Live Comments

Japan’s Wage Cycle Keeps Improving as Real Pay Rises for Sixth Month

Japan's wage growth remained robust in June, reinforcing the Bank of Japan's case for continued policy normalization. Real wages rose 1.6% y/y, matching May's upwardly revised gain and marking a sixth consecutive monthly increase, the longest positive streak since 2021. More notably, nominal cash earnings climbed 3.4%, extending a run of monthly increases above 3% to five months, the longest such streak in more than 34 years.

The strength in pay was supported by another solid round of summer bonuses and this year's strong "shunto" wage negotiations. Special earnings, which include bonuses, rose 3.5%. Summer bonuses also topped JPY 1 million on average for the first time since comparable records began in 1981, reflecting healthy corporate profitability.

Separately, Japan's largest business lobby, Keidanren, said major companies agreed to average wage increases of 5.37%, exceeding 5% for a third consecutive year.

The latest figures reinforce the view that Japan's long-awaited wage-price cycle continues to gain traction. Combined with recent PMI surveys showing firms raising selling prices at one of the fastest rates in nearly two decades, the wage data support the BOJ's assessment that upside inflation risks remain, keeping the door open to further interest rate hikes in the months ahead.

Data Summary

| Indicator | June | May | Trend |

|---|---|---|---|

| Real wages (y/y) | +1.6% | +1.6% | Sixth straight increase |

| Nominal cash earnings (y/y) | +3.4% | +3.2% | Fifth straight month above 3% |

| Inflation used for wage calculation (y/y) | 1.9% | 1.7% | Higher |

| Special earnings / Bonuses (y/y) | +3.5% | — | Stronger |

Key Takeaways

- Real wages rose 1.6% y/y in June, extending gains to a sixth consecutive month, the longest positive streak since 2021.

- Nominal wages increased 3.4% y/y, marking a fifth straight month above 3%, the longest such run in more than three decades.

- Wage growth was supported by strong summer bonuses and another robust round of shunto wage negotiations, with average pay settlements of 5.37%.

- Government energy subsidies helped keep inflation below 2%, allowing real wage growth to remain positive despite higher import costs.

- Economists expect stronger wage growth to feed into consumer prices later this year as firms pass on higher labor and raw material costs.

- The report reinforces the BOJ's normalization narrative, strengthening the case that inflation is becoming increasingly supported by domestic wage growth rather than imported price shocks alone.

China Private Services PMI Slows Sharply to 50.4 as Domestic Demand Loses Momentum

China's services sector remained in expansion in July, but growth slowed sharply as domestic demand weakened. The RatingDog China General Services PMI fell from 54.1 in June to 50.4, its lowest reading since September 2024, while the Composite PMI declined from 53.6 to 50.8, marking the slowest pace of overall private sector growth in a year. The latest survey suggests economic activity continued to expand, but momentum softened noticeably after a stronger first half.

The moderation was driven primarily by weaker domestic demand. Total new business increased for a 43rd consecutive month, but growth slowed to its weakest pace since March. In contrast, external demand remained comparatively resilient, with new export business staying in expansionary territory for a second straight month despite easing from June's year-to-date high. Cost pressures also continued to ease, with input price inflation slowing to its weakest since January, while firms raised selling prices only modestly.

Despite softer demand, the survey contained several encouraging signs. Employment increased for a third consecutive month, the longest period of job creation since the second half of 2024, while backlogs of work rose for a ninth straight month, suggesting firms continue to see enough activity to support hiring. However, business confidence weakened to its lowest level since February 2020, highlighting growing caution over the economic outlook. The report points to an economy that is still expanding, but one that is becoming increasingly dependent on resilient exports as domestic demand loses momentum.

Data Summary

| Component | July 2026 | June 2026 | Trend |

|---|---|---|---|

| Services PMI | 50.4 | 54.1 | ▼ Lowest since Sep 2024 |

| Composite PMI | 50.8 | 53.6 | ▼ Slowest growth in one year |

| Business activity | Expanded | Expanded | Growth slowed sharply |

| New business | Expanded | Expanded | Weakest growth since Mar 2026 |

| New export business | 52.0 | Higher | Still in expansion |

| Input costs | Increased | Increased | Inflation eased to lowest since Jan 2026 |

| Selling prices | Increased | Increased | Inflation moderated |

| Employment | Expanded | Expanded | Third consecutive monthly increase |

| Outstanding business | Increased | Increased | Ninth straight monthly rise |

| Business confidence | Positive | Positive | Lowest since Feb 2020 |

Key Takeaways

- China's Services PMI dropped sharply to 50.4 from 54.1, marking the weakest expansion since September 2024.

