Sample Category Title

Markets Cautious But Not Panicked, Hope for US-EU Deal Remains

The reaction to US President Donald Trump’s latest tariff salvo has been relatively muted so far. Germany’s DAX and France’s CAC opened mildly lower, but losses remain limited. In currency markets, Euro is holding steady, trading largely inside Friday’s ranges without triggering major downside momentum. The market appears to be bracing for drawn-out negotiations rather than immediate escalation.

Optimism is underpinned by Trump’s negotiation history—often characterized by bold opening demands followed by compromise. The fact that the 30% tariff on EU imports is scheduled to take effect in August, not immediately, reinforces the view that space remains for a diplomatic resolution. The final rate will likely land well below 30%, even though above the UK's 10% benchmark.

European Trade Commissioner Maros Sefcovic warned Monday that the 30% tariff would severely disrupt transatlantic trade, but voiced hope that a resolution could still be achieved. “We have to do everything we can to prevent this super-negative scenario,” he said. Talks between the EU and Washington are ongoing, and the EU has not yet announced any retaliatory measures, which has helped temper market nerves.

Elsewhere, South Korea is also looking for a way out of the tariff web. Trade Minister Yeo Han-koo said an in-principle agreement might be achievable before August 1. Speaking to local media, he hinted Seoul may open up its agricultural markets while protecting strategic industrial sectors. “Twenty days are not enough to come up with a perfect treaty,” he acknowledged, but reiterated the urgency of preventing damaging tariffs on Korean exports.

In currency markets, the Canadian Dollar is leading gains, while Swiss Franc and Yen are benefitting from mild safe-haven demand. New Zealand and Australian Dollars remain under pressure, despite China’s better-than-expected trade numbers. Sterling is weak as well. Dollar and Euro are trading near mid-pack.

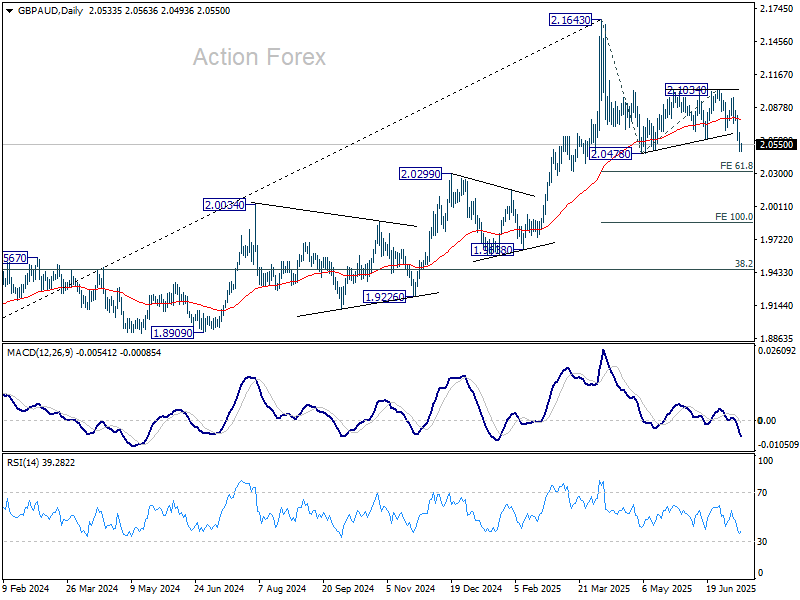

Technically, one pair to watch is GBP/AUD. After last week's extended decline, it's now pressing 2.0478 support. Firm break there will resume whole fall from 2.1643, and target 61.8% projection of 2.1643 to 2.0478 from 2.1034 at 2.0314. Decisive break there could prompt further acceleration to 100% projection at 1.9869.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is down -0.89%. CAC is down -0.42%. UK 10-year yield is down -0.009 at 4.620. Germany 10-year yield is up 0.01 at 2.735. Earlier in Asia, Nikkei fell -0.28%. Hong Kong HSI rose 0.26%. China Shanghai SSE rose 0.27%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield rose 0.07 to 1.577.

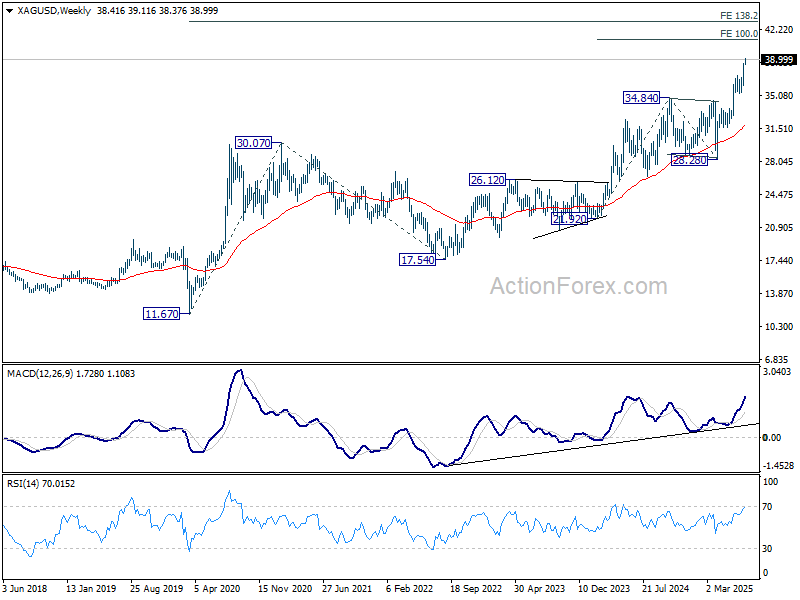

Silver hits near 14-year high and targest 40 as global flows accelerate

Silver’s rally picked up pace on Monday, hitting its highest level since late 2011 after last week’s decisive upside breakout. The metal has surged alongside broad-based strength in precious metals, with Palladium reaching its highest since October 2024 and Gold rebounding to a three-week high. Renewed investor interest across the complex suggests increasing demand for portfolio diversification amid geopolitical and trade policy risks.

