Sample Category Title

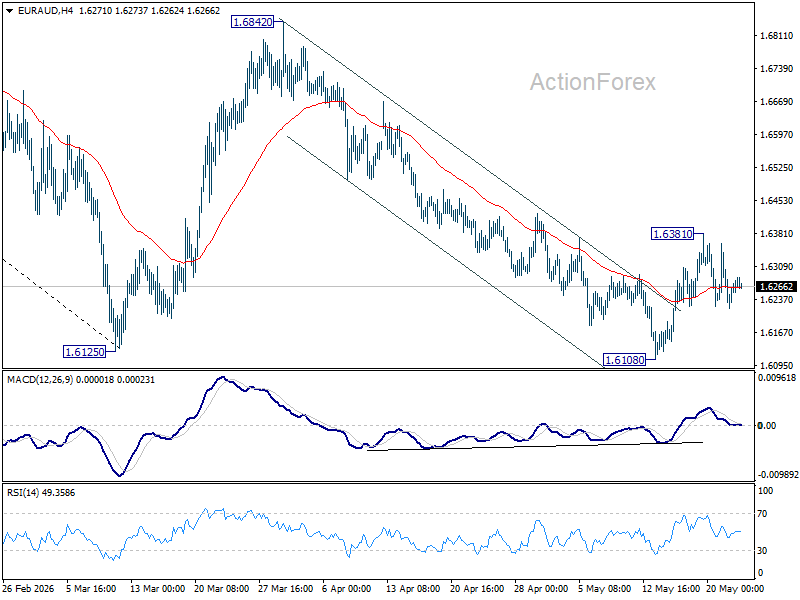

EUR/AUD Weekly Outlook

EUR/AUD recovered to 1.6381 last week but retreated since then. Initial bias remains neutral this week first. A short term bottom should be in place, and rise from 1.6108 is seen as the third leg of the corrective pattern from 1.6125. Above 1.6381 will bring stronger rebound to 55 D EMA (now at 1.6451) and above. Nevertheless, firm break of 1.6108 will resume the larger down trend from 1.8554.

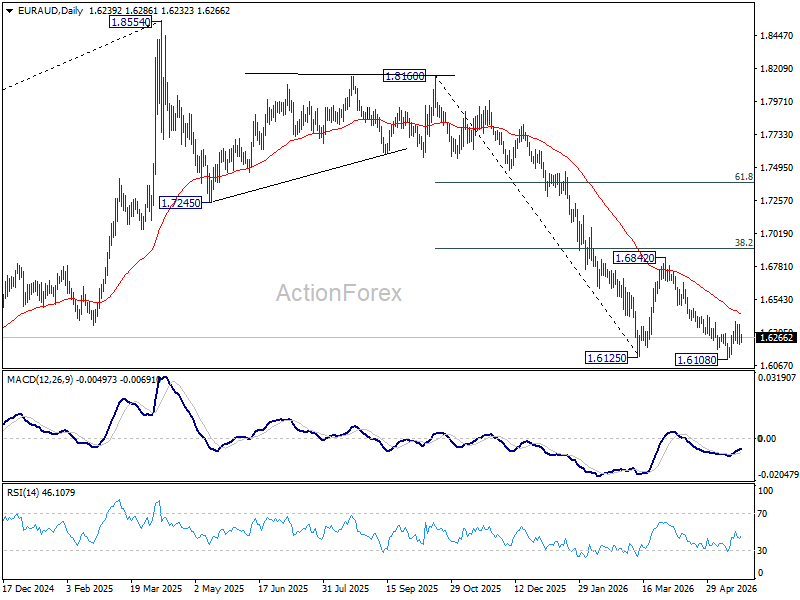

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7012) holds, even in case of strong rebound.

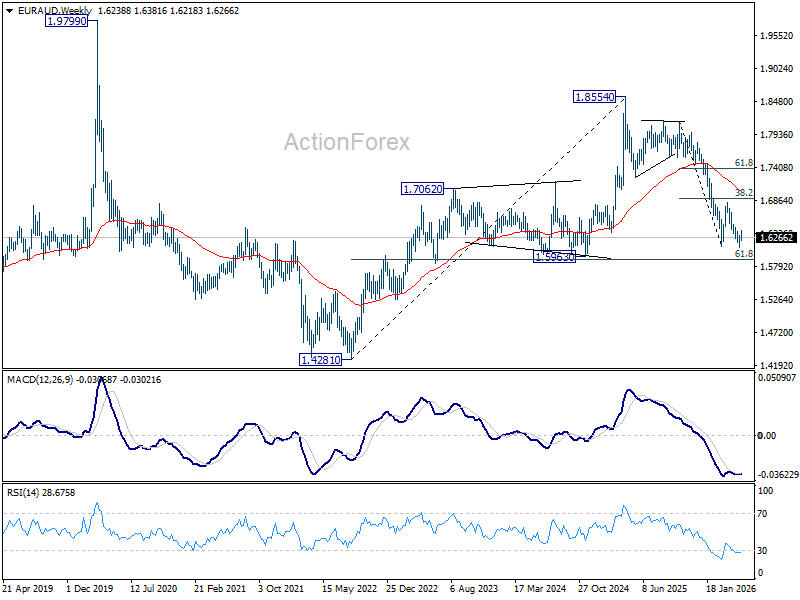

In the longer term picture, fall from 1.8554 is seen as the third leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Sustained trading below 55 M EMA (now at 1.6578) will confirm this bearish case, and pave the way back towards 1.4281.

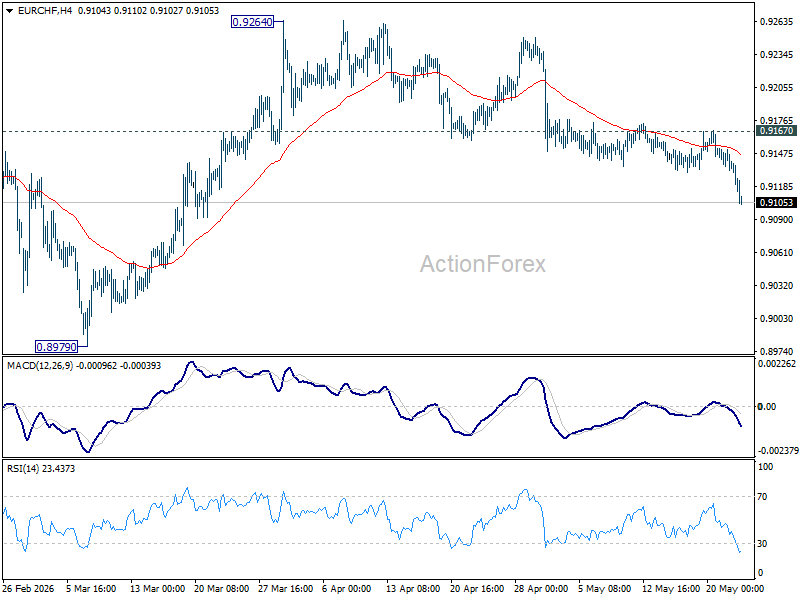

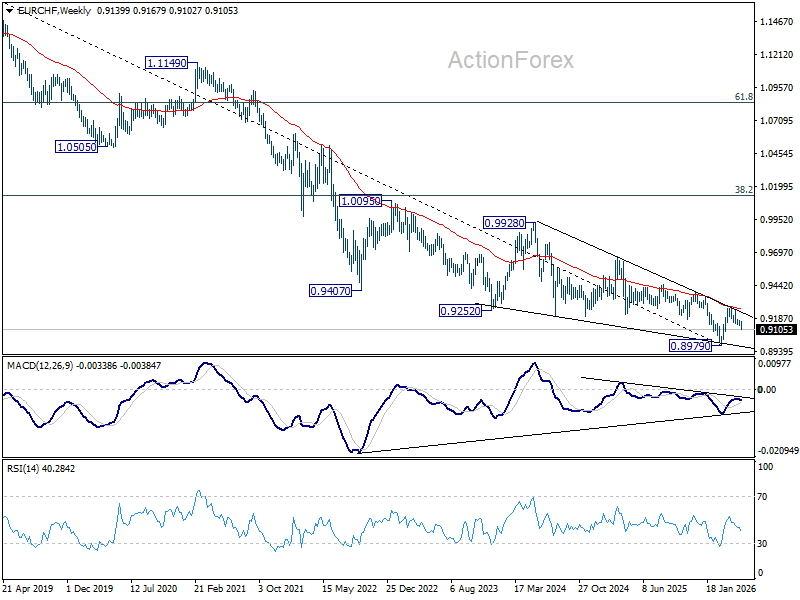

EUR/CHF Weekly Outlook

EUR/CHF's fall from 0.9264 extended lower last week and accelerated after failing to break above 55 D EMA (now at 0.9166). The development confirms that rebound from 0.8979 has already completed. Initial bias is on the downside this week for retesting 0.8979 low. For now, risk will stay on the downside as long as 0.9167 resistance holds.

In the bigger picture, the rejection by 55 W EMA (now at 0.9258) suggests that the down trend from 0.9928 (2024 high) is still in progress. Firm break of 0.8979 will confirm down trend resumption. Outlook will stay bearish as long as 0.9394 resistance holds, in case of another rebound.

In the long term picture, outlook will stay bearish as long as 0.9407 support turned resistance (2022 low) holds. However, firm break of 0.9407 will argue that the down trend from 1.2004 (2018 high) has completed with five waves down to 0.8979. Stronger rebound should then be seen to 38.2% retracement of 1.2004 to 0.8979 at 1.0135 in the medium term.

A Final Path to Peace? Markets Weekly Outlook

- Discover our weekly market outlook, exploring themes and events that forged financial flows throughout the week.

- Participants went through a rollercoaster of emotions in the past week, from a rejected Iranian offer to a severe hawkish repricing and finally, a promising path to peace.

- Traders are getting ready for next week's important bet for peace.

- Get ready for next week's action by exploring upcoming events across global markets.

Week in Review: Earnings Break Records, Pulling Markets Higher

Market participants endured an absolute rollercoaster of emotions over the past five sessions, navigating a market that violently whipsawed between extreme fear and sudden euphoria. The week kicked off with intense anxiety as the United States firmly rejected an initial Iranian diplomatic offer, a move that immediately spiked crude oil prices and threatened to reignite severe inflationary pressures.

Compounding this geopolitical dread was a severe, hawkish monetary repricing. Following the official confirmation of Kevin Warsh as the incoming Federal Reserve Chairman, institutional capital aggressively scrambled to price in a revolutionary, austere era of balance sheet reduction.

This emerging trade unleashed a ruthless wave of US Dollar dominance, temporarily suffocating equities, precious metals, and crypto beneath the weight of surging bond yields.

However, just as the technical charts looked their bleakest, the narrative completely flipped. A sudden, highly promising path to peace emerged, supported by strategic Middle Eastern mediation.

This breakthrough triggered a massive risk-on relief rally heading into the weekend.

As the geopolitical clouds finally begin to clear, traders are aggressively recalibrating their portfolios, getting ready for next week's incredibly important bet on global stability.

