Sample Category Title

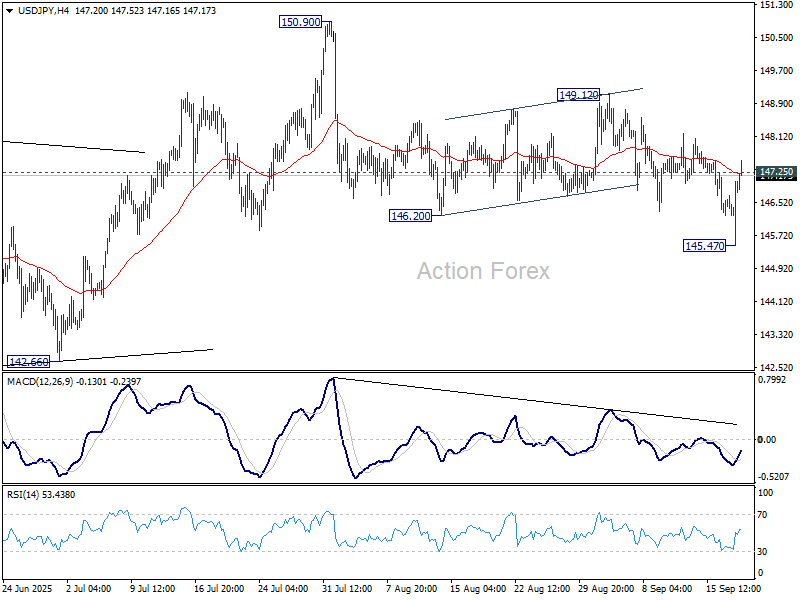

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.98; (P) 146.51; (R1) 147.54; More...

Intraday bias in USD/JPY is turned neutral with break of 147.25 minor resistance. Outlook is also mixed up by the current rebound. On the upside, break of 149.12 resistance will suggest that pullback from 150.90 has completed as a correction, and rise from 139.87 is still in progress. Further rise should then be seen back to retest 150.90 next. On the downside, below 145.47 will resume the fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

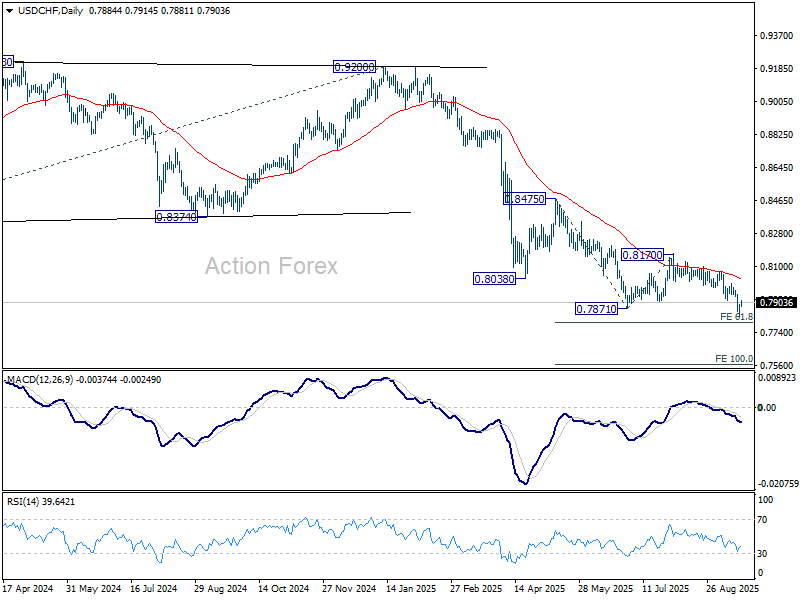

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7847; (P) 0.7871; (R1) 0.7912; More….

Intraday bias in USD/CHF is turned neutral with current recovery. Some consolidations would be seen above 0.7828 temporary low. But upside should be limited below 0.8006 resistance to bring another fall. On the downside, break of 0.7828 will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. Firm break there will pave the way to 100% projection at 0.7566.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

