Sample Category Title

(BOE) Bank Rate maintained at 4%

Monetary Policy Summary, September 2025

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 17 September 2025, the MPC voted by a majority of 7–2 to maintain Bank Rate at 4%. Two members voted to reduce Bank Rate by 0.25 percentage points, to 3.75%. The Committee voted by a majority of 7–2 to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £70 billion over the next 12 months, to a total of £488 billion.

There has been substantial disinflation over the past two and a half years, following previous external shocks, supported by the restrictive stance of monetary policy. That progress has allowed for reductions in Bank Rate over the past year. The Committee remains focused on squeezing out any existing or emerging persistent inflationary pressures, to return inflation sustainably to its 2% target in the medium term.

Underlying disinflation has generally continued, although with greater progress in easing wage pressures than prices. Twelve-month CPI inflation was 3.8% in August, and is expected to increase slightly in September, before falling towards the 2% target thereafter. The Committee remains alert to the risk that this temporary increase in inflation could put additional upward pressure on the wage and price-setting process. Pay growth remains elevated, but has fallen and is expected to slow significantly over the rest of the year. Services consumer price inflation has been broadly flat over recent months. Upside risks around medium-term inflationary pressures remain prominent in the Committee’s assessment of the outlook.

Underlying UK GDP growth has remained subdued, consistent with a continued, gradual loosening in the labour market, as well as a margin of slack in the economy. Downside domestic and geopolitical risks around economic activity remain.

At this meeting, the Committee voted to maintain Bank Rate at 4%. A gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate. The restrictiveness of monetary policy has fallen as Bank Rate has been reduced. The timing and pace of future reductions in the restrictiveness of policy will depend on the extent to which underlying disinflationary pressures continue to ease. Monetary policy is not on a pre-set path, and the Committee will remain responsive to the accumulation of evidence.

Minutes of the Monetary Policy Committee meeting ending on 17 September 2025

1: Before turning to its immediate policy decisions, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP was estimated to have grown by 0.4% in 2025 Q2, a little stronger than had been assumed in the August Monetary Policy Report. Within that, euro-area GDP had expanded by 0.1% and US GDP by 0.8%. Robust US growth in Q2 had partly reflected an unwind of erratic weakness in Q1, which had been depressed by the front-loading of imports in anticipation of US tariff announcements. US final private domestic demand, which abstracted from some of the volatility associated with trade, had expanded by 0.5% in Q2, accounted for by robust business investment.

3: The euro-area and US labour markets had remained close to balance. The notable slowing in US employment growth this year appeared to have largely reflected lower labour supply growth. That was consistent with the relative stability of the US unemployment rate over this period, albeit suggesting increasing upside risks to US unemployment looking ahead.

4: Since the MPC’s August meeting, the US effective tariff rate had continued to rise and was now estimated to be close to 20%. The Committee discussed the extent to which higher tariff rates between the United States and its trading partners over the course of this year had impacted activity. Global growth had been resilient in recent months. This might, in part, have reflected front-loading of exports to the US, lags in the implementation of higher tariff rates, and the rerouting of some traded goods through alternative routes or to different destinations. There could also be impacts on activity from increased tariff rate dispersion between countries and across products. As such, the impact of higher tariff rates could be slower, although not necessarily smaller, than previously assumed.

5: Recent indicators suggested that the outlook for global growth in 2025 Q3 would be slightly stronger than had been assumed in the August Report. Looking further ahead, geopolitical risks around economic activity remained and the outlook for global trade policy continued to be highly uncertain. Aspects of US tariff policies were facing domestic legal challenge in coming weeks. Trade policy uncertainty was estimated to have increased slightly since the Committee’s August meeting, albeit it was still significantly lower than earlier in the year.

6: Twelve-month HICP euro-area inflation was unchanged at 2.0% in August, with core inflation remaining at 2.3%. Twelve-month US CPI inflation had increased to 2.9% in August from 2.7% in July, with core inflation remaining at 3.1%.

Monetary and financial conditions

7: UK financial conditions were a little tighter compared with those at the time of the MPC’s previous meeting. This had largely reflected a shift up in the market-implied path for Bank Rate, and some appreciation in the sterling effective exchange rate, with slightly higher equity prices providing a limited offset. It was too soon to see a material impact of either the shift in the market-implied path or August’s Bank Rate reduction on the lending rates offered by banks to households and corporates, given the usual lags. More generally, annual growth in aggregate broad money had remained in line with the rate seen in 2025 so far.

8: Market participants had attributed the rise in UK short-term interest rates to the Committee’s August and subsequent communications, alongside UK data developments. In contrast, the rise in longer-maturity gilt yields over the same period had been accounted for by global factors to a greater degree, reflecting a continued increase in term premia that was in large part related to the fiscal outlook in advanced economies.

9: At its meeting on 11 September, the European Central Bank Governing Council had maintained its deposit facility rate at 2%, in line with market expectations. At its meeting ending on 17 September, the Federal Reserve’s Federal Open Market Committee was expected to reduce the federal funds rate by 25 basis points.

10: Market expectations were for Bank Rate to remain unchanged at this meeting. In the Bank’s latest Market Participants Survey (MaPS), the distribution of Bank Rate expectations had shifted upwards relative to the August survey, consistent with the relatively shallower profile of cuts implied by market pricing.

11: The vast majority of MaPS respondents expected the overall pace of reduction in the stock of UK government bond purchases held for monetary policy purposes to be slower over the coming year relative to the preceding 12 months. In recent months, the largest cluster of responses had remained in the £70 to £85 billion range, although the distribution had shifted down such that the latest median expectation was for a stock reduction of £65 billion.

Demand and output

12: UK GDP had risen by 0.3% in 2025 Q2, stronger than the 0.1% increase that had been expected in the August Monetary Policy Report. Household consumption had risen by 0.1%, while business investment had fallen by 4.0% unwinding a similar-sized increase in Q1. Government expenditure had risen by 2.0% in Q2. Within the external trade data, UK export volumes to the United States had fallen by 27% in Q2, accounted for by weakness in vehicle and metal exports.

13: The level of monthly GDP had been unchanged in July, following a 0.4% rise in June. Private-sector services activity had also been flat on the month, while manufacturing output had declined quite sharply. Export volumes to the United States had increased by 20% on the month, however, consistent with the bounce-back that was expected following the agreement of the UK-US Economic Prosperity Deal.

14: Most business surveys, which were likely to be more reflective of market sector rather than public sector output, had picked up somewhat over recent months. For example, the S&P Global UK composite PMI output index had risen to 53.5 in August, only slightly below its historical average, and accounted for by a pickup in service-sector activity. The future output PMI had also increased to close to average. Nevertheless, Agents’ intelligence suggested that business sentiment had remained low. Most contacts were not expecting any substantial pickup in activity until 2026.

15: Taken together, the steer from business surveys and other intelligence was consistent with a slight increase in the pace of underlying growth in the second half of this year, to around ¼% per quarter. This was broadly consistent with the median of the non-parametric probability distribution around 2025 Q3 GDP growth generated by Bank staff’s quantile mixed-data sampling model, although there was also a significant downside skew in that distribution.

