Sample Category Title

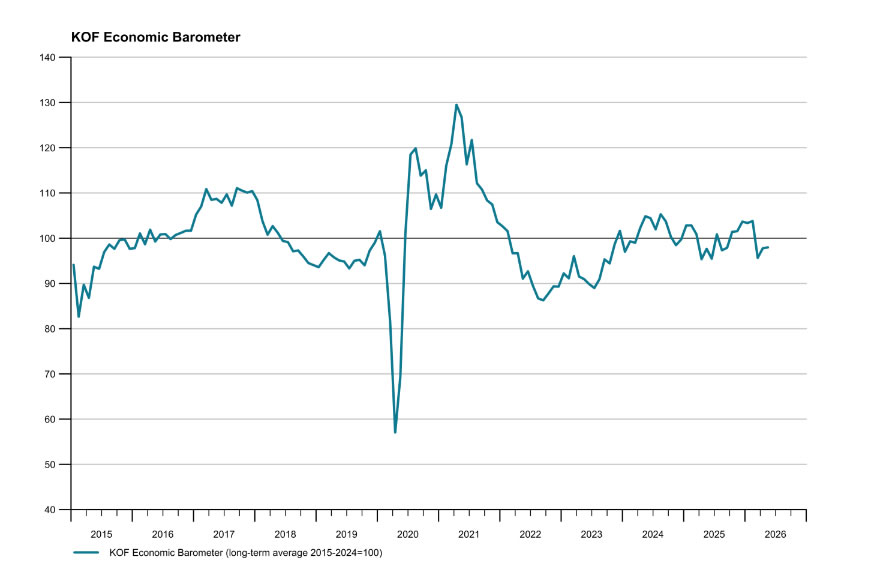

Swiss KOF Barometer Edges Higher to 98.0, But Outlook Remains Subdued

Switzerland's KOF Economic Barometer rose marginally from 97.8 to 98.0 in May, extending the modest improvement seen in the previous month. However, the leading indicator remains below its medium-term average, suggesting that the outlook for the Swiss economy continues to be subdued despite signs of stabilization. The latest reading points to an economy that is expanding only modestly as businesses continue to navigate a challenging external environment.

According to the KOF, underlying developments across sectors were mixed. Manufacturing indicators continued to face pressure, highlighting ongoing weakness in industrial activity. That softness was partly offset by more favorable conditions in financial and insurance services, which helped cushion the broader economy.

On the demand side, foreign demand indicators showed some improvement, offering a potential source of support for exporters in the months ahead. Domestic demand, however, remains less encouraging. KOF noted that indicators for private consumption deteriorated, suggesting households remain cautious despite relatively stable economic conditions.

| Indicator | Previous | Actual |

|---|---|---|

| KOF Economic Barometer | 97.8 | 98.0 |

Sunrise Market Commentary

Markets

News agency Axios has played a prominent part over the past months in reporting on the situation between the US and Iran. Information hasn’t been always that accurate, but financial markets at least treated it as some kind of short term compass. Yesterday, Axios cited two US officials on an agreement on a 60-day MoU to extend the ceasefire and launch negotiations on Iran’s nuclear program. They added that US President Trump still had to give his final approval to the diplomatic breakthrough. The interim deal would contain “unrestricted” shipping through Hormuz (no Iranian toll system) with Iran vowing to remove all mines within 30 days. The US would lift its naval blockade in proportion to the restoration of commercial shipping. The MoU would include an Iranian pledge not to pursue a nuclear weapon, but what to do with the pile of highly enriched uranium remains unsolved. The same goes for the release of frozen Iranian funds. Markets started regaining hope on a way out of the stalemate since the previous weekend. Brent crude currently trades around $92.5/b compared with last week’s close around $104.5/b. Yesterday’s $4/b intraday-drop offered support for both bonds and risk assets. The US yield curve bull flattened with yields ending 1.1 bp (2-yr) to 3.8 bps (30-yr) lower. German yields shed 2 to 3 bps across the curve. Intraday swings were larger though as core bonds had been suffering early on the session. Main US equity benchmarks closed up to 0.9% (Nasdaq) higher following an hesitant start. EUR/USD at first attempted to settle below 1.16 yesterday, before returning to the 1.1650 comfort zone. We continue treating these developments cautiously as on the face of it, the interim deal has more of buying time rather than effectively moving towards a workable solution.

There were plenty of eco data yesterday. US April PCE deflators were a tad softer-than-expected on a monthly basis with headline growing by 0.4% and core by 0.2%. Annual figures nevertheless matched consensus with rises from 3.5% Y/Y to 3.8% Y/Y for the top number and from 3.2% to 3.3% for the underlying series. Next month, our KBC Nowcast suggests a first 4%-reading since May 2023. Based on the unconditional forecast, that could remain the case for several months. Minutes of the April ECB meeting suggested that a June rate hike is in the making: “It had become increasingly likely that adopting a ‘looking through’ approach was not appropriate. It was argued that this situation shifted the primary focus to determining the most appropriate timing for a rate increase.” A number of officials wouldn’t have opposed moving already in April. Today’s eco calendar has some national European inflation numbers in store which could further cement the case. France, Spain, Italy and Germany all report today.