One notable driver has been rising demand out of India, where investors are shifting from Gold to Silver as a catch-up trade after years of underperformance. Silver is also seeing structural demand growth tied to industrial applications—especially in solar energy and electric vehicles—which is outpacing domestic production. This dual push from both speculative and real-economy buyers is adding fuel to the current run.

Technically, Silver is on track to 61.8% projection of 31.65 to 37.28 from 36.24 at 39.71, or even further to 40 pscyholgical level. However, upside could be capped by medium term level of 100% projection of 21.92 to 34.83 from 28.28 at 41.20 on first attempt.

NZ BNZ services rises to 47.3, but outlook remains grim

New Zealand’s services sector showed mild improvement in June, with BusinessNZ Performance of Services Index rising to 47.3 from May’s 44.1. Despite the gain, the index remains well below its long-run average of 52.9 and firmly in contraction territory. Subcomponents showed modest upticks—new orders rose from 43.4 to 48.8, employment edged up from 47.1 to 47.4, and activity/sales climbed to 44.5. Inventories just breached the 50-mark at 50.6.

Still, the broader backdrop remains discouraging. 66.2% of surveyed businesses offered negative comments, citing subdued consumer confidence, elevated living costs, and policy-related uncertainty. Public sector retrenchment, inflation, and rising interest rates continue to bite, while seasonal factors like winter and lower tourist activity weigh on demand. BNZ’s Doug Steel summed it up bluntly: “The timeline for New Zealand’s long-awaited economic recovery just keeps getting pushed further and further out.”

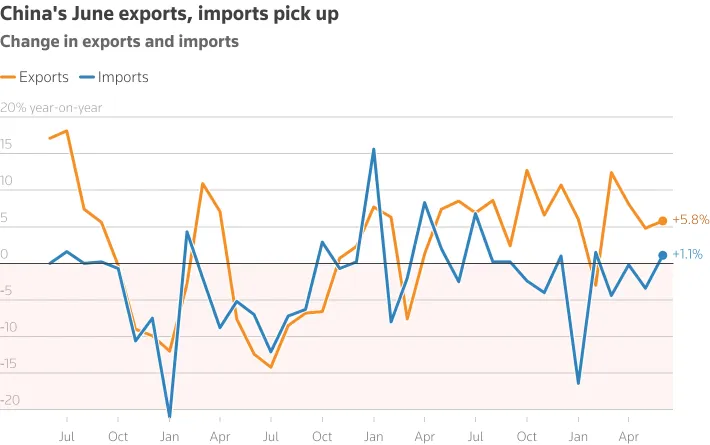

China’s exports growth accelerates to 5.8% yoy in June on tariff truce window

China’s exports rose 5.8% yoy in June, beating expectations of 5.0% yoy and marking a pickup from May’s 4.8% yoy. The improvement comes as exporters moved quickly to take advantage of the 90-day tariff truce with the US, front-loading shipments ahead of anticipated disruptions.

The stronger-than-expected performance helped lift China’s trade surplus to USD 114.8B, slightly above consensus and up from USD 103.2B in May.

Imports rose 1.1% yoy, the first positive reading of the year and a tentative sign of stabilization in domestic demand.

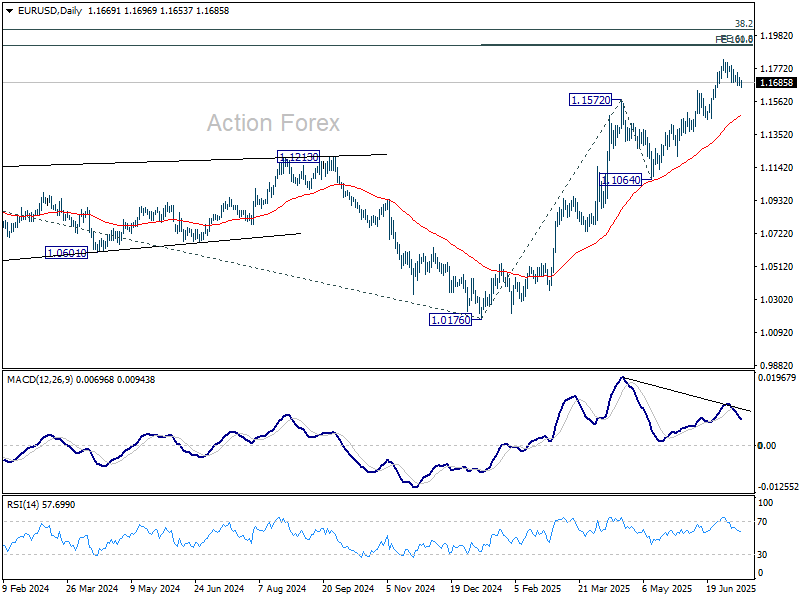

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1665; (P) 1.1690; (R1) 1.1714; More...

EUR/USD is still extending the correction from 1.1829 and intraday bias remains neutral for the moment. Downside should be 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, sustained break of 1.1630 will bring deeper fall to 55 D EMA (now at 1.1474) instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Silver hits near 14-year high and targest 40 as global flows accelerate

Silver’s rally picked up pace on Monday, hitting its highest level since late 2011 after last week’s decisive upside breakout. The metal has surged alongside broad-based strength in precious metals, with Palladium reaching its highest since October 2024 and Gold rebounding to a three-week high. Renewed investor interest across the complex suggests increasing demand for portfolio diversification amid geopolitical and trade policy risks.

One notable driver has been rising demand out of India, where investors are shifting from Gold to Silver as a catch-up trade after years of underperformance. Silver is also seeing structural demand growth tied to industrial applications—especially in solar energy and electric vehicles—which is outpacing domestic production. This dual push from both speculative and real-economy buyers is adding fuel to the current run.

Technically, Silver is on track to 61.8% projection of 31.65 to 37.28 from 36.24 at 39.71, or even further to 40 psychological level. However, upside could be capped by medium term level of 100% projection of 21.92 to 34.83 from 28.28 at 41.20 on first attempt.

