Sample Category Title

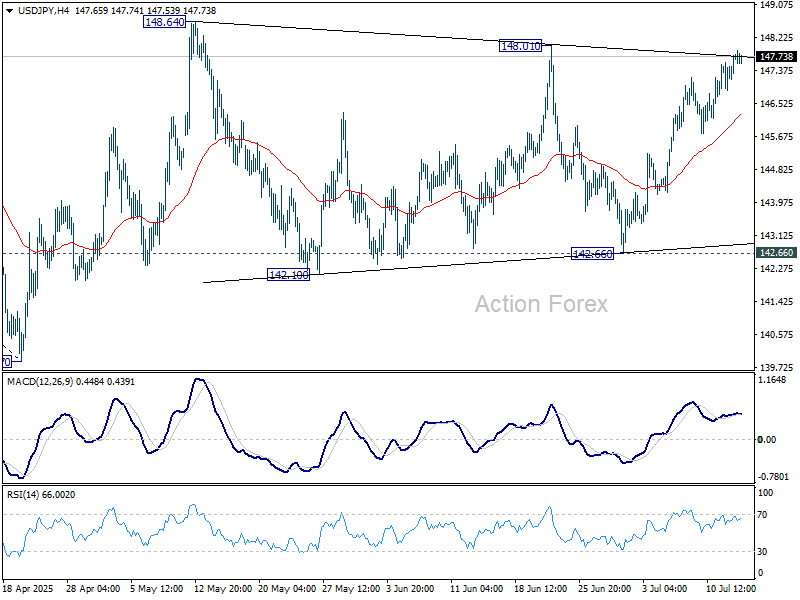

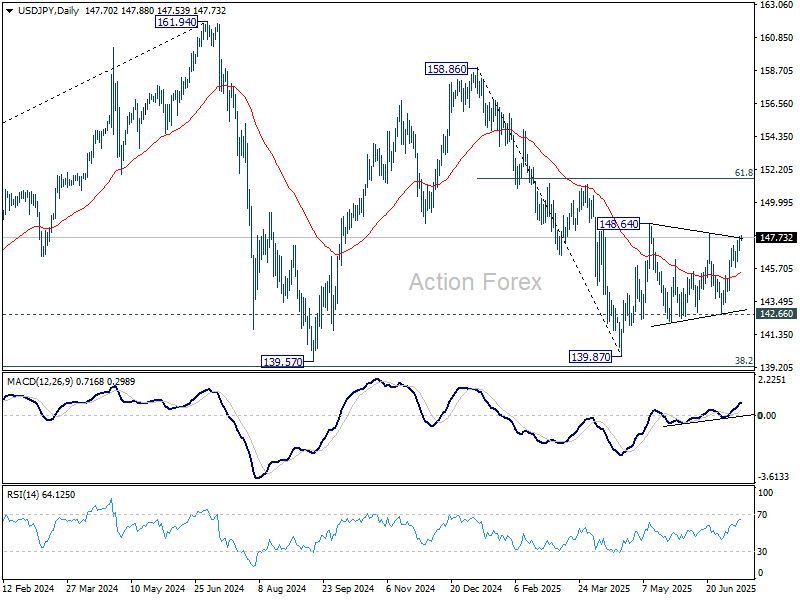

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.13; (P) 147.46; (R1) 148.05; More...

Intraday bias in USD/JPY remains neutral with focus on 148.01 resistance. Firm break there will indicate that consolidations pattern from 148.64 has completed. Further rise should then be seen to resume the rally from 139.87, to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