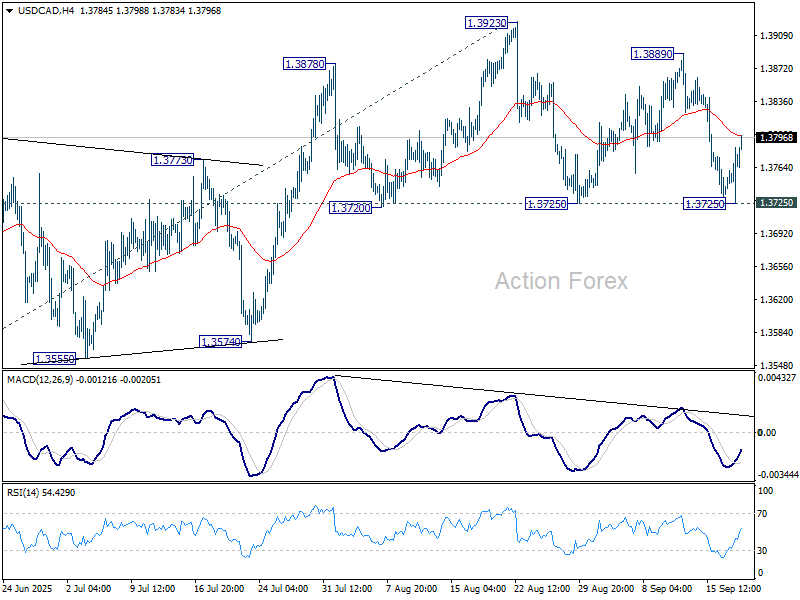

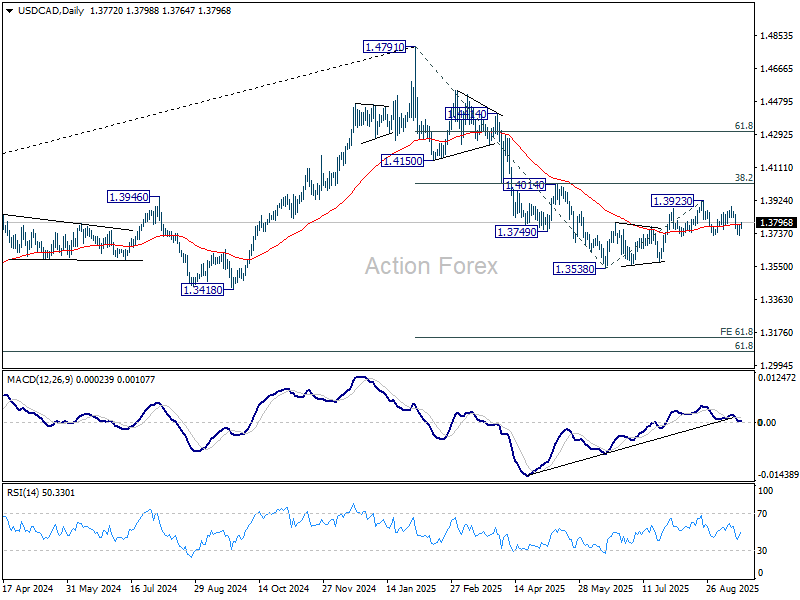

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3738; (P) 1.3763; (R1) 1.3798; More...

Intraday bias in USD/CAD stays neutral for the moment. With 1.3725 support intact, rise from 1.3538 could still extend higher. Break of 1.3889 should resume the corrective rise through 1.3923 to 1.4014 cluster resistance. On the downside, though, firm break of 1.3725 will indicate that the corrective rebound has completed, and bring deeper fall back to 1.3574 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Main Conclusion After Yesterday is We’re Lkely Up for a Very Volatile Year-end.