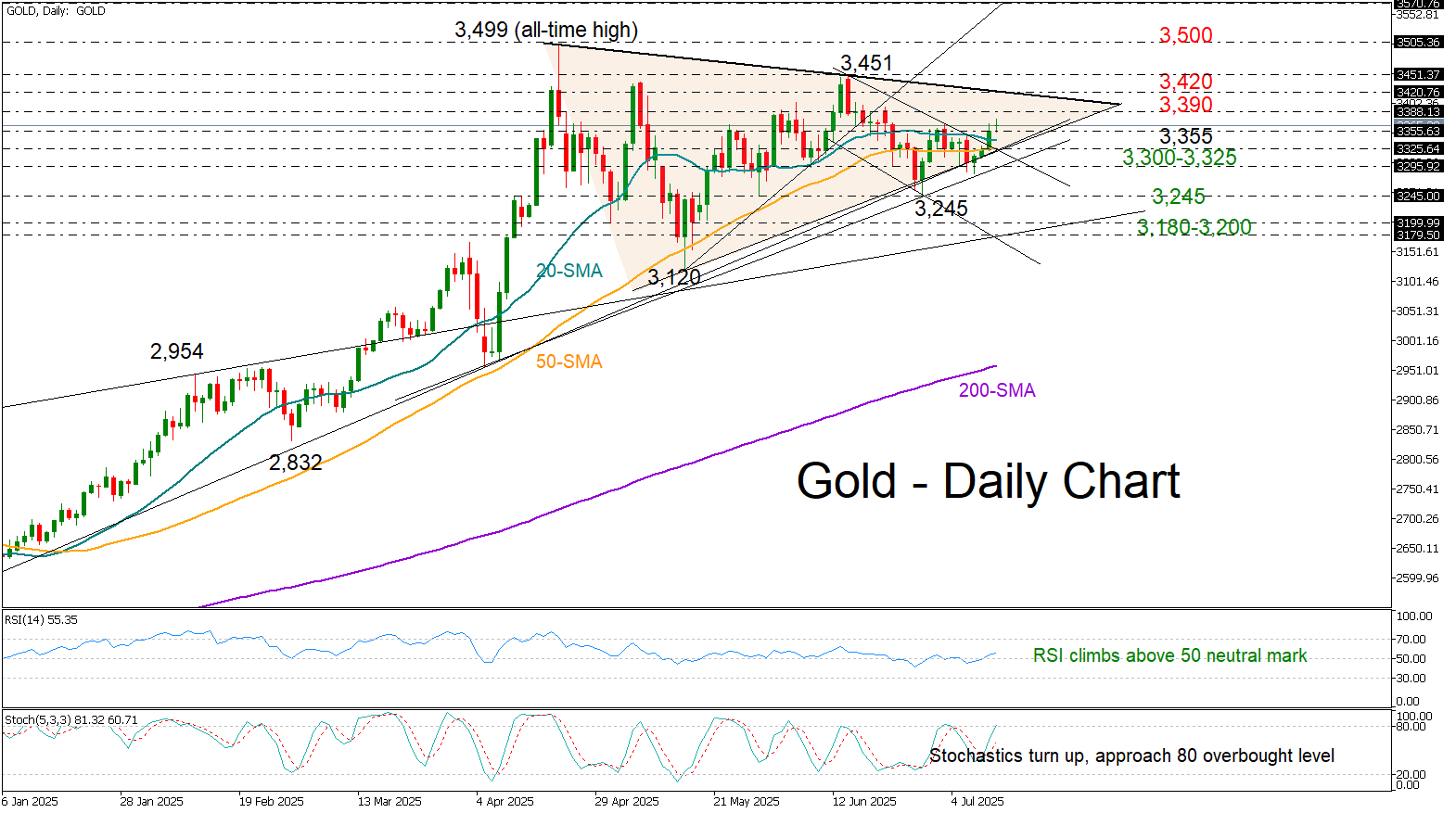

Gold: Is the Latest Bounce Sustainable?

- Gold crosses above 3,355 resistance as tariffs threats return.

- Short-term bias is positive but key obstacles still lie ahead.

- Support at 3,300–3,325 critical for downside risk.

Gold opened Monday’s session with a mild upside gap at 3,363 and above its short-term simple moving averages (SMAs), following President Trump’s announcement of increased tariffs on European Union and Mexican goods – raising them to 30% effective August 1.

Investors did not react aggressively, interpreting the move as another negotiating tactic by the U.S. president to accelerate progress in the trade talks. Nevertheless, Friday’s channel breakout, followed by Monday’s modest upside move, was enough to lift the price above the key 3,355 barrier – a level that has repeatedly capped bullish momentum since April.

The next upside target is the 3,390 resistance zone from June, followed by a tentative descending trendline drawn from April’s peak, currently near 3,420. A decisive break above this trendline could pave the way for a retest of the previous high at 3,450, with the psychological 3,500 level coming into focus next. Further gains could even push the price toward the 161.8% Fibonacci extension of the previous downleg at 3,570, and eventually to the round 3,600 mark.

However, with the stochastic oscillator nearing the 80 overbought threshold, a sustainable breakout above 3,420 cannot be taken for granted. On the downside, the support trendline between 3,300 and 3,325 will be closely monitored. If this floor gives way, selling pressure could intensify, dragging the price toward 3,245, and then potentially down to the 3,180–3,200 zone.

All in all, the precious metal could gain fresh bullish momentum in the coming sessions. However, whether it can strengthen its outlook above 3,420 – and more crucially, resume its record rally beyond 3,500 – remains to be seen.

Bitcoins Surge to $123k. China Exports Rise, DAX Retests 24000 Support

Asian Market Wrap

U.S. and European stock futures dropped at the start of the week after President Trump announced a 30% tariff on goods from the EU and Mexico.

S&P 500 futures fell 0.4%, and European stock futures dipped 0.6%. Meanwhile, Asian stocks stayed mostly flat, with small gains in Hong Kong and China.

President Trump’s new tariff threats are challenging the market’s strength after he increased trade measures on countries like Canada, Brazil, and Algeria last week. Despite warnings, investors seem to expect Trump to back down, as he has done before. This confidence helped the S&P 500 and MSCI All Country World Index hit record highs this month.