News & Views

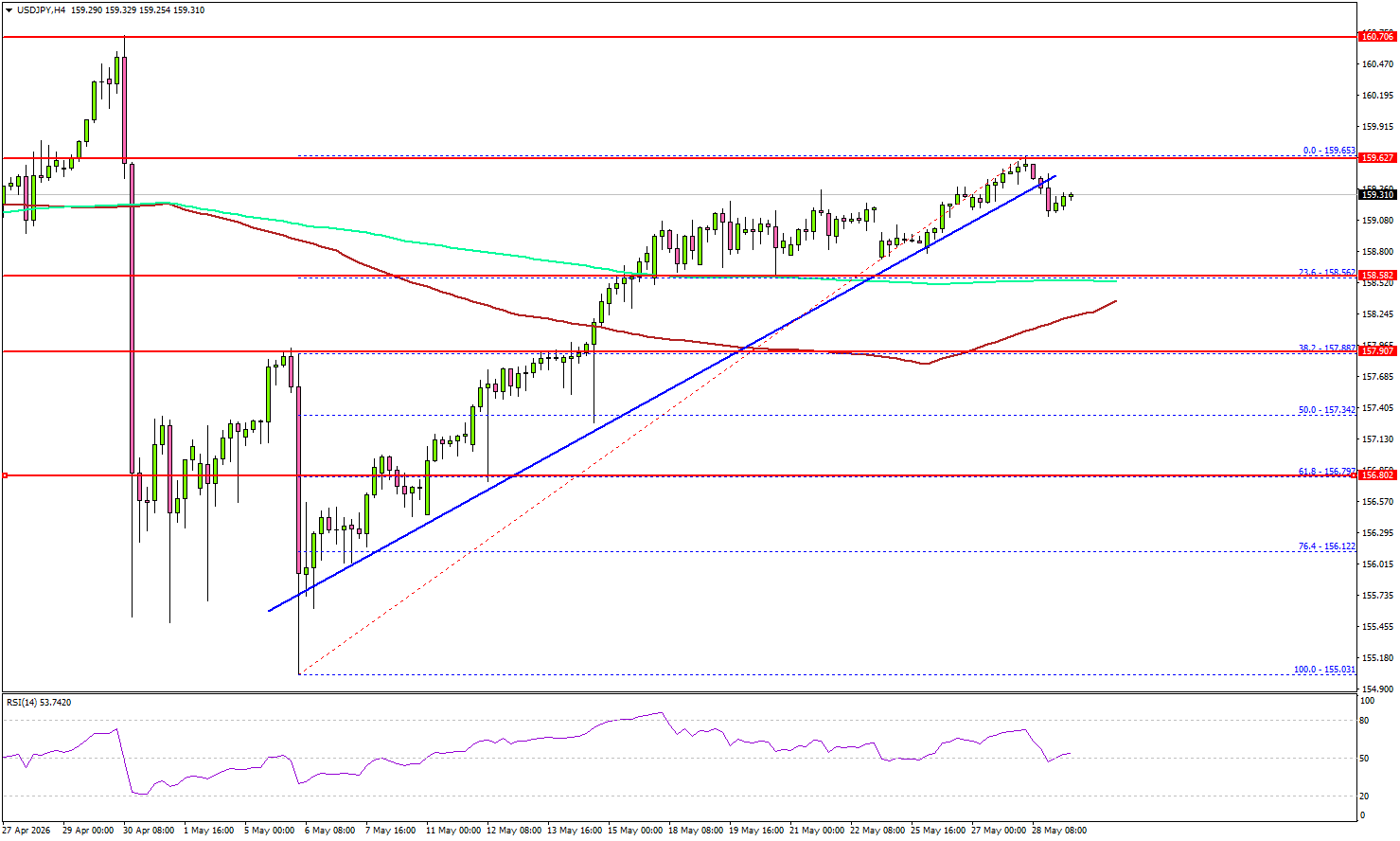

CPI inflation in the Tokyo area, which is seen as a precursor for national Japanese trends, eased further this month. CPI ex fresh food rose 0.3% M/M and 1.3% Y/Y (from 1.5%). The core measure excluding fresh food and energy also eased to 0.1% M/M and 1.6% (from 1.9%). However, government measures to trim the cost of utility prices and tuition fees were for a large part responsible for the softer set of inflation data The easing in inflation comes as the BOJ assesses the timing of a next rate hike, probably already at the June16 policy meeting. Aside from mild Tokyo CPI data, a series of national data including April industrial production (+ 0.8% M/M), retail sales (1.3% M/M and 2.1% Y/Y) and labour market data (jobless rate from 2.7% to 2.5%) all come in on the better side of expectations. Today’s data releases don’t change money market expectations for the June policy meeting. Markes still discount a 75-80% probability for a rate hike from 0.75% to 1%. The yen trades little changed (USD/JPY 159.3).