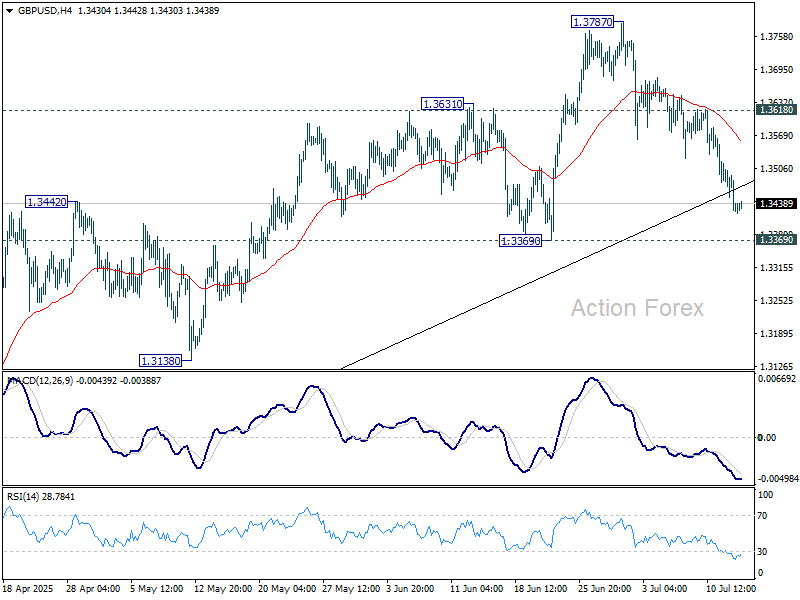

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3396; (P) 1.3454; (R1) 1.3484; More...

Intraday bias in GBP/USD remains neutral. Pullback from 1.3787 could extend lower but downside is expected to be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. However, firm break of 1.3369 will bring deeper correction back to 1.2706/3206 support zone.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3019) holds, even in case of deep pullback.

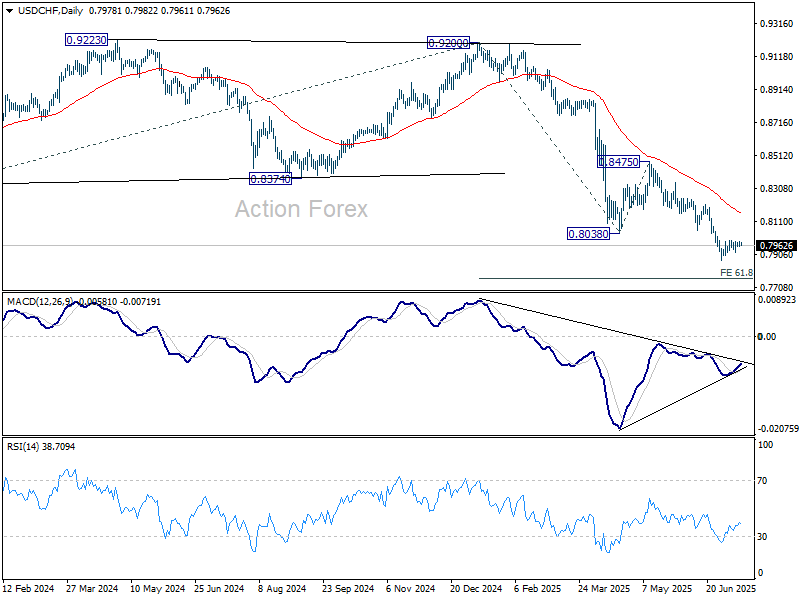

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7962; (P) 0.7973; (R1) 0.7992; More….

Intraday bias in USD/CHF remains neutral as consolidations continue above 0.7871. Stronger recovery might be seen but upside should be limited by 0.8054 support turned resistance. On the downside, firm break of 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