Markets

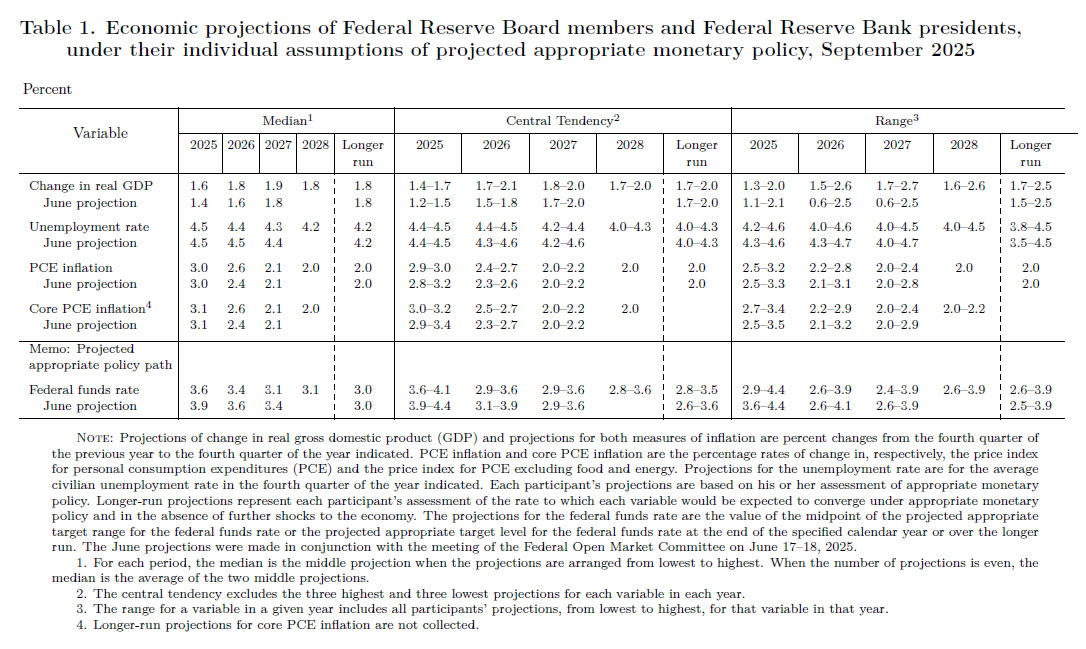

Let’s start with the numbers. In its updated quarterly Summary of Economic Projections, the US central bank raised its growth path over the 2025-2027 policy horizon from 1.4%-1.6%-1.8% to 1.6%-1.8%-1.9%. Expectations around the unemployment rate shifted from 4.5%-4.5%-4.4% to 4.5%-4.4%-4.3%. Finally, both headline and core PCE deflators are now projected at 2.6% next year instead of 2.4%. Summarizing: stronger growth, lower unemployment and higher inflation. Without additional context, this calls for raising the Fed funds rate instead of lowering it. Yet the latter was the (as expected) outcome at yesterday’s FOMC meeting. The Fed lowered its policy rate by 25 bps to 4%-4.25% after keeping it stable at 4.25%-4.50% since the start of the year. Fed Chair Powell labelled the rate cut as a “risk management decision”. Compared with the July policy statement and in line with the pivot made by Powell at the Jackson Hole conference, the Fed now judges that downside risks to employment have risen. In light of that shift in balance from “attentive to the risks to both sides of its dual mandate”, the committee almost unanimously decided to lower the Fed funds rate. It’s a strong signal from within the Fed that governors back Powell and push back against any political attempts to manipulate the independent central bank. Only President Trump’s recently installed Fed governor Miran voted in favour of a 50 bps rate cut. The median estimate for the end-of-year Fed Funds rate now stands at 3.5%-3.75% from 3.75%-4% in June. Powell stressed that this median hides a split between 9 governors in favour of back-to-back action in October and December and 1 (Miran) even suggesting an additional 125 bps split over those two meetings and 9 governors preferring either a status quo from here on (6), only one rate cut (2) or even a rate hike (1). It’s also telling that the press release didn’t hint at a continuation of gradual rate cuts if things play out as expected, suggesting that data dependency and a meeting-by-meeting approach is more than ever name of the game. Given the new risk assessment, we think that disappointing labour market data carry a bigger weight than upward inflation surprises. We don’t draw any conclusions from median policy rate estimates for 2026 (3.25%-3.5%), 2027 (3%-3.25%) and 2028 (3%-3.25%) other than there is no willingness to get rates below a neutral 3% (only 5 out of 19 governors in 2026, 6 in 2027 and 8 in 2028). Markets initially reacted in dovish fashion after the median 2025 estimate confirmed a scenario of two more 25 bps rate cuts this year. EUR/USD set a new YTD top at 1.1919, but returned back to the 1.18 area after US Treasuries changes tack. US yield eventually added 4.2 bps (30-yr) to 6.9 bps (5-yr) with the 2-y and 10-y yields bouncing off technical support at respectively 3.5% and 4%. The main conclusion after yesterday is that we’re likely up for a very volatile year-end.

News & Views

After pausing since April, the Bank of Canada (BoC) cut its policy rate by 25 bps to 2.5% yesterday. The BoC sees further weakness in the economy after growth contracted by about 1% in Q2 as exports and investment heavily weighed on growth. Employment recently declined mainly due to job losses in trade-sensitive sectors, but job growth also slowed in the rest of the economy. The BoC expects slow population growth and weakness in the labour market to weigh on household consumption in the months ahead. CPI inflation was 1.9% in August and measures of core inflation were near 3%, but the BoC assess underlying inflation to be closer to 2.5%. The combination of weaker growth and less upside inflation risks justified yesterday’s rate cut. The MPC concludes that it will carefully proceed, with particular attention to risks and uncertainties, without giving concrete guidance on the next policy step. Markets still discount a final cycle cut by early next year.

