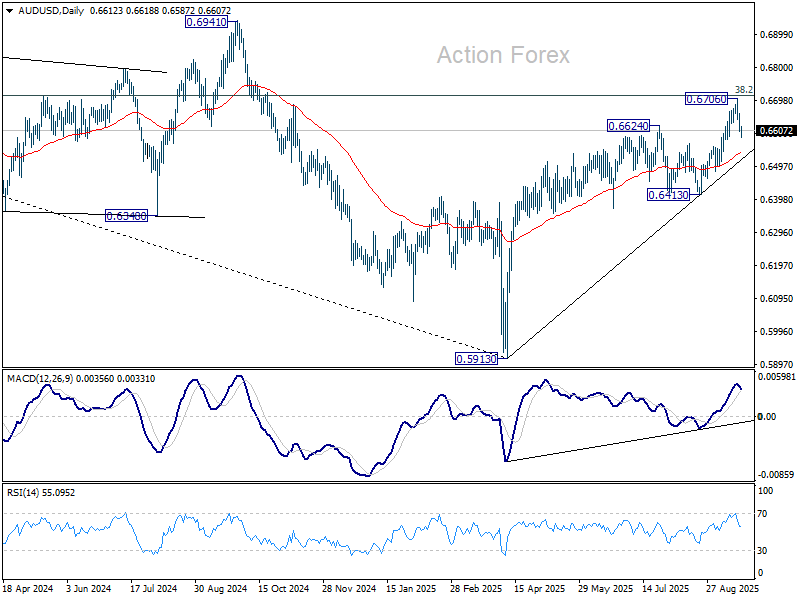

AUD/USD Daily Report

Daily Pivots: (S1) 0.6593; (P) 0.6626; (R1) 0.6646; More...

Intraday bias in AUD/USD remains neutral for the moment. Some more consolidations would be seen, but further rally is expected as long as 55 D EMA (now at 0.6541) holds. Decisive break of 0.6713 fibonacci level will carry larger bullish implications. However, sustained break of 55 D EMA will confirm short term topping and rejection by 0.6713. Deeper fall should then be seen back to 0.6413 support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

