Sample Category Title

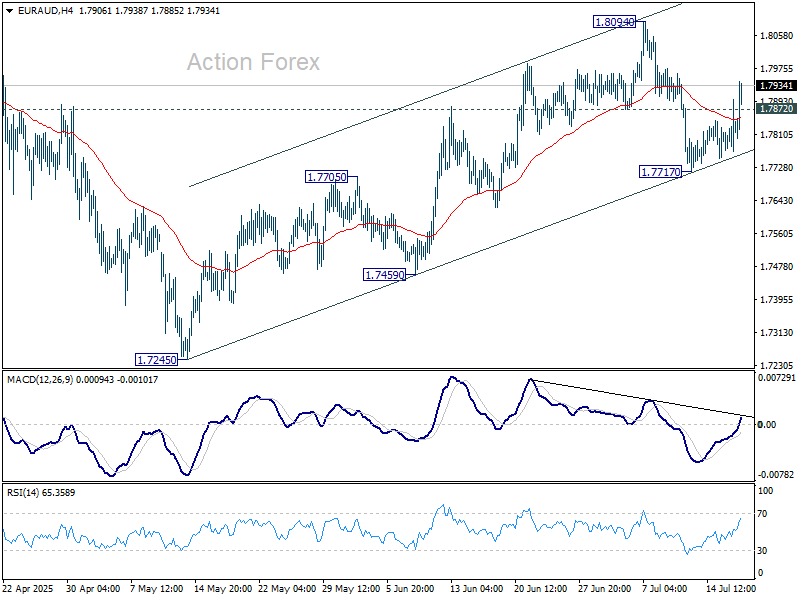

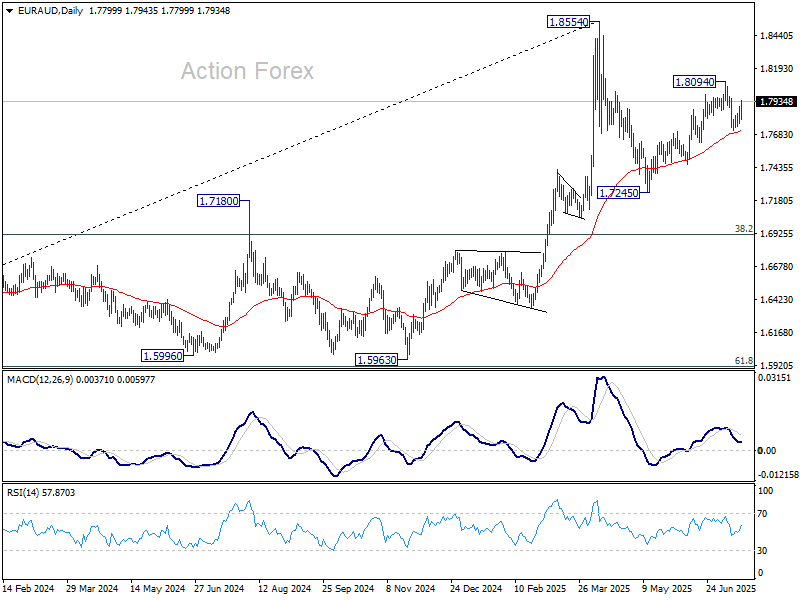

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7769; (P) 1.7834; (R1) 1.7896; More...

EUR/AUD's break of 1.7872 resistance argues that pullback from 1.8094 has completed already. Strong support from 55 D EMA (now at 1.7706) suggests that rise from 1.7245 is still in progress. Intraday bias is back on the upside for 1.8094 first. Firm break there will target 1.8554 high next.