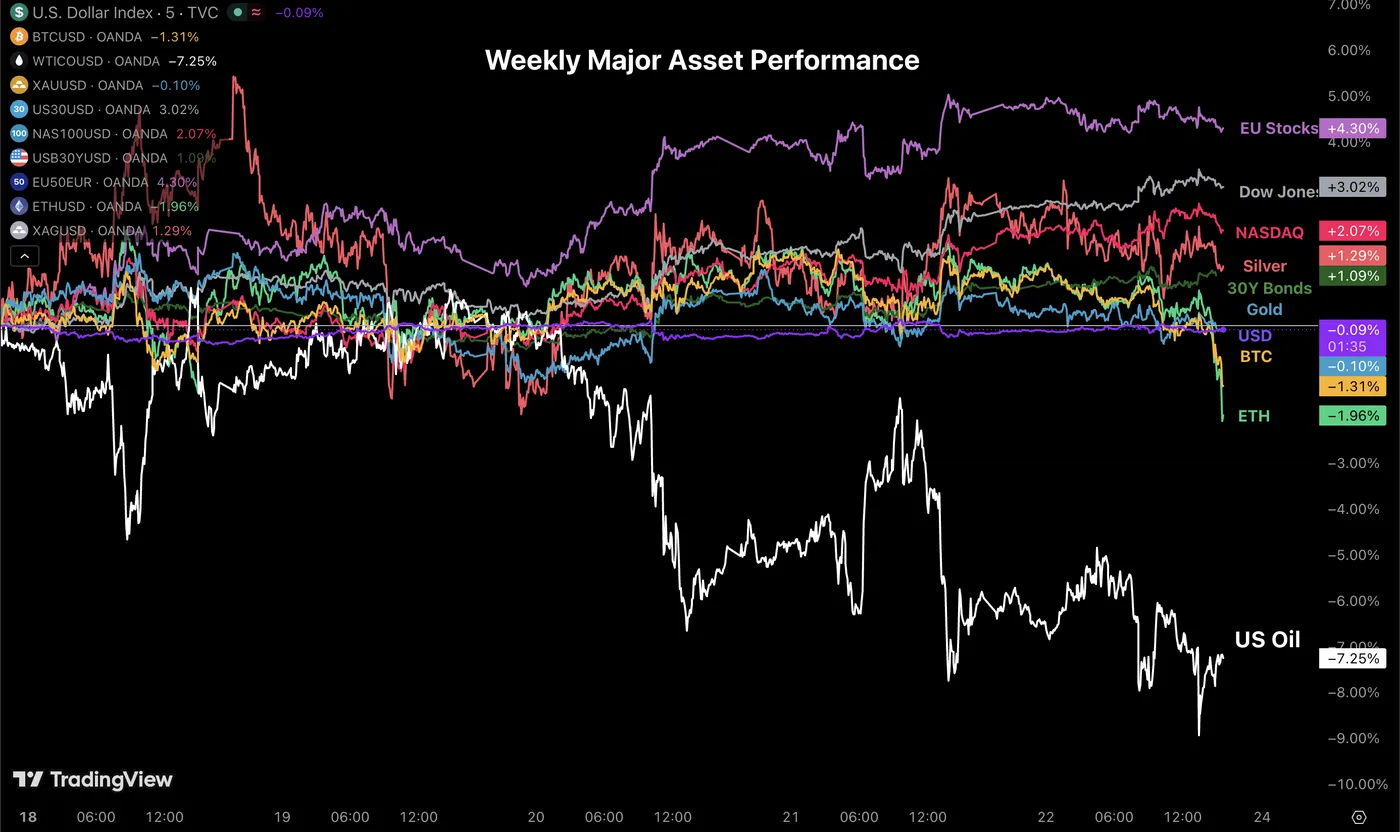

Weekly Performance Across Asset Classes

Weekly asset performance. Source: TradingView, May 22, 2026.

With oil tumbling 7%, the rest of the market shines. European stock markets are once again at the top of global assets.

Keep an eye on the huge outflows in cryptos towards the end of the week.

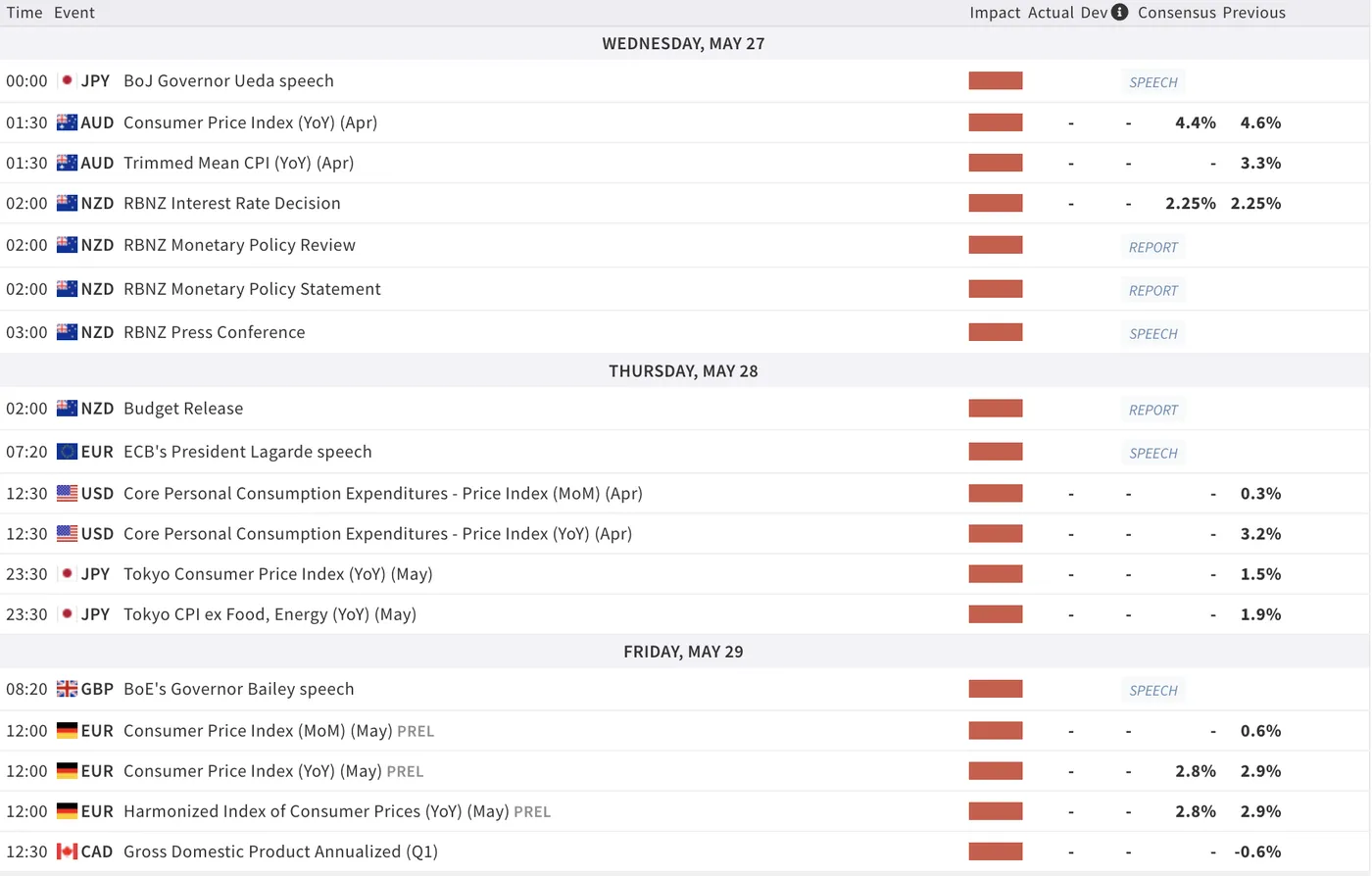

The Week Ahead: GDP Releases and a Potential Path to Peace

Asia Pacific Markets: RBNZ Meeting, Australian and Japanese CPI

The entire action in Asia will be focused on Wednesday and Thursday, with a key inflation release for Australia, shortly followed by the RBNZ rate decision, where a hike is mostly priced.

And do not forget the Japanese Tokyo CPI on Thursday evening.

Europe and UK Markets: German CPI and Many Central Bank Speeches

The action will be relatively dull in Europe with only central bank speeches, all the way to Friday with German CPI.

Expect European traders to focus on US Dollar flows and the entire Iran peace process.

North American Markets: US and Canadian GDP

Next week will focus on the American and Canadian GDP releases, in between a few lower-tier numbers.

Do not forget to keep a close eye on US markets and the entire US-Iran peace process, with huge expectations for an actual entente.

Next Week's High-Tier Economic Events

Next week's economic calendar. Courtesy of TradingEconomics.

Safe trades and keep an eye on US-Iran developments.

The Weekly Bottom Line: Markets Position for Higher-For-Longer Oil Prices

Canadian Highlights

- Headline CPI rose to 2.8% on gasoline, but core measures remain well-behaved and inflation breadth remained at pre-pandemic norms.

- Next week’s GDP release should confirm decent Q1 growth, but the focus will shift to early Q2 momentum amid signs of labour market cooling in April.

- While energy pass-through is expected to lift core inflation starting in late Q2, soft inflation in the hear-and-now supports a patient near-term BoC stance.

U.S. Highlights

- Markets remained focused on the Middle East conflict this week, with the 10-year Treasury yield briefly touching a sixteen-month high mid-week.

- Rising yields have also dragged mortgage rates higher, weighing on both home sales and residential construction.

- FOMC minutes from the April 28-29 meeting showed an increasingly hawkish committee, amid rising inflationary pressures.

Canada – Soft Inflation Dynamics Give BoC Room to Stay Patient

Canadian financial markets seemingly exhaled a bit this week, catalyzed (to borrow a phrase from PM Carney) by constructive developments for the inflation backdrop. One important trigger was messaging that a U.S.-Iran deal may be in its final stages. Accordingly, oil prices slid, with the benchmark WTI dropping about $10/barrel, as of writing. The other major catalyst was an April inflation report that was soft at its core. The Canadian 5-year bond yield (which underpins the popular 5-year mortgage rate product) was off about 15 bps (at the time of writing) while equities were higher on the week.

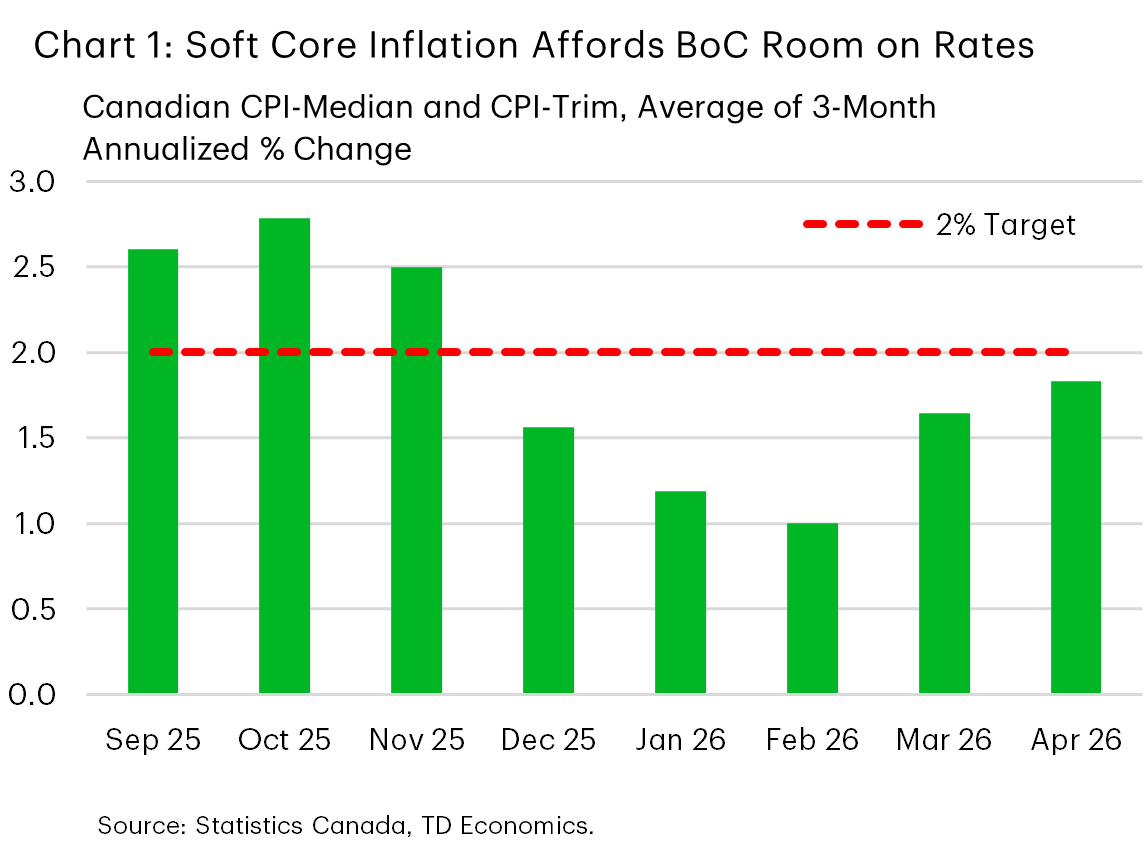

Markets were braced for a “3-handle” on inflation last month. Instead, overall inflation clocked in at 2.8%. While this was an acceleration from March, as expected given the jump in gasoline prices, there was little evidence that the inflationary pressures from the war were materially feeding into prices more broadly yet. The Bank of Canada’s two preferred core inflation measures ticked higher when measured on a shorter-term basis. However, they were still below the BoC’s 2% target, on average (Chart 1). Interestingly, air transportation prices were down on year-on-year terms, which was surprising given the trajectory of fuel prices since the onset of the war. Meanwhile, inflation’s breadth across categories – a favoured metric by the BoC – reduced a bit and was at 2018/19 levels, when inflation was comfortably in the target range.