The Brazilian central bank kept its policy rate unchanged at 15% and stuck with a rather hawkish bias by saying that in the current context of heightened uncertainty, the committee “will remain vigilant”. They will not hesitate to resume the hiking cycle if appropriate. The economy shows some moderation in growth, but the labor market is still strong. Headline inflation and measures of underlying inflation remain above the 3% inflation target and the central bank expects inflation at 3.4% in Q1 2027. Also inflation expectations remain too high, requiring a significantly contractionary monetary policy for a prolonged period. The Brazilian real yesterday finished the session near the strongest level against the dollar since June last year.

Less Dovish, More Reassuring

The Federal Reserve (Fed) started cutting rates yesterday, delivering a widely expected 25bp reduction. The new dot plot shows a median projection of two more 25bp cuts this year and one additional cut in 2026. But the details matter: six members expect no further change, two even pencilled in a rate hike, while nine members see more than just a quarter-point of easing next year, with two of them projecting cuts of up to a full percentage point. In short, the median suggests that Trump won’t get the deep cuts he’s called for — the Fed is not bowing to political pressure.

That’s reassuring. Reassuring because:

- The Fed remains independent and data-driven. It acknowledged slowing job gains (with a 900k downside revision to NFP figures) but also noted that unemployment remains low, while inflation “moved up and remains somewhat elevated.”

- The Fed doesn’t see a major economic downturn. On the contrary, it revised growth and inflation forecasts higher as it announced the first of a series of rate cuts.

Markets weren’t sure how to take the news. The S&P 500 swung before closing just 0.1% lower. The Russell 2000 surged but erased most of its gains, leaving behind a shooting star candlestick. The US 2-year yield rebounded and the dollar index bounced from a fresh yearly low. Today’s session will be key to gauge whether risk appetite holds. Early signs are positive: US and European futures point higher, suggesting that a reasonably dovish Fed, combined with stronger earnings prospects, looser financial conditions and a weaker dollar, keeps risk assets in a sweet spot.

But geopolitical risks are never far. Just as Nvidia looked set to move past China’s regulatory hurdles — having agreed to a 15% licensing fee to secure export approvals — Beijing went a step further: instructing Alibaba and ByteDance to terminate their orders for Nvidia’s chips. That could cost Nvidia between $300m–$1bn in annual revenue. No surprise, the stock dropped more than 2.5%, breaking below its 50-day moving average. A deeper correction could be in the cards unless the narrative shifts.

Asian markets cheered the Fed’s cut. The Nikkei 225 rose 1.3% to a fresh ATH despite political uncertainties in Tokyo. The CSI 300 hit its highest level since March 2022, while the Hang Seng index briefly touched a four-year high. The Kospi also advanced to a record.

Elsewhere, the Bank of Canada (BoC) followed the Fed with its own 25bp cut, helping the TSX hold near all-time highs. But today’s Bank of England (BoE) decision will be the opposite story: rates are expected to stay on hold, with the UK facing slowing growth, sticky inflation and political/budget worries. Sterling is already under pressure against both the dollar and the euro. The BoE’s hawkish divergence, however, doesn’t appeal to traders: the BoE’s cautious tone isn’t backed by growth momentum. With the US dollar poised for a rebound as crowded shorts likely to be unwound, yesterday’s peak in Cable could mark the start of a move toward 1.31–1.33 over the next six weeks. Against the euro, sterling is also set to weaken. As for the EURUSD, the 1.20 handle — if reached — may act as solid resistance. The Fed’s stance reassures dollar bulls that policy isn’t politically captured, opening space for a medium-term dollar recovery cycle, even if the longer-term outlook remains bearish amid trade tensions, geopolitics and US debt concerns.

As such, gold is offered near ATH and silver is down for a third straight session. Both risk further short-term correction if the dollar strengthens. Crude oil remains capped near $65/bbl, with dollar strength limiting upside. A sustained break out of the $62–65/bbl range doesn’t look likely this week.