- The Composite PMI slowed to 50.8, signalling the weakest pace of private-sector growth in a year as both manufacturing and services lost momentum.

- Domestic demand softened noticeably, with new business expanding at the slowest pace since March, while export demand remained comparatively resilient.

- Cost pressures continued to ease, with input cost inflation slowing to its weakest since January, providing some relief to businesses.

- Employment expanded for a third consecutive month and backlogs of work increased for a ninth straight month, suggesting firms are still seeing sufficient workloads.

- Business confidence weakened to its lowest level since February 2020, highlighting growing caution over China's economic outlook despite continued expansion.

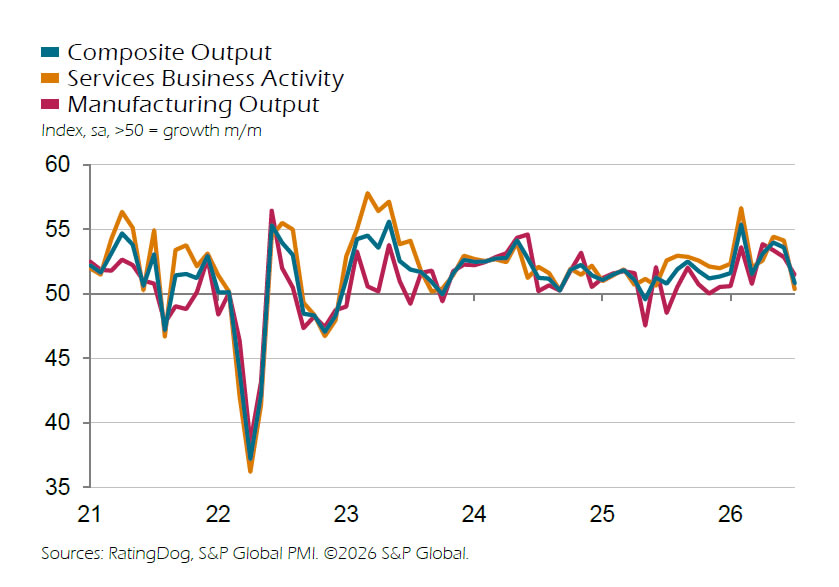

Japan Services PMI Eases to 51.2 in July, Composite Holds at 52.7

Japan's services sector continued to expand in July, but the pace of growth slowed as demand softened from earlier in the year. The S&P Global Japan Services PMI fell to 51.2 from 52.2 in June, signaling a second consecutive monthly expansion but at a more modest pace. Businesses cited events, promotional campaigns and new contract wins as supporting activity, although some firms reported that underlying demand remained relatively subdued.

The moderation in services was largely offset by the manufacturing sector, where output recorded its strongest increase since early 2014. As a result, the Composite PMI edged only slightly lower to 52.7 from 52.8, pointing to another solid expansion in overall private sector activity. Even so, the broader growth trajectory has eased from the stronger pace seen in the first quarter, before the Middle East conflict disrupted global supply chains and raised business costs.

Inflation remained the dominant theme across the survey. Companies continued to report rapid increases in input costs and passed those pressures on through higher selling prices, with output price inflation reaching its second-fastest pace in nearly two decades of data collection. The findings suggest official inflation could strengthen further in the coming months, reinforcing expectations that the Bank of Japan will face continued pressure to normalize monetary policy despite signs that services sector growth has moderated.

Data Summary

| Component | July 2026 | June 2026 |

|---|---|---|

| Services PMI | 51.2 | 52.2 |

| Composite PMI | 52.7 | 52.8 |

| Business activity | Expanded | Expanded |

| New business | Expanded | Expanded |

| Input costs | Increased sharply | Increased sharply |

| Selling prices | Second-fastest rise in nearly 20 years | Elevated |

| Overall outlook | Positive | Positive |

Key Takeaways

- Japan's Services PMI eased to 51.2 from 52.2, indicating the services sector continued to expand but at a slower pace.

- The Composite PMI remained broadly stable at 52.7, as booming manufacturing activity offset softer services growth.

- Service providers continued to benefit from new contracts, events and promotional activities, although many firms reported more subdued underlying demand.

- Inflation pressures remained intense across both manufacturing and services, with firms continuing to face rapid increases in input costs.

- Selling prices rose at the second-fastest pace in nearly two decades, suggesting official inflation could strengthen further in the months ahead.

- The survey reinforces expectations that the Bank of Japan will remain under pressure to continue policy normalization, even as overall economic growth moderates from the stronger pace seen before the Middle East conflict.