BoE maintained Bank Rate at 5.25%, as widely expected. The announcement revealed a subtle dovish shift as evidenced by the voting and adjustments in the accompanying statement. Although these changes are not strong enough to warrant an immediate rate cut in June, they suggest that the central bank is inching closer to easing monetary policy.

The meeting concluded with a 7-2 voting split, with Deputy Governor Dave Ramsden joining the typically dovish Swati Dhingra in advocating for a rate cut. Additionally, BoE has explicitly stated its intent to monitor incoming data to assess whether risks from “inflation persistence are receding”, to determine the duration for which current Bank Rate is maintained.

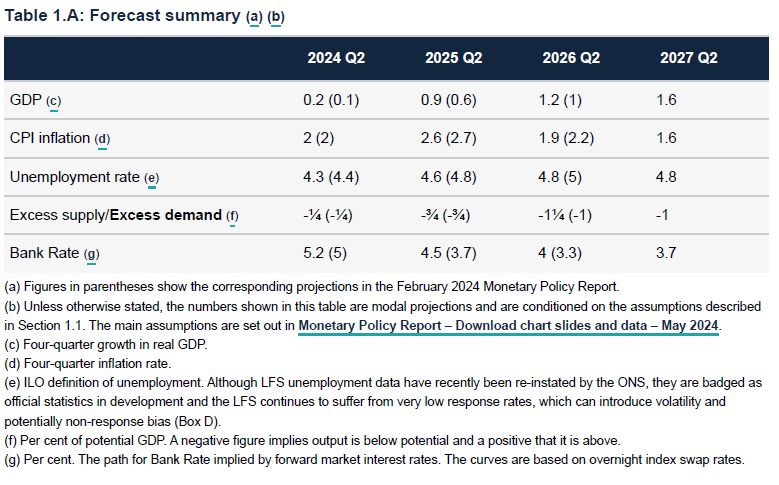

Furthermore, in its updated economic forecasts, BoE revised GDP growth projections upwards across the board and lowered CPI expectations for the coming years.

Four-quarter GDP growth is projected to be at 0.2% in Q2 2024 (revised up from 0.1%), 0.9% in Q2 2025 (up from 0.6%), 1.2% in Q2 2026 (up from 1%) , and then 1.6% in Q2 2027.

CPI inflation is projected to be at 2% in Q2 2024 (unchanged), 2.6% in Q2 2025 (down from 2.7%), 1.9% in Q2 2026 (down from 2.2%, and then 1.6) in Q2 2027.

Full BoE statement and Monetary Policy Report.

US initial jobless claims rises to 231k, vs exp 210k

US initial jobless claims rose 22k to 231k in the week ending May 4, above expectation of 210k. That’s also the highest level since late August 2023. Four-week moving average on initial claims rose 4.75k to 215k.

Continuing claims rose 17k to 1785k in the week ending April 27. Four-week moving average of continuing claims fell -6.25k to 1781k.

Full US jobless claims release here.