Sample Category Title

Post-FOMC US Dollar Surge Shifts Global Markets – DXY Outlook

A theme that had been building throughout this entire year was how a compromised Federal Reserve independence, combined with a more isolationist US policy (and de-globalization), would send the US dollar into shambles.

In fact, this theme has been a favorite for Market enthusiasts, particularly as a compromised US dollar would participate in a rewiring of all financial flows.

Since COVID, a spectacular rise in the USD supply has ramped up inflationary pressures, which got exacerbated by ever-higher government spending, hurting confidence in Fiat currencies.

Particularly after the surprising dovish shift from FED speakers, initiated by Trump-appointed Governor Waller and Bowman, Market participants were afraid of a US central bank that would be pressured by the Trump administration and influenced in its activity, further hurting the Greenback.

This turn accelerated even more after Powell's recent appearance at the Jackson Hole Symposium, which is known for providing market-shambling speeches from central bankers.

It was argued that the speech wasn't as dovish as interpreted, but metals flying higher decided otherwise.

Now, the tides have calmed: the Wednesday press conference, combined with a not-so-dovish 25 bps cut, has proven early dovish speak to be justified, and the US dollar, which had seen catastrophic days leading to the September meeting, is now making a sharp comeback.

Let's examine multi-timeframe comprehensive charts of the Dollar Index (DXY) to see how this change may affect US dollar flows in the long run.

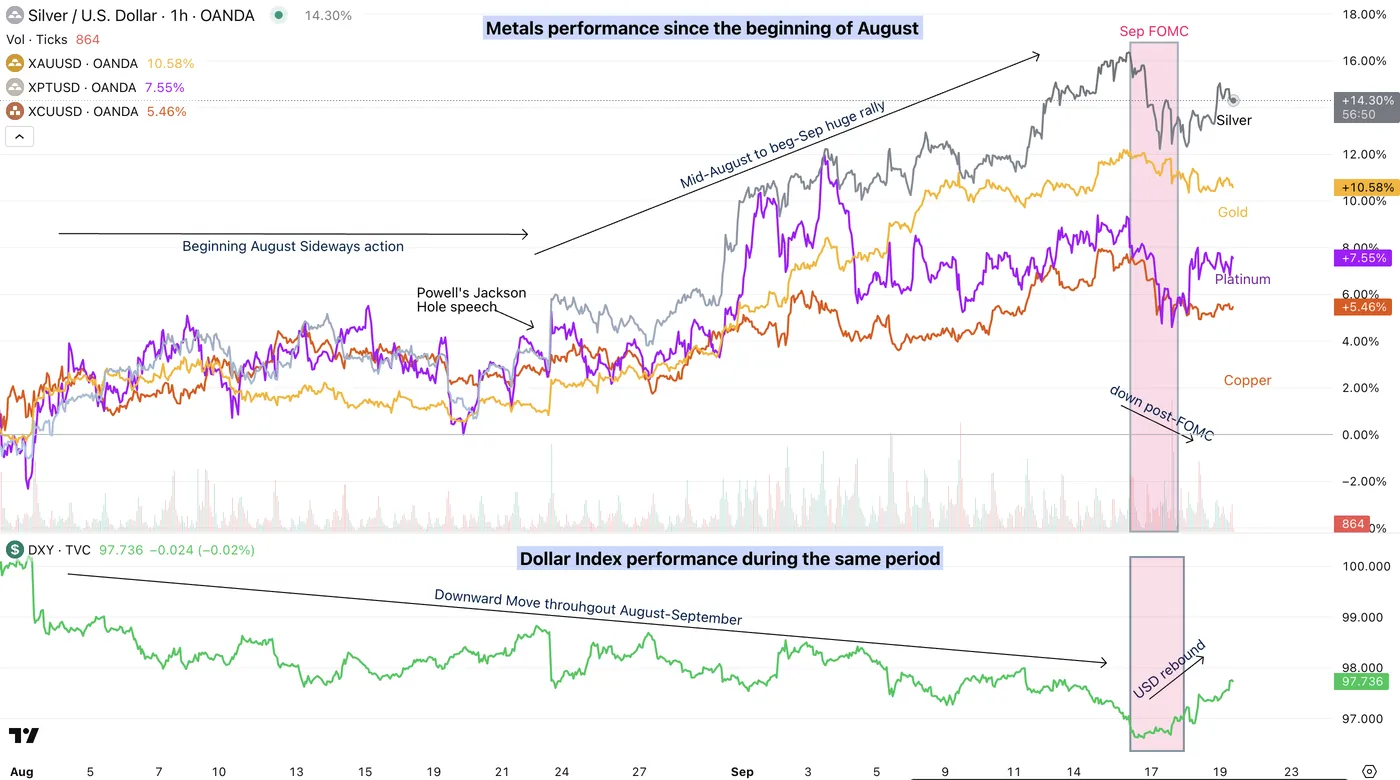

A re-upload of how US dollar movement influences metals

Dollar Index and Metals comparative Performance since beginning August, September 19, 2025 – Source: TradingView

This chart was uploaded on a piece published yesterday on metals (referenced just above) and is very pertinent to how USD ups-and-downs have a huge influence on trajectories for all asset classes, and particularly commodities.

A Dollar Index (DXY) multi-timeframe comprehensive analysis

Dollar Index daily chart

Dollar Index Daily Chart, September 19, 2025 – Source: TradingView

This Daily picture overlook retraces back to how volatile FX and US Dollar flows have been since September 2024.

Between immense buying flows at the end of 2024, followed by a n-shape downard reversal for the USD throughout 2025, volatility-enthusiasts got exactly what they needed.

You may observe the different themes and dynamics directly on the chart, but one thing to observe is how the most-recent fast-paced fall right ahead of Wednesday's FOMC meeting has been met with a consequent huge rally, with buying flows seeing continuation in today's session.

We'll see more details on this on the short-timeframes, but a clear double bottom has taken shape – The rest will be to see how this will influence markets looking forward.

Dollar Index 8H chart and levels

Dollar Index 8H Chart, September 19, 2025 – Source: TradingView

Looking closer, we spot how sharp the rebound has been after a huge pre-FOMC descent which surprised Participants.