There are a few caveats to keep in mind with April inflation. One is that it takes time for a spike in energy costs to feed through into core inflation. We reckon that we should be seeing some pass-through starting in June, which is also when hotel rates will be pressured higher by the World Cup games played in Toronto and Vancouver.

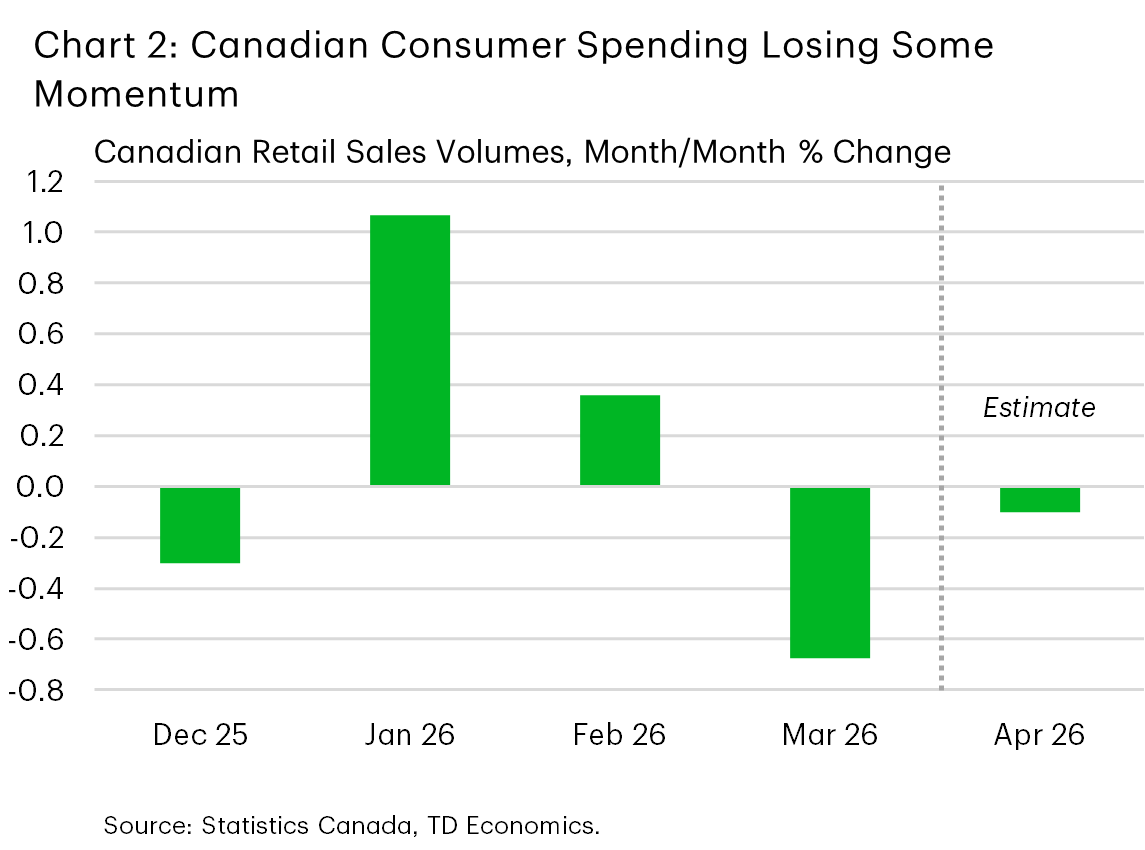

The second is that soft underlying inflation could be signalling a weak economy that’s limiting the ability of firms to pass through cost increases. Indeed, this week featured a steep 0.7% monthly decline for March retail sales volumes (Chart 2). Looking ahead, next week will bring the first quarter real GDP report and a preliminary monthly reading for April. We think the economy expanded by about 1.5% annualized in Q1, in line with the BoC’s forecast. Potentially more interesting will be the early read on second quarter activity. This will be known with certainty next week, but earlier estimates suggest that monthly GDP was flat in March. The labour market also cooled last month, while preliminary retail spending data points to a subdued performance after stripping away price gains. If economic activity was indeed modest to begin Q2, this could challenge the BoC’s call for a 1.5% annualized gain in real GDP.

All told, this week’s events added notable weight to the narrative that the Bank of Canada can be patient on rates, with no move expected at their next meeting on June 10th. For our part, we see the Bank of Canada staying on hold for the remainder of the year, conditional on a relatively speedy resolution to the tensions in the Middle East.

U.S. – Markets Position for Higher-For-Longer Oil Prices

The economic calendar was light this week, so financial markets—which remain highly sensitive to developments in the Middle East—took centre stage. The bond market selloff continued this week, with Treasury yields and oil prices moving higher. The 10-year Treasury yield pushed toward 4.7%, the highest since January 2025, while oil prices—as measured by the WTI benchmark—briefly touched $109. Both have since retraced on renewed hopes of a U.S.-Iran deal. However, markets seem to be converging around a “higher-for-longer” outlook for both oil prices and interest rates.

Higher treasury yields are already passing through to the real economy via higher mortgage rates. After trending down toward 6% before the U.S.-Iran war, 30-year mortgage rates have climbed back to 6.5% this week, marking the fourth year they’ve remained above 6%. This deterioration in affordability will translate into another subdued spring homebuying season and will weigh on residential construction. Single-family housing starts edged lower in April and remain below year-ago levels. Multifamily starts are faring better, as high mortgage rates are propping up the rental market.

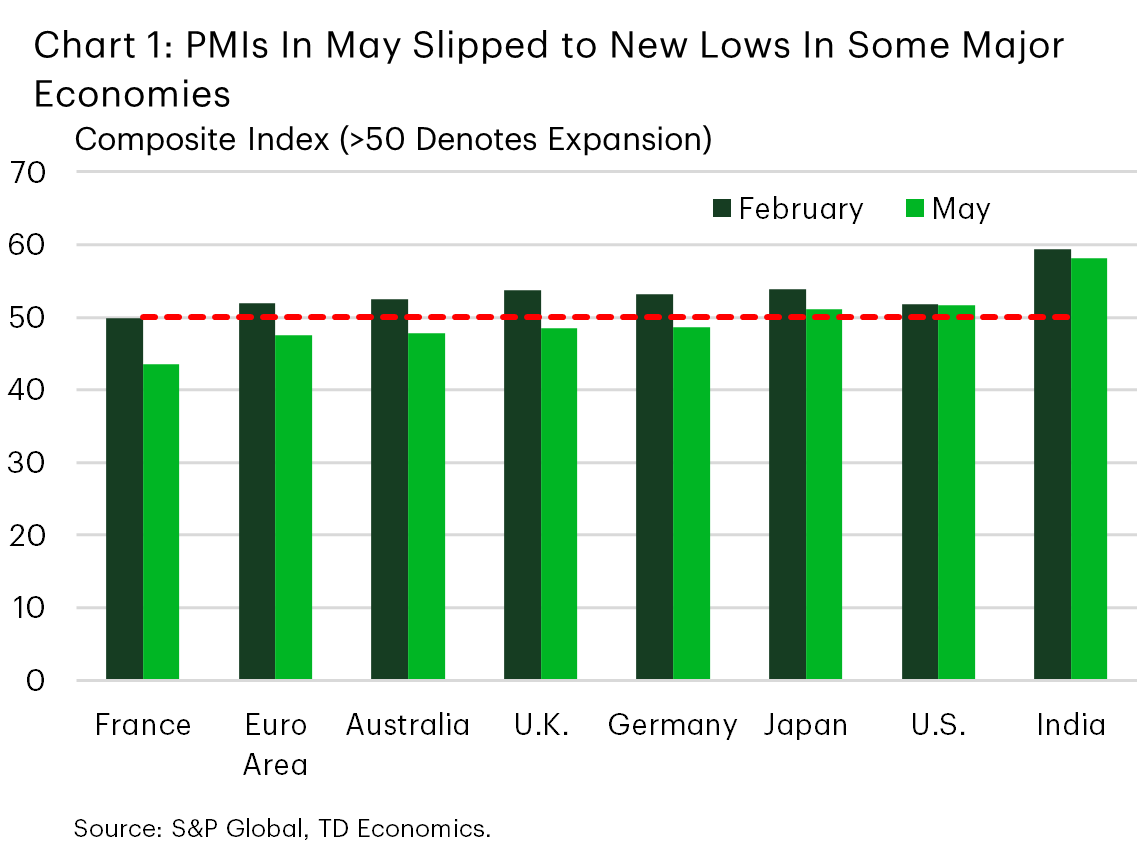

Economic activity in the U.S. has shown surprising resilience in the face of the oil supply shock. However, as the conflict drags into a third month, May’s Purchasing Managers Indexes for other key global economies point to a broad-based loss of momentum due to high energy costs (Chart 1). Purchasing manager confidence in many European economies reached multi-year lows, while input cost pressures have reignited, reaching multi-year highs. This mix of weakening output and resurgent costs raises concerns of a potential stagflationary shock, particularly if oil prices remain near $100 per barrel through the rest of this year.

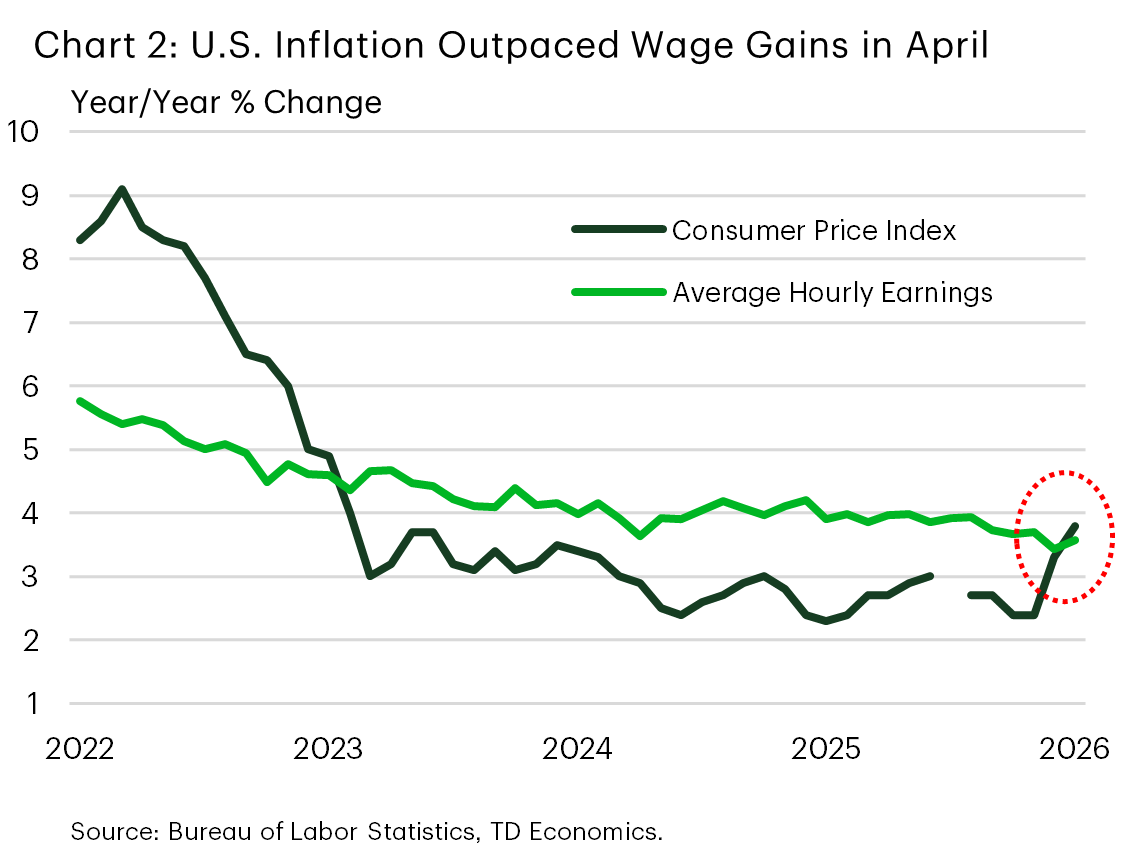

As discussed in our Quarterly Q&A report, the U.S. economy is more insulated from higher oil prices due to several factors. American households also have some cushion in the form of higher tax refunds, lower taxes, and rising stock prices. Still, U.S. consumer spending growth is expected to downshift this year, holding below 2% through most of 2026. With inflation again outpacing wage gains (Chart 2), the latest price shock, combined with higher mortgage rates, will continue to test consumers’ resilience. The upcoming release of April income and spending data will provide a temperature check on households’ financial well-being.

