Sample Category Title

Bank of Canada Cuts Rates as Labour Market Softens

The Bank of Canada (BoC) cut its policy rate to 2.50%, in line with market expectations.

The statement noted that “underlying inflation is running around 2.5%” and that the removal of retaliatory tariffs on imports from the U.S. “will mean less upward pressure on the prices of these goods going forward”. One notable inclusion was CPI excluding taxes once again receiving a call out (2.5% year-on-year).

The press conference opening statement noted that the labour market has softened, underlying inflation pressures have cooled, and the removal of retaliatory tariffs means there is “less upside risk to future inflation”.

Looking forward, emphasis will be place on examining how export growth evolves and the knock-on effects it will have on “business investment, employment and household spending”.

Key Implications

The phrase that stood out is that “Governing Council is proceeding carefully, with particular attention to the risks and uncertainties”. This will help rein in market pricing from becoming overly aggressive on rate cut expectations. But, at the same time, we have long maintained this would not be a one-and-done scenario for the BoC.

Economic slack will persist, and the risks appear disproportionately on the downside, with little reason to believe there will be quick resolution to trade issues – particularly with the U.S. triggering the review of USMCA yesterday, well in advance of the timeline.

Officials have space to deliver another cut with core inflation metrics softening and the labour market showing visible strains. We look for the BoC to deliver another 25 basis points of easing at their next meeting in October. Beyond that, we’ll need to assess the state of the economy and overall environment. The ball goes into the government’s court with their Budget on November 4th. The BoC will factor in spending and other initiatives for the decision in December.

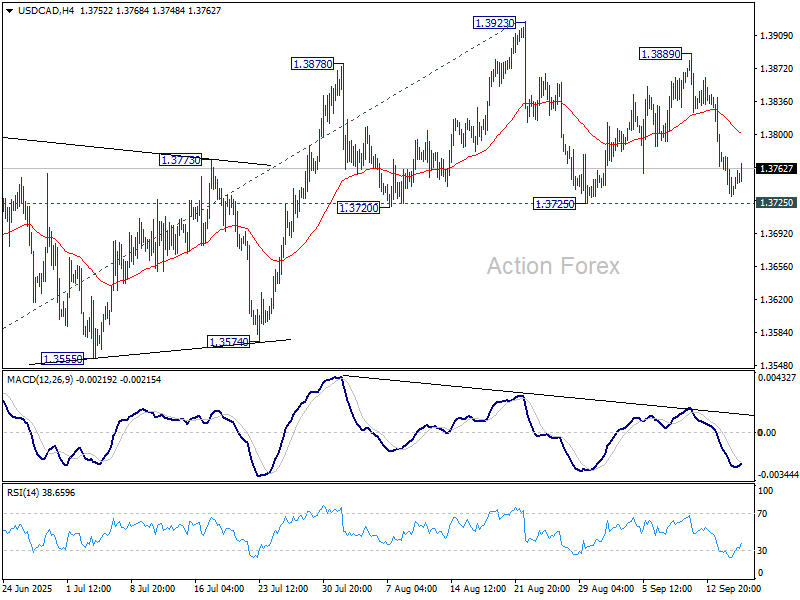

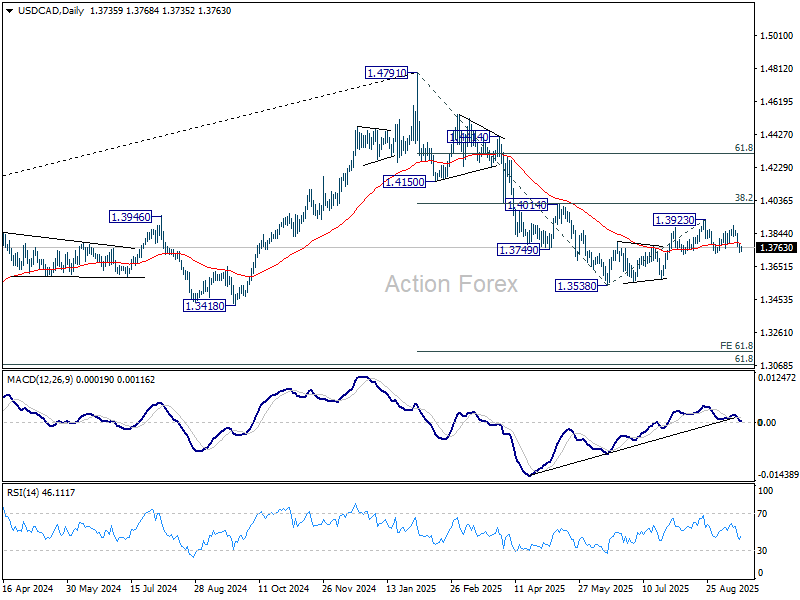

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3721; (P) 1.3752; (R1) 1.3770; More...