The South African Reserve Bank (SARB) yesterday raised its policy rate by 25 bps to 7%. It was a spilt decision. The move was supported by 4 MPC members. Two policymakers preferred to keep the policy rate on hold. Governor Kganyago indicated that also a 50 bps step was discussed, but that the SARB preferred a more cautious approach as it awaits more data. The hike comes as inflation rose to 4% from 3.1% in April. This was mostly due to higher energy costs, but services inflation also accelerated to 4.6%. The SARB has a 3% inflation target (+/- 1% tolerance band). The SARB also raised inflation forecasts for this year and next year to 4.4% and 3.7% respectively and indicated that these forecasts entail some second round effects. The SARB explored three scenario (also taking into account the potential effects of El Nino), but all these scenario’s imply higher inflation and lower growth (expected at 1.2% this year from 1.4%). They also took notice of a stronger ZAR than last year, helping to contain imported inflation. The rand yesterday continued it recent rebound with USD/ZAR trading near 18.9.

With Hawkish ECB Minutes, Focus Turns to Euro Area Inflation Prints

In focus today

In the euro area, we will receive May flash inflation data from Germany, France, Italy and Spain, covering 75% of the aggregate euro area print. The rise in inflation has so far been largely confined to a few energy components, like car fuel, and we expect energy to remain the primary driver pushing euro area HICP inflation up to 3.2% y/y in May (April: 3.1% y/y). Core inflation is also expected to edge up to 2.3% y/y (April: 2.2% y/y), though mainly driven by base effects rather than a pick-up in underlying momentum.

In Sweden, Q1 national accounts are due, where we expect growth of 0.2% q/q and 2.4% y/y, slightly better than the flash GDP estimate. Households showed signs of weakness at the beginning of the year, but recently the picture has improved, as both the monthly consumption indicator and retail sales have picked up.

In Norway, unemployment figures and retail sales data will be released. The labour market remains relatively tight and despite some tentative signs of rising unemployment, we expect the seasonally adjusted unemployment rate to hold steady at 2.1% in May (April: 2.1%). On the consumption side, households are facing stronger headwinds from lower real wage growth, slowing employment growth and higher mortgage rates, all of which will gradually dampen consumption growth. Against this backdrop, we expect retail sales to have been unchanged in April (March: -0.1%).

Economic and market news

What happened overnight

In Japan, May Tokyo core CPI (excluding fresh food and energy), viewed by the Bank of Japan (BoOJ) as a gauge for trend inflation, increased 1.6% y/y (cons: 1.8%, April: 1.9%). Markets expect inflation to re-accelerate as elevated oil prices and a weak yen keep pressure on the BOJ, with markets largely pricing in a 25bps hike to 1.0% at next month's meeting.

What happened yesterday

In the euro area, the minutes came in on the hawkish side, with the ECB framing rate hikes as a question of not if but when. The ECB appears to be gearing up for a potential June hike, repeatedly noting that more information will be available then. Upside risks to inflation and downside risks to growth had both intensified since the March meeting, creating a "complicated policy trade-off", though members were careful to note there was "no evidence yet of strong second-round effects".

Also in the euro area, firms' selling price expectations declined slightly in both industry and services in the European Commission's May business survey, offering the ECB some relief after April's record surge. Selling price expectations for the industry are still very elevated, though below 2022 levels, and we should therefore expect price increases on core goods. However, the decline in services expectations should give the ECB some comfort as the index has risen only marginally following the Iran war. This suggests that the energy shock is not propagating to broader services prices (at least outside of transportation services).

In the US-Iran war, Axios reported that the two sides have reached an agreement for a 60-day ceasefire extension, which would also include reopening the Strait of Hormuz to shipping, though the deal is still pending approval from both Trump and Iranian leadership. If approved, negotiators would use the extended truce to address issues such as Iran's nuclear programme.

In oil market, Brent crude fell to USD 92/bbl after US and Iran seems to be nearing an agreement to extend the truce another 60 days. That is the lowest level since the ceasefire announcement in the start of April. Between these two announcements, Brent crude has traded well above USD 100/bbl on some days, and we see a risk that this could happen again as the situation remains fragile. Meanwhile, the US made another big draw of 9mb on its strategic reserves last week which helps contain the immediate pressure on oil prices.

In Norway, mainland GDP grew 0.2% q/q in Q1. This is marginally weaker than Norges Bank (NB) expected in the Monetary Policy Report in March of 0.4% q/q and will in isolation lower the probability of a rate hike in June. Revisions were negative as well, leaving the mainland GDP level approximately 0.45 percentage points below what NB had anticipated in Q1. We still view the May inflation figures (10 June) and the Regional Survey (11 June) as decisive for the June decision, but the figures clearly suggest that monetary policy was already restrictive ahead of the March hike.

