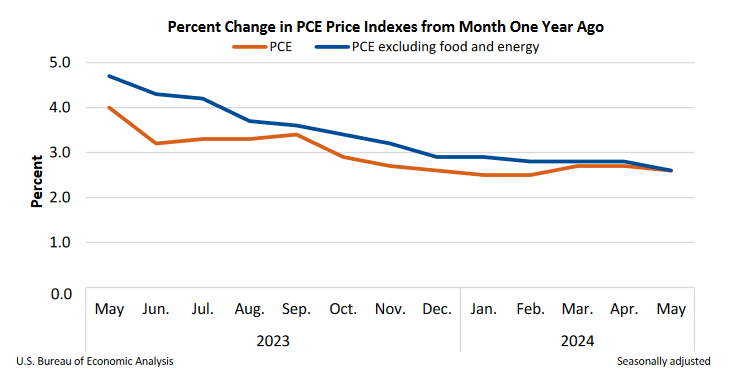

In May, US PCE price index was flat mom, matched expectations. PCE core price index (excluding food and energy) rose 0.1% mom. Both matched expectations. Prices for goods fell -0.4% mom while prices for services rose 0.2% mom. Food prices rose 0.1% mom while energy prices fell -2.1% mom.

From the same month one year ago, headline PCE price index slowed from 2.7% yoy to 2.6% yoy. PCE core price index slowed from 2.8% yoy to 2.6% yoy. Both matched expectations. Goods prices were down -0.1% yoy while services prices were up 3.9% yoy. Food prices were up 1.2% mom and energy prices were up 4.8% yoy.

Also, personal income rose 0.5% mom or USD 114.1B, above expectation of 0.4% mom. Personal spending rose 0.2% mom or USD 47.8B, below expectation of 0.3% mom.

Canada’s GDP grows 0.3% mom in Apr, matches expectations

Canada’s GDP grew 0.3% mom in April, matched expectations. Both goods-producing (+0.3%) and services-producing (+0.3%) industries contributed to the growth with 15 of 20 sectors increasing in the month.

Advance information indicates that real GDP rose 0.1% mom in May. Increases in manufacturing, real estate and rental and leasing and finance and insurance were partially offset by decreases in retail trade and wholesale trade.

Full Canada GDP release here.