Sample Category Title

Sunset Market Commentary

Markets

This morning, it initially looked that risk premia at the ultra-long end of the yield curve could remain the focus for markets. The Japanese 10-y yield tested the cycle /YTD top levels near 1.6%. The 30-y yield even touched an all-time top near 3.21%. However, this time were no spillovers to markets outside Japan. Markets shifted into wait-and-see modus ahead of the US CPI data. German ZEW economic confidence improved more than expected, both for the measure on the current situation (-59.5 from -72.0) and the expectations series (52.7 from 47.5). The indicator had little impact on trading. Even so, equity resilience suggests a similar attitude (slight gains for Eurostoxx 50 and US equities) with investors staying hopeful on a reasonable outcome of the trade negotiations.

The eagerly awaited June US CPI report wasn’t able to given any clear directional guidance. At 0.3% M/M and 2.7% Y/Y and 0.2%/2.9% Y/Y for core inflation (ex food and energy) the report was very close to expectations. A rise in prices of apparel (0.4%) and some household furnishings and equipment might be indication of some pass-through of higher costs, but its too early to draw any firm conclusions. Vehicle prices declined again. Services prices ex energy rose 0.3%. Shelter price inflation was a modest 0.2%. If anything, the conclusion might be that it takes time for tariffs to move the overall picture on inflation, also as those items only have a rather limited weight in the inflation basket compared to e.g. services. US short-term yields briefly dipped after the release but most of this move was quickly undone. US yields are trading +2.5 bps (2-y) and -1.0 bps lower (30-y). Already this morning, German/EMU curves bull flattened and this move was maintained after the US CPI release. The German 2-y yields trades little changed (2-y). The 30-y declines 5.5 bps. Both the price action in the US and even more in the German yield curve suggest this a correction on recent steepening as LT yields were closing in on high profile levels, rather than a reaction to CPI. Hardly any USD reaction to the CPI data. The DXY trade-weighted (98.1) index lost marginal ground after the CPI release, but the move didn’t continue. EUR/USD drifts lower to 1.165. The yen still underperforms with USD/JPY at 148.5 and EUR/JPY 172.8, touching the highest level since July last year. EUR/GBP this morning just didn’t touch the 0.87 barrier, currently trading near 0.8675. Tomorrow, the UK June CPI data will be published with the labour market data to be released on Thursday. This evening markets also will keep a close at the Mansion House speech of Bailey. Markets look out whether the BoE governor will again shift the focus to sub-trend growth and easing of labour market conditions, suggesting more room for the BoE to cut rates later this year.

News & Views

Canadian inflation slowed to 0.1% m/m in June from 0.6% in May. That was nevertheless enough to lift the 1.7% y/y reading to 1.9%. The core measures watched closely by the Bank of Canada (trimmed, mean) ranged between 3% and 3.1% y/y while the common core gauge (CPI ex food and energy) came in at 2.6%. These latter gauges have been going nowhere for the last three months (since April) now. That’s unlikely to sooth the central bank let alone to convince it to cut rates further from the current 2.75% (in place since March). The BoC in its latest policy meeting (June 4) and referring back then to April data, specifically mentioned the uptick in core inflation and added that households continue to expect tariffs will raise prices while businesses plan to pass on those costs. US President Trump threatened Canada with a 35% in one of his tariff letters last week. The Canadian Loonie strengthens slightly against an overall weaker USD today. USD/CAD drops to 1.367. Canadian government bond yields trade little changed across the curve.

OPEC in its monthly report said that the global economy may perform better than expected in the latter half of the year despite the rumbling trade conflicts. Shorter term and going over the summer months, refineries’ crude intake would remain elevated, helping support the demand outlook. The robust outlook meant the oil cartel made no changes to its global oil demand growth for 2025 and 2026 after reductions in April. The OPEC analysis came after the IEA trimmed its demand forecast last week but later said that the market may be tighter than it appears. Brent oil prices trade little changed today around $69.3/b.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1648; (P) 1.1673; (R1) 1.1691; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Consolidations from 1.1829 could extend further. Downside should be 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, sustained break of 1.1630 will bring deeper fall to 55 D EMA (now at 1.1481) instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