Additionally, the Oil Investment Survey showed positive adjustments for both 2026 and 2027, though the upward revisions were smaller than at the same time last year, pointing to nominal declines of approximately 1% this year and a flat development next year. The release came in on the weak side, though it is unlikely to be a determining factor for NB's short-term rate setting.

In Sweden, the NIER survey edged up to 99.3 in May (April: 99.2), with consumer confidence rising to 92.4 (April: 91.7) and the manufacturing index increasing to 100.5 (April: 100.0). Notably, price plans also increased, consistent with rising input prices in the PMI, supporting our view of higher inflation pressure ahead. Price plans typically lead inflation by around three months and will be closely watched, as considerable uncertainty remains around whether firms have altered their price-setting behaviour.

In the US, April core PCE came in slightly below expectations at +0.2% m/m (cons: +0.3%), causing a modest dovish market reaction with yields down and the USD broadly weaker. Real private consumption continued to grow, with consumers absorbing higher costs by drawing down savings. Notably, goods prices are becoming an increasingly important driver of core inflation. On the growth side, Q1 GDP was revised down to 1.6% q/q AR from the 2.0% flash estimate, though underlying growth remained fairly solid. Consistent with recent remarks, Fed's Williams noted that monetary policy is "well positioned" while flagging that persistently high inflation would warrant higher rates.

Equities: Equities rebounded yesterday, driven by US. S&P 500 up 0.6% ending not far from best levels, while markets in Nordics and Europe remained sluggish. US and Asia continue to outperform, as the momentum trade in semis/memory resumed yesterday. But this was also a session of growth stock preference; companies within medtech, software and materials fared particularly well. Gains in software triggered by strong earnings from Snowflake, beating estimates, raising its outlook and on top of it all, announcing an AI deal with Amazon; thereby disproving the software-scare among investors.

The latest growth and momentum are benefitting the US sector composition more than Europe, alongside a strong macro backdrop. Along the same lines, Asian equities are rallying this morning (Nikkei 225 2.5%, Kospi 3%, Hang Seng 1%). Since the market troughed on 30 March, US equities have returned nearly twice as much as European equities (S&P 500 19% vs Stoxx 600 10%). It is a crazy outperformance, but we think this gap will continue to grow, and Europe outperforming briefly the week when the Strait of Hormuz reopen is a blip on the curve.

FI and FX: The tentative US-Iran deal to extend the ceasefire is taking centre stage this morning. That said, while oil prices have extended the decline back down towards the lower 90s USD/bbl the reaction in rates and FX markets has still been muted with e.g. interday moves in FX majors kept within +/- 1 standard deviations. More importantly, US PCE inflation yesterday contributed to sending yields lower with 30Y US Treasury yields now firmly back below the 5.00% level, the US swaps curve has bull flattened while EUR/USD FX spot is trading around 1.1640. In the Scandies, short-end rates spreads to EUR have widened for NOK but remained stable in SEK. EUR/SEK and EUR/NOK have both been relatively stable with SEK notably outperforming NOK.

S&P 500 Nabs Records on US-Iran Ceasefire Extension Amid Hot PCE Inflation Shock

Key takeaways

- Global equities climbed to fresh record highs after the US and Iran agreed to extend their ceasefire, boosting risk appetite and driving strong gains in technology and AI-related stocks.

- Hotter-than-expected US core PCE inflation at 3.3% y/y reinforced the “higher for longer” interest rate narrative, further reducing expectations for Federal Reserve rate cuts under new Fed Chair Kevin Warsh.

- AI infrastructure and enterprise technology spending remain the dominant market driver, with blockbuster developments from Anthropic, Snowflake, Amazon, and Dell reinforcing the ongoing AI capex supercycle despite growing concerns over potential overcapacity.

- Chart of the day: Nasdaq 100 minor bullish trend intact, en route to another potential fresh all-time high at 30,728/795 with key short-term support at 29,700.

Top macro headlines

- US and Iran agree to extend ceasefire: The S&P 500 and Nasdaq bounced back to hit fresh record highs on Thursday after the United States and Iran officially agreed to extend their ceasefire. US Treasury Secretary Scott Bessent confirmed that a permanent agreement to completely wind down the three-month-old war is within reach, provided Iran satisfies key conditions, including uranium disposal and fully reopening the Strait of Hormuz.

- US core PCE inflation jumps to 3.3% y/y, creating policy “wedge”: The Bureau of Economic Analysis released April's Personal Consumption Expenditures (PCE) report, revealing that headline PCE inflation rose to 3.8% y/y (up from 3.5% in March). More critically, core PCE inflation (excluding food and energy) climbed to 3.3% y/y, creating a rare inflationary "wedge" by running significantly hotter than core CPI (2.8% y/y), further squashing hopes for Federal Reserve interest rate cuts.

- Anthropic secures staggering $965 Billion valuation: Artificial intelligence startup Anthropic closed a massive $65 billion funding round, vaulting its private valuation to $965 billion and rocketing past OpenAI. The firm is tracking to hit a $50 billion annualized revenue run-rate next month after Q1 sales expanded 80-fold.