The EU had been working on a deal with the U.S. to avoid higher tariffs, but Trump’s latest move has dampened optimism in Brussels. However, he hinted at possible adjustments. The EU is now planning to work more closely with other countries affected by Trump’s tariffs, according to sources.

China Exports Beat Forecasts Ahead of Trump’s Latest Tariff Deadline

China's exports picked up in June as companies hurried to fulfill orders during a temporary tariff truce between Beijing and Washington. Shipments to Southeast Asian transit hubs were especially strong ahead of next month's deadline.

China's exports grew by 5.8% in June 2025, reaching $325.2 billion. This was slightly better than the expected 5% rise and faster than May's 4.8% growth. The increase came as tariff pressures eased temporarily before the August deadline.

Rare-earth exports jumped 32% from May, likely due to agreements made in June to ease restrictions and restore global supply. Last month, the U.S. and China signed deals to reopen rare-earth trade after China's export controls in April disrupted supply chains and caused some auto factories to shut down.

Source: LSEG

European Open

European stocks dropped on Monday, led by carmakers. The STOXX 600 index fell 0.6% to 544.3 points, while most regional indexes also declined. However, the UK's FTSE 100 rose 0.2%.

Adding to trade tensions, Italy's Foreign Minister Antonio Tajani said the EU has prepared $24.5 billion worth of tariffs on U.S. goods if no deal is reached.

In the market, European car stocks fell 1.4%, and the retail sector dropped 1%.

On the bright side, AstraZeneca shares rose 1.9% after announcing that its drug Baxdrostat successfully met key goals in a study for patients with hard-to-treat high blood pressure.

On the FX Front, The euro dropped to a three-week low on Monday, while the U.S. dollar gained slightly, benefiting from tariff uncertainty though it’s unclear if this will continue.

The dollar rose 0.28% against the Mexican peso to 18.6763.

Other currencies saw mixed movements:

The British pound fell 0.15% to 1.3470.

The Japanese yen rose slightly to 147.31 per dollar.

The Australian dollar dropped 0.12% to 0.6566.

The New Zealand dollar slid 0.37% to 0.5987.

Outside of tariffs, Trump said on Sunday it would be "great" if Federal Reserve Chair Jerome Powell stepped down, again pressuring the Fed to lower interest rates.

Traders are waiting for June inflation data, due Tuesday, which could give clues about future U.S. rate cuts. Markets expect the Fed to lower rates by over 50 basis points by December.

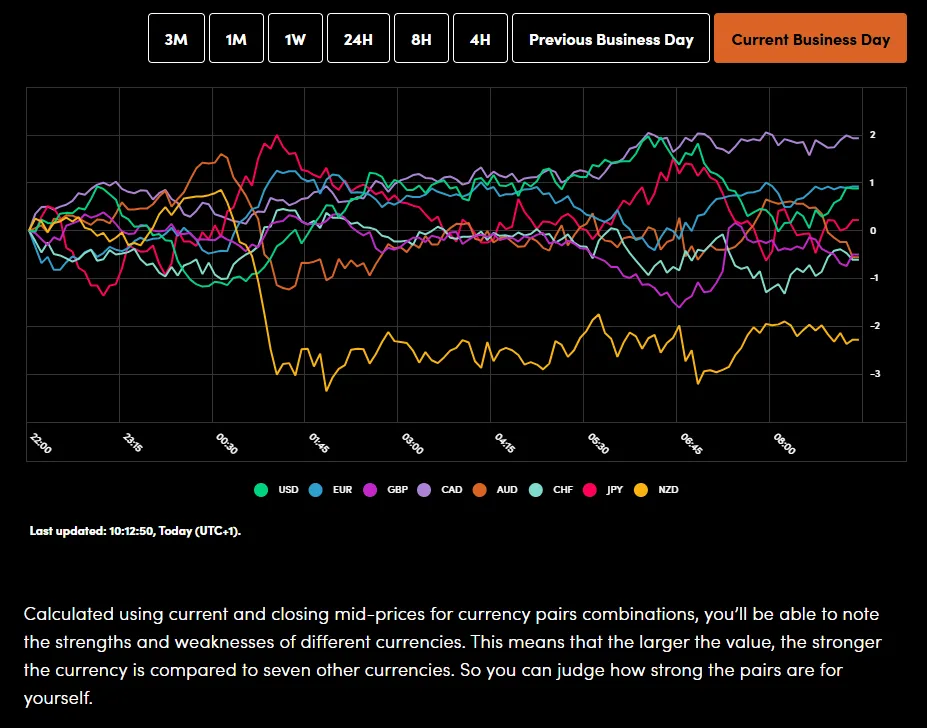

Currency Power Balance

Source: OANDA Labs

Looking at commodities and Oil prices edged higher this morning and trades above the 200-day MA..

Gold prices have been mixed since the market opened last night with choppy price action a sign of the uncertainty at present.

Economic Data Releases and Final Thoughts

Looking at the economic calendar, it is a quiet start to what is expected to be a busy week from a data perspective.

ECB policymakers will be speaking today which is the highlight before Tuesday's US CPI release which will be followed by inflation releases from Canada, UK and Japan later in the week.

Earnings season also gets underway this week with some heavyweights reporting on their Q2 performance and outlook for the rest of the year. Add to this the ongoing tariff and trade developments and markets could be set for a volatile week.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