In the bigger picture, price actions from 1.8554 medium term are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

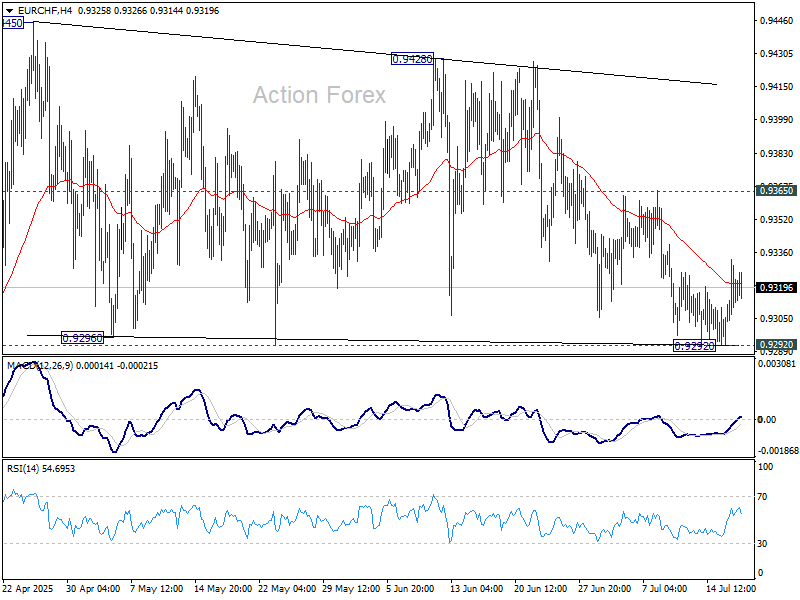

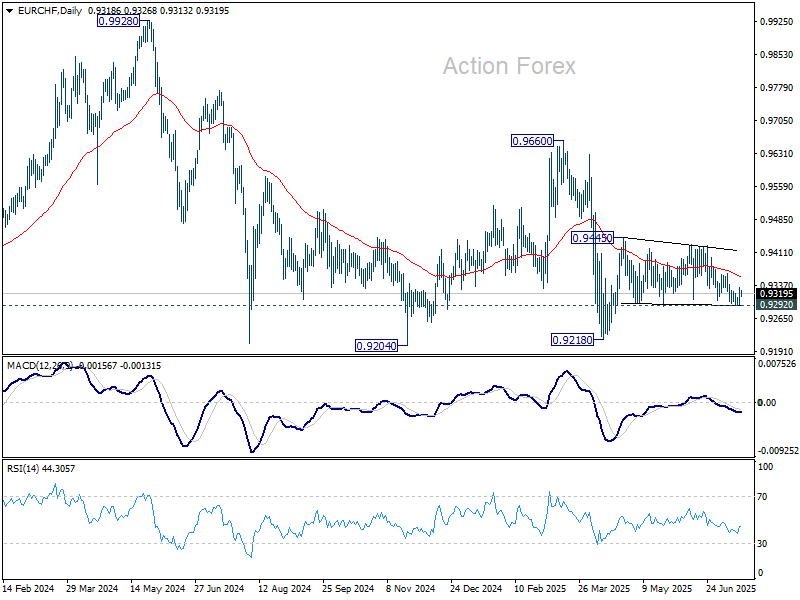

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9298; (P) 0.9317; (R1) 0.9342; More....

Intraday bias in EUR/CHF remains neutral for the moment. On the upside, break of 0.9365 resistance will suggest that fall from 0.9428 has completed. Further rally should be seen to retest 0.9428/45 resistance zone. Firm break there will resume the rebound from 0.9218. On the downside, firm break of 0.9292 support will bring retest of 0.9218 low instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9437) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1561; (P) 1.1642; (R1) 1.1721; More...