Outlook in USD/CAD is unchanged and intraday bias stays neutral. On the downside, firm break of 1.3725 support will complete a head and shoulder top (ls: 1.3878, h: 1.3923, rs: 1.3889). That would indicate that corrective rebound from 1.3538 has already completed, and turn near term outlook bearish. Deeper fall should then be seen to 1.3574 support. On the upside, however, break of 1.3923 will resume the rebound towards 1.4014 cluster resistance.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Loonie Steady as BoC Cuts as Expected, Fed Now in Spotlight

The forex markets were steady in early U.S. trading, with the BoC’s widely expected 25bps rate cut to 2.50% generating little reaction. The decision was fully priced in, and the absence of fresh guidance left traders reluctant to adjust positions.

The BoC struck a cautious balance in its statement, offering no explicit signal of further cuts. Policymakers acknowledged risks to both growth and inflation, but the tone suggested slightly more concern about the economy and labor markets than price pressures. This leaves the door open for more easing, though the Bank appears inclined to proceed carefully.

Attention now shifts firmly to the Fed’s policy announcement. A 25bps cut to 4.00–4.25% is widely anticipated, but the real market drivers will be the voting split, the updated economic projections, and the tone of Chair Jerome Powell’s press conference. Together, these will shape expectations for the pace of easing into 2026.

In currency performance so far this week, Dollar remains the weakest, reflecting markets’ anticipation of Fed easing. Aussie and Kiwi have also lagged, while Sterling and Loonie are holding steady in the middle of the pack. Safe-haven demand has supported Swiss Franc, which leads the majors, followed by Euro and then Yen.

For now, traders are in wait-and-see mode. The Fed’s communication will be decisive in determining whether Dollar’s selloff deepens, whether yields break below 4%, and whether risk assets such as equities and Gold extend their strong runs.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.44%. CAC is down -0.08%. UK 10-year yield is down -0.013 at 4.631. Germany 10-year yield is down -0.015 to 2.680. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 1.78%. China Shanghai SSE rose 0.37%. Singapore Strait Times fell -0.32%. Japan 10-year JGB yield fell -0.012 to 1.592.

BoC cuts to 2.50%, warns trade shocks still a drag

The BoC lowered its overnight rate by 25bps to 2.50% at today’s meeting, in line with widespread expectations. The move underscores the central bank’s effort to provide additional support as Canada’s economy struggles with weaker growth and softer inflation risks.

In its statement, the Governing Council said a “weaker economy and less upside risk to inflation” justified the cut, helping to better balance risks. The Bank highlighted that shifts in global trade continue to “add costs” even as they “weigh on economic activity.”

Looking ahead, policymakers said they will be closely monitoring how U.S. tariffs and evolving trade relationships affect exports, investment, employment, and household spending. They also flagged the risk that supply chain reconfiguration could pass higher costs onto consumers, stressing that inflation expectations remain a key guide for future decisions.

Eurozone CPI finalized at 2.0%, services drive price growth

Eurozone inflation was confirmed at 2.0% yoy in August, unchanged from July, while core CPI held steady at 2.3% yoy. Services remained the main driver of inflation, contributing +1.44 percentage points to the annual rate, followed by food, alcohol, and tobacco (+0.62pp), and non-energy industrial goods (+0.18pp). Energy remained a drag, subtracting -0.19pp.

For the EU as a whole, CPI was finalized at 2.4%, also unchanged from the previous month. Inflation trends varied sharply across member states. Cyprus (0.0%), France (0.8%), and Italy (1.6%) registered the lowest rates, while Romania (8.5%), Estonia (6.2%), and Croatia (4.6%) recorded the highest. Compared with July, annual inflation fell in nine member states, was stable in four, and rose in fourteen.