- Snowflake inks $6B Amazon deal as tech earnings explode: Defying fears that AI automation would kill traditional enterprise software providers, Snowflake surged up to 35% after signing a landmark $6 billion deal with Amazon and upgrading its full-year sales forecast. Concurrently, Dell Technologies skyrocketed 40% in after-hours trading, following blowout quarterly results.

Key macro themes

- The rare PCE-CPI inflation wedge: A significant structural challenge has emerged for newly confirmed Federal Reserve Chair Kevin Warsh. The Fed's preferred price barometer, the core PCE index, has broken higher to 3.3%, creating an unusual divergence from the 2.8% CPI benchmark. Because this underlying inflation spike stems directly from the Strait of Hormuz conflict choking global energy supplies, traditional monetary policy tools are constrained, and higher interest rates cannot lower oil transit costs but run the risk of severely bruising an already slowing economy.

- The K-shaped bifurcation of Wall Street vs. Main Street: The latest macro data dump exposes a profound macroeconomic split. Corporate profit margins remain near record highs as companies exploit structural supply shortages and the ongoing AI capex boom to drive revenues. Conversely, Main Street consumers are under acute duress; the U.S. personal savings rate plummeted to a near-historic low of just 2.6% in April, a level eclipsed in weakness only once in the past 18 years, as soaring gas prices near $5 a gallon erode real wage growth.

- AI Infrastructure overcapacity skepticism: Despite record-breaking stock market indices, a distinct undercurrent of institutional skepticism is building regarding the trillions of dollars pouring into AI capital expenditures. Several portfolio managers are warning of near-term overcapacity as commercial entities experience budget fatigue; for instance, Microsoft has begun cutting internal Claude code licenses due to prohibitive costs, while Uber has already entirely exhausted its 2026 AI coding capital allocation.

Global market impact (last 24 hours)

Equities: Wall Street rallied forcefully, with the S&P 500 gaining 0.6% to close at 7,563, while the tech-heavy Nasdaq 100 outperformed, hitting a fresh all-time high with a gain of 0.8%. Overall, Technology (1.4%) and Healthcare (1.3%) led, while defensive sectors, Consumer Staples (-0.6%) and Utilities (-1%) underperformed. Conversely, European bourses fell, with the FTSE 100 shedding 0.7% and DAX dropping 0.3%.

Fixed Income: Sovereign bond yields edged lower following the extension of the Middle East truce. The benchmark U.S. 10-year Treasury yield fell by roughly 3 basis points to anchor at 4.45% as the sovereign yield curve bull-flattened.

FX: The U.S. Dollar Index weakened by 0.2%, pulling the USD/JPY pair away from the critical 160.00 intervention line. Risk-sensitive currencies, the New Zealand Dollar (NZD) and Australian Dollar (AUD), led the G10 currencies higher with gains of 0.6% and 0.3% against the USD, while the South African Rand (ZAR) outperformed across emerging markets.

Commodities: Crude oil prices extended losses, with Brent and WTI crude hitting close to six-week lows of $92.41/bbl and $88.52. In contrast, precious metals rebounded, supported by a pull-back in longer-term US Treasury yields, with spot gold surging 0.9% to settle at $4,496/oz, still below the 20-day moving average at $4,585/oz.

Asia Pacific impact

- Equity and currency volatility: Before the late-session Wall Street ceasefire bounce, regular-hour Asian equity benchmarks fell by up to 1% as they digested sticky global yields. Currencies stabilized slightly following the 0.2% drop in the greenback, relieving pressure on the Japanese yen near the 160 psychological threshold. Asia Pacific benchmark stock indices recovered sharply in today’s Asia opening session; Nikkei 225 (+1.9% to record high), Hang Seng Index (+0.4%), China A50 (+0.5%), KOSPI (+2.2% to record high), ASX 200 (+1%), and STI (+ 0.7%).

- Corporate labour and tech supply chains: Highlighting an immense structural divergence, Samsung Electronics' advanced chip workers secured a historic 10-year corporate pay package including bonuses of up to $416,000. These massive wins by a regional bellwether are expected to significantly harden the bargaining positions of other domestic unions, introducing structural wage inflation into the region.

- Derivative infrastructure race: Financial localization is accelerating. While U.S. exchanges prepare to launch futures contracts tied to raw computing rental power, China is actively designing a brand-new futures market for AI tokens used to price localized AI services, sparking a structural derivatives race with Washington.

Top 4 events to watch today

- Japan Consumer Confidence (May) - 1:00 pm SGT (consensus:32, Apr:32.2) Impact: USD/JPY, JPY crosses, Nikkei 225

- Germany Harmonised Inflation Rate Prelim (May) - 8:00 pm SGT (consensus: 2.8% y/y, Apr: 2.9%) Impact: EUR/USD, EUR crosses, DAX

- Fed Speak - Bowman (9.10 pm SGT), Paulson (9.15 pm SGT) Impact: Short-end US Treasuries, USD, US stock indices

- US-Iran peace deal news flows Impact: All asset classes

Chart of the Day - Nasdaq 100 Bullish Trend Intact

Fig. 1: US Nasdaq 100 CFD minor trend as of 29 May 2026 (Source: TradingView).