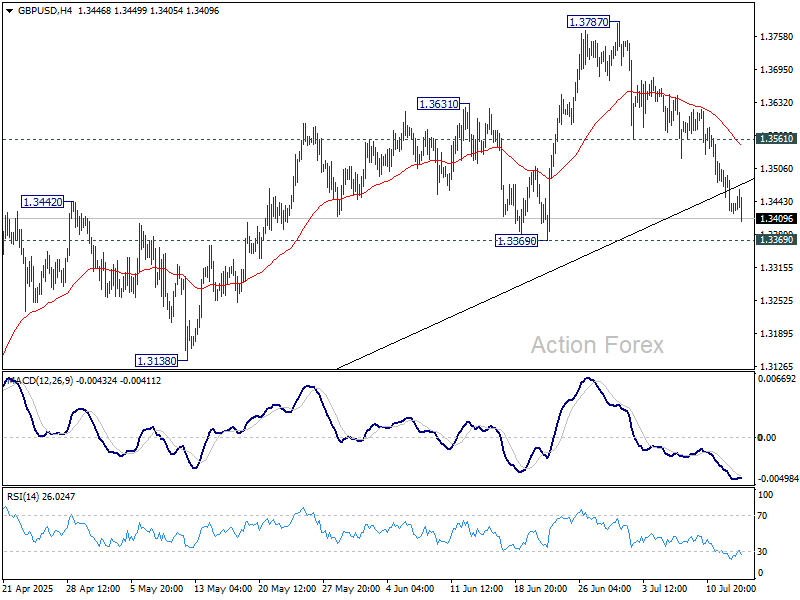

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3396; (P) 1.3454; (R1) 1.3484; More...

Intraday bias in GBP/USD stays neutral and outlook is unchanged. Pullback from 1.3787 could extend lower but downside is expected to be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. However, firm break of 1.3369 will bring deeper correction back to 1.2706/3206 support zone.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3019) holds, even in case of deep pullback.