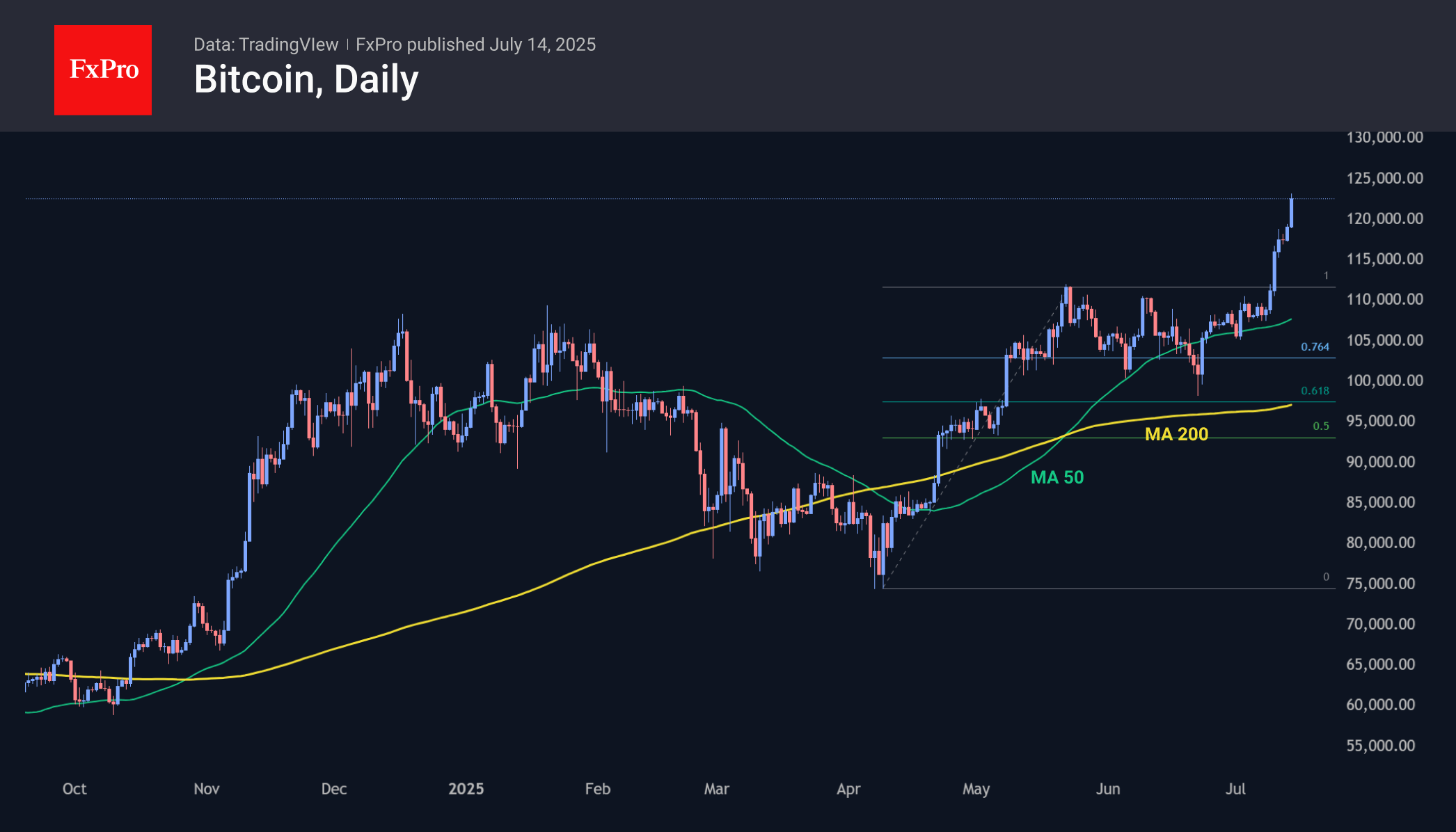

Chart of the Day - Bitcoin (BTC/USD)

From a technical standpoint, Bitcoin has been on a tear printing fresh all-time highs on a regular basis.

Overnight the worlds largest cryptocurrency hit a fresh all-time high just above the $123k mark.

There is a slight pullback this morning down to the $122k but the rally does not appear to be over. There is a possibility of a short-term pullback should market participants indulge in some profit taking but demand remains strong.

Institutional demand spiked over the last two weeks which helped Bitcoin breakout following a period of consolidation.

The rally overnight has now made Bitcoin the 5th largest asset globally (by market cap), surpassing Amazon.

Technical Analysis is a challenge as we have no historical price data to analyze but i will be monitoring whole numbers and psychological levels as well as the RSI for potential moves.

Bitcoin (BTC/USD) Daily Chart, July 14. 2025

Source: TradingView.com (click to enlarge)

Support

- 117500

- 112000

- 109000 (Bear flag retest)

Resistance

- 123236

- 125000

- 130000

GOLD (XAUUSD) Calling the Rally from the Intraday Equal Legs Area

Hello fellow traders,

In this technical article, we are going to present Elliott Wave charts of GOLD (XAUUSD) . As our members know we are long in GOLD from previous equal legs area. As a result, members are now benefiting from profits in positions that remain risk-free. Recently, the commodity completed another intraday correction within the Equal Legs zone. In the following sections, we will outline the current Elliott Wave count.

GOLD 1 Hour Elliott Wave Analysis 07.11.2025

GOLD has completed a 5-wave structure from the 3246.33 low, labeled as wave ((i)) in black. It is currently correcting in wave ((ii)) black, which is unfolding as a Double Three pattern. The correction appears incomplete at this stage. We anticipate further short-term weakness toward the Equal Legs area at 3290.56–3256.9. In that zone, we expect buyers to emerge and initiate another rally toward new highs. Therefore, we recommend avoiding short positions within this area.

GOLD 1 Hour Elliott Wave Analysis 07.11.2025

A few days later, GOLD completed the pullback exactly at the previously mentioned zone. As expected, the commodity found buyers and produced a decent bounce. Wave ((ii)) ended at the 3283.39 low. The short-term cycle from the July 9th low now shows a sequence of higher highs, confirming the continuation of the rally. While price remains above the 3283.39 low, the next expected target area is 3403.85–3432.44.