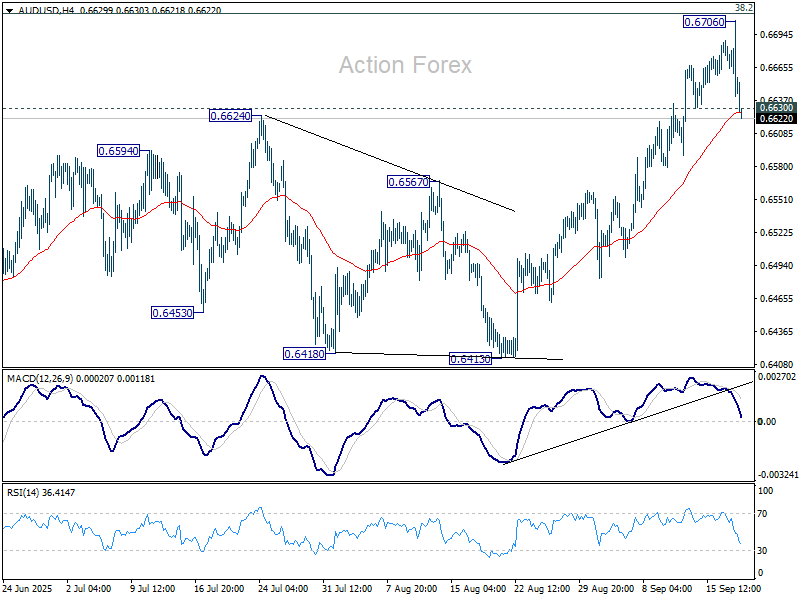

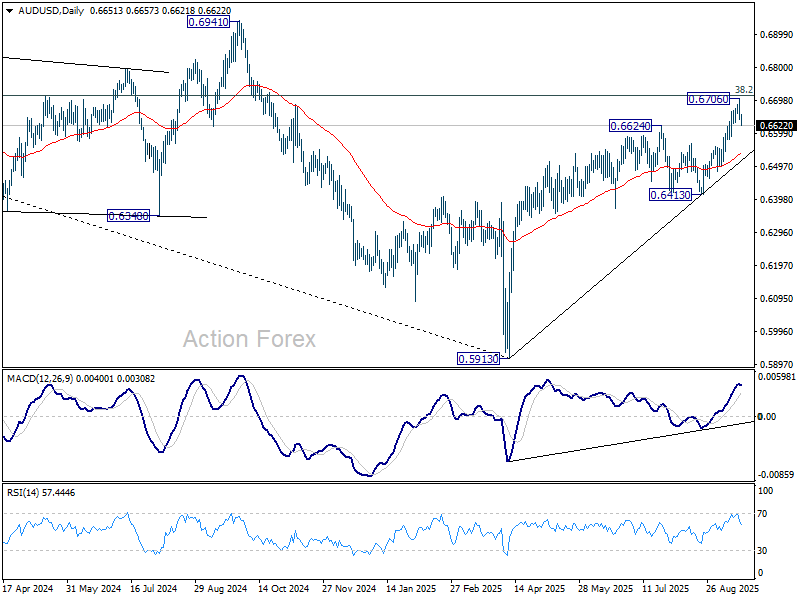

AUD/USD Daily Report

Daily Pivots: (S1) 0.6626; (P) 0.6667; (R1) 0.6692; More...

Intraday bias in AUD/USD is turned neutral first with break of 0.6630 minor support. Some consolidations would be seen, but further rally is expected as long as 55 D EMA (now at 0.6539) holds. Decisive break of 0.6713 fibonacci level will carry larger bullish implications. However, sustained break of 55 D EMA will confirm short term topping and rejection by 0.6713. Deeper fall should then be seen back to 0.6413 support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

Dollar Finds Relief from Fed, Kiwi Crashes on GDP, BoE Next

Volatility surged overnight as markets digested the Fed’s 25bps cut and updated projections. The Dollar initially sank on confirmation of two more cuts this year, only to rebound sharply as traders judged the overall stance less dovish than expected. The reversal pulled Wall Street and Gold lower from record levels, while 10-year yields firmed after briefly dipping under 4%.

The rebound in the greenback suggests the worst of the selling pressure may have passed for now, though it remains too early to call a trend reversal. Much will depend on whether incoming U.S. data validate the Fed’s relatively upbeat growth and employment forecasts. Any downside surprises could quickly reignite selling pressure.

In the Asia-Pacific, the spotlight was on New Zealand, where GDP contracted much deeper than expected in Q2. The breadth and depth of weakness spurred calls for deeper RBNZ easing. The central bank’s projection of an OCR at 2.50% by year-end looks increasingly conservative, with Westpac and others arguing that faster and deeper cuts are warranted.

Australia added to the gloom with softer labour market figures, with sharp decline in full-time positions. While the RBA is still expected to hold rates at 3.60% later this month, the probability of a November cut has clearly increased as labour market cracks widen.

As a result, Dollar currently leads the performance board for the day so far, followed by the Loonie and Sterling. At the bottom, Kiwi remains the weakest, trailed by Aussie and Swiss Franc, with Euro and Yen holding middle ground.

Attention now turns to the BoE, where a hold at 4.00% is widely expected. The latest UK CPI showed headline inflation steady at 3.8% in August—almost double the BoE’s 2% target—while wage growth remains firm despite signs of a softening jobs market. The persistence of price pressures has left policymakers cautious about cutting too quickly.