With a policy rate that is still modestly restrictive, a stable labour market, and rising inflationary risks, the Fed is likely to remain on the sidelines this year. This was evident in the release of FOMC minutes from the April 28-29 meeting, which showed a growing hawkish bias among the committee. In a speech earlier this week, FOMC member Barkin suggested that there is a growing risk that if left unchecked, persistently elevated price pressures could unanchor inflation expectations. Should this occur, it would prevent the Fed from “looking through” the supply shock, and could ultimately force its hand to raise rates.

Economics Week Ahead

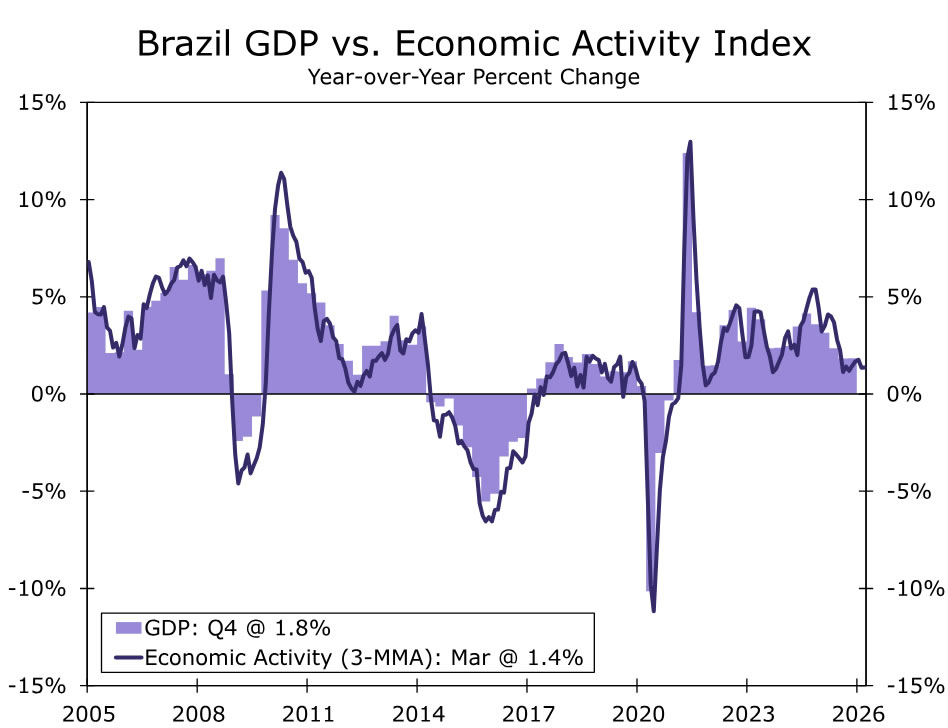

Next week’s U.S. data should point to a resilient, but increasingly strained, consumer spending environment. We expect the PCE deflator rose 0.4% in April, weighing on household purchasing power and leaving real income growth soft. The housing market remains constrained, with renewed affordability pressures and supply-side constraints, and we expect new home sales fell back toward a 669K pace in April as higher mortgage rates and a weak labor market weigh on demand. In emerging markets, Brazil’s growth likely held firm in Q1, but momentum is set to slow as inflation risks rise and policy remains restrictive. In Australia, we expect headline CPI to rise 4.7% year over year, driven largely by Easter holiday travel, with trimmed mean at 3.4%, while temporary fuel excise cuts keep energy prices more contained.

United States:

- Personal Income & Spending (Thursday), New Home Sales (Thursday)

G10 Economies:

- Australia CPI (Wednesday)

Emerging Markets:

- Brazil GDP (Friday)

U.S. Week Ahead

Personal Income & Spending • Thursday

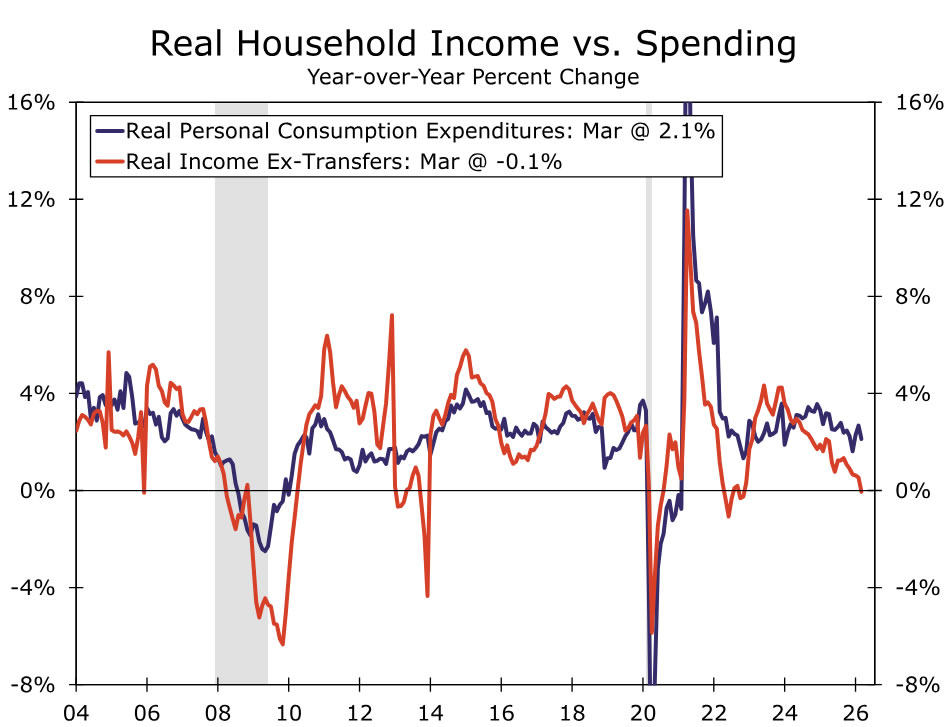

Broad consumer spending carried into April, but the backdrop is becoming more challenging as the conflict in Iran drags on. Control group retail sales (sales excluding gas, autos, building materials, and restaurants) rose 0.5% during the month and growth remained positive even when adjusting for higher prices. That decent growth, along with some modest upward revisions to prior data, suggests goods spending started off on a decent clip in the second quarter. Still, households are operating in a constrained environment, with rising trade-offs in how spending is allocated.

We estimate consumer inflation measured by the PCE deflator rose 0.4% in April, offsetting nearly all the 0.5% gain we expect in nominal spending growth. Renewed price pressure is eroding household purchasing power, while a cooling labor market and lackluster hiring are weighing on wage growth. We look for broad personal income to rise 0.4%, leaving real income growth weak and unlikely to sustain current spending momentum.

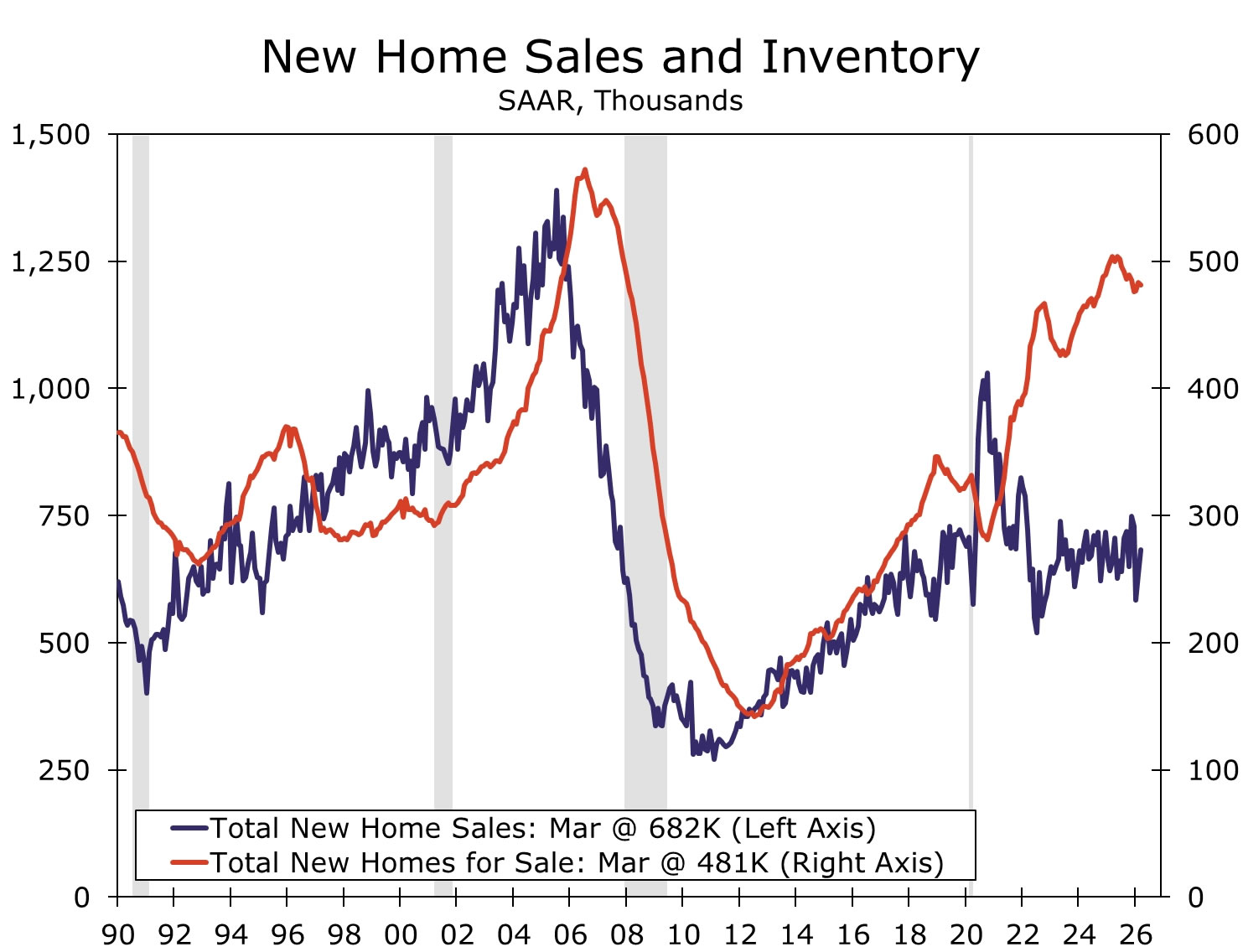

New Home Sales • Thursday

The trend in sales has firmed over the past several months. During March, the pace of sales rose to 682K, a 3.3% year-over-year gain. That said, the new home market remains generally soft. Builders continue to lean on incentives such as mortgage rate buy-downs and price cuts to support demand, and in March, the median new home price was down 6.2% on a yearly basis. Meanwhile, inventory remained high with the count of new homes available for sale at 481K in March.