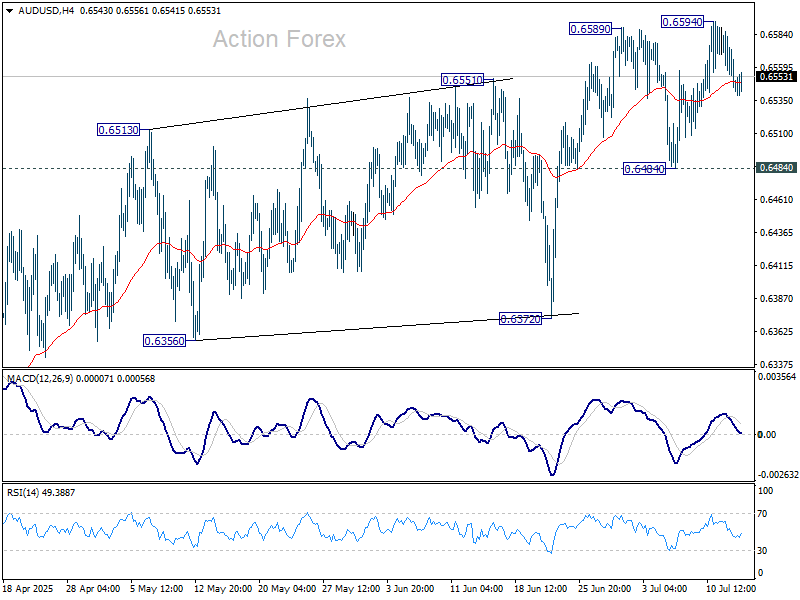

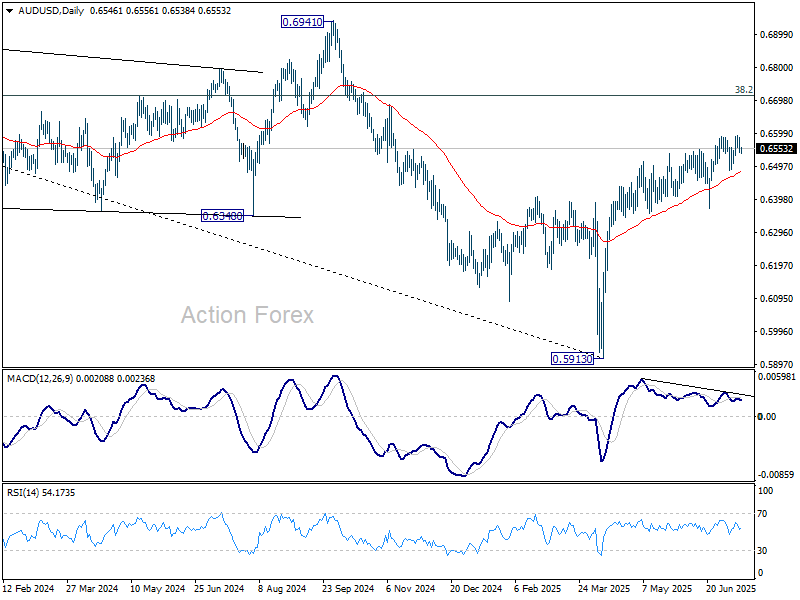

AUD/USD Daily Report

Daily Pivots: (S1) 0.6530; (P) 0.6559; (R1) 0.6575; More...

Intraday bias in AUD/USD remains neutral and more consolidations would be seen below 0.6594. Further rise is expected as long as 0.6484 support holds. Above 0.6594 will resume the rally from 0.5913 and target 0.6713 fibonacci level.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