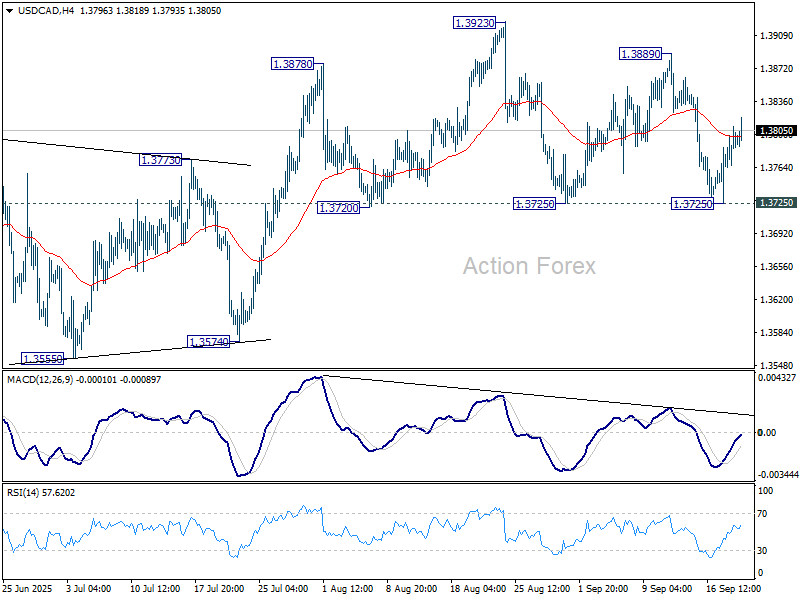

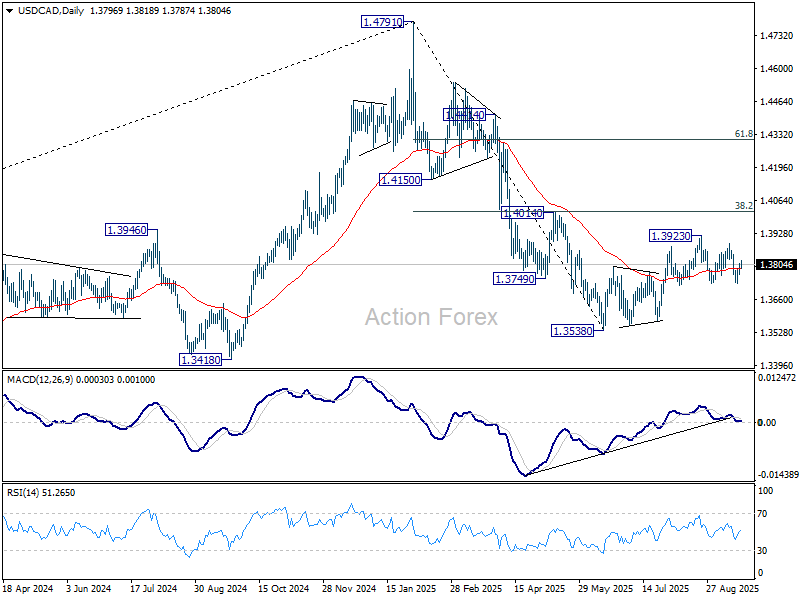

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3772; (P) 1.3791; (R1) 1.3816; More...

Intraday bias in USD/CAD remains neutral, and with 1.3725 support intact, rise from 1.3538 could still extend higher. ON the upside, break of of 1.3889 should resume the corrective rise through 1.3923 to 1.4014 cluster resistance. On the downside, though, firm break of 1.3725 will indicate that the corrective rebound has completed, and bring deeper fall back to 1.3574 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

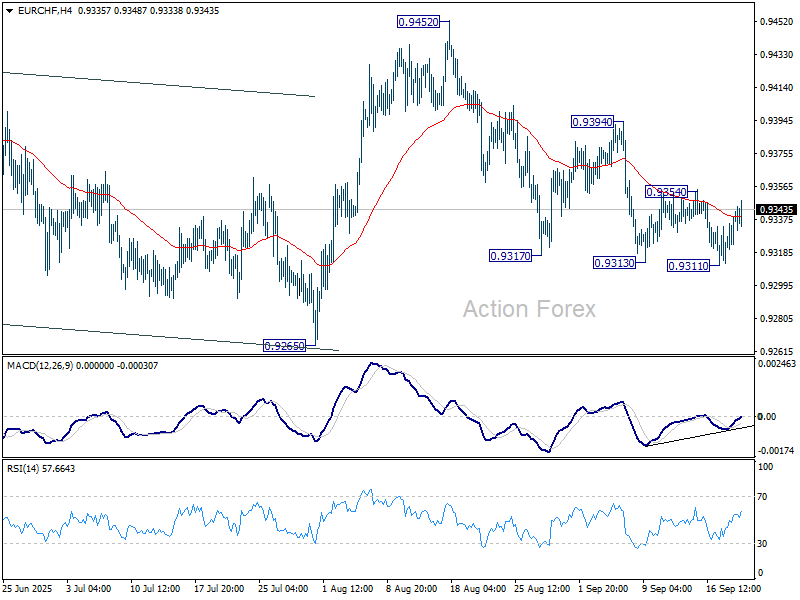

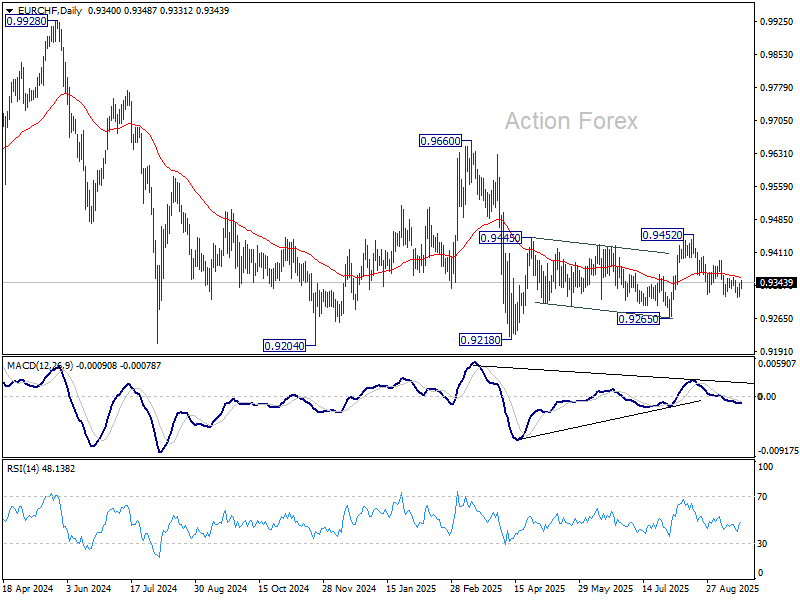

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9318; (P) 0.9331; (R1) 0.9354; More...