UK CPI steady at 3.8% in August, goods prices firm, services ease

Inflation in the UK held steady in August, with CPI unchanged at 3.8% yoy, matching consensus. On the month, prices rose 0.3%. Core CPI, which strips out food, energy, alcohol, and tobacco, eased from 3.8% yoy to 3.6% yoy, a notch below expectations of 3.7% yoy and another sign that underlying pressures are easing gradually.

Goods prices provided an offset, rising from 2.7% yoy to 2.8% yoy, their highest since October 2023. By contrast, services inflation slowed from 5.0% to 4.7%, pointing to softer domestic price dynamics. While still elevated, the services pullback is significant given its importance in shaping medium-term inflation risks.

The BoE meets tomorrow and is expected to hold rates steady, but the August CPI figures will feed into the debate over November’s decision. Softer core and services readings suggest disinflationary progress is intact, leaving policymakers room to consider another rate cut if incoming data on growth and jobs reinforce the trend.

Japan August exports near flat, -13.8% US plunge balanced by other markets

Japan’s trade deficit narrowed in August to JPY -242.5B, smaller than expectations for JPY -513.6B, as exports outperformed forecasts. Overall exports dipped just 0.1% yoy to JPY 8425B, beating projections for a 1.9% yoy decline. Imports, however, fell -5.2% yoy to JPY 8668B, a steeper drop than the -4.2% yoy contraction expected.

The details highlighted stark divergences. Exports to the U.S. tumbled -13.8% yoy, the sharpest fall since February 2021, led by a -28.3% yoy plunge in autos and a -38.9% yoy drop in chipmaking equipment. By contrast, shipments to Asia rose 1.7% yoy, while exports to Western Europe jumped 7.7% yoy. Exports to mainland China slipped 0.5% yoy, though shipments to Hong Kong surged 14.4% yoy.

Australia leading index turns below trend, but RBA to wait until November to cut again

Australia’s Westpac Leading Index growth rate slipped into negative territory in August, falling from 0.11% to -0.16%. It marks the first below-trend reading since September 2024 and a sharp moderation from February’s peak of 0.86%.

Westpac noted the weakness is “not overly concerning” but highlights a “clear softening” from earlier in the year, consistent with the economy slowing after a relatively strong June quarter. It expects growth of 1.9% in 2025, better than the 1.3% expansion in 2024 but still below trend, with a return to trend pace only in 2026.

The RBA meets on September 29–30, where policymakers are almost certain to hold the cash rate steady at 3.6%. Westpac argues that incoming data should eventually validate benign inflation and soft demand, paving the way for a 25bp cut in November, followed by two further cuts in 2026. For now, the RBA will proceed cautiously, watching for confirmation of underlying trends before easing again.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3721; (P) 1.3752; (R1) 1.3770; More...

Outlook in USD/CAD is unchanged and intraday bias stays neutral. On the downside, firm break of 1.3725 support will complete a head and shoulder top (ls: 1.3878, h: 1.3923, rs: 1.3889). That would indicate that corrective rebound from 1.3538 has already completed, and turn near term outlook bearish. Deeper fall should then be seen to 1.3574 support. On the upside, however, break of 1.3923 will resume the rebound towards 1.4014 cluster resistance.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

BoC cuts to 2.50%, warns trade shocks still a drag

The BoC lowered its overnight rate by 25bps to 2.50% at today’s meeting, in line with widespread expectations. The move underscores the central bank’s effort to provide additional support as Canada’s economy struggles with weaker growth and softer inflation risks.

In its statement, the Governing Council said a “weaker economy and less upside risk to inflation” justified the cut, helping to better balance risks. The Bank highlighted that shifts in global trade continue to “add costs” even as they “weigh on economic activity.”

Looking ahead, policymakers said they will be closely monitoring how U.S. tariffs and evolving trade relationships affect exports, investment, employment, and household spending. They also flagged the risk that supply chain reconfiguration could pass higher costs onto consumers, stressing that inflation expectations remain a key guide for future decisions.

Bank of Canada lowers policy rate to 2½%

The Bank of Canada today reduced its target for the overnight rate by 25 basis points to 2.5%, with the Bank Rate at 2.75% and the deposit rate at 2.45%.