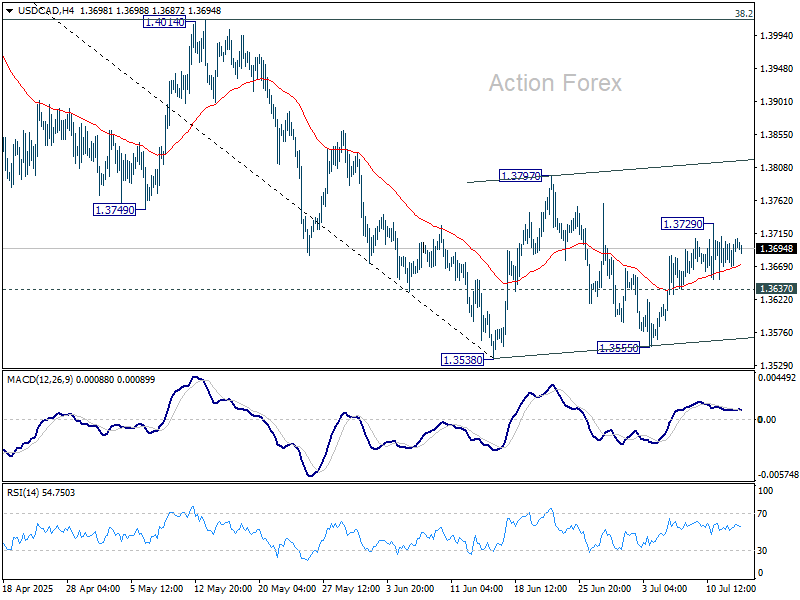

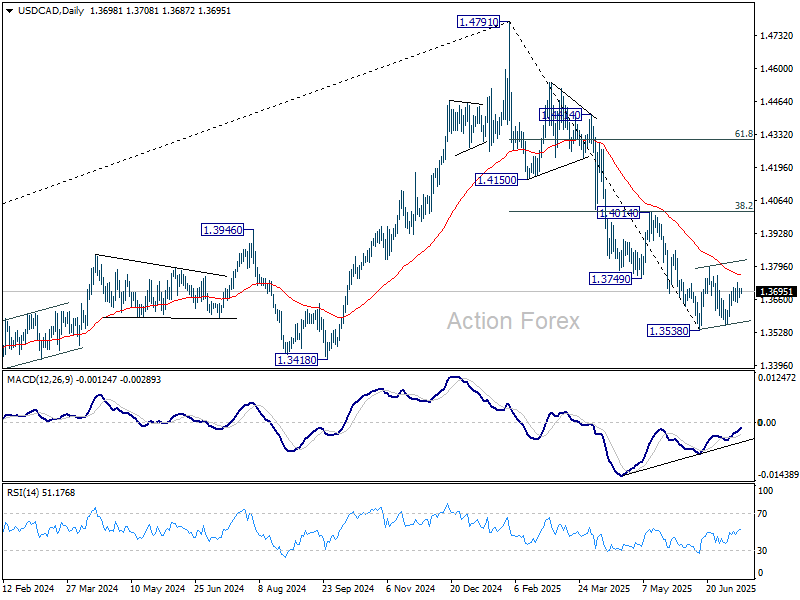

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3680; (P) 1.3695; (R1) 1.3719; More...

Intraday bias in USD/CAD stays neutral for the moment. Overall, price actions from 1.3538 are seen as a corrective pattern, which is now in its third leg. Stronger rise could be seen and above 1.3728 will target 1.3797 resistance and probably above. On the downside, break of 1.3637 minor support will bring retest of 1.3538/55 support zone.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

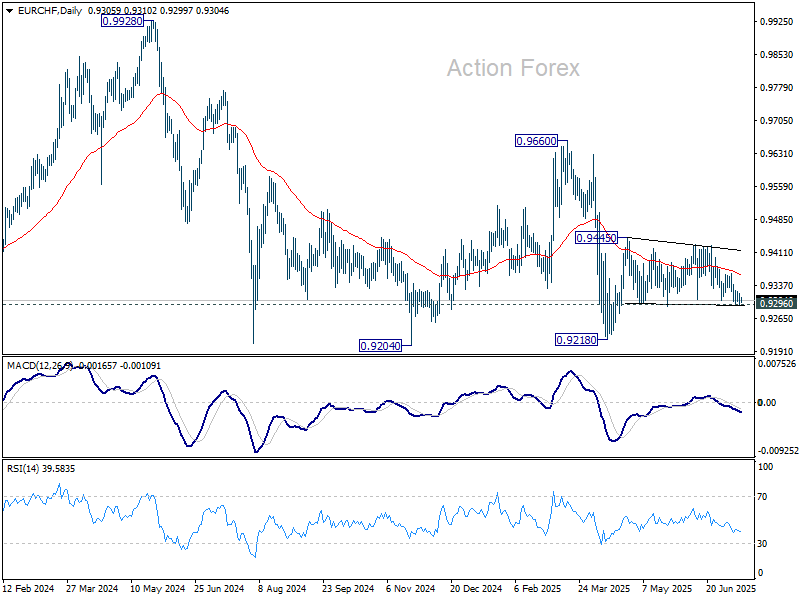

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9298; (P) 0.9309; (R1) 0.9322; More....