16: Incorporating the bounce-back in trade volumes, Bank staff expected headline GDP to increase by around 0.4% in 2025 Q3, slightly stronger than the underlying trend in growth.

Supply, costs and prices

17: Consistent with the subdued outlook for activity, firms’ demand for labour and hiring intentions had softened further. Survey-based measures, such as the S&P Global UK composite PMI and the KPMG/REC Report on Jobs, indicated that hiring momentum had remained weak. The latest Agents’ intelligence pointed to an easing in recruitment difficulties and gradual reductions in employment intentions. Notwithstanding some dispersion among outturns from individual employment indicators, an estimate of underlying employment growth calculated by Bank staff had remained near zero. This weakness continued to be partly attributable to the impact of increases in employers’ National Insurance contributions (NICs), as suggested by respondents to the Decision Maker Panel (DMP) Survey.

18: The ratio of vacancies to unemployment had continued to fall below Bank staff’s estimate of its equilibrium level. Vacancies had declined in the three months to August, with falls broad-based across sectors, but at a somewhat slower pace than previously. The unemployment rate had been unchanged in the three months to July. The overall weakening in earlier-stage indicators of the tightness of the labour market were expected to lead to some modest deterioration in late-stage indicators, such as the redundancy rate, in due course. Taken together, slack was continuing to build slowly in the labour market, although with no signs currently that a sharper loosening was underway.

19: A broad set of indicators suggested that pay growth had continued to ease, although it had remained at levels above those that could be explained by economic fundamentals. Private sector regular average weekly earnings (AWE) growth had fallen to 4.7% in the three months to July, down from 4.8% in the three months to June. Higher-frequency estimates of AWE growth had continued to moderate. Median private sector pay growth derived from HMRC payrolls had also weakened in July, although to a lesser extent.

20: The latest data on pay settlements and pay expectations had remained consistent with the August Monetary Policy Report projection for a significant decline in wage growth, to around 3.8% by year-end. The latest intelligence from the Agents had continued to suggest that average pay settlements for 2025 would be in line with the range reported in the Agents’ annual pay survey and the DMP Survey. Despite the expected decline in pay growth, the impact of the increase in employers’ NICs appeared to be delaying a reduction in total labour cost growth until next year.

21: Twelve-month CPI inflation had been 3.8% in August, in line with expectations in the August Report, following 3.8% in July and 3.6% in June. This had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes. The rise in headline inflation this year was largely accounted for by increases in a range of administered prices and food prices, alongside the impact on inflation from previous falls in energy prices dropping out of the annual comparison. Core CPI inflation had been 3.6% in August, in line with expectations at the time of the August Report.

22: Core consumer goods price inflation had been 1.6% in August, with an increase in food price inflation to 5.1%. Intelligence from the Banks’ Agents pointed to higher global and domestic commodity prices as having accounted for much of the increase over the past year, with higher wholesale prices for beef, cocoa beans and coffee in particular. Labour costs and costs associated with new packaging regulation had also accounted for some of the increase in food prices.

23: Services consumer price inflation had fallen to 4.7% in August from 5.0% in July, and compared to 4.7% in May and June. This elevated level of services inflation reflected past strength in wage growth, temporary upward pressures from firms adjusting to labour costs from the employers’ NICs increase, and increases in administered prices. There had been signs of continuing disinflation in some measures of underlying services inflation.

24: CPI inflation was projected to stay around 3¾% over the second half of this year, with a temporary peak of 4.0% in September, in line with the projection in the August Report. This continued to reflect some near-term upward pressure on inflation largely from food and services prices, which was expected to be offset during 2025 Q4 by a slight decline in projected core goods and energy inflation.

25: Households’ short and medium-term inflation expectations had remained elevated relative to historical averages, likely reflecting a heightened attentiveness to the rise in headline CPI inflation in recent months, and particularly in food items. The Citi/YouGov measure of median one-year ahead inflation expectations had remained at 4.0%, while the Bank/Ipsos measure had increased to 3.6%. Both medium-term measures were elevated. In particular, the Bank/Ipsos measure had increased to a series-high of 3.8%.

26: Measures of businesses’ inflation expectations had risen to a lesser extent than household measures. According to the DMP Survey, businesses’ year-ahead own-price expectations remained at 3.7% in the three months to August, unchanged from the July outturn. Year-ahead CPI expectations had risen slightly to 3.3%.

27: Near-term inflation expectations reported in the Market Participants Survey had increased, with the median profile for CPI inflation implying a peak of 3.9% in the third quarter of this year. The median respondent had continued to expect inflation to be at the 2% target at the three-year horizon. There had been little change in medium-term UK financial market inflation compensation measures.

The immediate policy decisions

28: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

Bank Rate decision

29: The Committee’s deliberations at this meeting had focused on a number of key policy questions, including the extent of progress on underlying disinflation, and the balance between upside risks from inflation persistence and downside risks to demand and, in turn, inflation.

30: Underlying disinflation had generally continued. Pay growth remained elevated, but had fallen and was expected to slow significantly over the rest of the year. Services consumer price inflation had been broadly flat over recent months, and was likely to remain around these levels in the near term in part reflecting developments in administered prices. Continued moderation in wage growth was likely to feed through to lower total labour cost and services price inflation over time, but there was uncertainty about how long this process would take. The MPC would continue to monitor closely developments in services CPI data, other indicators of pricing intentions such as in the DMP Survey, and profit margins.

31: Twelve-month CPI inflation had been 3.8% in August, and was expected to increase slightly in September, before falling towards the 2% target thereafter. The Committee remained alert to the risk that this temporary increase in inflation could put additional upward pressure on the wage and price-setting process, including via developments in salient items such as food prices and as headline inflation was likely to stay higher for longer above the 2% target relative to the May Monetary Policy Report. Some indicators of inflation expectations had also continued to increase over recent months, and the MPC was focused on the extent to which this could lead to renewed second-round effects. In general, upside risks around medium-term inflationary pressures remained prominent in the Committee’s assessment.

32: Underlying UK GDP growth had remained subdued, consistent with a continued, gradual loosening in the labour market, as well as a margin of slack in the economy. There remained uncertainty around the degree to which slack had opened up and would continue to build. Weak employment growth pointed to further spare capacity building and some indicators of labour demand had continued to soften. Set against that, possible structural changes in the labour market over recent years meant that sufficient slack might not have emerged to return inflation sustainably to target. There were also signs that output growth was now stronger than employment growth, alongside the possibility that adjustments in hiring related to recent increases in firms’ costs had now largely occurred.

33: As set out in Box A in the August Report, and reflecting the usual lags of policy, the past restrictiveness of the UK monetary policy stance was estimated to be weighing on the current level of demand, which would contribute to the disinflationary process. The degree of restrictiveness was, however, also estimated to have fallen over the past 18 months as Bank Rate had been reduced.