Looking forward, we expect new home sales fell back to a 669K unit pace in April. Mortgage rates have legged higher in recent months and are currently hovering around 6.5%, largely reflecting the war in the Middle East and the potential for an end to the Fed's easing cycle on account of higher inflation. In addition to renewed affordability challenges, weak labor market fundamentals represent another headwind for demand. What's more, builders are contending with several supply-side constraints, including elevated inventory levels, higher land prices and increased building material and labor costs.

G10 Week Ahead

Australia CPI • Wednesday

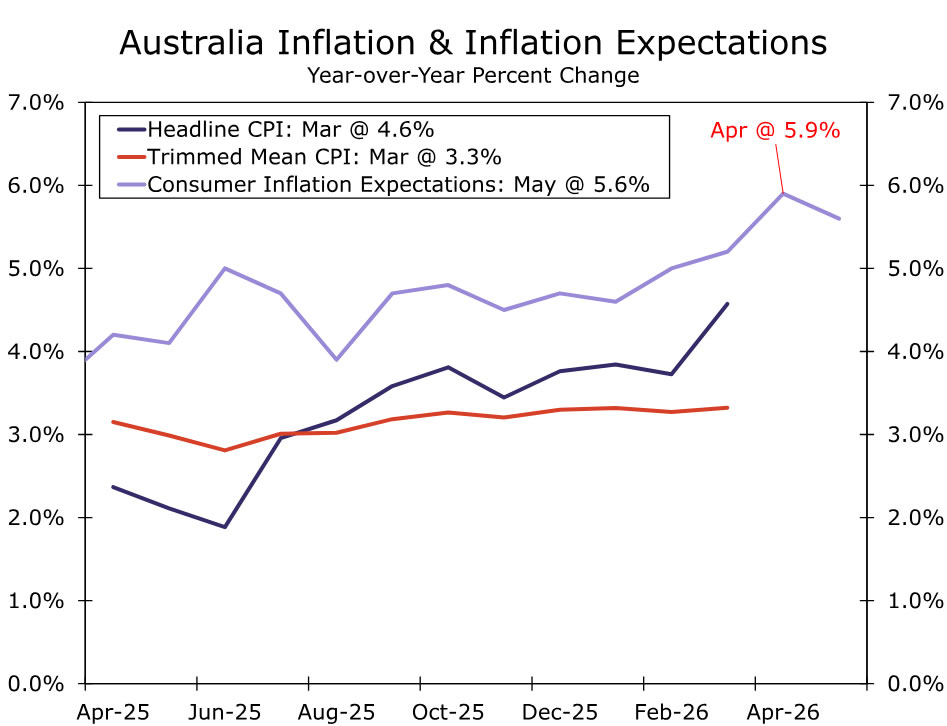

Next week brings Australia’s April inflation release. We expect headline CPI to rise 4.7% year over year, with trimmed mean inflation at 3.4%. In March, CPI rose 4.6%, driven largely by a 33% month-over-month surge in fuel prices. The government announced temporary measures to reduce fuel excise by half from April 1, which lowered average petrol pump prices. At its May monetary policy meeting, the Reserve Bank of Australia (RBA) said it expected the measure to subtract around 0.5 percentage points from year-over-year inflation in April.

Still, the cost shock appears broader than fuel. April PMIs and business surveys pointed to stronger price pressures, with firms also raising output prices at one of the fastest rates in the survey’s decade-long history. Pass-through may be visible across food, recreation, and housing-related categories. Restaurants have enacted temporary fuel surcharges, while reports also point to sharp increases in building material costs, including pipes, timber, and plastic. Seasonal Easter travel could also lift recreation and culture inflation.

With the RBA focused on inflation risks and inflation expectations as its "north star,” the April data will be important for gauging how quickly higher input costs are moving through the broader inflation basket. A stronger-than-expected print would raise upside risks to the Cash Rate, especially after the 2026–27 Federal Budget leaned more stimulative. At the same time, recent labor market data have shown some signs of easing, which supports a data-dependent approach. We continue to expect a June hold and an August hike, bringing the Cash Rate to a terminal rate of 4.60%, with the RBA’s next move contingent on developments in the Middle East conflict, inflation’s response to this year’s three rate hikes, growth, and labor market conditions.

EM Week Ahead

Brazil GDP • Friday

Brazil’s Q1-2026 GDP data are due next week and are likely to show that the economy expanded by 1.0% quarter over quarter and 1.5% year over year. Strong real wage gains and supportive fiscal policy have continued to underpin consumption, helping activity start the year on solid footing. However, growth is likely to soften beyond Q1 as restrictive policy weighs more heavily on activity. The inflation backdrop has also become more complicated, as disinflation from last year’s aggressive tightening faces renewed external price pressures from the war in the Middle East and persistent domestic fiscal risks. Election-year dynamics are also likely to add pressure for more stimulative fiscal policy, while longer-term inflation expectations have moved higher across survey-based and market-based measures. These factors should constrain the scope for monetary easing.

Against this backdrop, we still expect the Brazilian Central Bank (BCB) to proceed with monetary easing, but at a more cautious pace than anticipated at the start of the year. We now see fewer cuts over the remainder of 2026. While easing is still likely to extend into 2027, we expect a higher terminal rate as policy decisions become increasingly driven by the evolving inflation outlook, rather than growth conditions alone.

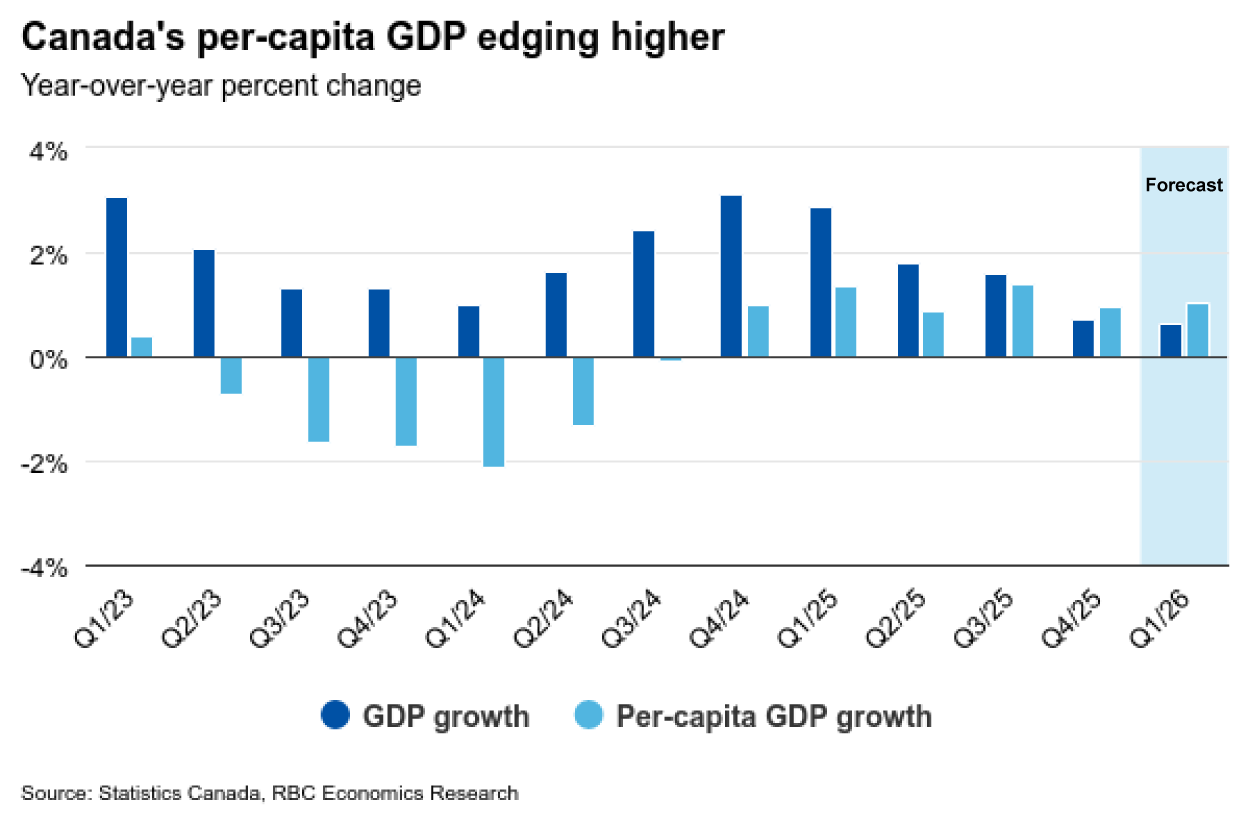

Canada’s GDP Growth Likely Turned Positive in Q1 After Q4 Contraction

Canada’s economy likely returned to growth in Q1 2026 with gross domestic product bouncing back by an annualized 1.7% after declining 0.6% in Q4, supported by improving domestic growth drivers.

Details behind the decline in Q4 were less concerning than headlines—domestic demand improved with governments, consumers, and businesses all increasing spending while the offset mainly come from using up inventories, and another decline in residential investment.

Residential investment will remain a soft spot in Q1 with home resales continuing to decline, but household and government spending have both been picking up and a large inventory subtraction in Q4 is unlikely to be repeated.

A surge in Q1 imports could leave net exports subtracting about 4 percentage points from growth, but that’s also consistent with firming consumer spending and business investment. Temporary disruptions from large strikes in the education and transportation (postal) sectors subtracted from Q4 growth, but will add to Q1 output with workers back on the job.

Broadly, the 1.7% quarterly annualized growth in Q1 was again against a backdrop of rapidly slowing immigration and population growth. By our count, interpolating recent demographic trends (specifically a declining non-permanent resident population) would suggest little change in overall population in Q1, and further acceleration in per capita economic growth.

This remains consistent with our overall expectation that per person economic conditions in Canada should continue to improve in 2026 after rising in 2025 for the first time in three years. That is, however, contingent on key assumptions that oil prices start to normalize beyond this quarter, and broader U.S. tariffs won’t escalate.

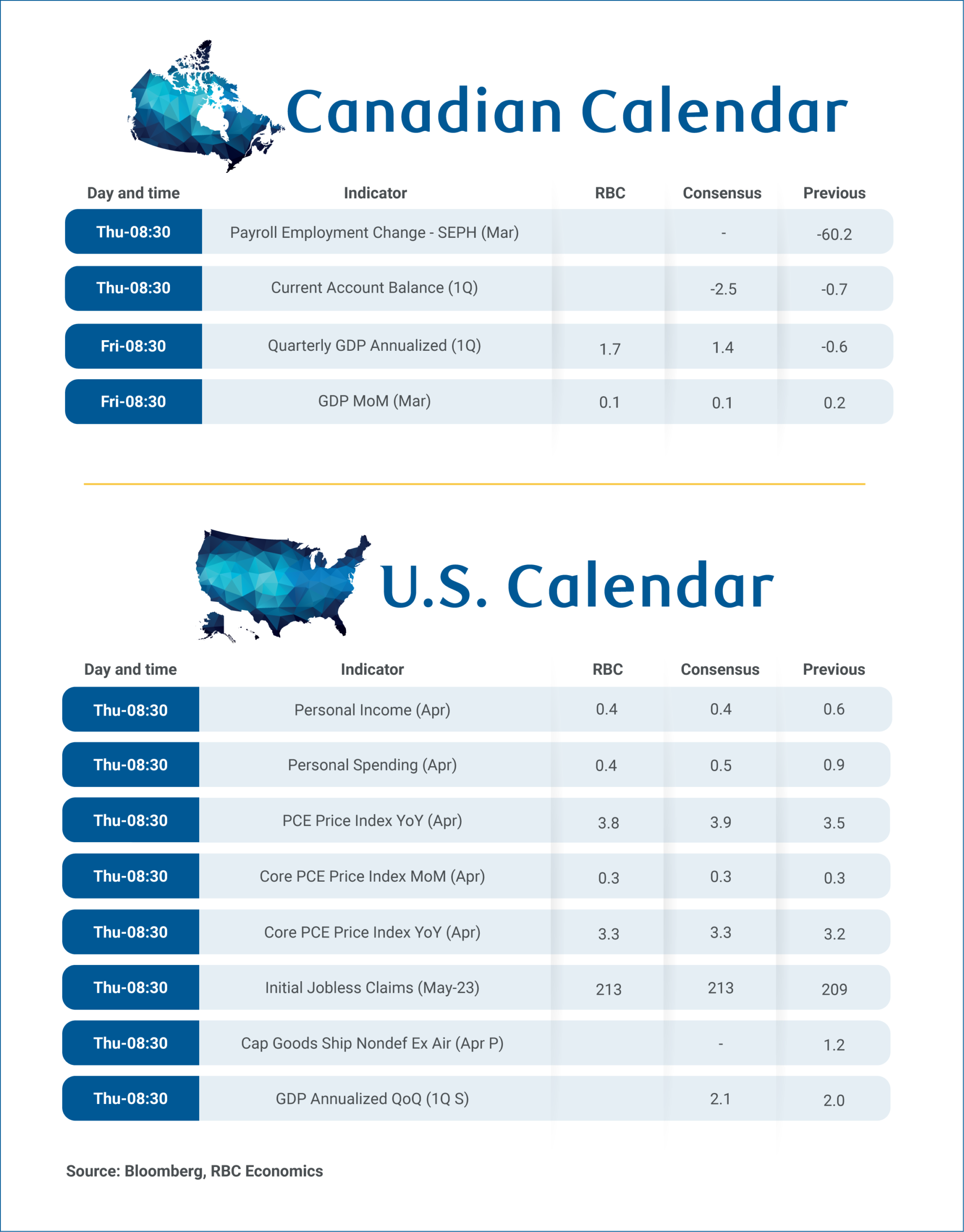

Monthly GDP points to modest increase in March

We expect GDP to have continued to grow in March, expanding 0.1% from February in real terms after advancing at an average pace of 0.15% in the previous two months. That’s above Statistics Canada’s preliminary estimate from a month ago calling for a flat reading in March.

