Sample Category Title

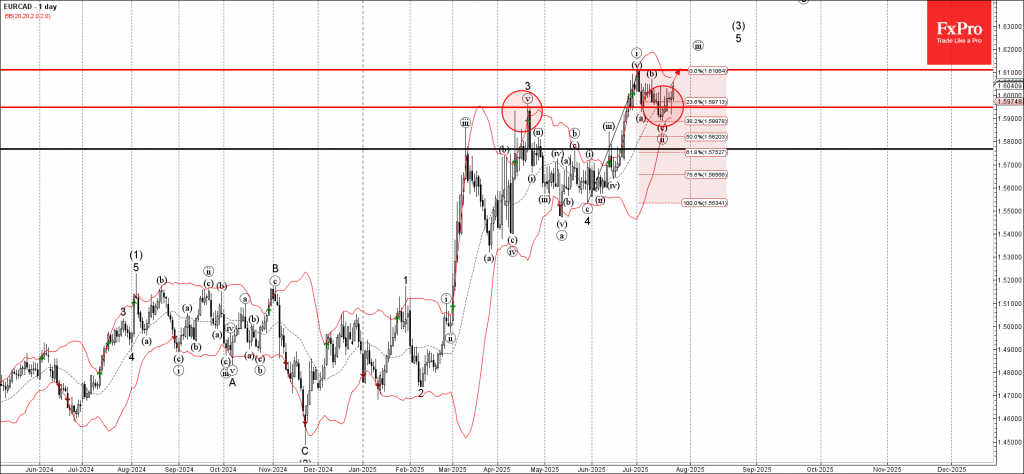

EURCAD Wave Analysis

EURCAD: ⬆️ Buy

- EURCAD reversed from support zone

- Likely to rise to resistance level 1.6100

EURCAD currency pair earlier reversed up from the support zone between the key support level 1.5950 (former monthly high from April), 20-day moving average and the 38.2% Fibonacci correction of the upward impulse from May.

The upward reversal from this support zone started the active minor impulse wave iii – which belongs to the intermediate impulse wave (3) from the end of 2024.

Given the overriding daily uptrend, EURCAD currency pair can be expected to rise to the next resistance level 1.6100 (which stopped the previous impulse wave i in June).

ECB Review – Exceptional Uncertainty, But Still in a Good Place

- ECB decided to leave policy rates unchanged at today's meeting as expected.

- Lagarde struck a positive tone in her economic assessment, although ECB still assess the balance of risk to growth as being tilted to the downside. Trade negotiations and data will likely determine whether to end the cutting cycle or not.

- We still pencil in a final 25bp cut at the September meeting, although risks are tilted towards a hold due to recent data improvement and positive trade news.

ECB decided as widely expected to leave policy rates unchanged at today's meeting, and did not provide any significant news compared to the June meeting. Economic data has overall been aligned with expectations, while underlying inflation continues to soften with wage growth coming lower. Today's statement noted that uncertainty remains 'exceptionally' high due to the US-EU trade dispute, making it unnecessary for the central bank to provide any new signals at this point. ECB still consider the risk for growth as tilted to the downside, but Lagarde repeated that monetary policy remains 'in a good place'. Today's decision to hold rates was unanimous according to President Lagarde.

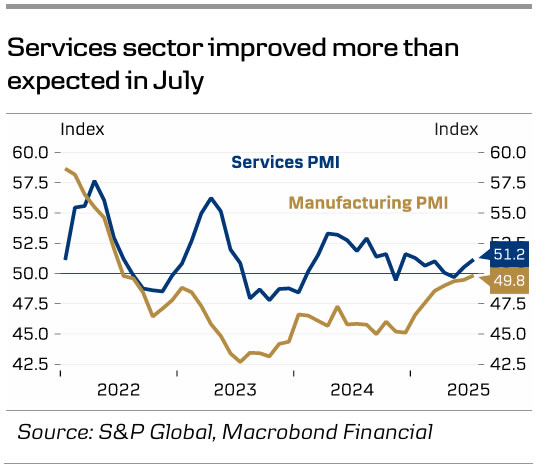

Lagarde struck an optimistic tone in her economic assessment. Particularly, she highlighted that the growth surprise in the first quarter of the year was not only due to Irish front-loading of exports to the US but also domestic demand (consumption and investments) being higher than expected. Hence, growth has been developing a little better than expected. She said that the June baseline projections still hold, when asked about the trade rumors of a 15% tariff rate on the EU. We also highlight that today's services PMI, which rose more than expected to 51.2, is another positive surprise. The weakening of the services sector seen in the past months has been a key argument for a cut in September by the ECB, but this improvement weakens that argument.