34: Downside domestic and geopolitical risks around economic activity remained. Members continued to judge that there were downside risks around consumption growth and upside risks around the path of the saving ratio, including from the risk of greater precautionary saving behaviour by households. Greater uncertainty could also lead to downside risks to business investment. There appeared, however, to be less of an immediate risk that the labour market would loosen very rapidly. Although global growth had so far been resilient, risks from trade policy developments remained and could be slower to materialise.

35: Seven members preferred to maintain Bank Rate at 4% at this meeting. Alongside a small tightening in financial conditions, there had been limited economic news since the previous MPC meeting, and these members’ views on the main risks and the required strategy to achieve the 2% target sustainably in the medium term had not changed materially. The key question for monetary policy remained whether upside risks to the continuing process of disinflation, from elevated inflation expectations and possible structural changes in price and wage-setting behaviour, could be outweighed by downside risks stemming from the potential for a more substantial weakening in demand. There remained a range of views among these members about the balance of risks to inflation, and the most important factors contributing to it.

36: Two members preferred a 0.25 percentage point reduction in Bank Rate. The disinflation process was continuing. The inflation hump was expected to normalise, with the most significant contributions coming from one-off changes in administered prices and global food inflation in a limited set of items, neither related to demand pressure. Consumer spending and investment remained subdued, while wage settlements had fallen further from around 3.5% in the first half of 2025. Along with domestic demand weakness and emerging slack, recent developments pointed to downward risks to global growth. Given this balance of risks, a less restrictive policy path was warranted to insure against an increased risk of recession, below-target inflation and a further deterioration in supply capacity.

37: The Committee judged that a gradual and careful approach to the further withdrawal of monetary policy restraint remained appropriate. The restrictiveness of monetary policy had fallen as Bank Rate had been reduced. The timing and pace of future reductions in the restrictiveness of policy would depend on the extent to which underlying disinflationary pressures would continue to ease. Monetary policy was not on a pre-set path, and the Committee would remain responsive to the accumulation of evidence.

Annual decision on the pace of reduction in the stock of UK government bond purchases held for monetary policy purposes

38: In line with the commitment made in the August 2022 MPC minutes, the Committee had again reviewed the pace of reduction in the stock of UK government bonds (gilts) held for monetary policy purposes in the Asset Purchase Facility (APF), a process known as quantitative tightening (QT).

39: QT had continued to contribute to meeting the Committee’s objective of reducing the risk of a ratchet upwards in the size of the Bank’s balance sheet over time, increasing the headroom and flexibility available to the Bank to use its balance sheet in the future if needed.

40: The MPC would continue to be guided by a set of key principles. First, the Committee intended to use Bank Rate as its active policy tool when adjusting the stance of monetary policy. Second, sales would be conducted so as not to disrupt the functioning of financial markets, and only in appropriate conditions. Third, to help achieve that, sales would be conducted in a gradual and predictable manner over a period of time.

41: The Committee had set out its latest assessment of QT in the August 2025 Monetary Policy Report. In setting Bank Rate, the MPC had taken account of financial market conditions that reflected the effects of announced and expected QT. Any tightening effect from QT would have led to a slightly lower path for Bank Rate, all else equal. Given that the impact of QT was judged to have been modest, this was unlikely to have made a material difference to the appropriate path for Bank Rate over the past year.

42: The MPC recognised that, as well as being uncertain, the effect of QT might vary over time. In common with other advanced economies, term premia on long-term government bonds had risen through 2025. That had reflected global economic policy uncertainty, high issuance of government bonds across countries and structural changes within the UK bond market that had reduced demand for long-term government debt. Although the UK gilt market had continued to function in an orderly manner, these factors could pose a risk that QT would have a greater impact on market functioning than previously.

43: Over the previous 12 months, following the MPC’s September 2024 decision about the pace of QT, the stock of gilts held for monetary policy purposes had been reduced by £100 billion, of which £13 billion had been through gilt sales.

44: At its September 2025 meeting, the Committee considered the case for the Bank to reduce the stock of UK government bond purchases held for monetary policy purposes by £70 billion from October 2025 to September 2026, of which £21 billion would be through gilt sales.

45: Seven members supported that stock reduction. A decrease in the pace of QT to £70 billion from £100 billion over the previous year, would be consistent with the MPC’s key principles and objective. This decision was made with the knowledge that the Bank would choose as part of its operational considerations to vary the maturity composition of sales, as set out in the Market Notice accompanying these Minutes.

46: One member preferred to maintain the pace of QT at £100 billion over the coming year to provide continuity and consistency in the MPC’s approach, particularly as gilt market developments had been predominantly unrelated to QT.

47: One member preferred to slow the pace of QT to £62 billion, retaining £13 billion of sales, having been informed that in this case the Bank would maintain equal proportions of sales across maturity buckets, as in previous years. Relative to the majority decision, the slower pace and balanced tenors would reduce the potential for volatility in short rates and would moderate upward pressure on the middle tenor interest rates, which was where monetary policy transmission was the strongest.

48: The Financial Policy Committee (FPC) had been briefed ahead of the MPC’s decision.

49: All MPC members reaffirmed that there would be a high bar for amending the planned reduction in the stock of purchased gilts outside a scheduled annual review. That was in order to remain consistent with the principles that Bank Rate should be the active policy tool when adjusting the stance of monetary policy, and that gilt sales undertaken through QT should be predictable. In judging whether that bar was met, the FPC would also have a role through its assessment of financial stability.

50: The Chair invited the Committee to vote on the propositions that:

- Bank Rate should be maintained at 4%; and

- The Bank of England should reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £70 billion over the next 12 months, to a total of £488 billion.

51: Seven members (Andrew Bailey, Sarah Breeden, Megan Greene, Clare Lombardelli, Catherine L Mann, Huw Pill and Dave Ramsden) voted in favour of the first proposition. Two members (Swati Dhingra and Alan Taylor) voted against this proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 3.75%.

52: Seven members (Andrew Bailey, Sarah Breeden, Swati Dhingra, Megan Greene, Clare Lombardelli, Dave Ramsden and Alan Taylor) voted in favour of the second proposition. Two members voted against this proposition. Catherine L Mann preferred a stock reduction of £62 billion. Huw Pill preferred a stock reduction of £100 billion.

Operational considerations

53: On 17 September, the stock of UK government bonds held for monetary policy purposes was £558 billion.

54: At this meeting, the MPC had voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £70 billion over the 12-month period from October 2025 to September 2026. The details of the first quarter of the associated gilt sales programme, covering 2025 Q4, were set out in a Market Notice accompanying these minutes.

55: Since gilt sales had commenced in 2022 Q4, the Bank had scheduled auctions in order to reduce the APF as evenly as possible across maturity sectors. For the year starting 2025 Q4, the Bank would aim to sell fewer long maturity sector gilts than gilts at other maturities, such that approximately 40% of the MPC’s target would be met by selling short maturity sector bonds, 40% by medium maturity sector bonds, and 20% by long maturity sector bonds, measured in initial proceeds terms. The MPC had been briefed on these operational arrangements.