The outlook beyond September is less clear. Markets remain divided over whether the BoE will cut again in November. Governor Andrew Bailey has already warned of “considerably more doubt about exactly when and how quickly” further easing might occur, noting that investors have started to internalize this slower trajectory. Today’s decision and guidance will be pivotal in shaping expectations heading into year-end.

In Asia, at the time of writing, Nikkei is up 1.27%. Hong Kong HSI is down -0.88%. China Shanghai SSE is down -0.18%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.006 at 1.598. Overnight, DOW rose 0.57%. S&P 500 fell -0.10%. NASDAQ fell -0.33%. 10-year yield rose 0.050 to 4.076.

Fed less dovish than expected, Gold risks deeper pullback

The FOMC’s rate cut overnight initially pressured Dollar and Treasury yields lower, while Gold surged to new records. But sentiment quickly reversed as markets interpreted the decision and projections as less dovish than hoped. The Dollar rebounded, 10-year yields recovered after slipping below 4%, and Gold retreated from its peak.

The turning point came from Chair Jerome Powell’s tone at the press conference. He described the cut as a matter of “risk management,” not a reflection of significant economic weakness. By calling policy “more neutral,” Powell signaled the Fed’s intent to stay flexible rather than embark on aggressive easing.

There are other less dovish than expected elements too:

- The vote reinforced that cautious stance. Only newly confirmed Governor Stephen Miran dissented in favor of a larger 50bps move. Even typically dovish members Christopher Waller and Michelle Bowman sided with the majority, suggesting that the Committee remains cautious about delivering outsized easing.

- The Fed’s dot plot met market expectations by signaling two more cuts this year, in October and December. However, only one additional cut is projected in 2026 and another in 2027, showing a shallow glide path rather than a deep easing cycle.

- The projections for growth and employment painted a more confident picture. GDP forecasts were revised higher across the board, to 1.6% in 2025, 1.8% in 2026, and 1.9% in 2027. The unemployment outlook was left unchanged at 4.5% in 2025, but nudged lower to 4.4% in 2026 and 4.3% in 2027, reflecting a view of continued labor market resilience.

- On inflation, the Fed raised its 2026 core PCE forecast from 2.4% to 2.6%, signaling concern that price pressures could linger longer than previously expected.

The combination of slightly firmer growth, resilient labor markets, and sticky inflation explains the Fed’s reluctance to commit to a faster easing cycle.

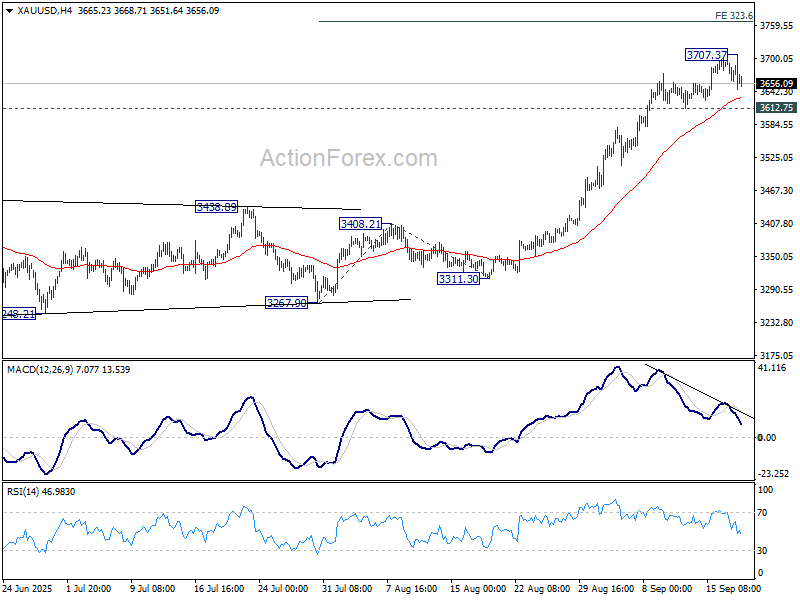

Technically, for Gold, further rise would remain in favor as long as 3612.75 support holds. But considering bearish divergence condition, strong resistance should emerge from 323.6% projection of 3267.90 to 3408.21 from 3311.30 at 3763.34 to cap upside. Meanwhile firm break of 3612.75 support will confirm short term topping, and bring deeper correction back towards 3499.79 resistance turned support.