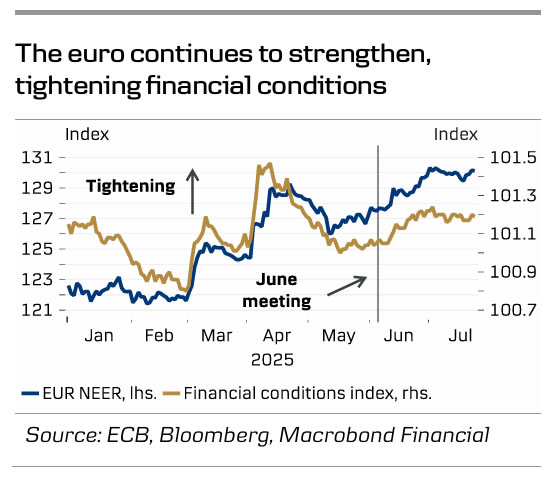

As expected, Lagarde abstained from providing any policy signals in terms of the recent strengthening of the euro. ECB is not targeting the exchange rate, but obviously it matters for the inflationary and economic outlook. But unlike previous comments from GC member De Guindos, Lagarde did not provide any clarity on when the euro appreciation will start complicating the current baseline forecast for inflation. Asked about the risk of inflation undershooting, Lagarde referred to 'three or four' governors who have expressed such concerns. However, the majority of the GC is not worried of the undershooting projection of inflation averaging 1.6% in 2026.

We continue to project a final cut in September, although we admit that both today's strengthening of the euro area services PMIs and the progression in US-EU trade talks have increased the likelihood of another hold. However, a lot can happen in the data coming in between now and the September meeting. We think that the combination of softening wage growth and underlying inflation is still likely to trigger a final 'insurance cut' - especially if trade uncertainty was to persist beyond August 1, which cannot be ruled out.

The slightly hawkish economic assessment from Lagarde at today's meeting triggered renewed upward pressure on EUR rates with the front rising 5bp the remarks. Markets are now only discounting rate cuts worth 7bp for September and 19bp by year-end. EUR/USD also rose 0.5% to 1.178 during the press conference.

USDJPY Re-enters Its Range After US-Japan Trade Deal—Will It Hold?

USDJPY hasn’t failed to generate some volatility in the past few weeks.

The pair, which had seen some steep up moves since the beginning of July, has been met by some sharp realities for its bulls.

Such Daily ranges are strong, and without weekly closes or a substantial fundamental change, Technicals indicate that they are expected to hold.

In today’s analysis, however, we will try to spot if anything from the new situation emerging in Japan has the potential to create a real upside breakout or if the range is deemed to continue.

Also we'll be monitoring the effect of the ISM PMI results on the pair – Services PMI Came in with a beat (55.2 vs 53.0 exp) and Manufacturing PMI missed (49.5 vs 52.5)

The immediate reaction is one of an USD selloff but this is subject to change

For a quick reminder, Japanese elections happened and the Ruling coalition (LDP + Komeito) lost its majority in the Upper House for the first time in a while.

The present government had a lot of influence on the dovish policies from the Bank of Japan, and with the ongoing situation, Japan's PM Ishiba might have to depart from his functions (he indicated he should stay to treat with the US Deals)

As a matter of fact, the Deal got reached yesterday, further confirming the newfound boost in the Yen that had already started to happen around the elections – There has been talks about the Deal not being implemented if "Trump is not happy" Scott Bessent said, but that would be a political mistake.

PM Ishiba pledged to make sure that the deal concludes.

Let's now take a look at the technicals to see if they indicate anything new to tilt the scales further.

Can we learn anything new from Client Positioning?

Trader Sentiment for USDJPY – July 24, OANDA Labs

Positioning isn't giving us much – normally providing us with a decent contrarian indicator and with a small tilt long, the assumption would be for some small downside correction, however the difference in positioning is not so big.