Growth was led by wholesale sales, particularly in the machinery, equipment and supplies subsector, reflecting increased deliveries to government clients. Manufacturing output also rose, supported by an ongoing recovery in the auto sector after earlier disruptions. Those gains were offset partially by contracting mining and oil and gas extraction output and weaker retail activities in March.

Canada’s March Survey of Employment, Payrolls and Hours (SEPH) will be watched closely after a sharp drop in jobs in the timelier Labour Force Survey (LFS) in 2026 to April. SEPH employment counts have been persistently lagging paid employment counts in the LFS (unchanged from a year ago as of February in SEPH versus a 0.4% increase in the LFS). Still, job vacancies in the SEPH (not available from the LFS) have been edging higher in a sign labour demand is stabilizing. We expect SEPH wage growth will continue to underperform surprisingly firm LFS readings in recent months. SEPH wage growth has been running around 3%, which is more consistent with an elevated unemployment rate vs. the 4.5% plus readings from the LFS in March and April.

We expect personal income and spending to have both risen 0.4% in April in the U.S. from March, the latter entirely reflecting a surge in prices led by gasoline, while real spending declined 0.1%.

Summary 5/25 – 5/29

Monday, May 25, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 12:30 | CAD | Corporate Profits Q/Q Q1 | -1.60% |

| 12:30 | CAD |

| Corporate Profits Q/Q Q1 | |

| Consensus | |

| Previous | -1.60% |

Tuesday, May 26, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Mar | 1.00% | 0.90% |

| 13:00 | USD | Housing Price Index M/M Mar | 0.10% | 0.00% |

| 14:00 | USD | Consumer Confidence May | 91.6 | 92.8 |

| 13:00 | USD |

| S&P/Case-Shiller Home Price Indices Y/Y Mar | |

| Consensus | 1.00% |

| Previous | 0.90% |

| 13:00 | USD |

| Housing Price Index M/M Mar | |

| Consensus | 0.10% |

| Previous | 0.00% |

| 14:00 | USD |

| Consumer Confidence May | |

| Consensus | 91.6 |

| Previous | 92.8 |

Wednesday, May 27, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 3.00% | 3.10% |

| 01:00 | AUD | Westpac Leading Index M/M Mar | -0.10% | |

| 01:30 | AUD | CPI M/M Apr | 0.60% | 1.10% |

| 01:30 | AUD | CPI Y/Y Apr | 4.40% | 4.60% |

| 01:30 | AUD | Trimmed Mean CPI M/M Apr | 0.40% | 0.30% |

| 01:30 | AUD | Trimmed Mean CPI Y/Y Apr | 3.40% | 3.30% |

| 02:00 | NZD | RBNZ Interest Rate Decision | 2.25% | 2.25% |

| 08:00 | CHF | UBS Economic Expectations May | -30.3 |

| 23:50 | JPY |

| Corporate Service Price Index Y/Y Apr | |

| Consensus | 3.00% |

| Previous | 3.10% |

| 01:00 | AUD |

| Westpac Leading Index M/M Mar | |

| Consensus | |

| Previous | -0.10% |

| 01:30 | AUD |

| CPI M/M Apr | |

| Consensus | 0.60% |

| Previous | 1.10% |

| 01:30 | AUD |

| CPI Y/Y Apr | |

| Consensus | 4.40% |

| Previous | 4.60% |

| 01:30 | AUD |

| Trimmed Mean CPI M/M Apr | |

| Consensus | 0.40% |

| Previous | 0.30% |

| 01:30 | AUD |

| Trimmed Mean CPI Y/Y Apr | |

| Consensus | 3.40% |

| Previous | 3.30% |

| 02:00 | NZD |

| RBNZ Interest Rate Decision | |

| Consensus | 2.25% |

| Previous | 2.25% |

| 08:00 | CHF |

| UBS Economic Expectations May | |

| Consensus | |

| Previous | -30.3 |

Thursday, May 28, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 01:30 | AUD | Private Capital Expenditure Q1 | 1.00% | 0.40% |

| 09:00 | EUR | Eurozone Economic Sentiment May | 92 | 93 |

| 09:00 | EUR | Eurozone Services Sentiment May | 0.1 | 0.9 |

| 09:00 | EUR | Eurozone Industrial Confidence May | -7.8 | -7.7 |

| 09:00 | EUR | Eurozone Consumer Confidence May F | -19 | -19 |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||

| 12:30 | CAD | Current Account (CAD) Q1 | -1.9B | -0.7B |

| 12:30 | USD | Initial Jobless Claims (May 22) | 210K | 209K |

| 12:30 | USD | Personal Income M/M Apr | 0.40% | 0.60% |

| 12:30 | USD | Personal Spending M/M Apr | 0.50% | 0.90% |

| 12:30 | USD | PCE Price Index M/M Apr | 0.50% | 0.70% |

| 12:30 | USD | PCE Price Index Y/Y Apr | 3.80% | 3.50% |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.30% | 0.30% |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 3.30% | 3.20% |

| 12:30 | USD | Durable Goods Orders Apr | 3.30% | 0.80% |

| 12:30 | USD | Durable Goods Orders ex Transport Apr | 0.50% | 0.90% |

| 12:30 | USD | GDP Annualized Q1 P | 2% | 2% |

| 14:00 | USD | New Home Sales Apr | 661K | 682K |

| 14:30 | USD | Natural Gas Storage (May 22) | 96B | 101B |

| 16:00 | USD | Crude Oil Inventories (May 22) | -3.8M | -7.9M |

| 01:30 | AUD |

| Private Capital Expenditure Q1 | |

| Consensus | 1.00% |

| Previous | 0.40% |

| 09:00 | EUR |

| Eurozone Economic Sentiment May | |

| Consensus | 92 |

| Previous | 93 |

| 09:00 | EUR |

| Eurozone Services Sentiment May | |

| Consensus | 0.1 |

| Previous | 0.9 |

| 09:00 | EUR |

| Eurozone Industrial Confidence May | |

| Consensus | -7.8 |

| Previous | -7.7 |

| 09:00 | EUR |

| Eurozone Consumer Confidence May F | |

| Consensus | -19 |

| Previous | -19 |

| 11:30 | EUR |

| ECB Monetary Policy Meeting Accounts | |

| Consensus | |

| Previous | |

| 12:30 | CAD |

| Current Account (CAD) Q1 | |

| Consensus | -1.9B |

| Previous | -0.7B |

| 12:30 | USD |

| Initial Jobless Claims (May 22) | |

| Consensus | 210K |

| Previous | 209K |

| 12:30 | USD |

| Personal Income M/M Apr | |

| Consensus | 0.40% |

| Previous | 0.60% |

| 12:30 | USD |

| Personal Spending M/M Apr | |

| Consensus | 0.50% |

| Previous | 0.90% |

| 12:30 | USD |

| PCE Price Index M/M Apr | |

| Consensus | 0.50% |

| Previous | 0.70% |

| 12:30 | USD |

| PCE Price Index Y/Y Apr | |

| Consensus | 3.80% |

| Previous | 3.50% |

| 12:30 | USD |

| Core PCE Price Index M/M Apr | |

| Consensus | 0.30% |

| Previous | 0.30% |

| 12:30 | USD |

| Core PCE Price Index Y/Y Apr | |

| Consensus | 3.30% |

| Previous | 3.20% |

| 12:30 | USD |

| Durable Goods Orders Apr | |

| Consensus | 3.30% |

| Previous | 0.80% |

| 12:30 | USD |

| Durable Goods Orders ex Transport Apr | |

| Consensus | 0.50% |

| Previous | 0.90% |

| 12:30 | USD |

| GDP Annualized Q1 P | |

| Consensus | 2% |

| Previous | 2% |

| 14:00 | USD |

| New Home Sales Apr | |

| Consensus | 661K |

| Previous | 682K |

| 14:30 | USD |

| Natural Gas Storage (May 22) | |

| Consensus | 96B |

| Previous | 101B |

| 16:00 | USD |

| Crude Oil Inventories (May 22) | |

| Consensus | -3.8M |

| Previous | -7.9M |

Friday, May 29, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y May | 1.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 1.50% | 1.50% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y May | 1.90% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.70% | 2.70% |

| 23:50 | JPY | Industrial Production M/M Apr P | -0.30% | -0.40% |

| 23:50 | JPY | Retail Trade Y/Y Apr | 1.30% | 1.70% |

| 01:00 | NZD | ANZ Business Confidence May | -10.6 | |

| 01:00 | NZD | ANZ Activity Outlook May | 19.6 | |

| 05:00 | JPY | Housing Starts Y/Y Apr | 14.70% | -29.30% |

| 05:00 | JPY | Consumer Confidence Index May | 32.5 | 32.2 |

| 06:45 | EUR | France GDP Q/Q Q1 | 0.00% | 0.00% |

| 07:00 | CHF | KOF Leading Indicator Apr | 98 | 97.9 |

| 07:55 | EUR | Germany Unemployment Change Apr | 10K | 20K |

| 07:55 | EUR | Germany Unemployment Rate Apr | 6.40% | 6.40% |

| 12:00 | EUR | Germany CPI M/M May P | 0.10% | 0.60% |

| 12:00 | EUR | Germany CPI Y/Y May P | 2.80% | 2.90% |

| 12:30 | CAD | GDP M/M Mar | 0.10% | 0.20% |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -88.6B | -87.9B |

| 13:45 | USD | Chicago PMI May | 51.3 | 49.2 |

| 23:30 | JPY |

| Tokyo CPI Y/Y May | |

| Consensus | |

| Previous | 1.50% |

| 23:30 | JPY |

| Tokyo CPI Core Y/Y May | |

| Consensus | 1.50% |

| Previous | 1.50% |

| 23:30 | JPY |

| Tokyo CPI Core-Core Y/Y May | |

| Consensus | |

| Previous | 1.90% |

| 23:30 | JPY |

| Unemployment Rate Apr | |

| Consensus | 2.70% |

| Previous | 2.70% |

| 23:50 | JPY |

| Industrial Production M/M Apr P | |

| Consensus | -0.30% |

| Previous | -0.40% |

| 23:50 | JPY |

| Retail Trade Y/Y Apr | |

| Consensus | 1.30% |

| Previous | 1.70% |

| 01:00 | NZD |

| ANZ Business Confidence May | |

| Consensus | |

| Previous | -10.6 |

| 01:00 | NZD |

| ANZ Activity Outlook May | |

| Consensus | |

| Previous | 19.6 |

| 05:00 | JPY |

| Housing Starts Y/Y Apr | |

| Consensus | 14.70% |

| Previous | -29.30% |

| 05:00 | JPY |

| Consumer Confidence Index May | |

| Consensus | 32.5 |

| Previous | 32.2 |

| 06:45 | EUR |

| France GDP Q/Q Q1 | |

| Consensus | 0.00% |

| Previous | 0.00% |

| 07:00 | CHF |

| KOF Leading Indicator Apr | |

| Consensus | 98 |

| Previous | 97.9 |

| 07:55 | EUR |

| Germany Unemployment Change Apr | |

| Consensus | 10K |

| Previous | 20K |

| 07:55 | EUR |

| Germany Unemployment Rate Apr | |

| Consensus | 6.40% |

| Previous | 6.40% |

| 12:00 | EUR |

| Germany CPI M/M May P | |

| Consensus | 0.10% |

| Previous | 0.60% |

| 12:00 | EUR |

| Germany CPI Y/Y May P | |

| Consensus | 2.80% |

| Previous | 2.90% |

| 12:30 | CAD |

| GDP M/M Mar | |

| Consensus | 0.10% |

| Previous | 0.20% |

| 12:30 | USD |

| Goods Trade Balance (USD) Apr P | |

| Consensus | -88.6B |

| Previous | -87.9B |

| 13:45 | USD |

| Chicago PMI May | |

| Consensus | 51.3 |

| Previous | 49.2 |

Week Ahead: US PCE Inflation in Focus Amid Middle East Uncertainty, RBNZ Decides on Rates

- Middle East developments keep the Dollar range bound.