After remaining resilient to sharply higher US tariffs and ongoing uncertainty, global economic growth is showing signs of slowing. In the United States, business investment has been strong but consumers are cautious and employment gains have slowed. US inflation has picked up in recent months as businesses appear to be passing on some tariff costs to consumer prices. Growth in the euro area has moderated as US tariffs affect trade. China’s economy held up in the first half of the year but growth appears to be softening as investment weakens. Global oil prices are close to their levels assumed in the July Monetary Policy Report (MPR). Financial conditions have eased further, with higher equity prices and lower bond yields. Canada’s exchange rate has been stable relative to the US dollar.

Canada’s GDP declined by about 1½% in the second quarter, as expected, with tariffs and trade uncertainty weighing heavily on economic activity. Exports fell by 27% in the second quarter, a sharp reversal from first-quarter gains when companies were rushing orders to get ahead of tariffs. Business investment also declined in the second quarter. Consumption and housing activity both grew at a healthy pace. In the months ahead, slow population growth and the weakness in the labour market will likely weigh on household spending.

Employment has declined in the past two months since the Bank’s July MPR was published. Job losses have largely been concentrated in trade-sensitive sectors, while employment growth in the rest of the economy has slowed, reflecting weak hiring intentions. The unemployment rate has moved up since March, hitting 7.1% in August, and wage growth has continued to ease.

CPI inflation was 1.9% in August, the same as at the time of the July MPR. Excluding taxes, inflation was 2.4%. Preferred measures of core inflation have been around 3% in recent months, but on a monthly basis the upward momentum seen earlier this year has dissipated. A broader range of indicators, including alternative measures of core inflation and the distribution of price changes across CPI components, continue to suggest underlying inflation is running around 2½%. The federal government’s recent decision to remove most retaliatory tariffs on imported goods from the US will mean less upward pressure on the prices of these goods going forward.

With a weaker economy and less upside risk to inflation, Governing Council judged that a reduction in the policy rate was appropriate to better balance the risks. Looking ahead, the disruptive effects of shifts in trade will continue to add costs even as they weigh on economic activity. Governing Council is proceeding carefully, with particular attention to the risks and uncertainties. Governing Council will be assessing how exports evolve in the face of US tariffs and changing trade relationships; how much this spills over into business investment, employment, and household spending; how the cost effects of trade disruptions and reconfigured supply chains are passed on to consumer prices; and how inflation expectations evolve.

The Bank is focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval. We will support economic growth while ensuring inflation remains well controlled.

Information note

The next scheduled date for announcing the overnight rate target is October 29, 2025. The Bank’s October Monetary Policy Report will be released at the same time.