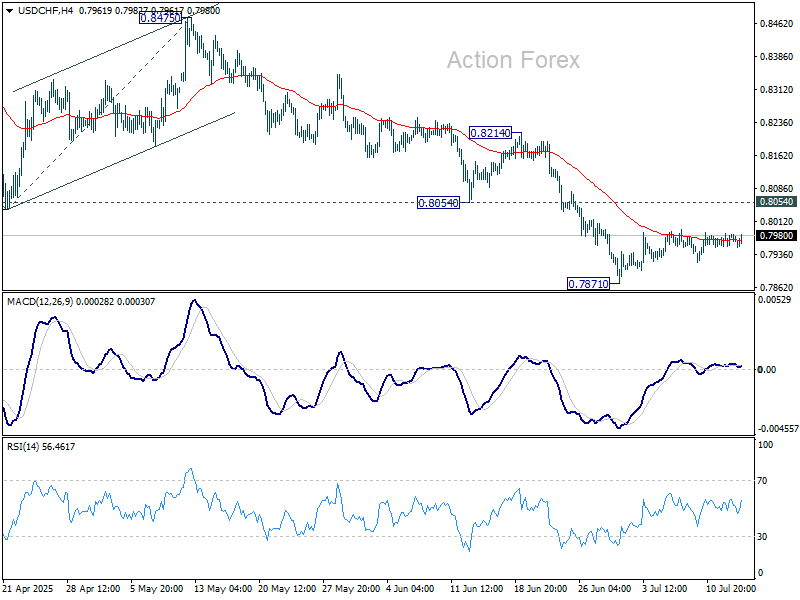

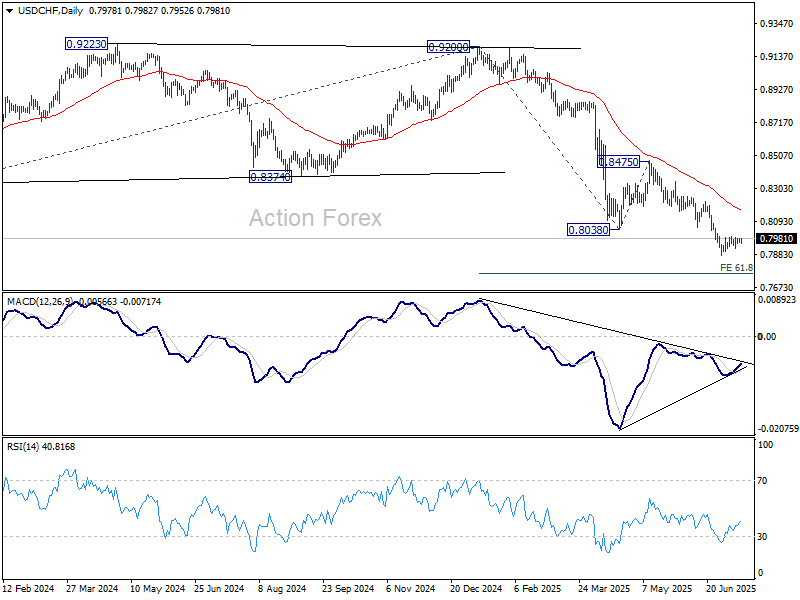

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7962; (P) 0.7973; (R1) 0.7992; More….

No change in USD/CHF's outlook as consolidations continue above 0.7871. Intraday bias stays neutral at this point. Stronger recovery might be seen but upside should be limited by 0.8054 support turned resistance. On the downside, firm break of 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

US Dollar Cannot Find a Direction Despite the Positive CPI Report

Market reactions have been very muted and mixed, even if the CPI report came out with a small but positive surprise.

For those who are discovering the number, US Headline CPI came in as expected (0.287 unrounded Headline vs 0.30% expected).

The Core number was however the more welcomed surprise, coming in at 0.2% (0.227%) vs 0.3% expected – This is what the FED prefers for their decisions.

For Canadian Data also, CPI Came in as expected (1.79% y/y, slightly stronger core)

Reactions have been a bit underwhelming overall, not what could have been expected. Nonetheless, more participants will be coming into the Market at 9:30 for the open, which may trigger some further volatility, totally absent for now.

Markets will need bigger surprises to move more, and except for Nasdaq and S&P Futures that are rising (slowly) on the news, it seems that players are waiting for something else to be on the move.

Let's take a look at US Dollar charts to see where we are after the CPI report.

Dollar Index 4H Chart

Dollar Index 4H Chart, July 15, 2025 – Source: TradingView

The Dollar has been grinding upwards since the 1st off July, now hanging around the 98.00 handle since yesterday with buyers showing some hesitancy.

It could have been assumed that participants would await for the number to move forward with the Dolalr buybacks, but for now the 4H Candle is a doji.

Look at the 98.00 PIvot Zone (+/- 15 pips) for immediate strength:

A break above would point towards a test of the 98.50 level that was key support on the way down, the next main resistance is closer to 99.00

A break below would look to test the 97.60 Support in confluence with the bottom of the Upwards Channel from this month that will need to hold to avoid resuming the main downtrend.

Dollar. Index 30M Chart

Dollar Index 30m Chart, July 15, 2025 – Source: TradingView

Looking closer shows further the lack of volatility from the data, with the Dollar Index confined within at 80 pip range – Other currencies have shown some wicks but no immediate reactions.

Data high in DXY: 98.15 – Low: 97.35, watch for any breakout beyond these points.

We will follow closely what the market is waiting for to start moving as the North-American session is still young and somne geopolitic turmoil might start to be into play between Ukraine and Russia - keep an eye on the news.

Safe Trades!