A temporary low is formed at 1.1561 and intraday bias is turned neutral. Risk will stay mildly on the downside as long as 1.1829 resistance holds. Fall from there correcting the rise from 1.1829 or whole rally from 1.0176. Below 1.1561 will target 55 D EMA (now at 1.1478). Sustained break there will target 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

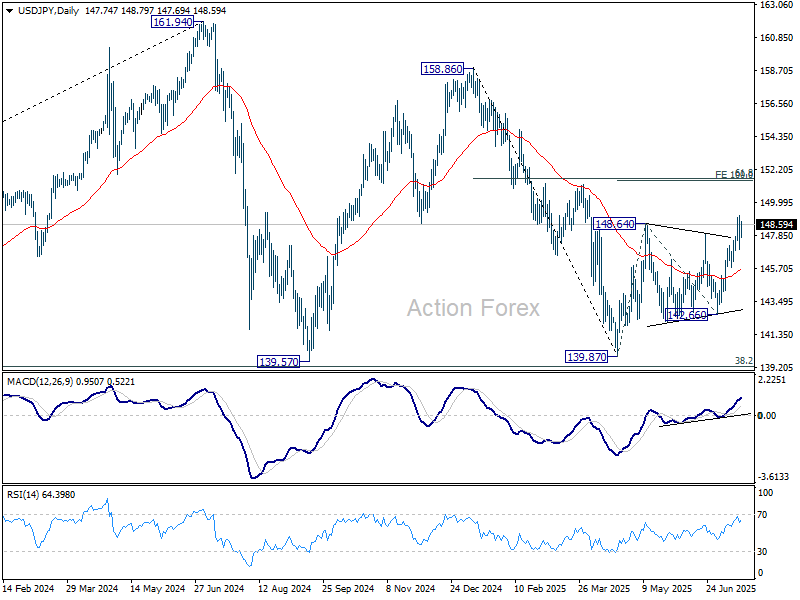

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.80; (P) 148.00; (R1) 149.08; More...

Intraday bias in USD/JPY is turned neutral first with a temporary top formed at 149.17. Some consolidations would be seen but downside should be contained by 55 D EMA (now at 145.56). Break of 149.17 will resume the whole rise from 139.87 to 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