Such hedging can occur, particularly ahead of such market-changing events, but the pace and shape of it was one of panic.

The immediate reaction to the dot plot created new 2025 lows, but looking further, an inability of sellers to close below the June lows, supplemented by a switch in the dollar fundamentals has created another environment for a rebound.

Nonetheless, the buying is currently stalling at the 200-period Moving Average just above the lows of the August range, acting as momentum pivot.

Moving above the MA would further amplify the upward reversal.

A rejection here, supplemented by a close below the pivot zone (97.25) would send the dollar to another wave of correction.

Levels to watch for the Dollar Index:

Support Levels:

- 97.25 to 97.60 current pivot, low of August range

- Major support at the 2025 lows 96.50 to 97.00

- 2025 lows 96.20

Resistance Levels:

- MA 200, immediate resistance 97.90

- 98.00 August Mid-Range, acting as resistance

- 98.50 to 98.80 Resistance Zone

- 100.00 Main resistance zone

Dollar Index 1H chart

Dollar Index 1H Chart, September 19, 2025 – Source: TradingView

Looking closer to the 1H timeframe, we see how far and fast the reversal in the Dollar went, bringing the index back above its pivot zone and just above the Pre-FOMC downward trendline.

Buyers will need to hold the retest of that trendline to maintain the path above (located right within the pivot) as overbought conditions put a short-term top to the move.

Now, the rest will be to monitor if sellers to enter here again, invalidating this theme, but momentum doesn't look that way too much – Always keep an open-eye in case a reversal back down happens from here.

Safe Trades!

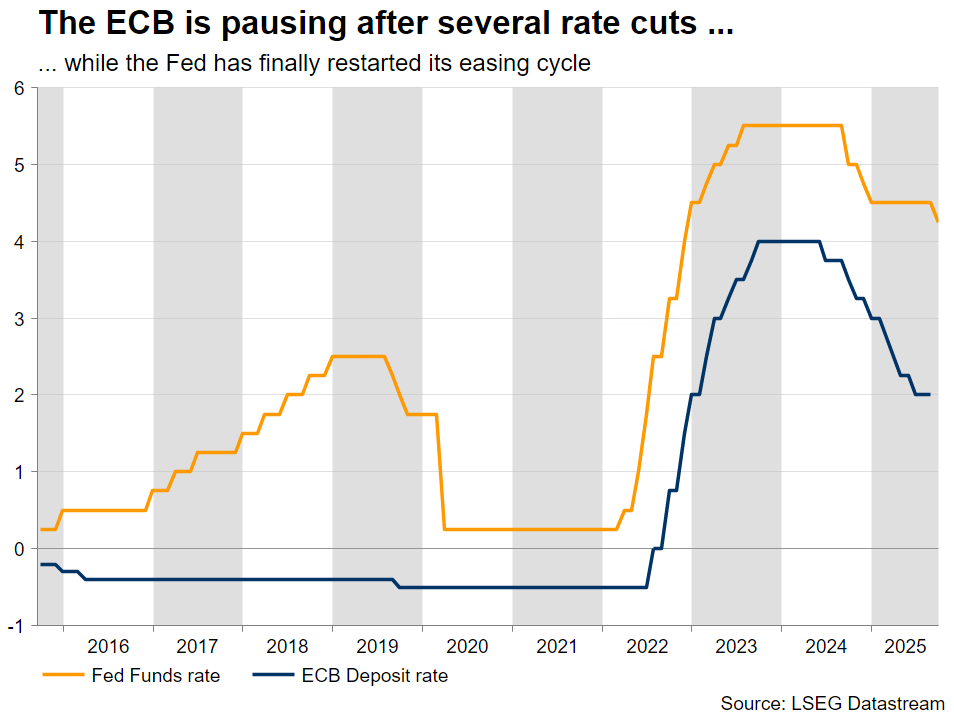

Where to Next, EUR/USD? Policy Gap Between ECB and Fed

- Fed cuts rate to 4.00–4.25% because of labor market situation in US

- Interest rate cuts in the Eurozone are in question due to inflation being under control

- Negative divergence has appeared on EURUSD, which can be a sign of correction ahead