USDJPY Technical Analysis

Daily Chart

USDJPY Daily Chart, July 24 2025 – Source: TradingView

Momentum shut back to neutral after the past 3 sessions of US Dollar selloffs after rejecting the 200-Day Moving Average and participants will now be testing the Immediate 146.00 Pivot region.

Any downside breach would see the 50-Day MA as support (currently at 145.20), with no other key zone for buyers to step in before the 142.00 Main Daily support.

4H Chart

USDJPY 4H Chart, July 24 2025 – Source: TradingView

Sellers regained some strength in the past few sessions and will have to push below the Pivot zone mentioned just before to further maintain the range.

Some mean-reversion happened at the 4H-200 MA at 145.72 which will be a key barometer for immediate momentum (breach below, bearish – Holding above, bullish)

There is some ongoing selling after the PMI data but some decent volumes would be required to retest the overnight levels.

30m Chart

USDJPY 30M Chart, July 24 2025 – Source: TradingView

Looking closer to the 30m intraday timeframe, the rejection at the immediate downwards trendline after testing 146.87 highs in the morning session does shows slightly bearish momentum.

Update: The ongoing selling actually has been met by some buying momentum after a bounce on the 30M MA 50 – buyers will now look to test the highs of the day, monitor any breakout from the immediate trendline.

Monitor reactions at the 146.00 level – some key intraday levels to place on your charts:

Support Levels:

- Immediate intraday support 146.37 and 30m MA 50

- 146.00 Pivot Zone (+/- 100 pips)

- Overnight lows 145.85

- Main Daily Support 142.00 region

Resistance Levels:

- Morning swing high 146.87

- 30m MA 200 147.20

- May Range extremes 147.50 to 148.00

Safe Trades!