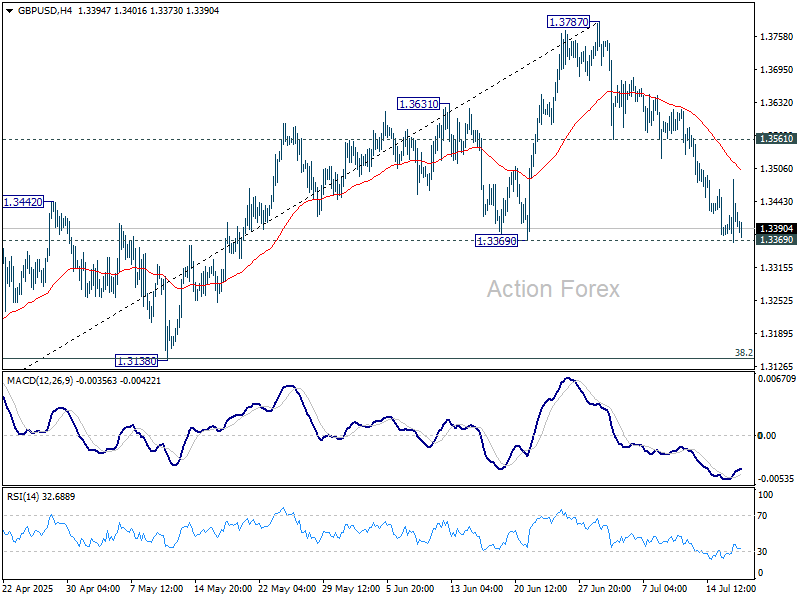

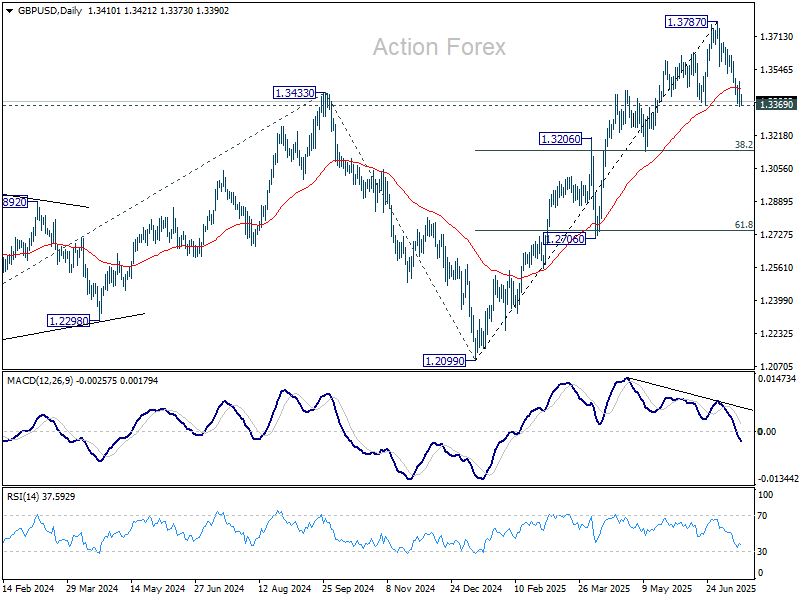

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3361; (P) 1.3424; (R1) 1.3482; More...

Intraday bias in GBP/USD remains neutral with focus on 1.3369 support. Decisive break there will suggests that it's already correcting the rise from 1.2099. Deeper fall should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Nevertheless, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3019) holds, even in case of deep pullback.

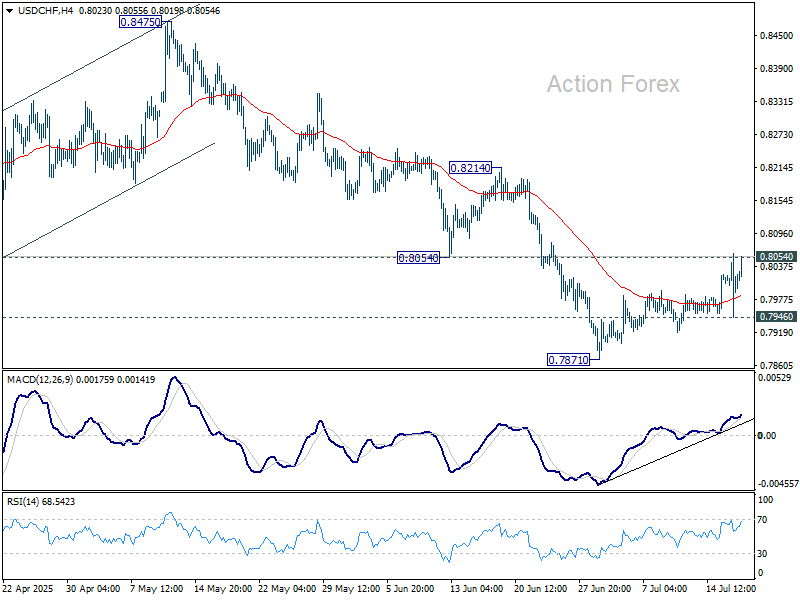

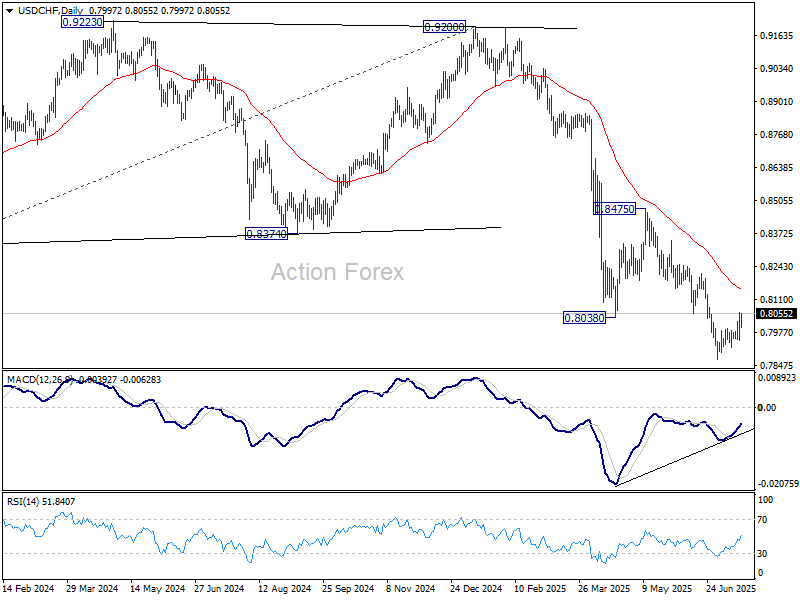

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7950; (P) 0.8006; (R1) 0.8065; More….