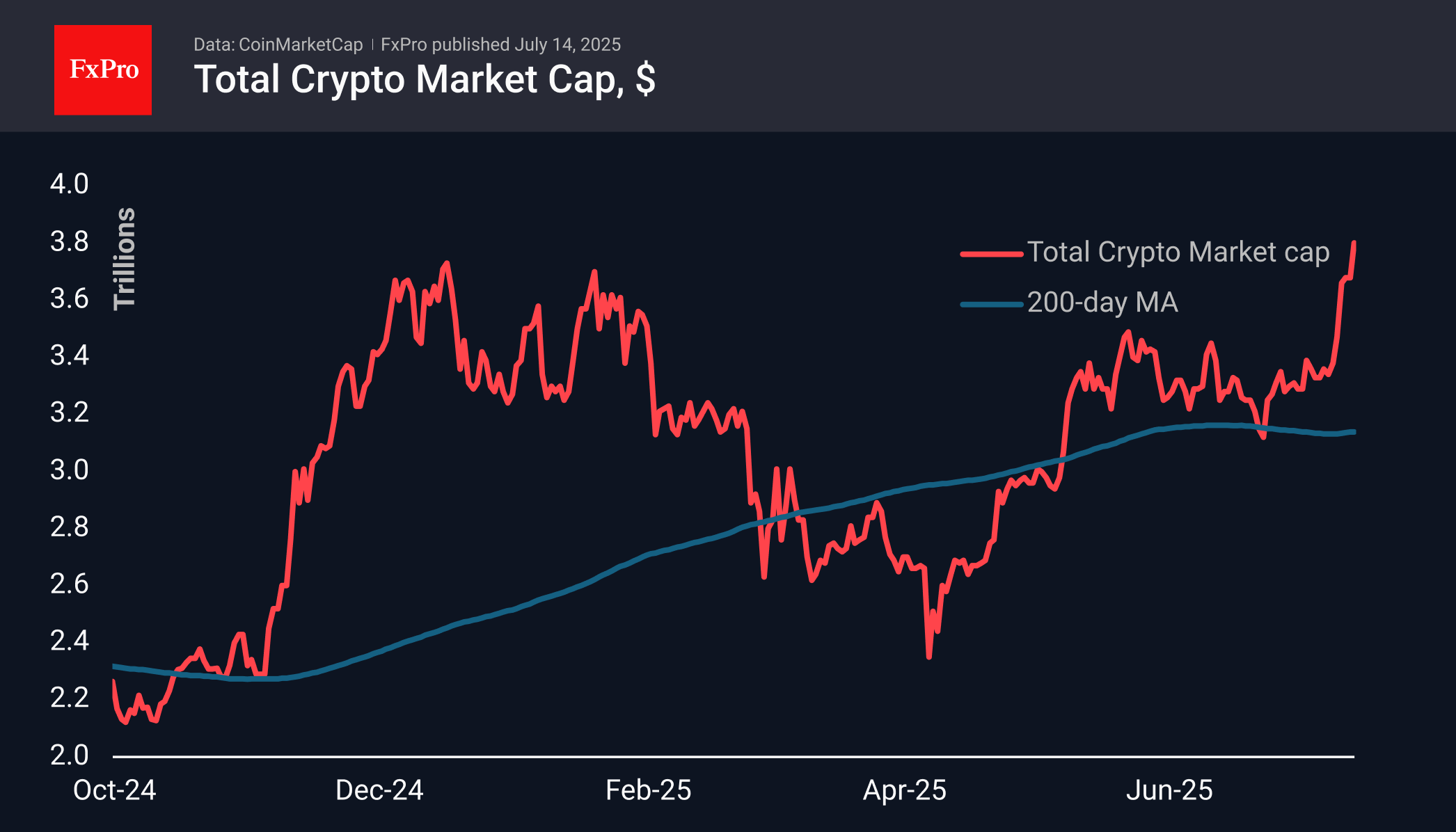

Confident Acceleration of Cryptocurrencies

Market Overview

The crypto market cap reached $3.8 trillion (+4% in 24 hours) and began to update historical highs following the first cryptocurrency. Altcoins outside the top ten are gaining momentum, indicating an expansion of the rally and strengthening positive sentiment.

The cryptocurrency sentiment index is not off the charts, and at 74, it is only on the verge of entering the extreme greed zone. The market is not overheating, retaining its potential for further growth.

Bitcoin has switched to rally mode, constantly updating historical highs and adding almost 13% over the past seven days. This is important growth, as the last six days have seen an update of maximum values. The April-June growth and correction pattern makes us consider the $135K area a potential big target in the short term.

News Background

Inflows into spot Bitcoin ETFs in the US have continued for the fifth week in a row, and for 11 of the last 13 weeks. According to SoSoValue, net inflows into spot BTC ETFs over the past week amounted to $2.72 billion, the highest in the last seven weeks. Cumulative inflows since the approval of Bitcoin ETFs in January 2024 have increased to $52.36 billion.

Inflows into spot Ethereum ETFs in the US have continued for the ninth week in a row, and for 11 of the last 12 weeks. Net inflows into ETH ETFs last week amounted to $908 million, the highest in the entire year of trading. Total net inflows since the ETF’s launch in July 2024 have increased to $5.31 billion.

Improvements in the macroeconomic situation and growing interest from institutional investors have once again boosted interest in Bitcoin, according to Kronos Research. This reflects the growing perception of the first cryptocurrency as a ‘regulated long-term asset’ comparable to gold.

According to Arkham, on 10 July, Bhutan transferred 213.31 BTC ($23.7 million) to the Binance exchange. The exact reason for the transfer is unknown, but such transactions usually precede the sale of assets.

On 10 July, SharpLink Gaming purchased 10,000 ETH from the Ethereum Foundation (EF) for $25.7 million at an average price of $2,572.37. On 11 July, ETH exceeded the $3,000 mark for the first time since early February.

Grayscale Investments has presented a list of 29 cryptocurrencies that should be included in investment products to diversify client assets.

Gold and WTI Crude Oil Climb Higher Amid Market Optimism

Gold price started a fresh increase above the $3,350 resistance level. WTI Crude Oil price climbed higher above $66.50 and might extend gains.

Important Takeaways for Gold and WTI Crude Oil Price Analysis Today

- The gold price started a fresh surge and traded above $3,330.

- A key bullish trend line is forming with support at $3,350 on the hourly chart of gold at FXOpen.

- WTI Crude Oil price started a decent increase above the $66.60 resistance levels.

- There was a break above a connecting bearish trend line with resistance at $67.15 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price formed a base near the $3,280 zone. The price started a steady increase above the $3,330 and $3,350 resistance levels.