FED Policy

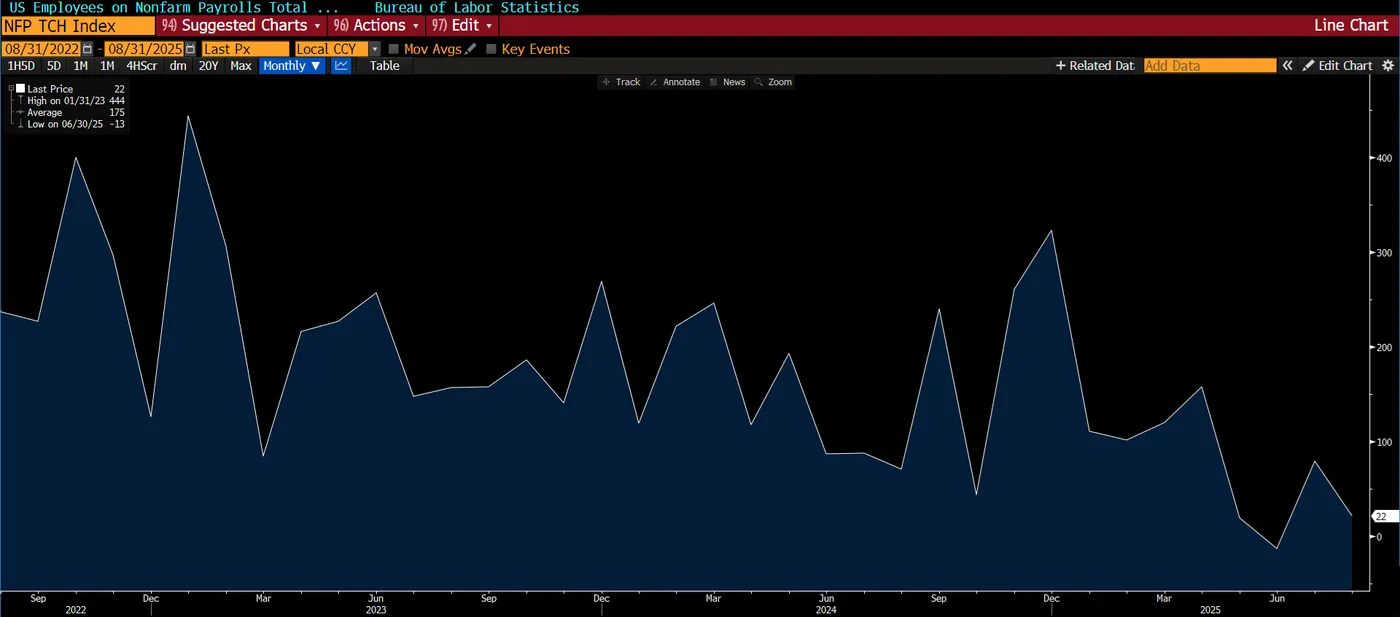

The United States Federal Reserve has decided to cut interest rates by 25 basis points, bringing the main rate to the 4.00-4.25% range. This is the first change after a nine-month pause in the cycle, and the decision itself is precautionary. The Fed, guided by a "risk management" approach, did not react to a specific economic shock but acted prudently amid increasing uncertainty.

A new element of communication was the growing attention paid to the labor market situation – despite relatively stable inflation and unemployment, a slowdown in the pace of employment and limited recruitment activity are visible, which may indicate the market's susceptibility to deterioration.

Non Farm Payrolls (in thousands), source: Bloomberg

ECB Policy

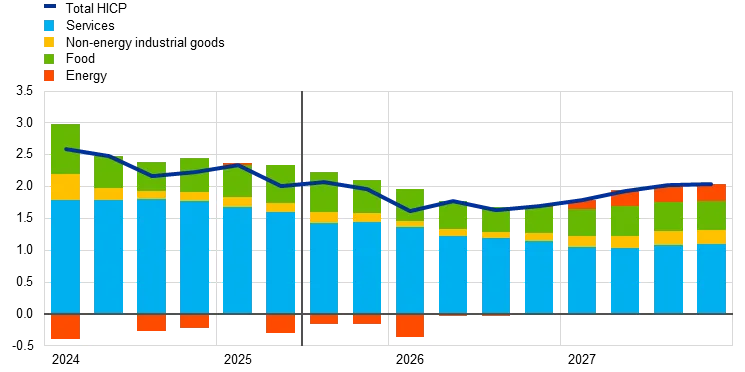

Meanwhile, in Europe, during the Eurogroup meeting in Copenhagen, members of the European Central Bank's Governing Council, Madis Muller and Mario Centeno, presented the ECB's monetary policy stance. The current policy remains moderately accommodative, and interest rates – including the deposit rate at 2% – have not changed in recent months. President Christine Lagarde emphasized that the ECB is at an opportune moment to achieve its 2% inflation target.

Madis Muller noted that inflation is currently "more or less on target," and the current level of rates supports economic growth, which in the coming quarters will be more dependent on domestic demand. Mario Centeno, in turn, pointed out the current risks to growth and inflation, which he believes are trending downwards. He did not rule out a future interest rate cut, although he currently sees no urgent need for it. The ECB forecasts inflation at 1.9% in 2027 and GDP growth of 1.3%. Structural challenges, such as higher tariffs from the US, weak industrial demand, and a growing propensity to save, limit the potential for economic recovery in the euro area.

HICP ECB Projections, source: European Central Bank

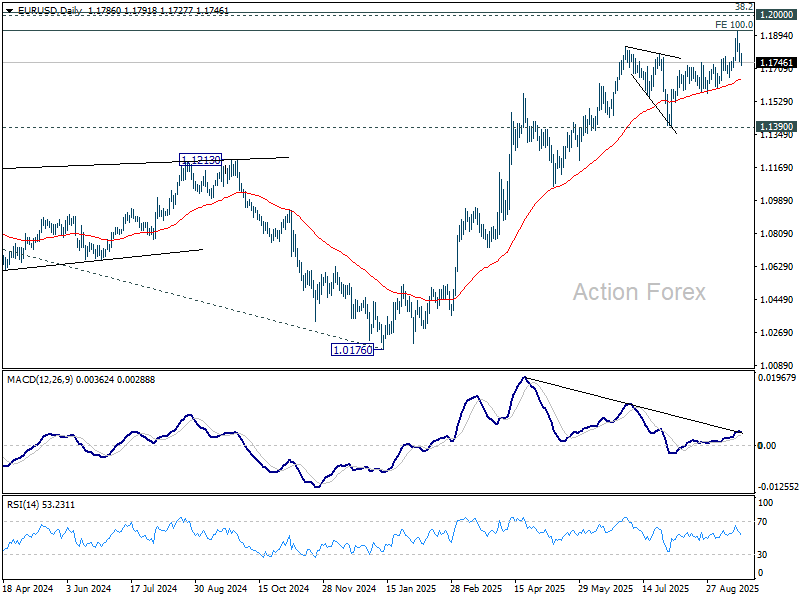

EUR/USD

EURUSD, daily timeframe, source: TradingView

In the foreign exchange market, the EURUSD pair has been in an upward trend since mid-January, when the exchange rate rose from 1.0178 to 1.1918, representing an almost 17% increase. Despite this, technical analysis indicates the possibility of a correction – a negative divergence has formed between the price and the RSI indicator. In the region of 1.14, there is important technical support – both horizontal and resulting from previous corrections within the trend.

A decline to this level could be merely a natural correction within a broad upward trend. Potential doubts about further US rate cuts could accelerate such a descent without disturbing the long-term upward structure. In turn, maintaining the current monetary policy in the euro area may strengthen the common currency's fundamentals against the dollar in the medium term.