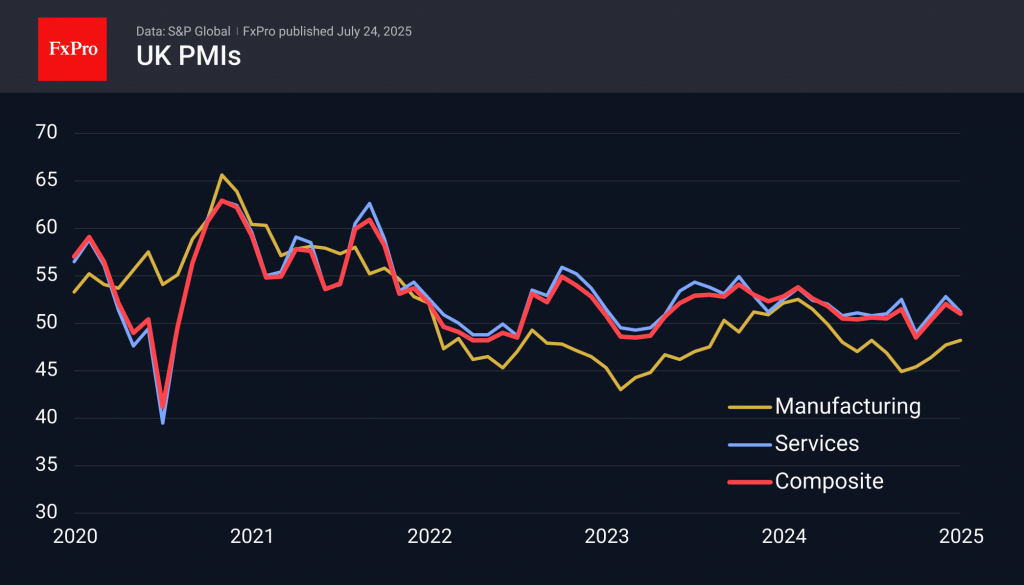

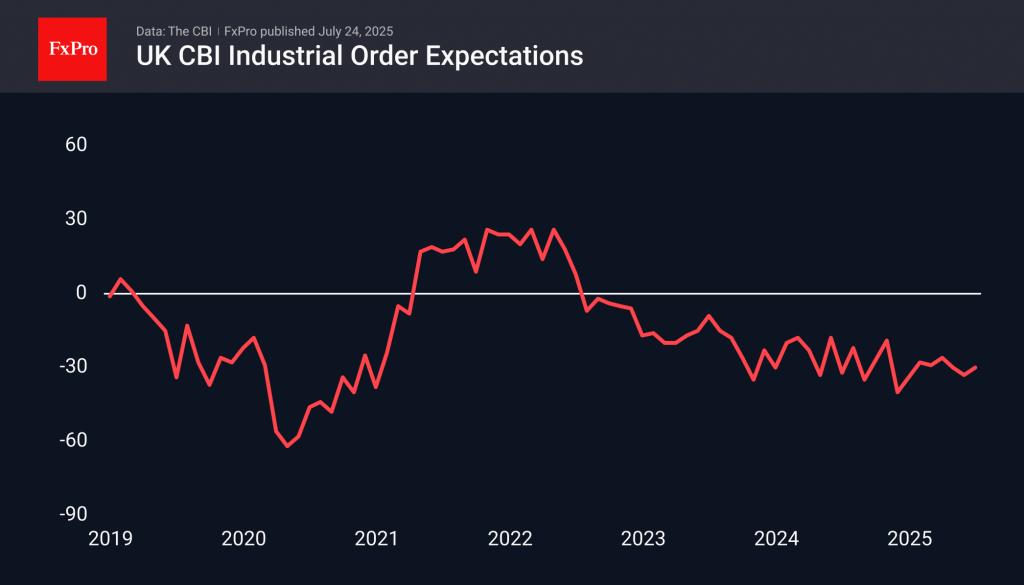

Business Activity in the UK is Under Pressure, as is Pound

Preliminary estimates of PMI business activity indices showed a slowdown in the growth rate of the services sector, while manufacturing activity slowed slightly.

The manufacturing PMI for July, at 48.2, was better than the average forecast of 47.9 and the previous value of 47.7. However, the indicator has remained in decline (<50) for the last 10 months.

The services PMI fell to 51.2, showing a slowdown after June’s reading of 52.8.

Another report, from the CBI, showed continued pessimism regarding industrial orders. The corresponding index stood at -30, remaining in contraction territory for the last three years.

All this indicates subdued economic activity in the UK. Although the Central Bank has been easing policy for a year now, this could potentially pave the way for further cuts in the key rate.

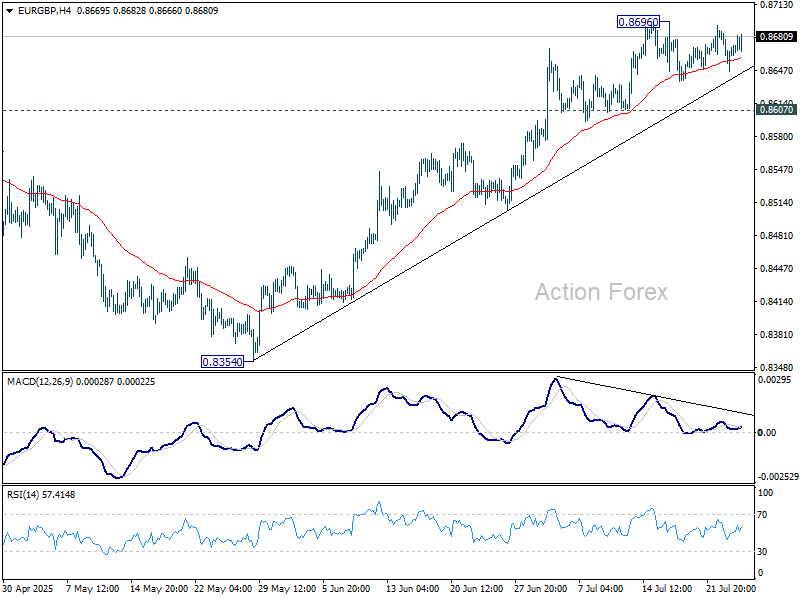

GBPUSD continued to decline against the background of this news, retesting the 50-day moving average. EURGBP has been trading near 0.8670, at the upper end of the range, since the end of 2023, and it looks like part of an upward drift within the 9-year range of 0.82-0.92.