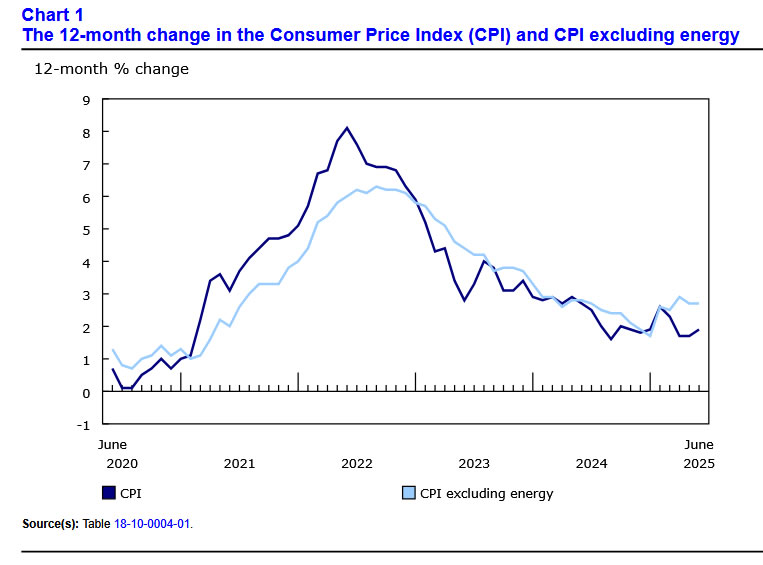

US: Inflation Heats up in June, as Tariff Impacts Start to Surface

The Consumer Price Index (CPI) rose 0.3% in June, in line with the consensus forecast in Bloomberg and an acceleration from May's gain of 0.1% m/m. On a twelve-month basis, CPI was up 2.7% (from 2.4% in May).

- Energy costs (0.9% m/m) turned higher last month – following a decline in May – while food prices (0.3% m/m) also came in on the hotter side and are now up 3.0% year-on-year (yr/yr).

Excluding food and energy, core inflation rose 0.2% m/m (0.23% m/m unrounded) – just shy of the consensus forecast calling for a gain of 0.3% m/m – but an uptick from May's 0.1% m/m. The twelve-month change edged higher to 2.9% (from 2.8% in May), while the three-month annualized ticked up to 2.4%.

Services prices rose a 'soft' 0.3% m/m (0.25% m/m unrounded), up from May's gain of 0.17% m/m. Primary shelter costs rose 0.3% m/m, while price growth for non-housing services were up just 0.1% m/m – matching April and May's gain.

- Travel costs (-1.5% m/m) remained a drag on non-housing services – having now recorded declines for five consecutive months. Hotel costs (-2.9% m/m) were the culprit last month, while airfares (-0.1% m/m) were largely flat, but have fallen a cumulative 14% since January. Meanwhile, price growth for medical (0.6% m/m), recreational (0.2% m/m) and other personal services (0.4% m/m) all edged higher in June.

Core goods prices rose 0.2% m/m, with notable tariff impacts on select categories including home furnishing (+1.0% m/m), medical products (+0.8% m/m) and apparel (+0.4% m/m). New (-0.3% m/m) and used (-0.7% m/m) vehicle prices were both lower on the month. Excluding vehicles, core goods rose 0.5% m/m, or the strongest monthly gain since August 2022.

Key Implications

Inflationary pressures heated up in June, as tariff impacts helped to push goods prices higher – even after accounting for the pullback in vehicle prices – while services inflation also gained some momentum following softer readings in two of the prior three months. Looking ahead, we expect tariff passthrough to intensify through the summer, as pre-tariff inventory stockpiles are drawn down, and businesses are forced to restock under significantly higher import duties.

But the degree of tariff passthrough remains uncertain. Today's profit margins for trade exposed sectors remains elevated, so there is room for goods sellers to absorb some of the price impact, particularly if consumer demand were to remain healthy. Moreover, should services inflation continue to cool on trend as it has through most of this year, it would provide some offset to higher goods prices – limiting the overall hit to inflation. It is this uncertainty that is keeping policymakers on the sidelines and will continue to do so for at least another few months. Fed futures are pricing in just a 60% probability of quarter-point rate cut by September, and we would say that's a fair assessment given the current inflation risks amid a still resilient economy.

Canada: Inflation Ticks Higher in June as Fall in Gasoline Prices Abates

Headline CPI inflation for June came in at 1.9% year-on-year (y/y), heating up from the 1.7% print in May and in line with expectations.

The uptick was due to gasoline prices falling to a lesser extent in June (-13.4% y/y vs. -15.5% in April) and faster price growth for passenger vehicles and furniture.

Prices for clothing and footwear also rose 2.0% y/y vs. 0.5% last month due to the women's clothing index not declining like it did in May. Statistics Canada also cited "uncertainty surrounding international trade" and tariffs putting upward pressure on costs for the clothing and footwear industry.