NZ economy shrinks -0.9%, Kiwi dives on bets of 50bps RBNZ cut next

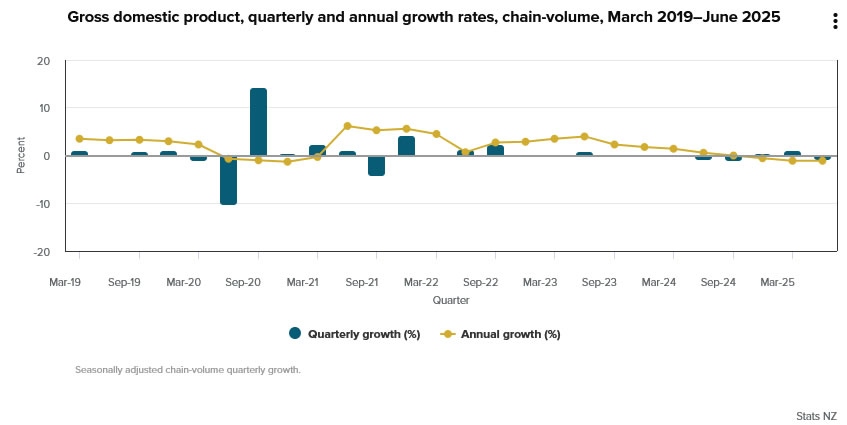

New Zealand’s economy contracted far more than expected in Q2, with GDP falling -0.9% qoq against consensus forecasts of -0.3% qoq. The release confirmed a deeper downturn, with economic activity now having declined in three of the last five quarters. The breadth of weakness points to rising headwinds that could force the RBNZ into a more aggressive easing cycle.

Goods-producing industries led the contraction with a -2.3% drop, while primary industries fell -0.7% and services output was flat. “The 0.9 percent fall in economic activity in the June 2025 quarter was broad-based with falls in 10 out of 16 industries,” said economic growth spokesperson Jason Attewell. Manufacturing was the single largest drag, contracting -3.5% in the quarter, while construction fell -1.8% following a modest rebound in Q1.

The scale of contraction triggered a wave of forecasts for deeper RBNZ easing. Westpac now expects a 50bp cut in October followed by a further 25bp reduction in November, compared with earlier projections of 25bp moves at both meetings. That would lower the OCR from the current 3.00% to 2.25% by year-end.

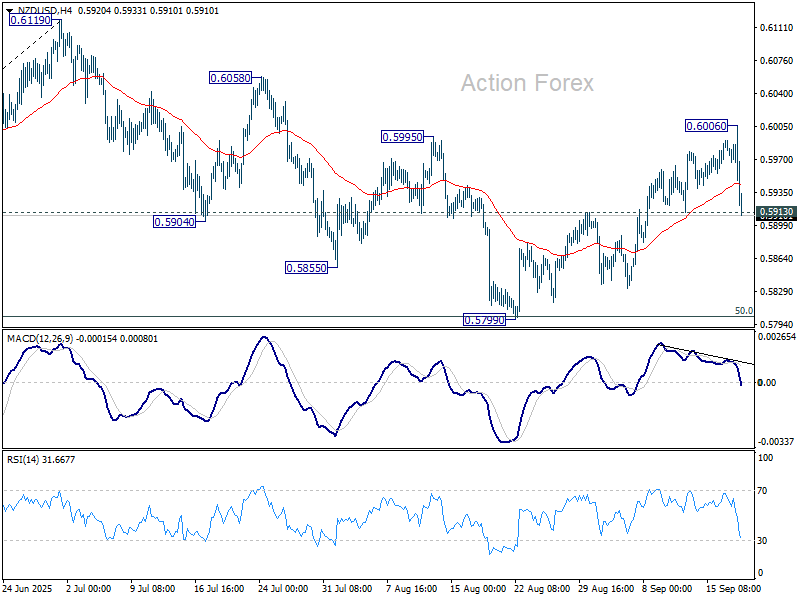

New Zealand Dollar responded by being sold off deeply after the release. Technically, immediate focus is now on 0.5913 support in NZD/USD with today's sharp fall. Firm break there will indicate that rebound from 0.5799 has completed as a corrective move to 0.6006. More importantly, that would argue that the decline from 0.6119 is not over yet, and would extend to 61.8% retracement of 0.5484 to 0.6119 at 0.57527 on resumption.

Australia jobs disappoint in August as employment falls -5.4k

Australia’s labor market weakened in August as total employment fell by -5.4k, against expectations for a 21.2k gain. The headline masked stark contrasts, with full-time jobs dropping by -40.9k while part-time roles increased by 35.5k. Hours worked fell -0.4% mom, underscoring signs of cooling demand for labor.

The unemployment rate held steady at 4.2% in line with forecasts, though the participation rate edged down to 66.8% from 67.0%. The data suggest that while unemployment remains low, underlying labor market conditions are softening.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6626; (P) 0.6667; (R1) 0.6692; More...