Intraday bias in USD/CHF stays neutral first and focus is on 0.8054 support turned resistance. Decisive break there will suggest that it's at least correcting the fall from 0.8475. Further rise should then be seen to 55 D EMA (now at 0.8151). Nevertheless, rejection by 0.8054 will retain near term bearishness. Below 0.7946 minor support will bring retest of 0.7871 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

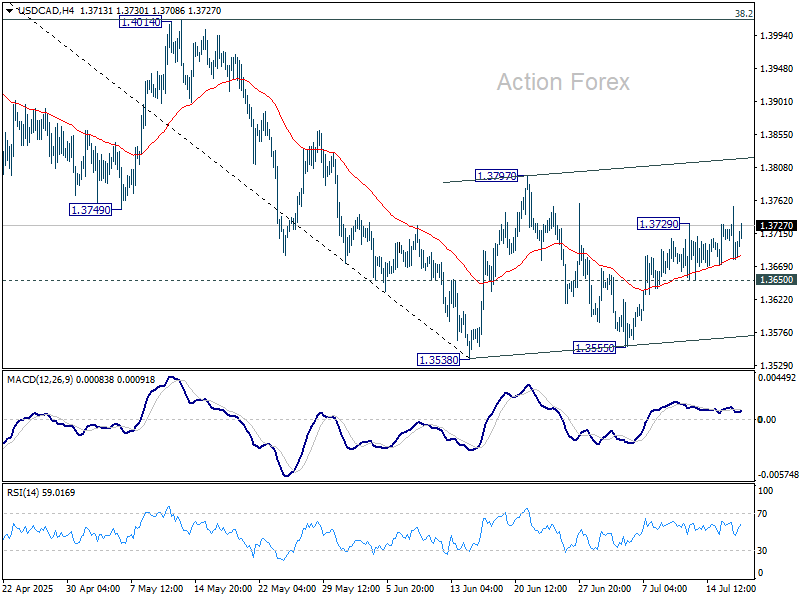

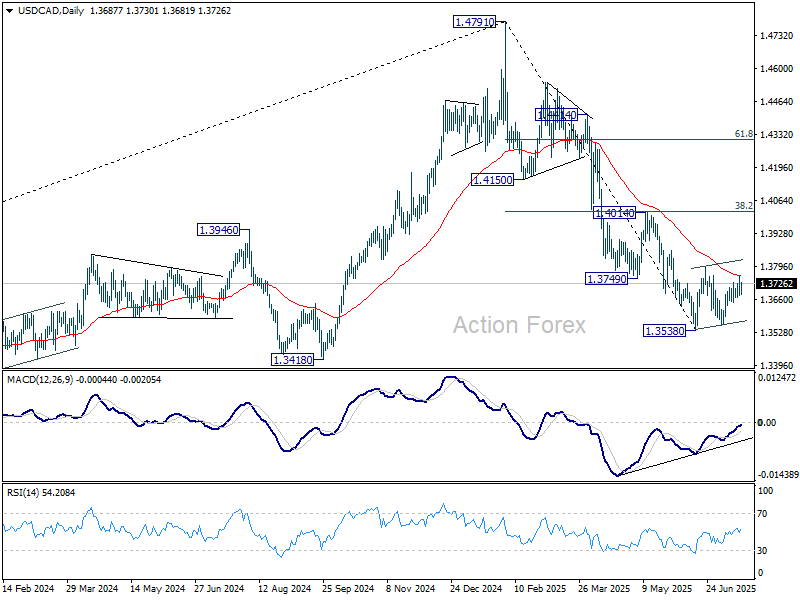

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3656; (P) 1.3705; (R1) 1.3731; More...