The intraday decline of 2% seen in the US Nasdaq 100 CFD (a proxy of the Nasdaq 100 E-mini futures) measured from Wednesday, 27 May US session high to Thursday, 28 May Asia session low has hit an inflection level at 29,700.

Thereafter, it staged a bullish reversal, which suggests that its minor uptrend phase from the 19 May 2026 low remains intact.

Watch the 29,700 key short-term pivotal support, and a clearance above 30,425 sees the next intermediate resistances coming in at 30,728/795 (upper boundary of the ascending channel & Fibonacci extension cluster) and 31,050 (Fibonacci extension).

On the other hand, a break and an hourly close below 29,700 negates the bullish tone for a minor corrective decline to expose the next intermediate supports at 29,433 and 29,110 (also the 20-day moving average).

RBNZ Hints at Bigger Hikes as Kiwi Surge Accelerates: NZD/JPY and AUD/NZD Analysis

The New Zealand Dollar extended its powerful rally on Friday as investors interpreted the latest comments from Reserve Bank of New Zealand officials as a signal that the tightening cycle could restart sooner — and perhaps more aggressively — than previously expected. Markets had already viewed July as a live meeting after this week's dramatic hawkish hold, but subsequent remarks from policymakers today have raised a more important question: not whether rates will rise, but how large future hikes may ultimately be.

Governor Anna Breman delivered the strongest signal, stating that "on balance, the OCR is likely to increase sooner and by more than previously signaled." Meanwhile, MPC member Hayley Gourley argued that acting earlier offered the best chance to keep inflation expectations anchored and later emphasized that the data received before July would determine "the speed and the magnitude of change." Those remarks have encouraged traders to consider the possibility that the RBNZ may eventually need to move more aggressively if the inflationary effects of the Middle East energy shock become increasingly embedded in the economy. Even policymakers who voted to hold rates this week continue to argue that OCR increases will be needed.

Currency markets have responded quickly to the evolving policy outlook. NZD/JPY has emerged as one of the clearest beneficiaries as investors contrast a hawkish RBNZ with the cautious Bank of Japan. Japan's latest inflation figures showed further moderation in Tokyo CPI, reinforcing expectations that the BoJ is unlikely to rush into additional tightening.

That widening policy gap has pushed NZD/JPY to the verge of a major breakout. Sustained move above 94.96 would mark the highest level since 2024 and confirm continuation of the broader uptrend from last year's low at 79.79. Next target will be 61.8% projection of 85.33 to 94.96 from 90.55 at 96.50. Near term outlook will stay bullish as long as 92.89 support holds, in case of retreat.

The same divergence theme is driving AUD/NZD sharply lower. Earlier this year, the Reserve Bank of Australia was widely seen as the more aggressive central bank after delivering three rate hikes. However, weaker Australian inflation data this week and recent signs of labor-market cooling have reduced expectations for further near-term tightening. With a June hold effectively locked in and August no longer certain, attention has shifted toward the possibility that the RBNZ may now be the central bank playing catch-up.

Technically, 1.2283 is seen as a medium term top in AUD/NZD, on bearish divergence condition in D MACD. Risk will stay on the downside as long as 1.2132 support turned resistance holds. Deeper fall would be seen to 1.1922 (38.2% retracement of 1.1412 to 1.2283 at 1.1950).

Strong rebound from 1.1922 will keep the corrective pattern from 1.2283 a sideway consolidations pattern only. However, firm break of 1.1922 will argue that it's already correcting the whole five wave rally from 1.0649, and set up deeper fall to 38.2% retracement of 1.0649 to 1.2283 at 1.1659 in the medium term.

USD/JPY Upside Exhaustion Signals Raise Pullback Concerns

Key Highlights

- USD/JPY seems to be struggling to clear the 159.65 resistance.

- It traded below a bullish trend line with support at 159.40 on the 4-hour chart.

- EUR/USD is still struggling to clear the 1.1675 resistance zone.

- Gold corrected some losses and tested the $4,525 resistance.

USD/JPY Technical Analysis

The US Dollar climbed above 158.50 and 158.80 against the Japanese Yen. USD/JPY even surpassed 159.20 before the bears appeared.

Looking at the 4-hour chart, the pair settled above the 158.50 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). However, it faced resistance near the 159.65 zone.

A high was formed at 159.65, and the pair is now correcting some gains. There was a move below a bullish trend line with support at 159.40. If the pair extends losses, it could test the 23.6% Fib retracement level of the upward move from the 155.03 swing low to the 159.65 high.

The first major support sits near the 158.50 level and the 100 simple moving average (red, 4-hour). The next support could be 157.85. A close below 157.85 might initiate a drop to the 61.8% Fib retracement level of the upward move from the 155.03 swing low to the 159.65 high at 156.80.