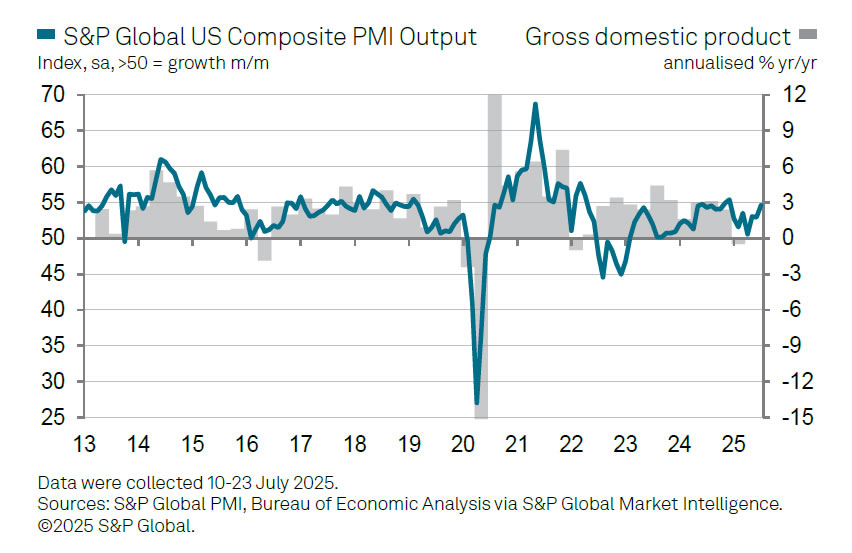

US PMI composite rises to 54.6, but growth uneven, inflation risks rise

US business activity surged in July, with Composite PMI jumping from 52.9 to 54.6, a 7-month high, driven by strength in services. PMI Services rose from 52.9 to 55.2, also a 7-month high. However, the manufacturing index dropped sharply from 52.9 to 49.5, slipping back into contraction for the first time this year.

S&P Global’s Chris Williamson noted the data signaled a sharp pickup in economic growth, with the survey pointing to a 2.3% annualized expansion in Q3, compared to 1.3% in Q2. But the rebound is uneven. Manufacturing is now dragging again, with the prior boost from tariff-related front-loading fading.

Business confidence weakened across both sectors, falling to one of the lowest levels in over two years. Tariff uncertainty and soft demand appear to be weighing heavily on forward-looking sentiment. Even in services, the outlook has dimmed despite the current strength in output.

Price pressures are also building. The survey highlighted one of the largest increases in selling prices in three years, with firms citing tariffs and rising labor costs as key drivers. This suggests upward pressure on consumer inflation will persist into the months ahead, keeping the Fed on edge despite soft spots in manufacturing.

Canada: Retail Sales Plunge as Auto Sales Pull-Back in May

Retail sales contracted by 1.1% month-on-month (m/m) in May, matching Statistics Canada's advanced estimate.

After adjusting for inflation, the volume of retail sales declined 1.4% m/m.

The sharp pull-back was led by auto sales, which fell by 3.6% m/m as the tariff-driven front-loading seen in the prior two months reversed course. Ex-autos, sales were down 0.2%.

Receipts at gas stations and fuel vendors plunged by -2.7%, reflecting the second consecutive monthly decline in fuel prices due to the removal of the consumer carbon tax.

Excluding auto sales and receipts at gas stations, core retail sales were flat in May. Sales at food and beverage stores – the biggest contributor to core sales – declined by 1.2% m/m in May. Most other categories rose, with building material and garden equipment and supplies dealers leading with 1.9% gain.

E-commerce sales declined by 1.7% m/m in May.

Statistics Canada's advanced estimate suggests a rebound in June, with a gain of 1.6%.

Key Implications

The two-month surge in auto sales came to an abrupt halt in May. While we expect some rebound in June, the reversal will likely be limited. Core sales activity remains soft. On a real per capita basis – a metric that gained attention last year as a recession signal when adjusted for rapid population growth – sales are now in contraction for the second straight month.

Consumer caution remains the dominant theme. Despite some recovery in traditional confidence measures, Canadians appear to be treading carefully as they assess the impact of tariffs. The Bank of Canada’s new sentiment index declined in Q2, weighed down by soft consumer spending data. Similarly, our internal Spend data suggests only a weak recovery in June, with quarterly momentum still muted. This persistent weakness in household demand will weigh on growth in the second quarter.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3535; (P) 1.3560; (R1) 1.3604; More...

Intraday bias in GBP/USD is turned neutral first with current retreat. Some consolidations could be seen but risk will stay on the upside as long as 1.3363 support holds. On the upside, above 1.3587 will target a retest on 1.3787 high first. Firm break there will resume whole rally from 1.2099 to 1.4004 fibonacci level.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.

