Live Comments

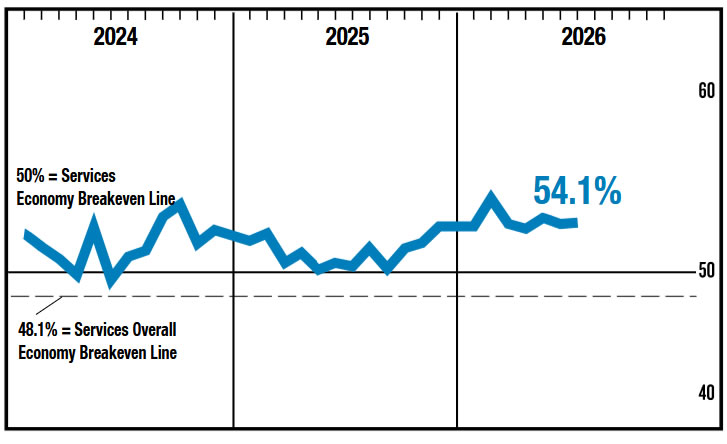

US ISM Services Holds Firm at 54.1 as Employment Contracts, Prices Accelerate

The US services sector continued to expand at a healthy pace in July, suggesting the economy remains resilient even as cracks emerge in the labor market. The ISM Services PMI edged up to 54.1 from 54.0, remaining comfortably above its 12-month average of 53.4. According to ISM's historical relationship, the latest reading is consistent with 1.9% annualized real GDP growth, indicating that overall economic activity continues to expand despite growing uncertainty over monetary policy and the outlook for employment.

Beneath the steady headline, however, the report revealed a more mixed picture. The Employment Index dropped sharply to 47.4 from 51.2, slipping back into contraction after just one month of growth. Survey respondents pointed to modest workforce reductions, with some firms citing AI adoption while others continued shifting jobs to lower-cost overseas locations. The weaker employment reading follows softer ADP payroll data earlier in the day, reinforcing signs that hiring momentum in the US economy is cooling.

Inflation pressures, meanwhile, moved in the opposite direction. The Prices Index climbed to 70.3, up from 67.7, marking the 110th consecutive month of rising input costs and lifting its 12-month average to the highest level since April 2023. The combination of resilient activity, softer hiring and firmer prices leaves the Federal Reserve with a familiar policy dilemma. While slowing employment supports the case for patience, persistent cost pressures are likely to keep policymakers cautious about declaring victory over inflation.

Data Summary

| Indicator | July 2026 | June 2026 | Trend |

|---|---|---|---|

| ISM Services PMI | 54.1 | 54.0 | ▲ Slight improvement |

| Market Expectation | 54.2 | — | Slight miss |

| Business Activity | 59.1 | 55.4 | ▲ Strong acceleration |

| New Orders | 57.2 | 55.1 | ▲ Demand strengthened |

| Employment | 47.4 | 51.2 | ▼ Back to contraction |

| Prices Paid | 70.3 | 67.7 | ▲ Inflation pressures intensified |

| New Export Orders | 52.0 | 50.4 | ▲ Faster expansion |

| Imports | 51.8 | 49.4 | ▲ Returned to growth |

| Backlog of Orders | 50.9 | 54.9 | ▼ Growth slowed |

| Supplier Deliveries | 52.8 | 54.4 | ▼ Delivery delays eased |

Key Takeaways

- ISM Services PMI edged up to 54.1 in July, signaling a 25th consecutive month of expansion and pointing to 1.9% annualized real GDP growth according to ISM's historical relationship.

- Business activity (59.1) and new orders (57.2) accelerated, indicating demand across the services sector remained healthy despite a softer macro backdrop.

- The Employment Index dropped sharply to 47.4, slipping back into contraction after one month above 50 and reinforcing earlier signs from the ADP report that labor demand is cooling.

- Survey respondents cited AI adoption, workforce reductions and continued hiring shifts to lower-cost overseas locations as factors behind weaker employment.

- The Prices Paid Index jumped to 70.3, marking the 110th consecutive month of rising input costs and its highest 12-month average since April 2023.

- The report delivers a mixed signal for the Fed: solid economic activity argues against recession concerns, while weaker hiring supports patience, but stronger price pressures keep inflation risks alive.