Any more losses might open the doors for a drop toward the 156.00 zone. On the upside, the pair could face resistance at 159.65. The next major resistance could be 160.00. A close above 160.00 could open doors for gains above 160.50. In the stated case, the bulls could aim for a move to 162.00.

Looking at EUR/USD, the pair is attempting to recover some losses, but it faces a major hurdle near the 1.1675 region.

Upcoming Key Economic Events:

- Fed's Bowman speech.

- Fed's Paulson speech.

- Chicago PMI for May 2026 – Forecast 49.7, versus 49.2 previous.

RBNZ Hawks Signal Rate Hikes Are Coming, July Meeting Now Live

Fresh comments from senior Reserve Bank of New Zealand officials today reinforced the hawkish message delivered at this week's policy meeting, strengthening the case that interest rate hikes are approaching and putting the July meeting firmly in play. While the RBNZ left the Official Cash Rate unchanged at 2.25%, the decision was split 3-3, with Governor Anna Breman casting the deciding vote to hold. The subsequent commentary suggests policymakers are no longer debating whether rates need to rise, but rather when the tightening cycle should resume.

Among the most hawkish voices was Monetary Policy Committee member Hayley Gourley, who voted for an immediate rate increase. Gourley told Reuters that the policy path points to change "sooner rather than later" and argued that acting early would provide the best opportunity to keep inflation expectations anchored.

"My view was that by increasing sooner rather than later, we had the best opportunity to keep inflation expectations anchored and therefore minimize the negative impact inflation may have for the economy," Gourley said. She also stressed that incoming data over the next five to six weeks would determine "the speed and the magnitude of change," effectively confirming that July is a live meeting.

Even officials who supported holding rates signaled that higher borrowing costs are likely ahead. Assistant Governor Karen Silk acknowledged that higher oil prices from the Middle East conflict will inevitably flow through to broader inflation pressures. "We can't have the oil price shock that we've had without it having some flow through further down the line," Silk said, adding that "you do need to have an increasing OCR to lean against that." Importantly, she rejected the idea that policymakers should simply wait for more quarterly inflation data before acting, stating that "we have always got to be forward looking."

Governor Anna Breman reinforced the shift in guidance, stating that "the OCR is likely to increase sooner and by more than previously signalled." Taken together, the comments suggest the RBNZ is increasingly concerned that the energy shock could become embedded in inflation expectations even as economic growth slows. While policymakers remain divided on timing, there now appears to be broad agreement that higher rates will be required.

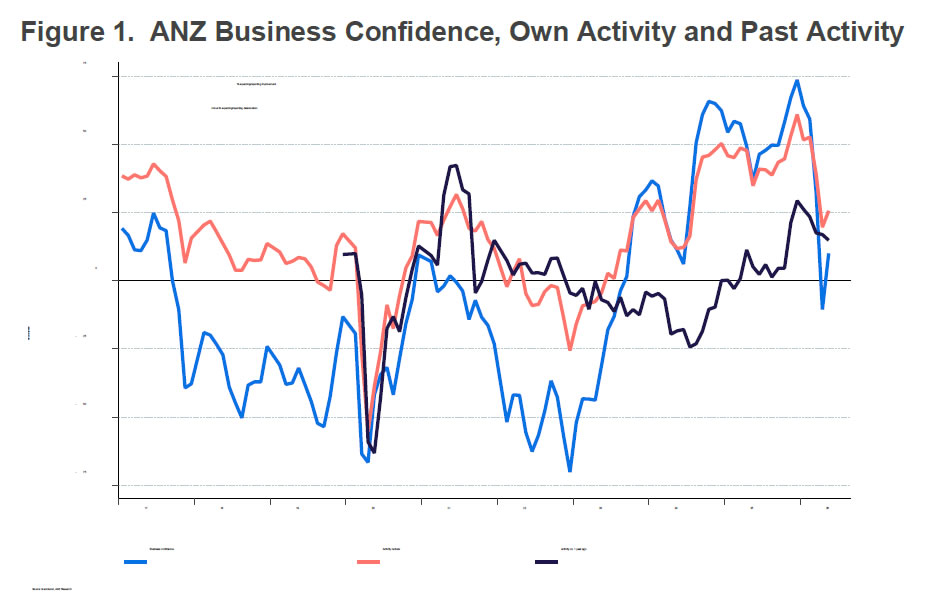

New Zealand ANZ Business Confidence Turns Positive, Inflation Pressures Stay Contained

New Zealand business sentiment improved sharply in May, suggesting firms are gradually adapting to the economic shock created by the Middle East conflict. ANZ Business Confidence jumped from -10.6 to 10.0, returning to positive territory, while firms' Own Activity Outlook rose from 19.6 to 25.6. The rebound indicates that some of the initial pessimism triggered by surging energy prices and global uncertainty has faded, although confidence remains well below levels seen before the conflict began.