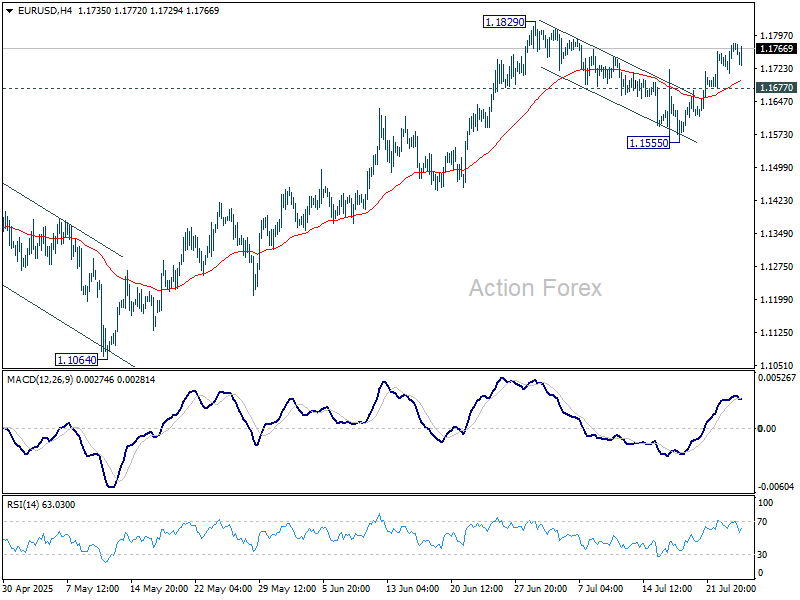

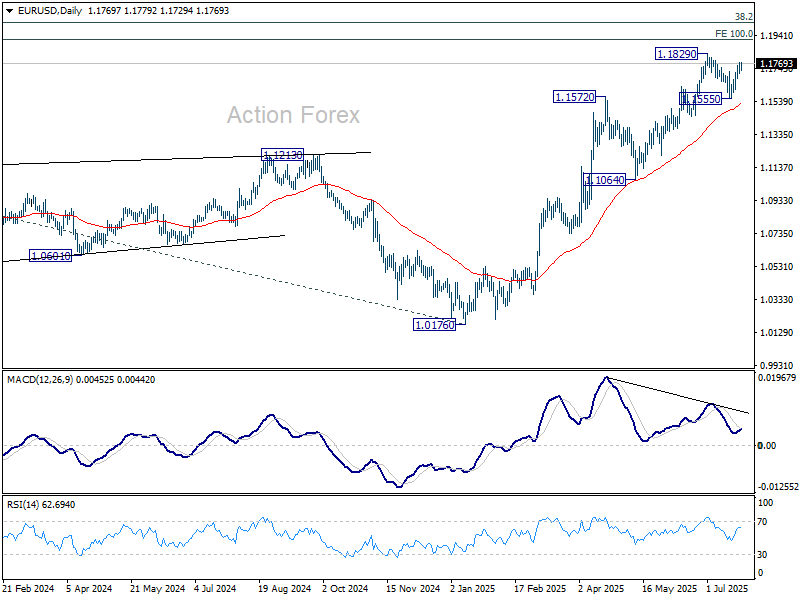

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1730; (P) 1.1753; (R1) 1.1794; More...

Intraday bias in EUR/USD remains on the upside at this point. Rise from 1.1555 is in progress for retesting 1.1829 high. Firm break there will resume whole rally from 1.0176, and target 1.1916 projection level. However, break of 1.1677 will delay the bullish case, and turn intraday bias neutral, with more consolidations below 1.1829 first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Euro Steady as ECB Holds, Lagarde Signals Comfort with Current Stance

ECB held its deposit rate at 2.00% as widely expected, with President Christine Lagarde delivering a message of cautious optimism. Euro was little changed following the decision, as Lagarde emphasized in the press conference that inflation is at 2% and the economy is evolving in a “relatively favorable” manner.

Lagarde acknowledged progress on wages, which are now “slowing as expected,” and said inflation expectations remain “firmly anchored” in both the short and longer term. Although some ECB members remain concerned about the risk of undershooting the inflation target, Lagarde made clear that the central bank sees no immediate pressure to act.