56: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

Jonathan Bewes was present on 15 September, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

GBP Holds Near Highs as Market Awaits BoE Decision

The GBP/USD pair stabilised around 1.3626 USD on Thursday, following a highly volatile session on Wednesday. The pair remains close to its highest level in over ten weeks, as markets await the Bank of England’s policy decision later today.

The BoE is widely expected to maintain rates at 5.25% (note: corrected from 4% based on current BoE rate) and may signal a reduction in its £100 billion annual bond-purchase program.

Recent data showed UK inflation held steady at 3.8% in August, matching both forecasts and July’s 18-month high. Labour market figures were broadly in line with expectations: unemployment remained at 4.7%, wage growth (ex-bonuses) came in at 4.8% (4.7% including bonuses), and payrolls declined by 8,000.

Market expectations for a BoE rate cut remain subdued, with only a one-in-three chance priced in for a reduction by December.

Meanwhile, the US Federal Reserve delivered a widely anticipated 25-basis-point cut yesterday, with traders now expecting at least two additional cuts by the end of 2025.

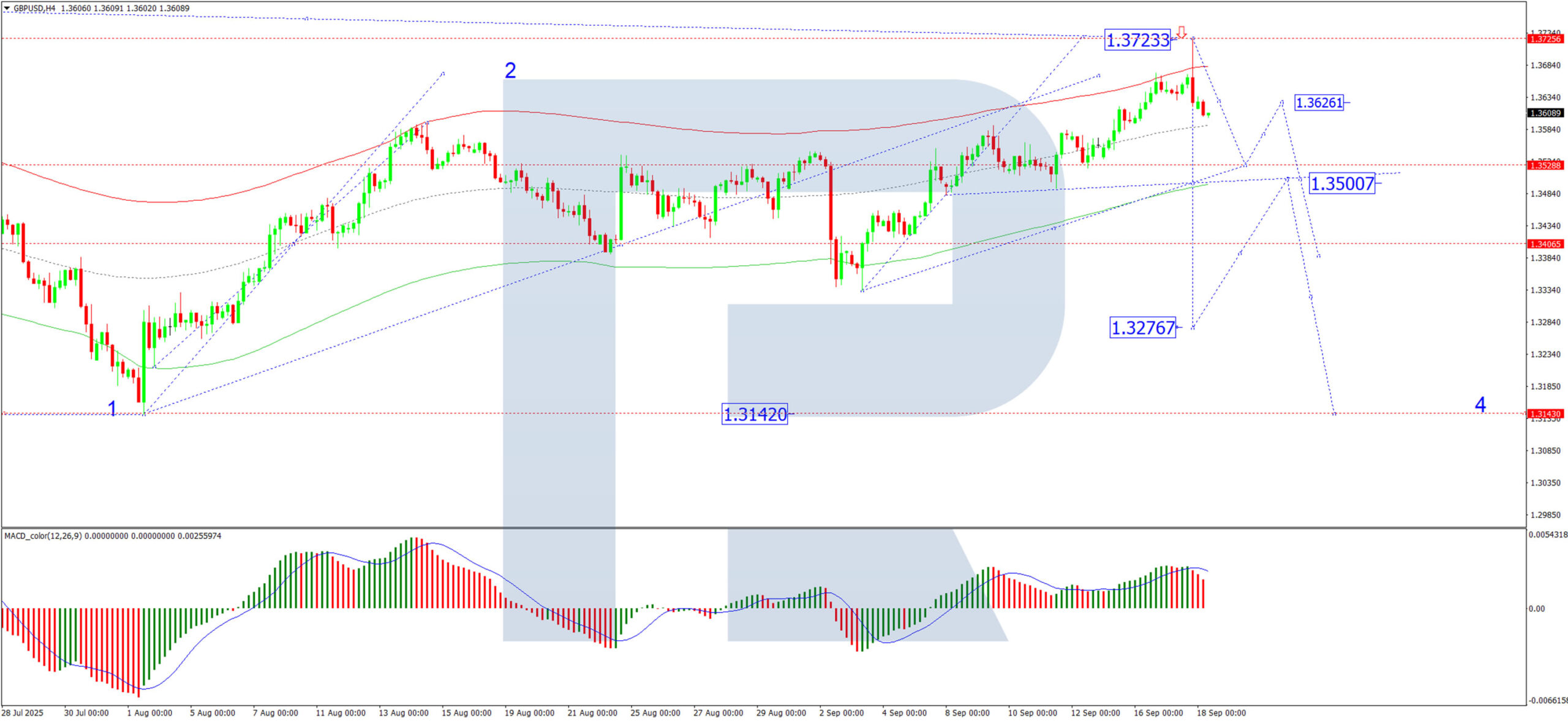

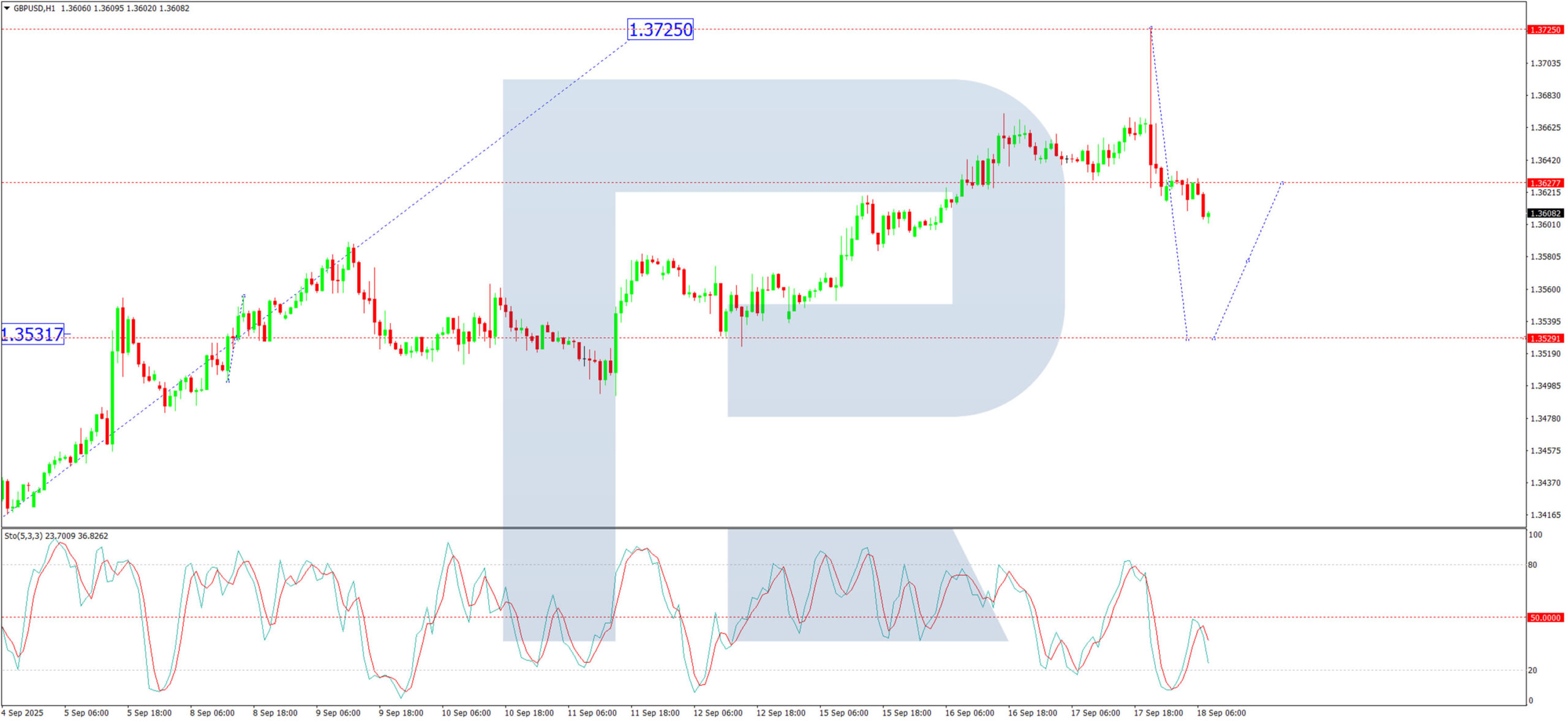

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD completed an upward move to 1.3723 USD, followed by a downward impulse to 1.3620 USD. The pair is now likely to form a consolidation range around this level. A break below 1.3620 USD could initiate a decline towards 1.3528 USD. A corrective rebound towards 1.3620 USD may then follow. Renewed selling pressure could subsequently drive the pair towards 1.3500 USD, with further downside potential to 1.3277 USD. The MACD indicator supports this outlook, with its signal line positioned above zero but turning decisively downward.