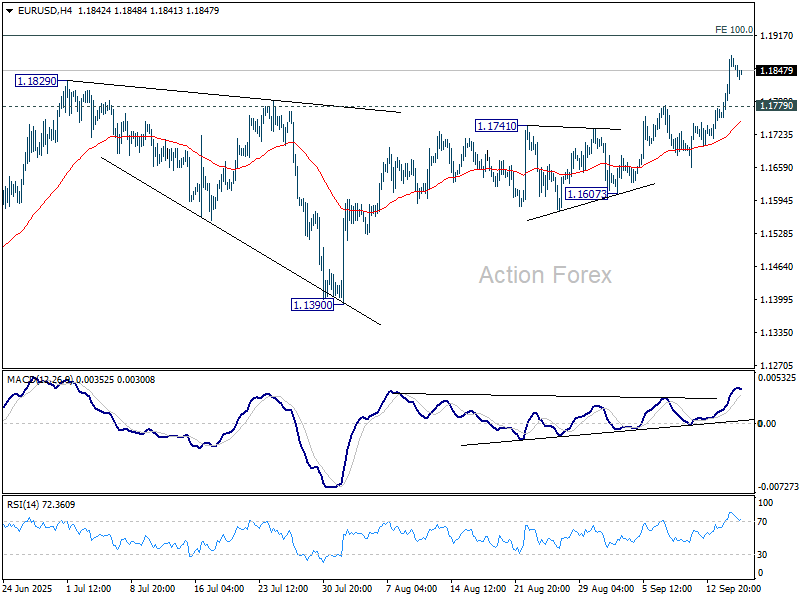

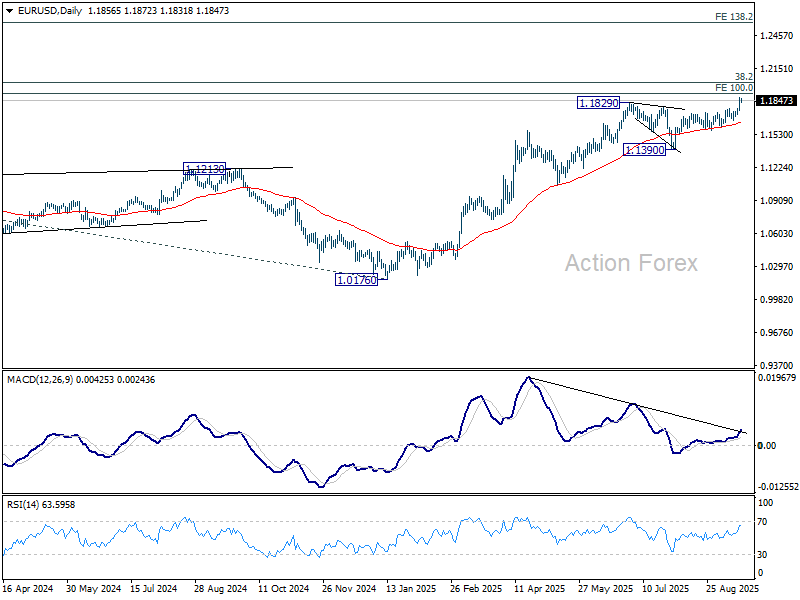

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1790; (P) 1.1834; (R1) 1.1911; More...

Intraday bias in EUR/USD remains on the upside for the moment. Current up trend should target 1.1916 projection, and then 1.2 psychological level. On the downside, below 1.1779 minor support will turn intraday bias neutral again first.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Sustained break of 1.2 psychological level will carry larger bullish implications. Next target is 138.2% projection at 1.2581. This will remain the favored case as long as 55 W EMA (now at 1.1215) holds.

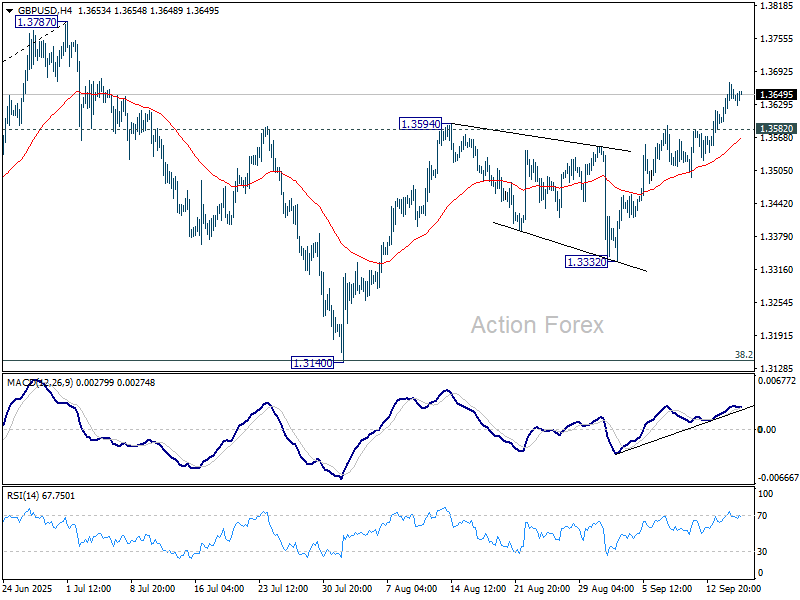

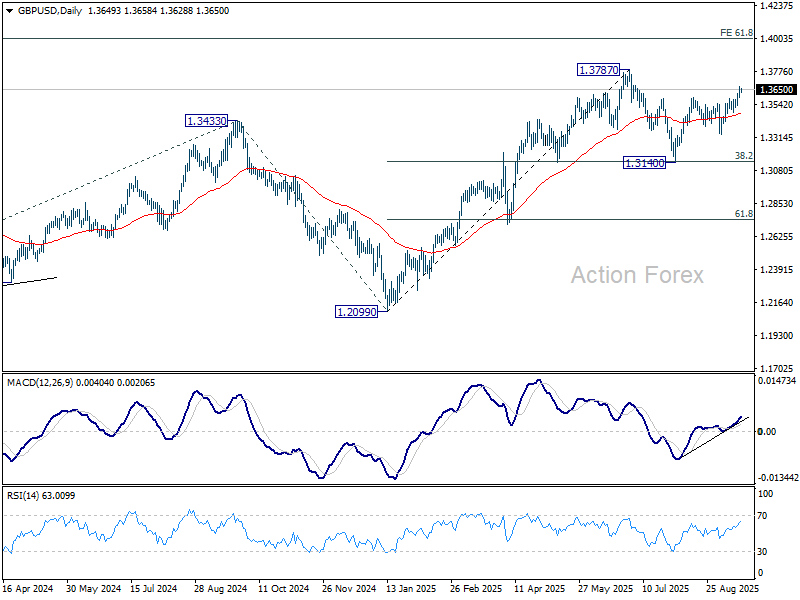

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3604; (P) 1.3638; (R1) 1.3680; More...