Intraday bias in EUR/CHF remains neutral for the moment. . On the upside, break of 0.9428/45 resistance zone will resume the rebound from 0.9218. On the downside, firm break of 0.9296 support will bring retest of 0.9218 low instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9437) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

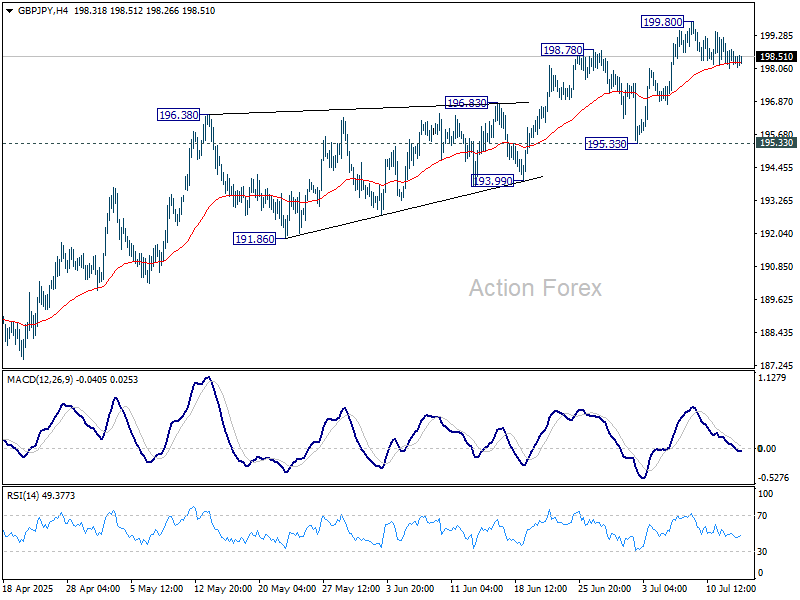

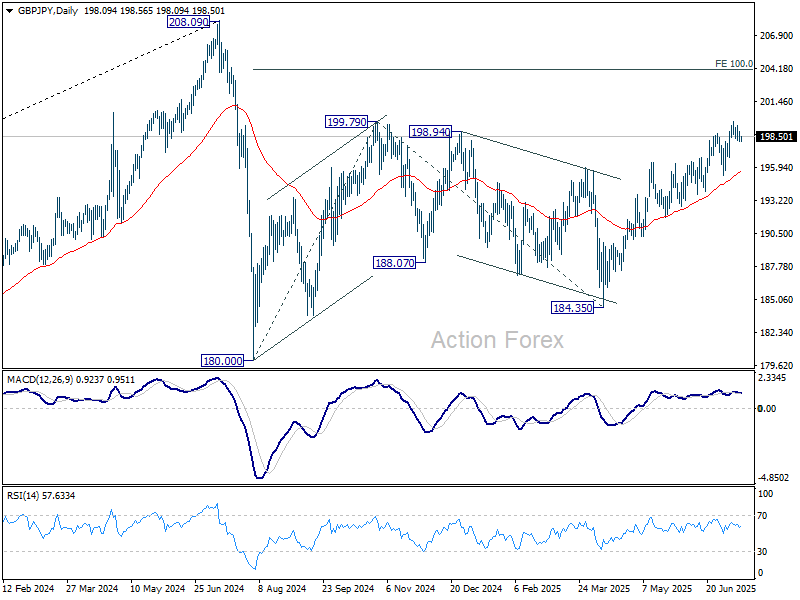

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.97; (P) 198.48; (R1) 198.86; More...