H1 Chart:

On the H1 chart, the pair has completed a downward impulse to 1.3620 USD. A consolidation phase is expected around this level. A break lower would likely trigger the first wave of a new downtrend towards 1.3530 USD. The Stochastic oscillator aligns with this near-term bearish view, as its signal line lies below 50 and is trending downward towards 20.

Conclusion

The pound is trading near multi-week highs as markets await guidance from the BoE. While UK inflation remains elevated, softening labour data and a dovish Fed have limited the GBP’s upside. Technically, the pair appears vulnerable to a near-term correction, particularly if the BoE maintains a cautious tone. Today’s decision and accompanying communications will be critical in determining whether cable extends its rally or enters a deeper corrective phase.

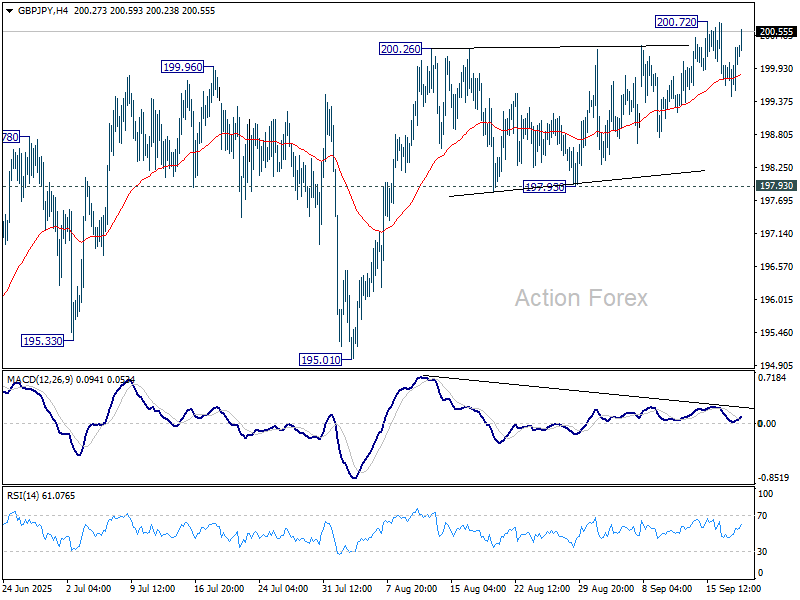

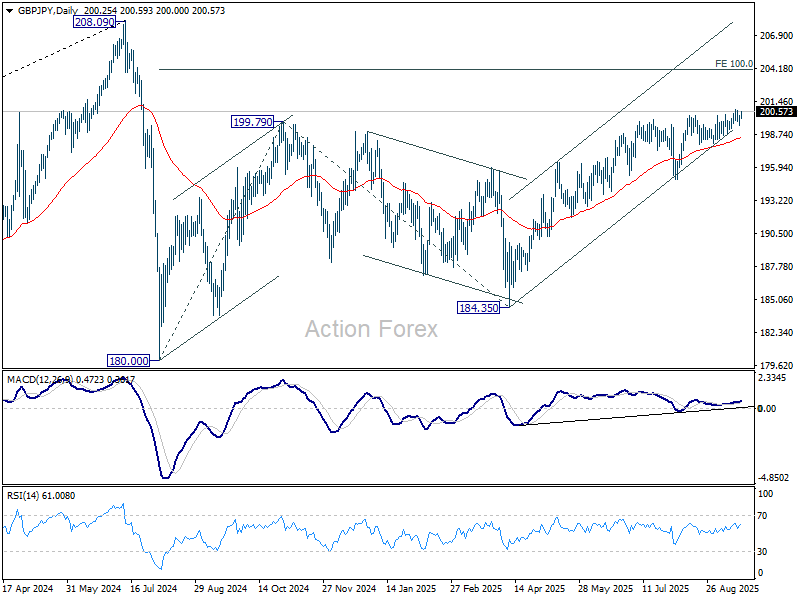

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.69; (P) 200.03; (R1) 200.57; More...

Intraday bias in GBP/JPY remains neutral and some consolidations could be seen below 200.72 temporary top. Further rise would be expected as long as 197.93 support holds. Firm break of 200.32 will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. However, considering bearish divergence condition in both D and 4H MACD, firm break of 197.93 will indicate bearish reversal and bring deeper fall back to 195.01 support first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