There was a decent move above the 50-hour simple moving average and $3,360. The bulls pushed the price above the $3,365 resistance zone. A high was formed near $3,373 and the price is now consolidating.

On the downside, immediate support is near the $3,350 level and the 23.6% Fib retracement level of the upward move from the $3,282 swing low to the $3,373 high.

Besides, there is a key bullish trend line forming with support at $3,350. The next major support sits at $3,330 and the 50% Fib retracement level.

A downside break below the $3,330 support might send the price toward $3,300. Any more losses might send the price toward the $3,280 support zone.

Immediate resistance is near the $3,370 level. The next major resistance is near $3,380. An upside break above $3,380 could send Gold price toward $3,400. Any more gains may perhaps set the pace for an increase toward the $3,420 level.

Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a decent upward move from $65.50. The price gained bullish momentum after it broke the $66.50 resistance and the 50-hour simple moving average.

The bulls pushed the price above the $67.00 and $67.50 resistance levels. There was a break above a connecting bearish trend line with resistance at $67.15.

The recent high was formed at $67.63 and the price started a downside correction. There was a minor move toward the 23.6% Fib retracement level of the upward move from the $65.54 swing low to the $67.63 high.

The RSI is now above the 60 level. Immediate support on the downside is near the $67.15 zone. The next major support on the WTI Crude Oil chart is near the $66.60 zone or the 50% Fib retracement level, below which the price could test the $65.50 level. If there is a downside break, the price might decline toward $64.70. Any more losses may perhaps open the doors for a move toward the $63.50 support zone.

If the price climbs higher again, it could face resistance near $67.85. The next major resistance is near the $70.00 level. Any more gains might send the price toward the $72.50 level.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

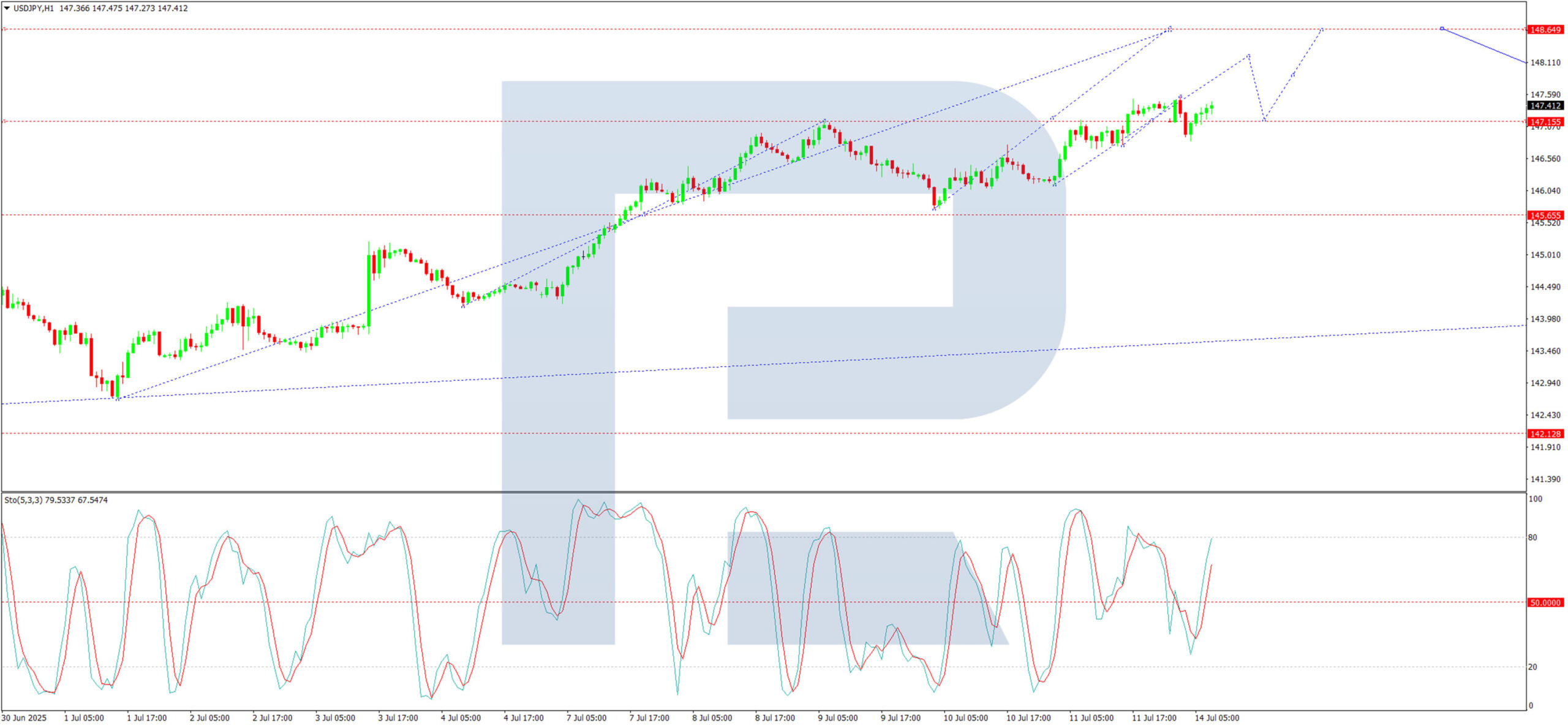

USD/JPY Extends Gains as Market Monitors US Tariff Policy

The USD/JPY pair climbed to 147.42 on Monday. Early in the session, the yen staged a partial recovery from last week’s losses amid heightened global trade risks, but the rebound proved short-lived as the currency resumed its downward trajectory.

Former US President Donald Trump announced plans to impose 30% tariffs on imports from the EU and Mexico, effective from 1 August. In response, officials from both the EU and Mexico signalled their willingness to engage in further negotiations with the US administration, hoping to secure more favourable terms.

Meanwhile, the EU is broadening consultations with other nations affected by the tariffs, including Canada and Japan, potentially paving the way for a coordinated response.