Intraday bias in GBP/JPY remains neutral first and more consolidations could be seen below 199.87. While deeper retreat cannot be ruled out, further rise is expected as long as 195.33 support holds. On the upside, break of 199.80 will resume the rally from 184.35 and target 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

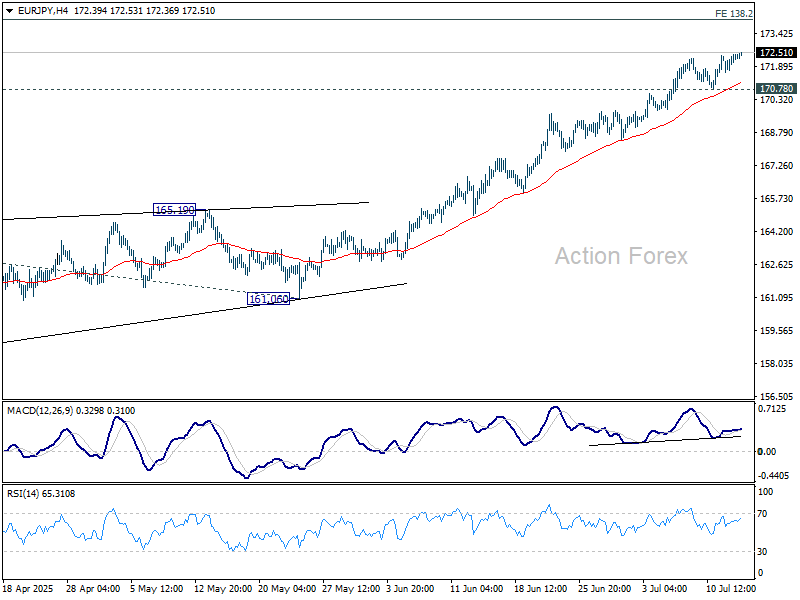

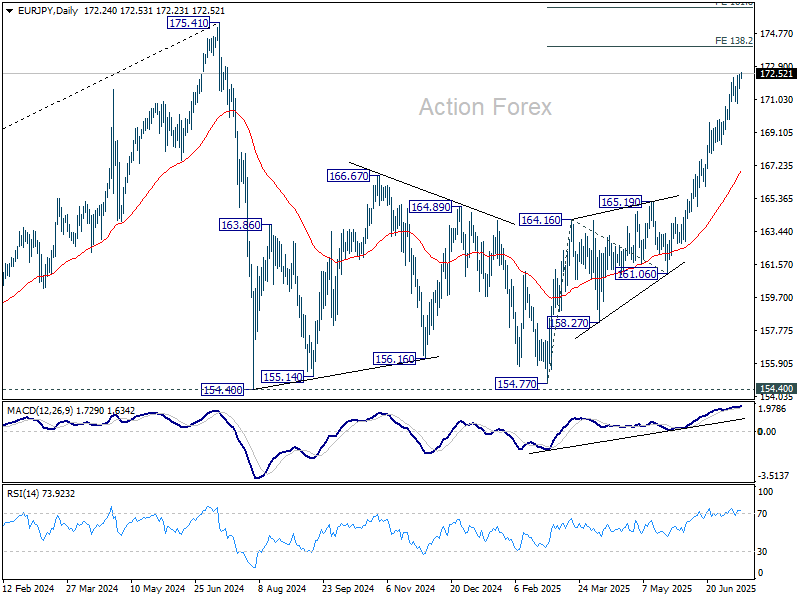

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.85; (P) 172.16; (R1) 172.64; More...

EUR/JPY's rally from 154.77 is in progress and intraday bias stays on the upside. Next target is 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. On the downside, below 170.78 support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, price actions from 175.41 (2024 high) are seen as correction to up trend from 114.42 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. Meanwhile, decisive break of 175.41 will confirm long term up trend resumption.