Intraday bias in USD/CAD is back on the upside with breach of 1.3729 temporary top. Further rise could be seen to 1.3797 resistance and above, to extend the corrective pattern from 1.3538. On the downside, break of 1.3650 minor support will bring retest of 1.3538/55 support zone instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Elliott Wave View: XAUUSD (Gold) Should Continue Rally

Elliott Wave sequence in XAUUSD (GOLD) suggest bullish view against September-2022 low in weekly. In daily, it should remain supported in 3, 7 or 11 swings to continue rally to extend higher. In daily, it ended ((4)) correction in 7 swings sequence at 3120.20 low in 5.15.2025 low against April-2025 peak. Above May-2025 low, it should continue rally targeting 3589 or higher levels, while pullback stays above 3246.55 low. In 4-hour, it placed 1 at 3452.5 low in proposed diagonal sequence. Within 1, it ended ((i)) at 3252.05 high, ((ii)) at 3245.20 low, ((iii)) at 3365.93 high, ((iv)) at 3245.20 low & finally ((v)) ended at 3452.50 high. It ended 2 in 7 swings correction at 3246.55 low in 6.29.2025. Within 2 pullback, it ended ((w)) at 3340.18 low, ((x)) at 3398.35 high & ((y)) at 3246.55 low in extreme area. It provided short term buying opportunity in extreme area, corrected 0.618 Fibonacci retracement of 1.

Above 2 low, It is showing nest in 1-hour sequence expecting further rally. It needs to break above 6.15.2025 high of 3452.5 to confirm the upside to extend daily sequence. Short term, it placed ((i)) of 3 at 3365.70 high, ((ii)) at 3282.43 low, (i) of ((iii)) at 3374.96 high & (ii) of ((iii)) at 3319.50 low. It is showing higher high since 2 low in 5 swings, which can be nest or a diagonal sequence, if breaks below 7.09.2025 low before rally higher above 6.29.2025 low. In (i), it ended i at 3330.32 high, ii at 3309.91 low, iii at 3374.02 high, iv at 3353.43 low & v at 3374.96 high. In (ii) pullback, it placed a at 3340.76 low, b at 3366.38 high & c as diagonal at 3319.50 low. It already broke above (i) high, confirmed upside can be possible as long as it stays above 3319.50 low.

Currently, it favors pullback in ii of (iii), while placed i at 3377.48 high. It expect pullback in 3 swings to hold above 3319.50 low before rally continue in iii of (iii). The further upside confirms when it break above 3452.50 high. Five swings rally from 6.29.2025 low, suggests more upside should be unfold. The next leg higher expect to erase the momentum divergence in 1-hour to be (iii) of ((iii)). Alternatively, if it breaks below 7.09.2025 low, it can be pullback against 6.29.2025 low, while ended ((i)) in diagonal at 3377.48 high. Gold is choppy after April-2025 peak. It can even do double correction, if breaks below 6.29.2025 low, correcting against May-2025 low before rally continue. We like to buy the pullback in 3, 7, or 11 swings pullback as it is bullish in weekly sequence.

XAUUSD (GOLD) – 60-Minute Elliott Wave Technical Chart:

XAUUSD (GOLD) Elliott Wave Technical Video:

https://www.youtube.com/watch?v=ba-cPlZc9M4

Markets Sensitive to Trump’s Attempt to Undermine Fed’s Independence

Markets

US President Trump sorted the problem of a dull eco calendar yesterday. Fed Chair Powell is the thorn in the US President’s side. And while he still claims it will be unlikely to fire Powell, he doesn’t rule anything out. Earlier court rulings clearly state that you can’t fire the Fed chair over a policy dispute – Trump is a long term advocate of lower policy rates – but you can do it for cause. One route president Trump seems to be exploring is mismanaging building costs in the renovation process of the Fed’s headquarters in Washington DC. This developing story adds to the ongoing rumours of a rapid confirmation process of Powell’s successor, ie the idea of a Shadow Fed Chair. Markets remain sensitive to Trump’s attempt to undermine the US central bank’s independence (and credibility). The louder he screams to lower short term interest rates, the more he risks driving up long term interest rates. The US 30-yr yield closed above 5% for a second consecutive session with a test of the 5.15% YtD top and the 5.18% 2023 top the likely way to go. US stock markets and the dollar traded volatile intraday on rumours about firing Powell soon which were later than denied. The S&P 500 lost almost 1% intraday, only to close 0.32% higher. EUR/USD spiked from levels just above 1.1560 to above 1.17, before finding a closing equilibrium near 1.1640. Throughout all the fuzz, a very large majority of Fed governors are backing Powell’s stance on (stable) interest rates in light of upside inflation risks. NY Fed Williams sees tariffs adding about one percentage point to inflation through H2 2025 and into 2026 with a weaker dollar adding somewhat to price pressures. “Maintaining this modestly restrictive stance of monetary policy is therefore entirely appropriate.”

Today’s eco calendar contains US retail sales, weekly jobless claims and Philly Fed business outlook. We don’t expect a lasting market impact following the decent early July US labour market data and this week’s sticky inflation numbers. Risks around the Fed chair story are asymmetric with any steps towards ousting Powell being a potential fire starter for US asset sales. UK labour market data this morning suggest that the BoE will stick with it’s gradual and careful cutting guidance when it lowers interest rates by another 25 bps at its early August policy meeting. Sterling might get some temporary reprieve after approaching the EUR/GBP 0.87 handle a second time yesterday. We err on the side of offloading any GBP exposure in case of short-term GBP-rally’s.

News & Views

Australian labour market data surprised negatively for the second consecutive month. Employment grew a meager 2k in June after the 1.1k contraction in May. Full time employment declined by 38.2k. This was ‘compensated’ for with a 40.2k rebound in part time employment. The unemployment rate jumped from 4.1% to 4.3% (highest since Nov 2021) as the number of unemployed people rose by 34k. Hours worked declined 0.9% in June, but following a 1.4% rise in May. The participation rate rose marginally from 67% to 67.1%. The Reserve Bank of Australia at the July 8 meeting left its policy rate unchanged at 3.85%, while the majority in the market expected a 25 bps cut. At the time, the RBA indicated that economic data were largely in line with its May forecast with inflation marginally higher. The RBA assessed the labour market as being tight. It indicated that wage growth was softening from its peak but productivity growth not picking up and growth in unit labour costs remaining high. In this uncertain context the RBA concluded that it could wait a little longer to see whether inflation returns to 2.5%. The central bank now might gradually give more weight to labour weakness. Key quarterly inflation data will be published on July 30. Markets fully discount a 25 bps cut at the August 12 meeting. The 3-y bond yields drops 8.8 bps to 3.42%. AUD/USD is falling below the 0.65 mark (from 0.653).

The European commission yesterday proposed its new budget (Multiannual Financial Framework) for the 2028-2034 period. It consists of almost €2tn, or 1.26% of the average EU gross national income between 2028 and 2034 1.13% in the previous budget). The majority of the funding comes from EU members states, but the commission also puts in place several new sources to fund the budget. Major priorities in the budget are supporting European competitiveness, prosperity and security. The budget also includes €100bn funding for Ukraine. Funding for agriculture will be reduced. Several countries already objected parts of the proposal. Yesterday’s proposal kickstarts an lengthy process of negotiations that ultimately will have to be agreed upon by EU members states (unanimously) by end 2027.

The Fed Drama

The day Donald Trump was re-elected for a second term as US President, we knew the headlines would be full of twists and turns. We expected surprising and unusual news every day—and yet, what we’ve seen so far has exceeded our expectations and prepared us for little. What’s happening feels surreal, and yesterday was no exception.