The Bank of Canada's CPI-trim measure was unchanged for the month at 3.0% y/y, while the CPI-median index ticked higher to 3.1% y/y. The CPI excluding the eight most volatile components and indirect taxes (CPIX) accelerated to 2.7% y/y, from 2.5% in May, while CPI excluding food and energy was virtually unchanged at 2.6%. On a seasonally adjusted monthly basis, inflation accelerated for three of the four measures, while monthly inflation for CPI excluding food and energy was unchanged (+0.26% month-on-month).

Key Implications

Another month of the inflation data coming in as expected. Top line price growth continues to be restrained by weak readings for gasoline. Moreover, "geopolitical conflicts" were cited as propping up crude prices in June, a factor that faded mid-month and should provide some offset in July. Meanwhile, core inflation held up on an annual basis, with the monthly figures also pointing to healthy price growth. The groundwork for July to continue June's story (weak top-line price growth and more core strength) looks to be set.

Healthy core price growth, coupled with last week's surprisingly robust employment gains now make a July cut from the Bank of Canada unlikely. However, renewed trade threats add to the uncertainty that has lingered over the economy since the start of the year. Looking forward, the course of trade negotiations and evidence of whether June's healthy labour market report was a one-off, or the start of a new trend, will be crucial. Ultimately, we believe that absent a quick resolution on trade, the economic backdrop should give the BoC space to deliver more easing this year.

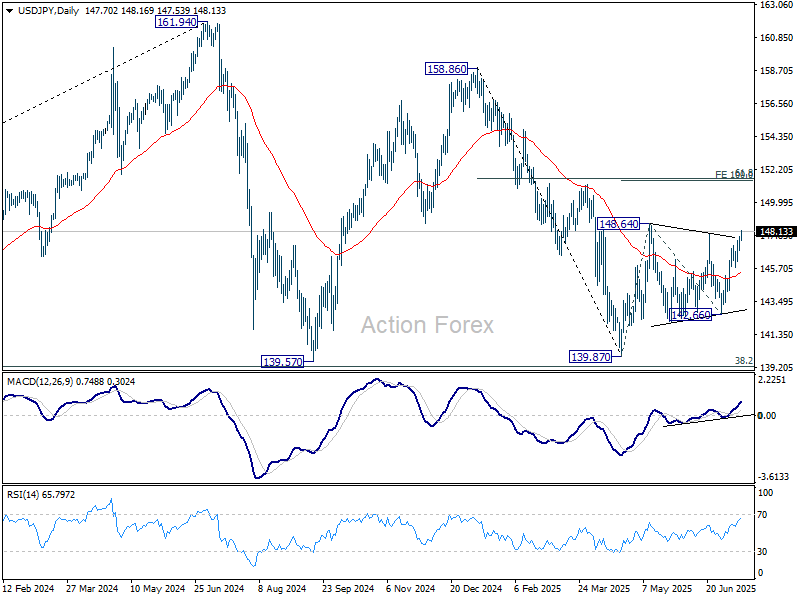

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.13; (P) 147.46; (R1) 148.05; More...

USD/JPY's breach of 148.01 resistance suggests that corrective pattern from 148.64 has completed with three waves to 142.66. Intraday bias is on the upside for 148.64 resistance first. Firm break there will confirm and target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. On the downside, below 146.84 minor support will mix up the outlook and turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Markets Calm as US CPI Leaves Fed Outlook Unchanged, Yen Slides Continue

Markets shrugged off the latest US CPI release, with muted reactions across assets. While annual core inflation ticked slightly higher, the modest rise appears to be a relief for Fed and investors alike. Overall, the data does little to shift expectations around the Fed’s easing path.

The July FOMC meeting remains firmly priced for a hold, with over 97% probability. As for September, futures imply around 60% odds of a rate cut. However, with US tariffs set to escalate from August 1 and trade talks still ongoing, there is considerable uncertainty over the coming weeks.

In FX, the standout move is the continued weakness in Yen. The currency is under pressure as investors position cautiously ahead of this weekend’s upper house elections. Sharp gains in long-dated JGB yields reflect growing anxiety over future fiscal policies and deficit spending, regardless of the outcome.