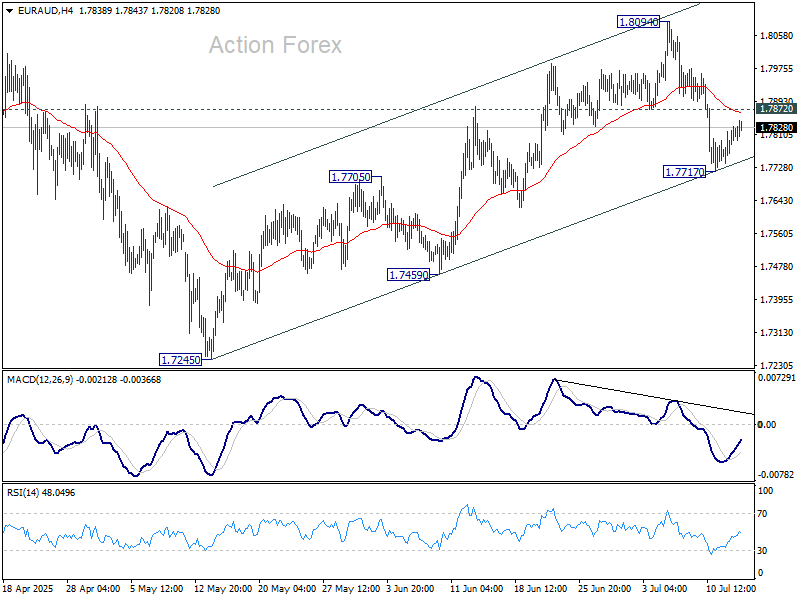

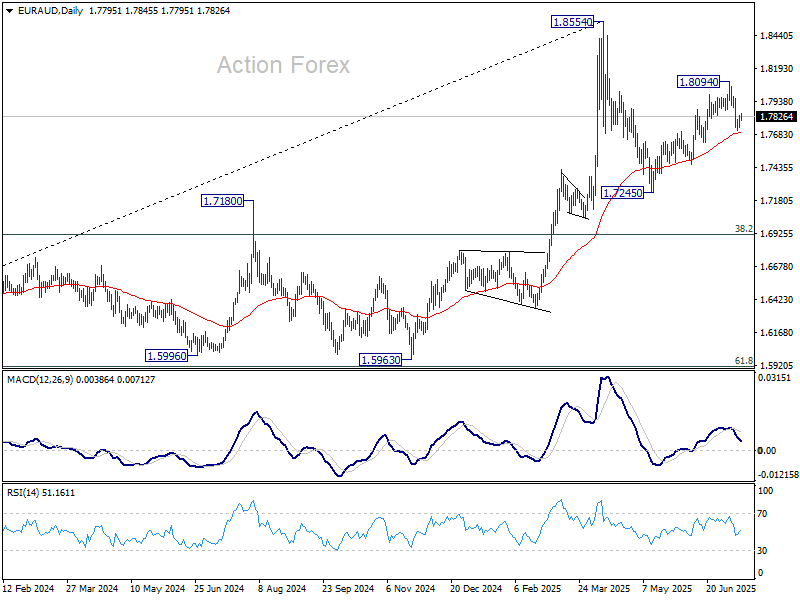

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7764; (P) 1.7798; (R1) 1.7856; More...

A temporary low is formed at 1.7717 in EUR/AUD with current recovery, and intraday bias is turned neutral first. On the downside, sustained trading below 55 D EMA (now at 1.7703) will argue that corrective pattern from 1.8554 is already in the third leg. Deeper fall should then be seen back to 1.7245 support. Nevertheless, strong rebound from 55 D EMA will maintain near term bullishness. Break of 1.7872 support turned resistance will bring retest of 1.8094 resistance.

In the bigger picture, price actions from 1.8554 medium term are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

The Disconnect Grows

The market reaction to the weekend’s tariff threats — this time targeting a 50% tariff on Mexican and European exports to the US — was mostly hopeful: that they won’t materialize. That’s how markets traded the news — on the assumption that negotiations will water things down to a 15%-ish rate, at least for the Europeans.