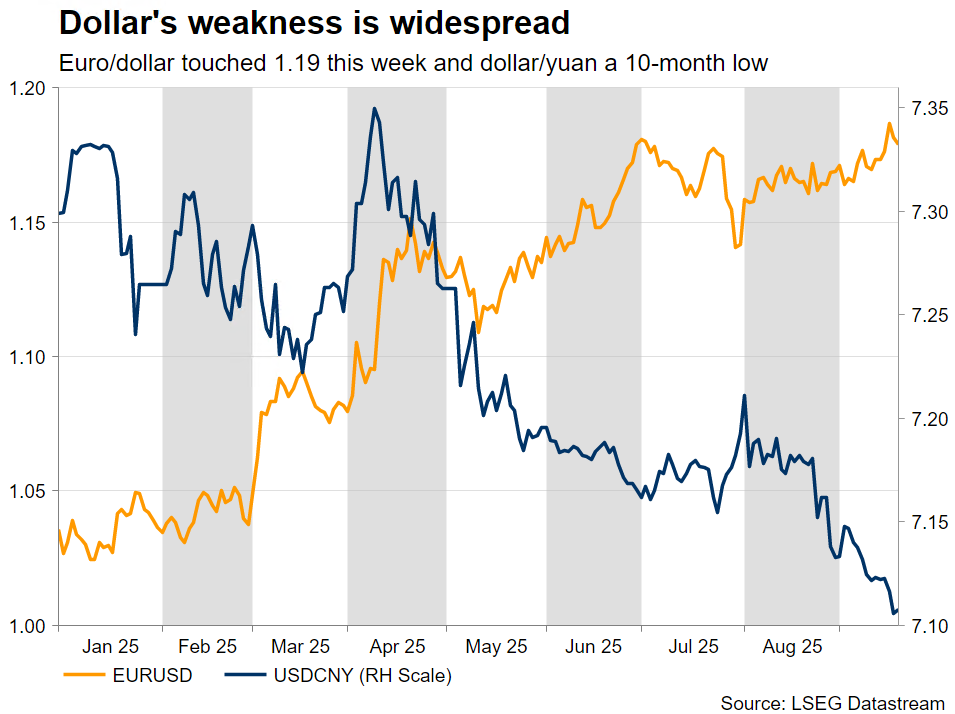

Week Ahead – Fedspeak and US Data to Set the Tone in Markets

- Dovish Fedspeak and soft PCE data may dent the dollar’s recovery.

- US-China negotiations continue, as yuan’s appreciation lingers.

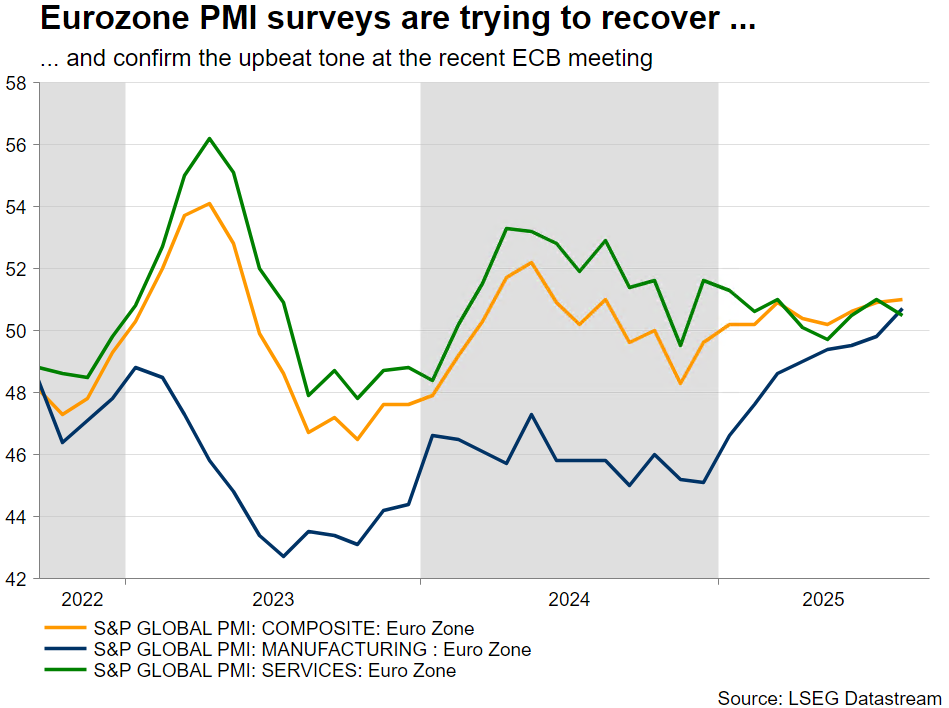

- Eurozone PMIs could cement the ECB pause; SNB might threaten with negative rates.

- Yen is bid after hawkish BoJ, but LDP contest might clip its wings.

- Aussie on the backfoot; next week’s data may offer a reprieve.

Post-FOMC period

An eventful week is coming to an end, with markets digesting the numerous central bank meetings, predominantly the Fed’s decision. The much-discussed 25bps rate cut was announced, with the US dollar being close to recording another negative week despite the post-FOMC meeting rally. Fed Chair Powell tried to dampen rate cut expectations by referring to Wednesday’s cut as a risk management move, but the dot plot told a different story.

Several investment houses are forecasting consecutive rate cuts in the remaining two Fed meetings of 2025. A plethora of Fed speakers will be on wires next week, with the focus being on Fed members Waller and Bowman and their likely remarks about failing to support the 50bps cut sought by newcomer Miran. Notably, US President Trump is also expected to chip in, most likely expressing his fury at Powell.

While dovish Fedspeak will most likely dominate the week, markets will also be monitoring incoming data and trade negotiations. The preliminary PMI manufacturing and services surveys on Tuesday could set the tone for the week, but barring a surprise at Thursday’s final Q2 GDP print, investors will be mostly interested in the durable goods report – often seen as a leading growth indicator – and Friday’s PCE report. Should the Fed’s favourite inflation metric accelerate, questions about the realistic chances of a back-to-back rate cut may arise.

The dollar is craving another small boost. Euro/dollar is hovering around 1.1770 at the time of writing, bouncing lower after posting a new four-year high at 1.1918, and dollar/yen continues to range-trade. That said, dovish Fedspeak and potentially soft data releases next week might hinder dollar’s ability to record a meaningful rally. On the flip side, stronger PCE data could offer some relief to the ailing dollar, damaging risk appetite.

Will China react to yuan’s appreciation as its economy remains fragile?

Meanwhile, the latest round of US-China negotiations resulted in the Tiktok agreement, meeting Trump’s demands. A Trump-Xi call later today is set to confirm the progress made, but could also address the Ukraine-Russia conflict. China stands by Russia at this stage, but Xi is mostly focused on addressing domestic challenges. Another set of measures to boost services consumption was announced this week.