Elsewhere, the Dollar and Euro are also softer. Sterling and Swiss Franc are trading closer to the middle of the pack. Commodity currencies are outperforming, led by Kiwi and Aussie, followed by the Loonie.

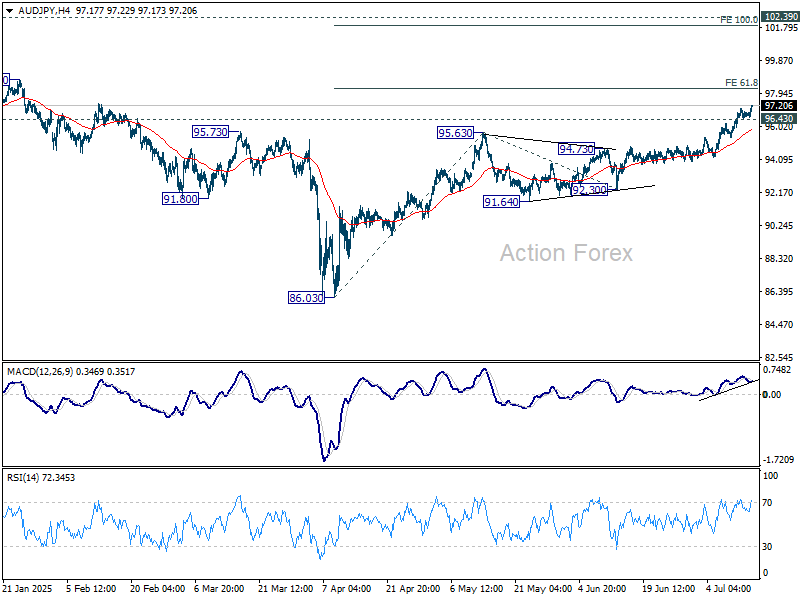

Technically, AUD/JPY's rally continues today and is on track to 61.8% projection of 86.03 to 95.63 from 92.30 at 98.23. Decisive break there could prompt further upside acceleration to 100% projection at 101.90. On the downside, break of 96.43 support will bring consolidations first.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is up 0.14%. CAC is up 0.01%. UK 10-year yield is down -0.044 at 4.564. Germany 10-year yield is down -0.054 at 2.678. Earlier in Asia, Nikkei rose 0.55%. Hong Kong HSI rose 1.60%. China Shanghai SSE fell -0.42%. Singapore Strait Times rose 0.26%. Japan 10-year JGB yield rose 0.015 to 1.592.

US CPI jumps to 2.7% yoy in June, core CPI undershoots expectation at 2.9% yoy

US CPI climbed 0.3% mom in June, matching forecasts, with the increase largely driven by a 0.2% mom rise in shelter costs and a 0.9% mom gain in energy prices. Food prices also edged higher, up 0.3% mom on the month. While the headline data aligned with expectations, the core CPI—excluding food and energy—rose just 0.2% mom, slightly below the anticipated 0.3% mom gain.

On a year-over-year basis, headline inflation jumped from 2.4% to 2.7%, in line with projections. However, core inflation ticked up only marginally from 2.8% to 2.9%, coming in under the 3.0% consensus. The annual energy index fell -0.8%, offering some offset to stickier components like food, which rose 3.0% over the year.

Canada's CPI rises to 1.9% yoy in June, core measures unchanged

Canada’s CPI rose 0.1% mom in June, falling short of the expected 0.2% mom gain. On an annual basis, headline inflation accelerated from 1.7% yoy to 1.9% yoy, matching expectations. The increase was driven partly by a smaller year-on-year decline in gasoline prices and firmer price gains in durable goods like vehicles and furniture.

Meanwhile, BoC’s preferred core inflation measures remained unchanged, with median and trimmed CPI steady at 3.0% and the common measure holding at 2.6%.

German ZEW jumps to 52.7, positive sentiment firmly established

Germany’s ZEW Economic Sentiment index jumped from 47.5 to 52.7 in July, beating expectations of 50.2 and marking the third consecutive monthly rise. Current Situation Index also improved sharply from -72 to -59.5, above forecast of -66.0. The data suggests that investor confidence is firming despite lingering global trade tensions, likely supported by hopes for a de-escalation in US-EU tariff threats and anticipated domestic fiscal stimulus.