Beneath the headline improvement, however, the survey painted a more mixed picture. Inflation expectations one year ahead eased from 3.81% to 3.63%, while wage expectations edged down from 2.53% to 2.48%. Employment intentions also improved notably, rising from -2.7 to 3.4, suggesting firms have become somewhat more optimistic about hiring.

ANZ noted that activity indicators remain considerably weaker than before the conflict, with retail and construction sectors continuing to struggle while agriculture and manufacturing have proven more resilient.

For the Reserve Bank of New Zealand, the survey may offer some reassurance that medium-term inflation pressures remain contained despite elevated headline inflation. ANZ emphasized that wage intentions provide a better guide to underlying inflation than short-term inflation expectations, and both measures remain below pre-conflict levels.

According to the ANZ, firms continue facing rising costs and profitability pressures but have limited ability to pass those costs on to customers in a soft demand environment. That dynamic may help contain broader inflation pressures even as the RBNZ continues preparing markets for likely OCR hikes later this year.

| Indicator | Previous | Actual |

|---|---|---|

| ANZ Business Confidence | -10.6 | 10.0 |

| Own Activity Outlook | 19.6 | 25.6 |

| Inflation Expectations (1-Year) | 3.81% | 3.63% |

| Employment Intentions | -2.7 | 3.4 |

| Wage Expectations (1-Year) | 2.53% | 2.48% |

Tokyo Inflation Cools Further, But Strong Growth Data Keeps BoJ Normalization on Track

Japan's inflation picture softened further in May, but the broader economy continued showing surprising resilience. Tokyo CPI core (excluding fresh food), widely viewed as a leading indicator of nationwide inflation trends, slowed from 1.5% yoy to 1.3% yoy, below expectations and marking the sixth consecutive month of deceleration. Headline inflation eased from 1.5% yoy to 1.4% yoy, while the closely watched core-core measure, excluding both fresh food and energy, slowed from 1.9% yoy to 1.6% yoy.

The decline in inflation was largely driven by government subsidies aimed at reducing utility, water, and tuition costs. However, policymakers are unlikely to take too much comfort from the softer readings. Analysts generally expect inflation to reaccelerate later this year as the impact of surging oil prices and a weak Yen feeds through to import costs. The persistence of Middle East-related energy risks remains particularly important for Japan, which remains heavily dependent on imported energy.

At the same time, activity indicators released for April painted a considerably stronger picture of the economy than expected. Industrial production rose 0.8% mom, sharply outperforming forecasts for a contraction. Manufacturers surveyed by the government expect output to surge another 5.1% in May. Retail sales also surprised to the upside with a 2.1% yoy increase, suggesting consumer demand remains relatively healthy despite higher living costs. The labor market also strengthened, with the unemployment rate falling from 2.7% to 2.5%, its lowest level in several months.

Taken together, the data reinforces that underlying economic conditions remain firm even as inflation temporarily cools. While softer CPI may reduce pressure for immediate tightening, resilient growth, a tight labor market, and expectations of renewed energy-driven inflation should keep policy normalization firmly on the table in coming months.

| Indicator | Previous | Forecast | Actual |

|---|---|---|---|

| Tokyo CPI Core (YoY) | 1.5% | 1.5% | 1.3% |

| Tokyo CPI Core-Core (YoY) | 1.9% | 1.6% | |

| Tokyo CPI Headline (YoY) | 1.5% | 1.4% | |

| Industrial Production (MoM) | -0.4% | 0.8% | |

| Industrial Production Outlook (May) | 5.1% | ||

| Industrial Production Outlook (June) | -0.4% | ||

| Retail Sales (YoY) | 1.4% | 1.3% | 2.1% |

| Unemployment Rate | 2.7% | 2.7% | 2.5% |

Gold (XAUUSD) Price Action Strong Elliott Wave Impulsive Reaction from Key Support Zone

The short‑term Elliott Wave view in Gold (XAUUSD) shows that the yellow metal has completed a three‑swing correction from the April 17, 2026 high. The pullback unfolded as a zigzag, with wave A ending at $4499.92 and wave B at $4773.58. Gold then declined in wave C to $4365.13, completing wave (2) as seen on the one‑hour chart. This level sits inside the key support zone, where wave C equals the 100%–161.8% Fibonacci extension of wave A. The broader support area spans $4137–$4380.

After testing this zone, Gold began a strong impulsive rally. The advance signals renewed momentum, but confirmation requires a break above the April 17 peak at $4890.97, which marked the end of wave (1). In the near term, wave (i) of the new cycle should finish soon. A corrective pullback in wave (ii) is expected, addressing the cycle from the May 28, 2026 low before the rally resumes. As long as the pivot at $4365.13 holds, pullbacks should attract buyers. These retracements are likely to form in three or seven swings, supporting further upside. The structure suggests Gold has shifted from correction to impulsive advance, with the support zone providing the base for the next bullish phase.

Spot Gold (XAUUSD) 60-Minute Elliott Wave Chart

XAUUSD Elliott Wave Video:

https://www.youtube.com/watch?v=aOmnScRdvPw