She also reiterated that the ECB will continue to rely on a broad set of economic data in shaping its policy, not individual datapoints. That suggests a steady hand into the September meeting, when updated economic projections could guide the next move. Market speculation of a final rate cut persists, but the ECB appears to be in no rush.

Currency markets remained broadly aligned with the recent risk-on sentiment. Aussie continues to outperform for the week so far. Yen and kiwi also post broadly gains. Dollar remains the weakest performer, followed by Loonie and Swiss Franc. Euro and sterling are holding in the mid-pack.

Technically, EUR/GBP's consolidations from 0.8696 continue today but based on the structure, it should be completing soon. Firm break of 0.8696 will resume the rally from 0.8354 to retest 0.8737 resistance.

In Europe, at the time of writing, FTSE is up 0.90%. DAX is up 0.31%. CAC is down -0.36%. UK 10-year yield is up 0.027 at 4.675. Germany 10-year yield is up 0.069 at 2.709. Earlier in Asia, Nikkei rose 1.59%. Hong Kong HSI rose 0.51%. China Shanghai SSE rose 0.65%. Singapore Strait Times rose 0.99%. Japan 10-year JGB yield rose 0.006 to 1.603.

US initial jobless claims fall to 217k vs exp 230k

US initial jobless claims fell -4k to 217k in the week ending July 19, below expectation of 230k. Four-week moving average of initial claims fell -5k to 224.5k. Continuing claims rose 4k to 1955k in the week ending July 12. Four-week moving average of continuing claims fell -2k to 1954k.

Canadian retail sales fall -1.1% mom in May, but rebound seen ahead

Canadian retail sales fell -1.1% mom to CAD 69.2B in May, with the decline driven largely by -3.6% mom drop at motor vehicle and parts dealers. While the headline figure disappointed, core retail sales—which exclude autos and gasoline—were flat, suggesting underlying consumption was more stable than the headline suggests.

Looking ahead, Statistics Canada’s advance estimate points to a 1.6% mom rebound in June sales, which could help ease fears of weakening domestic demand.

ECB holds at 2.00%, not pre-committing to any rate path

The ECB held its deposit rate steady at 2.00% today, as expected, pausing its easing cycle after a string of cuts since June 2024. In its statement, the central bank reiterated that it will remain "data-dependent" and take a "meeting-by-meeting". It emphasized that approach, the Governing Council is "not pre-committing to a particular rate path".

Policymakers noted that incoming data is "broadly in line" with prior assessments, with domestic price pressures continuing to ease and wage growth slowing. However, the ECB flagged "exceptionally uncertain" global conditions, citing persistent trade disputes as a key risk.

UK PMI composite falls to 51, BoE cut pressure builds

The UK economy showed signs of losing momentum in July, with Composite PMI falling from 52.0 to 51.0. A modest rise in Manufacturing PMI to 48.2 from 47.7 failed to offset a sharp slowdown in services activity, which dropped from 52.8 to 51.2. Overall, the data point to a fragile expansion at the start of Q3.

Chris Williamson at S&P Global Market Intelligence warned that output growth is now consistent with just a 0.1% quarterly GDP gain, and that “risks are tilted to the downside.” Persistent job shedding across sectors underscores the underlying weakness, raising concerns about near-term demand conditions.

With growth stalling and the labor market softening, Williamson said that will add pressure to the BoE to deliver another rate cut in August. While recent inflation data surprised to the upside, the BoE could “look through” those pressures and prioritize support for a struggling economy.

Eurozone PMI composite hit 11-month high, gradually regaining momentum

Eurozone private sector activity accelerated in July, with Composite PMI rising from 50.6 to 51.0—its highest level in 11 months. Manufacturing PMI improved slightly from 49.5 to 49.8, a 36-month high, edging closer to the 50-mark that separates expansion from contraction. Services PMI climbed to a six-month high of 51.2, from 50.5, pointing to broad-based improvement across sectors.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said the data suggests the Eurozone economy is "gradually regaining momentum." The manufacturing recession is "coming to an end," while services growth has picked up. Their GDP Nowcast model indicates the region is on track for “robust economic growth” in Q3, with Germany likely to show slight expansion while France may post a mild contraction, partly due to its domestic political uncertainty.

For the ECB, the data offers some relief. Services inflation—a key focus for policymakers—continued to ease in July. While goods prices stabilized, a stronger Euro and ongoing US tariffs are expected to put downward pressure on price levels in the months ahead.