Fed’s Kashkari: Better to Start Raising Rates Now Than Wait

Minneapolis Fed President Neel Kashkari defended his dissent at last week's FOMC meeting, arguing that the central bank should begin raising interest rates gradually rather than risk falling behind inflation. Speaking to CNBC from the Aspen Ideas Festival, Kashkari said he was not advocating aggressive tightening but believed the Fed should "start slowly moving up as we get more data in." He was one of three policymakers who voted for a 25-basis-point rate hike, while the majority opted to keep the federal funds rate unchanged at 3.50%-3.75%.

Kashkari's central argument was that current monetary policy has yet to become meaningfully restrictive. "I don't see evidence monetary policy is particularly restrictive right now," he said, pointing to robust corporate earnings, resilient consumer spending and a labor market that continues to hold up well. While acknowledging that June inflation showed some improvement as oil prices temporarily retreated, he warned that persistent supply shocks continue to threaten the inflation outlook. "We have more work to do to get inflation back down," he said, adding that he would "rather get going now in small steps than wait till later" and risk having to raise rates much more aggressively.

His remarks sharpen the contrast within the Federal Reserve following last week's meeting. Just a day earlier, Philadelphia Fed President Anna Paulson argued policy was already "mildly restrictive" and supported holding rates steady while assessing incoming data. Kashkari stopped short of explicitly calling for a September hike, stressing that future decisions would depend on economic data. He also revealed that Fed Chair Kevin Warsh encouraged independent judgment, recalling that Warsh told him to "do what you think is the right thing to do for the economy.

Key Takeaways

- Minneapolis Fed President Neel Kashkari argued the Fed should begin raising rates gradually rather than risk falling behind inflation and being forced into larger hikes later.

- Kashkari believes current monetary policy is not sufficiently restrictive, citing strong corporate earnings, resilient consumer spending and a still-solid labour market.

- Despite some improvement in June inflation, he warned that supply-side inflation risks remain, saying the Fed still has "more work to do" to return inflation to its 2% target.

- Kashkari did not explicitly endorse a September rate hike, emphasizing that upcoming economic data will determine the appropriate policy path.

- His comments highlight the growing divide within the FOMC, contrasting with Philadelphia Fed President Anna Paulson's view that policy is already "mildly restrictive."

- Kashkari also said Fed Chair Kevin Warsh encouraged independent judgment, suggesting an open policy debate despite the unusual three dissents at last week's meeting.

US ADP Employment Miss at 44k Growth Slows Sharply, But Wage Growth Stays Firm

US private-sector hiring slowed more sharply than expected in July. The ADP National Employment Report showed private employment increased by 44k, well below the 75k consensus forecast and down from a revised 95k in June. Hiring remained concentrated in the service sector, which added 47k jobs, while goods-producing industries shed 3k, leaving overall employment growth at its weakest pace in recent months.

The softer headline, however, was accompanied by continued resilience in wages. Annual pay growth for workers who stayed with their employers held steady at 4.4%, while wage growth for job changers accelerated to 7.0%, the strongest since August 2025.

ADP Chief Economist Nela Richardson noted that stronger pay gains for job changers suggest labour shortages persist in parts of the economy even as employers adjust hiring plans to shifting macroeconomic conditions.

Data Summary

| Indicator | July | June | Trend |

|---|---|---|---|

| ADP Private Employment | 44k | 95k | ▼ Hiring slowed sharply |

| Market Expectation | 75k | — | Missed by 31k |

| Goods-Producing Employment | -3k | — | ▼ Contracted |

| Service-Providing Employment | +47k | — | ▲ Continued growth |

| Small Businesses | +23k | — | ▲ Largest contributor |

| Medium Businesses | +8k | — | ▲ Positive |

| Large Businesses | +13k | — | ▲ Positive |

| Pay Growth – Job Stayers | 4.4% y/y | 4.4% | ► Unchanged |

| Pay Growth – Job Changers | 7.0% y/y | 6.7% | ▲ Highest since Aug 2025 |

Key Takeaways

- US private employment rose by just 44k in July, well below the 75k consensus forecast and down from a revised 95k in June, pointing to slower hiring momentum.

- Employment growth remained concentrated in the services sector (+47k), while goods-producing industries lost 3k jobs.

- Hiring was positive across businesses of all sizes, with small firms accounting for more than half of July's job gains.

- Wage growth remained resilient. Pay for job stayers held steady at 4.4%, while job changers saw pay growth accelerate to 7.0%, the strongest since August 2025.

- ADP said stronger wage gains for job changers suggest labour shortages persist in parts of the economy, even as employers become more cautious about hiring.

- The report reinforces the picture of a cooling—but not collapsing—labour market, keeping attention firmly on Friday's official nonfarm payrolls report for confirmation.