As such, losses in European stock markets remained contained, with the Stoxx 600 closing the session near flat, holding above the 50-day moving average. Major US indices even eked out gains, with the S&P500 hovering just a few points below all-time highs. All this, despite EU politicians’ retaliation plans targeting $84 billion worth of US goods — including cars, bourbon, and Boeing planes. Anyone care?

One bright spot: Nvidia has reportedly been cleared to resume selling its H20 chips to China. Given that the risks to its Chinese business were already broadly priced in, this could provide a tailwind. China also printed stronger-than-expected growth and industrial production figures this morning. But beyond that, the broader news remains less than encouraging — yet equity futures are in the green.

The disconnect

Meanwhile, the sovereign bond space is flashing warning signals. Long-term yields are spiking. Japan’s 30-year yield surged nearly 18bps on Monday and climbed further this morning to 3.20% — historically high territory. Investors are bracing for the possibility that the LDP maintains its majority in Sunday’s Upper House election, which would likely be seen as a mandate for further fiscal expansion — and fuel concerns over Japan’s already precarious debt sustainability.

PS: the Japanese government had already announced a reduction in the supply of these long bonds last month in an effort to calm the selloff — but the fears persist. Rising Japanese yields are having a domino effect across Western sovereign markets. The US 30-year yield continues flirting with the 5% psychological threshold, and a broad gauge of European 10-year yields spiked past 2.70%.

Rising yields are bad news for global risk appetite — or at least they should be in a rational market — as they imply higher borrowing costs for businesses. But again, no one seems to care.

Risks are piling up

Risks are piling up: the risk of global supply chain disruptions, a tariff-led jump in US inflation, pressure on company earnings, an unsustainable surge in G7 debt levels, political risks, geopolitical risks... Even if Trump backs down for now, the measures already in place — coupled with rising borrowing costs — will have real-world consequences sooner rather than later.

For US companies, the dollar’s more than 10% depreciation in H1 is expected to provide a boost to earnings, as roughly 40% of S&P500 revenues come from abroad and will translate into higher dollar revenue when converted back for reporting. But European companies won’t benefit from currency relief. The euro and Swiss franc appreciated significantly in the first half of the year. On top of that, many companies chose to ‘eat the tariffs’ — absorbing the cost to preserve their US market share while waiting for the trade dust to settle. This will show up somewhere — but markets don’t seem to have priced it in yet.

US banks kick off earnings

US big banks will start reporting Q2 earnings in the coming hours and days, and they’re expected to post a 1% decline in Q2. Meanwhile, the S&P500 Financials sector has rallied roughly 24% since the April dip. Looser regulations may be one reason behind the rally, as investors anticipate more lending capacity and better margins — yet the 24% rally barely matches the 1% decline in earnings. The bad news is that a 1% earnings drop is not great news. The good news is that it sets a low bar. If expectations are beaten, the rally could continue — despite the earnings decline. But slowing earnings will eventually make valuations too rich to ignore.

Even though the consensus expects a decent US earnings season, the widening gap between investor optimism and economic reality increases the risk of a sharp reversal. The more investors ignore troubling signals, the higher the chance of a painful correction.

On the macro front, the US will release its latest CPI data today. Both headline and core inflation are expected to accelerate from 0.1% to 0.3% MoM in June, driven by tariff-related pressures on cars, toys, furniture, and other exposed goods. Recent downside surprises in inflation were largely due to companies offloading existing stockpiles — built up ahead of tariff implementation. But those buffers are shrinking, and new imports will inevitably show up in prices. If inflation doesn't rise, it will mean companies are absorbing the costs — again, someone will pay. Whether it's the American consumer or the foreign exporter depends on product-level price sensitivity.

So, something has to give — but when and where remains the big unknown. It’s worth watching the economic data, the earnings, and global yields closely.