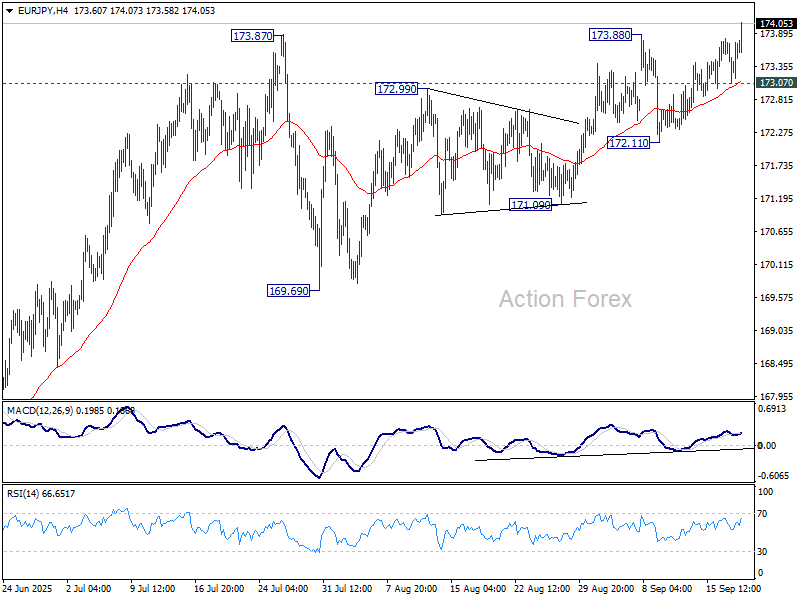

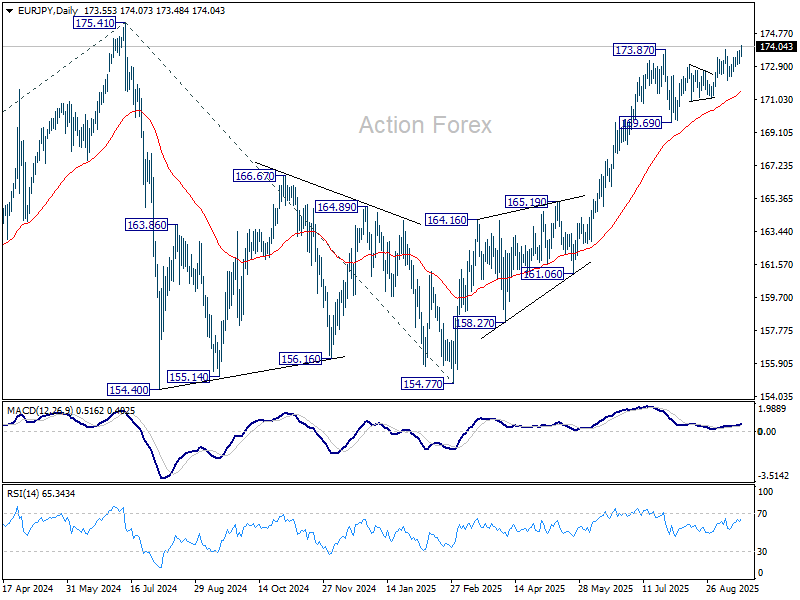

EUR/JPY Daily Outlook

Daily Pivots: (S1) 173.19; (P) 173.52; (R1) 173.95; More...

Intraday bias in EUR/JPY is back on the upside with break of 173.87/88 resistance. Rise from 154.77 is resuming and should target a retest on 175.41 high. On the downside, below 173.07 minor support will turn intraday bias neutral again first.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 169.69 support will delay this bullish case, and probably extend the correction from 175.41 with another fall.

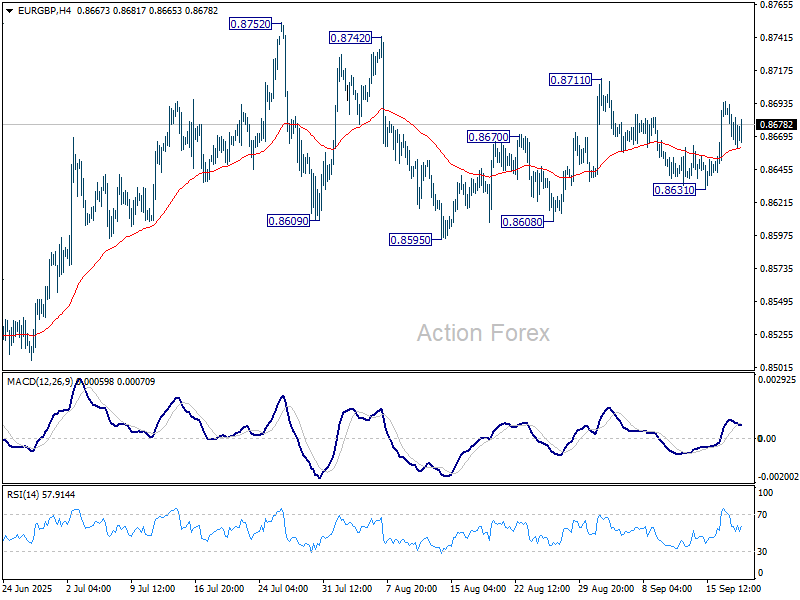

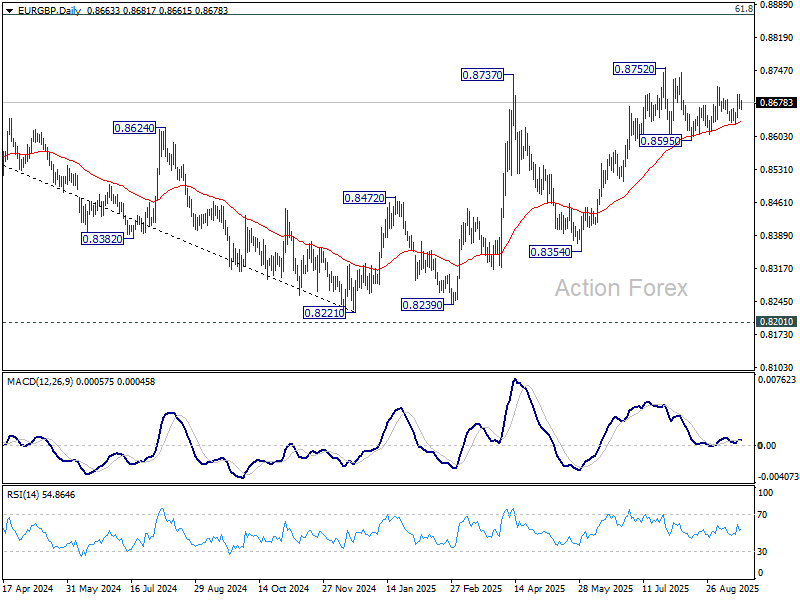

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8662; (P) 0.8680; (R1) 0.8715; More...

Intraday bias in EUR/GBP stays mildly on the upside at this point. Break of 0.8711 resistance will resume the rise from 0.8595 to retest 0.8752 high. For now, further rise is expected as long as 0.8631 support holds, in case of retreat.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.