The New York Times reported that Trump had drafted a letter to fire Federal Reserve (Fed) Chair Jerome Powell and asked GOP members for feedback. This news brought nothing new—everyone knows the relationship between the two men is frosty—but the mere drafting of a letter made things feel more serious and triggered volatility. The US dollar dropped sharply, and the 2-year Treasury yield tanked amid expectations that Powell’s replacement would aggressively cut rates to please Trump.

Then Trump denied any plans to fire Powell, saying he was only discussing the idea in concept. I’m quoting Bloomberg here: “that he is only discussing it in concept”—the concept of firing the Fed Chair because he’s not making the decisions Trump wants, even though Powell’s decisions make sense given economic realities.

Markets caught their breath after this initial shock, but investors remain skeptical about what comes next. In Turkish, we say, “where there’s no fire, there’s no smoke.” Here, we know that the smoke is coming from a big fire. The consequences of such an attack on the Fed’s independence could be dramatic. Not only would the US dollar and Treasuries tumble, but the Fed would lose a superpower: the one that helps it support turmoiled financial markets by buying billions of dollars in US debt.

Remember, the US—and a few privileged economic zones—are unique in that government bonds can be supported by their central banks purchasing their debt. This is due to credibility. If that credibility is lost, the Fed loses its most important tool. Believe me, if the Turkish central bank bought Turkish government bonds to finance government debt—yes, even the sound of it is funny—that would just be printing money, which in theory should lose its value. If QE and the Fed’s expanding balance sheet have worked so well over decades, it’s because the Fed enjoys a level of credibility that few others do. If that credibility disappears, lowering rates would severely hurt both the dollar and Treasuries.

In summary: keep an eye on safer havens—it looks like we might see some serious action at the Fed this fall.

Big banks’ record trading revenues

Trump’s comments on Powell caused some selloff across major US indices, but the S&P 500 still managed to close with gains. Softer-than-expected PPI data helped cool mounting inflation fears after the previous day’s CPI print surprised on the upside.

Bank earnings continued to impress. Goldman Sachs’ equity trading desk, for example, posted its best revenue in Wall Street history. Morgan Stanley and Bank of America scored their best Q2 results on record, benefiting from the high market volatility driven by constant twists in White House policies with global repercussions. The SPDR Financial Sector ETF fell to a three-week low before rebounding, though its daily chart looks toppish after a 24% rally since the April dip.

Elsewhere, Nvidia consolidated gains near a record high. Alphabet extended modest gains to $185 per share on news that it will debut new Pixel-branded hardware at an event on August 20, including several smartphones and a smartwatch powered by its own AI technology. Given the market’s muted reaction, investors don’t expect this to be a ‘first iPhone reveal’ level event. But since the iPhone is falling behind tech peers in the AI race, the window to replace it with a new big gadget is wide open. Note that the iPhone has dominated for nearly two decades—much longer than predecessors like Nokia, Ericsson, or BlackBerry, who all had their star moments but for much shorter periods. I’m not saying Google will invent the next big thing, but AI is about to get a face. Who will deliver it? We’ll find out.

Speaking of AI, ASML reported better-than-expected revenue and earnings yesterday but still suffered an 8% post-earnings slump due to uncertainties about next year’s revenue growth amid trade restrictions. The stock fell off its bullish trend from April through yesterday. However, ASML remains the sole chip equipment maker for the world’s leading chipmakers, so its business outlook is tied closely to theirs. This dip could be an interesting buying opportunity, though the broad AI rally should be approached with some caution. The divergence between semiconductors and ASML suggests the two should eventually converge.

Zooming out, the Stoxx 600 index remained under pressure yesterday despite gains in the S&P 500, weighed down by ongoing trade tensions. European leaders have agreed to retaliate if the threatened 30% US tariffs materialize. Potential measures include taxes on US tech giants, targeted curbs on US investments in the EU, and limited access for US companies to bid for European public contracts.

We’ll see if Trump chickens out—and whether this triggers a market correction. I often watch market corrections from my summer vacation—and I’ll be on vacation starting tomorrow.