- But Fed rate hike bets remain elevated ahead of key US PCE data.

- RBNZ decision and Australia CPI data to test steep implied rate paths.

- Accelerating Tokyo CPI figures could ease intervention fears.

- Flash Italian, French, German CPI numbers, and Canada GDP also on tap.

Geopolitics Continue to Dominate the Market

After recording its strongest week in two months, the US Dollar traded in a consolidative manner this week, with the Dollar index oscillating between 98.80 and 99.40. The greenback started Monday on a strong footing following fresh Middle East tensions, including hostile rhetoric between US and Iranian officials, as well as drone attacks.

That said, Iran offered the US a new peace proposal just after the frictions, while US President Trump said on Wednesday that they are in the “final stages” of peace talks with Iran. This, combined with news that some vessels successfully passed through the Strait of Hormuz, put a lid on the Dollar’s rally and allowed oil prices to pull back.

Nonetheless, although the greenback did not accelerate its advance, it did not slide either. Perhaps this was due to the Fed minutes revealing growing concern among policymakers about inflation getting out of control, with several members becoming more open to the idea of rate hikes.

US PCE Data in Focus Amid Elevated Inflation Concerns

This allowed investors to maintain bets of a 25bps rate hike in the foreseeable future. A hike is more than fully priced in by March, while there is a strong 70% chance that it may happen this year.

Even if oil prices do not rally further, inflation could stay elevated as annual rates compare prices now with prices a year ago, which were still much lower. Therefore, should incoming data continue to confirm that, investors may decide to bring even closer the timing of when they expect a rate hike.

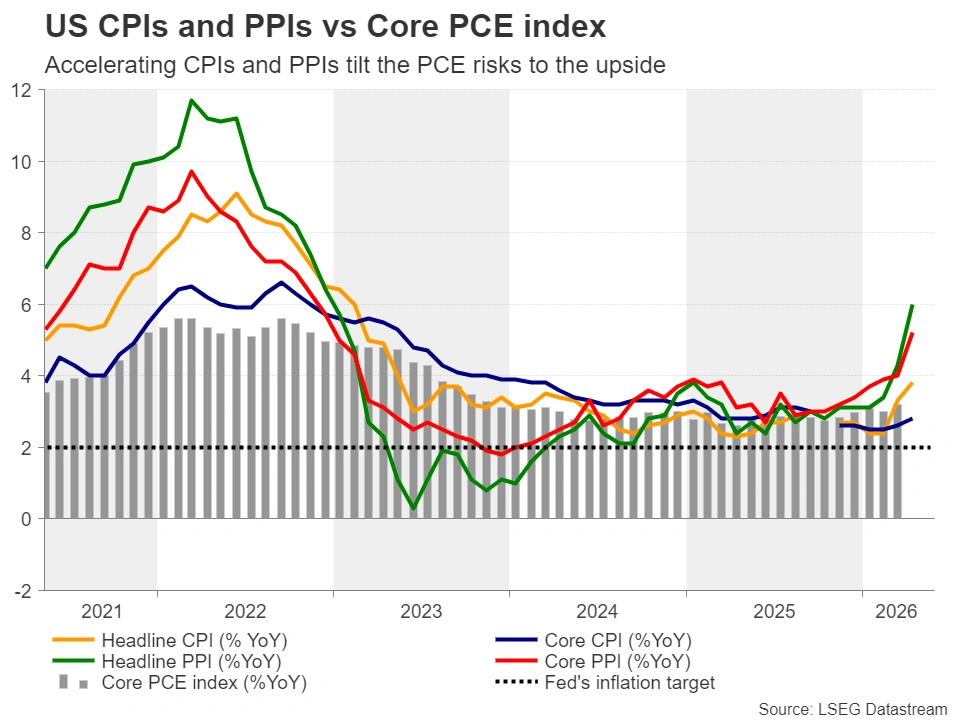

With all that in mind, Thursday’s core PCE index for April, the Fed’s favorite inflation gauge, comes alongside personal income and spending data for the same month, as well as the second estimate of GDP for Q1. Considering the hotter-than-expected CPI and PPI prints for the month, the risks surrounding the PCE indices may be tilted to the upside.

Higher-than-expected PCE rates, combined with decent growth-related data, could strengthen the case of a rate hike later this year and may allow the US Dollar to gain some more ground, especially if the US and Iran hit another dead end in peace talks.

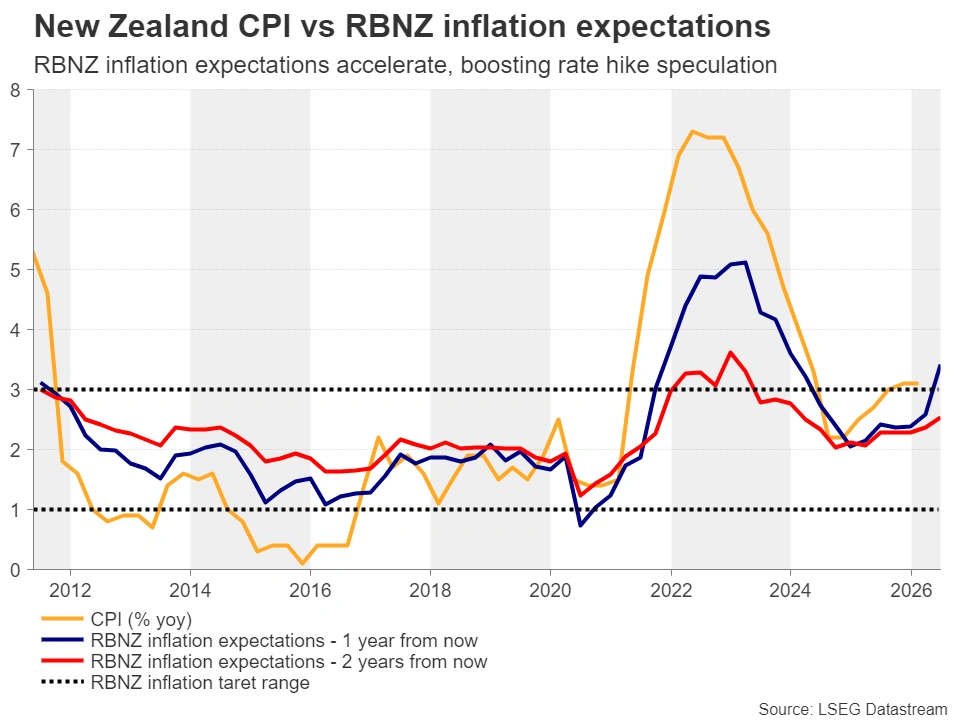

Will the RBNZ Reiterate Its Hawkish Message?

Flying to New Zealand, the Reserve Bank of New Zealand gathers to decide on monetary policy on Wednesday. When they last met, policymakers decided to keep the official cash rate unchanged at 2.25% but appeared concerned about the impact of the Middle East conflict on inflation and economic growth, signaling that they stand ready to act “decisively” if price pressures become more prominent.

This was interpreted as a hawkish hold, which combined with the acceleration in the 1- and 2-year inflation expectations, convinced investors that around three quarter-point rate hikes may be warranted by the end of the year. Although the probability of action at this gathering remains low at 25%, it rises to 80% for the July meeting.

Therefore, another hold accompanied by hawkish language could seal the deal for a July hike and perhaps send the Kiwi higher.

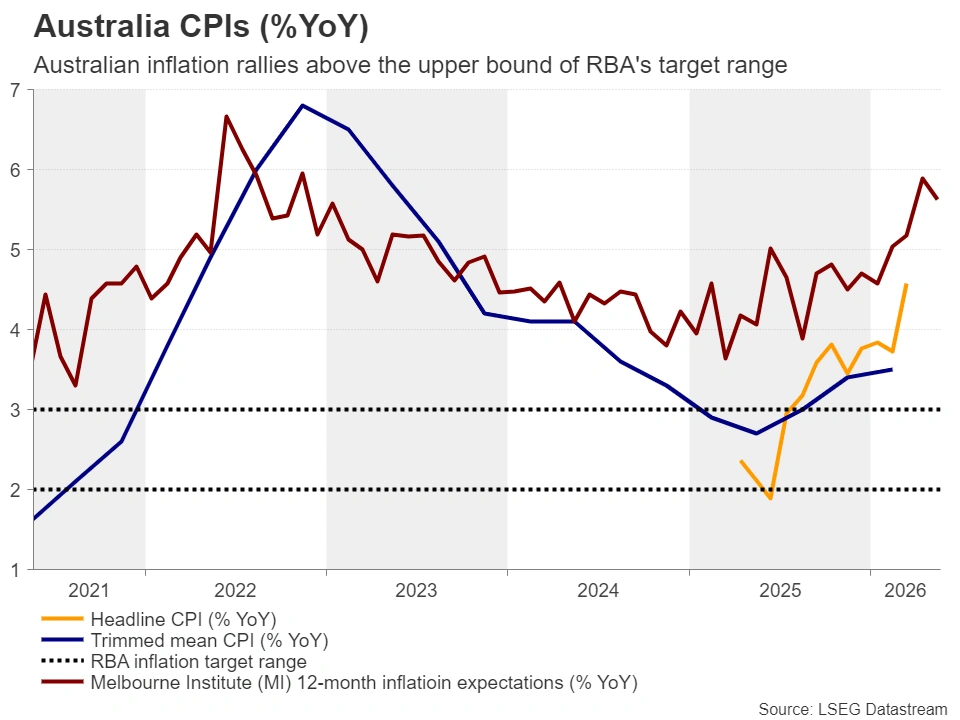

Australia’s CPI May Recharge the RBA

Only half an hour ahead of the RBNZ decision, Australia’s CPI inflation for April will be released. The RBA has already hiked three times, and although it appeared content to pause its tightening efforts for a while, there are still another 70bps worth of rate increases penciled in by the end of 2026, according to Australia’s Overnight Index Swaps.

The March CPI yearly rate jumped to 4.6% from 3.7%, and further acceleration could prompt traders to price in an even steeper implied path, which could add fuel to the Aussie’s engines. After all, the RBA has an inflation target range of 2–3%, and CPI rates are already well above the upper bound.