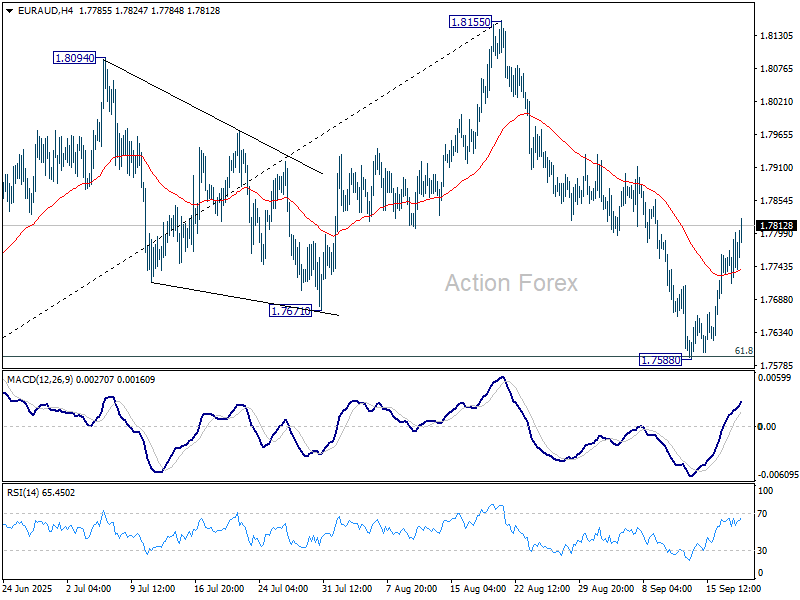

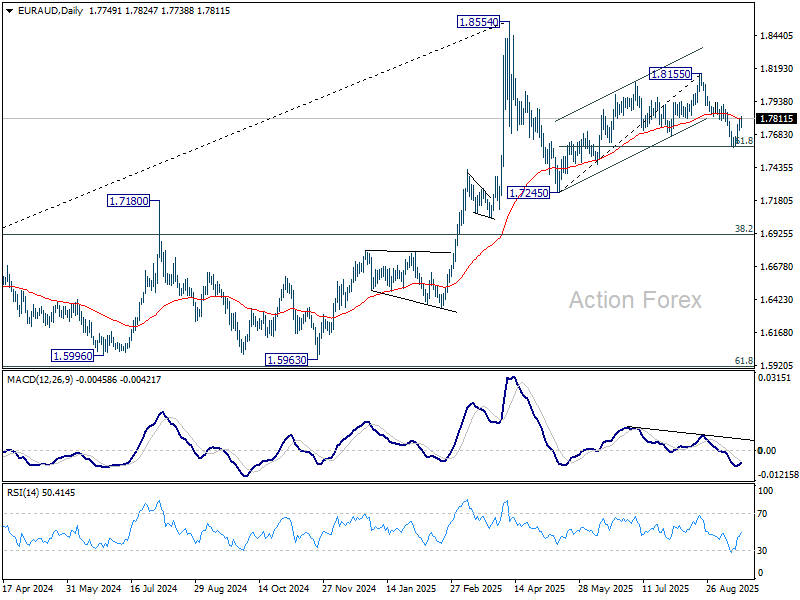

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7716; (P) 1.7759; (R1) 1.7800; More...

Intraday bias in EUR/AUD stays neutral at this point, with focus on 55 D EMA (now at 1.7808). Rejection by the EMA will maintain near term bearishness. Further break of 1.7588 support will extend the corrective pattern from 1.8554 lower gain, and target 1.7245 and possibly below. However, decisive break of the 55 D EMA will bring stronger rally back to 1.8155 resistance instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

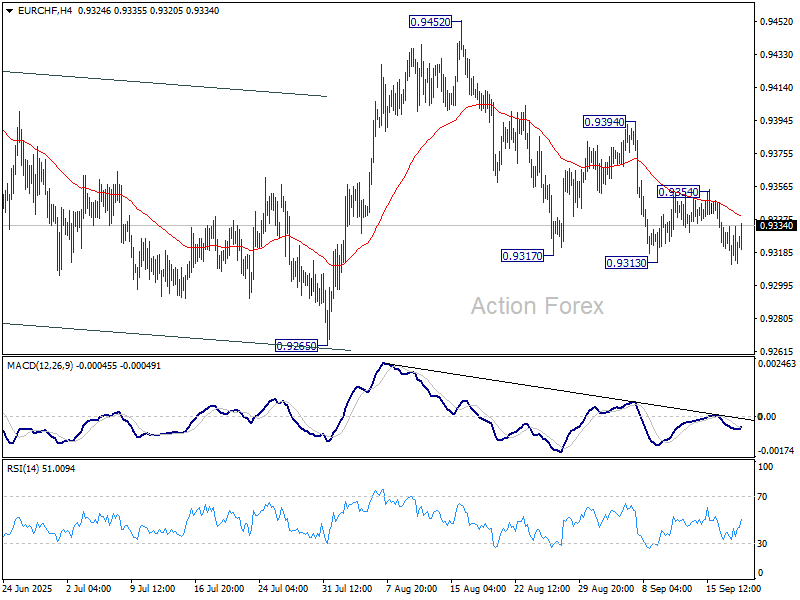

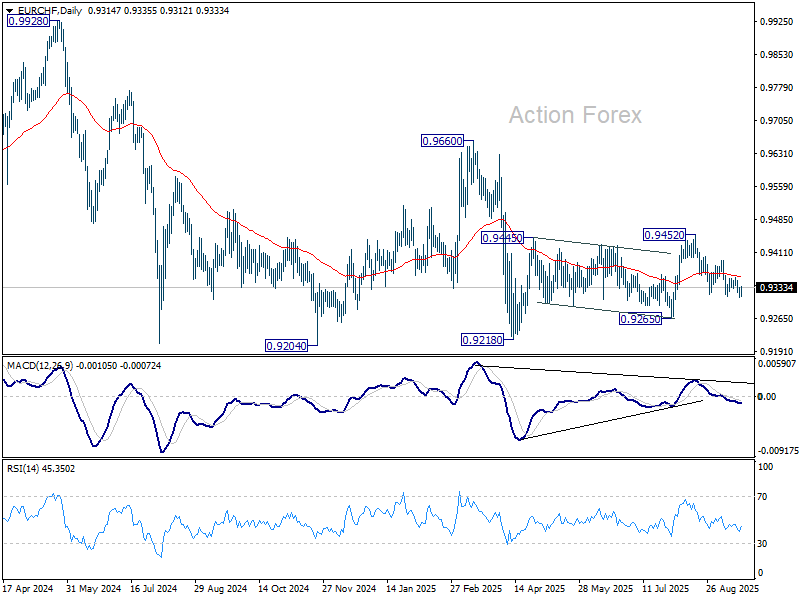

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9317; (P) 0.9334; (R1) 0.9344; More...

Range trading continues above 0.9313 and intraday bias in EUR/CHF stays neutral at this point. Further decline is expected with 0.9394 resistance intact. On the downside, break of 0.9313 will resume the fall from 0.9452 to retest 0.9218 low. On the upside, break of 0.9394 will bring stronger rally towards 0.9452 resistance instead.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

Dollar and the Pound Shift Course As Markets Assess Central Bank Decisions

The US dollar fell sharply on Wednesday following the Federal Reserve’s decision to cut rates by 0.25%. However, by the end of the session it had regained part of its losses, reflecting ongoing uncertainty over the regulator’s next moves. The pound, meanwhile, after an initial rise on the back of the weaker dollar, turned lower ahead of today’s Bank of England meeting, which could bring fresh volatility to the GBP/USD pair. The Bank of Canada meeting also added to the overall market mood, with the regulator signalling a cautious stance on future policy.

During today’s trading, the market’s attention is focused on fresh US releases: labour market data, initial jobless claims, as well as the Philadelphia Fed’s business activity index and capital expenditure figures. These numbers could either support a corrective rebound in the dollar or renew pressure if they confirm an economic slowdown. For the pound, the key drivers will be the outcome of the Bank of England’s voting and accompanying statements, with uncertainty still surrounding how far the regulator is willing to go in easing policy.