EUR/CHF is staying in range of 0.9311/9354 and intraday bias stays neutral. Further decline will remain in favor as long as 0.9354 resistance holds. Firm break of 0.9311 will extend the fall from 0.9452 to retest 0.9218 low. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.9354 will confirm short term bottoming, and turn bias back to the upside for 0.9394 resistance next.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

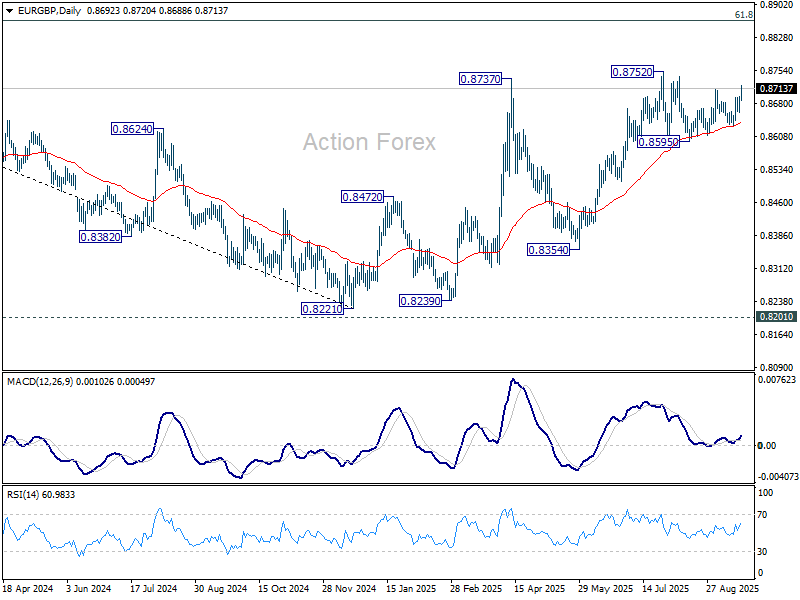

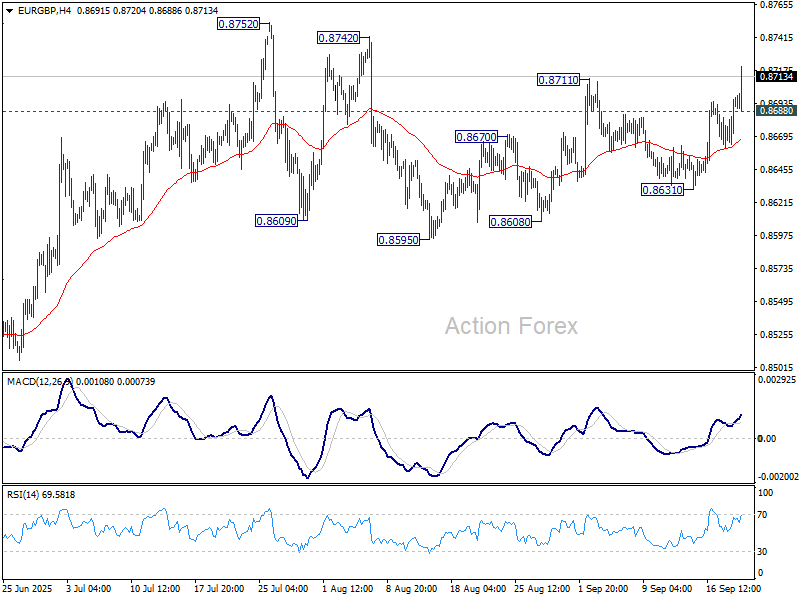

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8671; (P) 0.8685; (R1) 0.8710; More...

EUR/GBP's rally continues today and intraday bias stays on the upside. The rebound from 0.8595 is in progress for retesting 0.8752 high. Firm break there will extend the rise from 0.8221 to 0.8867 fibonacci level. On the downside, below 0.8688 minor support will turn intraday bias neutral again first. But further rise is expected as long as 0.8631 support holds, in case of retreat.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.