German GfK consumer sentiment dips to -21.5 as saving preference rises

German consumer confidence took another step back heading into August, with GfK Consumer Climate index falling to -21.5, down from -20.3 and missing expectations of -19.

The decline highlights persistent caution among households, delaying any meaningful rebound in consumer spending. According to Rolf Bürkl at NIM, the rise in saving appetite reflects a broader reluctance to commit to major purchases amid lingering uncertainty and elevated prices.

A durable improvement in sentiment, he emphasized, will require clearer signs of stability to reduce uncertainty and unlock household demand.

Japan's PMI composite unchanged at 51.5, inflation to ease over the summer

Japan’s Composite PMI was unchanged at 51.5 in July. Services drove growth, rising from 51.7 to 53.5, while Manufacturing slipped into contraction at 48.8, down from 50.1.

S&P Global noted that manufacturers saw weaker output and new orders, weighed down by tariff uncertainty and cautious customer behavior. Confidence weakened across the board, with optimism falling to the second-lowest level since August 2020. Firms responded by slowing hiring to the weakest pace in 18 months.

On the positive side, cost pressures eased, with input inflation at a four-year low—suggesting headline "inflation may ease further over the summer".

RBA's Bullock flags slower disinflation, sticks with gradual easing bias

RBA Governor Michele Bullock signaled in a speech caution over the inflation outlook, warning that the fall in trimmed mean inflation in Q2 "may not be quite as much as we forecast". While headline CPI is expected to dip into the lower half of the 2–3% target range, Bullock stressed that temporary cost-of-living relief is playing a role, and underlying pressures may prove more persistent. The RBA still anticipates inflation drifting toward 2.5%, but Bullock emphasized "we are looking for data to support this expectation".

On the labor market, Bullock dismissed surprise around the recent rise in unemployment to 4.3%, saying the outcome was in line with RBA’s May forecasts. Although the June monthly figure saw a noticeable uptick, vacancy rates remain stable and leading indicators "are not pointing to further significant increases in the unemployment rate in the near term."

Overall, she reaffirmed that a “measured and gradual” policy approach remains appropriate, especially with global risks—such as the trade war—showing signs of easing. Her remarks suggest the RBA remains on track for further easing, but will move cautiously, with the pace largely dictated by data flow—particularly the upcoming Q2 CPI print.

Australia PMI composite surges to 53.6, but inflation concerns linger

Australia’s private sector expanded more strongly in July, with the S&P Global Composite PMI rising from 51.6 to 53.6. Services led the way with a sharp rise from 51.8 to 53.8. Manufacturing returned to firmer growth at 51.6, up from 50.6.

S&P Global noted that business activity growth "hastened" at the start of Q3, supported by one of the fastest paces of new manufacturing orders in over two-and-a-half years.

However, the upbeat data came with warning signs. Business confidence slipped to an eight-month low, while manufacturers cut back on purchasing and slowed hiring. More critically, price pressures "intensified" during the month, pointing to renewed upside risks for inflation and "adding to the uncertainty for the interest rate outlook."

RBNZ’s Conway: Tariff fallout to cool NZ inflation

Speaking today, RBNZ Chief Economist Paul Conway said rising global tariffs and economic uncertainty are likely to "reduce medium-term inflation pressures" in New Zealand, and drag on the country’s economic rebound through mid-2026. While the US faces rising costs from tariff-induced supply chain disruptions, Conway said New Zealand is more likely to experience disinflation due to lower global growth and falling import prices.

He highlighted that strong export prices—particularly for dairy and beef—alongside lower domestic interest rates are supporting the economy for now. But widespread uncertainty is causing both consumers and firms to take a wait-and-see approach, which is curbing spending and delaying investment decisions.

Given this backdrop, Conway confirmed that the RBNZ retains a dovish tilt. If inflation continues to ease as expected, there is "scope to lower the OCR further".

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1730; (P) 1.1753; (R1) 1.1794; More...

Intraday bias in EUR/USD remains on the upside at this point. Rise from 1.1555 is in progress for retesting 1.1829 high. Firm break there will resume whole rally from 1.0176, and target 1.1916 projection level. However, break of 1.1677 will delay the bullish case, and turn intraday bias neutral, with more consolidations below 1.1829 first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.