Eurozone sentiment also edged up modestly, with the expectations index rising from 35.3 to 36.1, though falling short of the 37.8 consensus. The current conditions measure rose by 6.5 points to -24.2, signaling a gradual improvement in the broader bloc’s outlook.

ZEW President Achim Wambach noted that nearly two-thirds of respondents expect Germany’s economy to improve, citing optimism tied to a resolution of the US-EU trade standoff and government-led investment. Expectations were especially upbeat in sectors like machinery, metals, and electrical manufacturing.

Eurozone industrial production grows 1.7% mom in May, EU up 1.5% mom

Eurozone industrial production jumped 1.7% mom in May, comfortably beating market expectations of 1.1% mom. The strength was broad-based across key sectors, with notable gains in energy (+3.7%), capital goods (+2.7%), and non-durable consumer goods (+8.5%). However, weakness in intermediate goods (-1.7%) and durable consumer goods (-1.9%) tempered the overall picture.

Across the broader EU, industrial production rose 1.5% mom. At the national level, Ireland led the surge with a sharp 12.4% mom rise, followed by Malta (+3.4%) and Germany (+2.2%). On the flip side, industrial activity contracted most in Croatia (-2.9%), Slovakia (-2.8%), and Belgium (-2.7%).

Australia Westpac consumer sentiment edges up to 93.1, RBA hold damps household optimism

Australia’s Westpac Consumer Sentiment index edged up 0.6% mom to 93.1 in July, but the modest gain masked a clear sense of disappointment among households.

Westpac noted that sentiment was noticeably stronger before the RBA’s July meeting, with those surveyed prior to the decision reporting a reading of 95.6. That slipped to 92 among those surveyed after the RBA unexpectedly held rates steady, suggesting the decision dashed hopes for relief.

As a result, consumer confidence remains stuck at what Westpac called “cautiously pessimistic” levels.

Looking ahead, markets are eyeing the RBA’s next meeting on August 11–12. While the central bank may pause again if Q2 inflation overshoots, the more likely scenario is a confirmation that inflation stays inside the 2–3% target range. That would pave the way for a 25bps rate cut in August, with another expected in November.

China Q2 GDP growth slows to 5.2%, but beats expectations

China’s economy expanded 5.2% yoy in Q2, slightly above expectations of 5.1% yoy but down from 5.4% yoy in Q1. Sector data showed balanced growth across industries—primary output rose 3.7%, secondary 5.3%, and tertiary 5.5%. The National Bureau of Statistics noted that macroeconomic policies have supported stability, but also flagged persistent weakness in domestic demand and external headwinds.

June’s data painted a mixed picture. Industrial production accelerated from 5.8% yoy to 6.8% yoy, beating forecasts of 5.6% yoy and suggesting continued strength in export-facing sectors and manufacturing. However, retail sales cooled to 4.8% yoy, down sharply from May’s 6.4% yoy and missed expectation of 5.2% yoy.

Fixed asset investment year-to-date slowed to 2.8%, well below expectations of 3.7%. The decline in property investment deepened, falling -11.2% in H1, and private investment contracted -0.6%.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.13; (P) 147.46; (R1) 148.05; More...

USD/JPY's breach of 148.01 resistance suggests that corrective pattern from 148.64 has completed with three waves to 142.66. Intraday bias is on the upside for 148.64 resistance first. Firm break there will confirm and target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. On the downside, below 146.84 minor support will mix up the outlook and turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Canada’s CPI rises to 1.9% yoy in June, core measures unchanged

Canada’s CPI rose 0.1% mom in June, falling short of the expected 0.2% mom gain. On an annual basis, headline inflation accelerated from 1.7% yoy to 1.9% yoy, matching expectations. The increase was driven partly by a smaller year-on-year decline in gasoline prices and firmer price gains in durable goods like vehicles and furniture.

Meanwhile, BoC’s preferred core inflation measures remained unchanged, with median and trimmed CPI steady at 3.0% and the common measure holding at 2.6%.