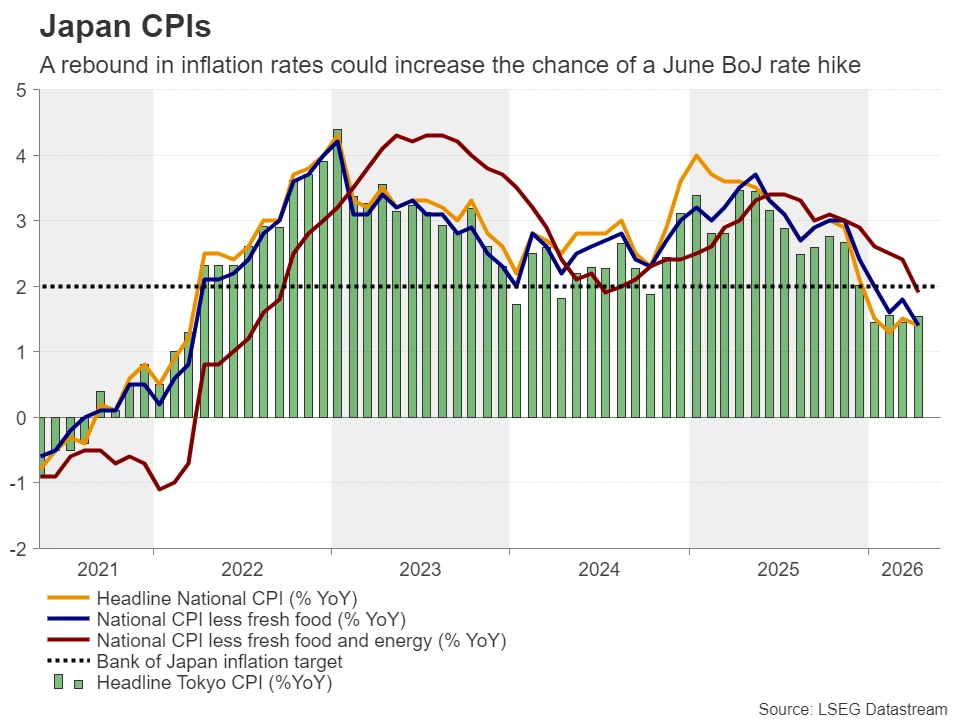

Yen Awaits Tokyo CPI Data for Intervention Relief

In Japan, the highlight is likely to be the Tokyo CPI report for May, accompanied by the industrial production and employment data for April. Even after Japanese authorities intervened a couple of times recently, the Yen is on the back foot against its US counterpart, with Dollar/Yen returning within the 158–160 zone, where Finance Minister Katayama tends to become more vocal about officials’ willingness to intervene.

Accelerating Tokyo CPI figures could strengthen the likelihood of a BoJ rate hike at the upcoming gathering and increase the chances of more increases in the coming months. According to Japan’s Overnight Index Swaps, there is a 75% chance of a hike on June 16, while another one is nearly fully factored in by the end of the year.

Increasing rate hike chances are likely to help the Yen strengthen and probably lessen the risk of intervention. However, the BoJ may need to satisfy market expectations if they really want to help any intervention to have the desired effect and avoid further speculative declines in the Yen.

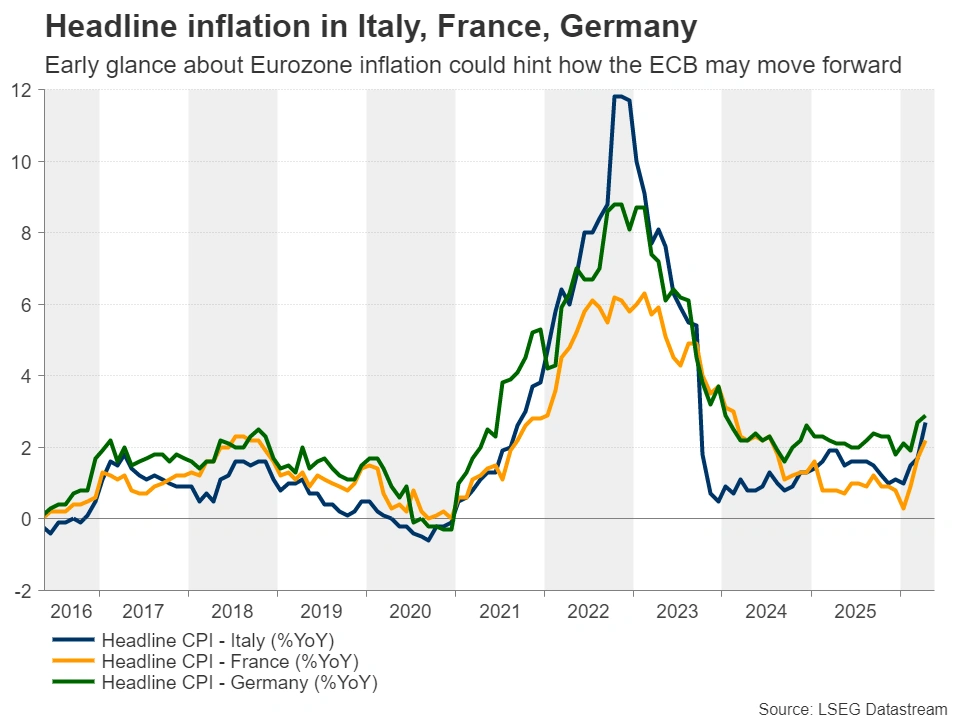

Italy, France, Germany Release Inflation Data; Canada GDP Also on Tap

Finally, on Friday, the preliminary CPI data for May from Italy, France and Germany will provide an early gauge of where inflation in the Eurozone may be headed. The Eurozone CPI data will be released on Tuesday, June 2. The ECB is now expected to press the hike button at its upcoming meeting while another 40bps worth of hikes may be on the cards thereafter. Increasing risks that inflation may spiral out of control could result in a more hawkish rate path, but whether this will help the Euro move higher remains doubtful.

While the ECB is expected to raise interest rates more aggressively than the Fed, at the same time, the Eurozone economy seems to be affected more severely by the current energy crisis and the war in the Middle East. This is evident by the weakening PMIs, with the bloc’s flash composite PMI for May sliding further into contractionary territory, to 47.5 from 48.8.

Canada’s GDP for Q1 and March are also on Friday’s agenda. The Loonie held relatively well amid the geopolitical chaos in the Middle East, perhaps receiving support from the rising oil prices. After all, Canada is the fourth largest oil exporting country in the world. Thus, if the data suggests that the Canadian economy remained resilient amid the turmoil, the Loonie could benefit a bit more.

Weekly Focus – The Fed on Course for Rate Hikes

This week we adjusted our Fed call and expect the next policy changes to be hikes rather than cuts, see Fed update. We look for 25bp rate hikes in December 2026 and March 2027. Previously, we expected the Fed to cut rates down to 3.00-3.25%. US nominal growth outlook has improved more than we expected previously as AI driven investment demand continues to fuel both growth and increasingly also inflation. Importantly, our change in call has not been driven by just the war in Iran. Instead, we think that demand-factors are fuelling more structural inflation. US weekly ADP job data this week confirmed the robust trend in the labour market with an average weekly change over the past four weeks of 42.25k up from 33k last week. US PMI manufacturing was solid rising to 55.3 from 54.5 while service PMI declined further from 51.0 to 50.9.

In the euro zone PMIs disappointed with the composite PMI falling to from 48.8 to 47.5, the lowest level since October 2023. The main reason was the services sector that fell to 46.4, a five-year low. Manufacturing PMI also dropped but is still around the average level of the past year. China's monthly data batch for April also showed the first signs of a negative impact from the Iran war with weakness in both retail sales and investments, see China Flash. It followed a strong start to the year with 5% growth in Q1. PPI inflation has increased sharply in recent months, so China has now become an inflationary force in the global economy after years of being a deflationary force.

The news rollercoaster on the Iran war continued over the past week. One day we are close to a deal; the next day we are not. We are still concerned that the closure of the Strait of Hormuz may drag out and keep oil prices elevated for longer. Bond markets cooled down after last week's sharp rise that continued into the beginning of this week. The factors driving the increase are a cocktail of strong US data, high inflation prints and fiscal worries across countries, not least UK, US and Japan. The move in expectations for the Fed towards tightening has been a key driver in the US bond market and as we now look for two hikes by the Fed, we have lifted our projection for 10-year treasury yields to 5.0% in 12 months.

We also changed our view on the USD as we believe the USD debasement story is fading and renewed Fed tightening will support the USD. We now see EUR/USD heading lower to 1.12 in 12 months vs a rise to 1.22 previously. Stock markets had a bumpy ride over the past week swinging with the ebbs and flows in bond markets and news out of the Middle East. We are still constructive on stocks on the back of robust nominal growth and strong earnings.

In the coming week focus continues to be on the Middle East, but US spending and PCE inflation data Thursday will also be in the spotlight. Friday focus turns to the first inflation data for May from Germany, France and Spain.

Sunset Market Commentary

Markets

Global bond markets are closing the week with some more gains. The common factor underpinning the move is hope on progress in the US-Iranian talks. The water is still deep on certain matters, particularly on the enriched uranium stockpile, but markets consider it a lower hurdle than the one for renewed escalation. Oil prices turned lower from as high as $112 on Monday to around $103, offering support to bonds. UK gilts outperformed US and European peers with weekly yield declines mounting to 23-29 bps. A set of unconvincing economic data – spanning retail sales, PMIs, consumer confidence and the labour market report – depressed BoE hiking bets. Governor Bailey and others before parliament have doused speculation somewhat too this week by saying markets have done the tightening job for them. They prefer to wait before actually pulling the trigger. The budgetary theme meanwhile, and with it risk premia, ebbed away again. It helped that the top contender in a potential challenge to prime minister Starmer, Andy Durnham, recently said he would keep the current set of fiscal rules. Bund yields dropped between 11 and 14.5 bps across the curve. ECB President Lagarde stuck to the non-committal script when speaking at the Eurogroup today, adding that she wasn’t going to give “much indication” on what could happen at the June meeting. US Treasury yields had to settle for about half of that. We were looking for the 10-yr yield to close the week above the upper bound of a 2023-2026 closing triangle (4.57%), which would have paved the way for a return to the 2023 high of 5%. That didn’t happen so far, offering Kevin Warsh some respite amidst his swearing-in scheduled today as the new Fed chair. Warsh in the past has criticized the Fed’s swollen balance sheet but his aim of shrinking it comes of course with implications for already elevated (long-term) bond yields. Warsh more generally promised a regime change at the Fed which next to winding down the balance sheet includes establishing a new framework for analyzing inflation and alter central bank communication (eg. less press conferences). Stock markets had a good run this week too, with gains for the EuroStoxx50 (+1% today) mounting to 3.4%. A mid-week rebound in US indices keep the previous record highs of early-May close. The stoic performance of currency markets stands out. EUR/USD hovered all week around but mostly above 1.16, DXY did the same around 99 and USD/JPY around 159. EUR/GBP slid from 0.875 levels earlier this week to 0.864 today. With the UK considered even more vulnerable to the energy price shock, the pound clearly outperforms against the euro when worries subside somewhat.

News & Views

Germany’s May IFO business climate painted a slightly more benign picture of the economy compared to yesterday’s PMI. Sentiment among companies recovered slightly following the slump in March and April, improving from 84.5 to 84.9. Companies assessed the current business situation somewhat more favorable (86.1 from 85.4) . Expectations for the coming months are also less pessimistic (index 83.8 from 83.5). Ifo assessed that the German economy is stabilizing even as the situation remains fragile. On a sector base, manufacturing and trade improved. Manufacturing companies turned more positive on the current situation, but expectations declined as orders continued to fall. Sentiment in the services sector even improved considerably especially as expectations recovered following a decline in the previous months. In construction, the business climate fell slightly.

As the is the case for several areas in FX of late, the realized volatility of the Czech koruna (against the euro) recently was very low, despite multiple sources of geopolitical turbulence. KBC Economics sees this move as being supported by strongly improved macro fundamentals of the Czech economy including, low inflation, solid GDP growth and a solid external position. The koruna continues to benefit from an attractive interest rate differential relative to the euro. CNB’s high foreign exchange reserves also are a strong stabilizing factor. Aside from macro fundamentals, the mechanics of the koruna market, particularly the way domestic exporters and importers hedge their exposure, have changed the mechanics of the koruna FX market. Instead of simple forwards, there has been a growing trend toward hedging using option structures, often linked to a specific exchange rate band, which drains volatility from the market. This regime holds for now, but if barriers are breached, hedging products may, on the contrary, temporarily amplify volatility.