Notably, despite pressure from the Fed rate cut and the appreciating yuan, the PBoC kept its seven-day repo rate unchanged at 1.40%. Consequently, there is a strong probability of a similar decision on Monday about the one- and five-year LPRs. That said, while the housing sector is probably in need of an LPR cut, the PBoC might want to evaluate the economic boost of the upcoming Golden Week before adjusting rates.

Will Eurozone PMIs justify the current ECB strategy?

The upbeat tone at the recent ECB meeting cemented expectations of a policy pause, with Tuesday’s OECD interim projections most likely confirming the anticipated growth acceleration. However, like for the Fed, data matter. On Tuesday, the pivotal preliminary PMI services and manufacturing surveys will be published, with investors paying extra attention to the German and French prints. In the case of the former, economists are expecting modest improvement in both indicators, despite the manufacturing one remaining in contraction. Coupled with a potentially stronger IFO survey print, one could argue that Germany might be gradually turning the corner. That same cannot be said for France though, where PMIs could weaken further due to the political turmoil.

What does all this mean for the euro? Strong data might benefit the euro, but the current rally in euro/dollar is mostly US-driven. Market concerns about Trump’s governing style, the various judicial cases, the attempted power grab at the Fed, and the lingering trend for de-dollarization boost the euro. A continuation of this trend should keep the euro supported, but a correction could be on the cards, with 1.1703 being the primary support level.

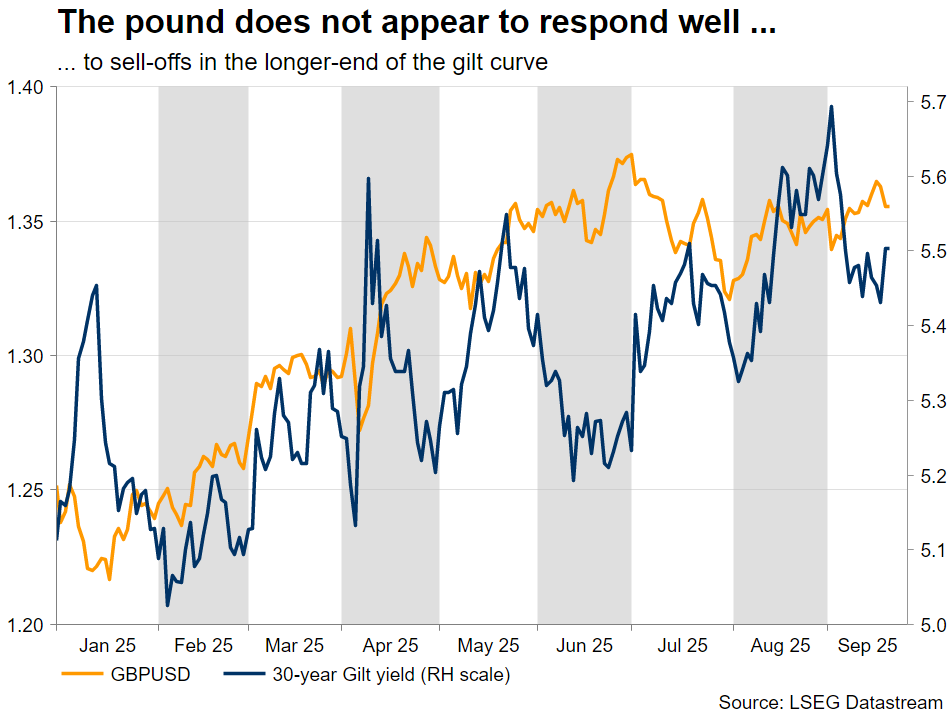

Pound’s early August rally against the Euro is gradually evaporating

Following the uneventful BoE meeting, which kept the door open to further accommodation, the focus shifts to economic data, with investors also preparing for the next Labour government crisis. Tuesday’s preliminary PMIs will offer the next piece in the growth jigsaw, though inflation remains the MPC’s main headache.

Meanwhile, there is a plethora of BoE speakers this week, potentially aiming to stir market expectations towards a November rate cut, since Thursday’s meeting involved only a statement. Any indication that the MPC is closer to a rate cut than currently perceived may put another dent in the pound’s recent rally against the dollar.

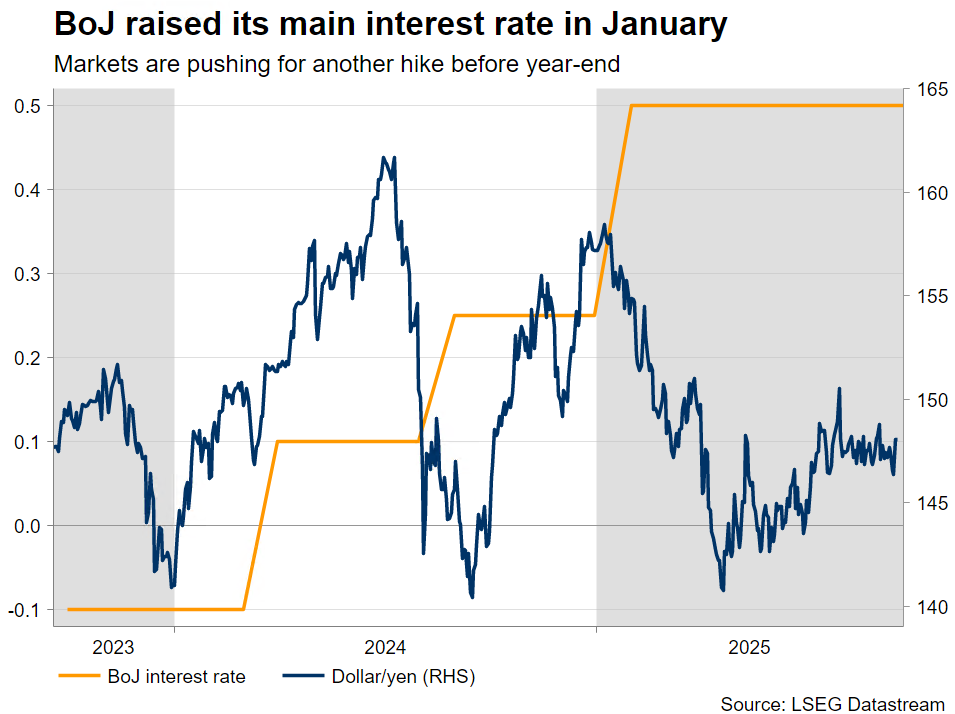

Yen stuck between BoJ and political developments

Similarly, the yen continues to dance to the tune of politics. The October 4 LDP leadership contest is hotting up with five candidates already in the starting line. They will gradually present their strategies, with investors focusing on their fiscal policy stance and their outlook on the BoJ, with most candidates unlikely to openly support Governor Ueda’s effort to normalize policy.