No change in GBP/USD's outlook and intraday bias stays on the upside. Current rise from 1.3140 is in progress and should target a retest on 1.3787 high. Decisive break there will resume larger up trend to 1.4004 projection level. On the downside, below 1.3582 minor support will turn intraday bias neutral first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

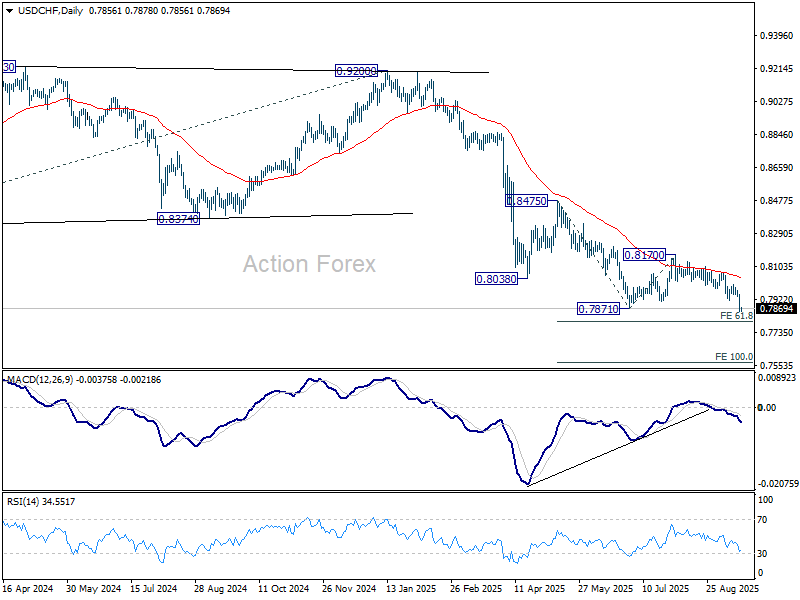

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7827; (P) 0.7888; (R1) 0.7920; More….

Intraday bias in USD/CHF stays on the downside for the moment. Current down trend should target 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. Firm break there will pave the way to 100% projection at 0.7566. On the upside, 0.7914 support turned resistance will turn intraday bias neutral for consolidations But recovery should be limited below 0.8006 resistance to bring another fall.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