Intraday bias in AUD/USD is turned neutral first with break of 0.6630 minor support. Some consolidations would be seen, but further rally is expected as long as 55 D EMA (now at 0.6539) holds. Decisive break of 0.6713 fibonacci level will carry larger bullish implications. However, sustained break of 55 D EMA will confirm short term topping and rejection by 0.6713. Deeper fall should then be seen back to 0.6413 support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

Australia jobs disappoint in August as employment falls -5.4k

Australia’s labor market weakened in August as total employment fell by -5.4k, against expectations for a 21.2k gain. The headline masked stark contrasts, with full-time jobs dropping by -40.9k while part-time roles increased by 35.5k. Hours worked fell -0.4% mom, underscoring signs of cooling demand for labor.

The unemployment rate held steady at 4.2% in line with forecasts, though the participation rate edged down to 66.8% from 67.0%. The data suggest that while unemployment remains low, underlying labor market conditions are softening.

NZ economy shrinks -0.9%, Kiwi dives on bets of 50bps RBNZ cut next

New Zealand’s economy contracted far more than expected in Q2, with GDP falling -0.9% qoq against consensus forecasts of -0.3% qoq. The release confirmed a deeper downturn, with economic activity now having declined in three of the last five quarters. The breadth of weakness points to rising headwinds that could force the RBNZ into a more aggressive easing cycle.

Goods-producing industries led the contraction with a -2.3% drop, while primary industries fell -0.7% and services output was flat. “The 0.9 percent fall in economic activity in the June 2025 quarter was broad-based with falls in 10 out of 16 industries,” said economic growth spokesperson Jason Attewell. Manufacturing was the single largest drag, contracting -3.5% in the quarter, while construction fell -1.8% following a modest rebound in Q1.

The scale of contraction triggered a wave of forecasts for deeper RBNZ easing. Westpac now expects a 50bp cut in October followed by a further 25bp reduction in November, compared with earlier projections of 25bp moves at both meetings. That would lower the OCR from the current 3.00% to 2.25% by year-end.

New Zealand Dollar responded by being sold off deeply after the release. Technically, immediate focus is now on 0.5913 support in NZD/USD with today's sharp fall. Firm break there will indicate that rebound from 0.5799 has completed as a corrective move to 0.6006. More importantly, that would argue that the decline from 0.6119 is not over yet, and would extend to 61.8% retracement of 0.5484 to 0.6119 at 0.57527 on resumption.

Fed less dovish than expected, Gold risks deeper pullback

The FOMC’s rate cut overnight initially pressured Dollar and Treasury yields lower, while Gold surged to new records. But sentiment quickly reversed as markets interpreted the decision and projections as less dovish than hoped. The Dollar rebounded, 10-year yields recovered after slipping below 4%, and Gold retreated from its peak.

The turning point came from Chair Jerome Powell’s tone at the press conference. He described the cut as a matter of “risk management,” not a reflection of significant economic weakness. By calling policy “more neutral,” Powell signaled the Fed’s intent to stay flexible rather than embark on aggressive easing.

There are other less dovish than expected elements too:

- The vote reinforced that cautious stance. Only newly confirmed Governor Stephen Miran dissented in favor of a larger 50bps move. Even typically dovish members Christopher Waller and Michelle Bowman sided with the majority, suggesting that the Committee remains cautious about delivering outsized easing.

- The Fed’s dot plot met market expectations by signaling two more cuts this year, in October and December. However, only one additional cut is projected in 2026 and another in 2027, showing a shallow glide path rather than a deep easing cycle.

- The projections for growth and employment painted a more confident picture. GDP forecasts were revised higher across the board, to 1.6% in 2025, 1.8% in 2026, and 1.9% in 2027. The unemployment outlook was left unchanged at 4.5% in 2025, but nudged lower to 4.4% in 2026 and 4.3% in 2027, reflecting a view of continued labor market resilience.

- On inflation, the Fed raised its 2026 core PCE forecast from 2.4% to 2.6%, signaling concern that price pressures could linger longer than previously expected.

The combination of slightly firmer growth, resilient labor markets, and sticky inflation explains the Fed’s reluctance to commit to a faster easing cycle.

Technically, for Gold, further rise would remain in favor aslong as 3612.75 support holds. But considering bearish divergence condition, strong resistance should emerge from 323.6% projection of 3267.90 to 3408.21 from 3311.30 at 3763.34 to cap upside. Meanwhile firm break of 3612.75 support will confirm short term topping, and bring deeper correction back towards 3499.79 resistance turned support.