The BoJ kept rates unchanged earlier today, and is preparing for the final two meetings of 2025. Ueda et al remain confident about the inflation outlook, partly due to the final US-Japan trade agreement, with next Friday’s Tokyo CPI report in focus. The yen has reacted positively to two hawkish dissidents at today’s meeting, but further hawkish signals are necessary to support a dollar/yen bearish breakout from the prevailing range.

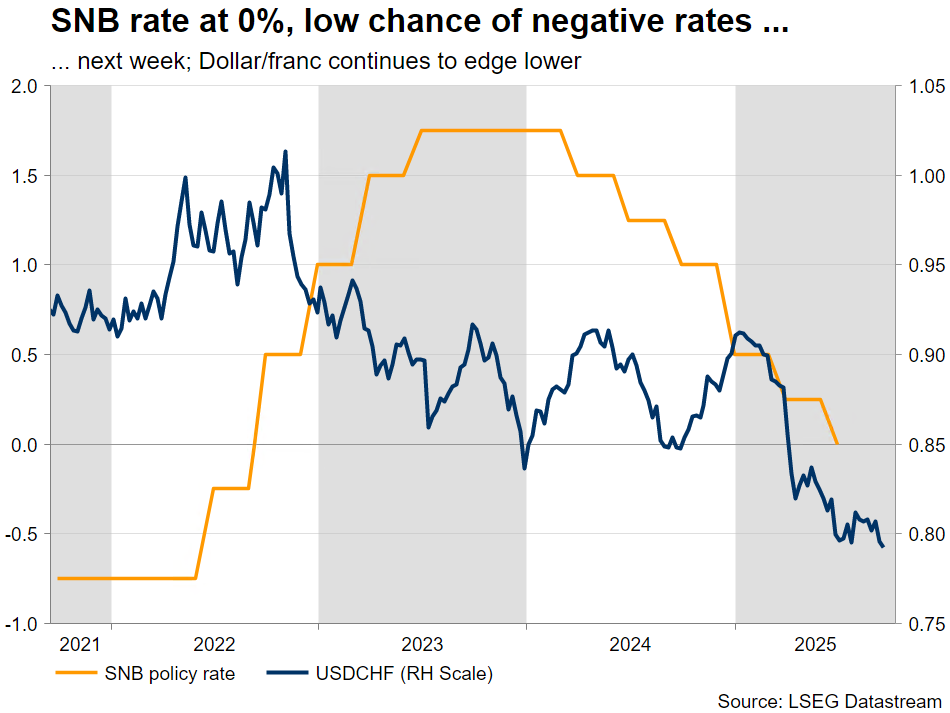

SNB to refrain from pushing rates to negative territory this time around

Unlike other central banks, the SNB has already pushed its policy rate to 0%. With consumer price inflation hovering just above zero, producer price inflation edging further into negative territory, the economy evidently slowing down, and the Swiss franc recording an impressive 13% rally against the dollar, the SNB is understandably pondering negative rates for the first time since mid-2022.

With the franc’s strength being mostly a product of the dollar’s broader weakness and of the search for a safe haven, a rate cut would serve as a signal of the SNB’s determination to achieve its price target. Therefore, while no rate cut is expected on Thursday, SNB President Schlegel is set to keep the door wide open for another rate cut, indirectly threatening a replay of the 2014-2022 period. Only time will tell if markets see this as an empty threat and continue to push dollar/franc lower.

Aussie might catch a bid

Finally, the antipodeans are losing ground this week against the dollar. With China still struggling to meaningfully restart its domestic economy, the Australian economy remains fragile. Growth in the second quarter of 2025 was encouraging, the labour market is not showing serious cracks and monthly inflation indicators are holding up following the mixed Q2 prints. Should next Tuesday’s preliminary PMIs and Wednesday’s CPI report post upside surprises, then chances of a September 30 rate cut might be dented, boosting the aussie.

Weekly Focus – Central Banks on a Relatively Steady Course

The September round of central bank meetings is nearing its end with perhaps a surprising sense of stability in financial markets. Despite the blurry outlook, mixed data signals and political pressure in the US, the rate decisions did not cause major volatility in broader financial conditions. That said, US bond yields have edged higher towards the end of the week, and broad USD has recovered despite the policy rate cut from the Fed.

The Fed's 25bp rate cut was backed by almost unanimous support from the FOMC voters. Only Stephen Miran, whose nomination the Senate confirmed at the last minute on Monday, voted for a larger 50bp move. In addition, the dot plot revealed that one non-voter would have preferred to maintain rates unchanged through the rest of the year.

The rate projections revealed greater dispersion in views towards the final two meetings of the year. 9 out of 19 participants predicted only one more rate cut before year-end, or none at all. The exact same number of participants favoured cutting rates at both of the two remaining meetings. Powell emphasized that the rate cut was motivated by a shift in the balance of risks towards weaker labour markets, rather than deterioration of the baseline outlook. In fact, median forecasts for both growth and inflation were revised up for 2026.

We made no changes to our previous call and still forecast only one additional cut this year at the December meeting, followed by three more cuts in 2026. Our forecast profile is aligned with the more hawkish camp of Fed participants, and above market pricing for the rest of the year, read more from our Fed review - Slim margins, 17 September.

Norges Bank delivered a mixed package, as it cut the policy rate by 25bp in line with our call, but paired the cut with hawkish forward guidance. We expect NB to stay on hold for the rest of the year and deliver four more cuts in 2026, see Reading the Markets Norway - A hawkish 25bp cut; enter DEC25-DEC26 flattener, 18 September. Both Bank of England and Bank of Japan kept rates unchanged, as widely expected, but the latter decision came with a hawkish tilt. BoJ announced a gradual reduction of its ETF and REIT holdings, and two members dissented in favour of a hike, which is now almost fully priced in by January.