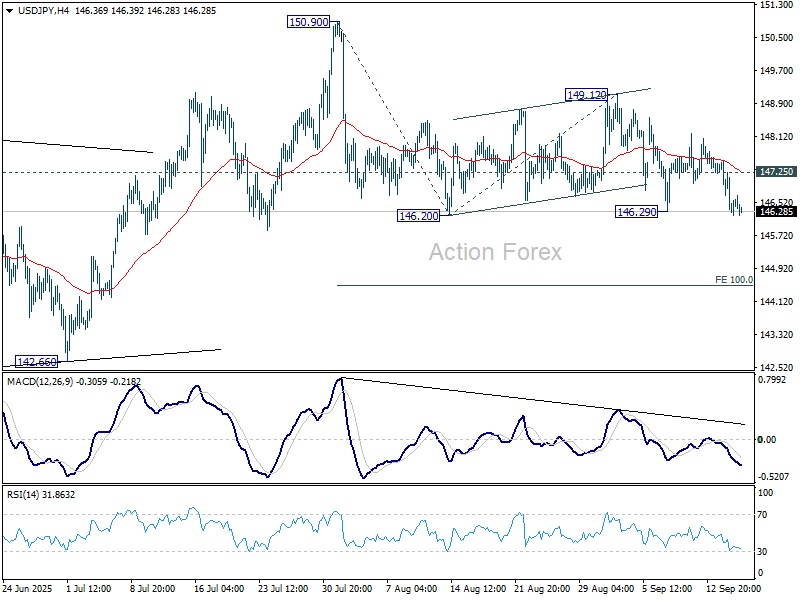

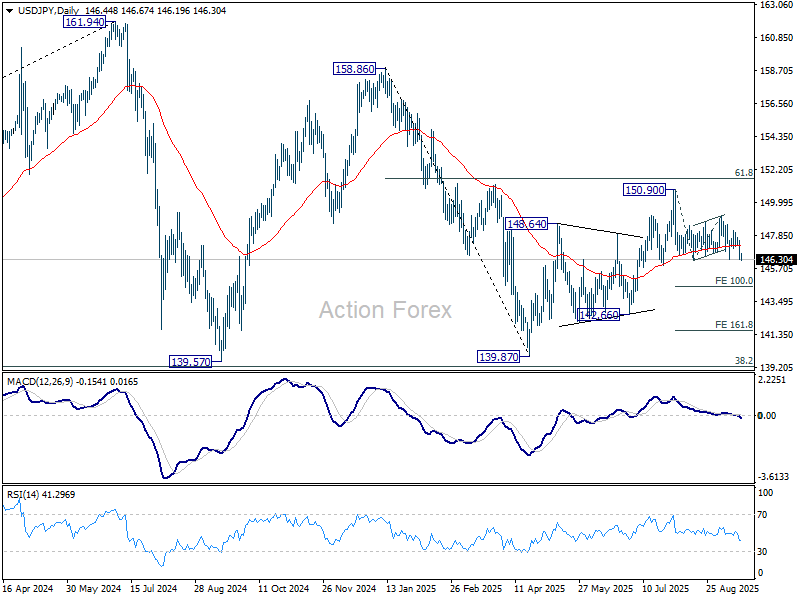

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.98; (P) 146.76; (R1) 147.24; More...

Intraday bias in USD/JPY remains on the downside for the moment. Sustained trading below 146.29 will solidify the case that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 100% projection of 150.90 to 146.20 from 149.12 at 144.42. On the upside, above 147.25 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

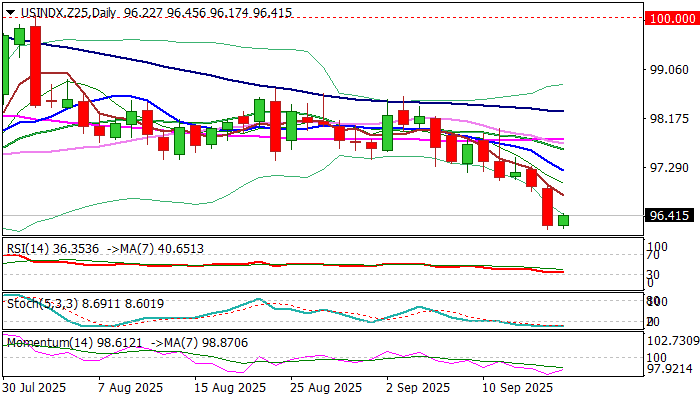

Dollar Index: Bears May Accelerate If Fed Signals a Start Policy Easing Cycle

Bears take a breather above new 11-week low on Wednesday, as markets await the verdict from Fed at the end of two-day policy meeting.

The dollar index extended the bear-leg from early Aug peak at 100 zone, a part of larger downtrend from early January peak at 110.00 (down around 12% for the year) and registered 1% loss in in the latest acceleration lower in past two days.

Wide expectations for Fed’s 0.25% rate cut today and high probability that the central bank would keep dovish stance and remain on track for further policy easing in coming months, added to factors that continued to pressure the US dollar.

Today’s upticks should stay capped under 96.80/97.20 zone (former low of July 24 / falling 10DMA) to keep broader bears intact.

Bears eye key support at 95.97 (2025 low, posted on July 1), loss of which will confirm a completion of 95.97/100.04 corrective phase and signal continuation of larger downtrend and expose immediate target at 95.18 (Fibo 76.4% of 89.15/114.72 uptrend.

Stronger acceleration lower cannot be ruled out (depending on Powell’s rhetoric) and may unmask psychological 90.00 level and 89.15 (2021 low).

Daily studies remain in full bearish configuration (boosted by the latest 20/55DMA bear cross) and support negative scenario, although oversold conditions should not be ignored.

Res: 96.82; 97.21; 97.42; 97.61.

Sup: 96.16; 95.97; 95.01; 94.41.