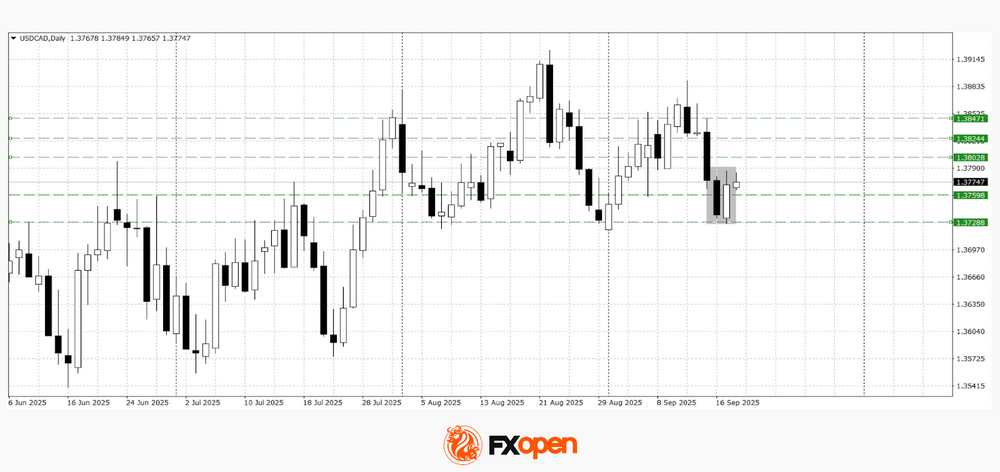

USD/CAD

Yesterday, the price tested 1.3730 and bounced sharply from that level, forming a bullish piercing line pattern. Technical analysis of USD/CAD suggests a potential continuation of the rise towards 1.3800–1.3820, in line with confirmation of the mentioned pattern. Should negative US data emerge, the pair may fall back towards 1.3730–1.3760.

Events that could influence USD/CAD’s direction:

- Today, 15:30 (GMT+3): US Initial Jobless Claims

- Today, 15:30 (GMT+3): Philadelphia Fed Manufacturing Index

- Tomorrow, 15:30 (GMT+3): Canada Core Retail Sales Index

GBP/USD

A three-day rally in GBP/USD ended with a rejection at 1.3725 and the formation of a bearish shooting star pattern. Technical analysis of GBP/USD points to a possible decline towards 1.3540–1.3560. If the pair manages to consolidate above 1.3670, yesterday’s high may be retested.

Events that could influence GBP/USD’s direction:

- Today, 14:00 (GMT+3): Bank of England Votes on Rate Cut

- Today, 14:00 (GMT+3): Bank of England Interest Rate Decision

- Today, 14:00 (GMT+3): Bank of England Monetary Policy Committee Minutes

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

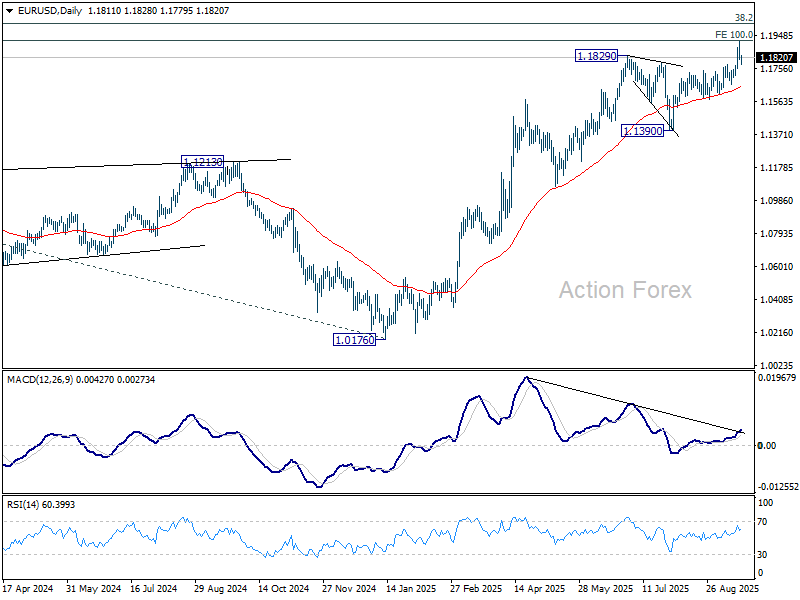

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1774; (P) 1.1847; (R1) 1.1885; More...

Intraday bias in EUR?USD is turned neutral first with current retreat. Some consolidations would be seen below 1.1917 temporary top first. Further rise is expected as long as 1.1741 resistance turned support holds. Above 1.1917 will resume larger up trend to 1.2 psychological level. However, firm break of 1.1741 should confirm short term topping, and turn bias back to the downside for 1.1607 support.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Sustained break of 1.2 psychological level will carry larger bullish implications. Next target is 138.2% projection at 1.2581. This will remain the favored case as long as 55 W EMA (now at 1.1215) holds.

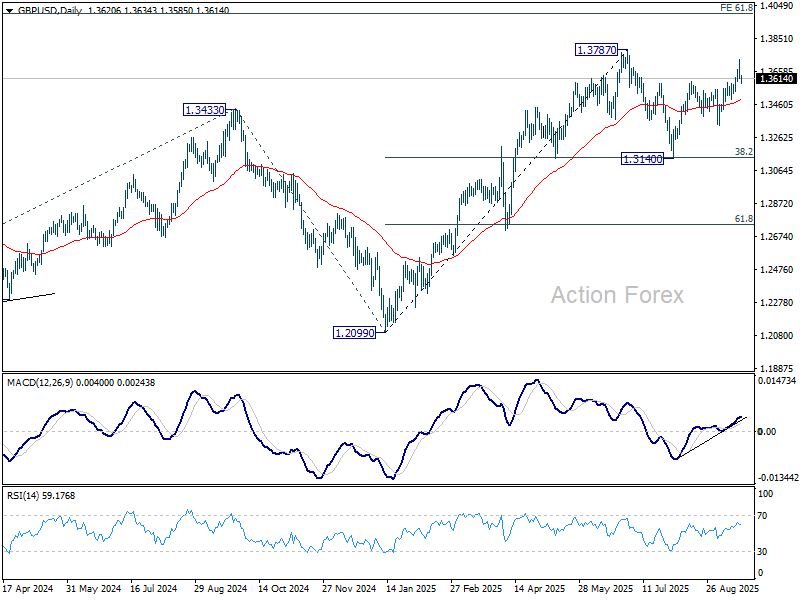

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3588; (P) 1.3657; (R1) 1.3694; More...

Intraday bias in GBP/USD is turned neutral first with current retreat, and some consolidations would be seen below 1.3725 temporary top. Further rise is expected as long as 55 D EMA (now at 1.3488) holds. Above 1.3725 will bring retest of 1.3787 high first. Decisive break there will resume larger up trend to 1.4004 projection level. However, sustained break of 55 D EMA will indicate that corrective pattern from 1.3787 is extending with another falling leg, and bring deeper fall to 1.3332 support and below.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.