Next week, the string of rate decisions concludes with Riksbank and the Swiss National Bank, both of which we expect to keep rates unchanged. Riksbank will likely signal an easing bias for coming months, and we forecast one more 25bp rate cut in November.

Focus will increasingly turn back towards macro data, which remains divided. US retail sales surprised positively in August (control group +0.7% m/m SA), as especially online sales held up ahead of expected tariff-driven price hikes. On the other hand, growth disappointed in China across both retail sales and industrial production. Even so, we expect China's Loan Prime Rates to remain unchanged on Monday, as the 1-week reverse repo rate (which is used to signal policy changes) has remained unchanged since May.

The most interesting data release of the week will be the September flash PMIs, which are due for release on Tuesday for euro area, the UK and the US. We expect to see gradual continuing improvement in the manufacturing indices whilst services activity growth has likely softened modestly from August.

Sunset Market Commentary

Markets

Dire public finances suddenly turned the spotlights back on the UK today. The monthly August deficit, a once only second tier number for markets, came in at £18bn. That was way bigger than both markets but more importantly, the Office of Budget Responsibility had predicted (£12.5bn). Total deficit in the running fiscal year (starting in April) now mounted to £83.8bn, again well above OBR forecasts. It’s another blow to UK chancellor Reeves and ups the ante for the November 26 annual budget. Reeves needs to strike a balance between her pledge not to raise taxes any further and stick to the government’s promised investment plans while abiding to her self-imposed fiscal rules (ie. simply borrowing your way out is not an option). Today’s setback comes days after news that the OBR is expected to lower its productivity forecast, meaning less economic growth and therefore less tax revenue. UK gilts underperform. The 30-yr yield adds 4 bps currently. The Bank of England yesterday announced that it would sell less long-term bonds as part of its QT programme (which has been lowered in scale as well, to £70bn from £100bn). But that seems to be a drop on a hot plate. Yields in other core areas rise too, be it to a lesser extent. US rates add 1.2-2.7 bps, leaving further behind the recent lows in the wake of the Fed’s rate cut on Wednesday. We’re closely watching the inflation expectations component, which is nearing the recent highs around 2.5%. There’s some buzz again around the Fed’s 2% target. Fed’s Kashkari said today the central bank is not ok with 3% inflation but some say Wednesday’s precautionary move (to support the labour market even though inflation is still too high and not expected to drop below target) is a sign the Fed is willing to tolerate higher inflation. European rates add a few bps as well with Bunds slightly underperforming vs. swap. Between euro area countries, the French spread has been trading higher than Italy’s every day all week in what is nothing less than a historical shift. The US dollar has a slight upper hand. DXY rises to 97.7 in a three-day win streak. EUR/USD drifts south to 1.175. Sterling loses ground as well with EUR/GBP pushing beyond 0.87(1). The Japanese yen pared early gains to trade flat around 148. The BoJ stood pat this morning but in a 7-2 split. The dissenters wanted to hike to 0.75%, saying that the 2% price target has been achieved.

News & Views

Previewing next week’s policy decision, it is widely expected that the MNB will leave its policy rate unchanged at 6.5%. Headline inflation (4.3% in August) has eased toward 4%, but underlying measures such as core inflation and inflation expectations remain uncomfortably high, leaving no room for a premature move. At the same time, the economic activity offers no strong support for policy tightening. Retail sales and underlining domestic demand is fragile. Growth remains subdued overall (0.4% Q/Q in Q2, but only 0.1% higher activity compared to the same period last year). Despite weak growth, MNB has no choice but to keep its focus on inflation. Positive news for policy makers: the forint performed rather well of late with EUR/USD moving toward 390. This should help to ease second round inflation effects. However, the forint remains vulnerable, amongst others as market position is quite strongly skewed HUF-long leaving the currency exposed to external shocks. In a somewhat longer term perspective, KBC assesses that a chances on a MNB rate cut are slim this year. A narrow window for a symbolic 25 bps cut in December could open if three conditions are met: 1. Rating agencies in their autumn reviews have to leave the Hungarian Credit rating unchanged; 2.The Fed has to continue policy easing global yields spreads; 3. The forint strengthening toward EUR/HUF 385 would give the MNB some room of maneuver. Even so, such a move won’t mark the beginning of a new easing cycle, but serve as a signal of flexibility, an acknowledgment that domestic and external conditions had aligned sufficiently to justify a modest step.

According to the German IFO institute, sentiment in residential construction in Germany clouded over again in August, with the index falling from minus 24.2 to minus 26.3 points. Both companies’ expectations for the coming months and their assessments of the current situation worsened. “The cautious upturn in sentiment of recent months is on hold,” said Klaus Wohlrabe, Head of Ifo Surveys. He assesses that it will take time before the increase in building permits is reflected in the order books. In a broader perspective, Ifo still sees companies struggling with weak demand. The share of companies with a lack of orders eased slightly but at 45.7% remains at a high level.

Canada’s Retail Sales Slips, Canadian Dollar Edges Higher

The Canadian dollar is in negative territory for a third straight day. In the North American session, USD/CAD is trading at 1.3820, up 0.18% on the day.

Canada's retail sales slide

Canada's retail sales declined by 0.8% m/m in July, a sharp dowrturn from the 1.6% gain in June. The volatility in retail sales reflects uncertainty over the US tariffs, which has affected consumer spending. August is expected to show a rebound, with a preliminary estimate of a 1% gain, which would make up for the July decline.

US unemployment claims slip

There are no US releases today but there was positive news from the employment front on Thursday. Unemployment claims fell to 231 thouand last week, down from 264 thousand a week earlier, which was the highest reading since October 2021. The sharp spike in claims, together with soft nonfarm payrolls, had elevated concerns about the health of the US labor market.

The latest unemployment claims release indicates that layoff are low, but hiring remains weak as the demand for workers has slowed. The Federal Reserve is keeping a close eye on the labor market and Fed Chair Powell cited the downside risk to employment as the reason for the rate cut, the first since December 2024.