Domestic data from Japan revealed that core machinery orders fell by 0.6% in May (month-on-month), reaching ¥913.5 billion. While still negative, the figure outperformed expectations of a 1.5% decline and marked a notable improvement over April’s steep 9.1% drop.

With a busy week ahead, further volatility in USD/JPY is anticipated.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY continues to advance within the third wave of its corrective movement towards 148.65. Today, we expect the pair to test this level before a potential pullback to 145.65 (testing from above). Subsequently, another upward wave could materialise, targeting at least 150.66. This scenario is supported by the MACD indicator, where the signal line remains above zero and points firmly upward.

H1 Chart:

The H1 chart shows the pair consolidating around 147.17, with the current structure suggesting further upside towards 148.65. Today, we anticipate an initial push to 148.18, followed by a retracement to 147.17, before another rise towards 148.65. The Stochastic oscillator corroborates this outlook, with its signal line positioned at 50 and trending upward.

Conclusion

The USD/JPY pair remains on an upward trajectory, supported by trade policy uncertainties and technical bullish signals. Traders should prepare for potential swings as the market digests incoming economic and political developments.

Asia Stocks Rally on China, Singapore Data; US Futures Dip on Trump’s EU Tariff Threat & Gold Shines

Major US stock indices extended their losses from last Friday into today’s Asian session. Both S&P 500 and Nasdaq 100 E-mini futures dropped by 0.5% at the time of writing, weighed down by renewed tariff anxieties. US President Trump issued a surprise escalation, threatening the European Union with a 30% tariff—an increase from April’s proposed 20%, if no improved trade terms are reached before the 1 August deadline.

This move follows a series of aggressive tariff demand letters sent to US trading partners over the past week. Hopes for a preliminary US-EU trade deal were dashed after recent media reports hinted at progress, only for negotiations to hit fresh roadblocks. Germany’s DAX reflected this disappointment with a second straight loss of 0.8% last Friday.

Asia stocks resilient on strong China, Singapore data

Despite Trump’s latest tariff salvo, Asia Pacific stock markets remained broadly resilient, supported by upbeat economic data from China and Singapore.

Hong Kong’s Hang Seng Index posted a third consecutive gain, rising 0.4% intraday as it rebounded from its 20-day moving average, now acting as support near 24,050. Singapore’s Straits Times Index (STI), known for its defensive and dividend-yielding components, rallied 0.4%, approaching the psychological 4,100 level. It’s on track for a sixth consecutive record close. In contrast, Japan’s Nikkei 225 slipped 0.2%, while Australia’s ASX 200 remained flat.

China and Singapore surprise to the upside in key data

China’s June exports rose 5.8% year-on-year to US$325 billion, beating expectations (consensus: 5%). The growth was driven by manufacturers shifting focus to alternative markets amid the ongoing trade friction with the US. Notably, exports to 10 South Asian countries surged by 17% year-on-year.

Singapore also exceeded expectations. Its Q2 GDP grew by 1.4% quarter-on-quarter (seasonally adjusted), beating forecasts of 0.7%, and reversing Q1’s revised 0.5% contraction—helping the city-state avoid a technical recession.

Gold rebounds on safe-haven demand amid tariff tensions

Gold (XAU/USD) regained momentum last Friday, rallying 0.9% to a three-week high and moving back above its 20-day and 50-day moving averages. Safe-haven demand has resurfaced, particularly after gold’s recent underperformance relative to silver.

In today’s Asia session, the precious metal edged up another 0.1%, testing the key intermediate resistance at US$3,360. It briefly hit an intraday high of US$3,374. Technical signals remain constructive, and a daily close above US$3,360 could confirm a new bullish phase over the next several sessions.

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Gold (XAU/USD) looks set for a potential minor bullish breakout

Fig 2: Gold (XAU/USD) minor trend as of 14 July 2025 (Source: TradingView)

Recent price actions of Gold (XAU/USD) have managed to retest and stage a rebound from its medium-term ascending trendline in place since the 31 December 2024 low.

It has formed a minor “Double Bottom” bullish reversal configuration, taking into account the two swing lows of 30 June and 9 July. Right now, Gold (XAU/USD) is breaking above the US$3,360 intermediate neckline resistance of the minor “Double Bottom” configuration (see Fig 2)

In addition, the hourly RSI momentum indicator has continued to flash a bullish momentum condition. Watch the US$3,328 key short-term pivotal support (also the 50-day moving average) for the next intermediate resistances to come in at US$3,400 and US$3,450 in the first step.

On the other hand, a break below US$3,328 negates the bullish tone for another choppy minor corrective decline sequence to expose the next intermediate support at US$3,293/3,282.

Bitcoin Price Surpasses $120K for the First Time: What’s Next?

Last week, while analysing the potential for a new all-time high in Bitcoin’s price, we highlighted that the amount of BTC held on cryptocurrency exchanges had dropped to its lowest level in months. This dynamic creates the potential for accelerated price growth should a wave of buyers – including institutional participants – enter the market.

It appears this may help explain the sharp rally in BTC/USD, which surged by over 12% in the past seven days, breaking through the key psychological resistance level of $120K for the first time in history.

Market sentiment is being further bolstered by US Crypto Week, which kicks off today. How might the situation develop from here?

BTC/USD Technical Analysis

Over the past three months, Bitcoin’s price action has been forming an ascending channel (highlighted in blue), with the current BTC/USD rate sitting near its upper boundary. Most, if not all, oscillators added to the chart would now indicate strong overbought conditions.

Given this setup, it is reasonable to assume that the market is vulnerable to a potential pullback. However, such a correction is unlikely to lead to a fundamental shift in sentiment.

We may see a repeat of the price pattern observed in May–June:

- Price consolidates near the midline of the channel;

- Bulls break out, pushing the price toward the upper boundary and creating a zone of imbalance (Fair Value Gap in the Smart Money Concept) – highlighted with a purple rectangle;

- Price retests the imbalance zone following a rejection from the upper channel boundary.

It is worth noting that the current zone is further supported from below by the $111.5K level, which previously acted as a significant resistance. As long as Bitcoin’s price remains above this threshold, any short-selling strategies may carry elevated risk.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.