- USDCAD is testing resistance at 1.3808. Next, there is resistance at 1.3821

- 1.3796 and 1.3783 are providing support

USDCAD 4-Hour Chart, September 19, 2025

Canada: Retail Sales Falter in July, But Rebound in August

Retail sales contracted by 0.8% month-on-month (m/m) in July, matching Statistics Canada's advanced estimate.

After adjusting for inflation, the volume of retail sales declined 0.8% m/m.

Auto sales continued to grow at a modest pace, rising 0.2% m/m and providing a small offset to the headline decline.

Receipts at gas stations and fuel vendors fell 0.9%, as gasoline prices continued to decline in July. In volumes terms, however, sales rose 0.2% m/m.

Core sales – excluding auto sales and receipts at gas stations – fell 1.2% m/m in July. Food and beverage stores led the decline (-2.5% m/m) despite ongoing price inflation. Sales at clothing and clothing accessories stores also retreated (-2.9% m/m), giving back some of the strong gains recorded in June.

The only categories to record gains were furniture and home furnishings stores (+1.0% m/m) and miscellaneous store retailers (+0.5% m/m), though neither added meaningfully to the headline.

E-commerce sales rose by 2.2% m/m in July.

Statistics Canada's advanced estimate points suggests that sales recovered in August, rising 1.0% m/m.

Key Implications

Volatility in the data remains exceptionally high, however nominal sales in Q3 are now tracking 1.1% annualized growth despite July's outsized weakness.

Cooling employment and softer wage gains are likely to catch up with consumers in Q3, reinforcing a more frugal mindset. While wealth effects could continue to buoy services spending among higher-income households, another leg up in domestic tourism and related spending appears unlikely. Goods demand, meanwhile, looks set for a sizeable contraction, with vehicle sales likely to pull back in in the third quarter.

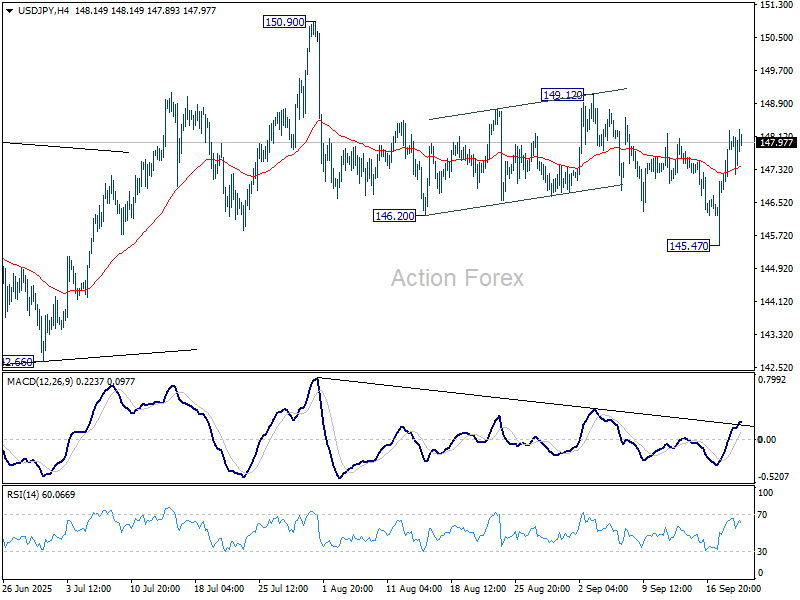

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.09; (P) 147.68; (R1) 148.59; More...

Outlook in USD/JPY is unchanged and intraday bias remains neutral. On the upside, break of 149.12 resistance will suggest that pullback from 150.90 has completed as a correction, and rise from 139.87 is still in progress. Further rise should then be seen back to retest 150.90 next. On the downside, below 145.47 will resume the fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

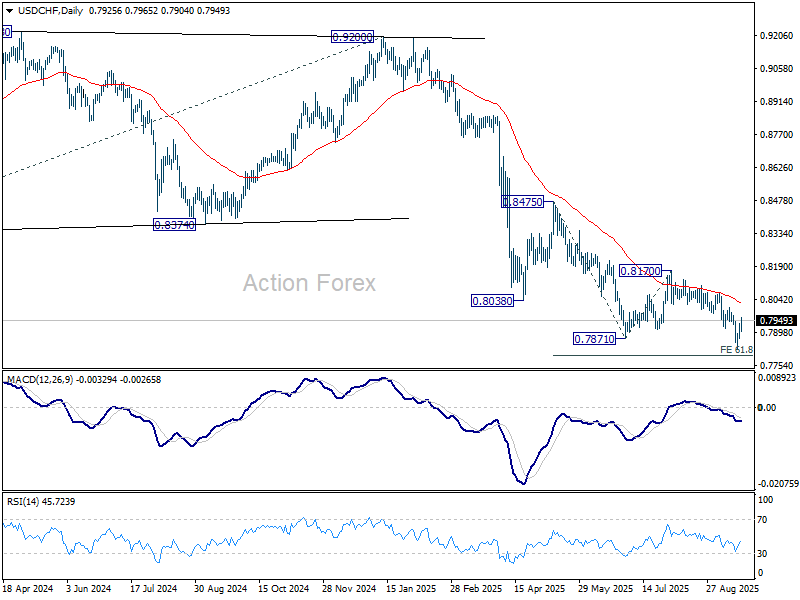

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7885; (P) 0.7912; (R1) 0.7951; More….

No change in USD/CHF's outlook and intraday bias stays neutral. While rebound from 0.7828 might extend higher, outlook will stay bearish as long as 0.8006 resistance holds. On the downside, break of 0.7828 will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1743; (P) 1.1795; (R1) 1.1841; More...

EUR/USD's break of 1.1741 resistance turned support indicates short term topping at 1.1917, after rejection by 1.1916 projection level. Intraday bias is back on the downside. Deeper fall should be seen to 1.1573 support next. For now, risk will stay on the downside as long as 1.1917 resistance holds, in case of recovery.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. Further rise could still be seen as long as 1.1390 support holds. Break of 1.1917 will target 1.2 psychological level. Decisive break there will carry larger bullish implications. However, considering bearish divergence condition in D MACD, firm break of 1.1390 will indicate medium term topping.